A friend just tipped me to the fact that a certain Elliott Wave outfit (we’ll call them Elliott Wavers Incorporated, or EWI) pronounced yesterday that 2011 and 2007 exhibit a “similar topping pattern.”

OMG!

I only wish I had had this very valuable information a couple of months ago. Oh, wait, I did. When I made the exact same observation in May. But wait, there’s more.

Now, only 36 points away from completing an obvious H&S; pattern, EWI says this market has a head and shoulders look about it. To me, this is like predicting the Giants might win the World Series — as Nelson Cruz started to swing at Brian Wilson’s 3-2 pitch in the bottom of the 9th in game 5.

In reality, the pattern was visible well before my June 21 post and we had just completed the “head.”

EWI goes on to describe the similarities, including the internal trend lines, broken support line and backtest that I describe in detail in early June [here and here]. They’ve also been noticed and written about by folks like Max Cherry and Austin Mitchum — long before EWI’s breakthrough discovery.

Last, EWI questions if there’s any “forecasting benefit in analyzing this chart?” Aside from the limited benefit in showing a similar psychological progression, they “haven’t found any price and time relationships between the two moves that would allow a more specific forecast.”

WTF!?!

Please indulge me as I set the record straight.

**********************************************************************************************************************

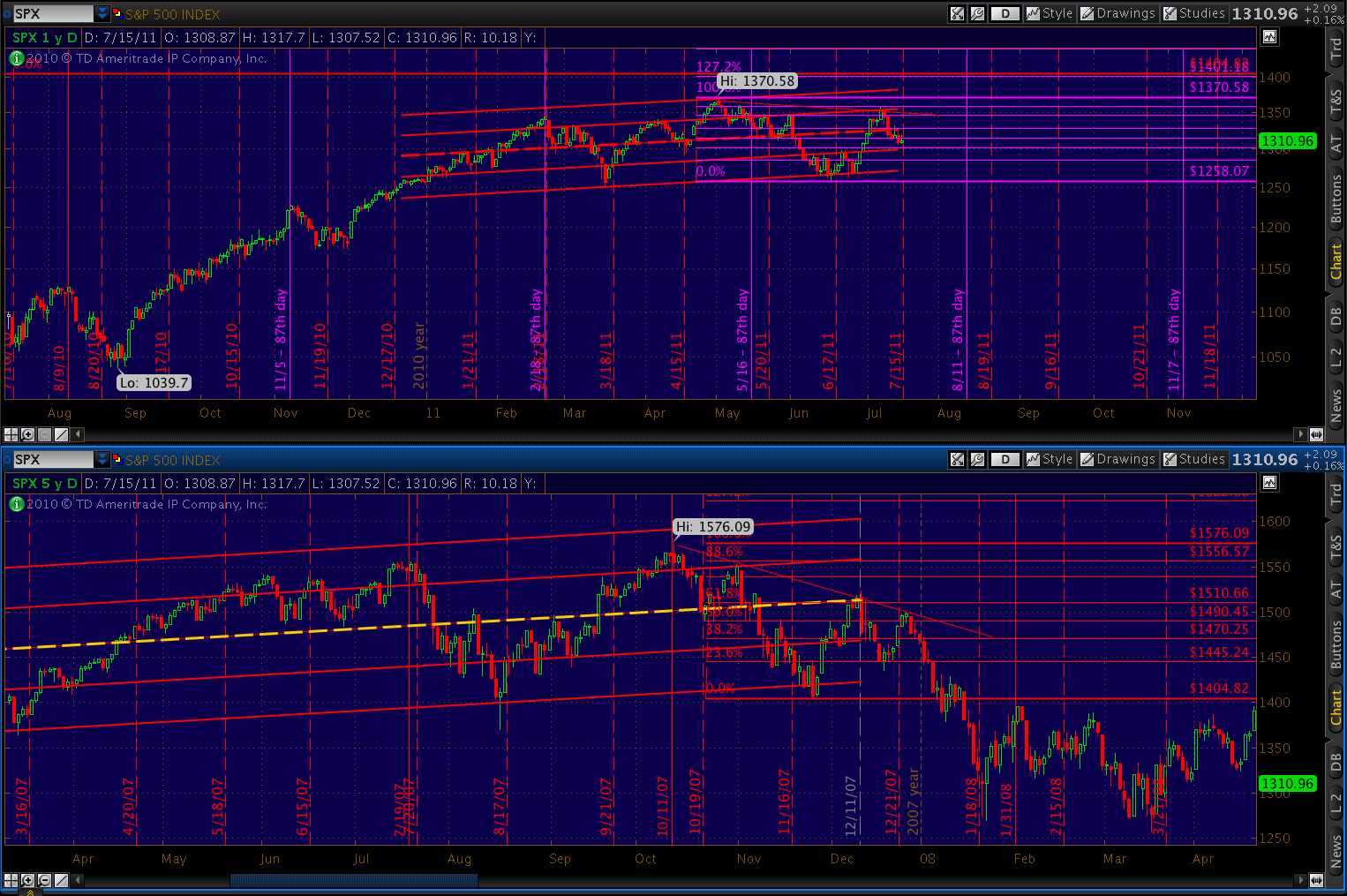

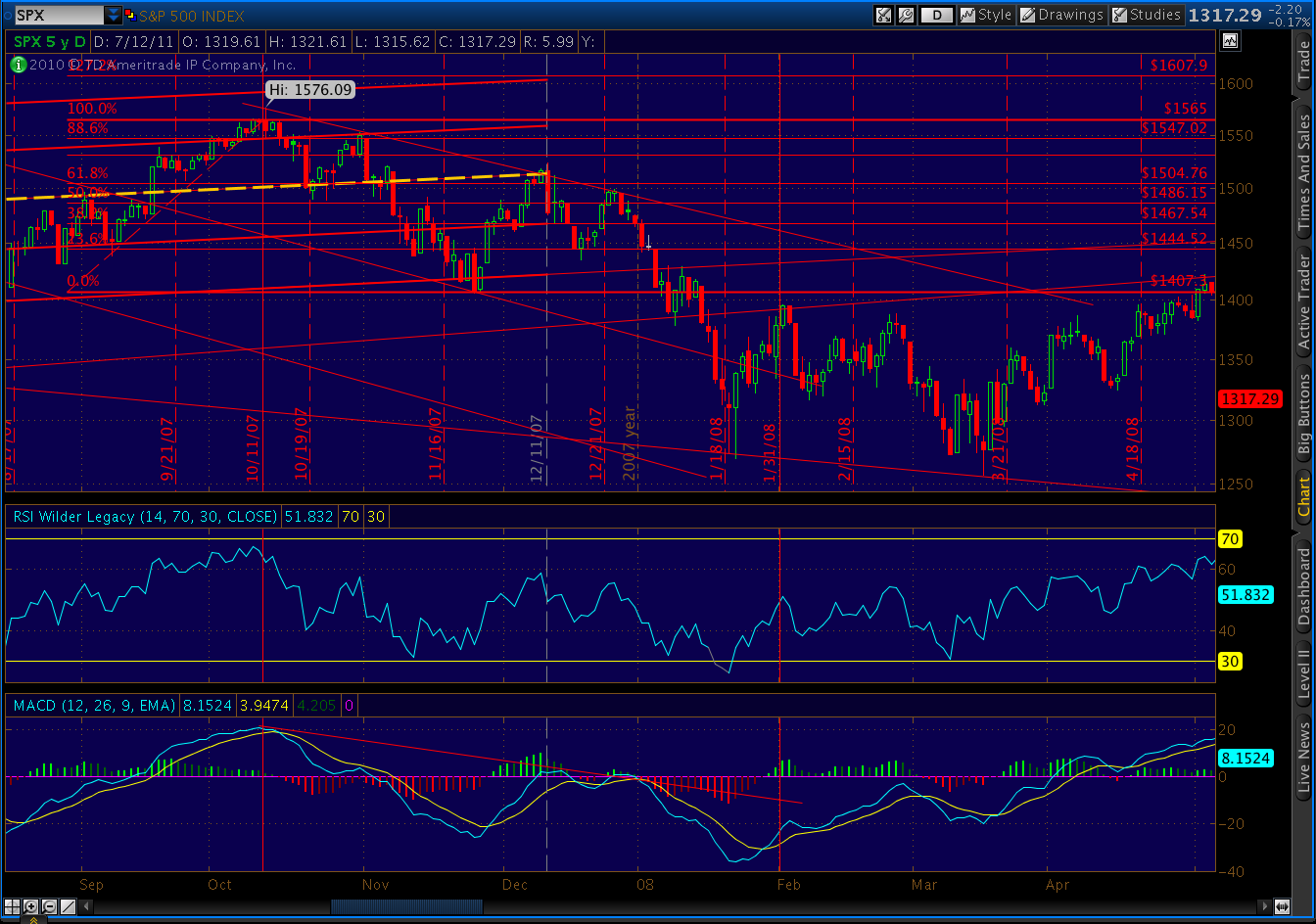

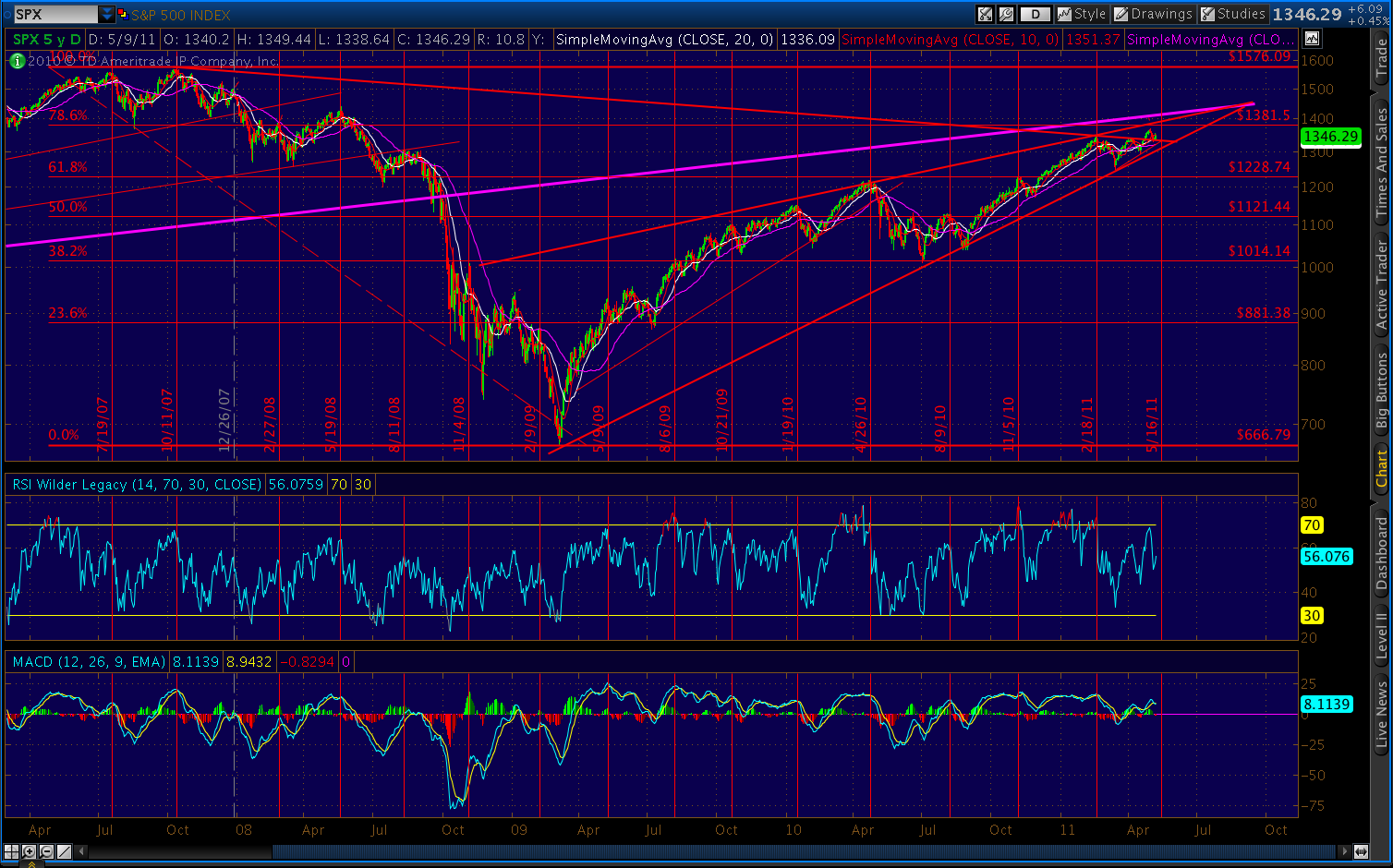

On May 31 [Why P[3] is My Top Bear Count] I noted “significant similarities between the past few months and the tops in 2000 and 2007.”

On June 3 [Here We Go] compared the market action between the patterns as related to breaking and backtesting the long term support trendline.

On June 8 [Deja Vu?] detailed the pattern that the 2000, 2007 and 2011 tops had in common, noting how the market, “once it drops below its long-term support, looks like it’s in for a free fall. But, it eventually finds new support in a parallel channel as I theorized a few days ago. The bottom of the channel is drawn off a recent major high and the top is drawn off the two most recent peaks. It pencils in nicely for 2000 and 2007…”

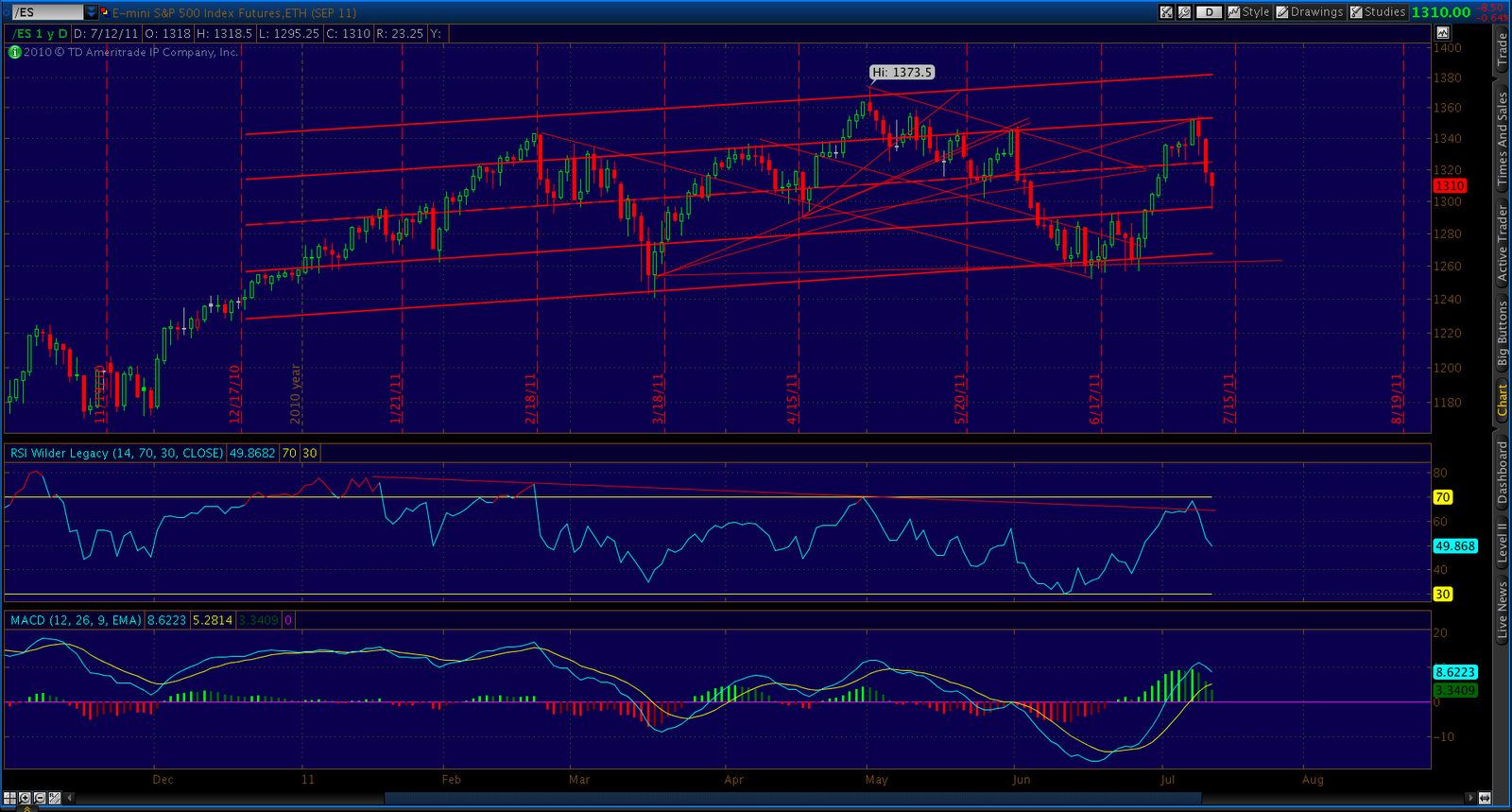

On June 10 with SPX below 1270 and amidst warnings of “flash crash!”, [Channel Surfing] showed how the pattern (accurately) promised one last return to the midline of the regression channel at around 1330. I showed how the channel I’d drawn corresponded well with a 2-standard deviation regression channel.

On June 12 [Update: Channel Surfing] reported that almost every major top since 1928 exhibited the same pattern. I suggested that the pattern was not only characteristic of tops, but a requirement. I formalized the description as: “…characterized by a multi-month pattern within a rising market that has at least two significant touches (of the index or its Bollinger Band) of at least 1.5 standard deviations on the upper and lower extremes of a regression channel commencing after a post-correction new high. It’s capped off by a third touch on the lower boundary and subsequent return to at least the midline before a final plunge to new lows. “

On June 16, [You’ve Got a Fan in Me] showed how the regression channel could also be defined in terms of fan lines from significant previous high and low pivot points. I used examples from 2007, 2000 and 1937 to demonstrate. The prior day’s post [Playing the Bounce] used the pattern to call the bottom at 1261.90 (it was the next day at 1258.07.)

On June 21 with SPX at 1294, [A Different Perspective] discussed how a return to the pattern midline around 1327 and subsequent fall would create a huge head and shoulders pattern that, by mid-August, would begin a decline to around 1200.

On June 23 [Deja Vu, All Over Again] showed how the 2000 and 2007 patterns corresponded, beat for beat, and charted the various trend lines that would govern the pattern’s completion. With SPX at 1287, the pattern still indicated a 1320-1330 target. I reiterated the pattern prediction the following day in the midst of the 25 point intra-day plunge triggered by the strategic petro reserve decision.

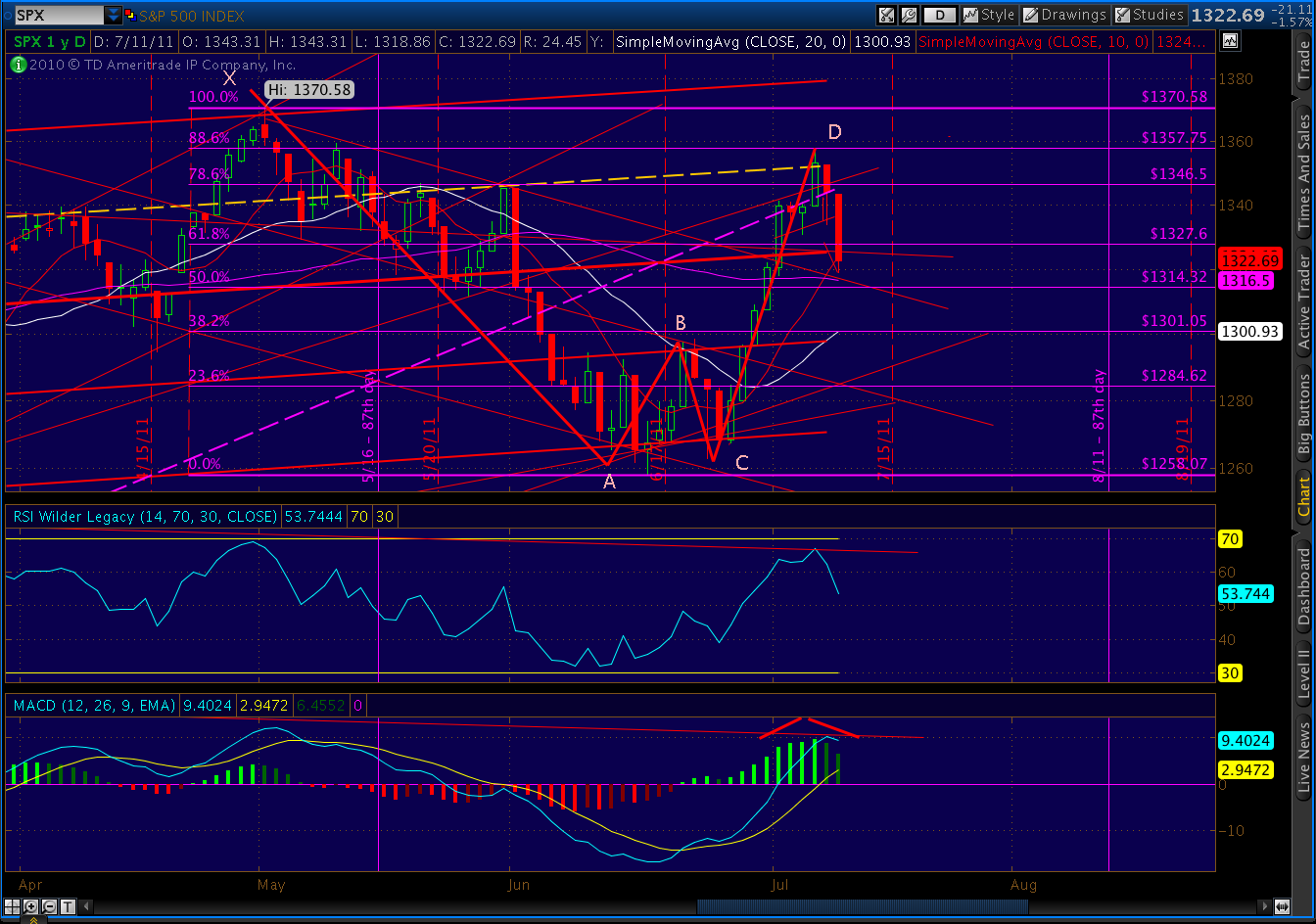

On June 26, [Cliff Diving] defined the decline from 1370 to 1258 as 1 of (1) of P[3], and the subsequent rise a corrective wave 2. I suggested the pattern interim target might also follow fibonacci guidelines. The midline, at 1322, was virtually the same as the .786 Fibonacci retracement line. With the market back to 1268 and bearish sentiment through the roof, I suggested the pattern would take us up 54 points in 5 days. It took 4. As I suggested on June 29, we would likely even overshoot (we did, hitting instead the .886 Fibonacci retracement.)

In June 29th’s post [Lunatic] I restated that contrary to popular opinion, the rally would not lead to new highs, but would merely complete a corrective wave 2, followed by wave [i] of 3 to around 1300 (it’s reached 1306, so far.)

On July 4, [Final Destination] suggested the next move down would stop north of 1298.61 in order to keep the bullish count alive. So far, so good, with Friday’s 1300.5 overnight low in the futures market.

On July 7, [Confidence Fairies] and [Then and Now] suggested we had reached the pattern high at 1356.87 right at the .886 Fibonacci level. The next day began a 5-day, 46-point decline. In [Friday the Bear Came Early], I suggested the peak was in — earlier than the 87-day cycle would indicate because that’s what happens in market tops.

When a big decline the next morning was quickly reversed and seemingly everyone turned bullish [She’s Come Undone] explained this was simply a throw-over, and that the pattern 1-standard deviation line had stepped in for 2007’s channel midline in defining the top and preventing any further advances. SPX declined 27 points the next day and, as mentioned above, seems to have petered out above 1298.61.

***********************************************************************************************************************

Obviously, the pattern hasn’t yet completed, and there’s no guarantee that it will. Anything can happen between now and then, including an extension of the pattern as occurred in 2000 (EWI didn’t mention that part, did they?)

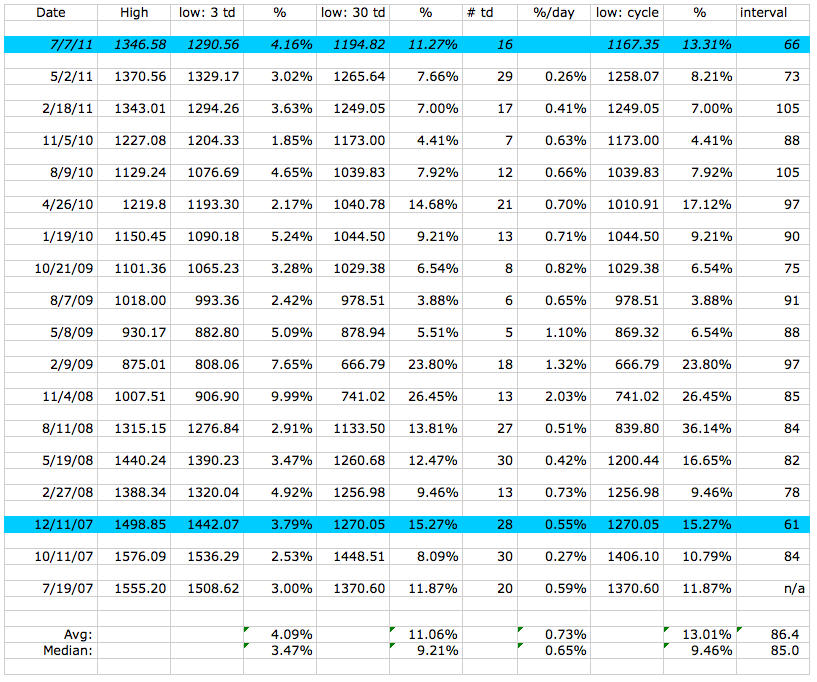

But, excuse me for thinking that a pattern that accurately predicted 3 tops and 2 bottoms in 60 days has some freakin’ forecasting value!!!!!

Maybe if I charged $59/month… but, then you’d expect other brilliant calls like shorting silver at $20.