Early results from reviewing a lot of market tops and would-be market tops… I have yet to find an example of the model I suggested not working. And, folks, this is kinda exciting stuff.

To recap, about a week ago I noticed [Watch for the Rebound] that the drop we were experiencing might set up an upward-trending channel that would embolden the bulls. The channel could be seen by drawing a trendline off the 1344 and 1370 highs, and a parallel bottom between the 1249 low and the to-be-established low.

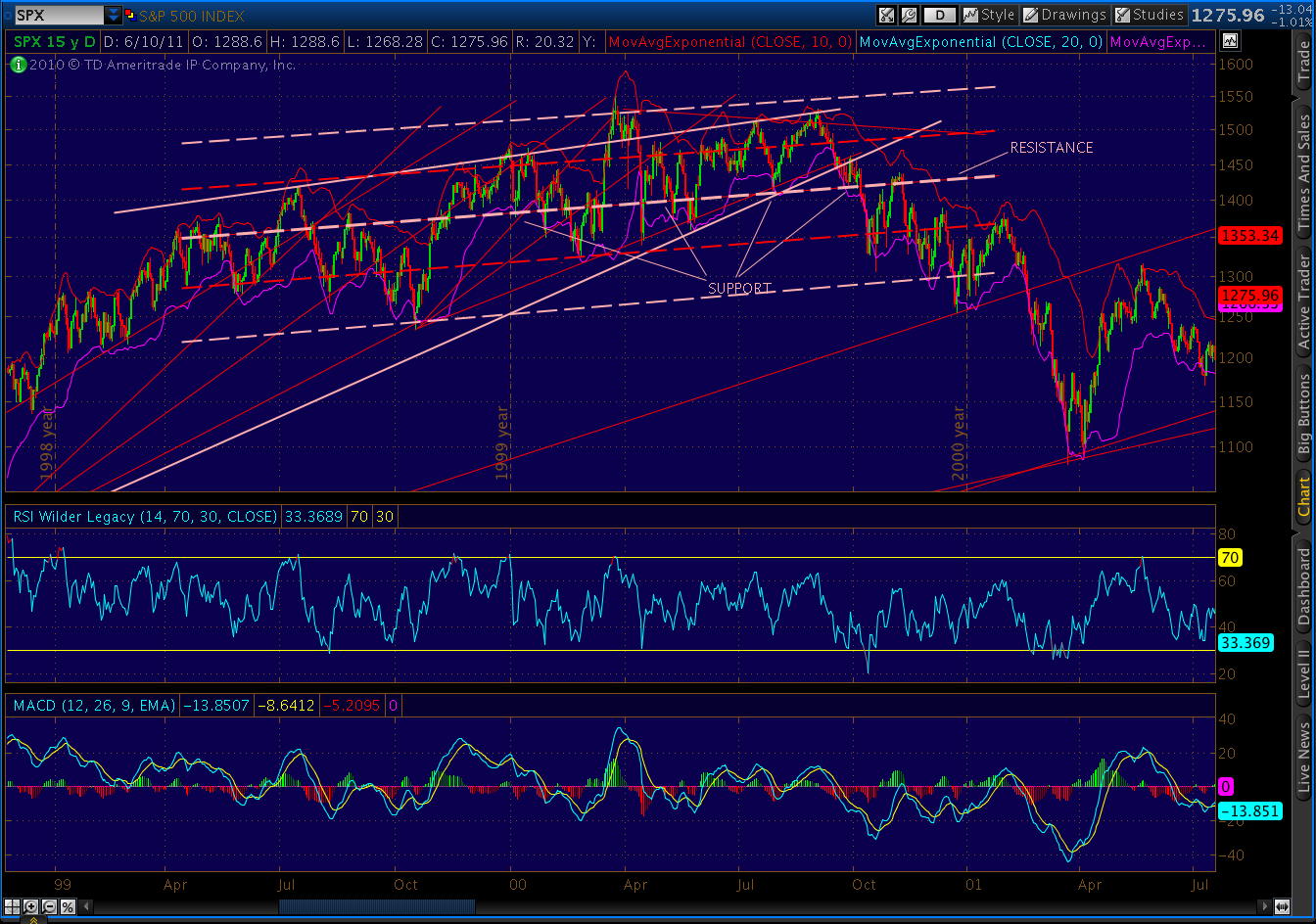

By this past Friday, it dawned on me [Channel Surfing] that what I had seen was actually a two-standard deviation regression channel. The tops in 2000 and 2007 were very similar in the way that they entered into and behaved while within such a channel. More importantly, the current market has behaved very similarly to those tops.

I spent a few hours today dragging two-standard deviation regression channels around to various market tops and what looked like could be market tops. Bottom line, I’m fairly well convinced that not only have market tops all behaved similarly, but that the pattern observed is predictive of a market top. In fact, I’m leaning towards calling this pattern a requirement of significant market tops.

It’s characterized by a multi-month pattern within a rising market that has at least two significant touches (of the index or its Bollinger Band) of at least 1.5 standard deviations on the upper and lower extremes of a regression channel commencing after a post-correction new high. It’s capped off by a third touch on the lower boundary and subsequent return to at least the midline before a final plunge to new lows. Here’s the view of the 2000 and 2007 tops I posted last week.

|

| 2000 TOP |

|

| 2007 TOP |

And, here’s where the market is now:

|

| 2011 TOP? |

So, while I’m pretty confident about the next move (up, in the short term), is this THE top?

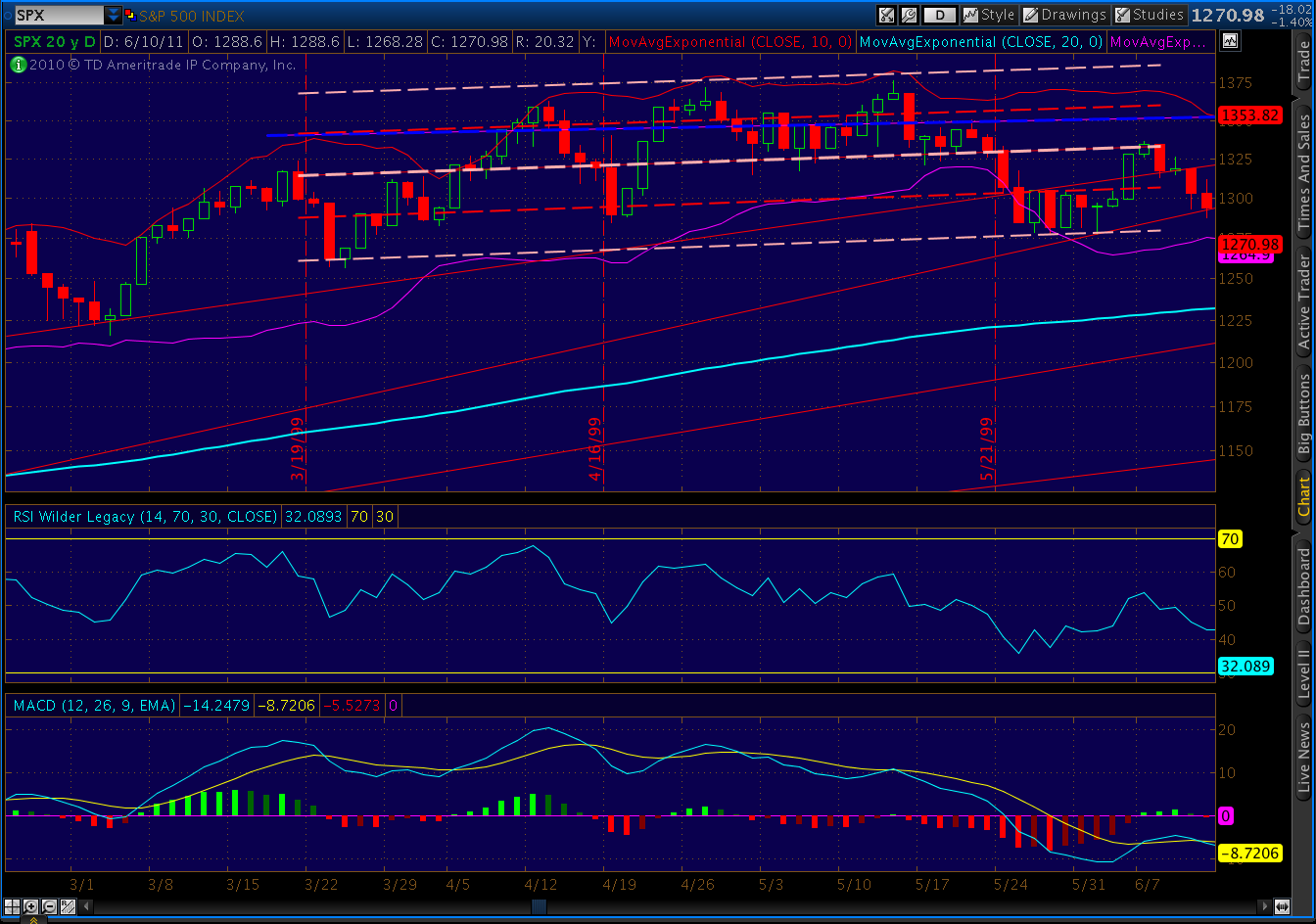

Even though it’s predictive of a top, this pattern doesn’t in and of itself mean a major top is imminent. Consider early 1999. From March through May, the pattern displayed perfectly. It featured a 100 point drop from May 13 through May 27, including 3 up and 3 down days of 20+ points off a 1375 high (hmmm… sounds familiar.)

|

| WHAT MIGHT HAVE BEEN |

Sure enough, after the 3rd touch of the bottom, the index rebounded to the midline at 1336. As might be expected, it fell back — but only to 1287, from where it traced out five waves up over the next month to 1420!

|

| WHAT WAS |

In a turn of events that only a fractologist could love, it retraced the entire pattern on a much larger scale over the next 1 1/2 years before finally resulting in the crash we all knew and loved. The initial, smaller scale channel can be seen in the far left of the much larger/longer pattern in the graph above.

What’s an investor to do? Look at the market’s behavior leading into the supposed top. In 1999, the market had just experienced a 12-day, 180 point swoon. So, a topping pattern that spanned only 100 points or so wasn’t at the same scale.

In 2007, the last major correction was just over 100 points (May – August ’06.) So, a topping pattern that spanned 200 or so points was completely in scale with the preceding action.

What about today’s market? So far, this channel is about 100 points. We had a 50-point, 1-month correction last November, so that seems reasonable. But, look back at the summer of 2010. We had a 200-point correction that lasted 7 months. The current topping pattern seems a little on the small side by comparison.

And, what’s up with the November pattern looking suspiciously like the summer pattern? Same thing happened with that fakeout in 1999 — a 65-point droop (also visible above) two months before the fun started that’s the spitting image of the 180-point one a few months before that.

Besides, look at the time involved in the downturns preceding the pattern. In each case, the larger correction was less than half the time span of the ultimate topping pattern. Last summer’s correction lasted 7 months, but this topping pattern is only 4 months old.

Could this be a head-fake, too? Short answer: yes. I have little doubt that we’re eventually going down after this week’s bounce back to the channel midline. My inclination is that it’s sooner than later. After all, we did lose the trendline of support that’s kept us going since Mar ’09 and the rising wedge since Oct ’10. The economy is on life support. And, ending QE2 is going to feel like cold turkey to this addicted market.

But, just to be safe, I’ll wait for a breakout in one direction or the other to tell me whether or not a larger pattern is developing. While I think it’s 50-50 at best, the possibility remains that this is a Minor 4 triangle, preparing the way for a Minor 5 push to 1370 or more.

Upon nearing the midline, I’ll place stops to protect the downside, and not go short until/unless we break below the channel. If the past is any guide (and isn’t it always?) the market would come back and backtest the channel before heading further south. So, at most, it’s an opportunity loss of 50 points or so. If this really is P[3], I’ll never miss those 50 points.

I know what you’re thinking: this is diametrically opposed to last week’s forecast (which seemed so great at the time!) But, given that the original 87-day cycle date isn’t until August 11th, it would make sense if the plonger énorme were delayed a bit. And, the leading candidate for the return to the midline isn’t until 6/29 or so. We could bounce around a bit, I suppose. But, how would we kill another six weeks if it isn’t by tracing out a (no doubt truncated) Minor 5?

Just for the record, I think this market stinks. I’m bearish. Period. There’s nothing happening in the world that gives me even the slightest confidence that we’ll come out of this looking good (okay, maybe the implosion of Newt’s campaign.) Any move up, if it happens, would be the direct result of market manipulation on the grandest scale by the Fed — which, of course, is desperate to prevent P[3]. Would they do it? In a heart beat. Could they do it? Maybe — at least temporarily. Lots of economic reports coming out next week, most of which could be pushed one way or the other.

Or, given that the war is essentially lost anyway, why not blow the remaining ammunition on a last gasp effort to turn things around and announce QE3? It would ultimately do more harm than good, but it might buy some time. Maybe call it something else, so people don’t catch on right away. Qualitative Easing, anyone?

Stay tuned.

Comments

2 responses to “Update: Channel Surfing”

Let's see if it works before we schedule the awards ceremony!

Major kudos to you for uncovering this pattern. I can only dream of being so organized and insightful. 🙂