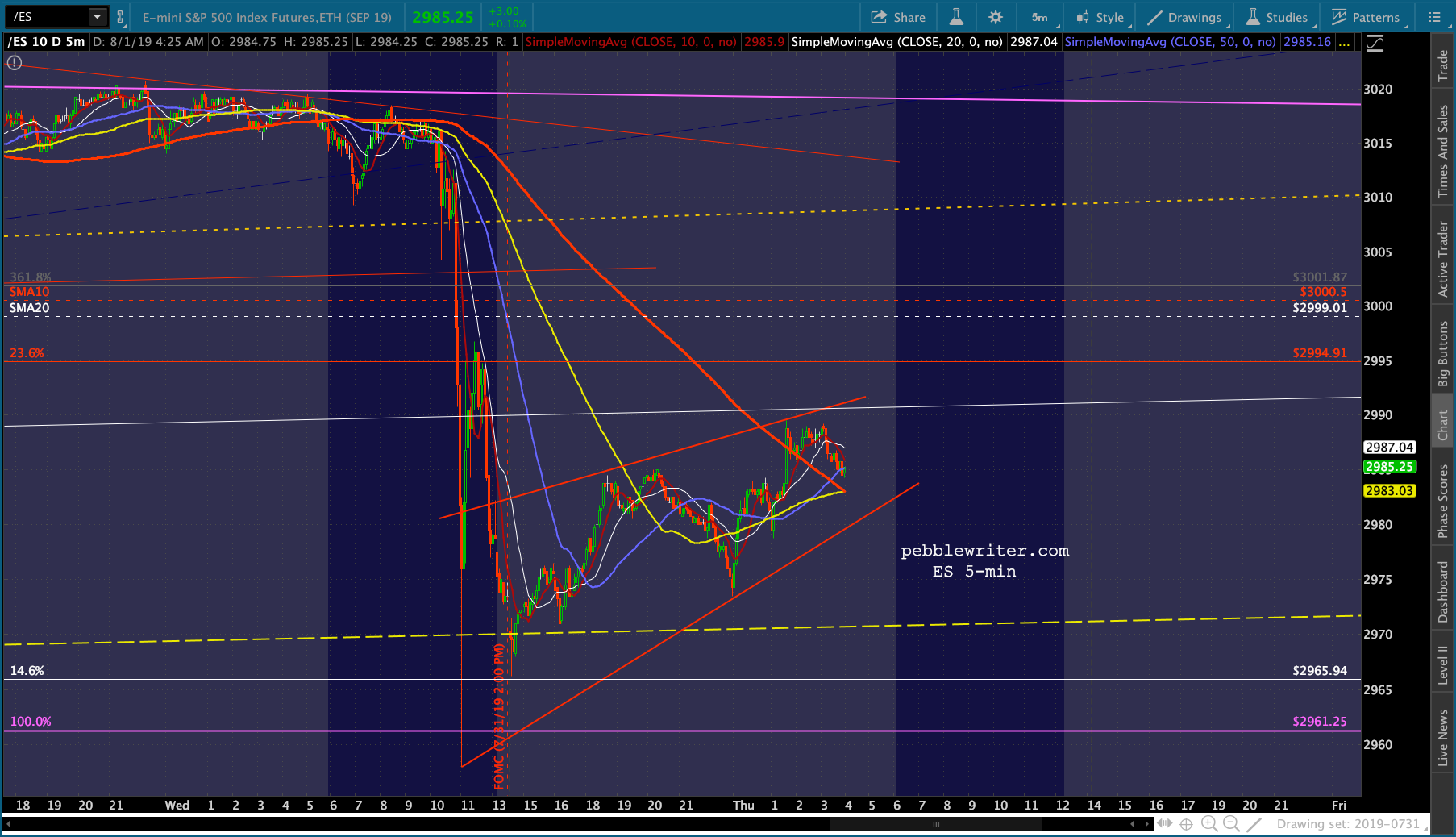

Since the top came two sessions earlier and 0.6% lower than our original forecast called for, I’ve spent the weekend adjusting the price and timing targets for the next 9 months. If it continues to play out as it has so far, the total drop will be greater than anything we’ve seen since the GFC.

It will feature 9 peak-to-trough moves of over 10%, 3 of which will exceed 20%. I’ve mapped out 23 significant turning points which average almost 300 points each. In short, it will be a trader’s market. It will test the resolve of buy-and-hold investors and trash the returns of momentum investors.

Buckle up.

continued for members… (more…)