When it comes to trade, there is no free lunch. A lower US dollar helps US exporters. But, for the US – a net importer by a huge margin – it raises the price of imports.

So, it was really interesting to watch Treasury Secretary Mnuchin

So, it was really interesting to watch Treasury Secretary Mnuchin step in it explain that a lower USD would be “beneficial to our trade imbalances” without mentioning the offsetting, and more troubling, inflation and interest rate repercussions.

If we didn’t have $21 trillion in debt (multiples of that off-book) in a rising interest rate environment, it probably wouldn’t matter. But, the CBO’s numbers, which assume 10-yr rates top out just over 3% (half the historical average), argue otherwise.

Mind you, I’m not complaining. I’ve been bearish on the USD for a very long time. In May 2017 [see: May 1 Update on US Dollar] we noted that DXY had broken below a long-term trend line and was susceptible to more downside.

Mind you, I’m not complaining. I’ve been bearish on the USD for a very long time. In May 2017 [see: May 1 Update on US Dollar] we noted that DXY had broken below a long-term trend line and was susceptible to more downside.

…if DXY drops through the SMA200 and the yellow TL, then we have some very obvious Fib targets including the .786 at 97.583, the .886 at 96.789 and the purple .618 where it intersects the purple channel midline at 96.465 in July or August. If the purple midline breaks down, the next major support isn’t until 91 in early September and 87-88 as early as the end of the year.

We’ve seen plenty of worrisome bumps along the way, with a couple of timely rallies in Q4 to support stocks. But, our charts have remained bearish even as the Fed, with its ineffectual rate hikes, struggled to argue otherwise [see: Will the FOMC Minutes Save the Dollar?]

DXY just tagged our 87-88 target, reaching 88.438 moments ago with its eye on the rising purple channel bottom around 87.423. As we discussed in yesterday’s updates on EURUSD and USDJPY, the big question is what now? The charts offer a compelling answer.

As we discussed in yesterday’s updates on EURUSD and USDJPY, the big question is what now? The charts offer a compelling answer.

continued for members…The big picture shows what happens if DXY doesn’t bounce here and break out of the falling white channel. Our view on TNX has been that it’ll run out of steam between 2.70-2.86%. In other words, a reversal is imminent. I believe this is paramount to the Fed, and drives everything else.

Our view on TNX has been that it’ll run out of steam between 2.70-2.86%. In other words, a reversal is imminent. I believe this is paramount to the Fed, and drives everything else.

As we noted yesterday, USDJPY reached long-term channel bottom support (though it could still dip lower to 108.16 intraday.)

As we noted yesterday, USDJPY reached long-term channel bottom support (though it could still dip lower to 108.16 intraday.)

And, EURUSD has reached important overhead resistance (though it still has potential up to 1.2597.)

And, EURUSD has reached important overhead resistance (though it still has potential up to 1.2597.) If DXY and USDJPY bounce and EURUSD runs out of juice here, we’d see interest rates drop. But, inflation fears remain a problem. In order to relieve those fears, oil and gas would need to drop — especially from the BoJ’s perspective. It would appear they’re both far enough above Jan 2017’s prices to have generated adequate inflation for Jan 2018.

If DXY and USDJPY bounce and EURUSD runs out of juice here, we’d see interest rates drop. But, inflation fears remain a problem. In order to relieve those fears, oil and gas would need to drop — especially from the BoJ’s perspective. It would appear they’re both far enough above Jan 2017’s prices to have generated adequate inflation for Jan 2018.

And, if USDJPY’s bounce is vigorous enough, they won’t be needed to prop up stocks for the next month or two. The yen carry trade should be strong enough all on its own (ok, maybe with a little help from VIX.)

And, if USDJPY’s bounce is vigorous enough, they won’t be needed to prop up stocks for the next month or two. The yen carry trade should be strong enough all on its own (ok, maybe with a little help from VIX.)

It’s entirely possible that, between Mnuchin and Trump, the dollar will continue sinking and the euro soaring. But, I suspect both Yellen and Powell are on the phone with The Donald right now, explaining to him about the deal they’ve made with Draghi and Kuroda. Draghi hinted at this in his chat this morning:

Third reason is use of language in discussing FX developments doesn’t reflect agreed terms of reference.

Below 87.259, DXY would have broken down. A plunge down there which corresponded with EURUSD 1.2597 and USDJPY 108.16 and TNX 2.70-2.86 and GC 1380 (no, I haven’t forgotten you, my gold bug friends!) would tie everything up in a nice, neat bow.

BTW, ES continues to hold the white channel bottom as it backtests the red channel top. If it breaks down, there’s support at the SMA10 at 2810.60 and the red channel bottom around 2788. If that breaks down, my next favorite target would be the SMA20 at the red channel top at 2763 (Monday.)

BTW, ES continues to hold the white channel bottom as it backtests the red channel top. If it breaks down, there’s support at the SMA10 at 2810.60 and the red channel bottom around 2788. If that breaks down, my next favorite target would be the SMA20 at the red channel top at 2763 (Monday.) Maybe, then, we’d finally get that pop in VIX we’ve been waiting for.

Maybe, then, we’d finally get that pop in VIX we’ve been waiting for.

UPDATE: 12:28 PM

While there’s potentially a little more to go in each of these targets, we’re close enough to start building long positions in DXY, USDJPY and Notes and short positions in EURUSD, CL/RB and ES/SPX.

I worry more about timing than being on the wrong side of these trades. EURUSD could bounce around for several of months, then come back to tag 1.2597 in April, May or June — or it could be done right here and now on an overshoot. DXY could bounce up to tag the falling SMA200 at, say, 91.92-92.47, then drop back down to the rising purple channel bottom in late July — even at a slightly higher low.

DXY could bounce up to tag the falling SMA200 at, say, 91.92-92.47, then drop back down to the rising purple channel bottom in late July — even at a slightly higher low. Gold might well be done, but it could still pop up and tag the 1380 neckline on Monday.

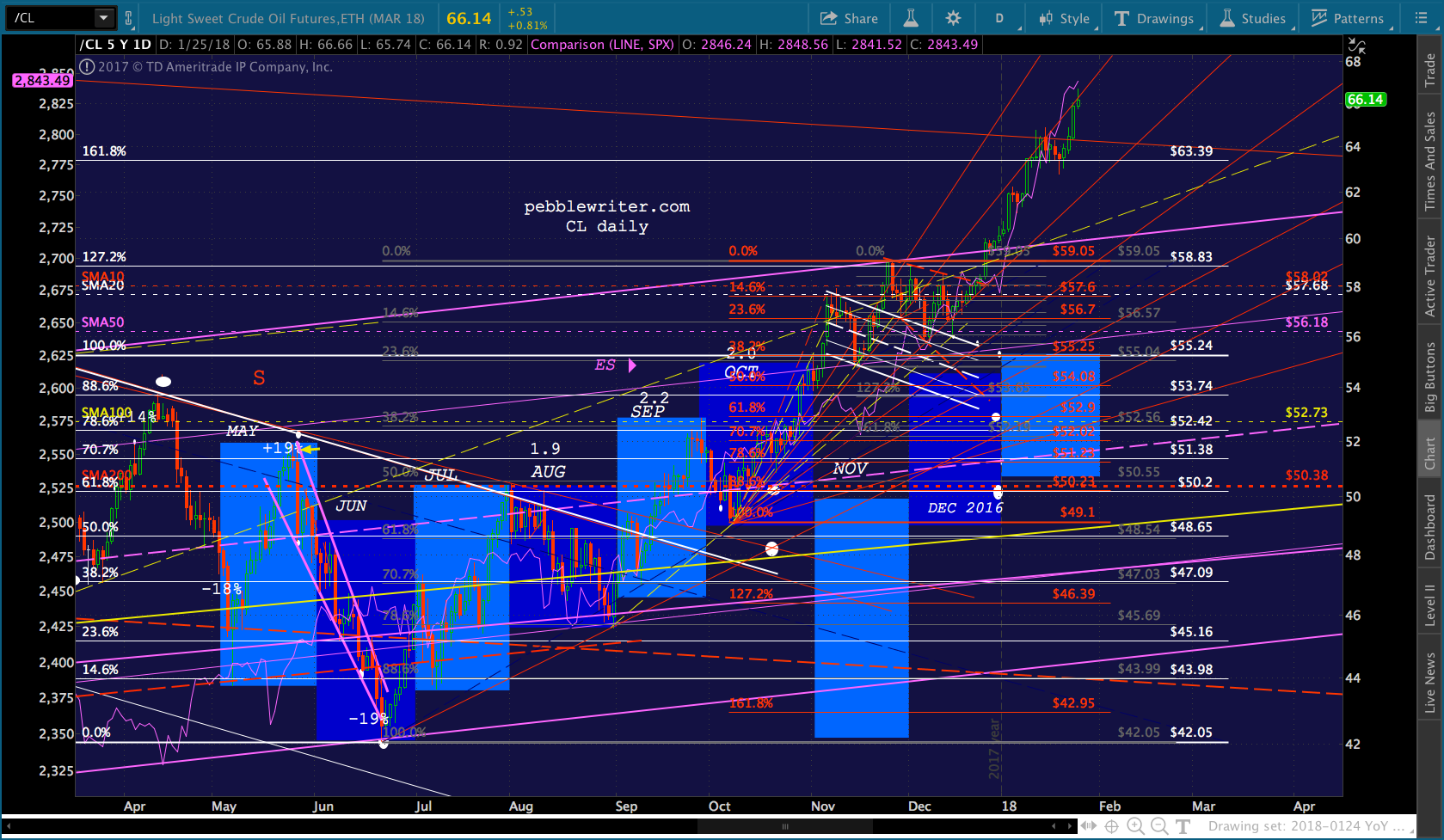

Gold might well be done, but it could still pop up and tag the 1380 neckline on Monday. CL should fall, but it could be limited to a backtest of the channel it broke out of at 60 — a modest 10% decline.

CL should fall, but it could be limited to a backtest of the channel it broke out of at 60 — a modest 10% decline. And, RB’s backtest could be as small as .04 (backtesting the channel) or as great as .34 (the .618). The SMA200 at 1.65 is a particularly interesting target and would provide a great deal of help with the inflation problem. Needless to say, a 10-15% decline in CL/RB would be a drag on stocks, which are no doubt considering a backtest of the 2.24 Fib extension.

And, RB’s backtest could be as small as .04 (backtesting the channel) or as great as .34 (the .618). The SMA200 at 1.65 is a particularly interesting target and would provide a great deal of help with the inflation problem. Needless to say, a 10-15% decline in CL/RB would be a drag on stocks, which are no doubt considering a backtest of the 2.24 Fib extension. Just be aware that timing is a potential issue. So, taking these positions now could mean sitting for a while with not much to show for it. As such, I’d be cautious with instruments with a time premium — options, leveraged ETFs, etc.

Just be aware that timing is a potential issue. So, taking these positions now could mean sitting for a while with not much to show for it. As such, I’d be cautious with instruments with a time premium — options, leveraged ETFs, etc.

Remember, each of these pairs/commodities is priced to support stocks. If they go sideways for a while, that’s no problem. They’ll simply take turns pushing SPX higher. One ramps while the other resets — with VIX ready to bridge any transition periods. Easy peasy. It’s probably what I would suggest if I worked for the Fed.

GLTA.