First, a confession. In 2004 I sat next to a guy at a Sundance Film Fesitval screening who was very excited about his company that would someday be able to play movies on your computer or even your cell phone. “Why won’t this guy shut up?” I asked myself as I scanned the theater for an empty chair.

The “guy,” of course, was Reed Hastings. At the time, they were barely profitable, having just posted their first net profit ever (a whopping $7 million in 2003.) The stock was hovering around $5/share.

I couldn’t, for the life of me, figure out how they’d ever compete against Blockbuster — which had turned down an offer to acquire the company for $50 million a few years earlier.

The 2004 annual report cover, to the left, illustrated the problem. Why wait for a movie to arrive in the mail when you could run down to the local Blockbuster and grab a copy (along with some tasty Goobers) right now?

Reed was obviously on to something and soon figured out online delivery — though he still hasn’t cracked the eGoober challenge. A $10,000 investment in the common at that time would be worth around $1 million now. Live and learn, right?

* * *

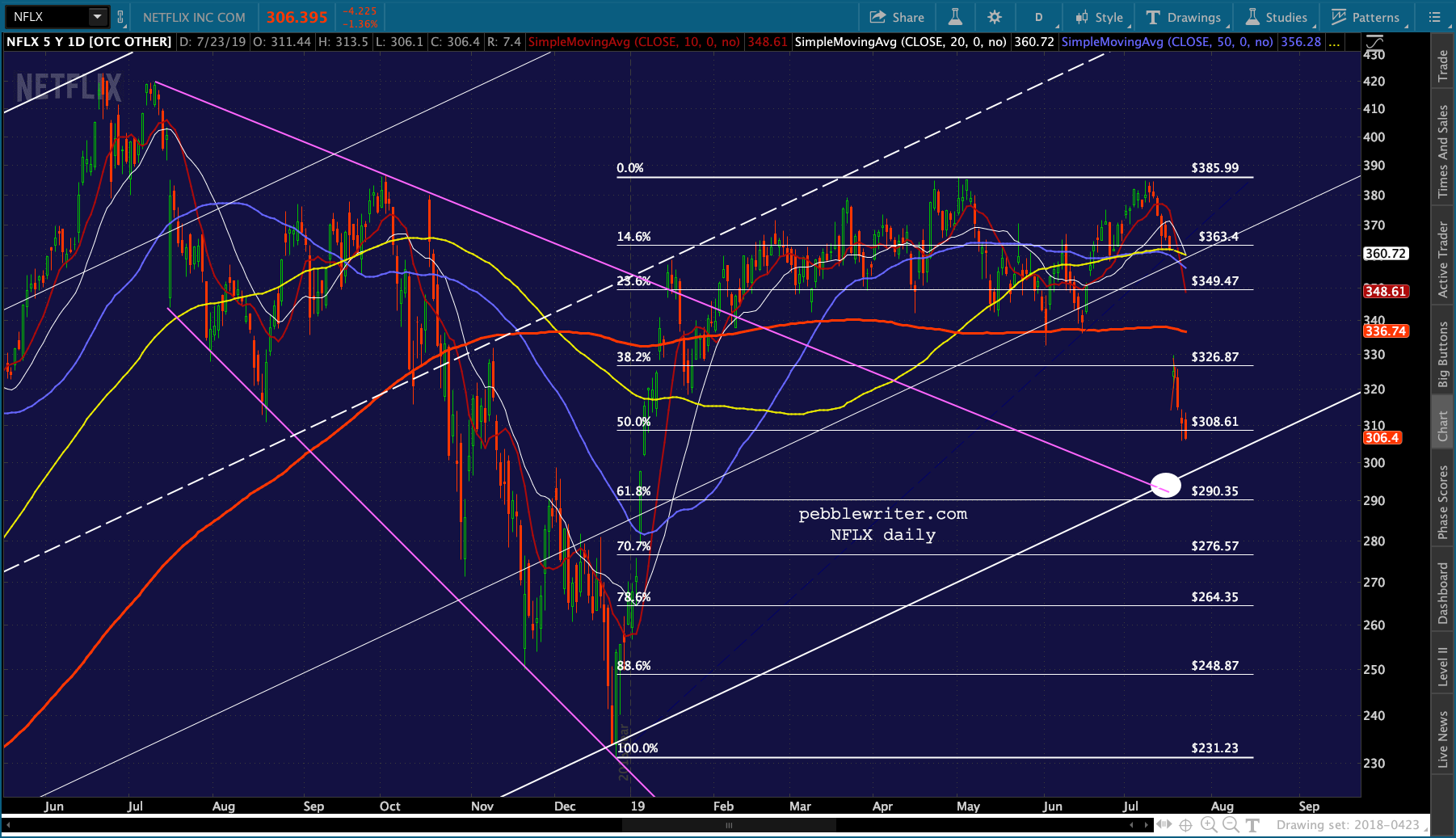

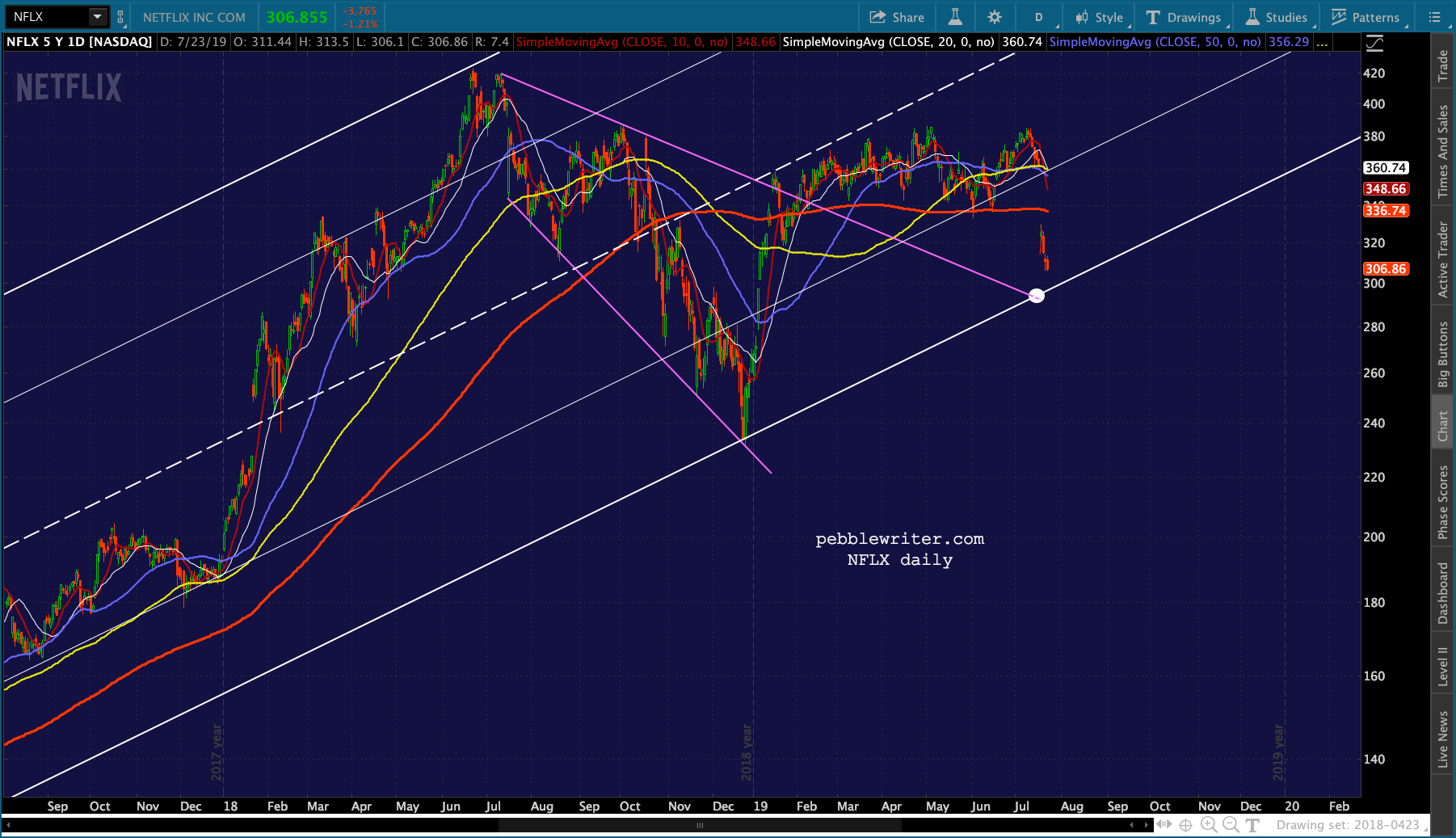

The stock is under pressure this morning as subscriber growth fell short of Street expectations and the company’s guidance. But, I’ll leave that to my fundamental brethren to suss out. My concern is that the stock will test critical support.

Last year we took a look at the chart and noted that at 400.48, it looked particularly vulnerable. From Netflix: Watch It! on July 16, 2018:

A quick glance at NFLX’s daily chart shows it has significant downside potential. The most obvious downside target is the 100-DMA at 338.73. But, the 200-DMA is approaching the white channel midline and should cross it at around 298-300 on or about August 6. It makes for a nice downside target if the SMA100 doesn’t hold. Should the SMA200 and channel midline fail, the bottom of the white channel is currently around 200 and (obviously) rising.

The stock soon tested then failed at the 100-DMA, but bounced just before reaching the midline and popped out of the falling white channel. It thus postponed the midline/200-DMA test until October 11 where it bounced yet again before plunging through to the channel bottom which, by then, was up to 230.

There are a lot of things that could happen to the stock, which has traded as low as 313 in after-hours. But, the critical level to watch is 295-300 where it would drop through the 200-DMA and test the channel bottom as well as backtest the broadening wedge (aka megaphone pattern.)

There are a lot of things that could happen to the stock, which has traded as low as 313 in after-hours. But, the critical level to watch is 295-300 where it would drop through the 200-DMA and test the channel bottom as well as backtest the broadening wedge (aka megaphone pattern.)

Anything lower would be very problematic for a stock which has been locked in the same rising channel for 6 1/2 years.

One note to those focused on the fundamentals. The observations I made last year still apply:

One note to those focused on the fundamentals. The observations I made last year still apply:

As an aside… I’ve been mystified as to the value ascribed to the company based on its ability to produce original content. What about the risk? Anyone who has worked in film or television can tell you that most productions don’t turn a profit.

I don’t want to get into production. There are passionate, talented filmmakers out there and I would pollute the craft.

Reed Hastings, Inc Magazine: Dec 1, 2005

Netflix has clearly hit some home runs with House of Cards, Stranger Things, etc. And, theoretically, producing content in-house can lower acquisition cost and diversify revenues.

But, extrapolating an unending string of popular and profitable productions is just plain silly. Some would say borrowing $1.8 billion to fund said productions is downright reckless.

Think New Line, which followed up the hugely successful Lord of the Rings trilogy with the expensive flop The Golden Compass. Investors would do well to remember that beta works in both directions.

* * *

It’s been ages since we offered a discount on memberships. For the next several days, quarterly subscriptions – normally $399 – will be discounted to only $299 for the first quarter. That’s 3 months for less than the price of two on a monthly subscription.

Click here to join now.

Update for members…Update: Jul 23, 2019

NFLX is closing in on our channel bottom and TL target. Note that the .618 retracement is at 290.35. So, we could get a slight overshoot that fakes out a few latecomers.

Note that the .618 retracement is at 290.35. So, we could get a slight overshoot that fakes out a few latecomers.