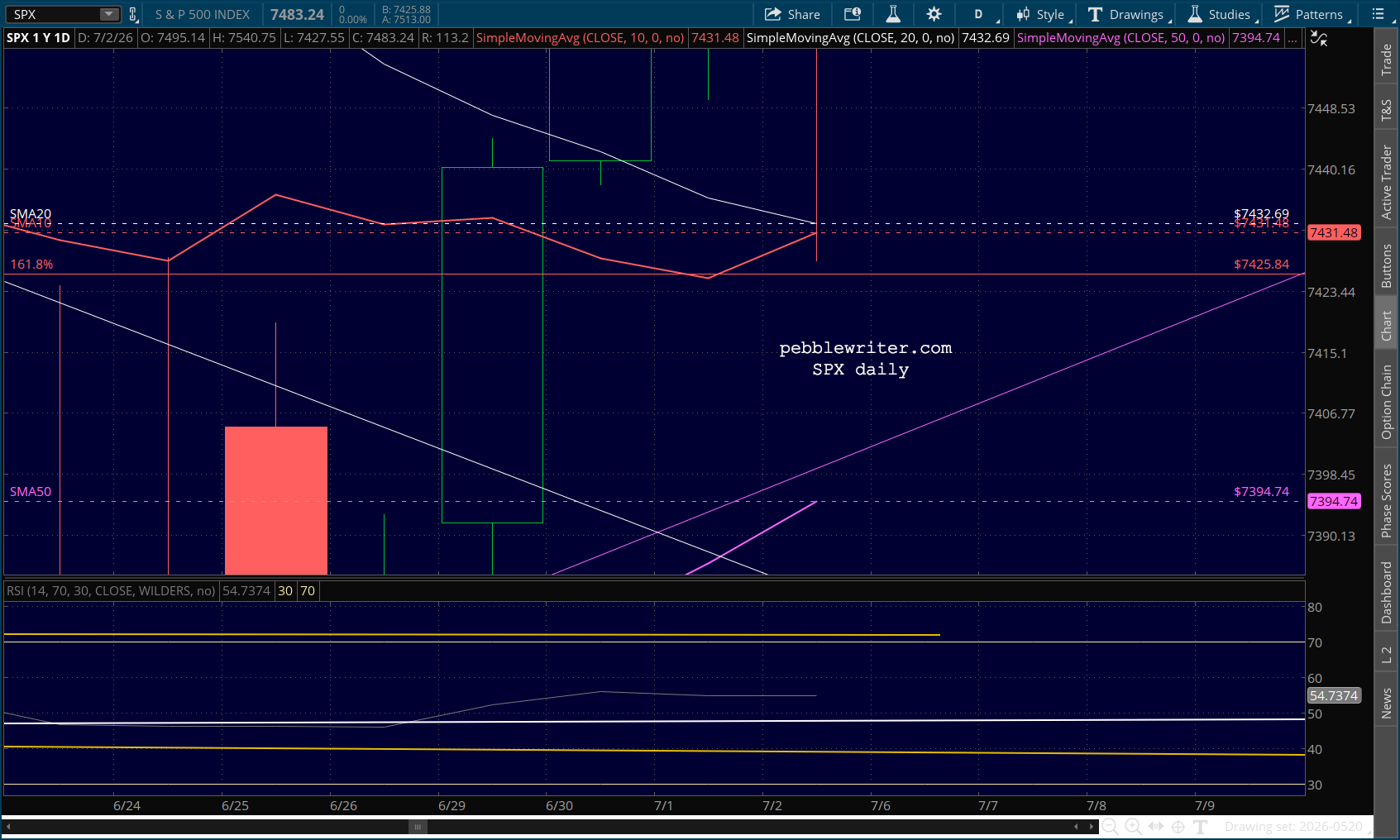

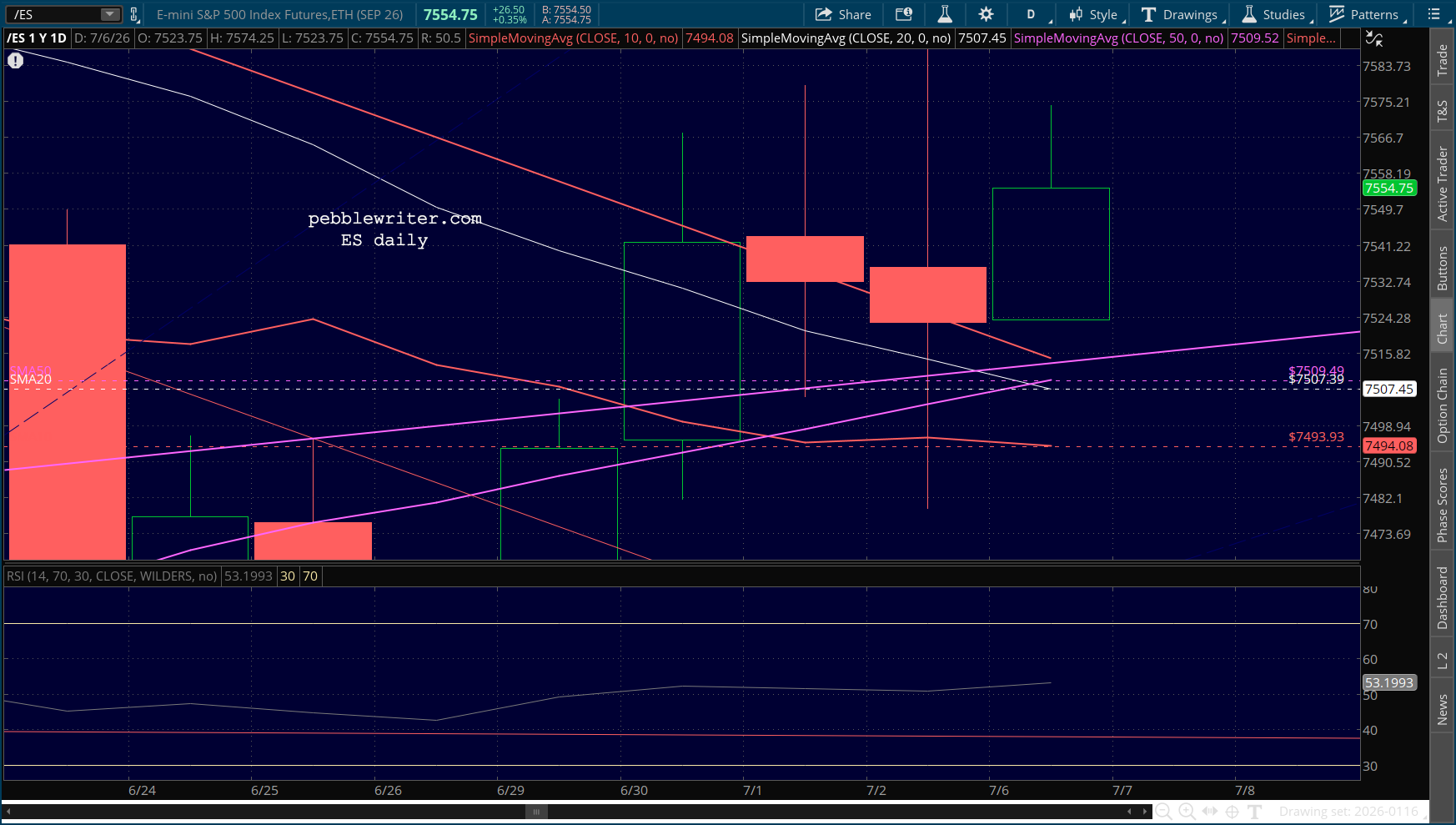

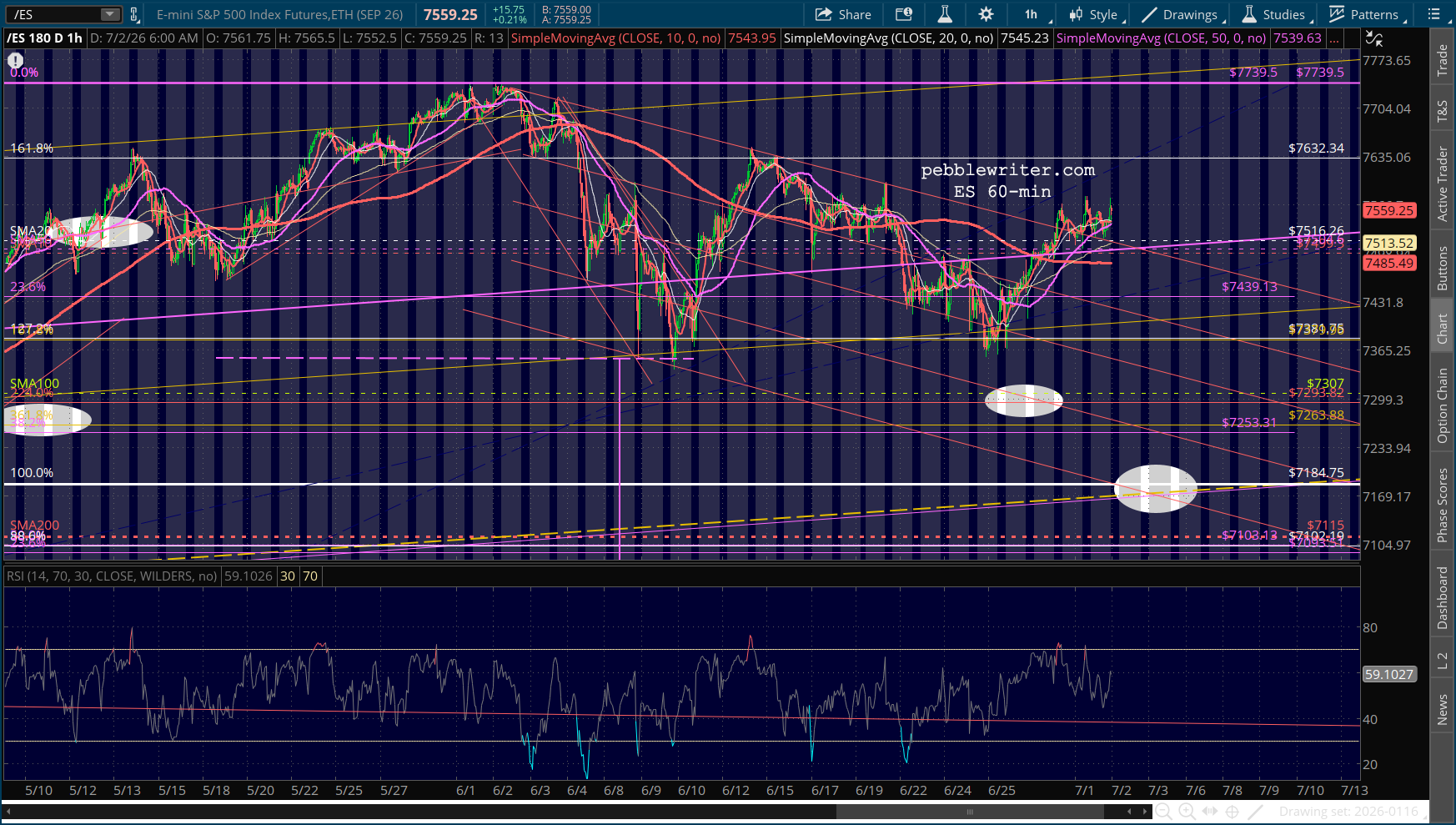

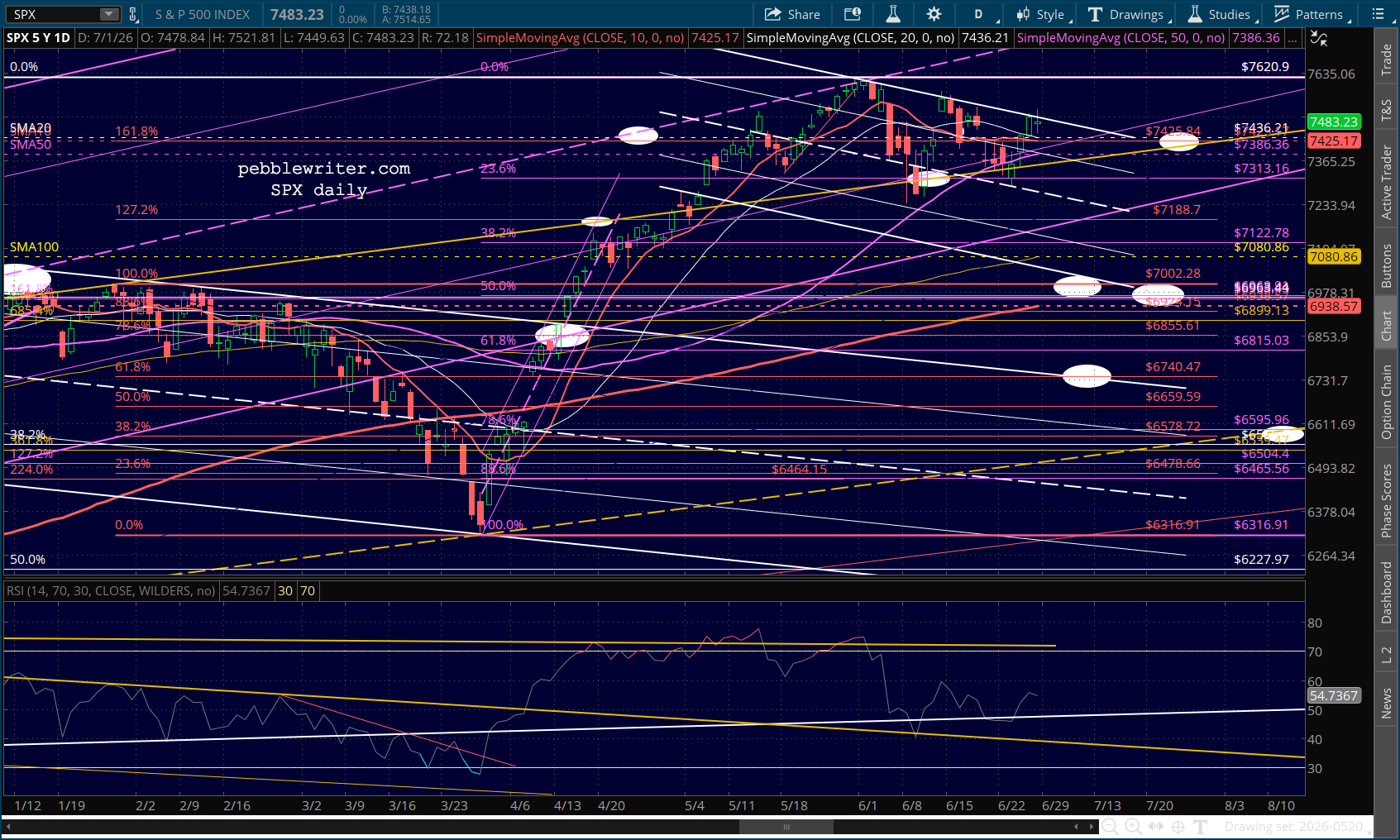

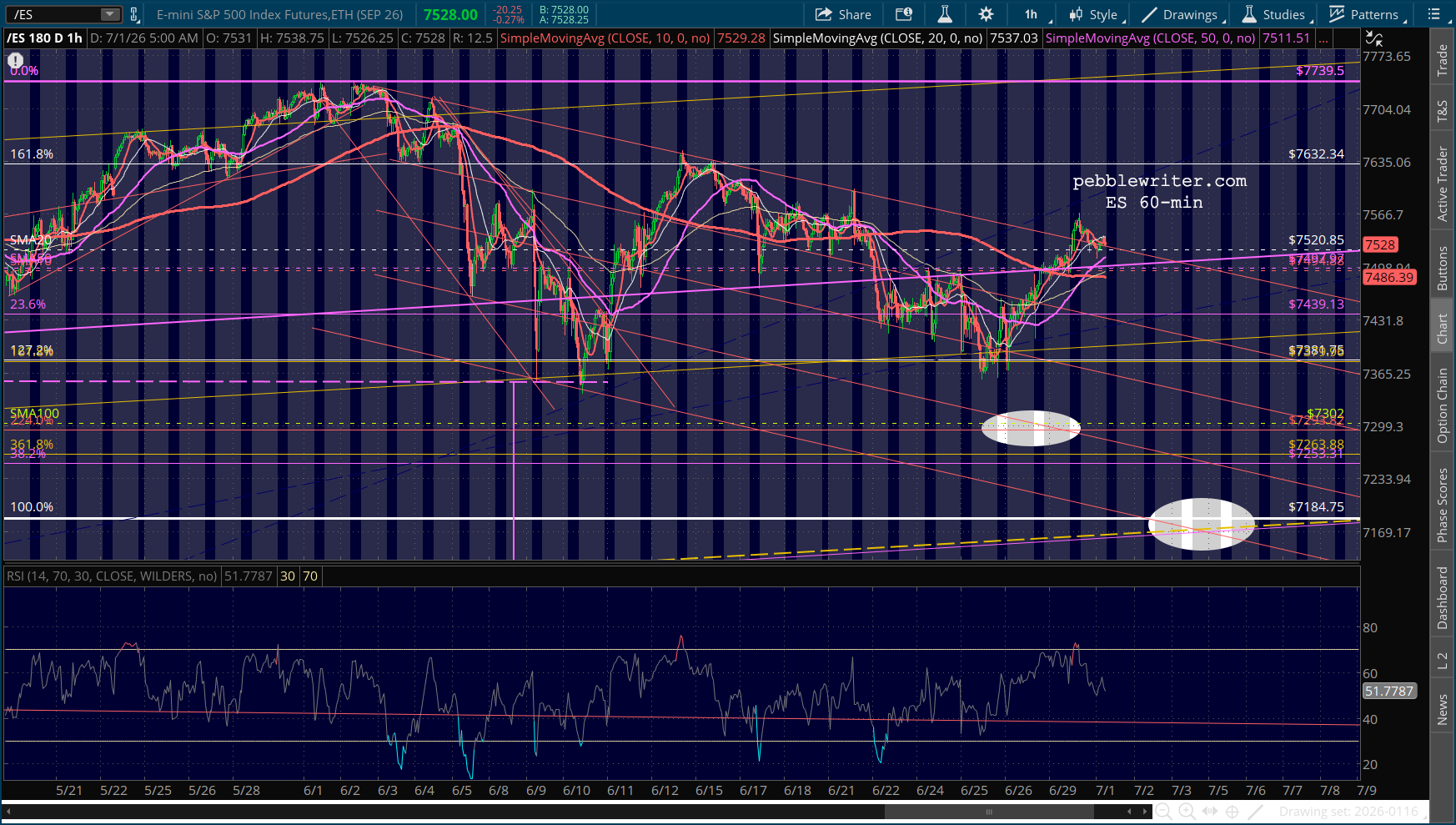

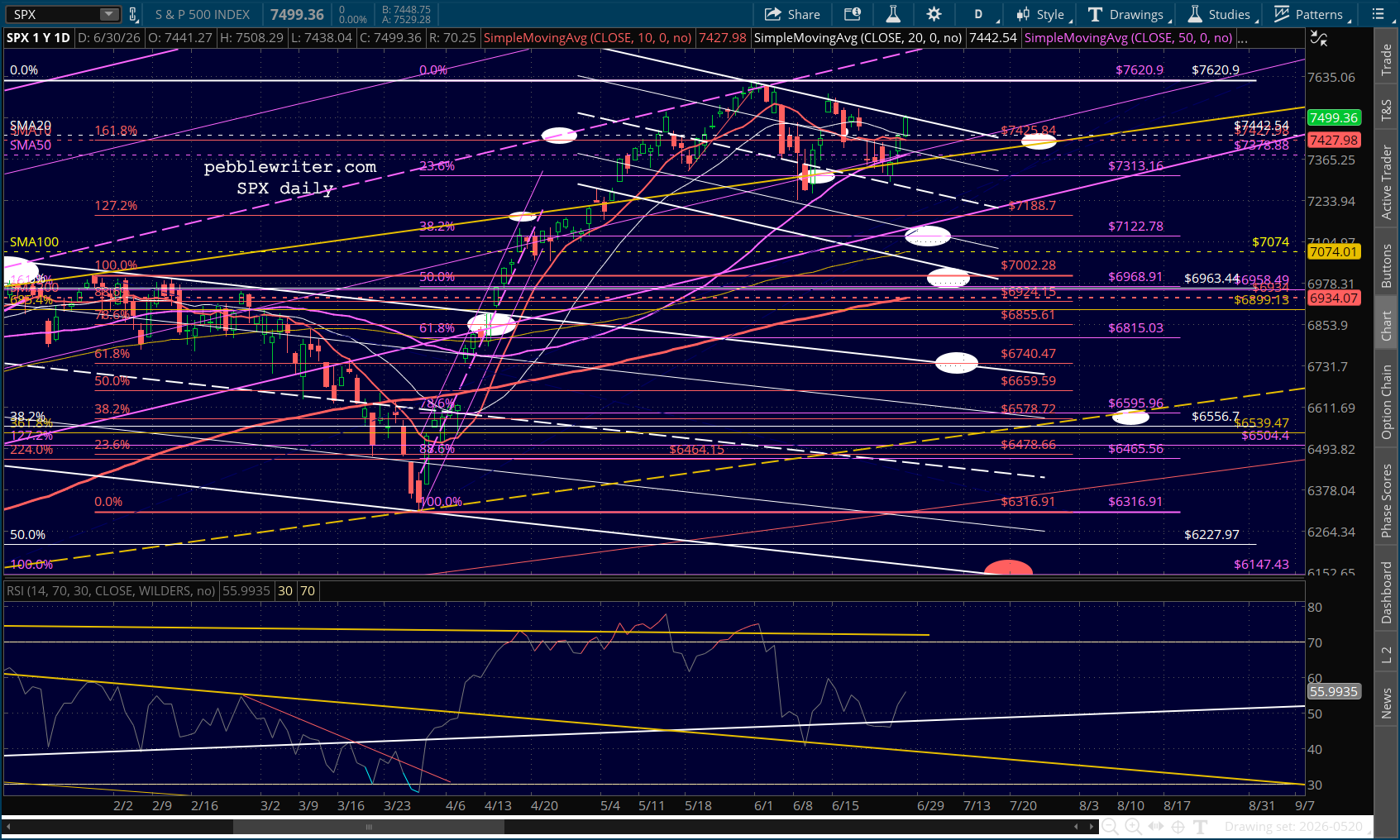

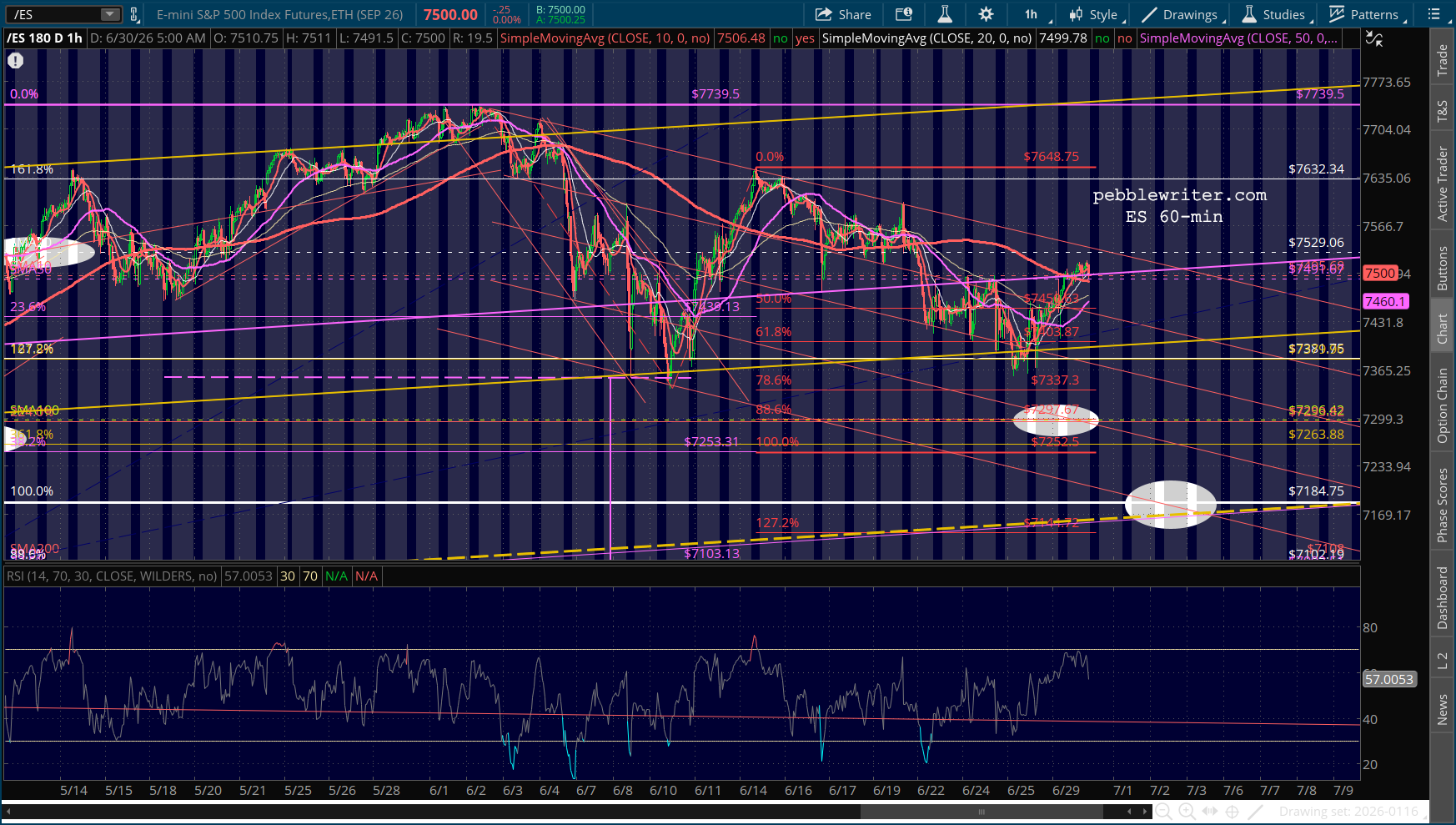

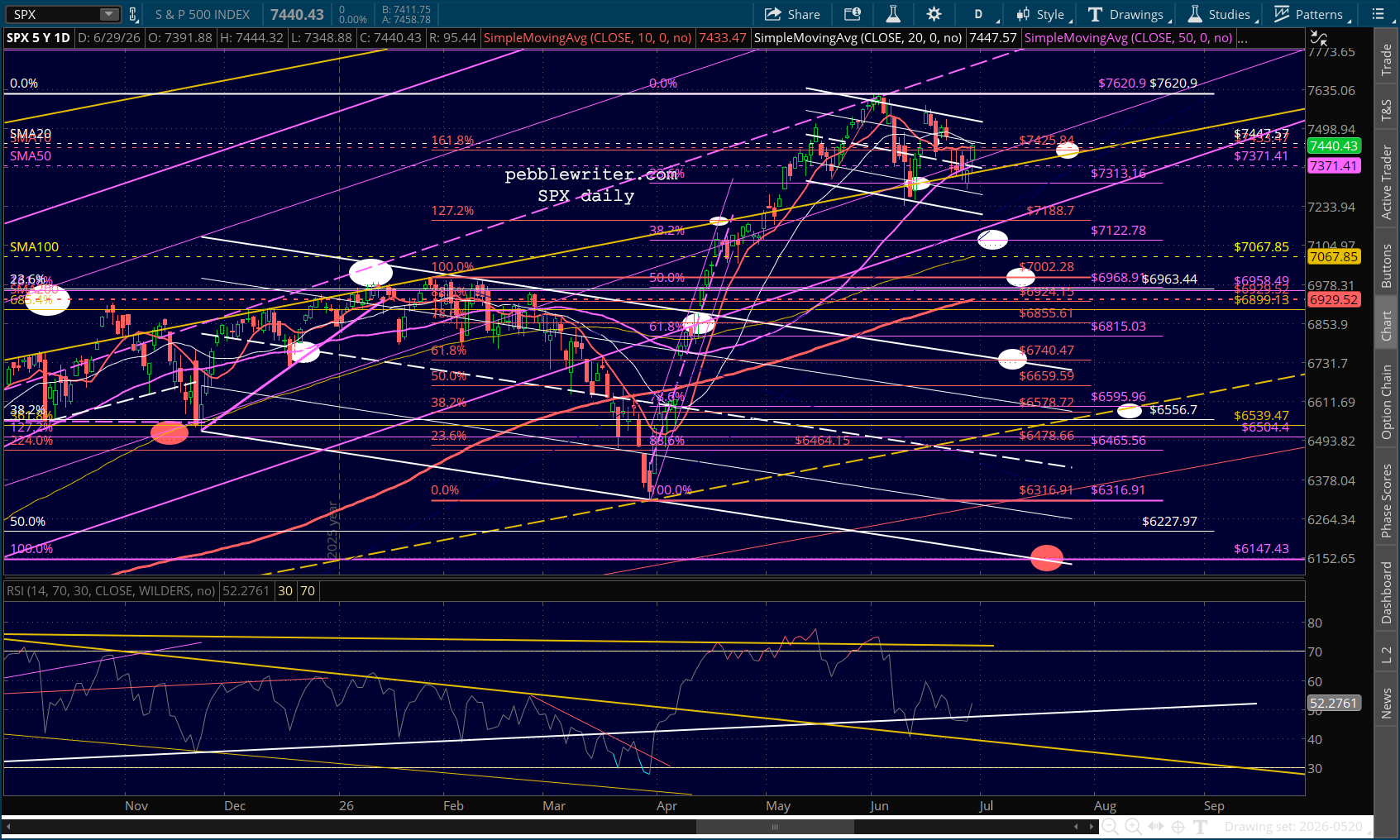

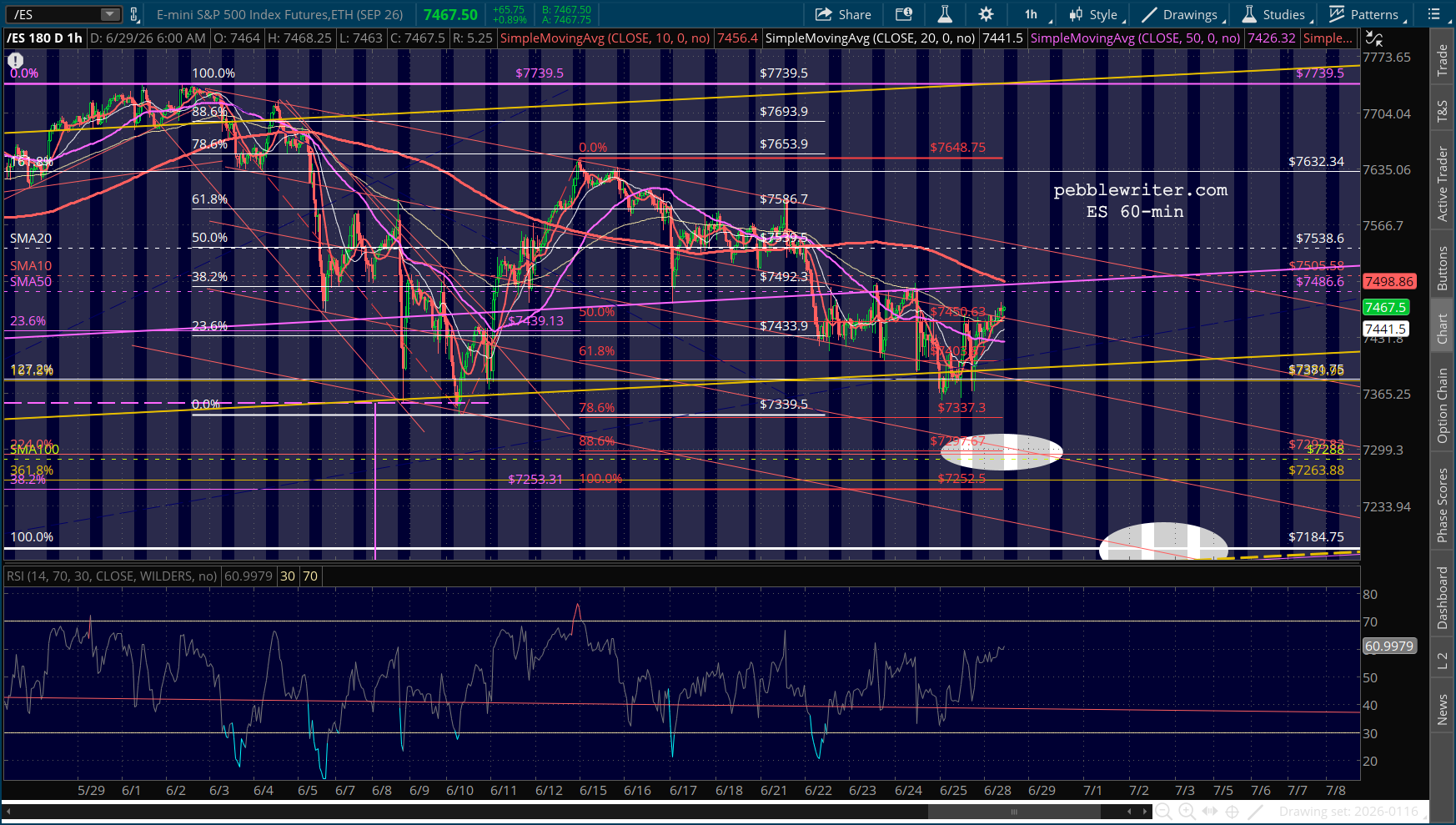

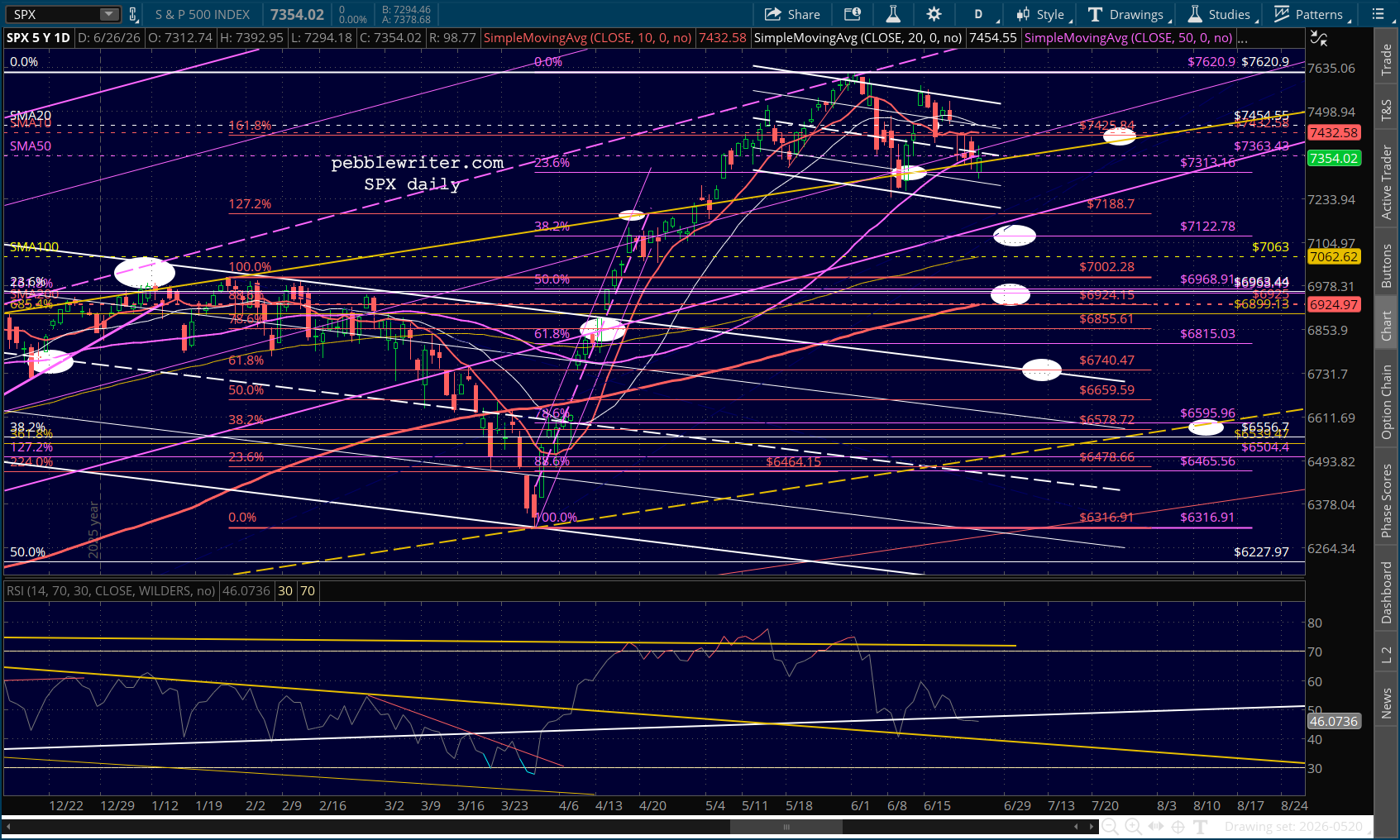

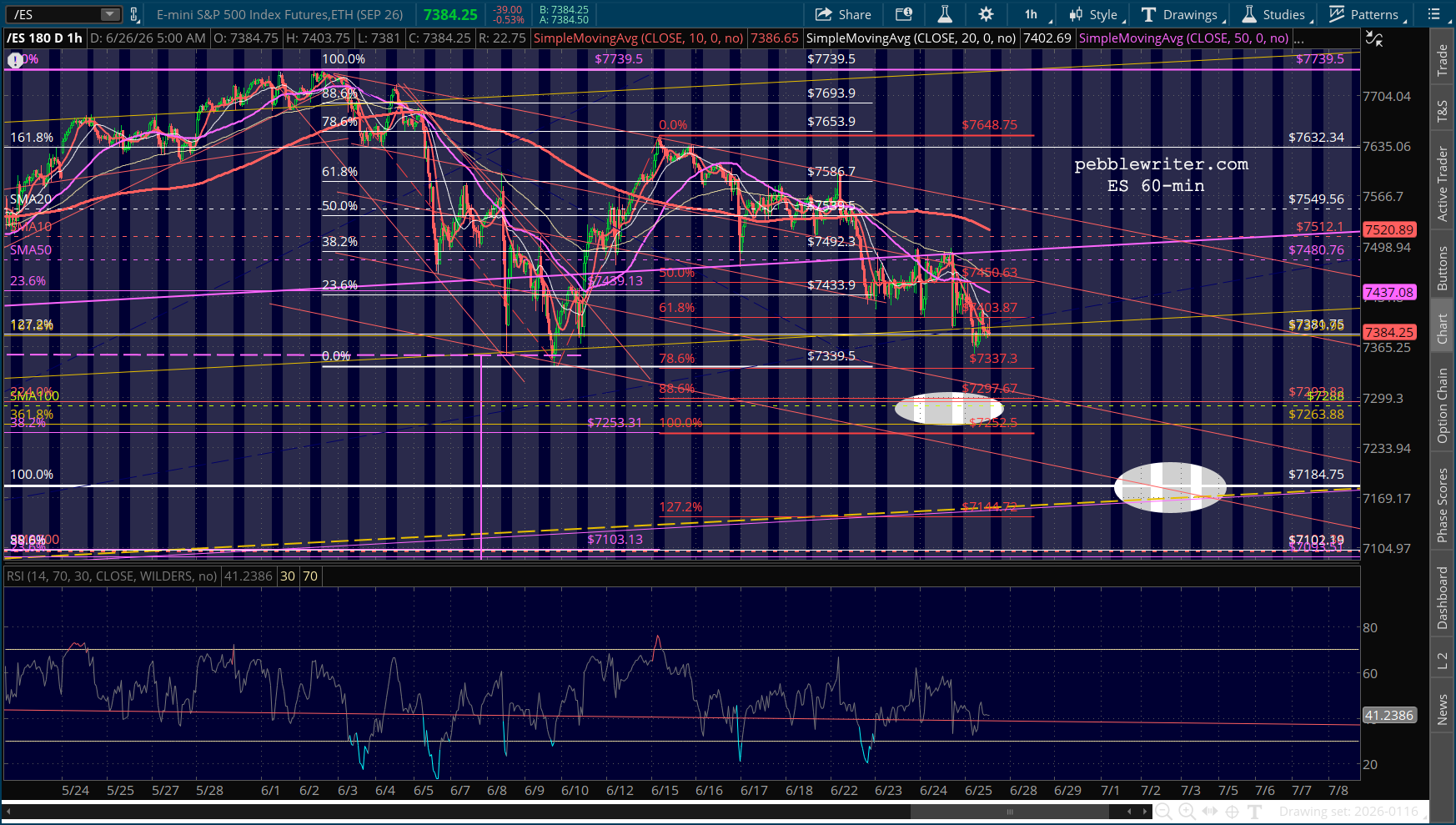

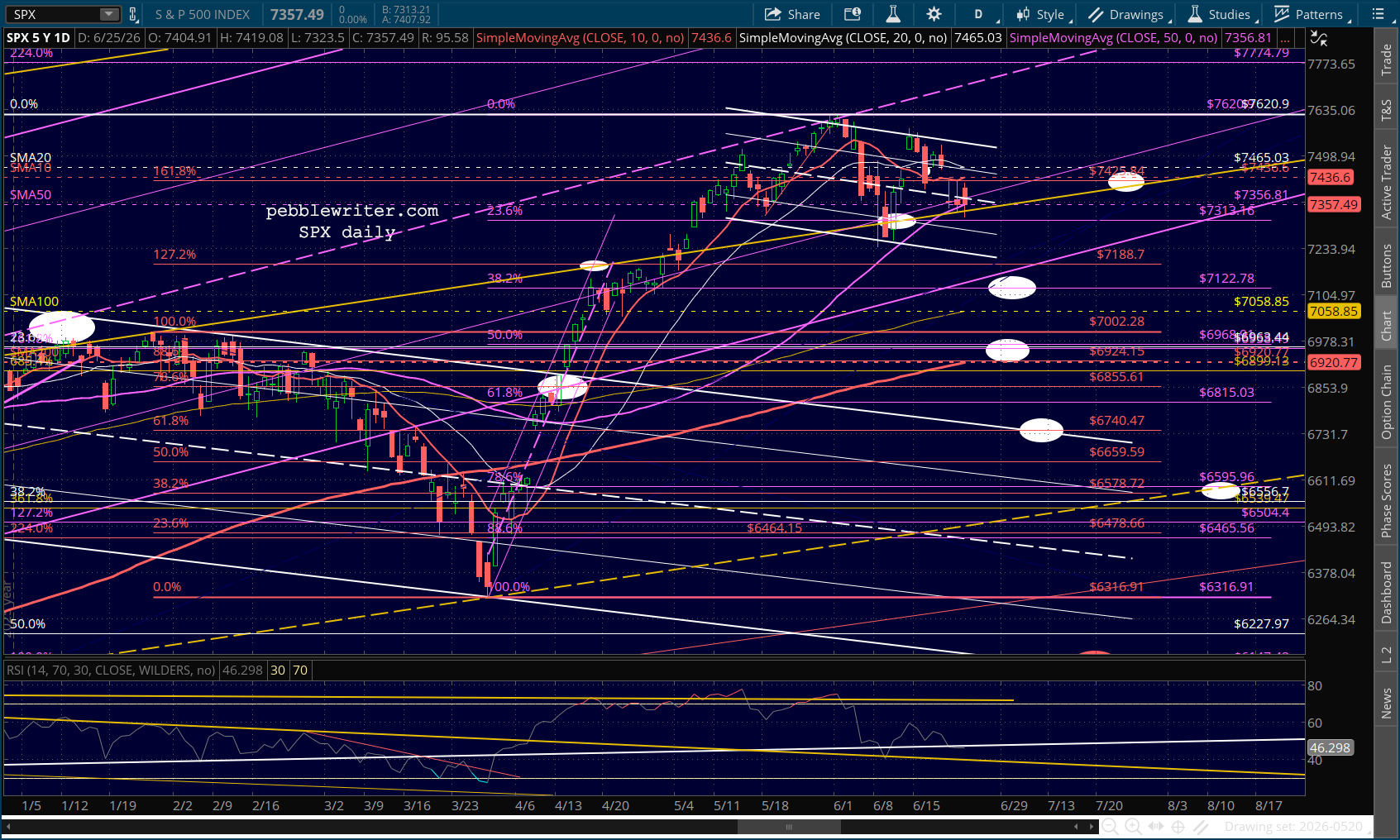

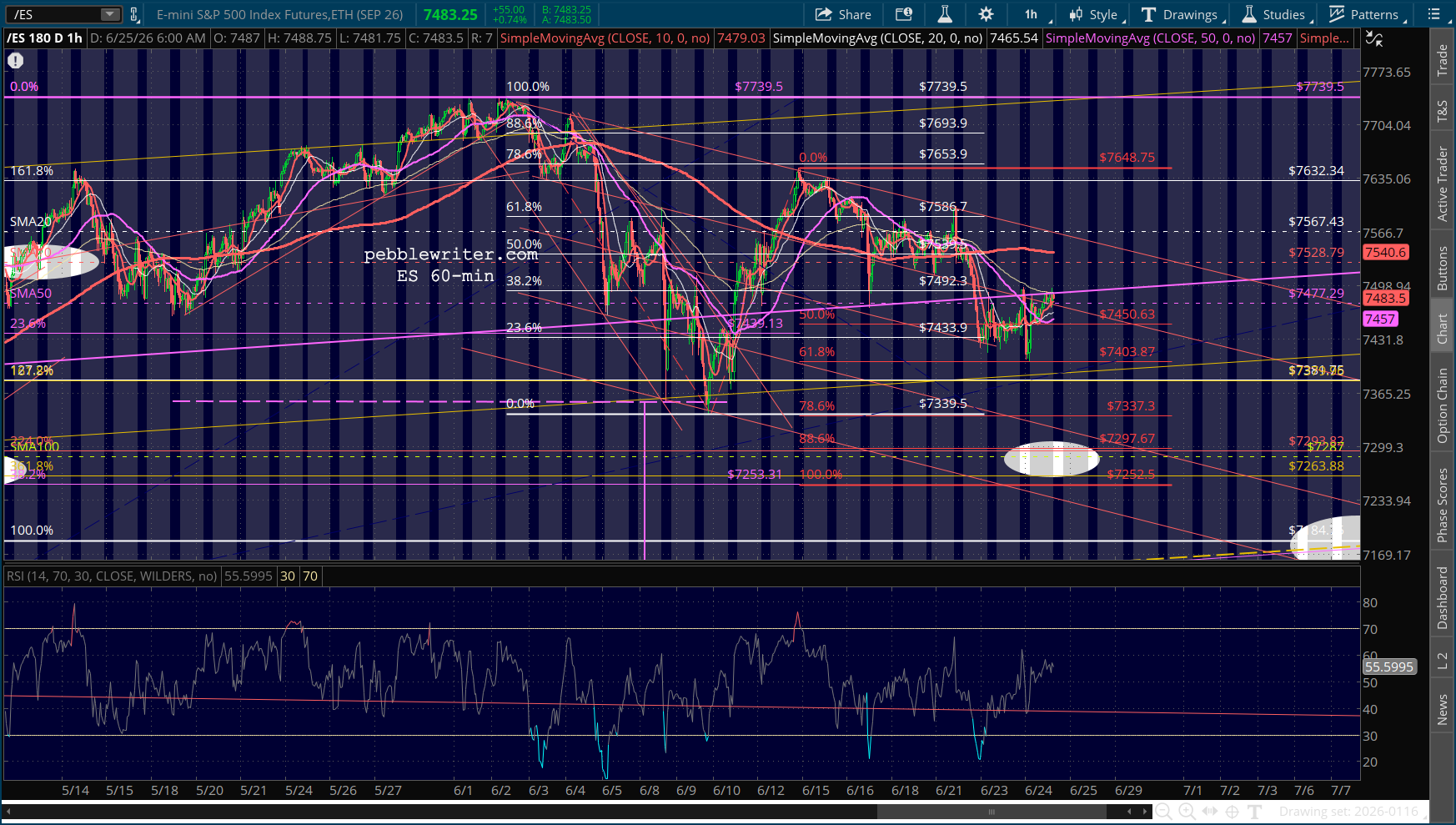

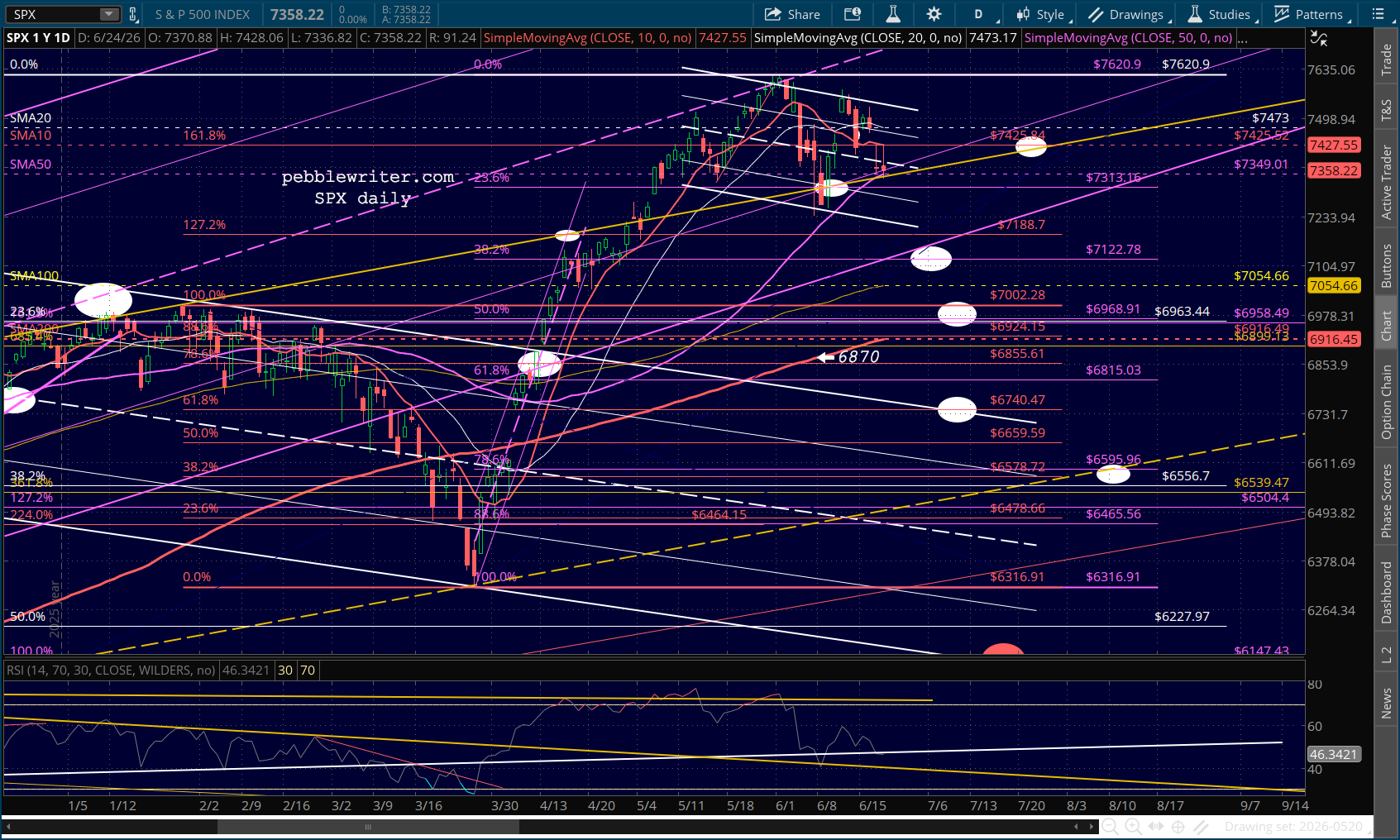

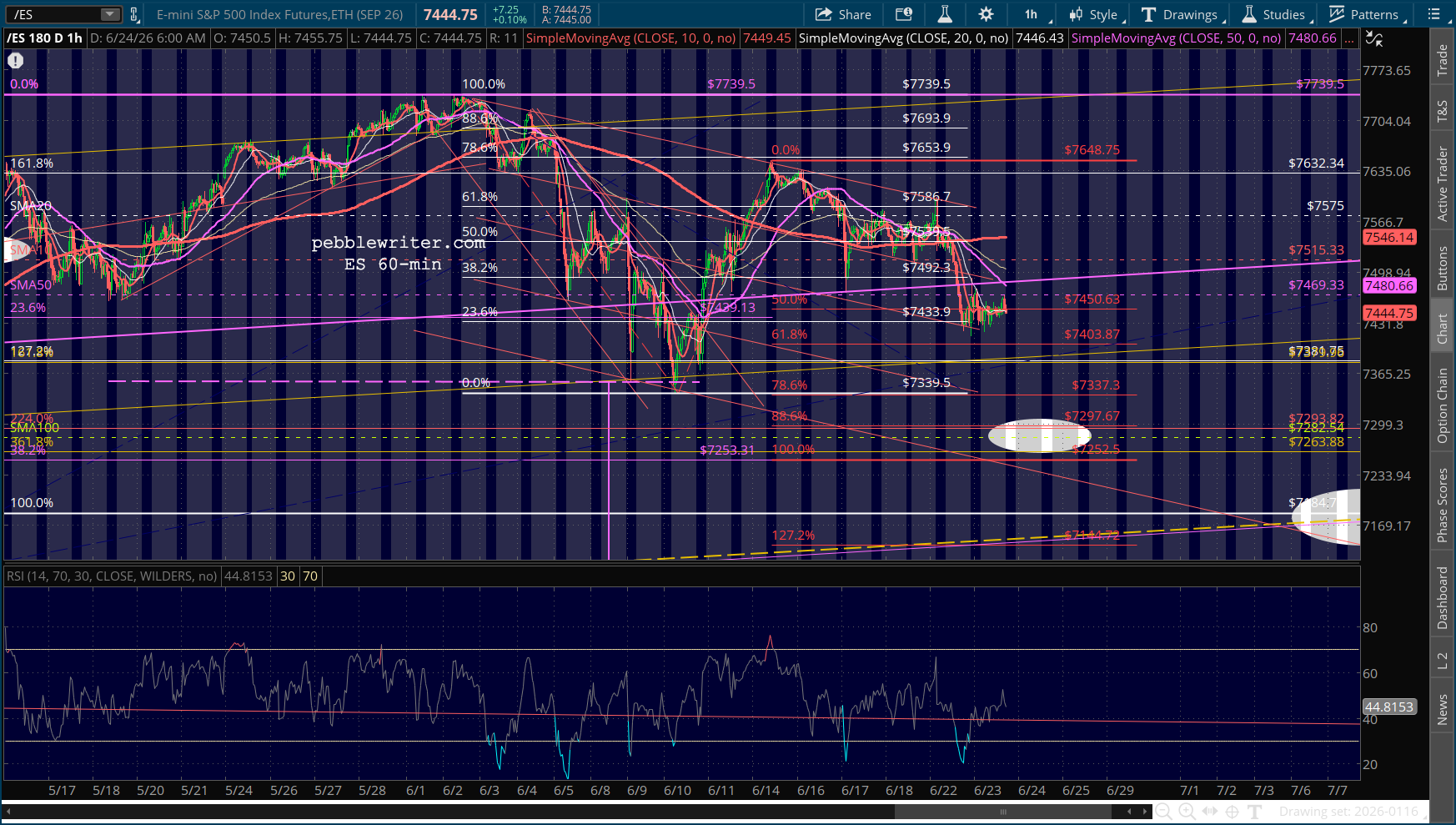

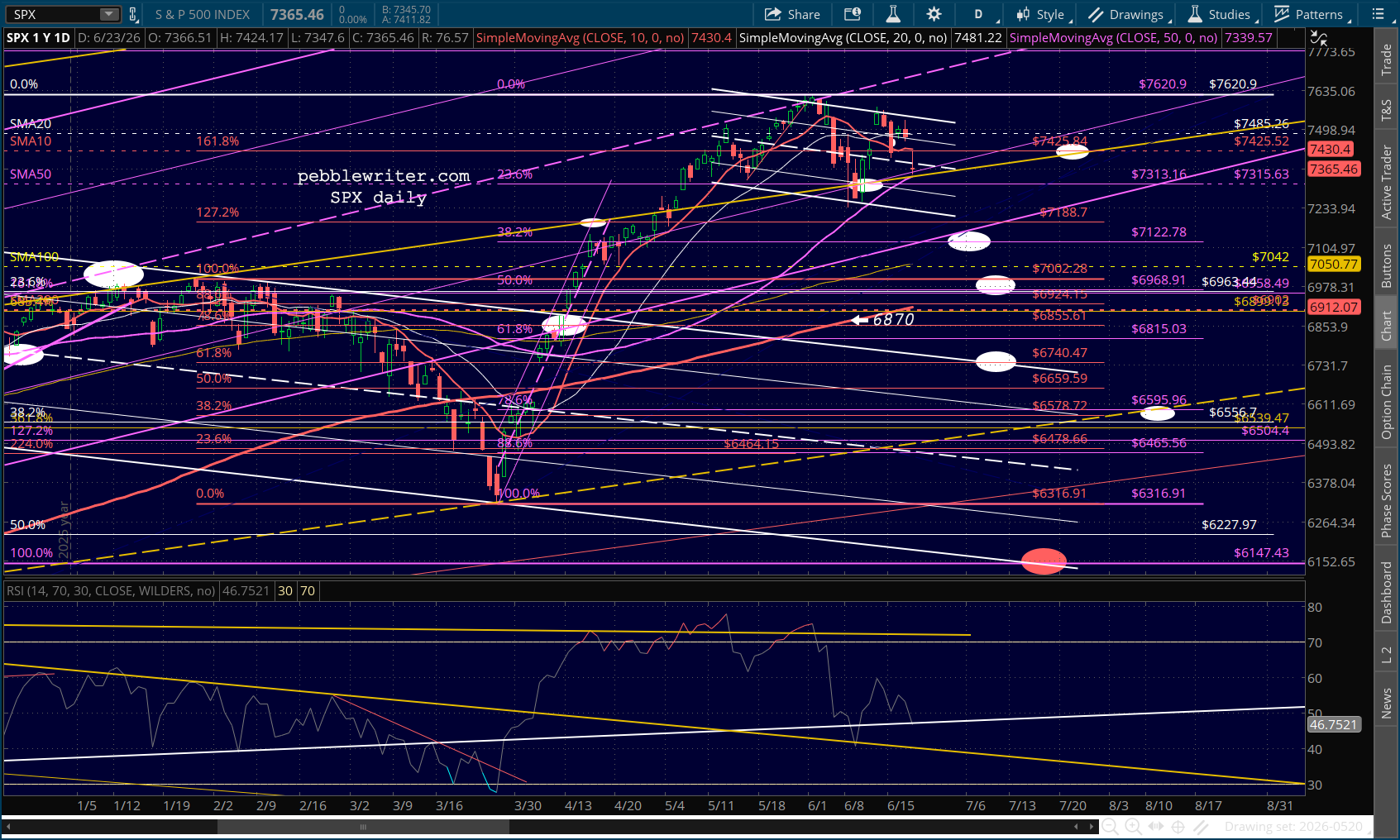

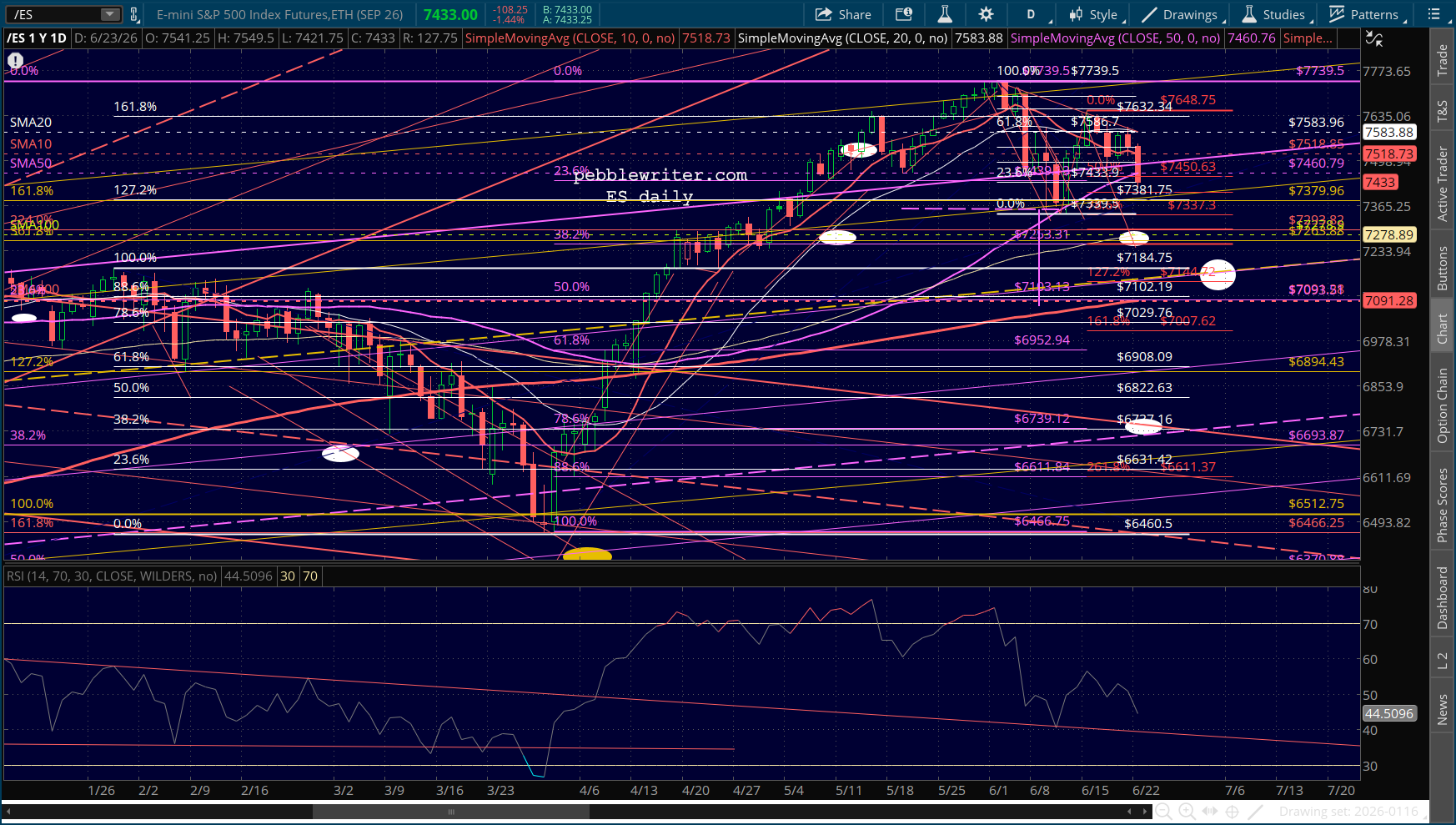

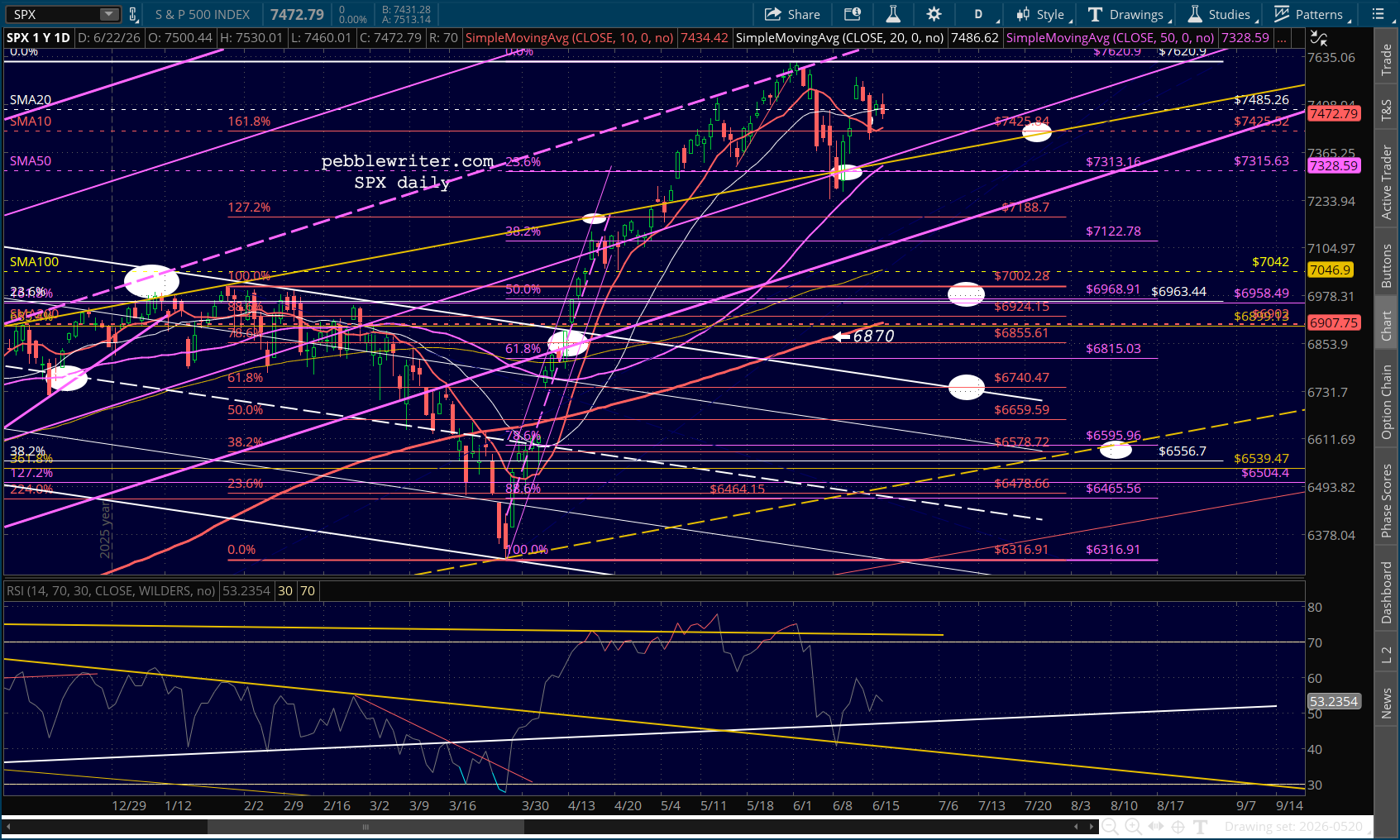

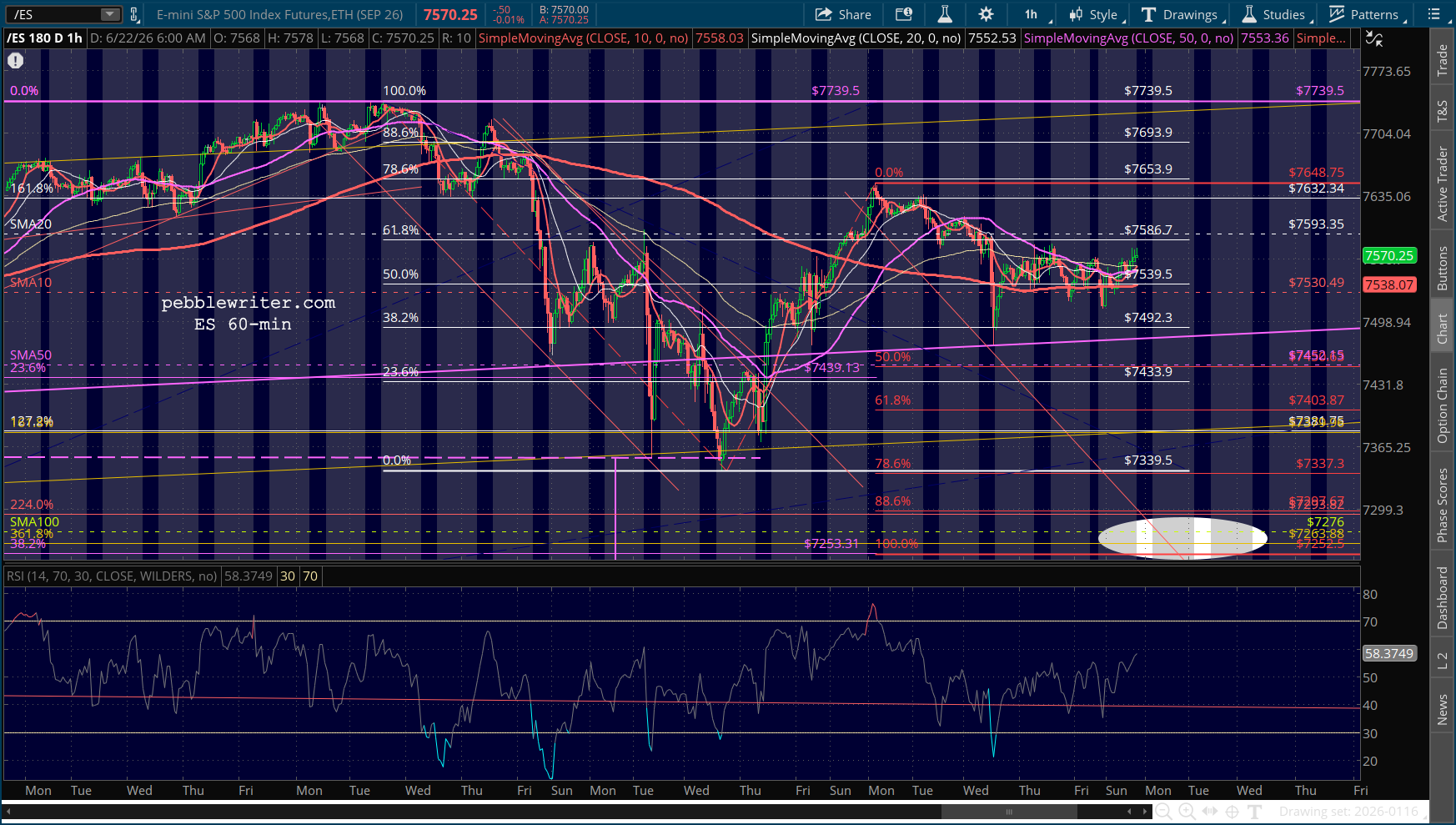

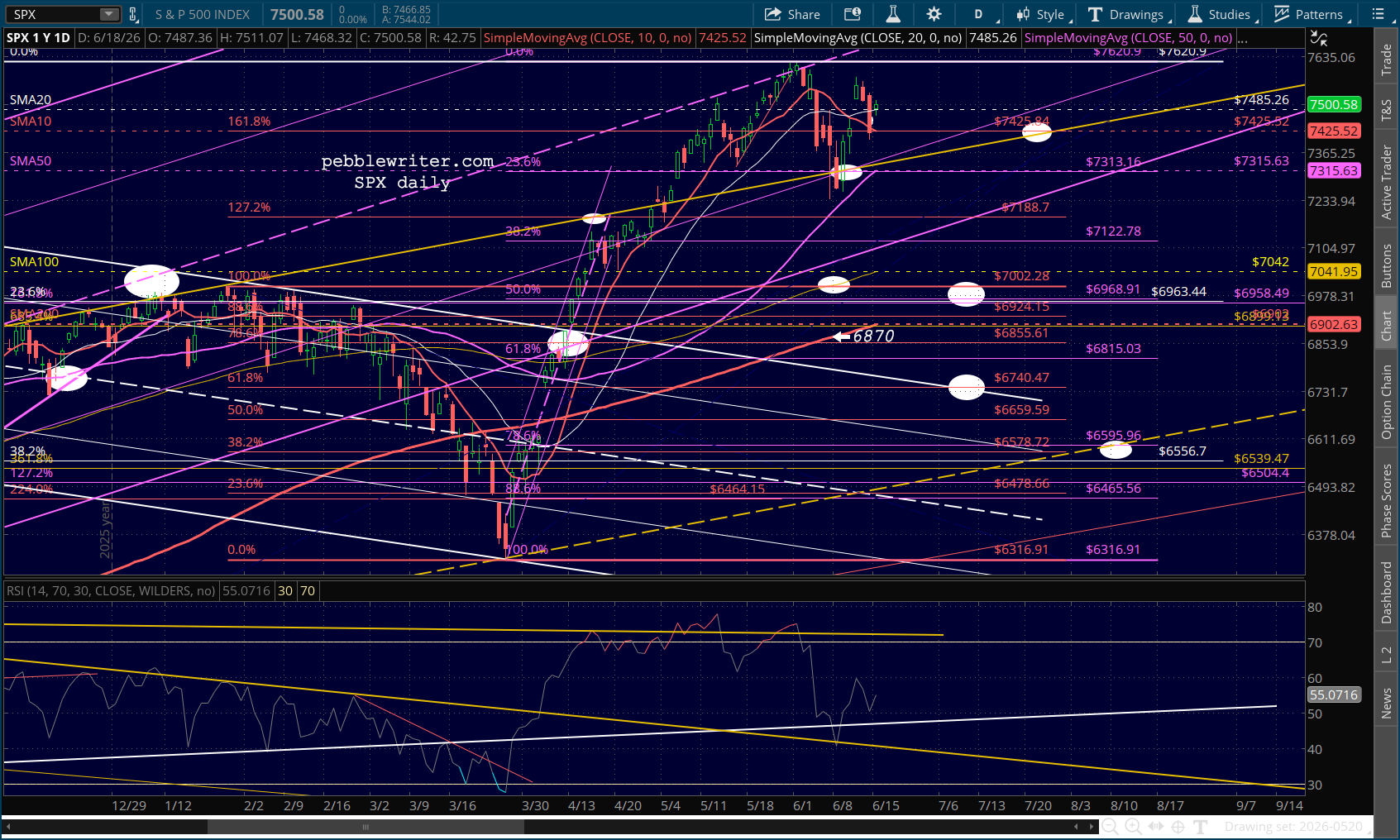

Which to believe: SPX, which just completed a bullish 10/20 cross, or ES, which is stubbornly showing a bearish 10/20 cross?

The odds of the stasis continuing rise with Trump ringing the bell today…

Which to believe: SPX, which just completed a bullish 10/20 cross, or ES, which is stubbornly showing a bearish 10/20 cross?

The odds of the stasis continuing rise with Trump ringing the bell today…

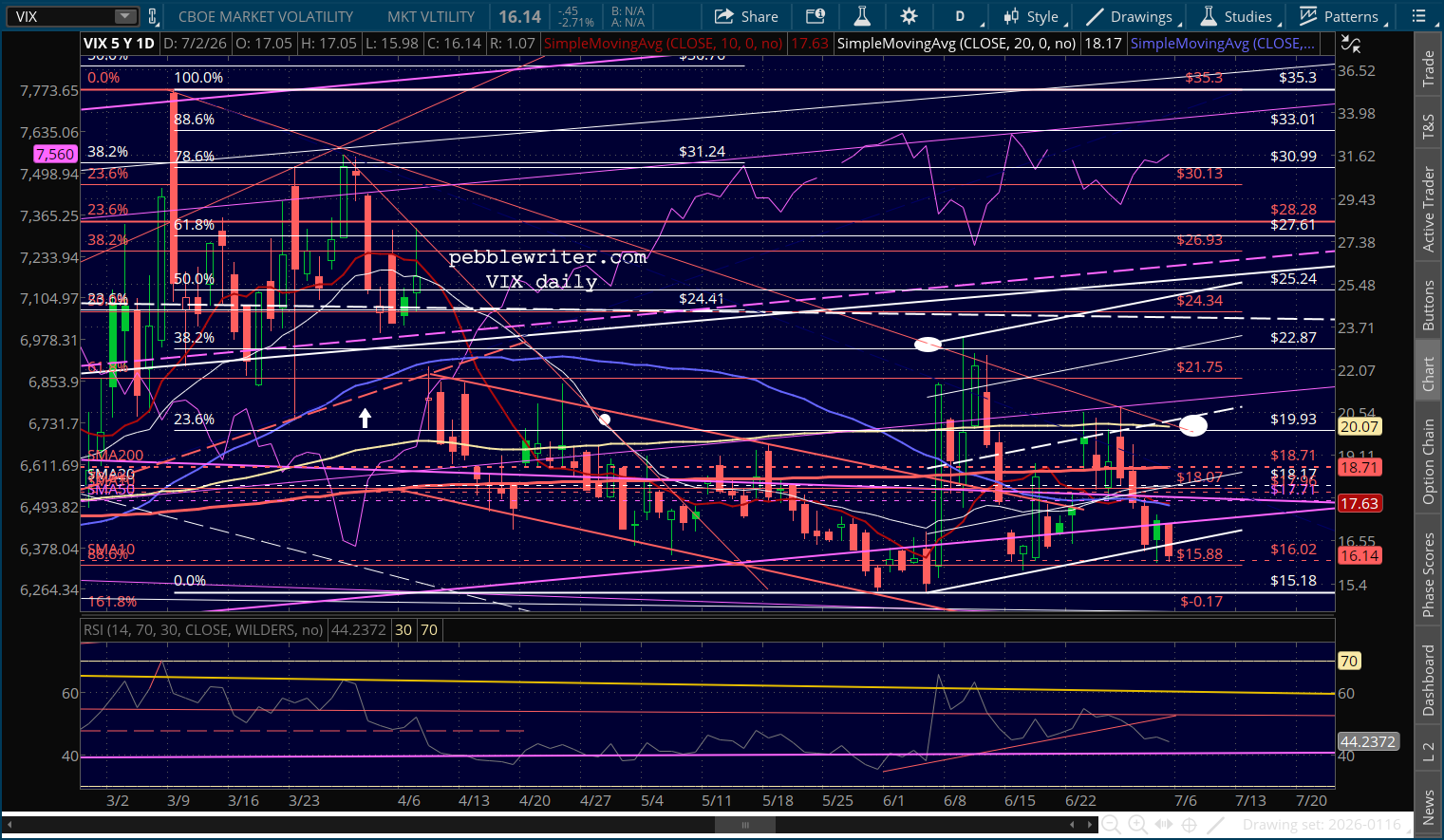

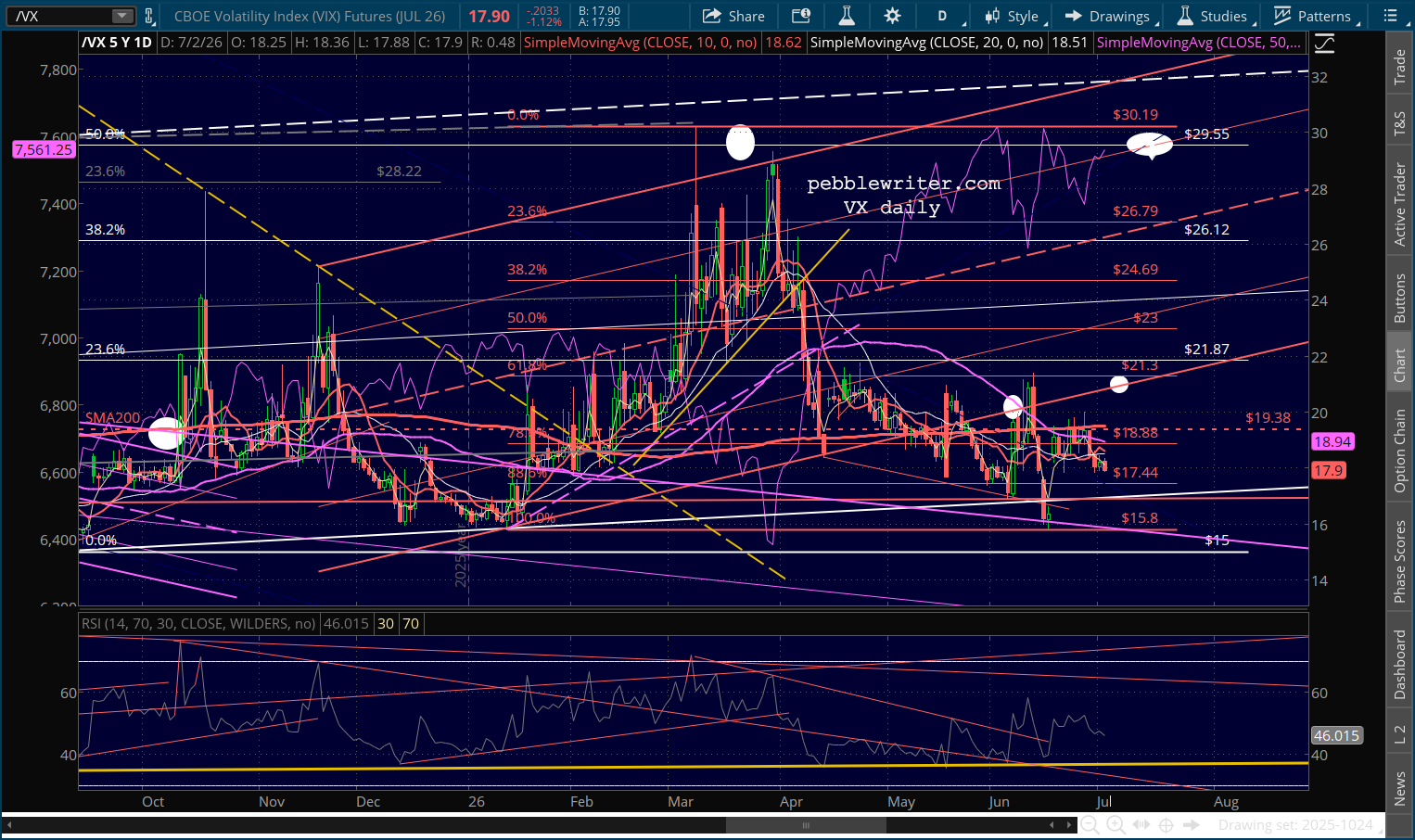

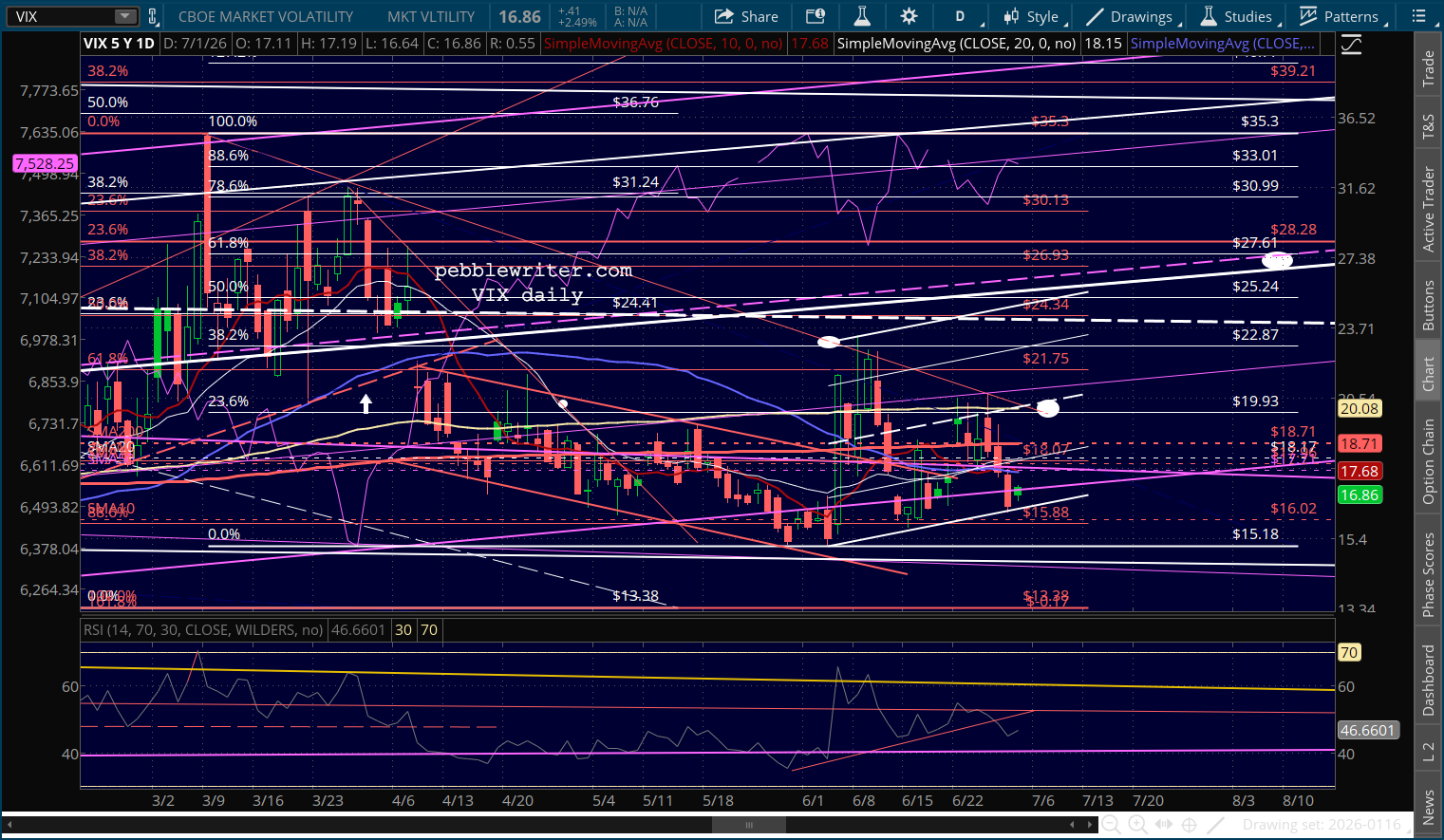

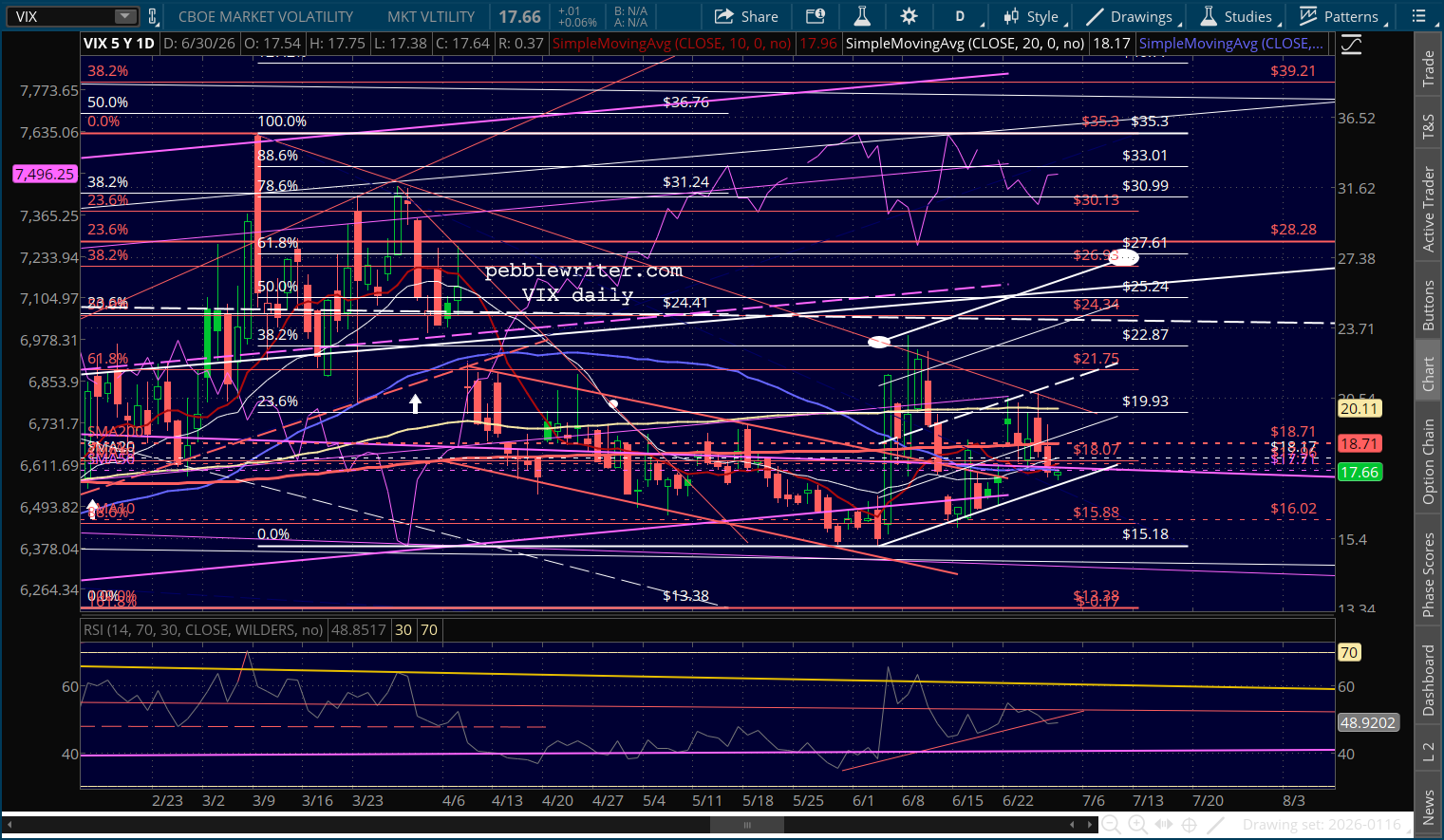

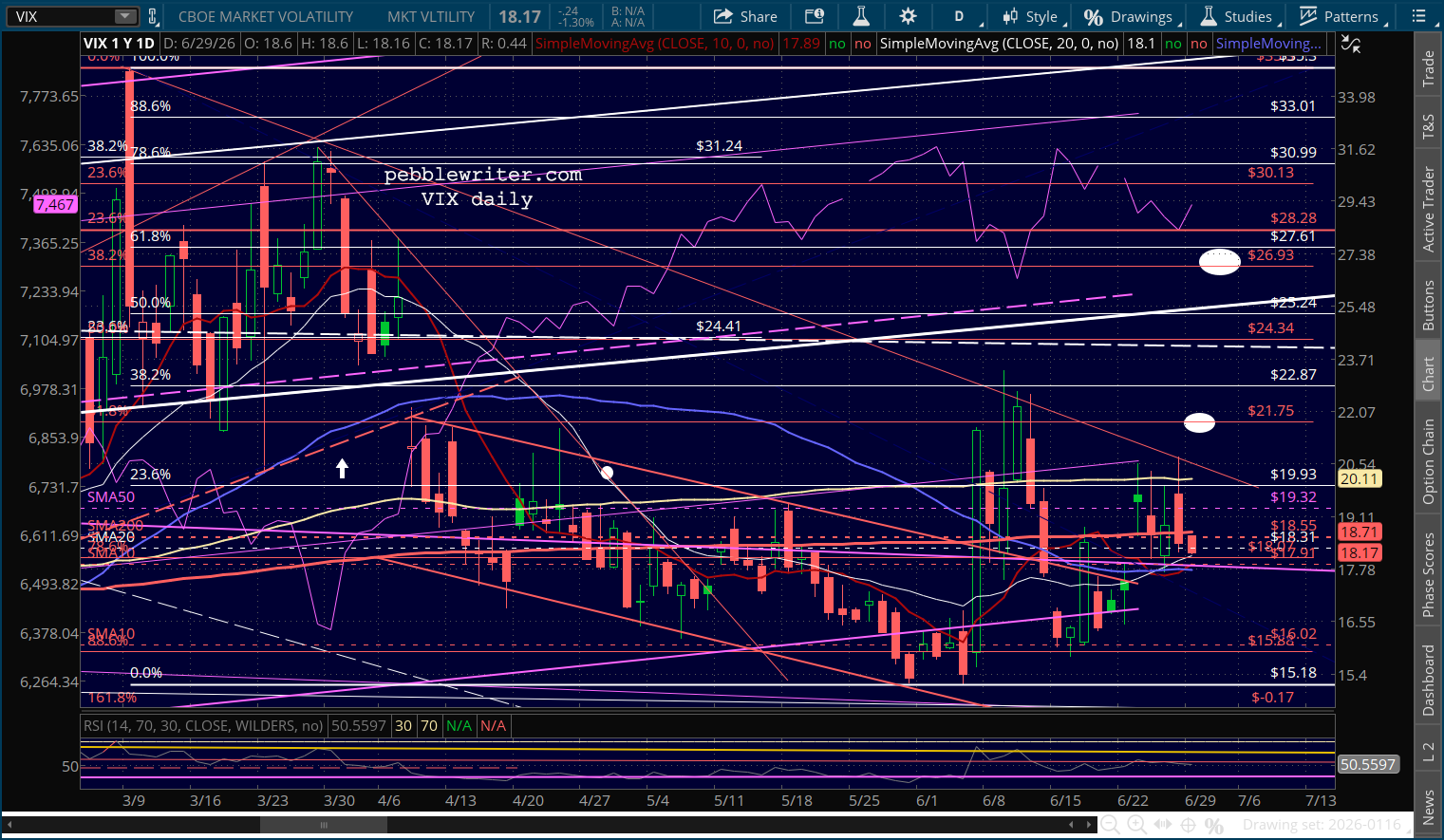

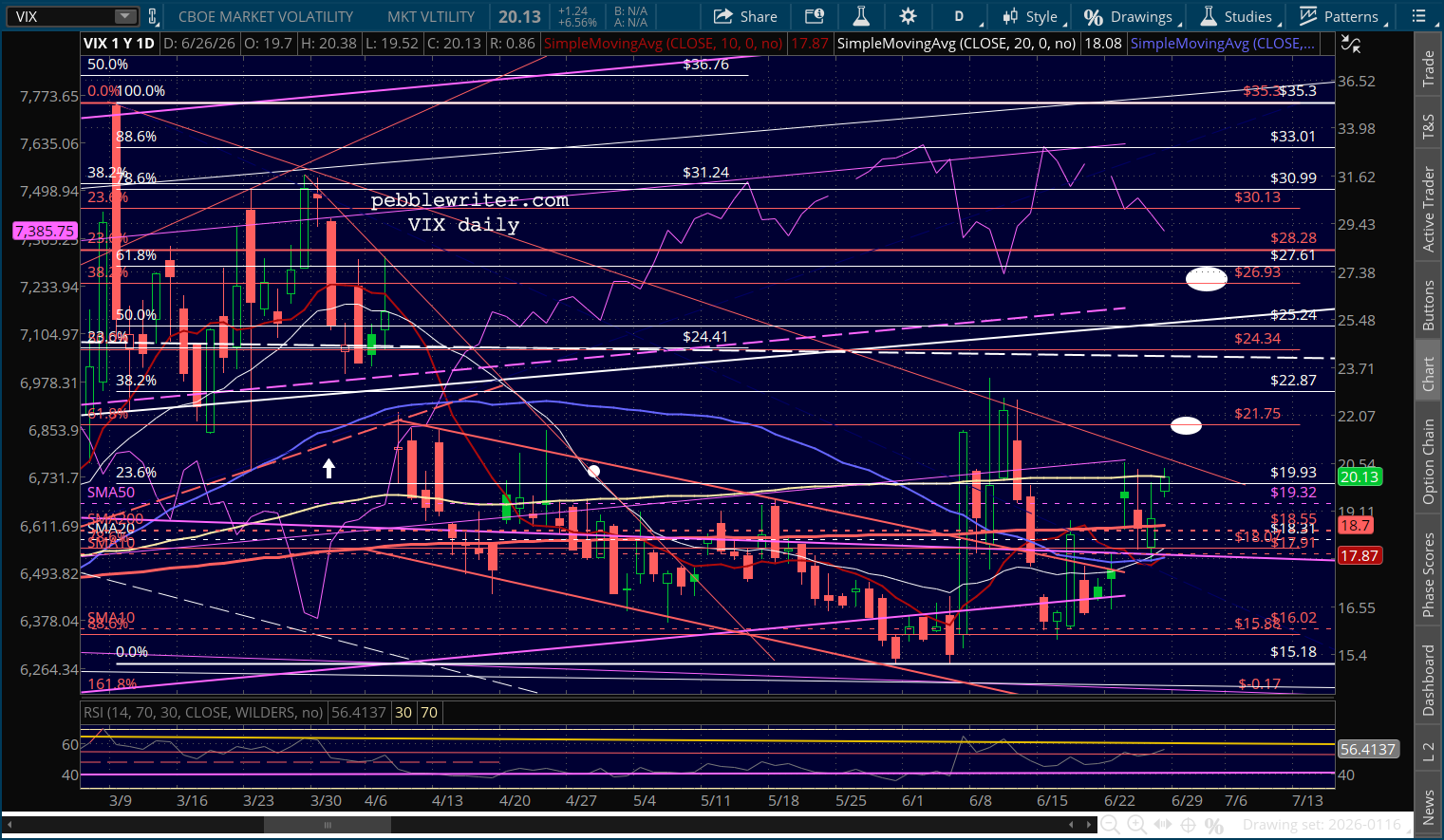

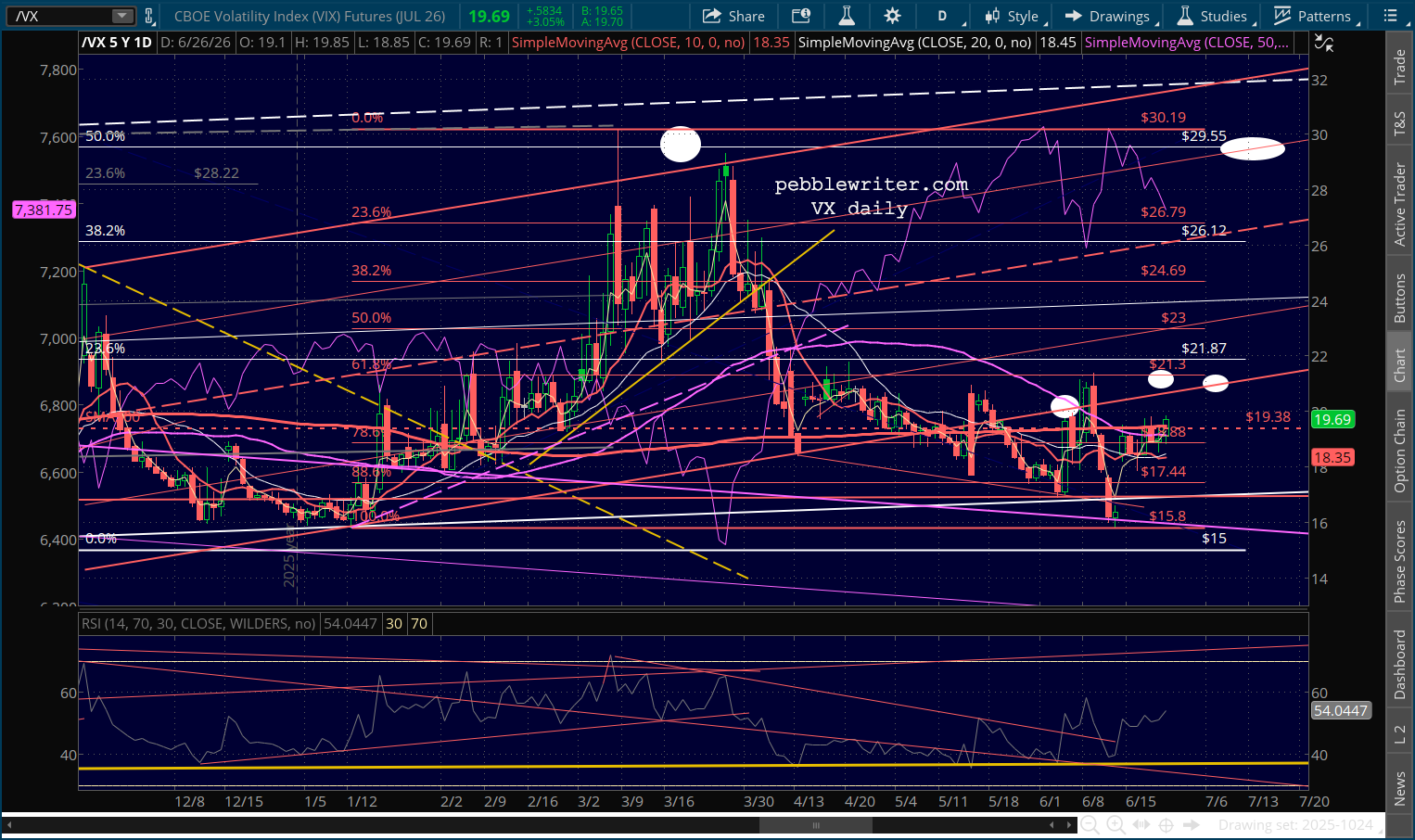

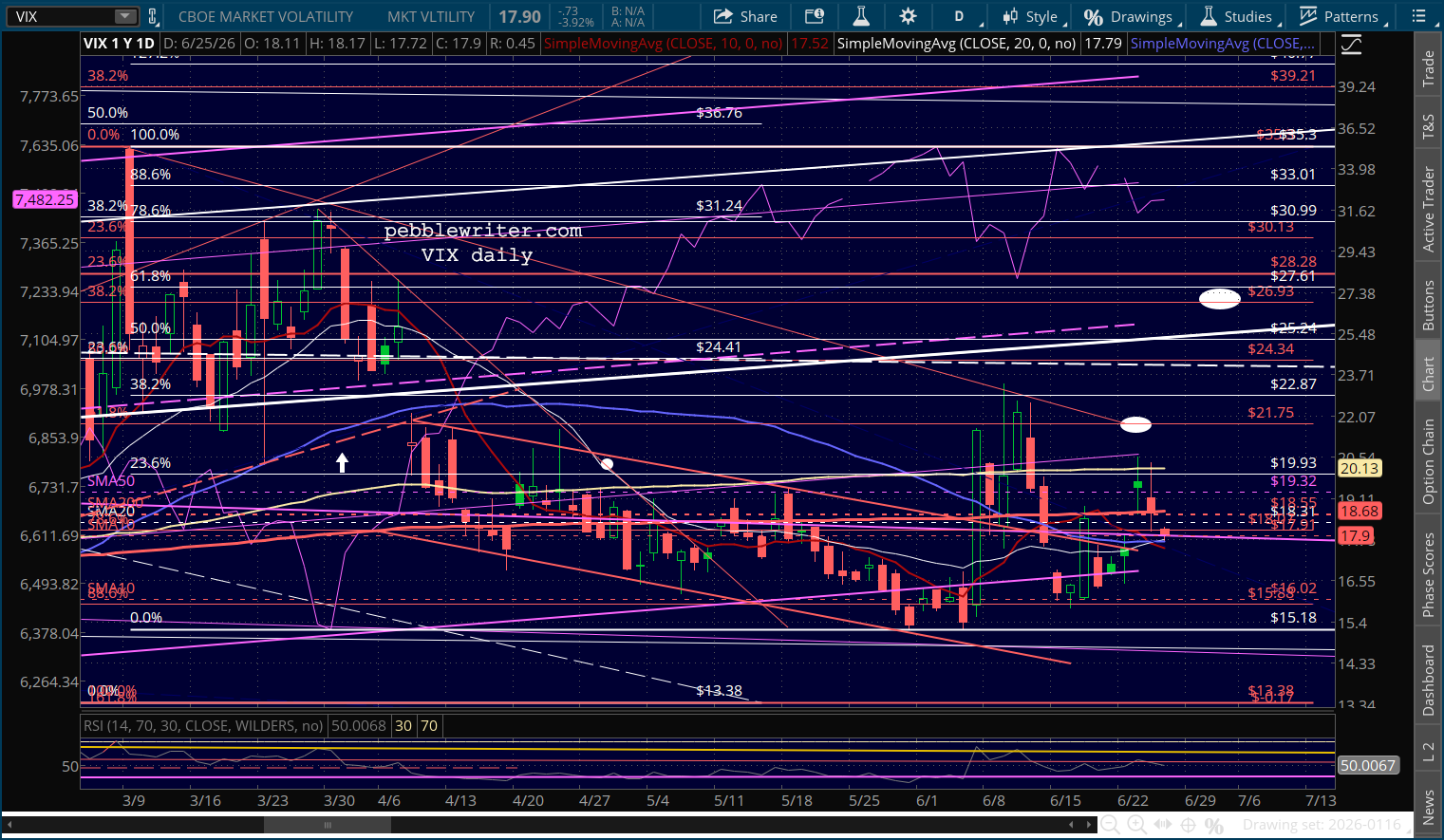

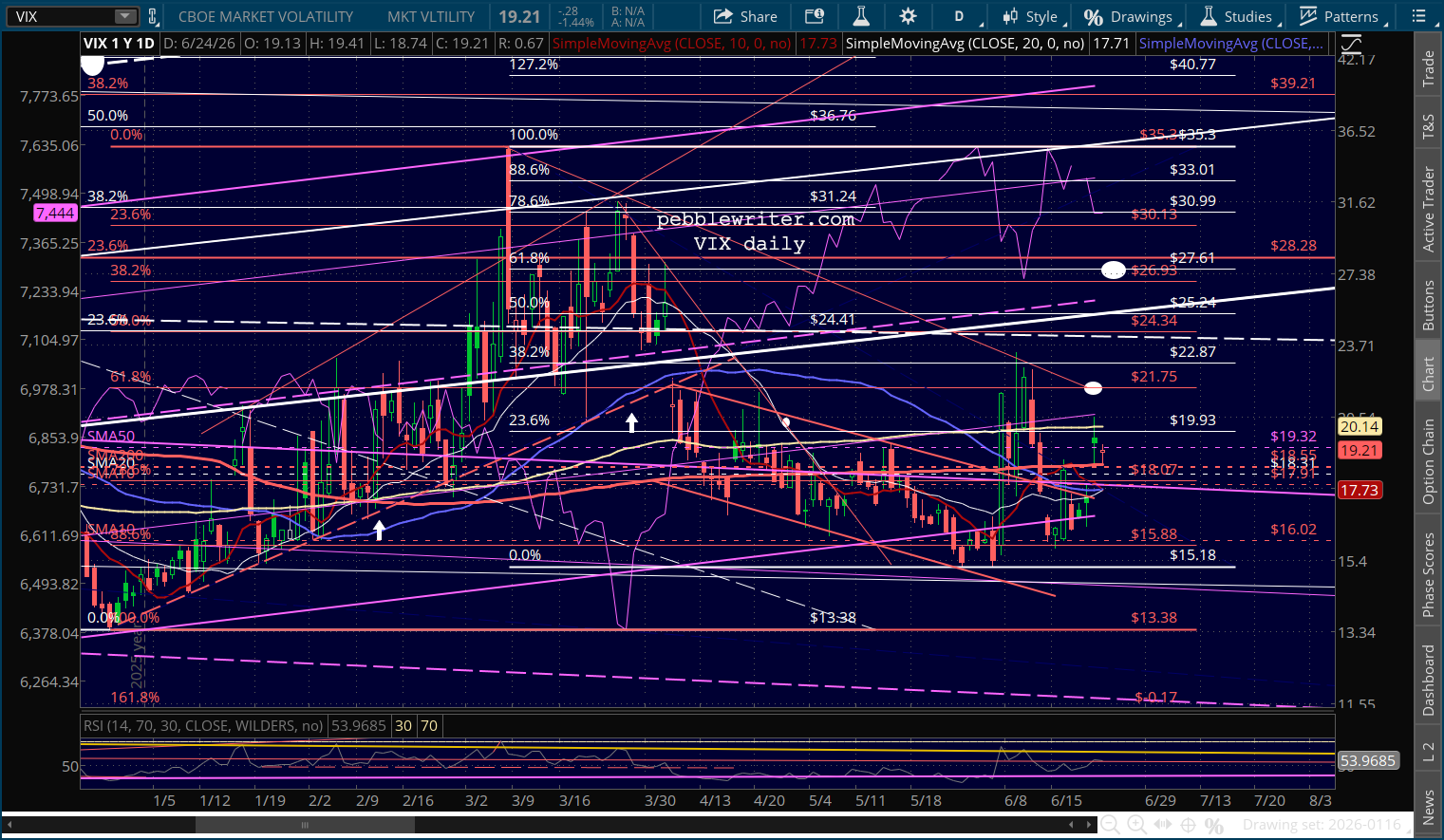

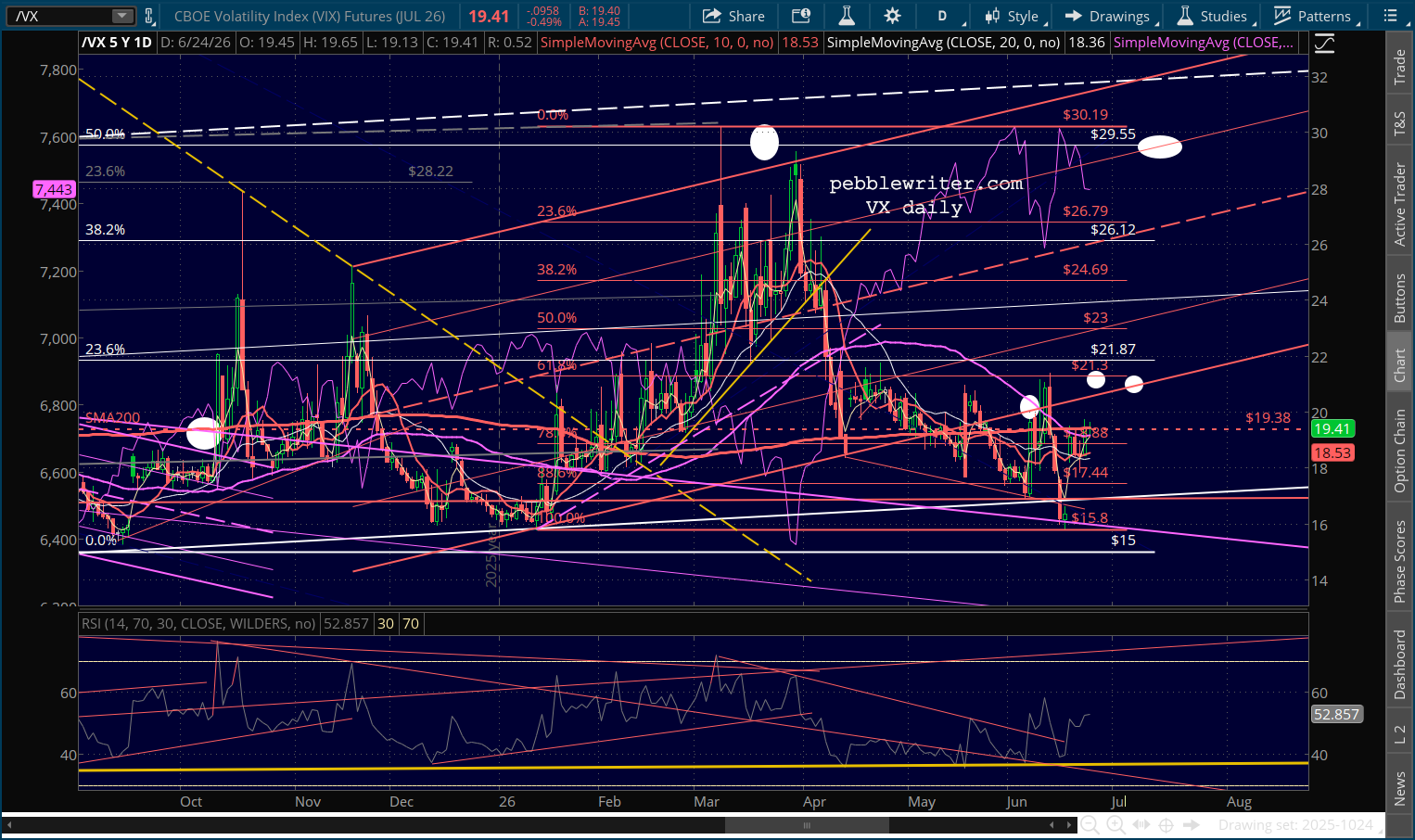

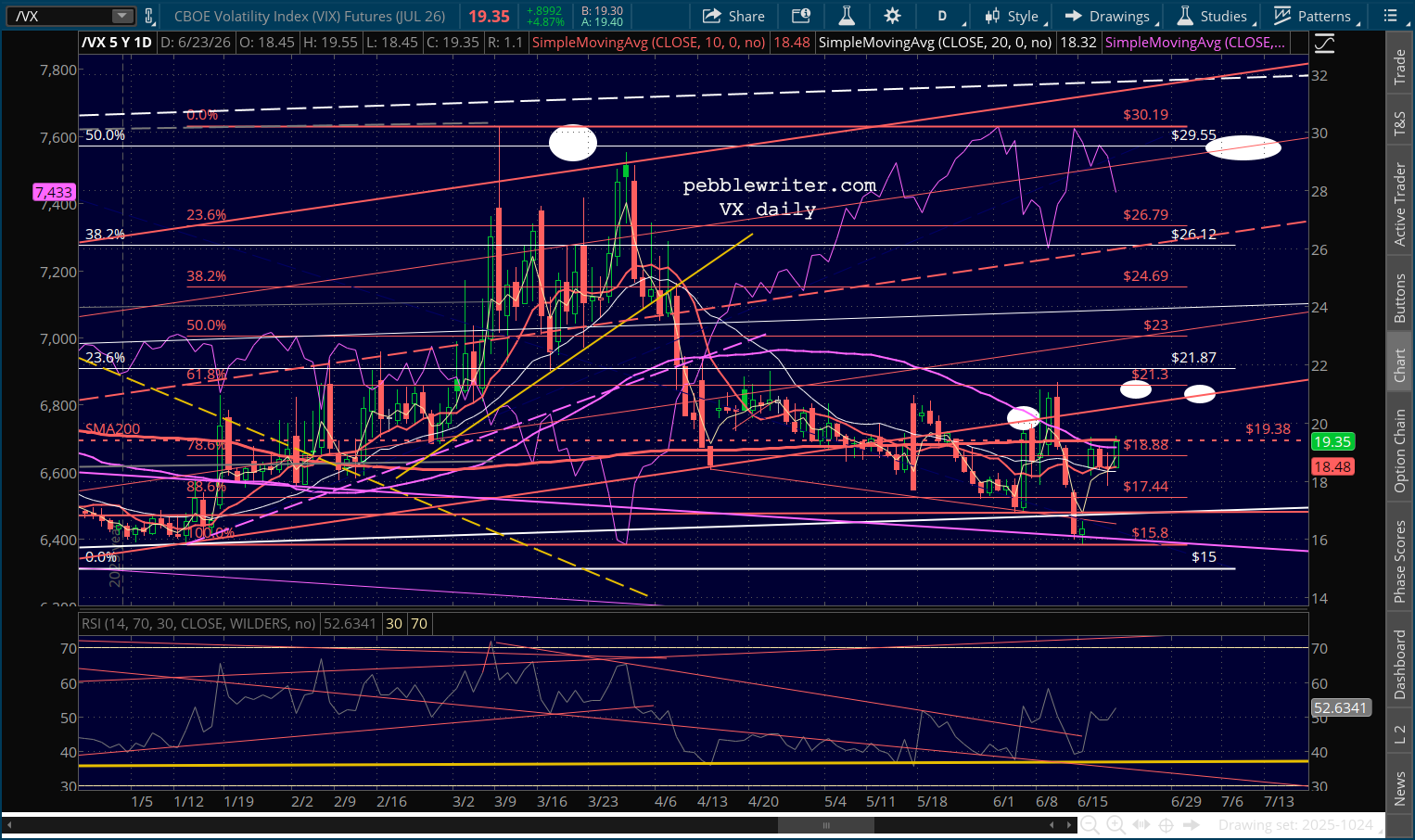

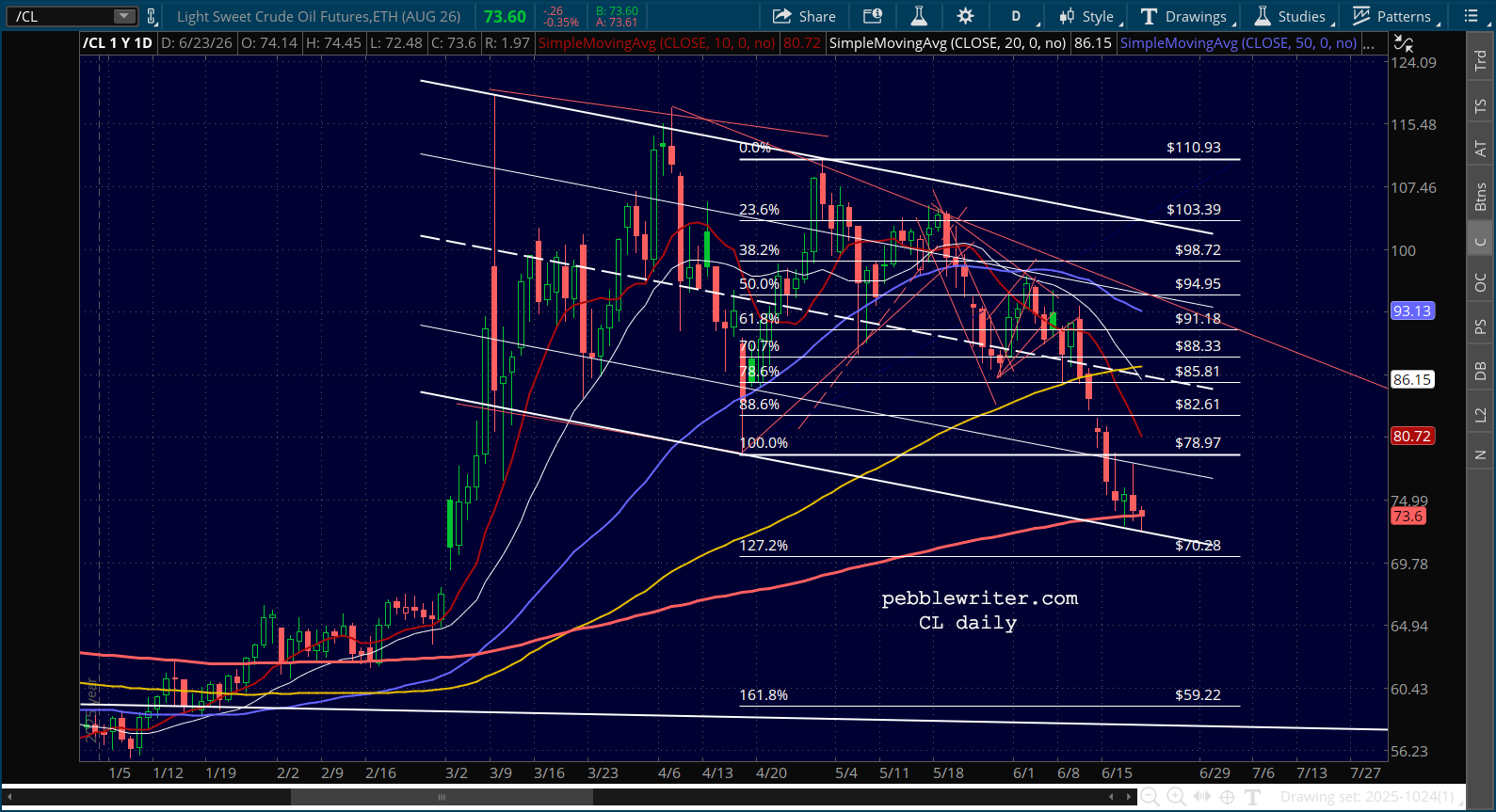

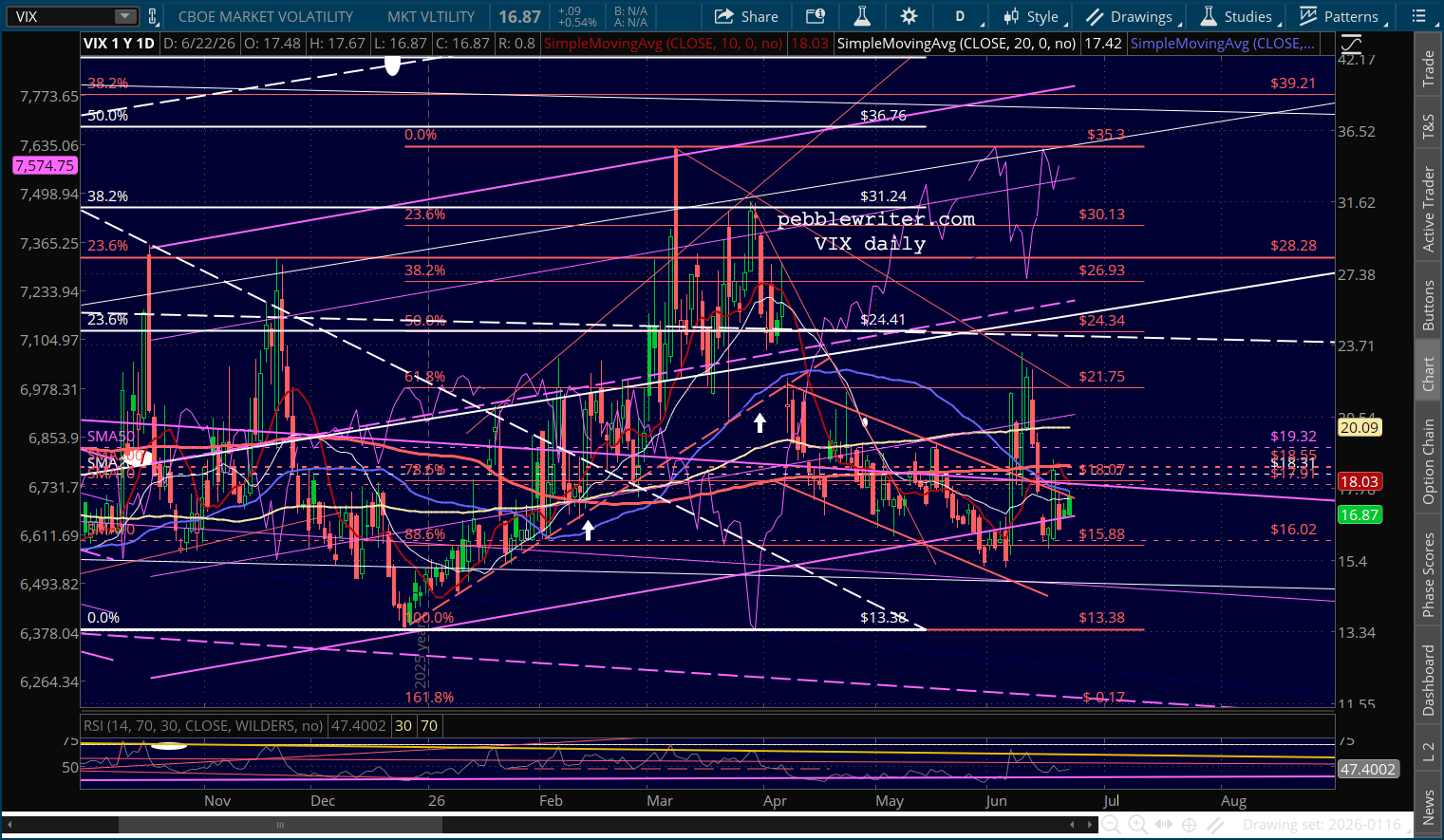

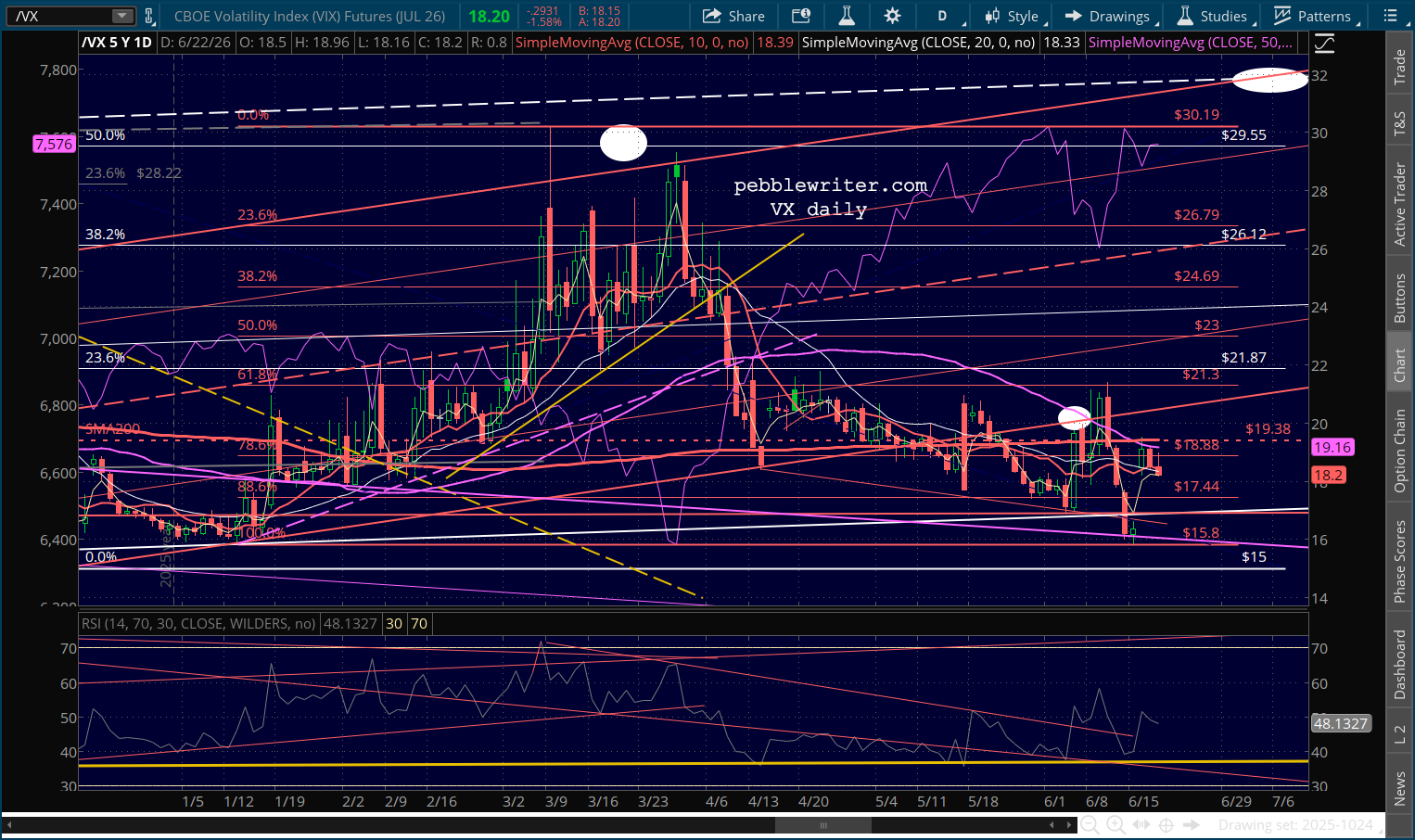

Futures are moderately higher following disappointing jobs data (57K vs 130K), CL’s drop through support, and another pointed decline in VIX. The algos are happy.

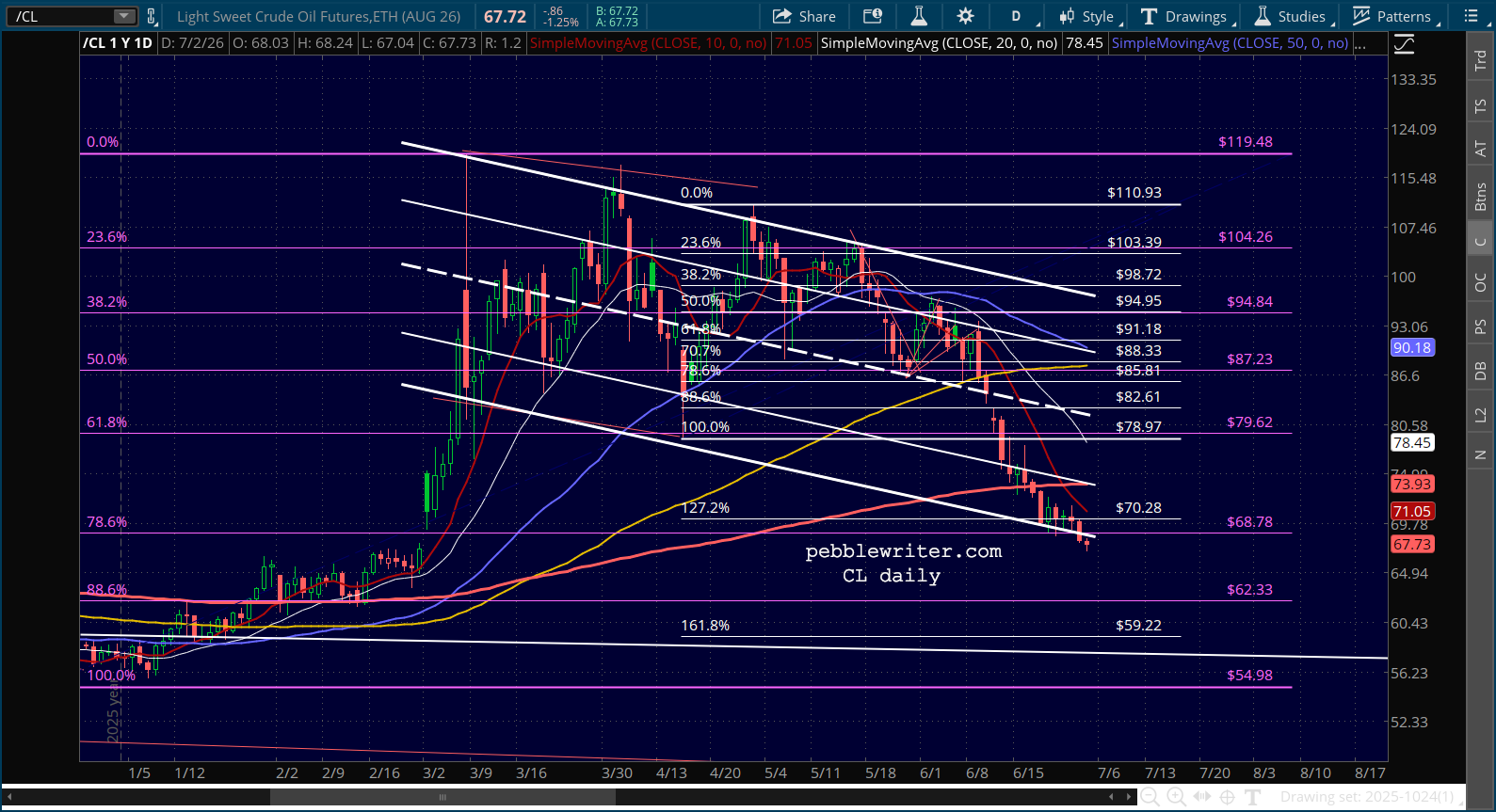

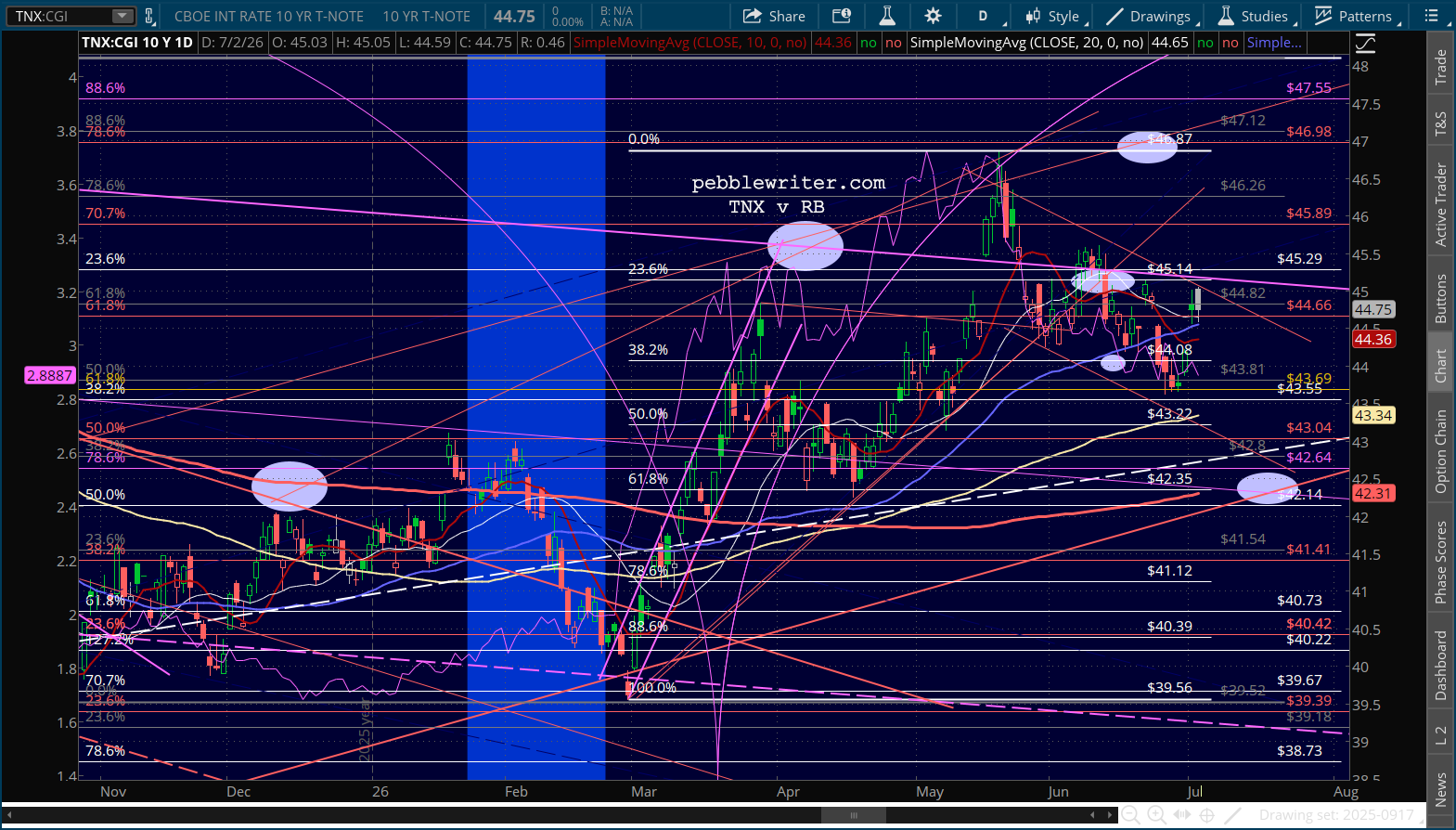

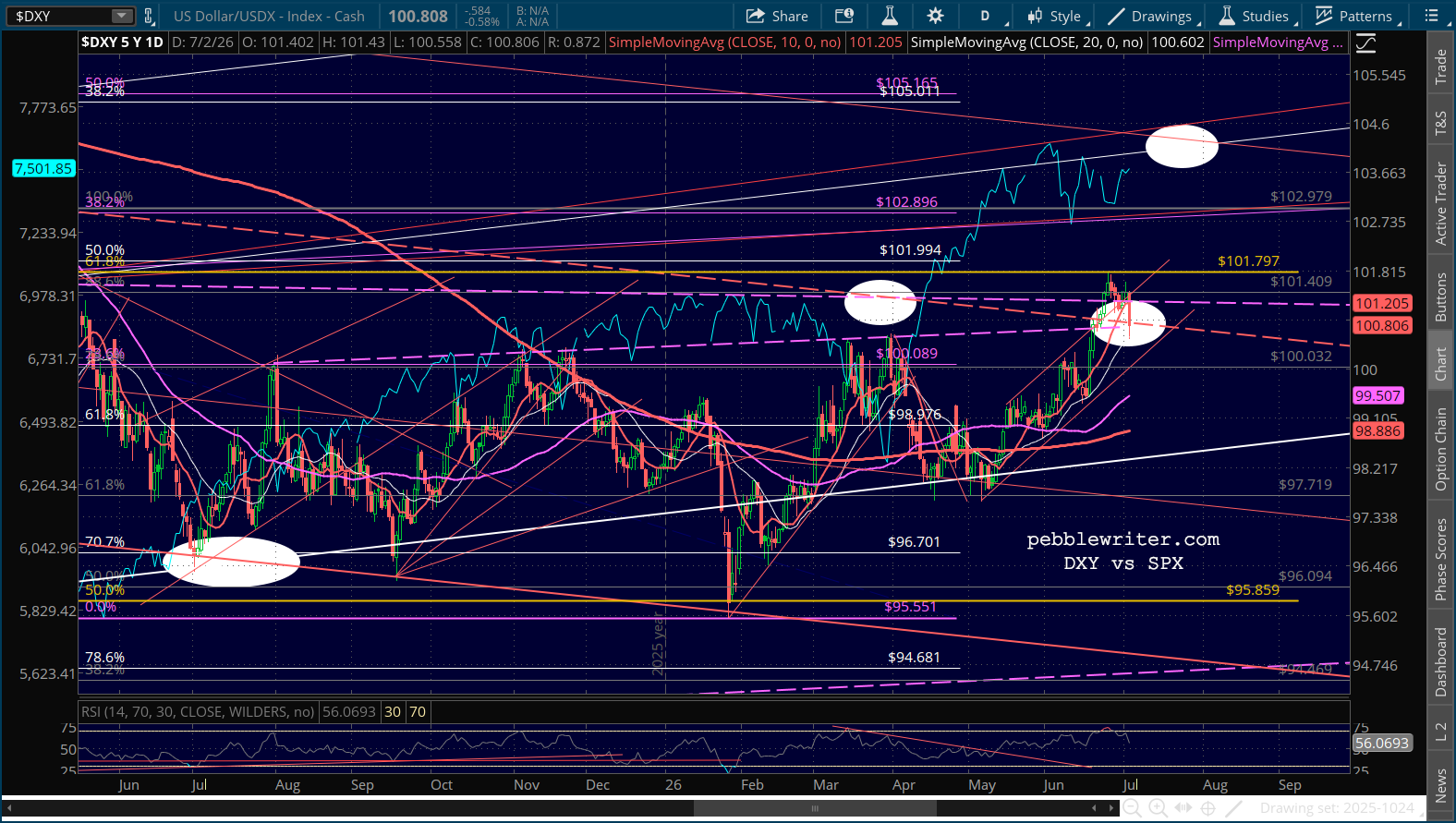

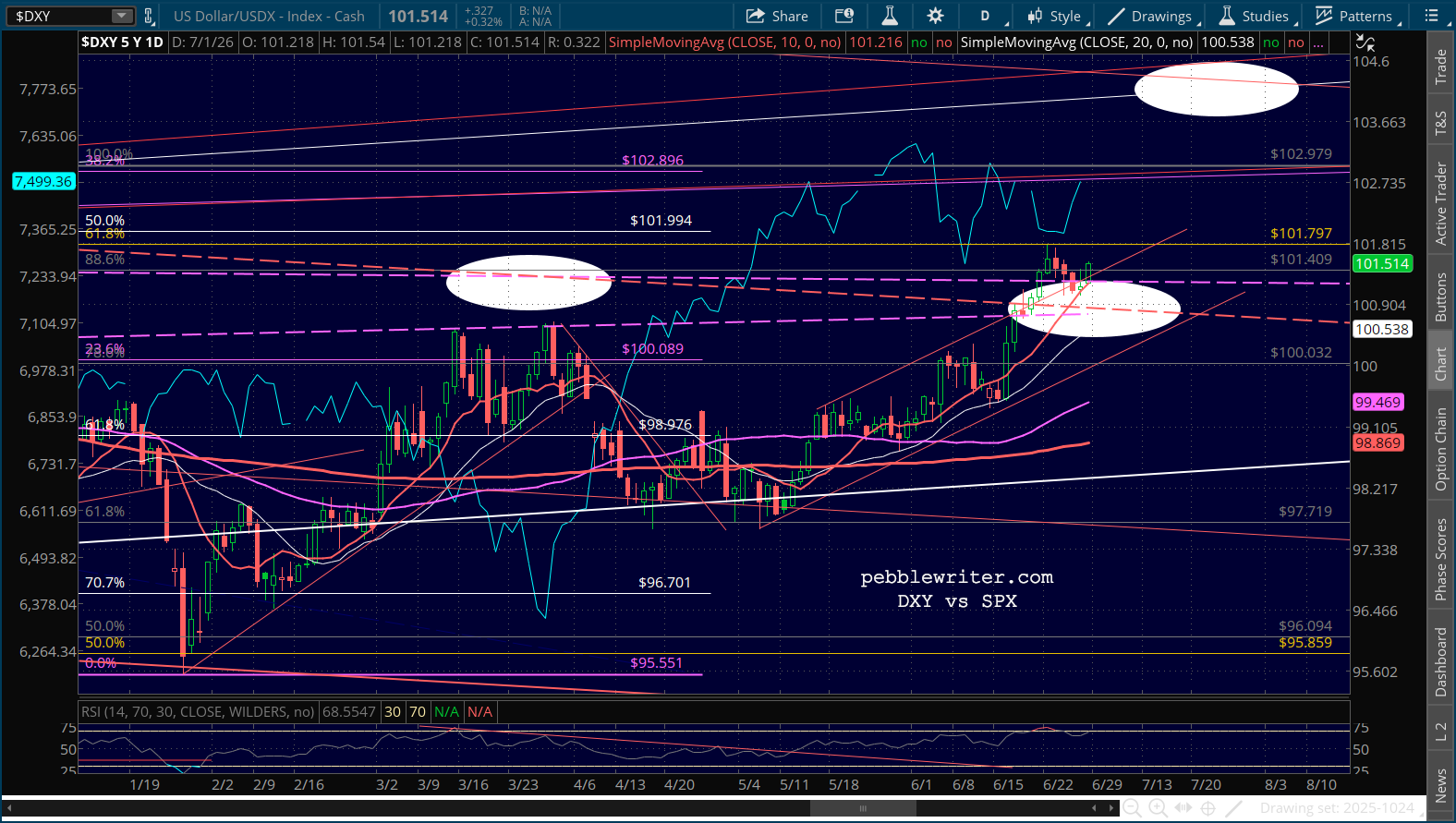

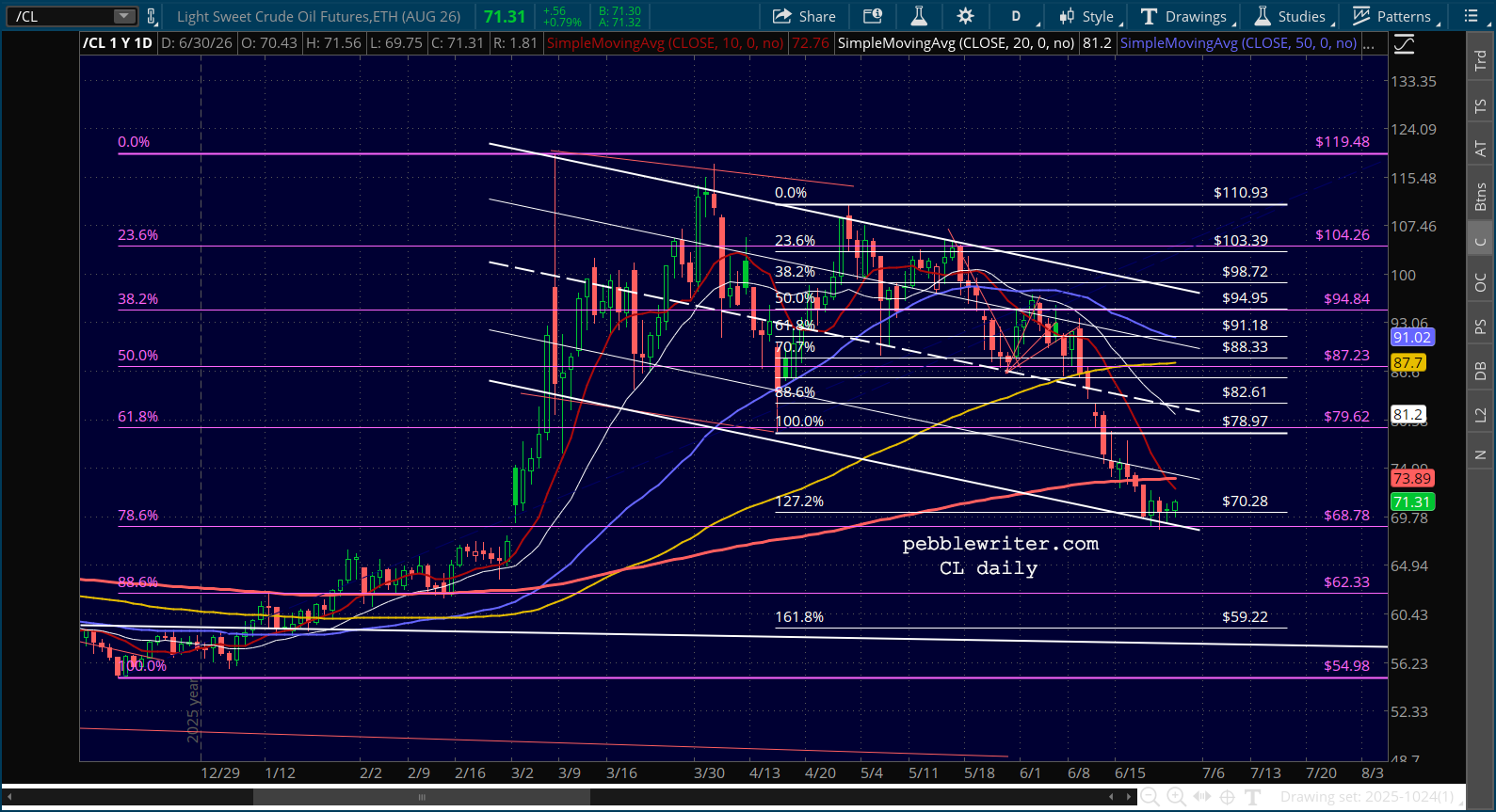

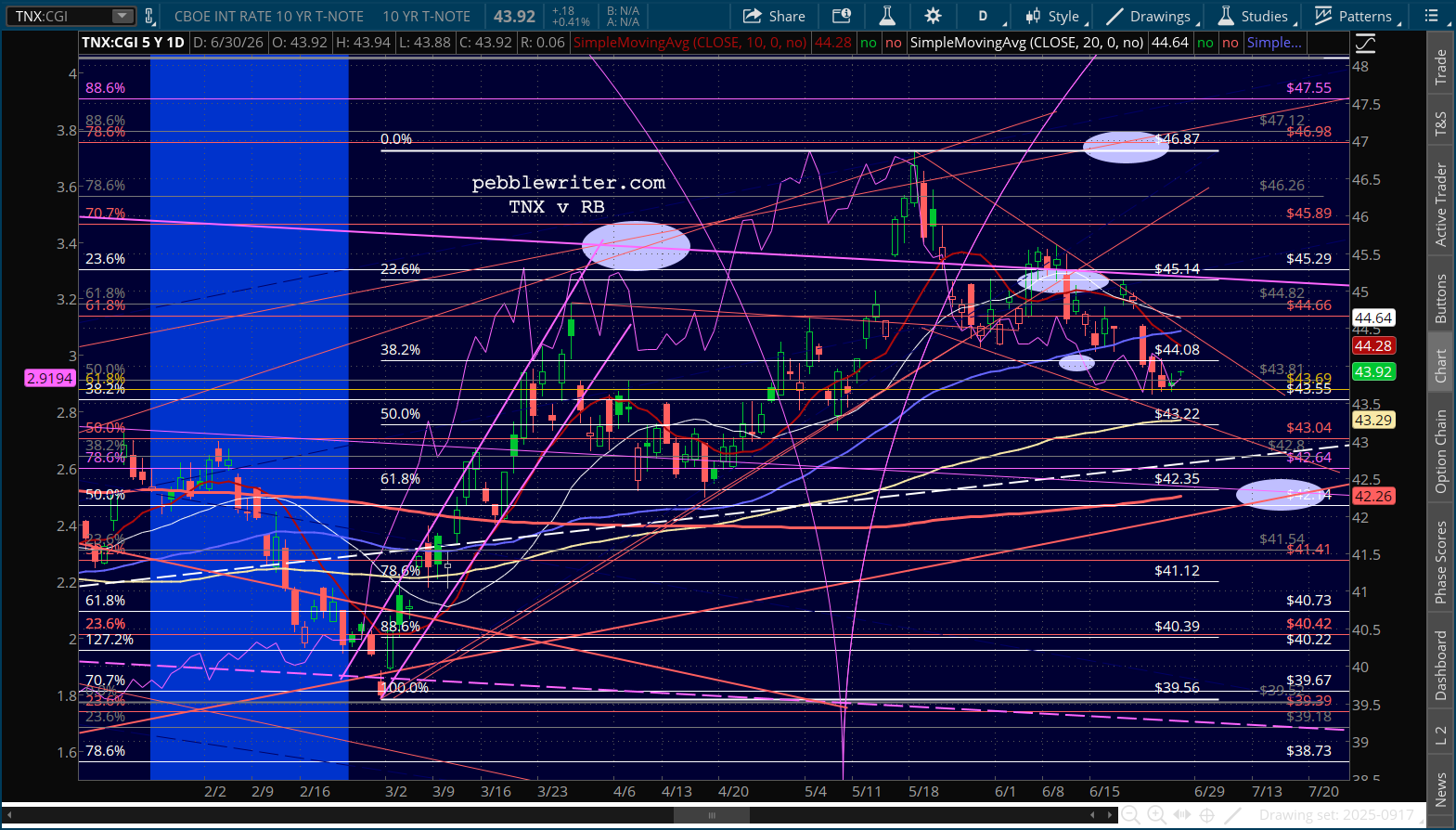

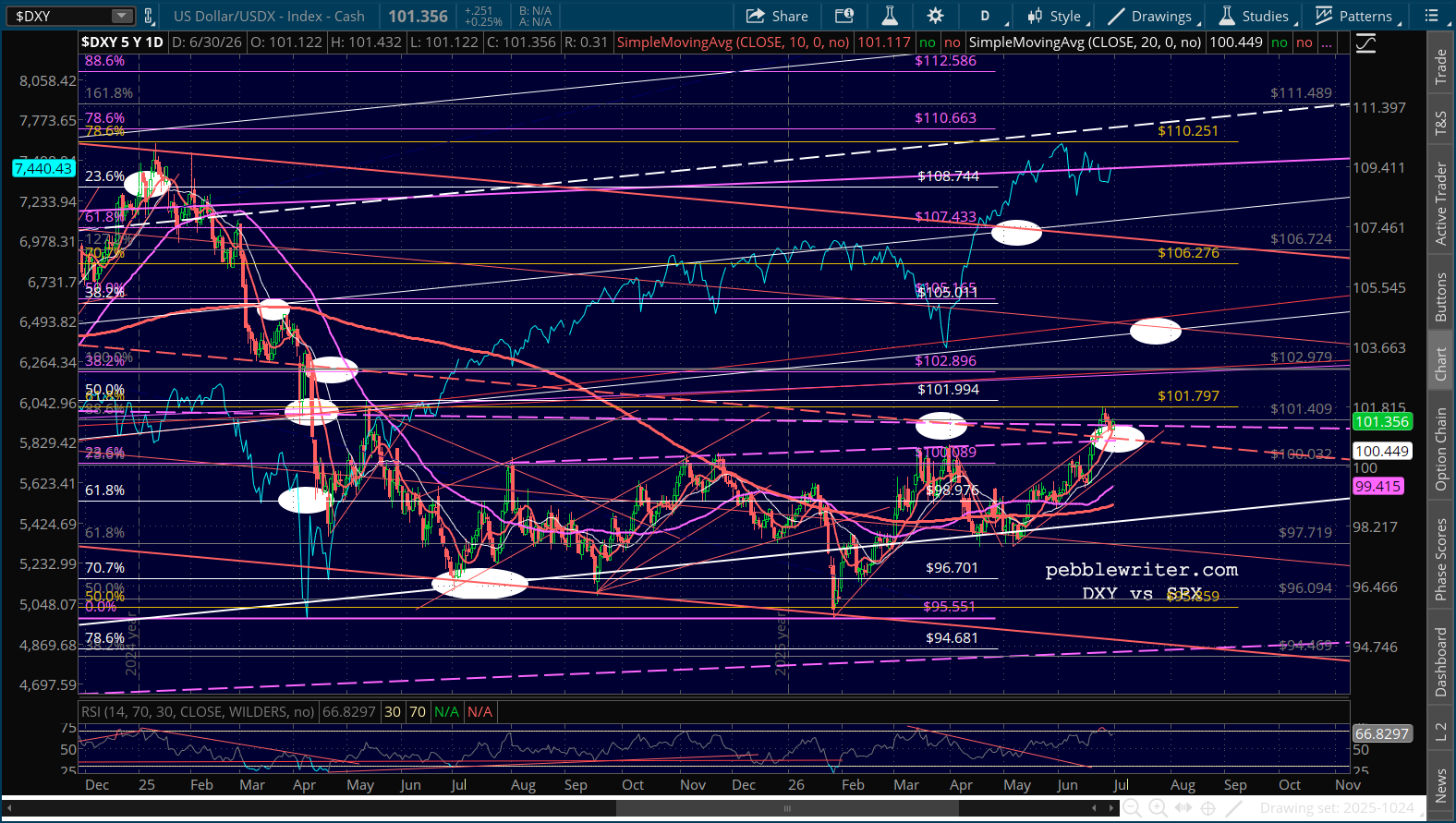

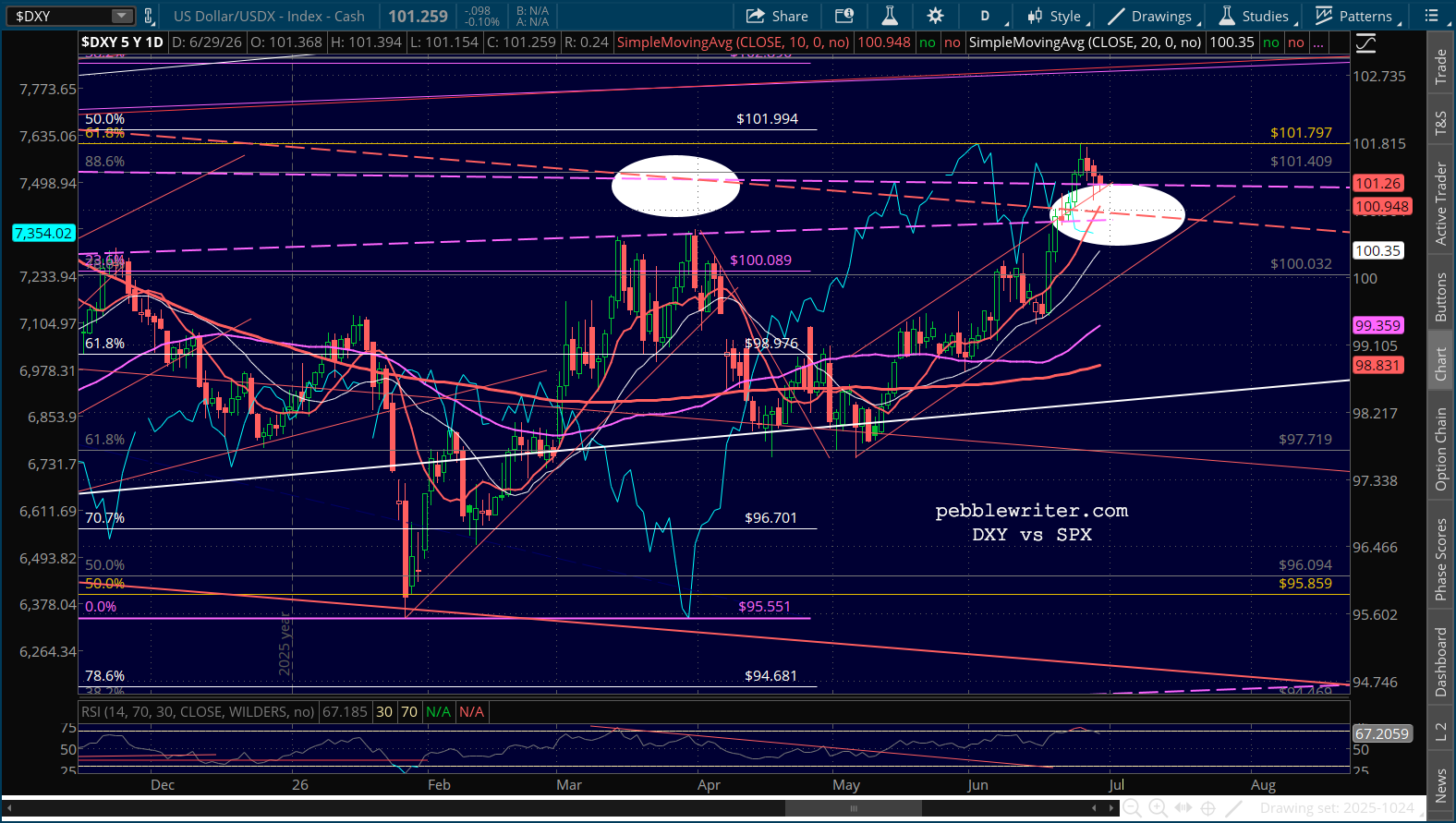

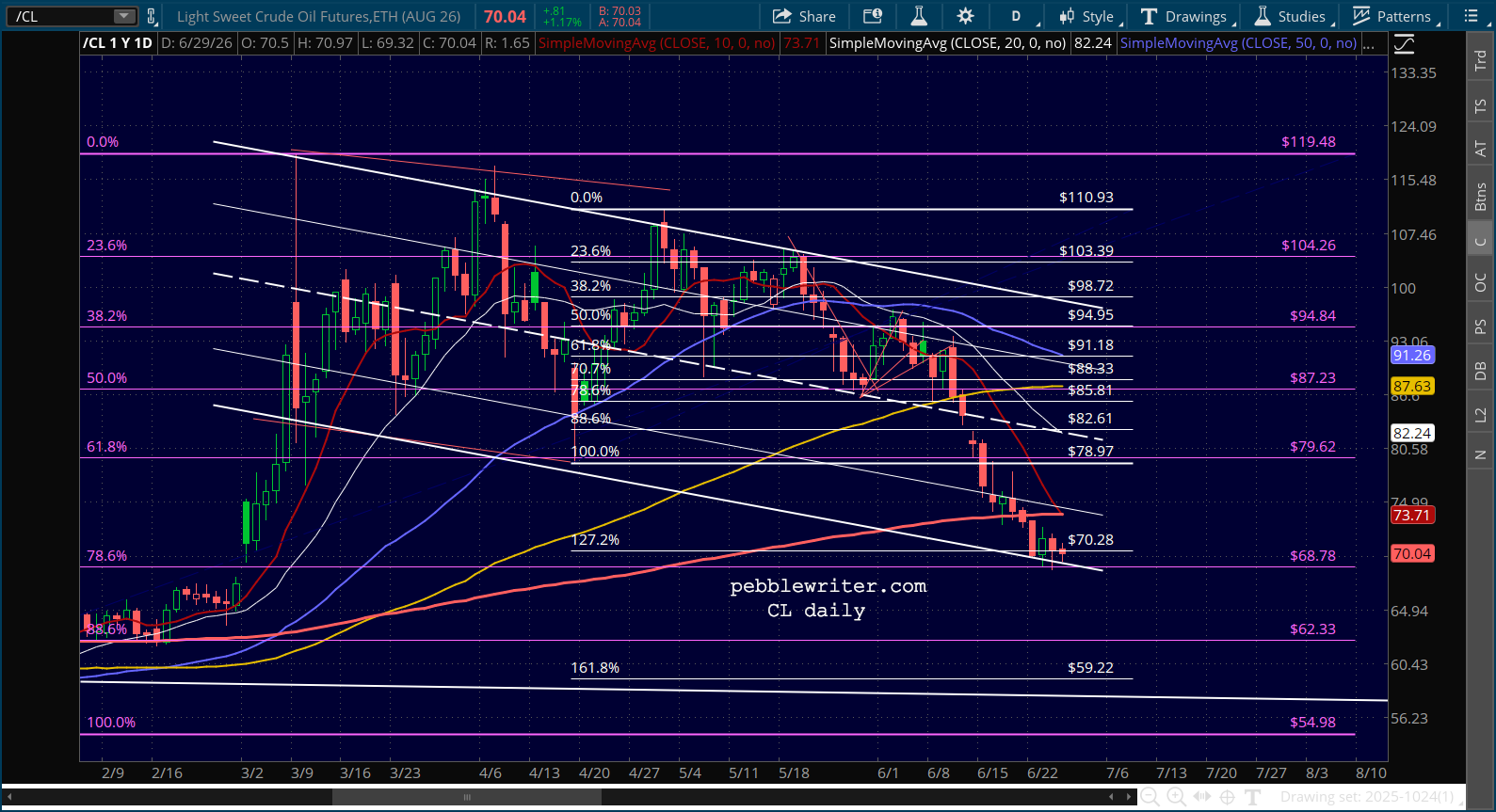

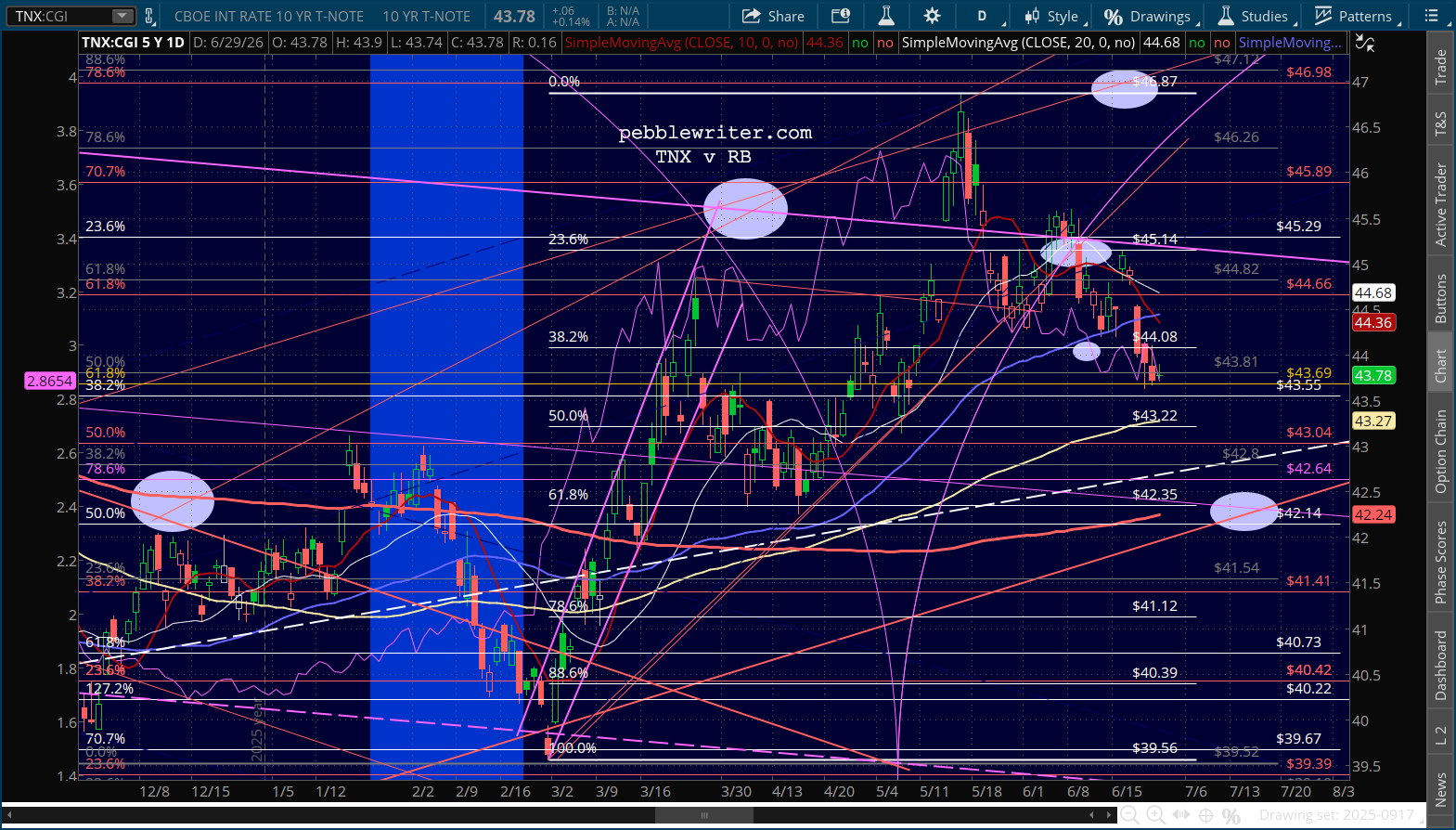

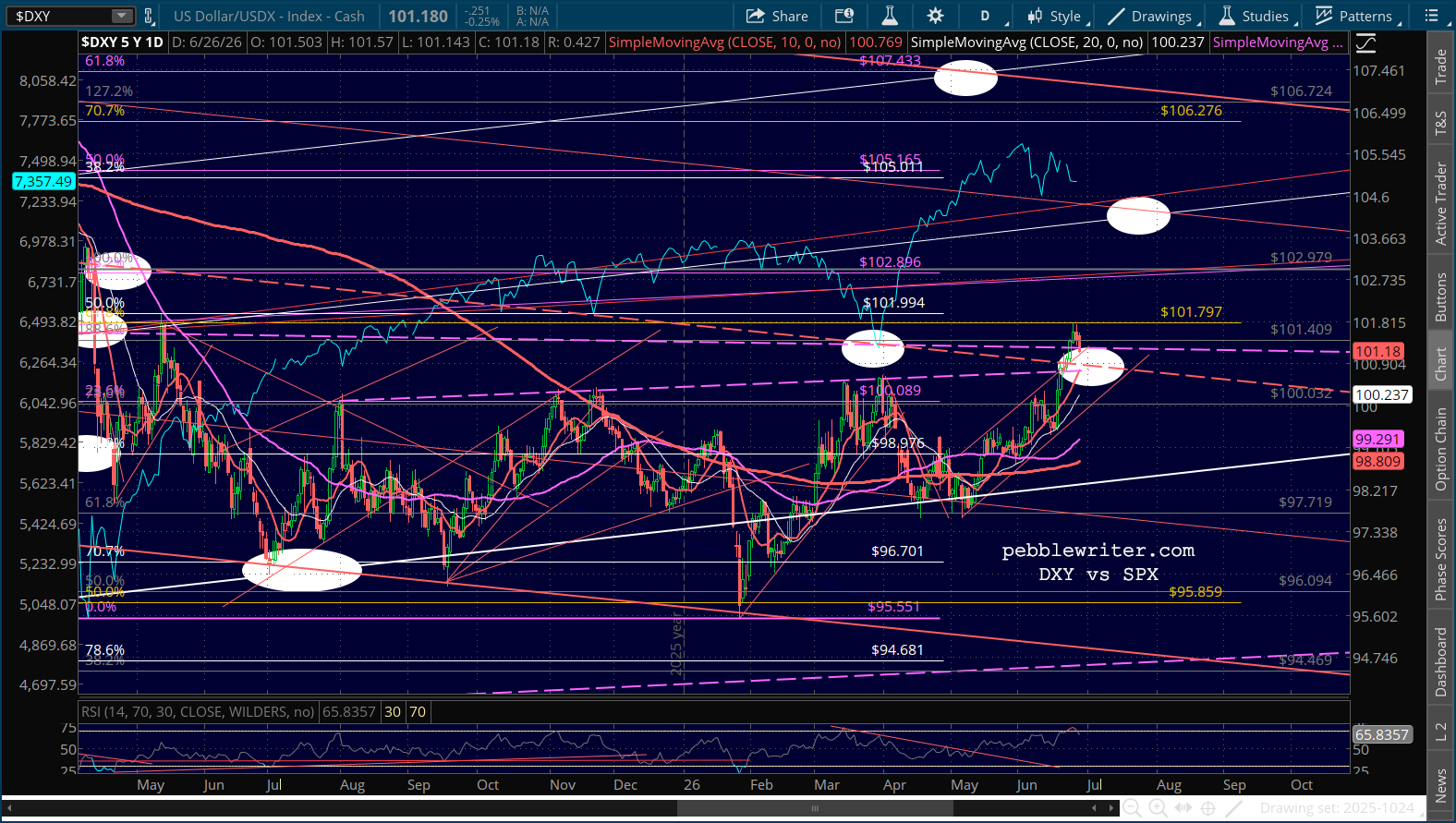

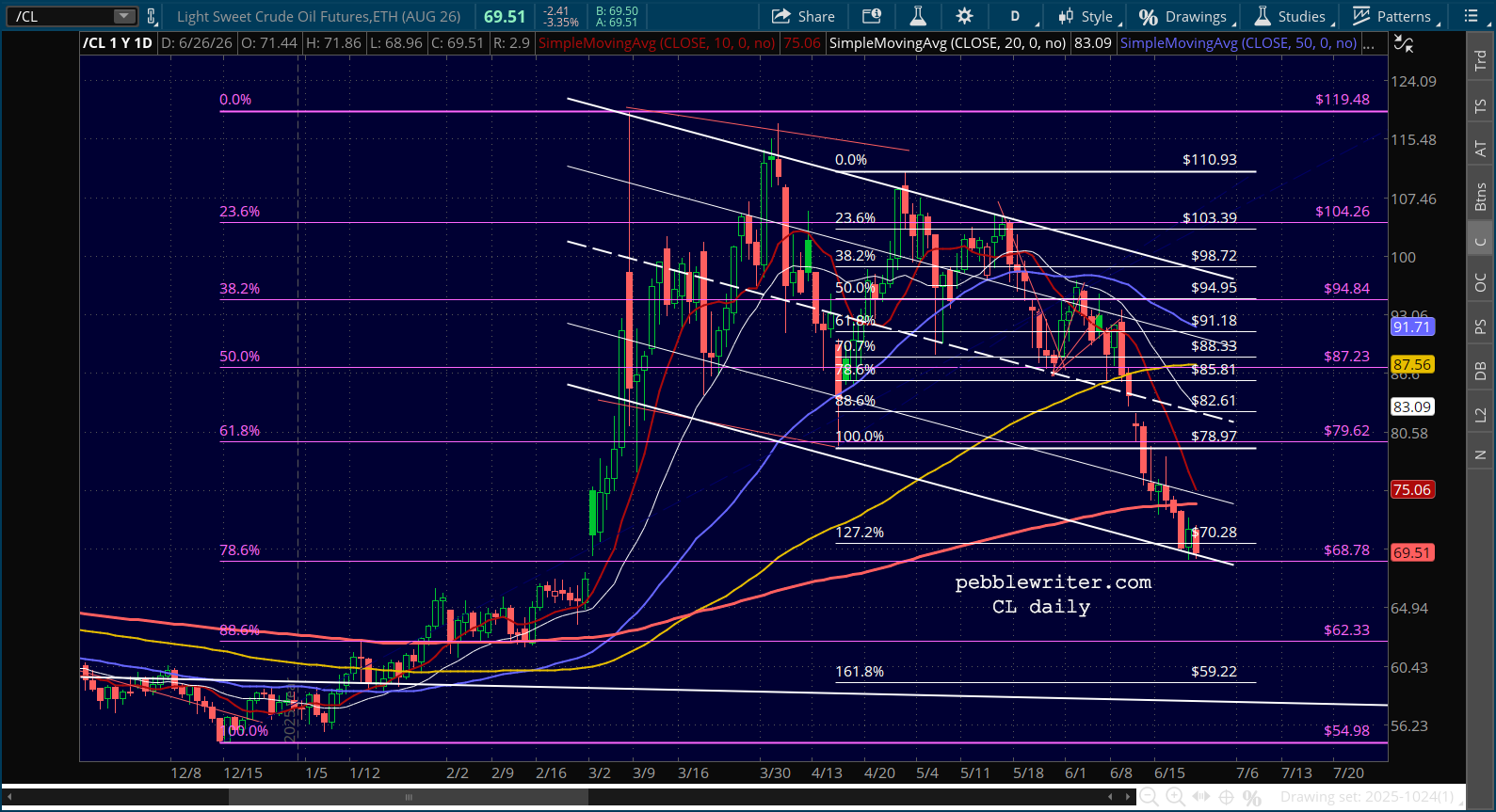

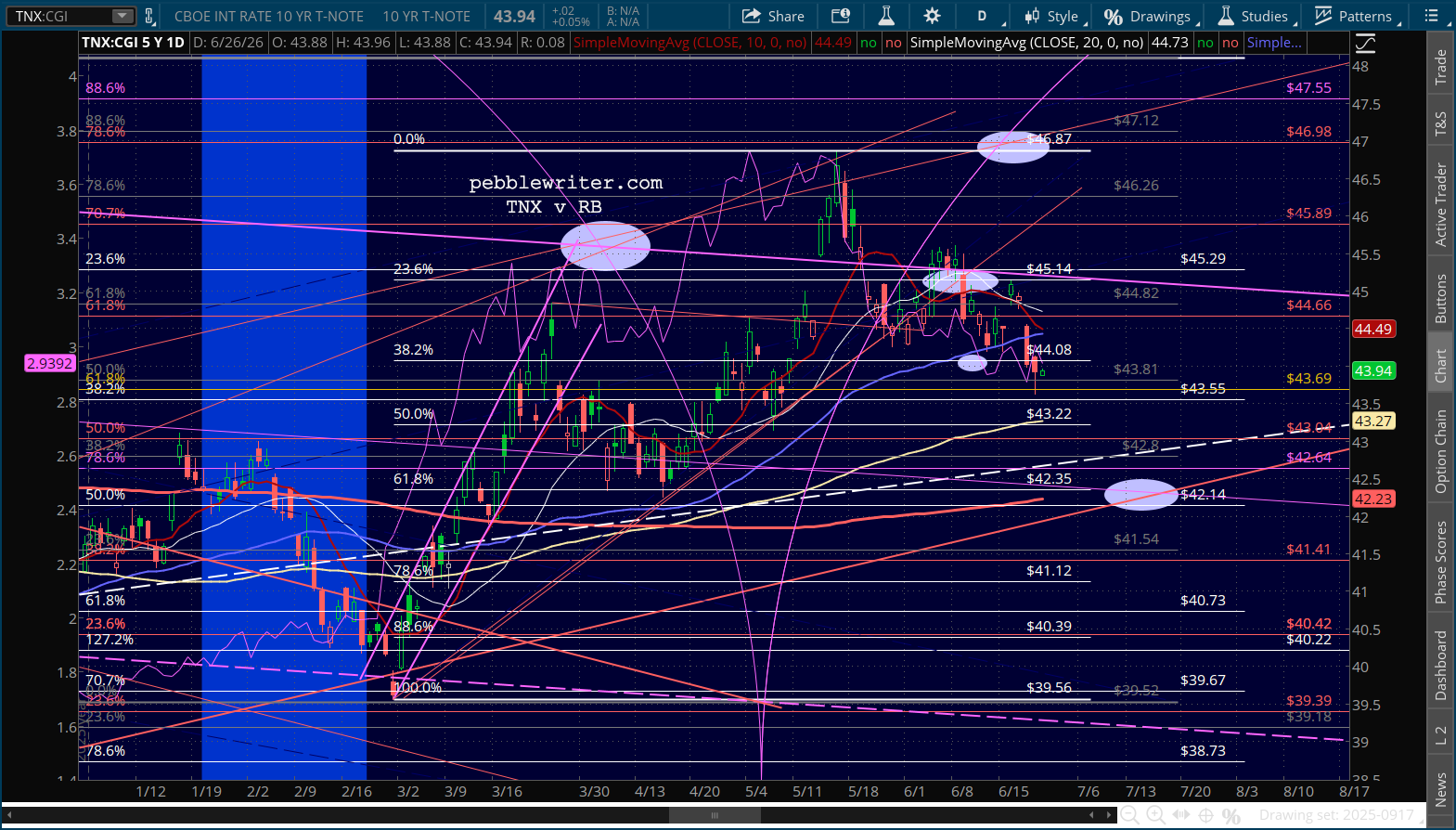

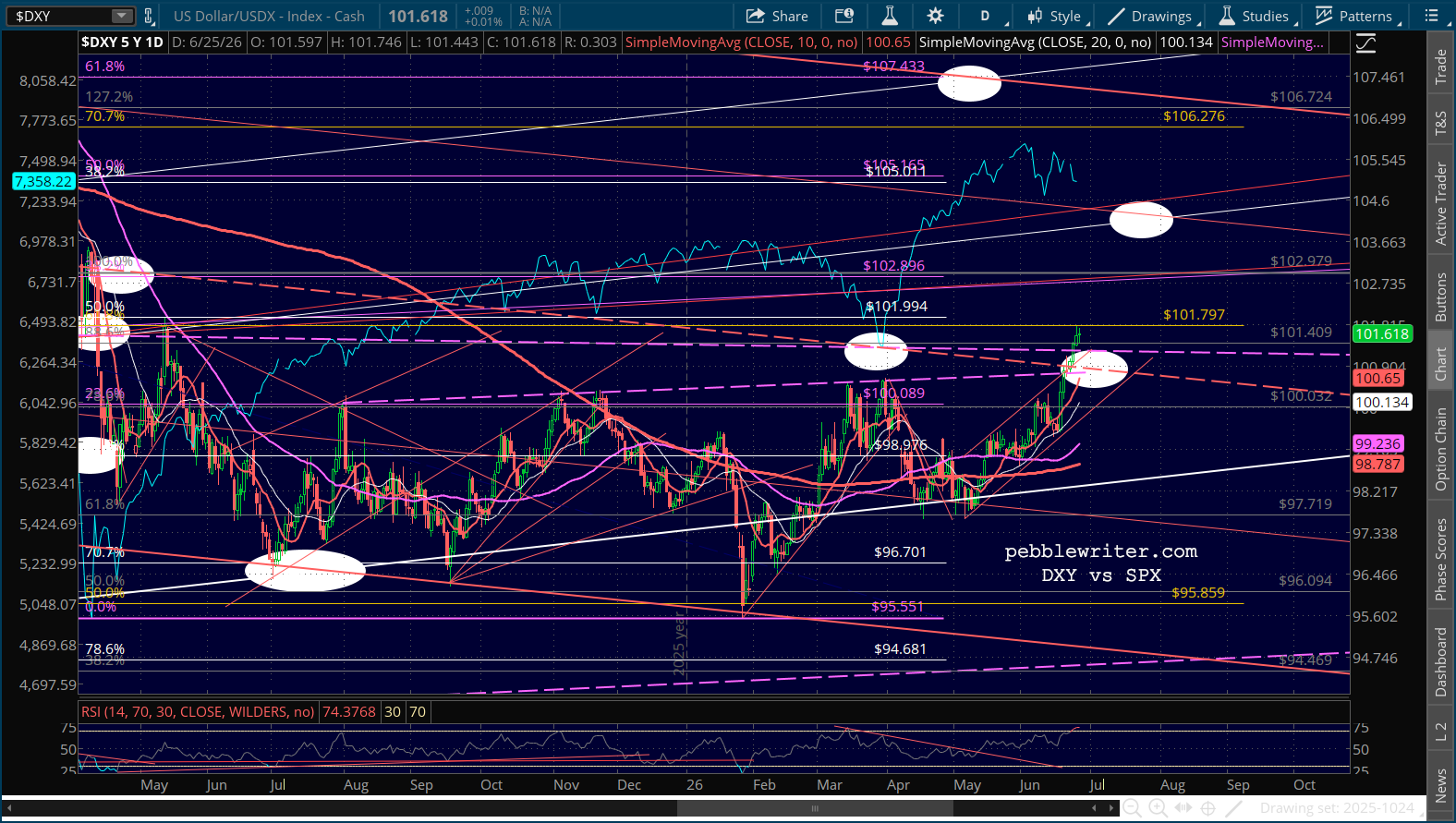

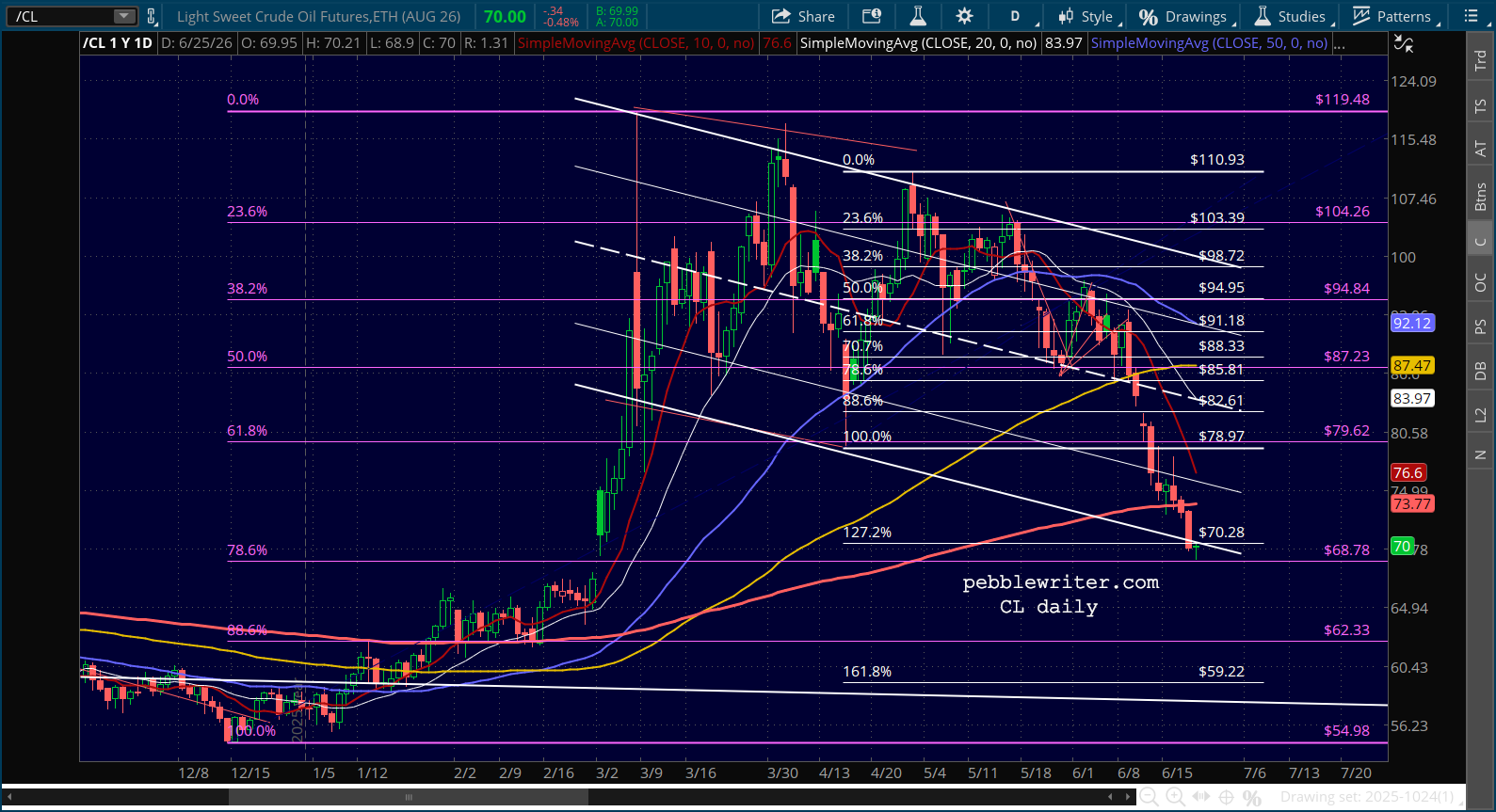

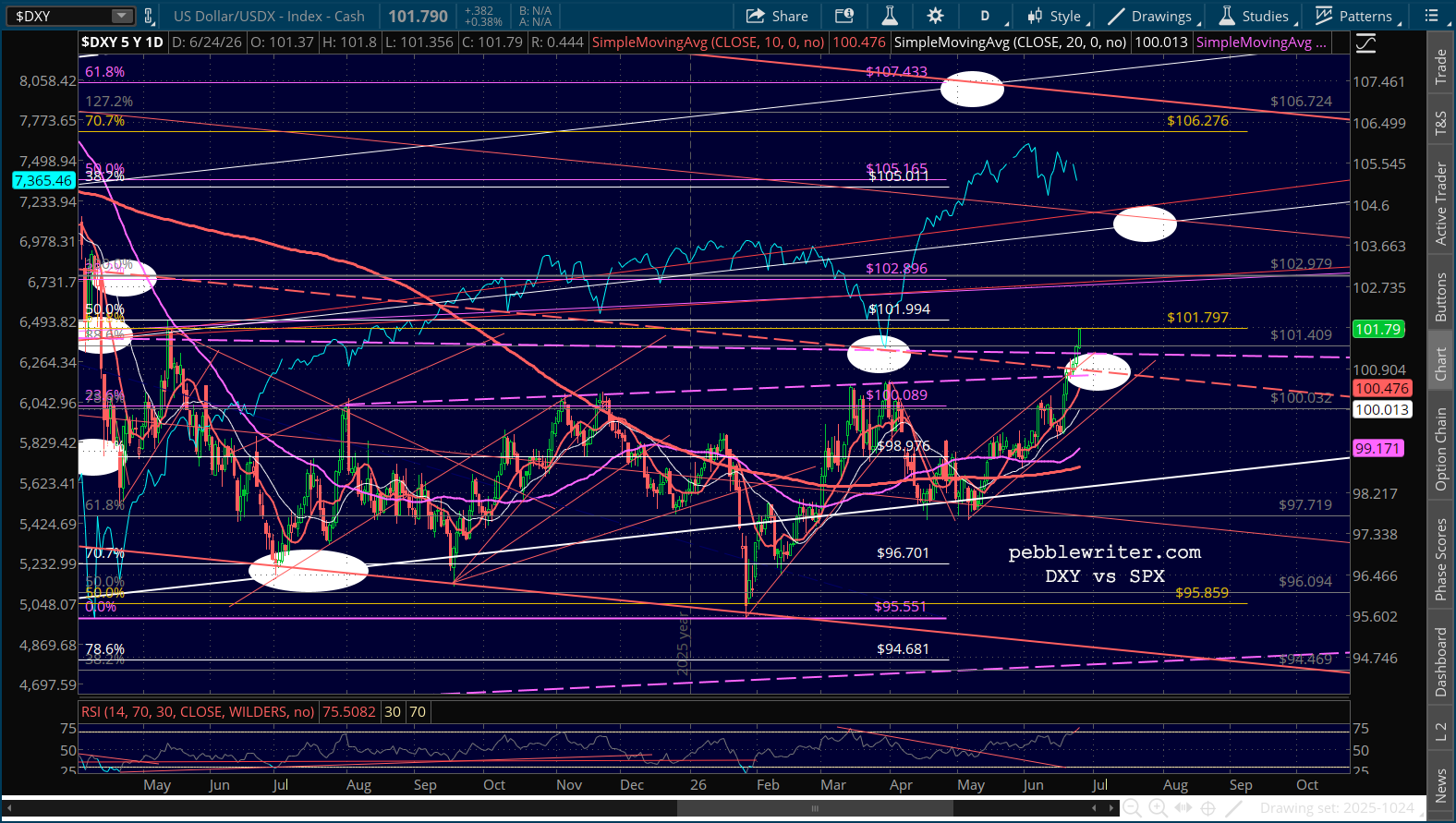

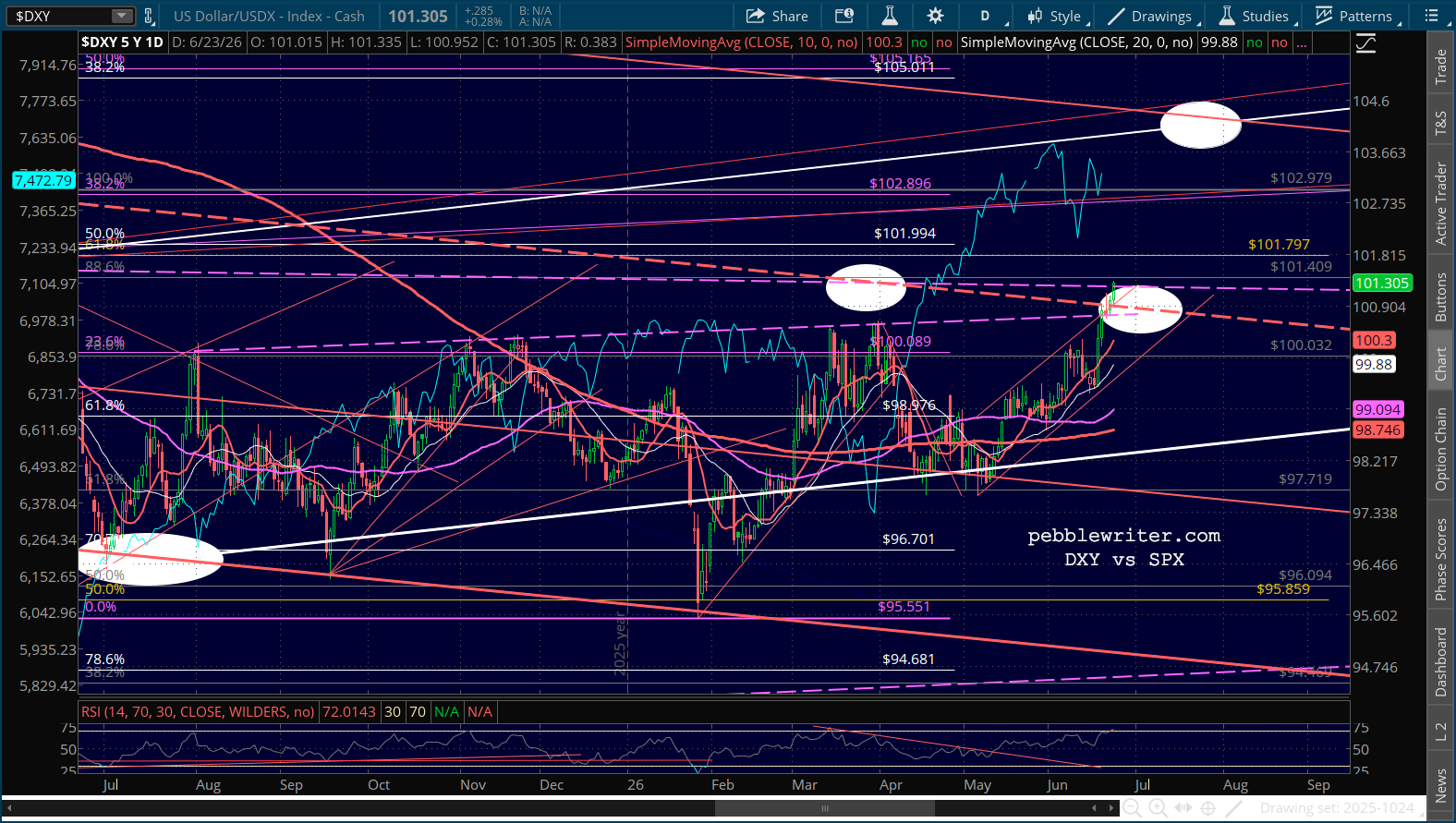

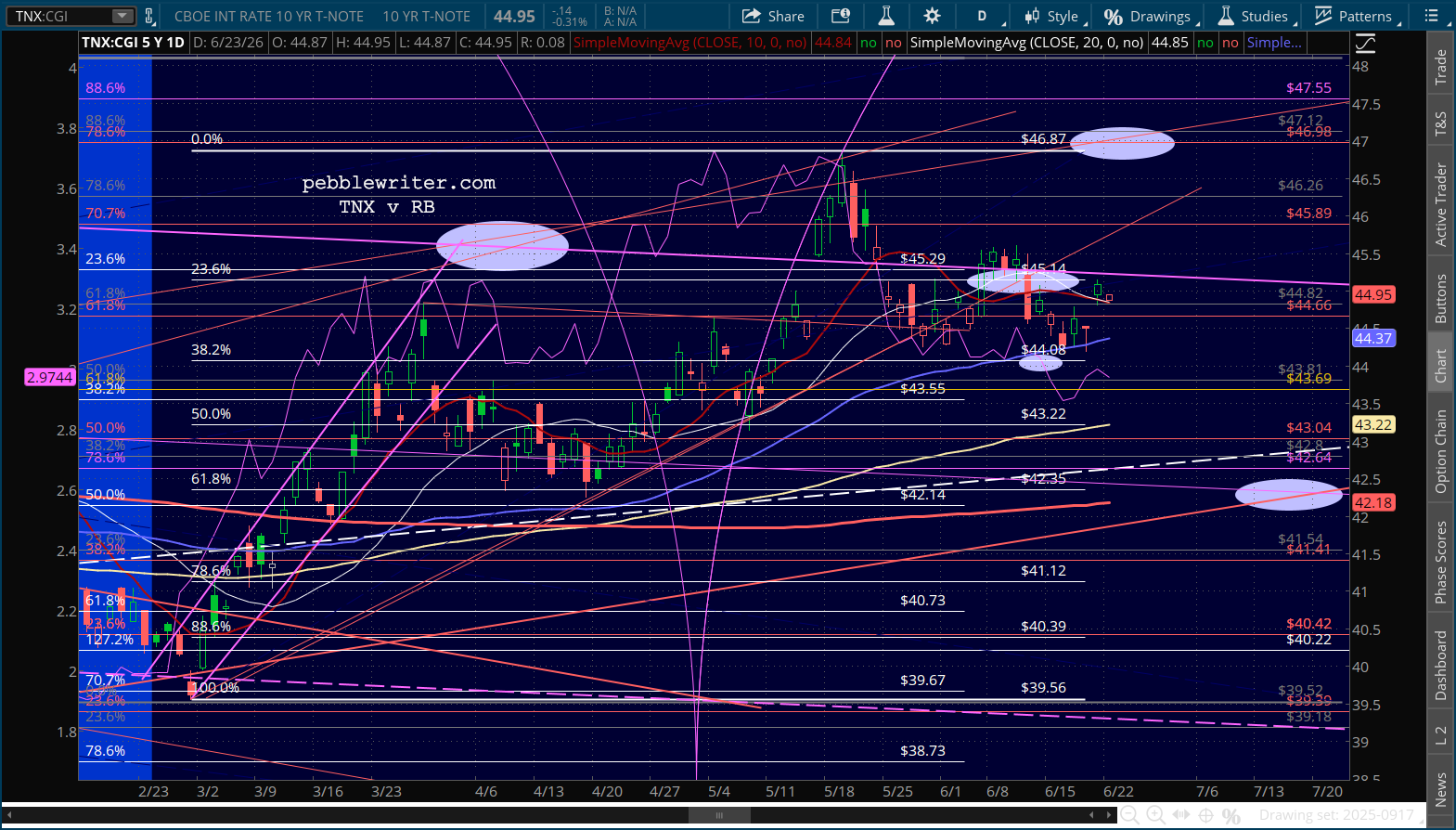

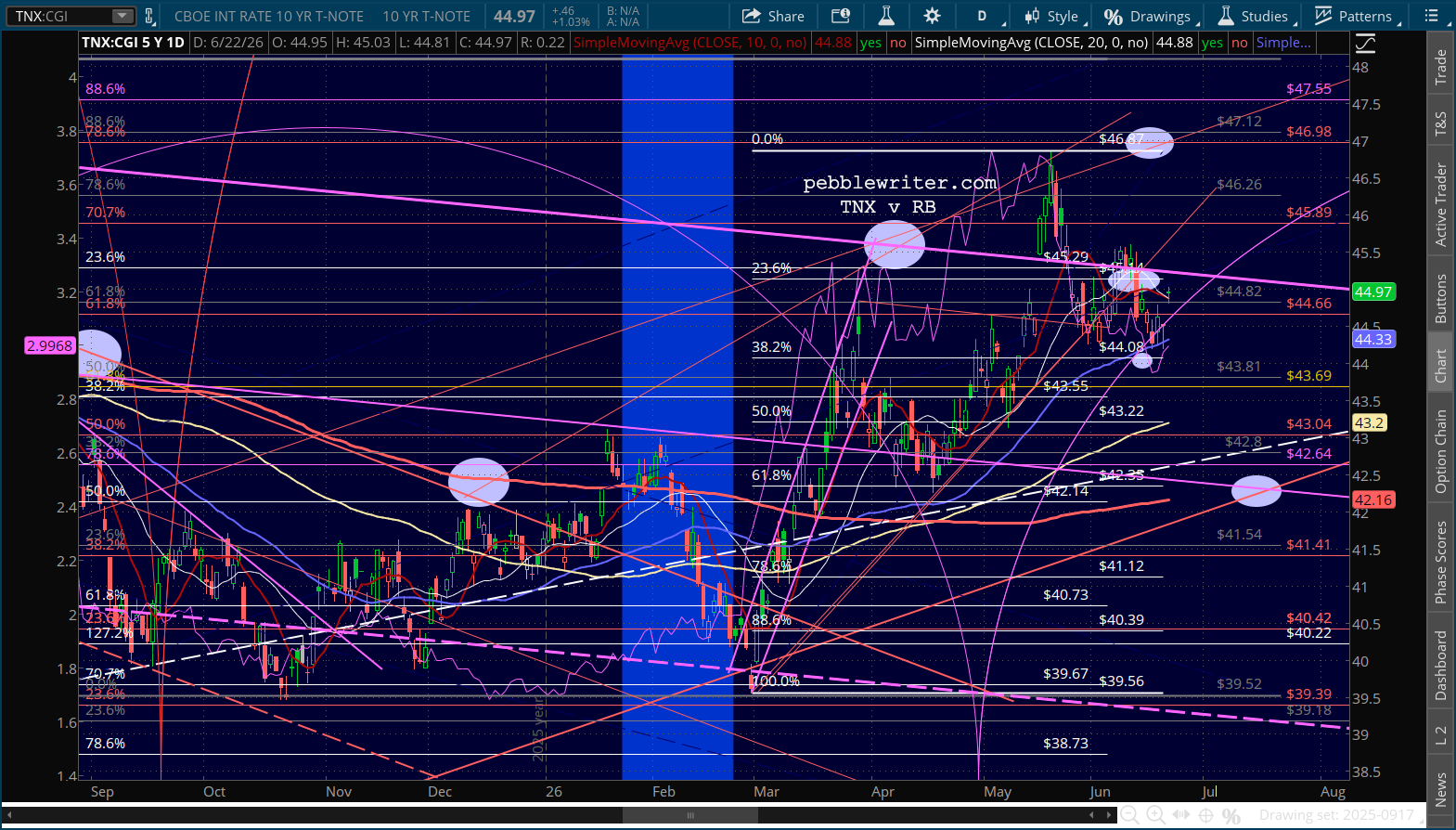

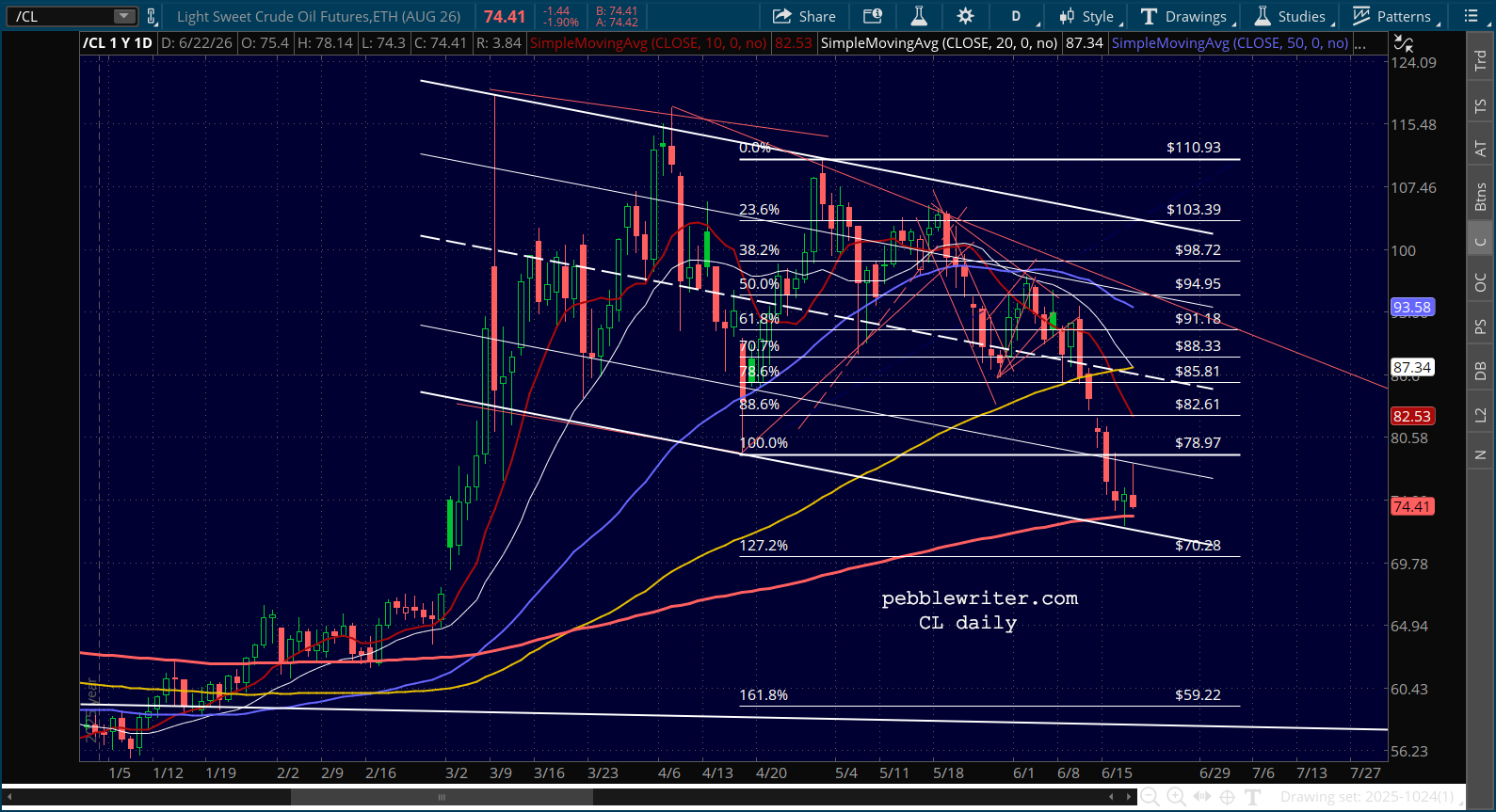

CL’s drop through the .786 at 68.78 helped the 10Y back off its breakout, which in turn reversed DXY’s breakout. The level to watch is 100.77.

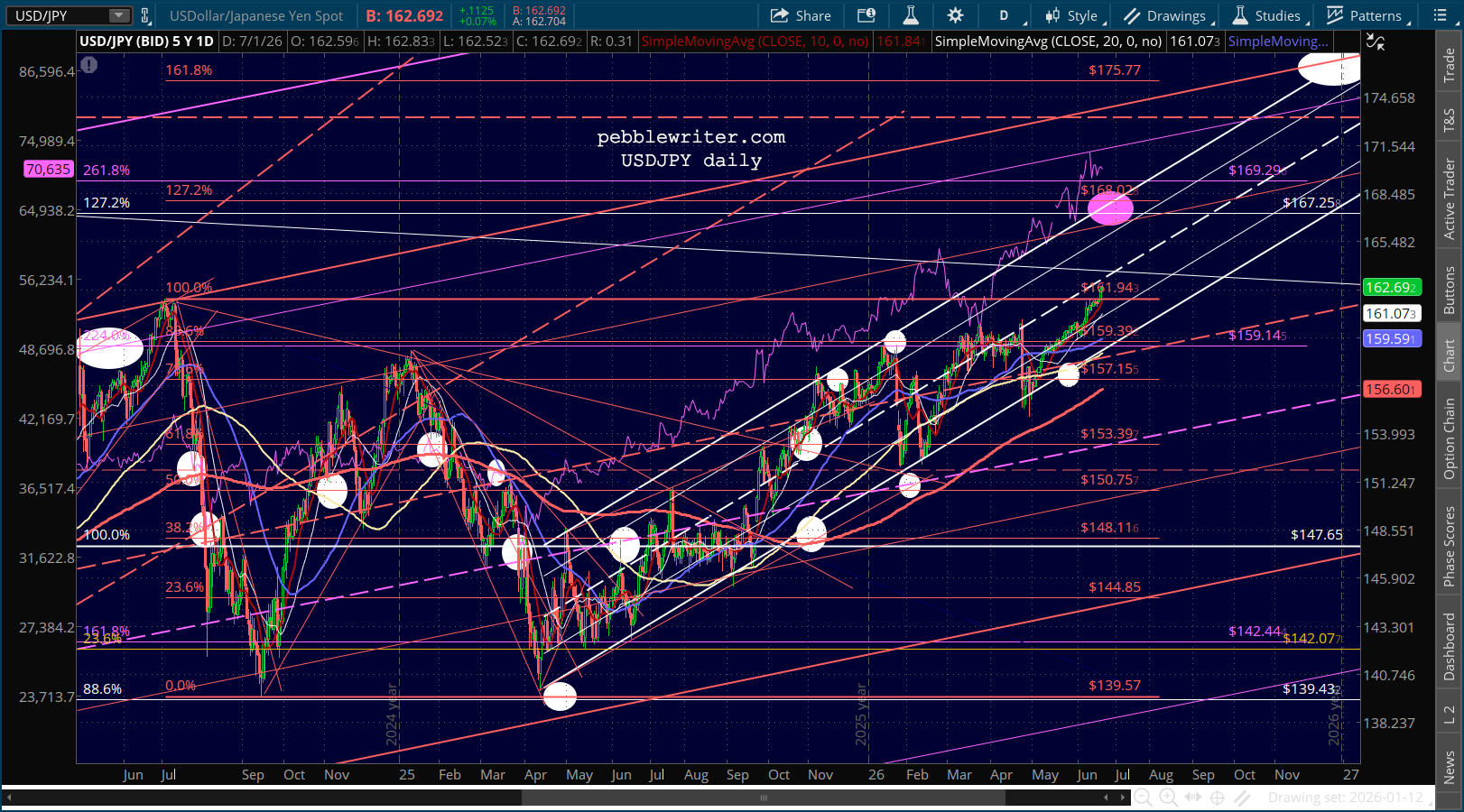

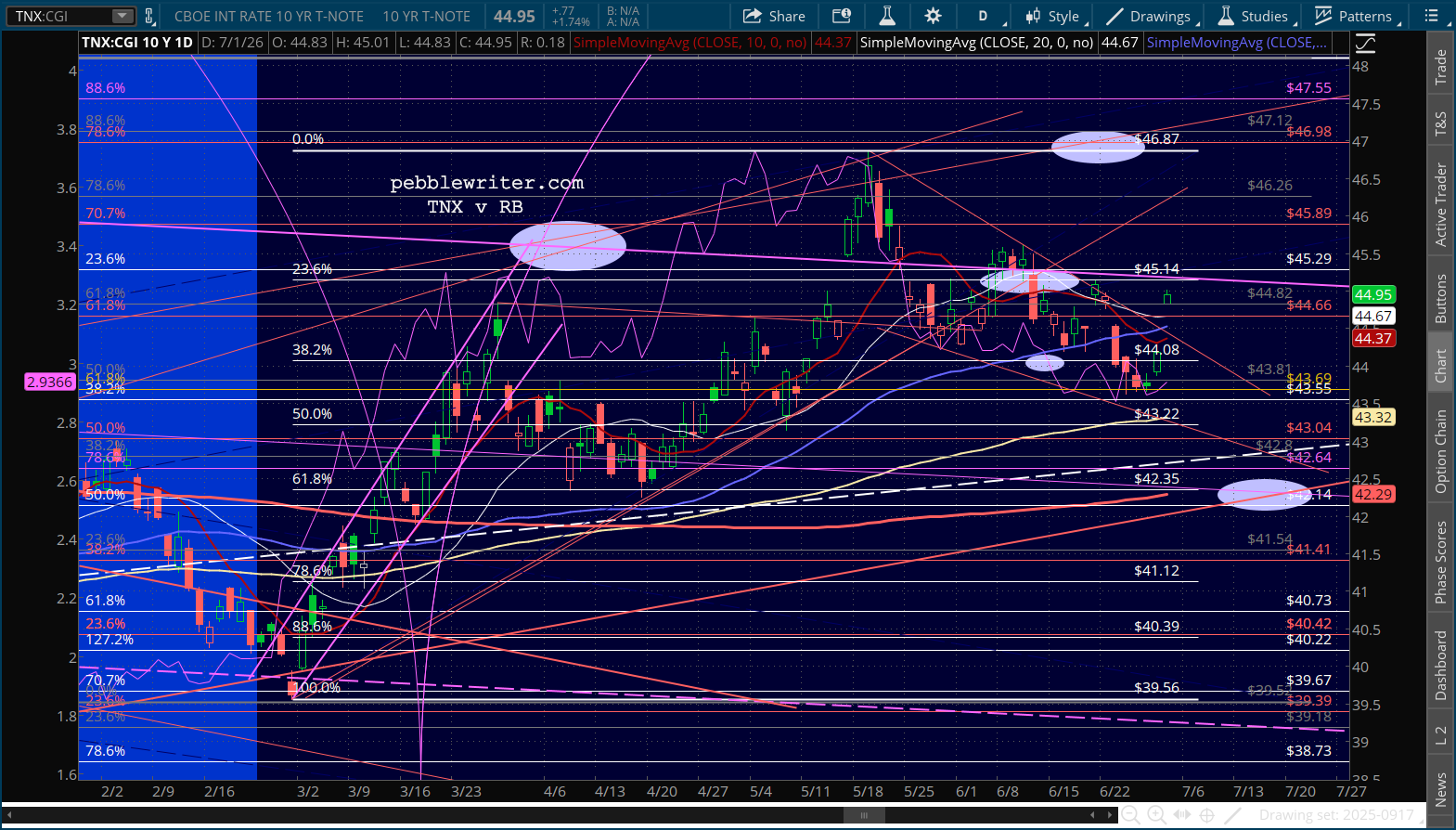

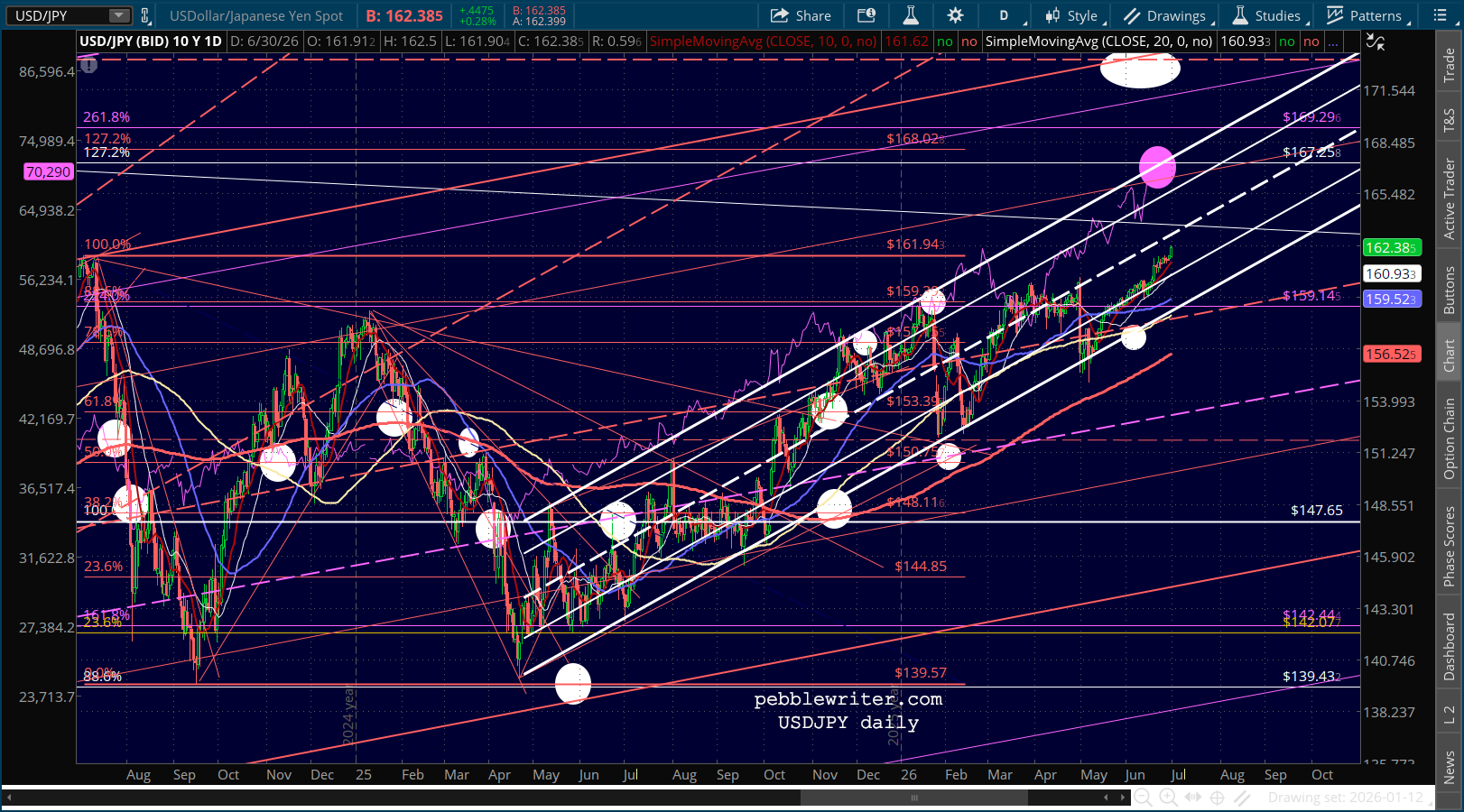

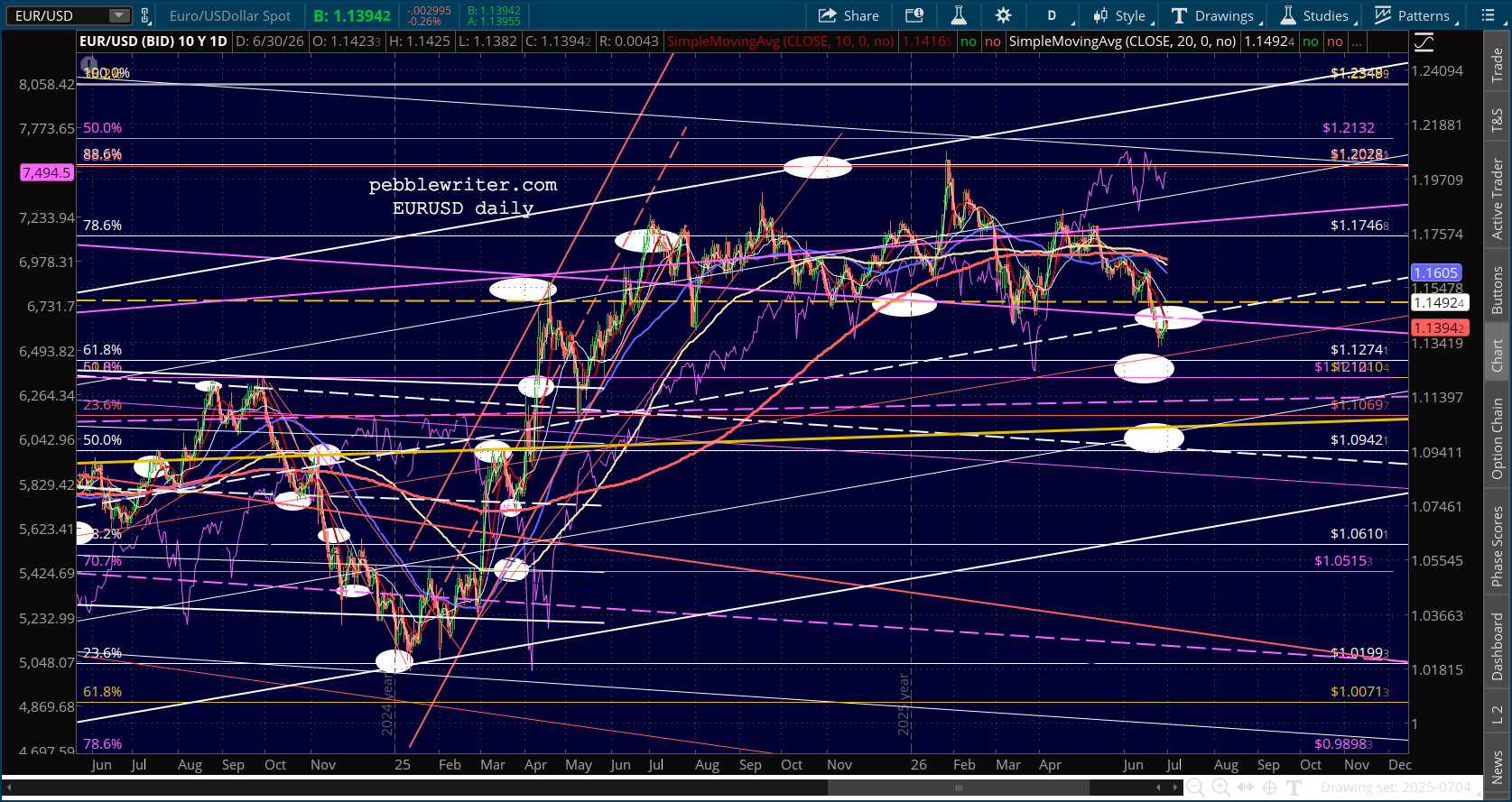

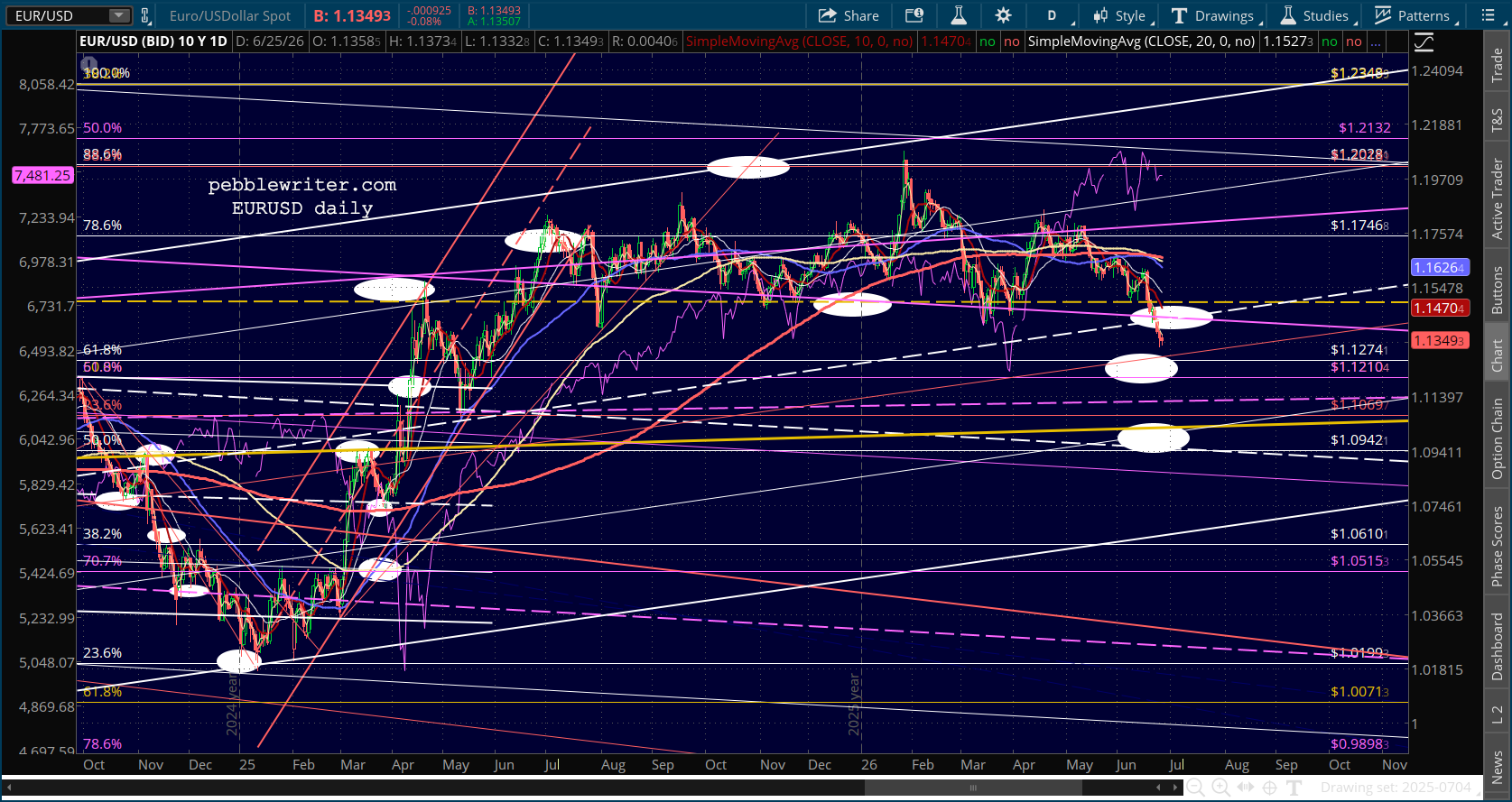

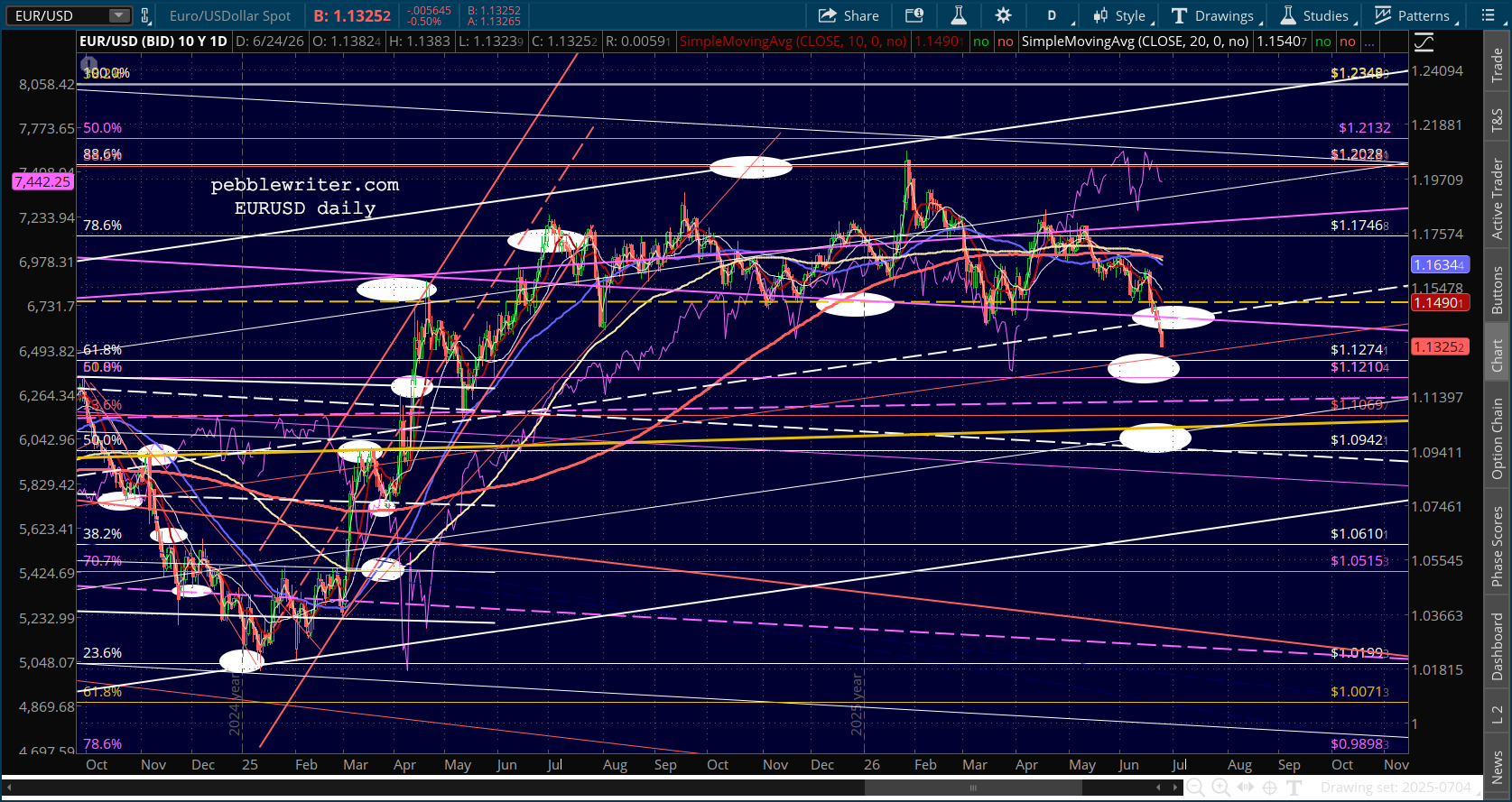

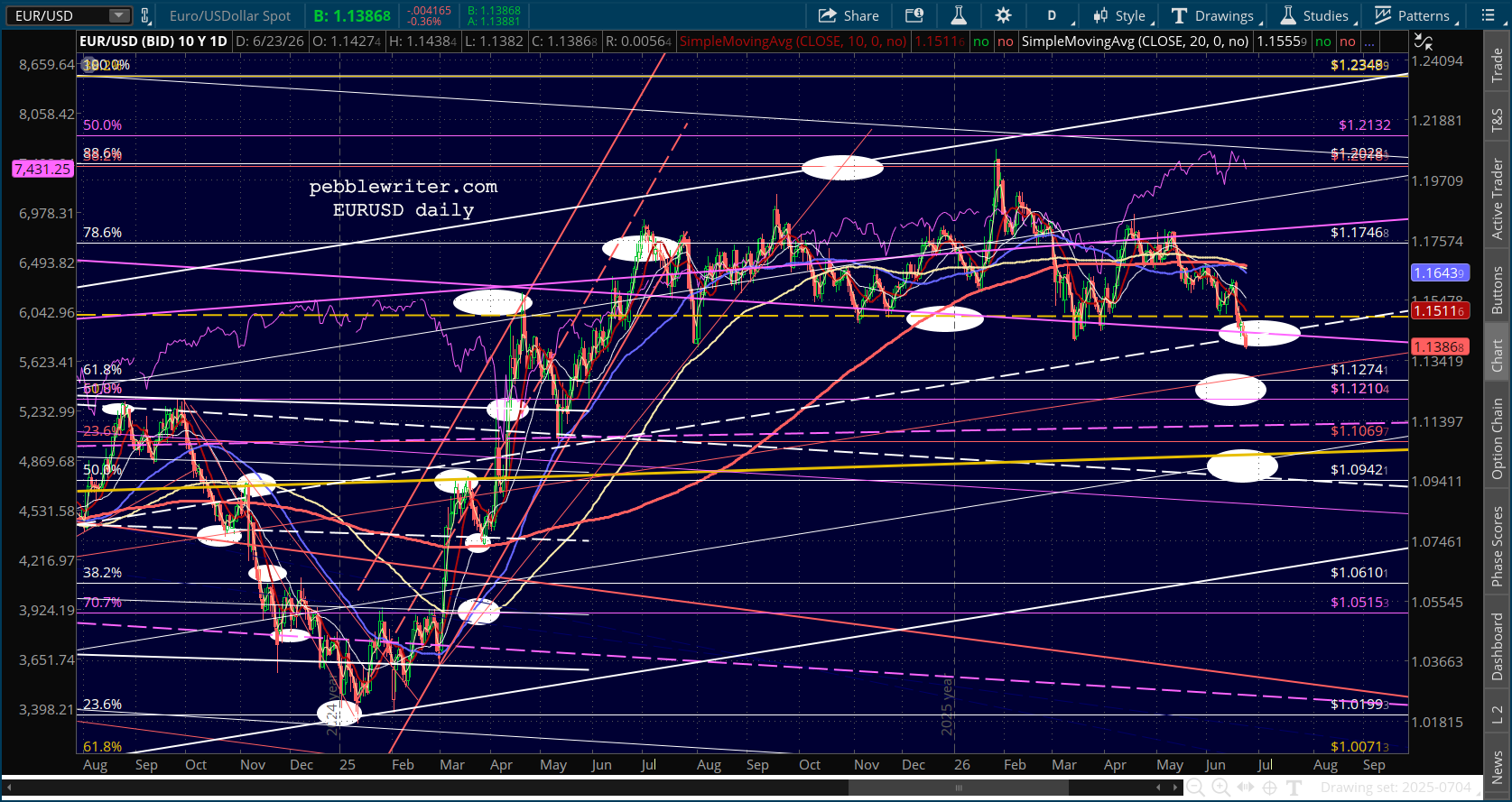

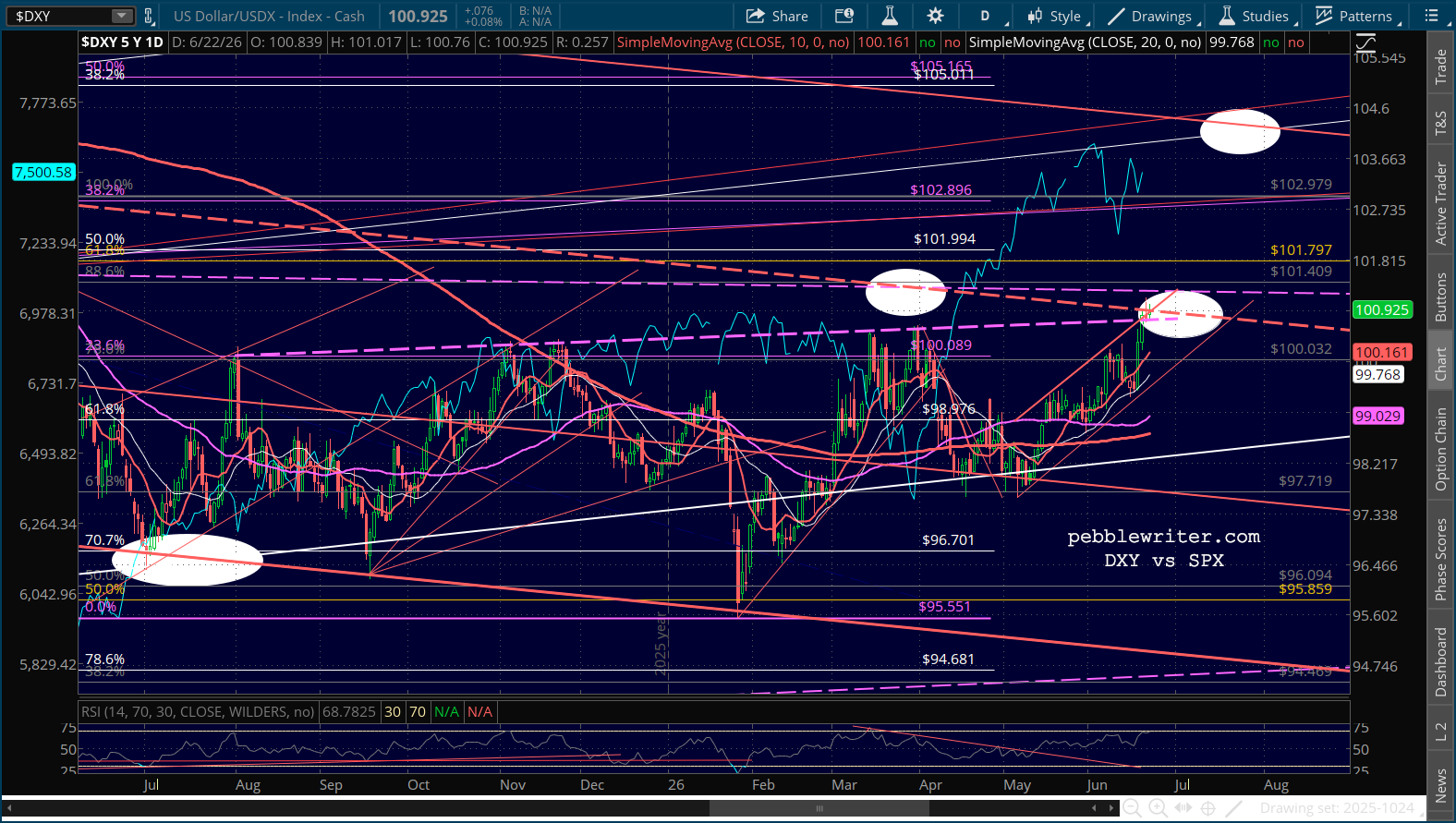

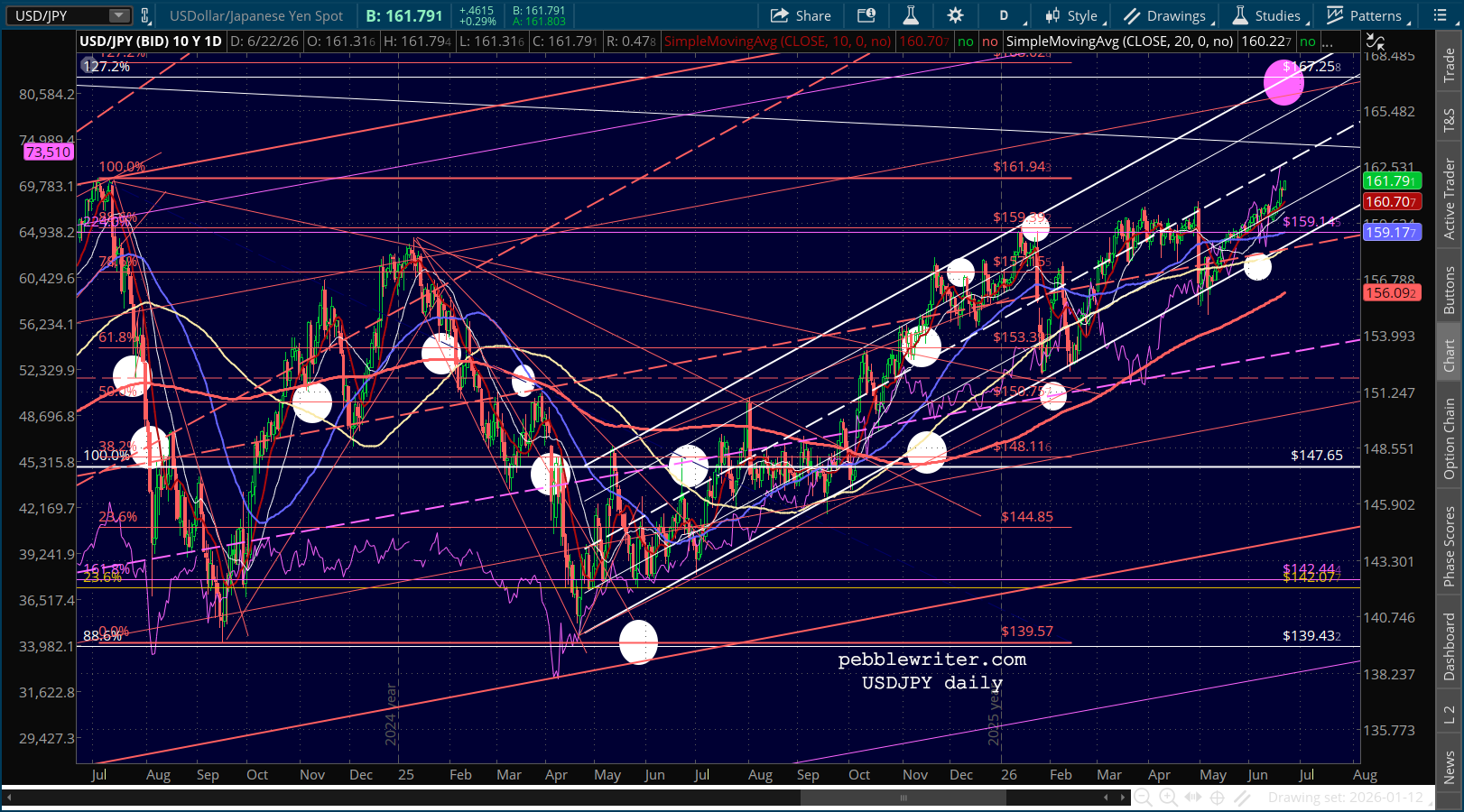

Futures are off moderately as Q3 kicks off. Currencies are taking center stage, with USDJPY making new highs and EURUSD breaking down. Don’t look now, but the 10Y just broke out.

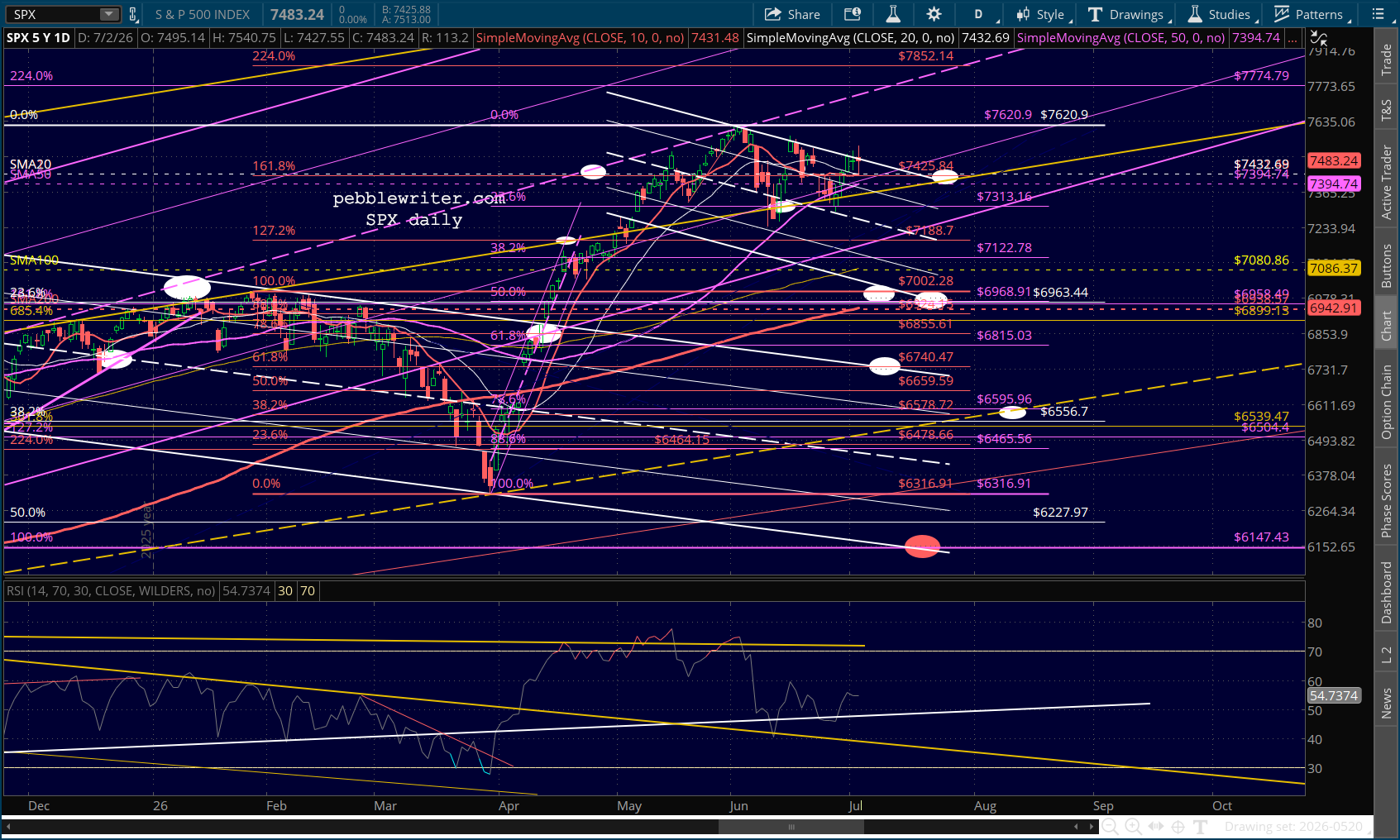

Futures are flat as we wrap the 2nd quarter. I’m not sure there’s a better descriptor than “irrational exuberance.” But, we’ll find out if, as I expect, we begin to backtest some of the previous tops and SMA200s over the next week or two.

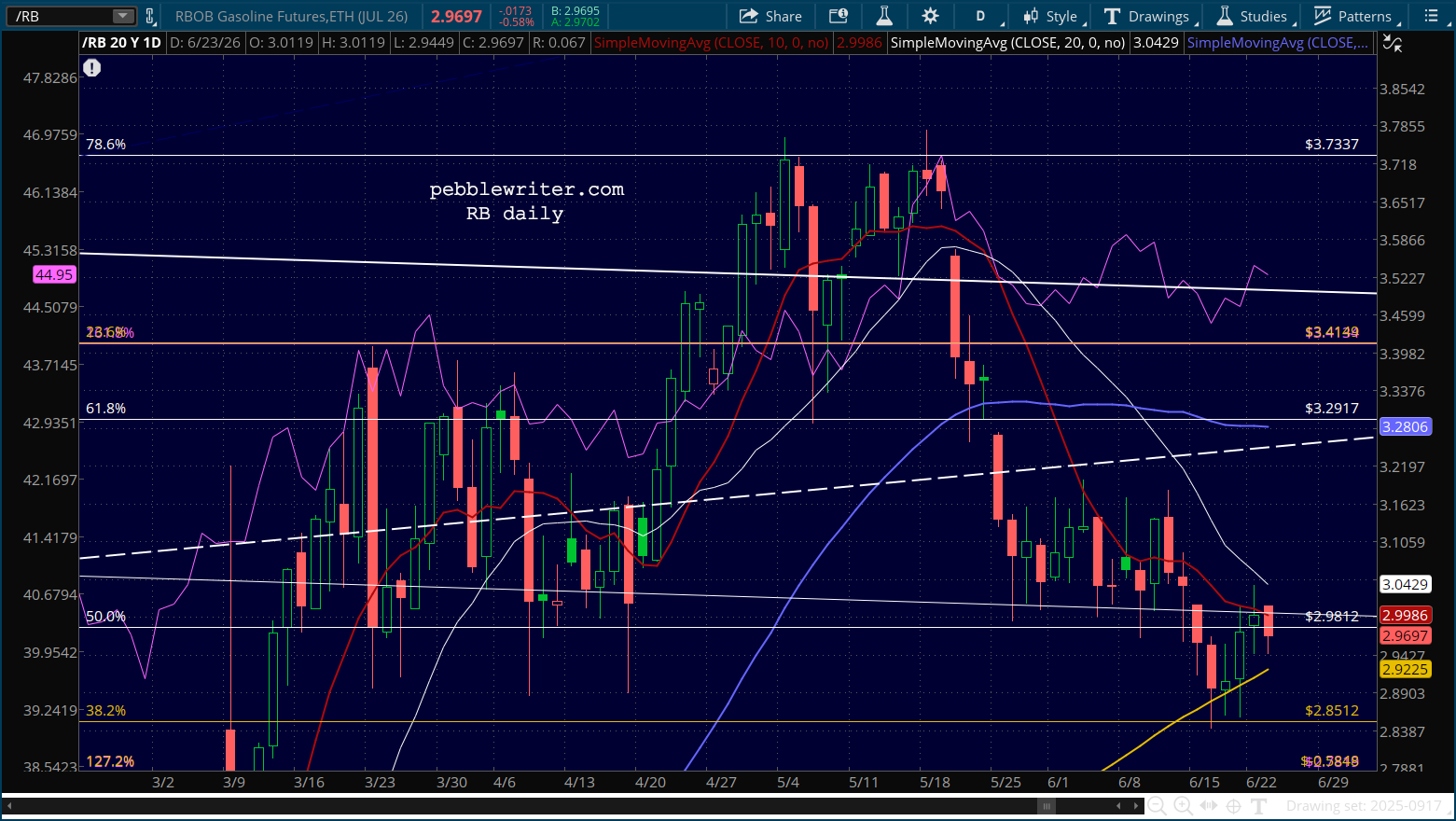

Oil continues to be a wildcard. And, my position has not changed. I cannot see Iran giving Trump any kind of win (though he will certainly continue to claim one) between now and the mid-terms.

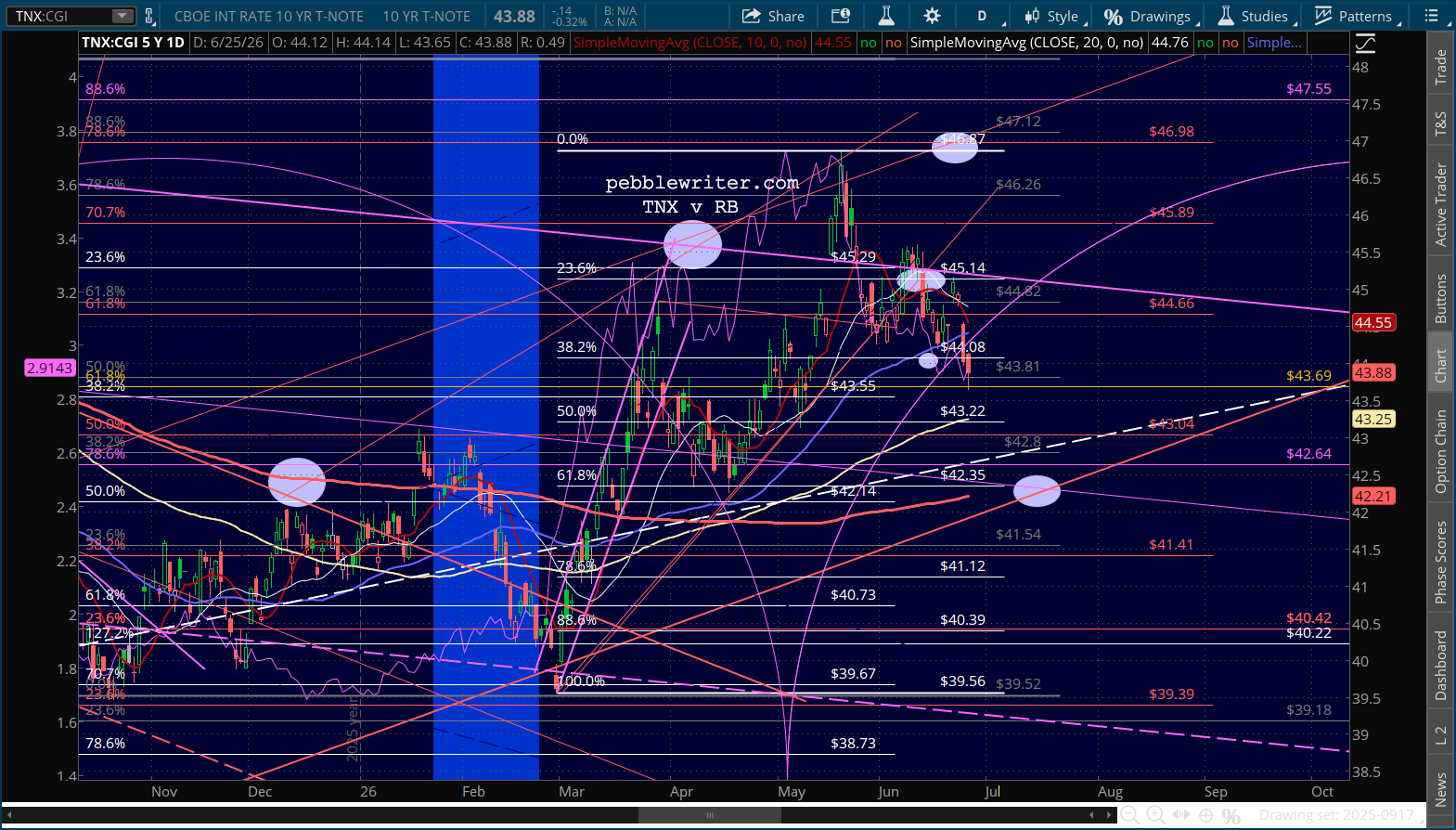

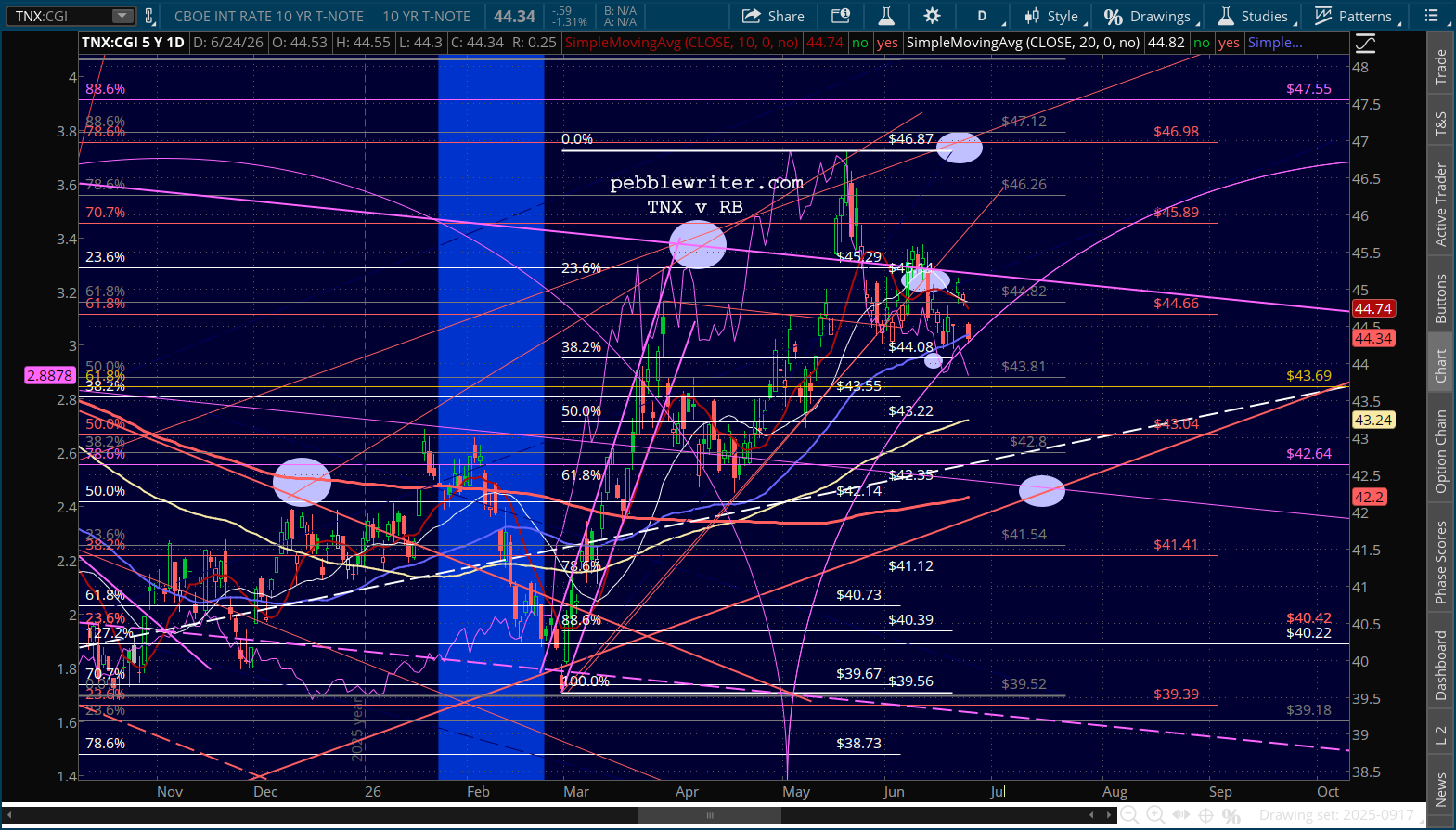

While the 10Y has been greatly affected by falling oil prices, the next leg lower (to 4.235% by Jul 22) is more likely to be driven by an equity selloff.

Meanwhile, the USJDPY is inching up on our 167.25 target…

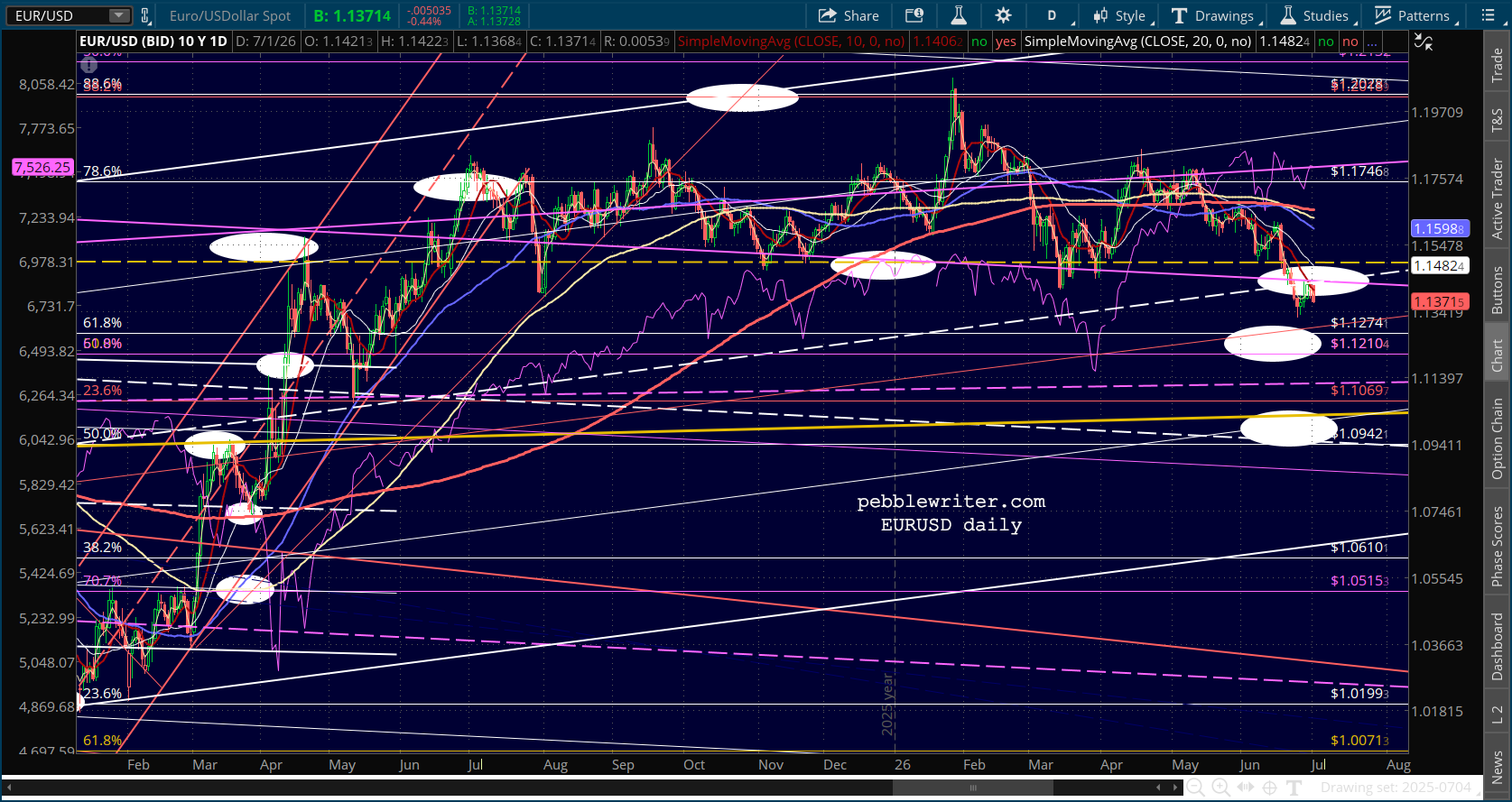

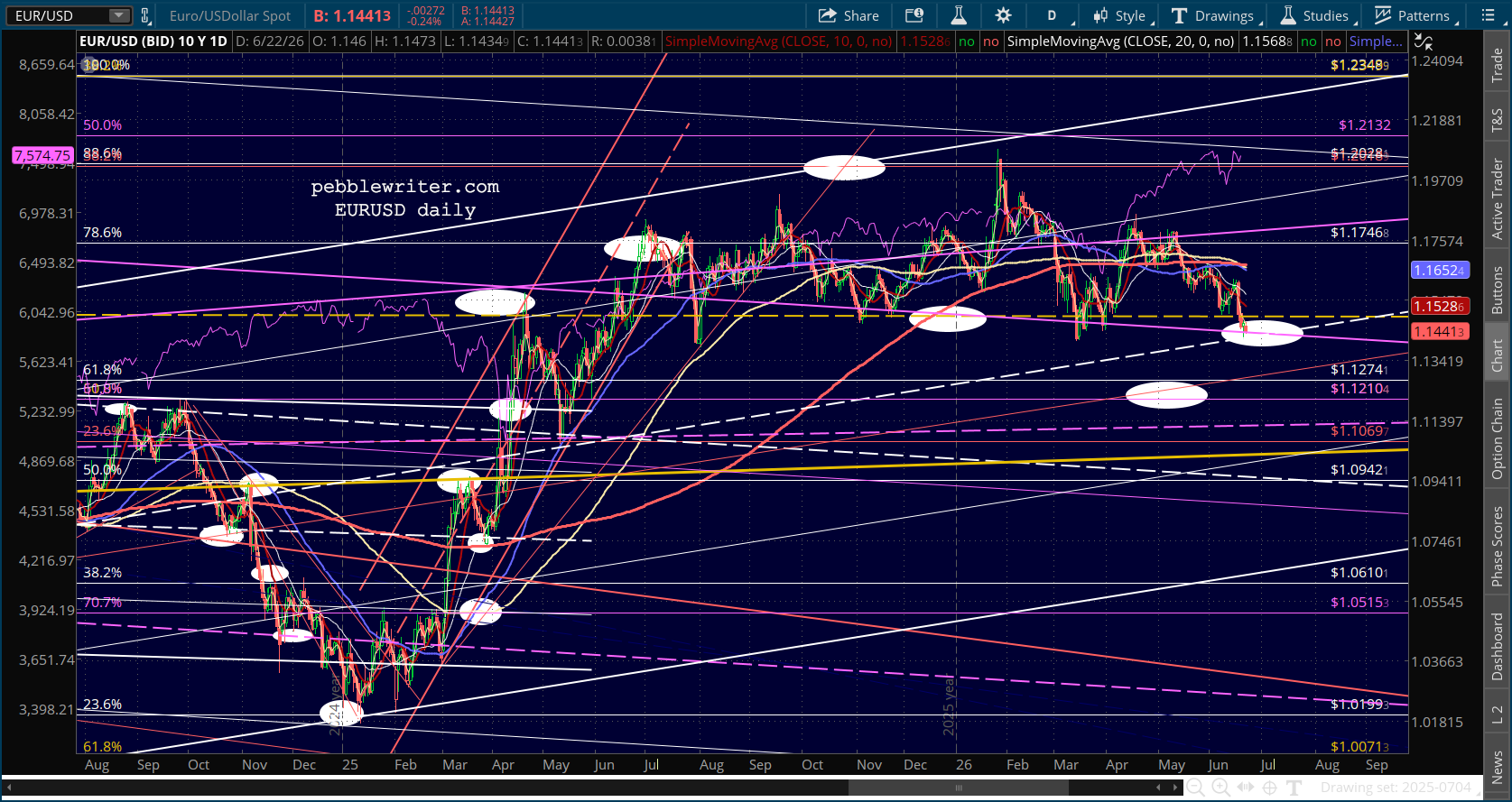

…as EURUSD backtests before heading to 1.09-1.12…

…and DXY breaks out more convincingly, with 104.2 the next significant resistance.

Stay tuned. It’s about to get really interesting…

It’s an end-of-the-month meltup for no apparent reason. There was little in the way of lasting selloffs last week, even as increased hostilities between the US and Iran pegged oil prices at strong support. The next two days should see some backtests of the 10-day and 50-day MAs.

The US trade deficit in goods grew by 27.4% t0 $105.8 billion in May, a substantial increase from the $85 billion expected. Imports soared by $10.9 billion to $313.4 billion as businesses increased imports to avoid shortages and higher prices. US dollar strengthening will continue to hurt exports, meaning the deficit should grow even faster in June.

Meanwhile, Iran fired on a ship in the Hormuz Straits in a striking counterpoint to the US assertion that there’s nothing to worry about in the Gulf.

Iran was responding to what it called an “interventionist, irresponsible and provocative” joint statement by the United States and six Gulf states that rejected Iran’s insistence that it could charge tolls on vessels transiting the strait. “Safe passage through the Strait of Hormuz cannot be guaranteed under ambiguous arrangements, parallel routes or decision-making that does not take Iran’s role as a coastal state into account,” Deputy Foreign Minister Kazem Gharibabadi said on X.

With oil prices being hammered lower, inflation should eventually make its way back to an acceptable level. But, that’s not the hand the Fed is being dealt just yet.

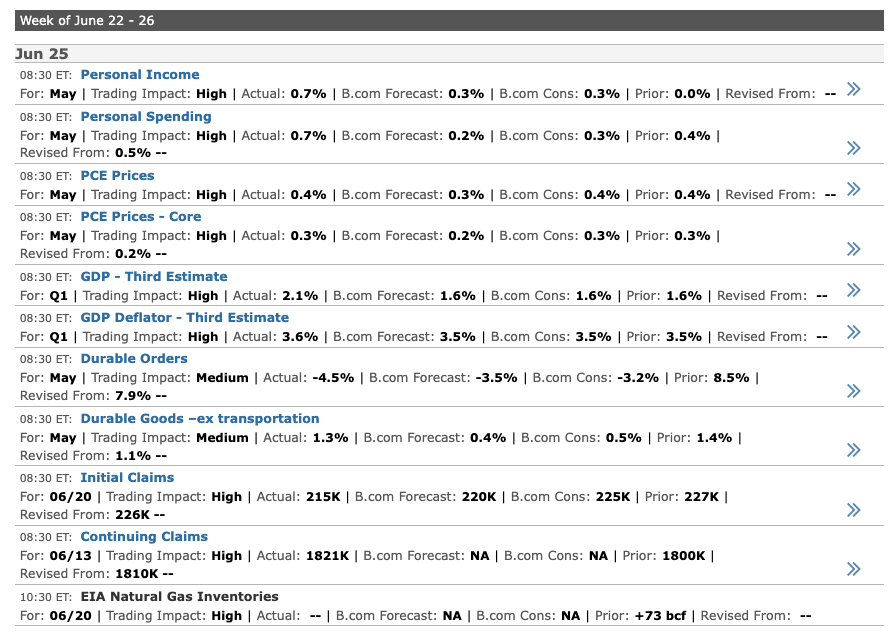

Headline PCE rose 4.1% YoY and 0.4% MoM, the highest since April 2023. Core PCE, which excludes food and energy prices, rose 3.4% YoY and 0.3% MoM – still high enough to concern the hawks and the doves, as was the personal income. personal spending, GDP and claims data — which won’t necessarily follow oil prices lower – at least any time soon.

Futures are still revved up by yesterday’s AI darlings and the bounce off the ascendant SMA50. But, it’s hard to get excited about such a narrow sliver of the market, especially when currencies and bonds are saying to sell, Now.

It’s pretty calm so far this morning, with most of the action percolating through the currency markets as DXY breaks out and the EURUSD breaks down.

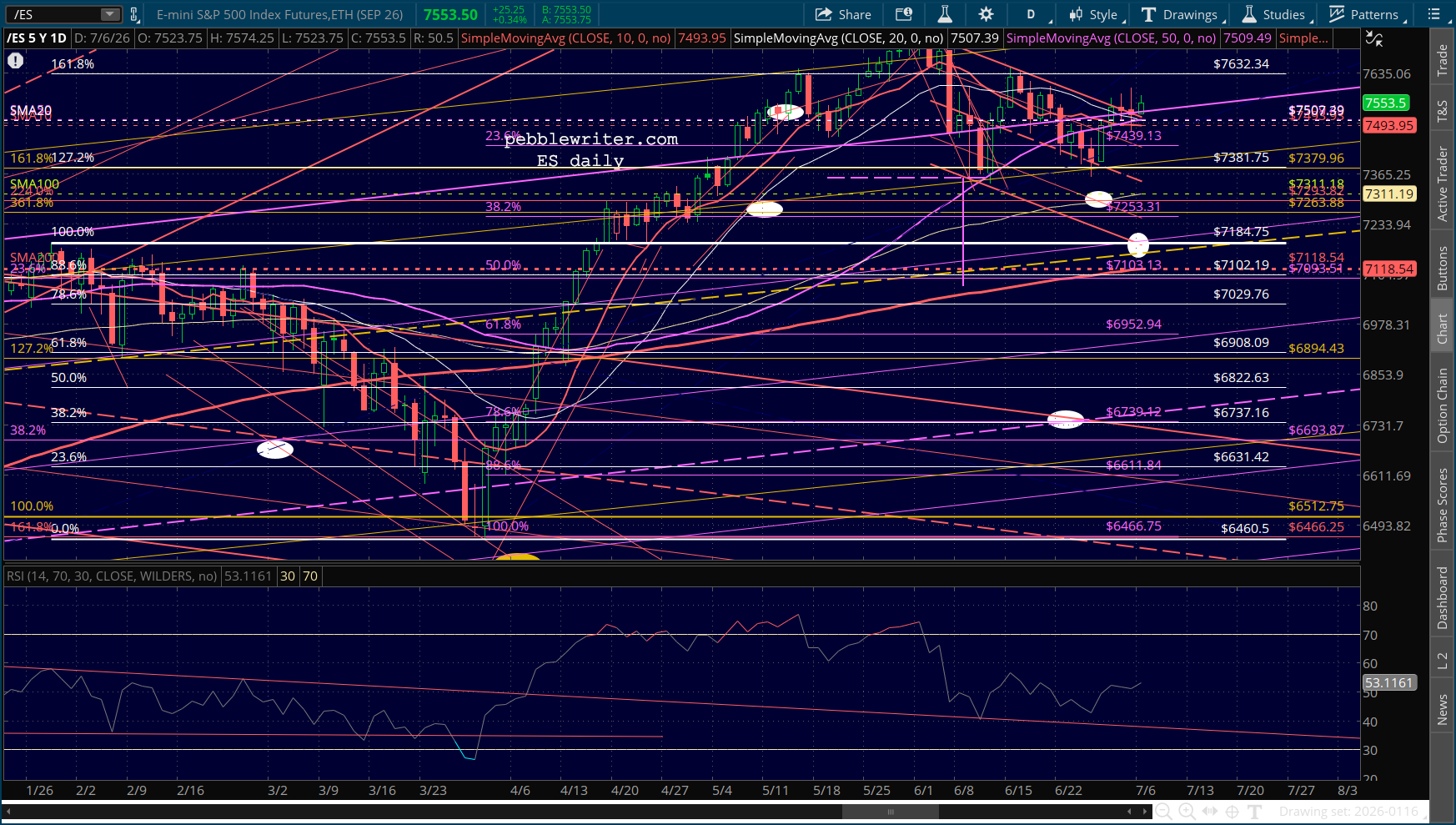

There should be more downside ahead, with backtests at SPX 7000 and ES 7184 looking pretty good.

One of my favorite past times as a kid was playing gin rummy with my grandfather. Gramps was a masterful player and could easily beat me with his eyes closed and one arm tied behind his back. When he declared “gin” (usually after repeatedly bemoaning his horrible luck… “woe is me”) and caught me with way too many high value cards in my hand, he would mimic a lumberjack as I laid each on the table, “timber! timber! timber!”

He let me win often enough to keep me coming back for more. I think the countless games we played when observing the stock market. Are the men pulling the levers behind the curtain allowing days like today just to keep permabears coming back for more, or might they really lose control at some point?

As Joshua would remind us, “the only way to [not lose] is not to play the game.” But, that’s no fun. And, how does it even make sense when we all know that markets only go up? Besides, if stocks were to fall 20% from here, how much joy would you get from declaring “I made 5% this past year” at the cocktail party?

Stocks are falling around the world, with Korea’s Kospi off 10%…

…and ES indicating a more modest 1.5% overnight plunge. As we’ve noted over the past several sessions, there is no shortage of downside targets. The trick is figuring out when Trump will swing into save-the-market via-social-media mode and “fix” things.

…and ES indicating a more modest 1.5% overnight plunge. As we’ve noted over the past several sessions, there is no shortage of downside targets. The trick is figuring out when Trump will swing into save-the-market via-social-media mode and “fix” things.

As we discussed yesterday, DXY’s strength spells trouble for stocks. Bulls need a reversal.

And, the Iran situation isn’t helping. There aren’t many analysts who buy the narrative that things are going great with the peace deal. It’s quite unlikely that Iran will suddenly decide to make Trump look like the victor.

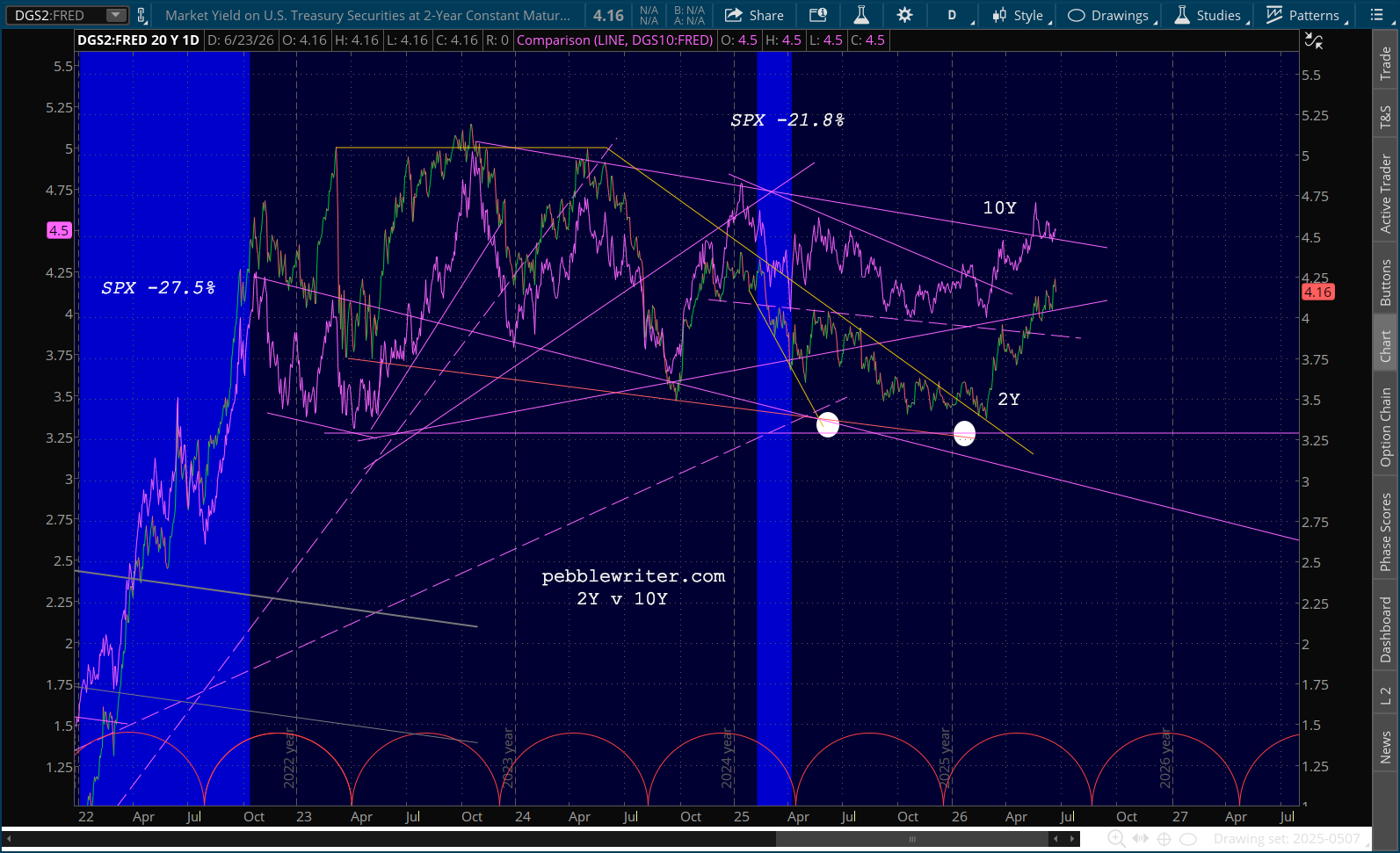

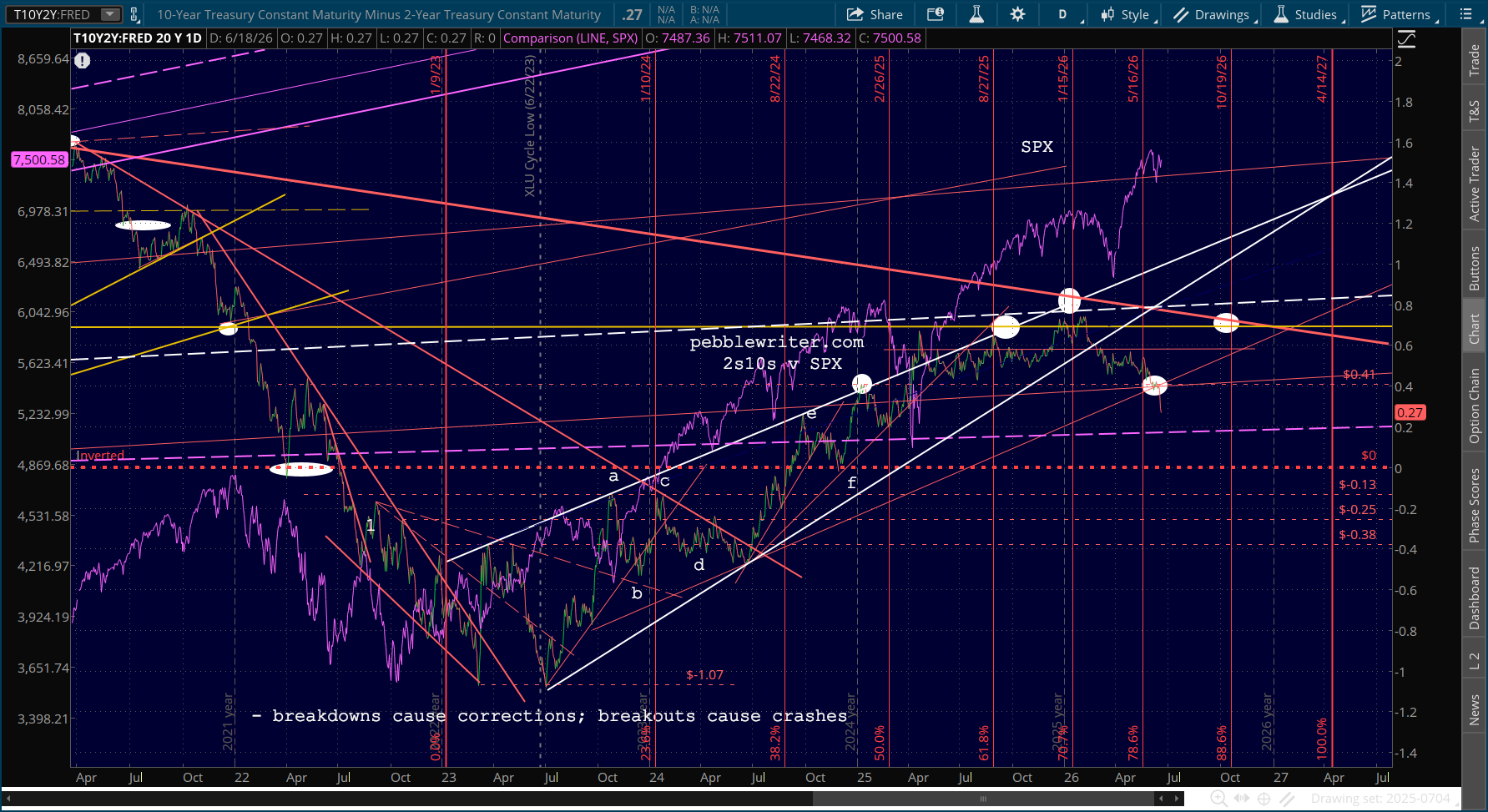

The algos were busy overnight, turning a 1/2% slump into a slight gain as we approach the open. But, the warning signs are building, starting with our 2s10s model. The latest breakdown is worrisome.

So is the currency picture. DXY has reached triple overhead resistance. A breakout would surprise no one given the US’ inflation problem. It’s decision time for EURUSD too.

The 10Y continues to threaten a breakout, but 4.25% in mid-July would more likely be the result of an equity correction than a sudden decline in inflation.

It’s likely to come down to CL and whether it bounces off its SMA200 or drops through it.

It’s why equity targets are all over the map.

GLTA