Job cuts rose to 228K (vs 200K expected) last week. It will officially register as a drop, however, as the previous week was revised from 198K to 246K. When viewed through the prism of new highs in bankruptcies and an earnings implosion…  …it’s not too surprising that futures are drifting lower.

…it’s not too surprising that futures are drifting lower. continued for members… (more…)

continued for members… (more…)

Tag: Inverse H&S

-

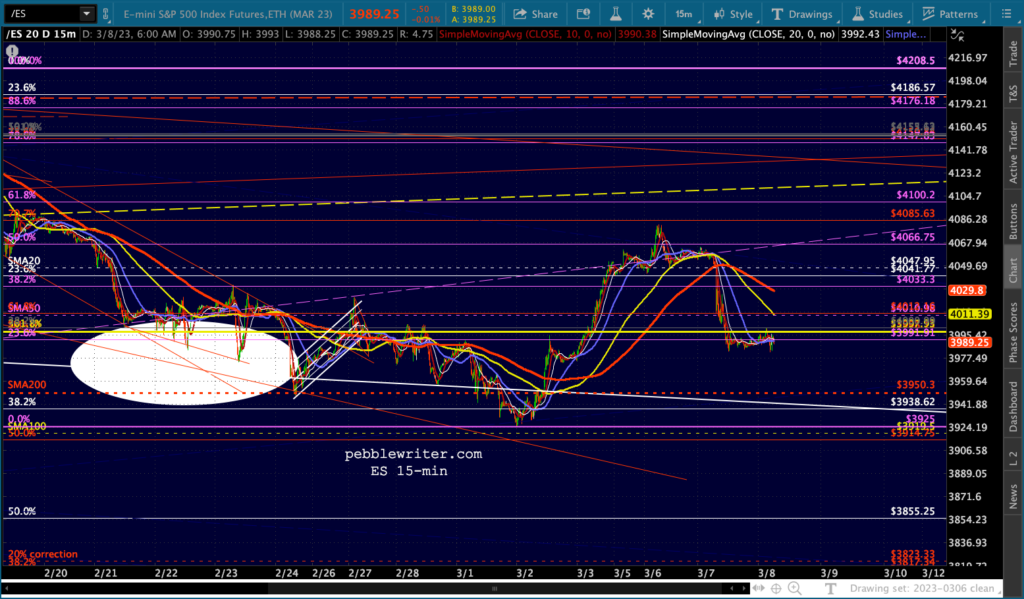

Jobless Claims Pile On

-

Charts I’m Watching: Apr 4, 2023

After reaching our next upside target, futures have settled into a pause.

No surprise, as the algo factors are doing the same.

No surprise, as the algo factors are doing the same.continued for members… (more…)

-

On the Bubble

Our yield curve model sounded the alarm on Friday. But, by the end of the day, it had backed off and cooler heads prevailed.

It’s important to recognize, however, that it remains on the bubble, with only a few basis points standing between a rally and another leg down. From a fundamental standpoint, there seems little doubt that the odds of a recession are on the rise.

It’s important to recognize, however, that it remains on the bubble, with only a few basis points standing between a rally and another leg down. From a fundamental standpoint, there seems little doubt that the odds of a recession are on the rise.continued for members… (more…)

-

Powell’s Testimony

Bottom line, a 50 bps rate hike is back on the table. We got the backtest we expected, and even a little bit more.

This morning’s ADP employment report further underscores the need to put the brakes on the economy. It will be interesting to see whether Powell’s tone becomes any less hawkish in light of yesterday’s sell off.

This morning’s ADP employment report further underscores the need to put the brakes on the economy. It will be interesting to see whether Powell’s tone becomes any less hawkish in light of yesterday’s sell off.continued for members… (more…)

-

Japan’s Runaway Inflation

Japan’s inflation hit a 40-year high in October, driven by a policy of placing stock market gains above all else.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.Although the BoJ has allowed the 10Y to rise to 0.24%…

…they have held short-term rates at -0.1% since 2016.

…they have held short-term rates at -0.1% since 2016. The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market.

The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market. The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.Luckily for Japan, they have no bond market per se. The entirety of Japan’s borrowings are purchased by the BoJ. This monetization of debt has gone on for years without repercussions – until now.

The Nikkei was locked in a falling price channel between Feb 2021 and Mar 2022, when the decline finally reached -20.7%. At that point, it was less than 1% away from its pre-pandemic highs of 24,140.

It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old.

It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old. Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.Come to think of it, the US faces similar problems.

* * *

In other news, VIX has sent the all-clear to algos to rally at least a little further – this being OPEX and all.

continued for members… (more…)

continued for members… (more…) -

PPI Lower Than Expected

October PPI came in at 8% annually and 0.2% monthly versus expectations of 8.3% and 0.4%. Core PPI remained unchanged at 6.7%.

Futures popped up to our 4050 IH&S target on the news, but had already ramped over 40 points prior to the print.

Futures popped up to our 4050 IH&S target on the news, but had already ramped over 40 points prior to the print. continued for members… (more…)

continued for members… (more…) -

VIX Sliding Away

Seemingly on a rail, VIX’s bump took it only to the top of the falling red channel in place for over a month.

A failure to break out means ES can top its 361.8 Fib extension and reach its IH&S targets.

A failure to break out means ES can top its 361.8 Fib extension and reach its IH&S targets.  continued for members… (more…)

continued for members… (more…) -

VIX at a Crossroads

For months, VIX has facilitated higher equity prices – plumbing new lows, breaking down, refusing to rise in cases of obvious market distress. Today, it reached a trend line off the previous highs, all of which corresponded with sizeable bounces in the equity markets. It’s an extremely important test for bulls.

continued for members…

continued for members… -

Inflation Rises

August CPI came in hot, rising 0.1% in August instead of the consensus 0.1% decline. Core was even worse: 0.6% versus 0.3% consensus. The annual print also disappointed, coming in at 8.3% versus expectations of 8.0% or less.

Having slightly overshot our 4153 target overnight, ES is now reversing sharply.

Having slightly overshot our 4153 target overnight, ES is now reversing sharply. continued for members… (more…)

continued for members… (more…) -

More Where That Came From

Yesterday marked the second day in a row of sharp declines in the equity markets following the 200-day moving average backtest and the passing of OPEX.

There’s more where that came from.

There’s more where that came from.continued for members… (more…)