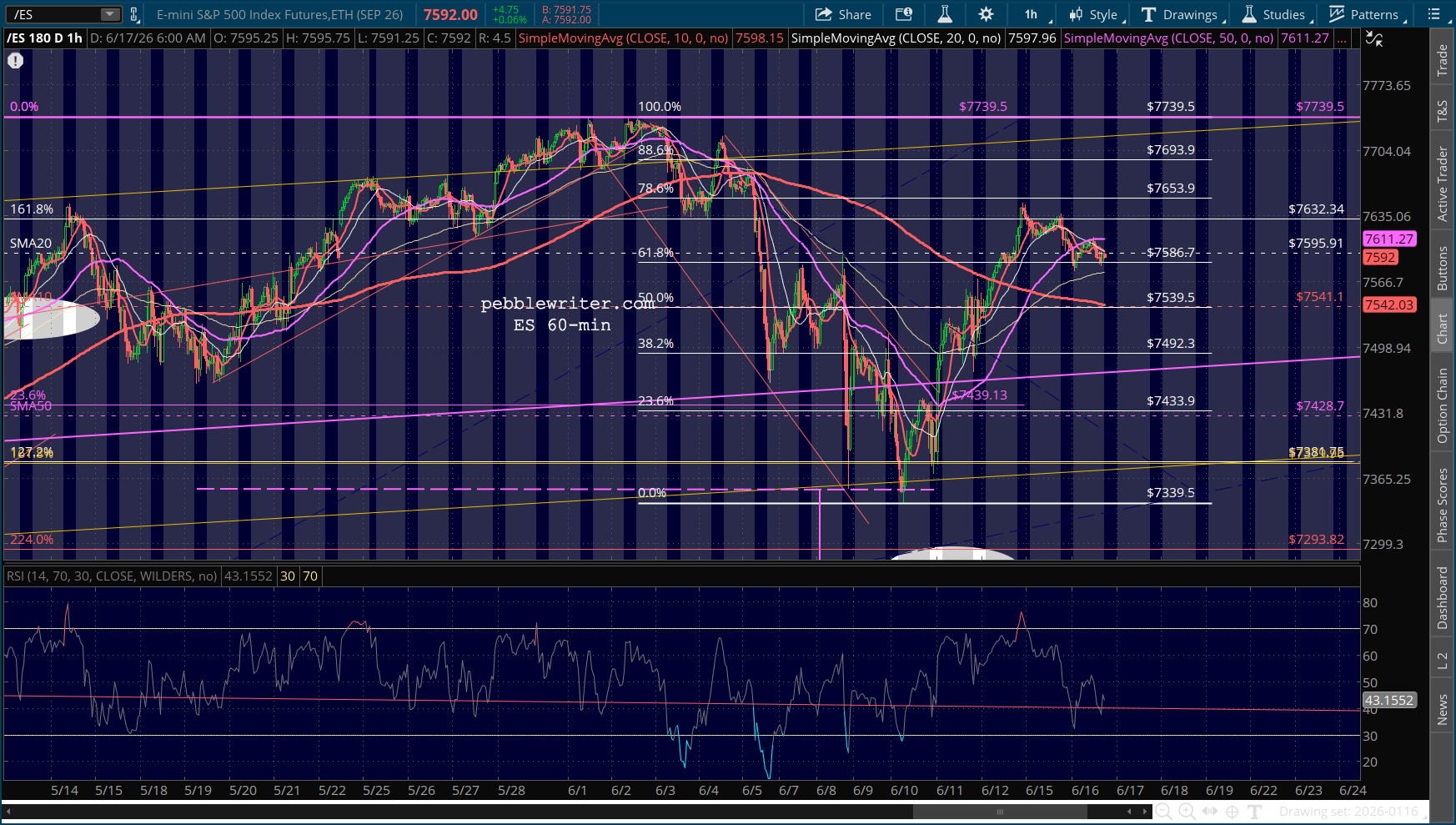

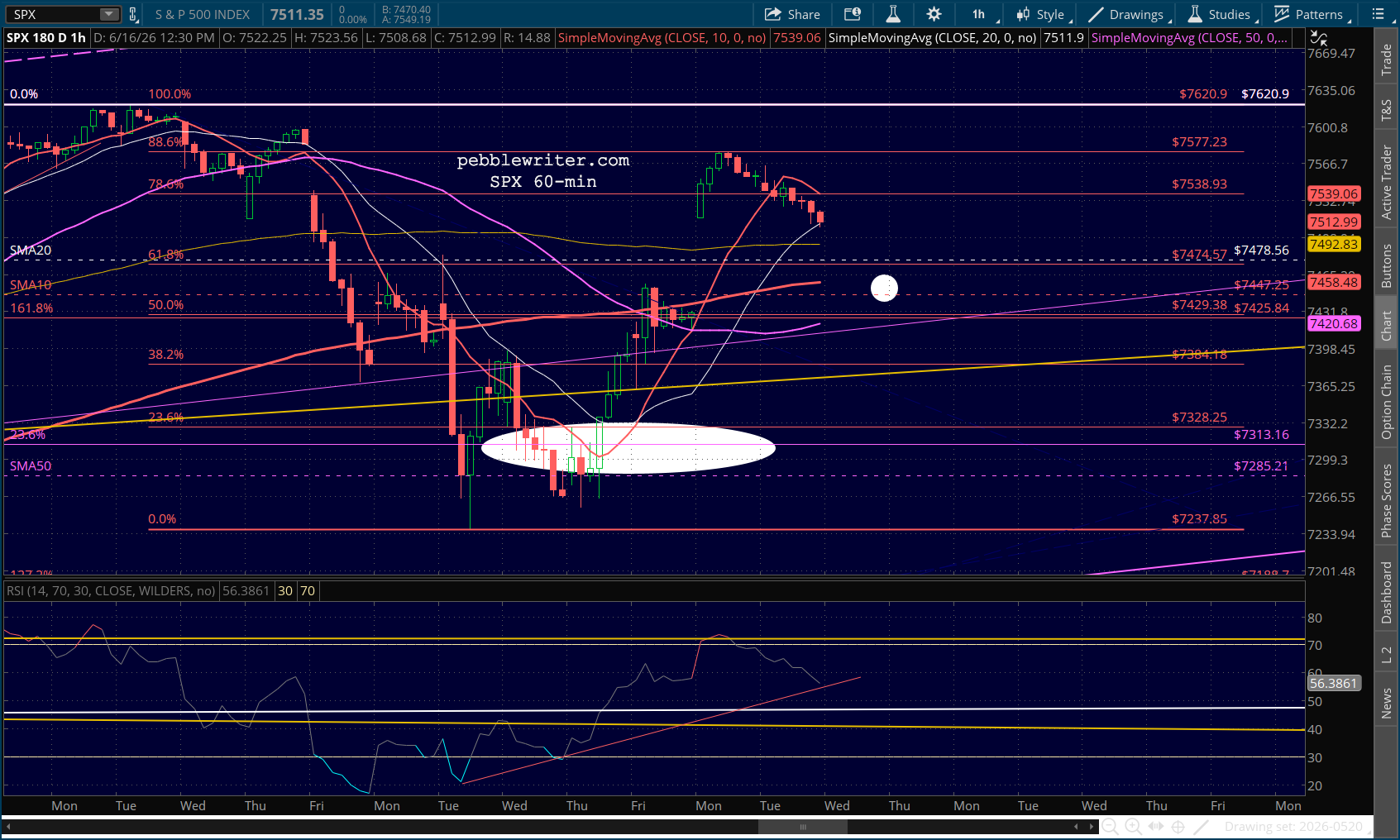

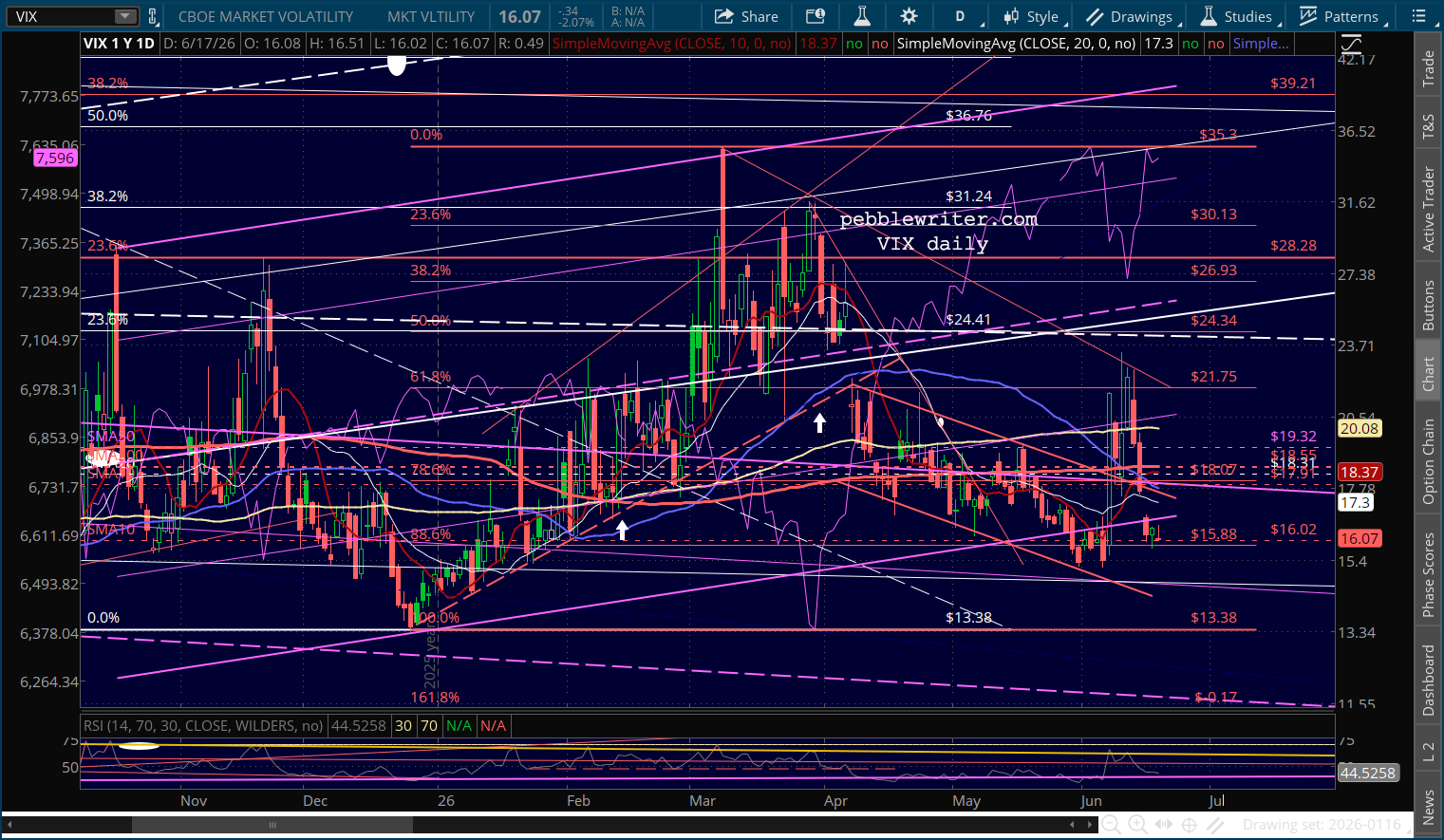

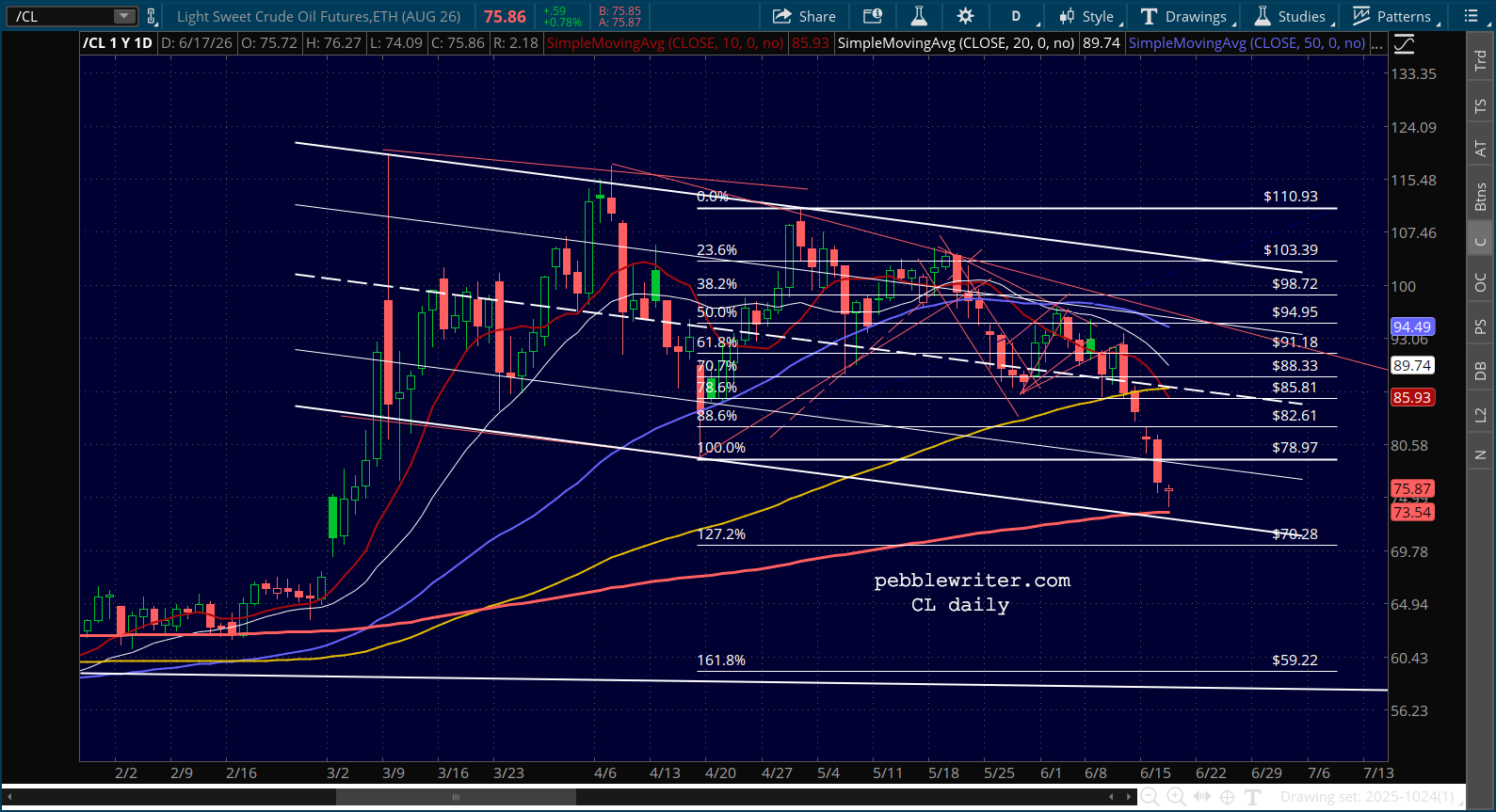

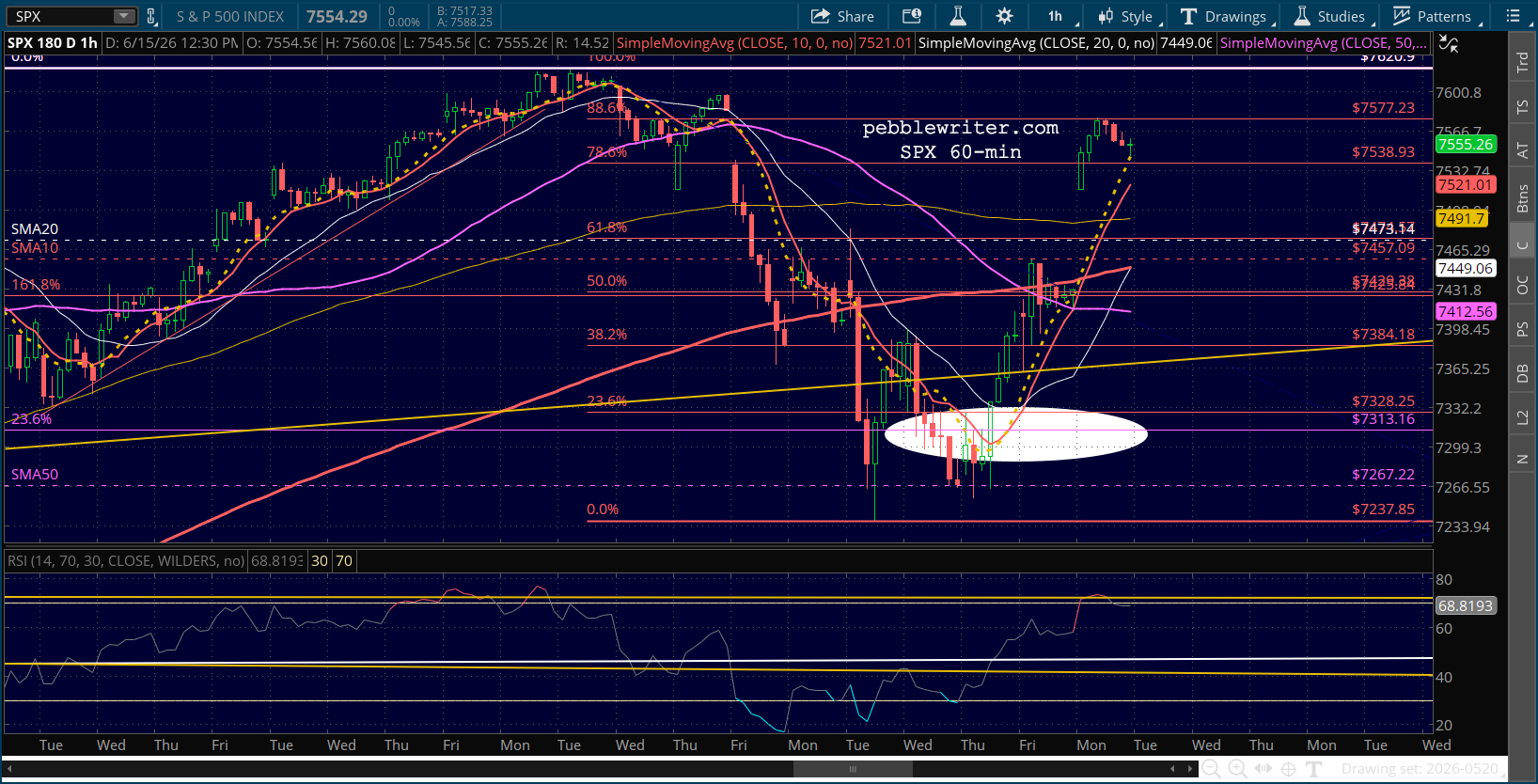

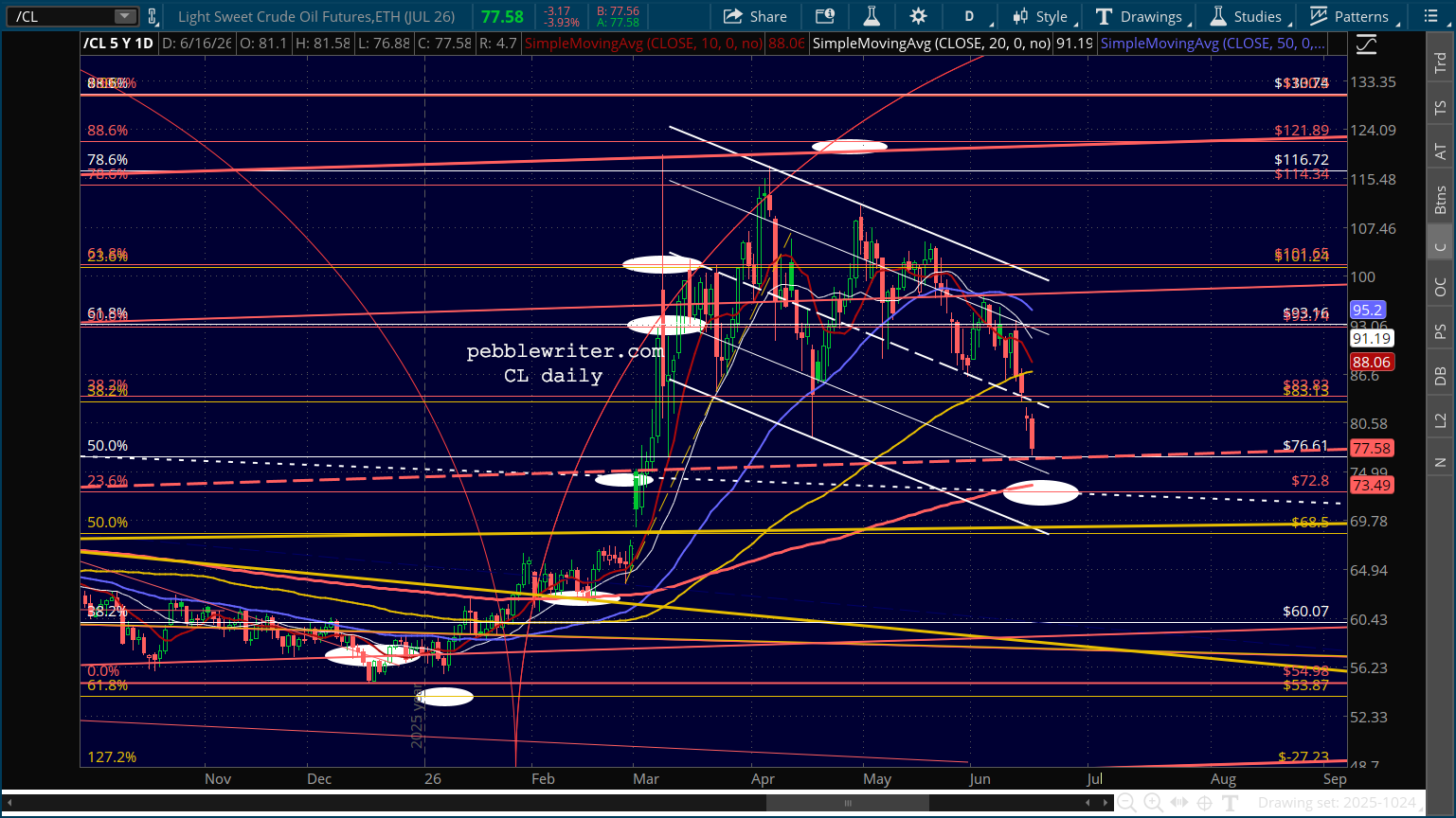

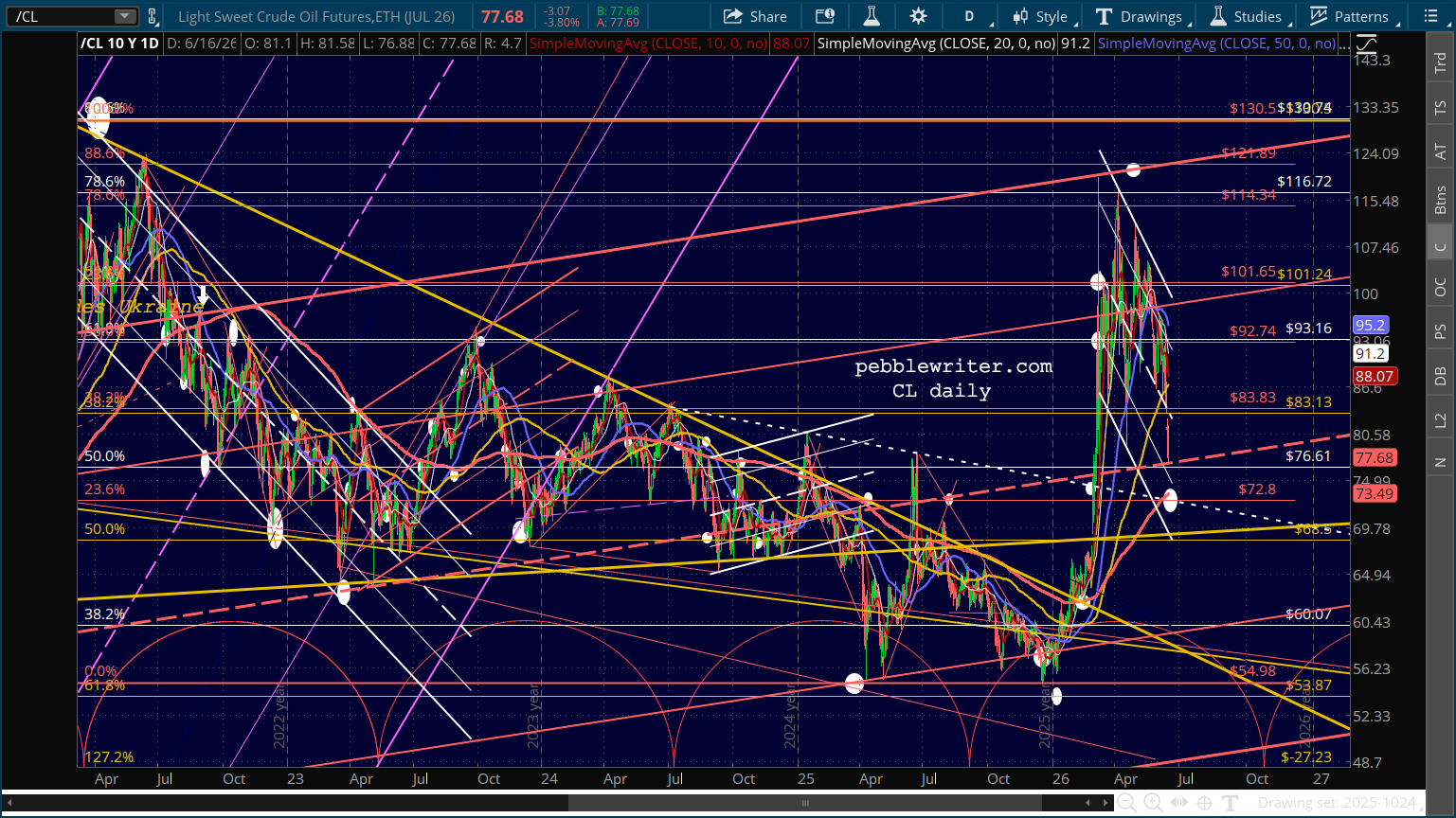

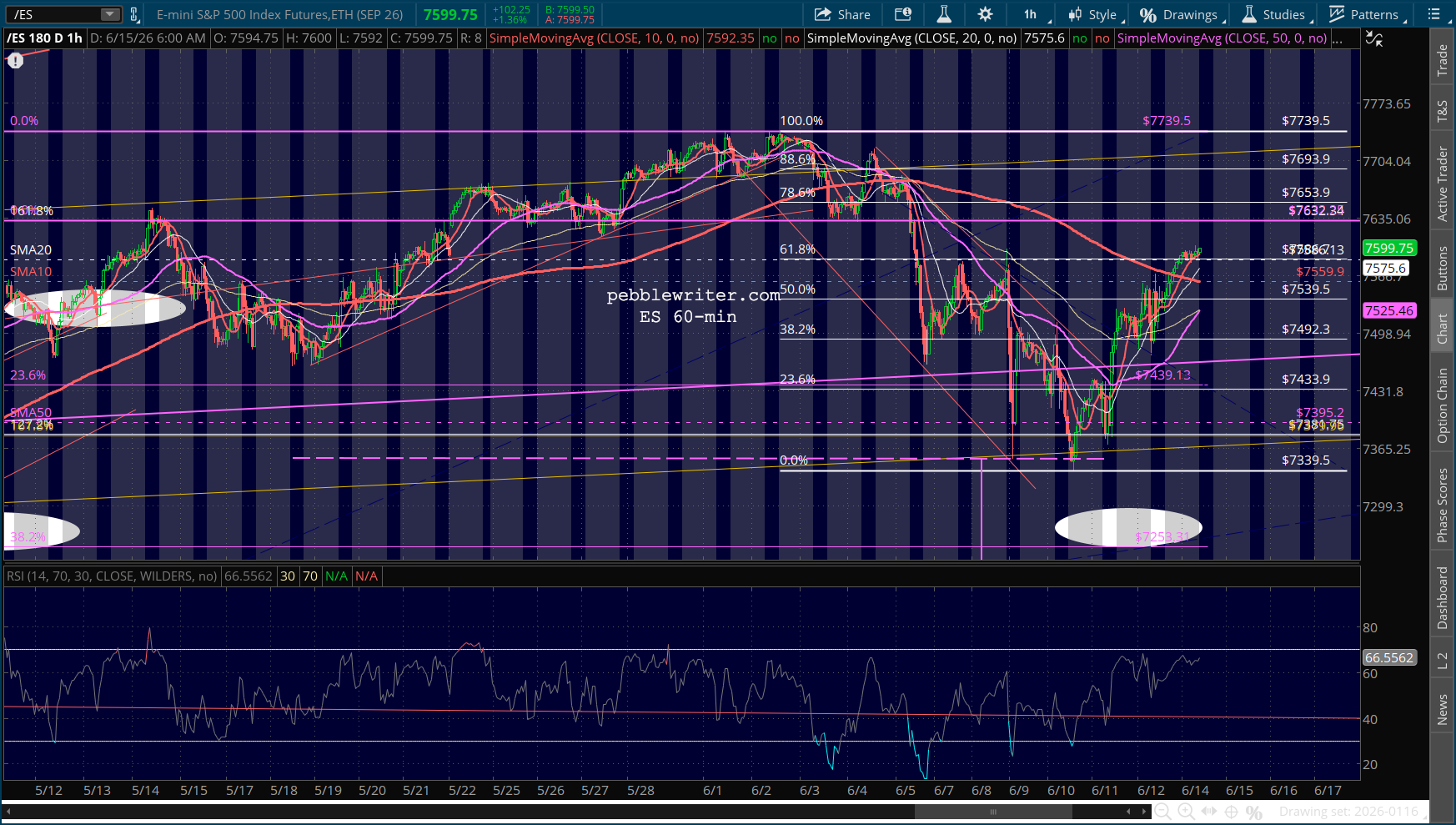

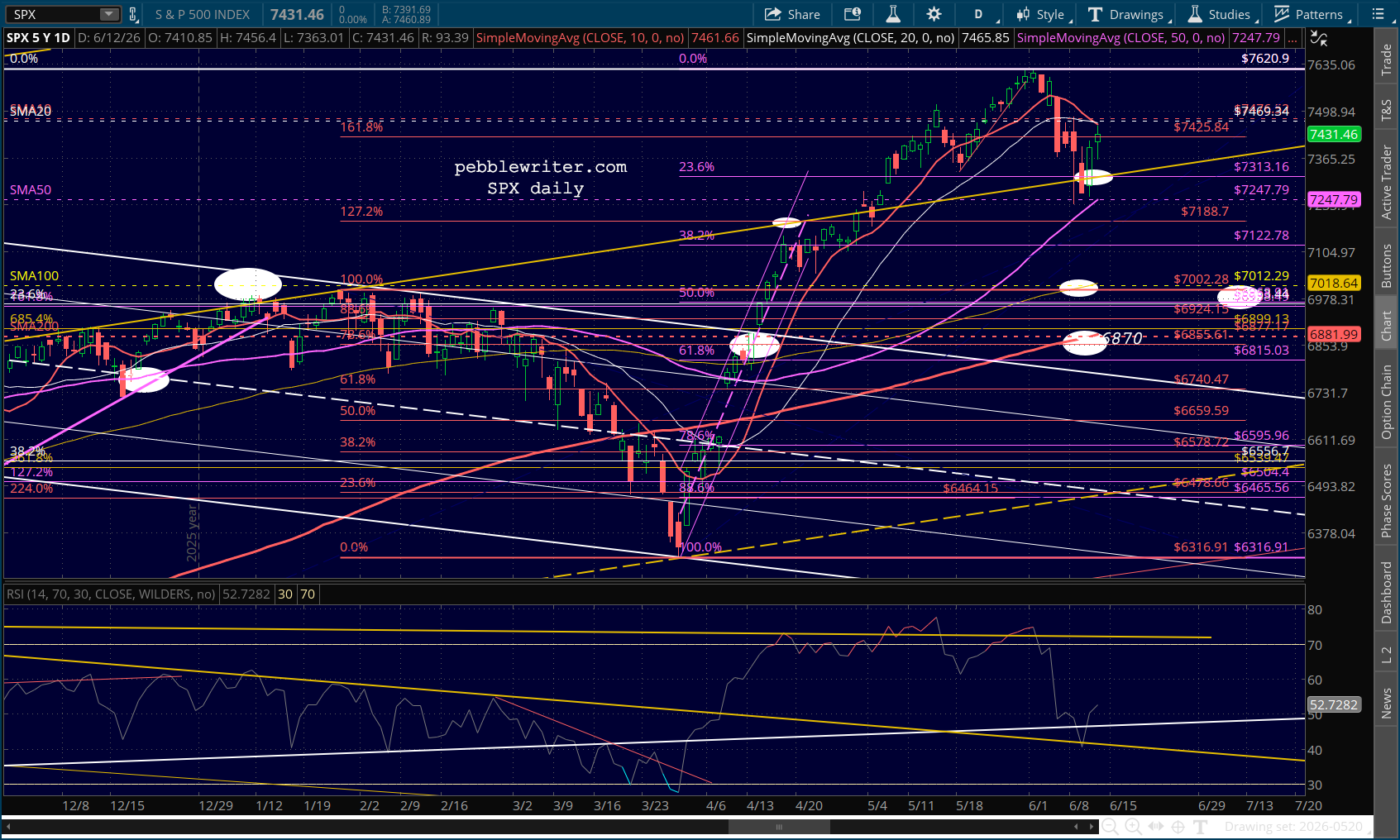

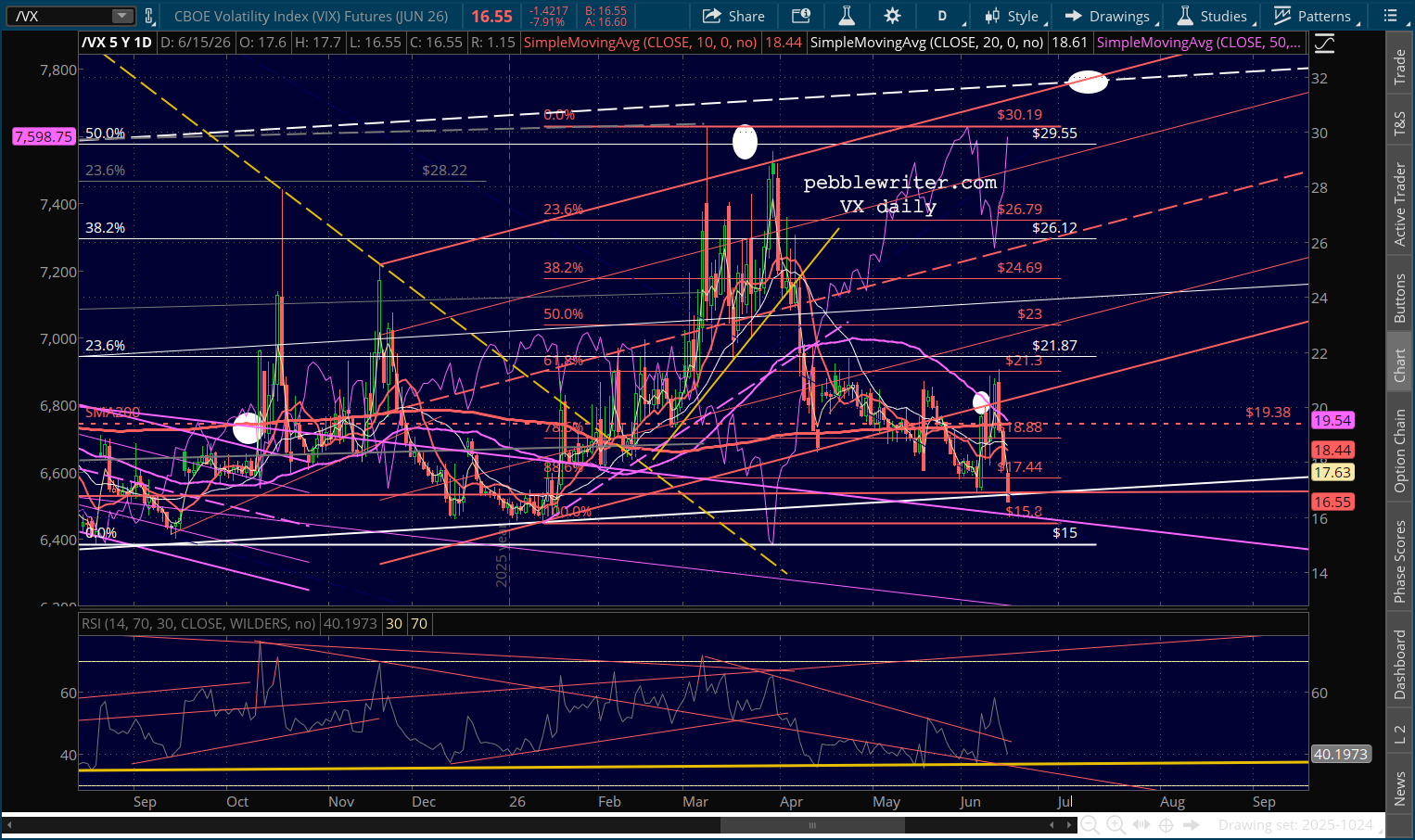

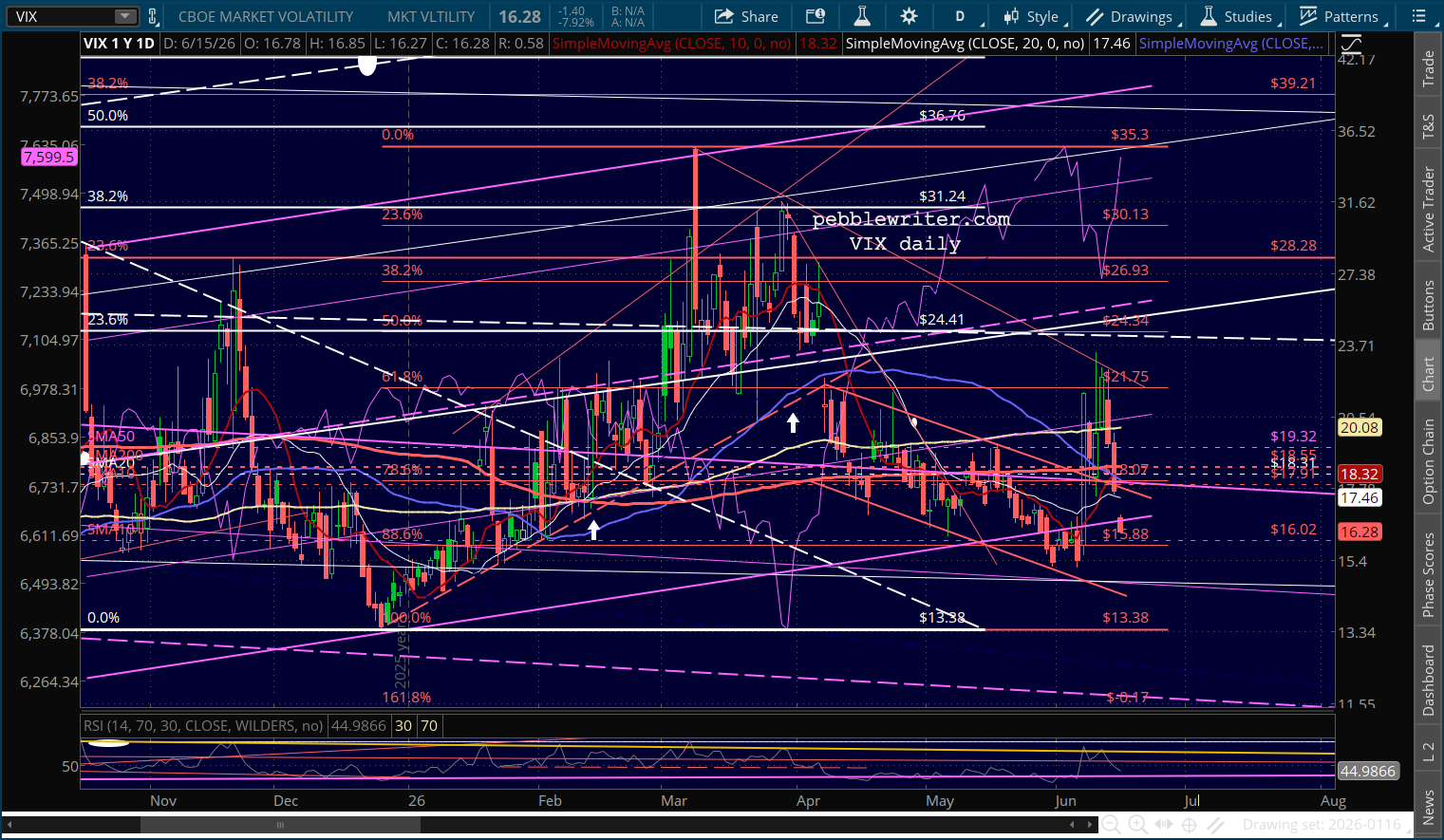

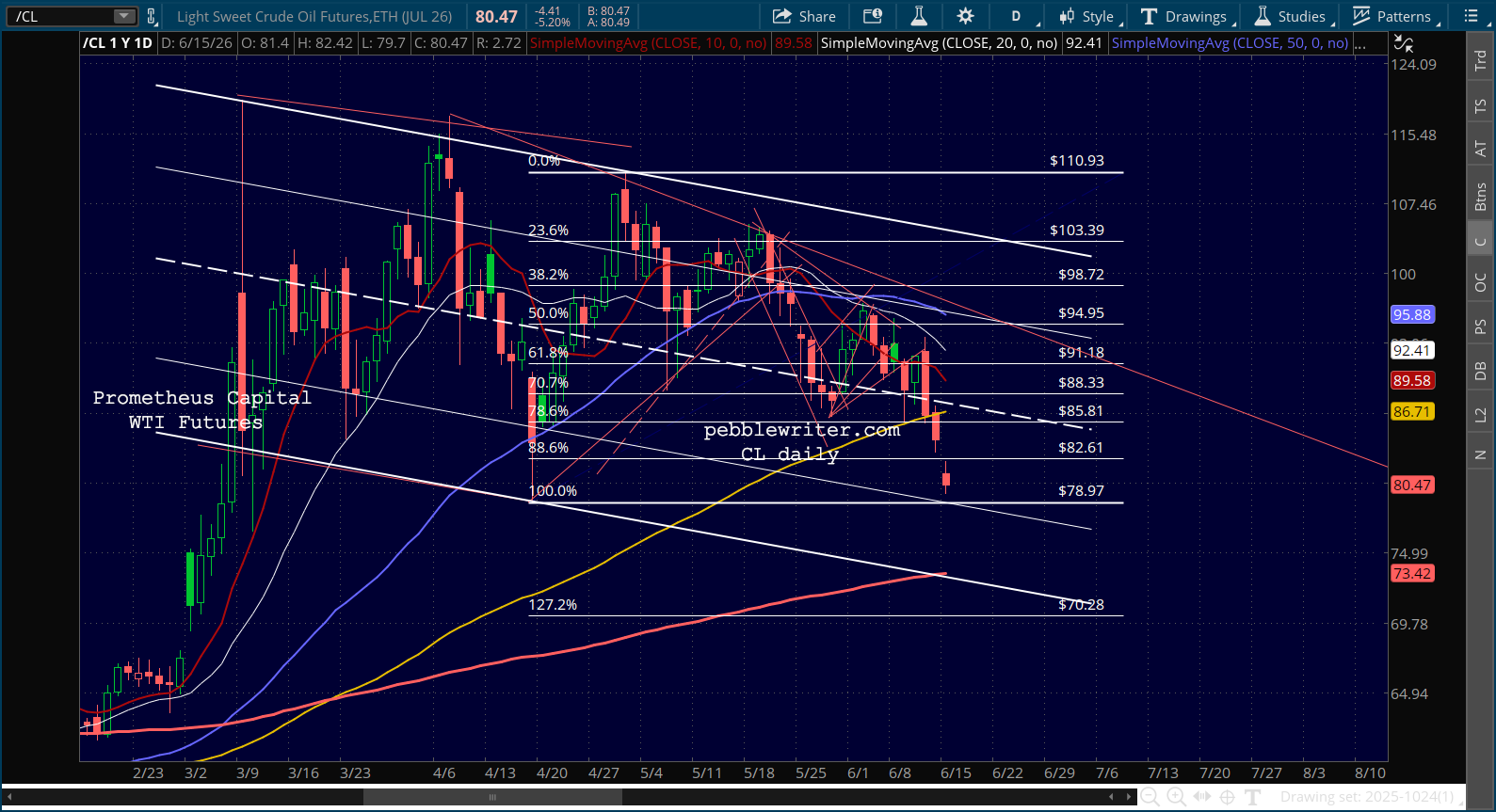

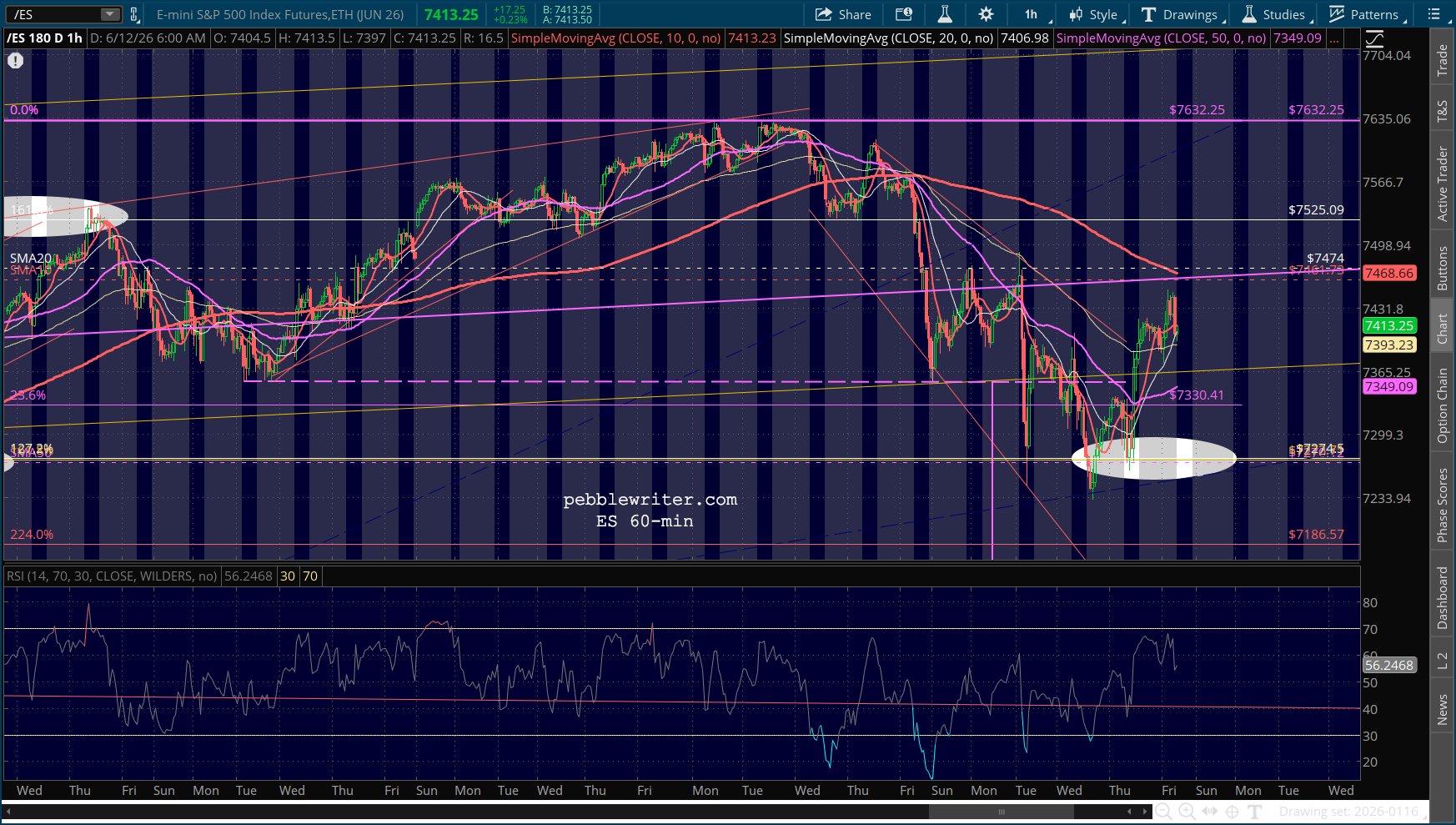

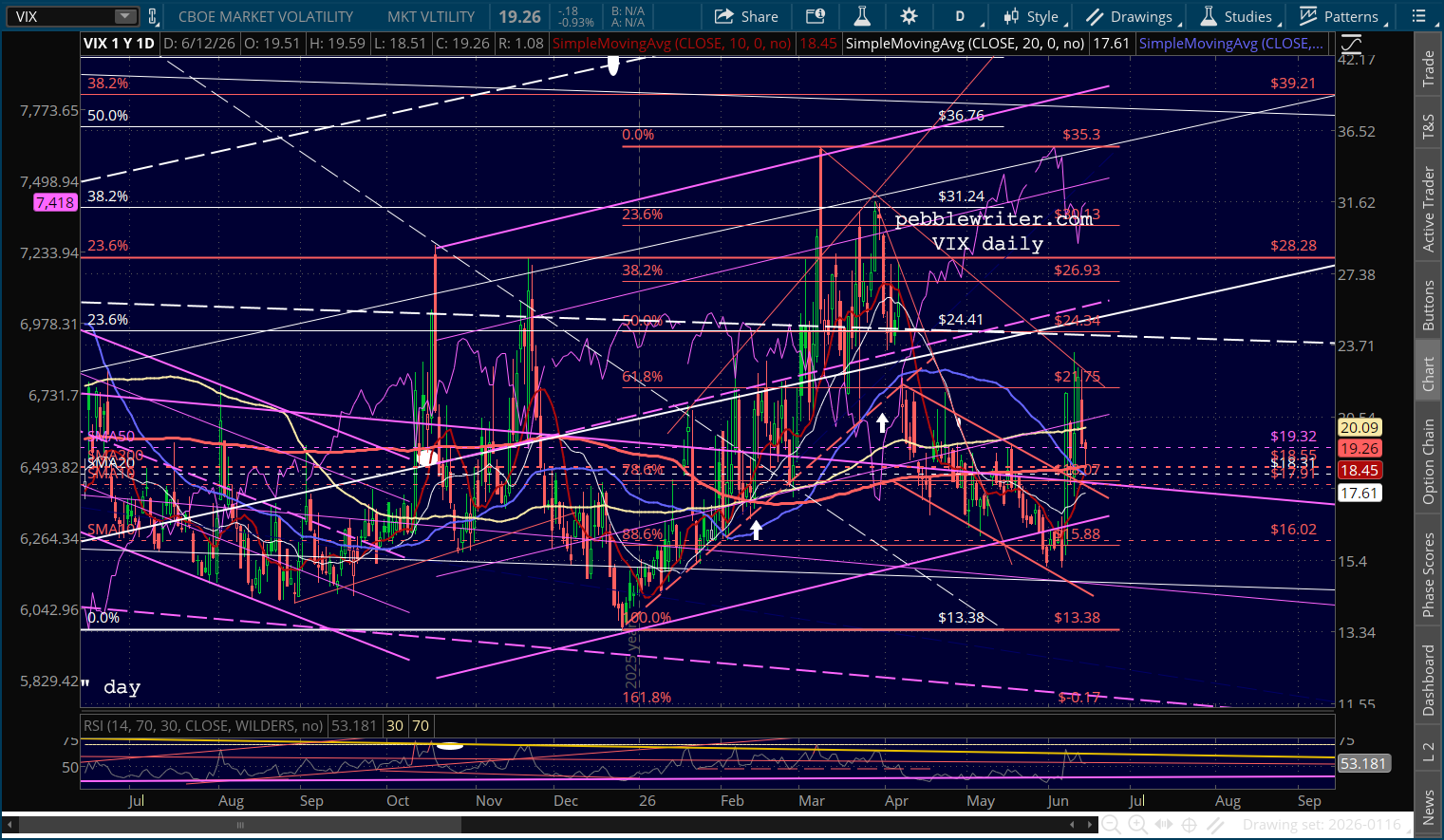

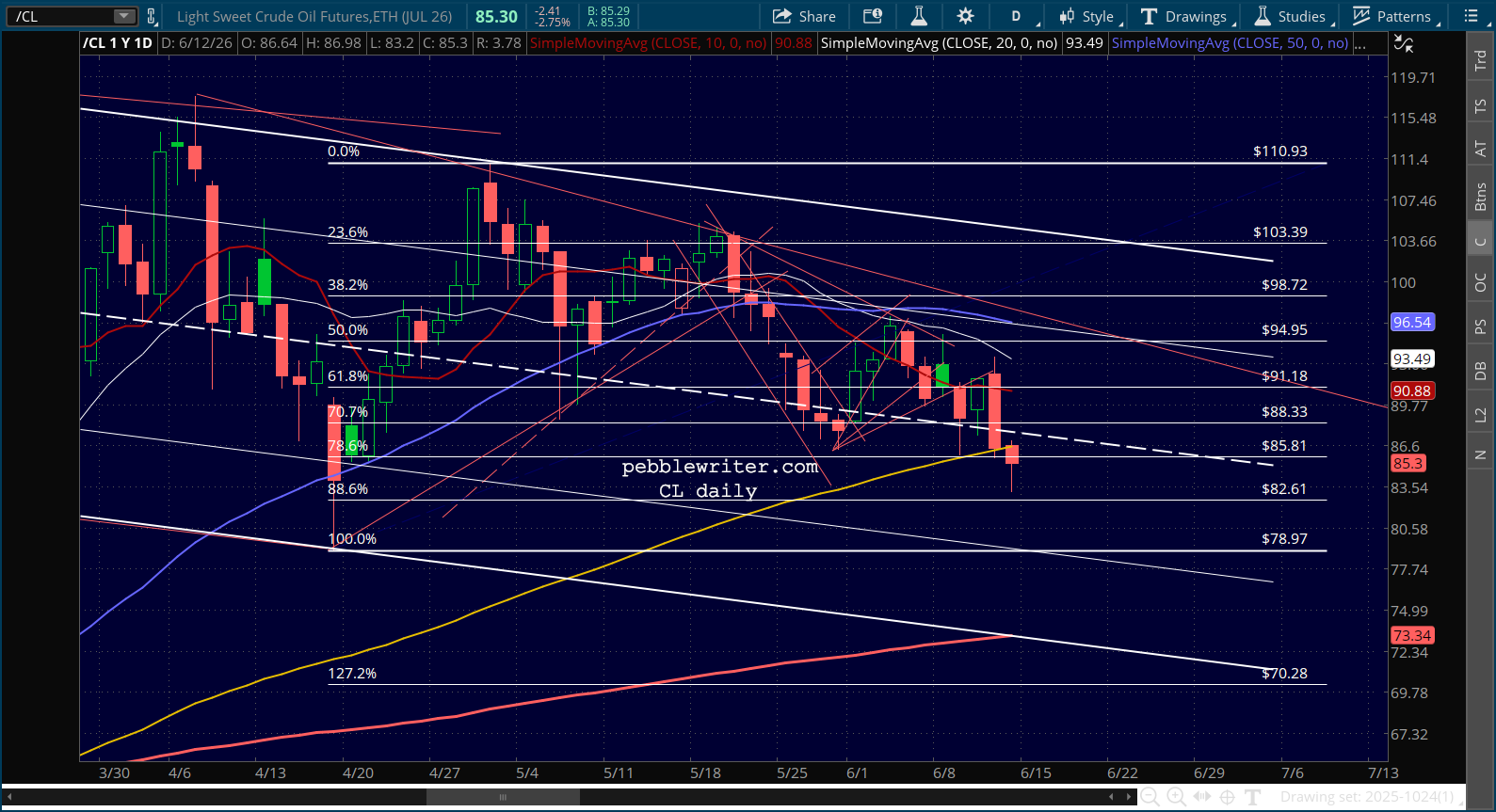

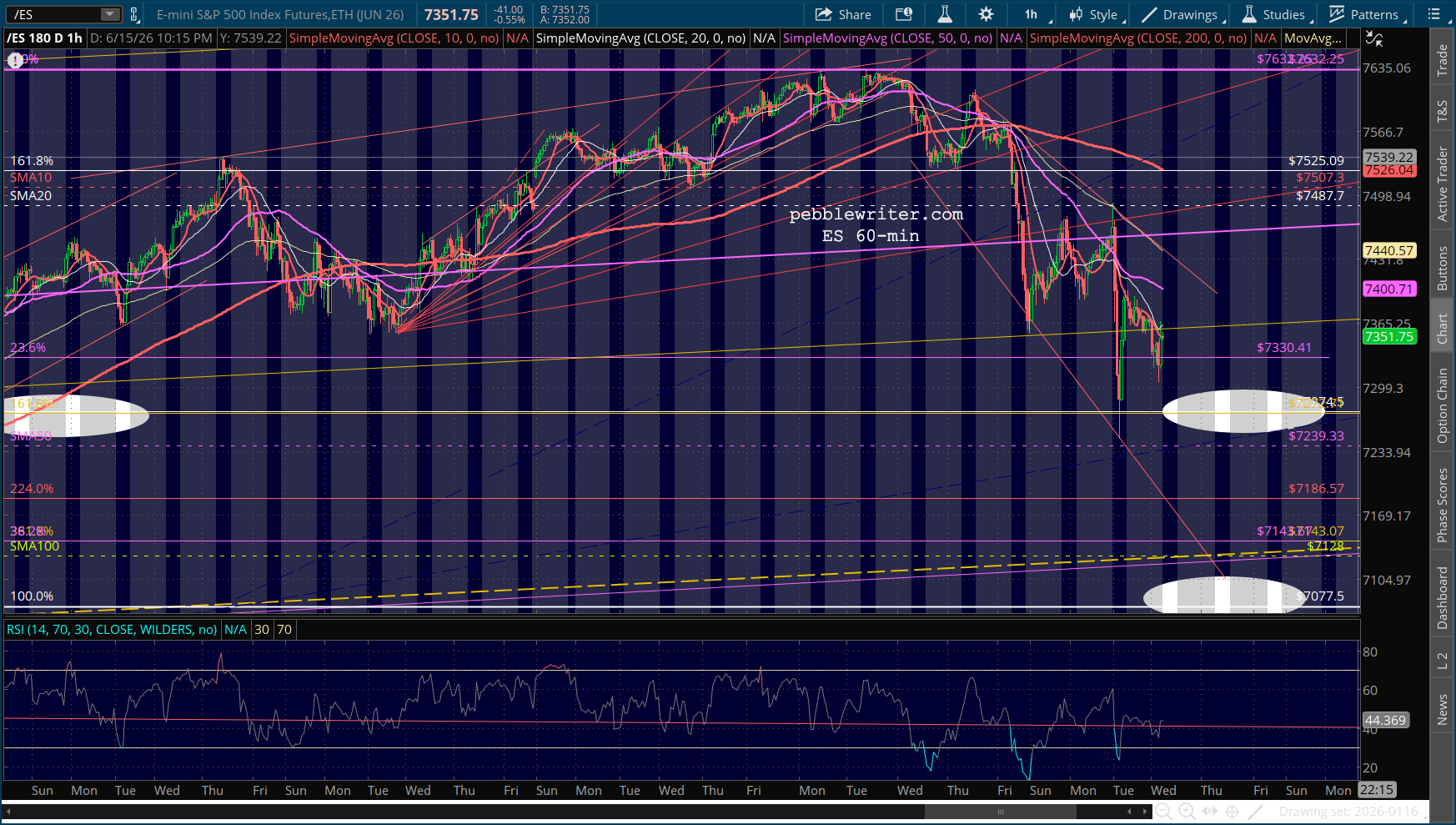

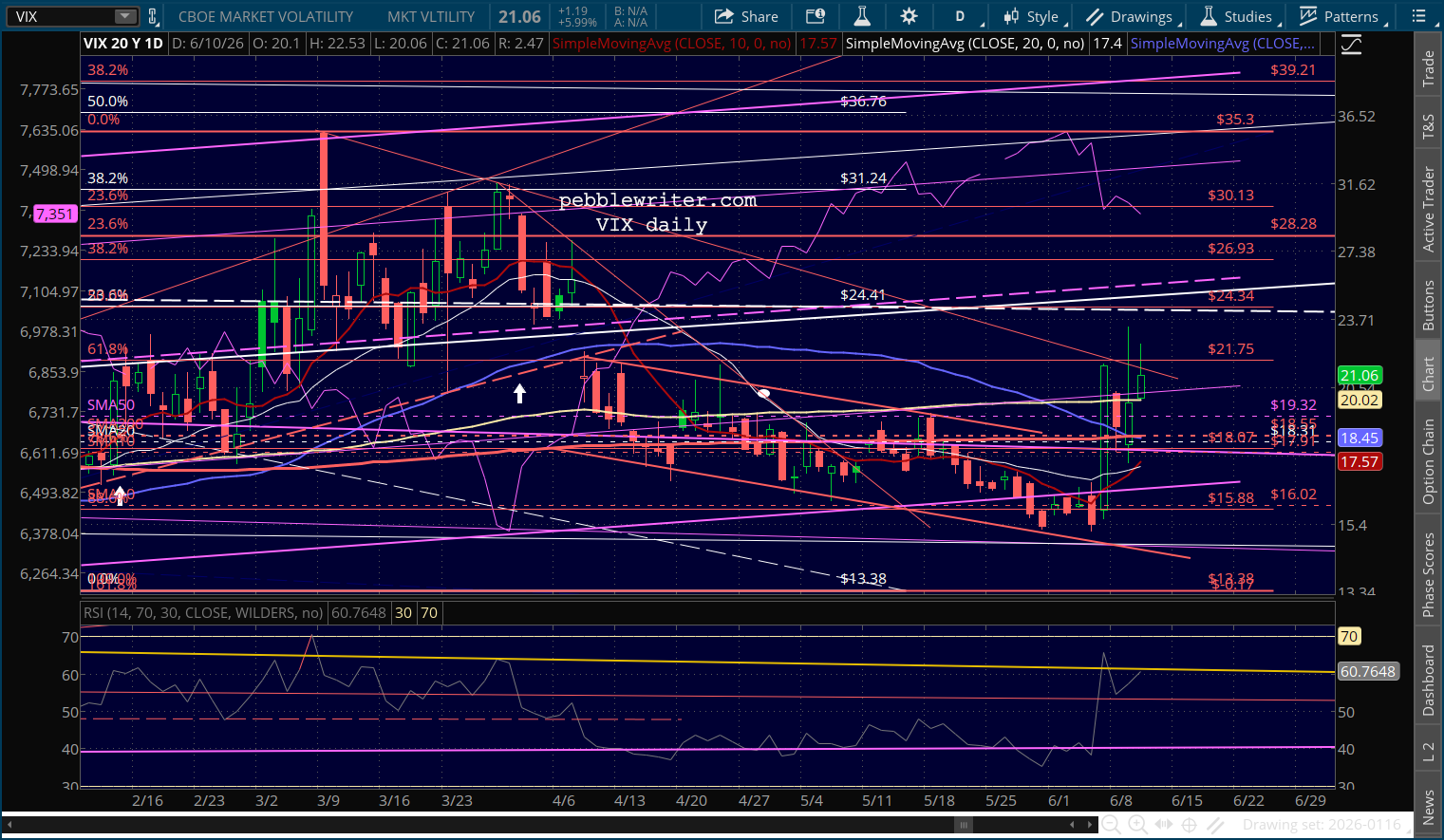

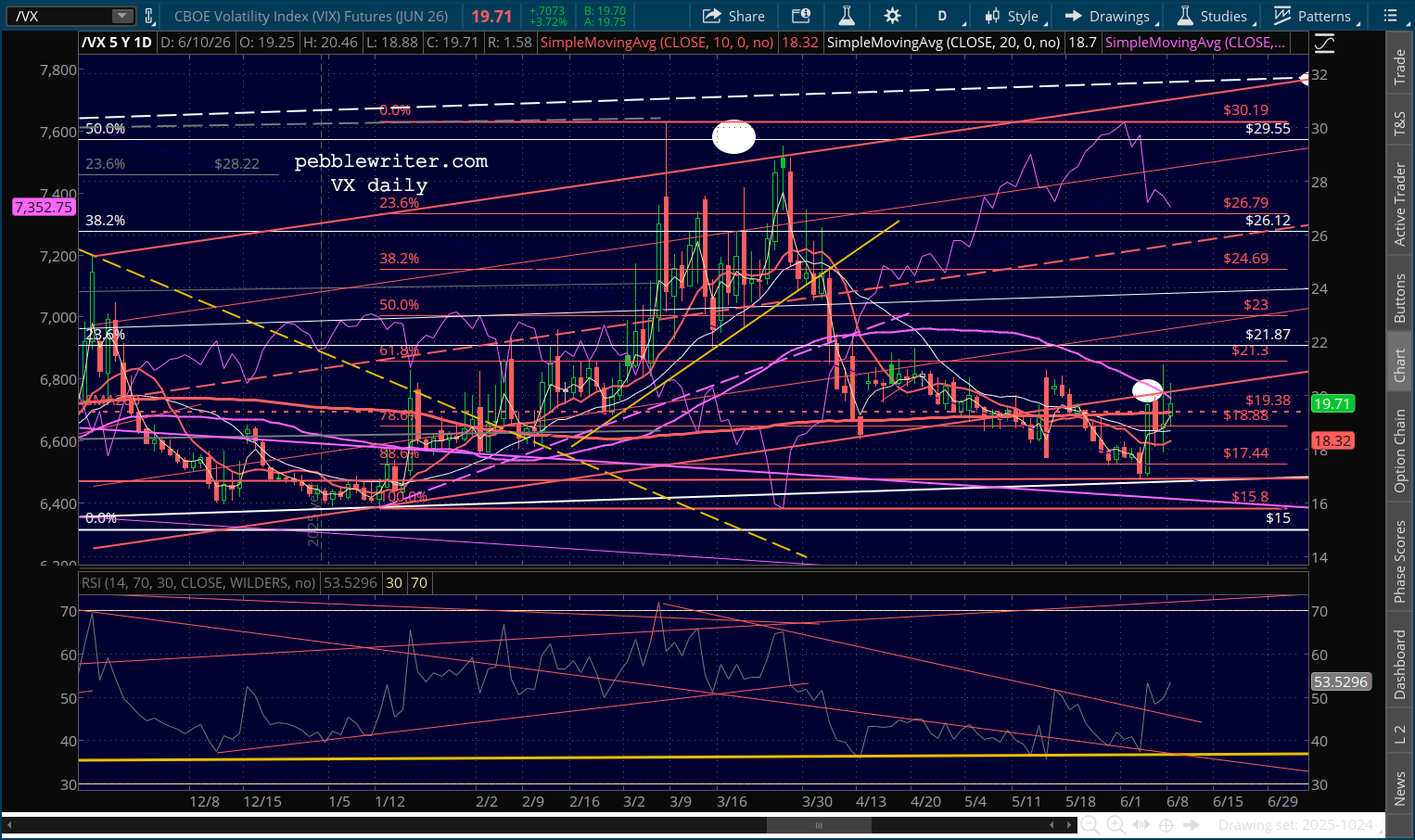

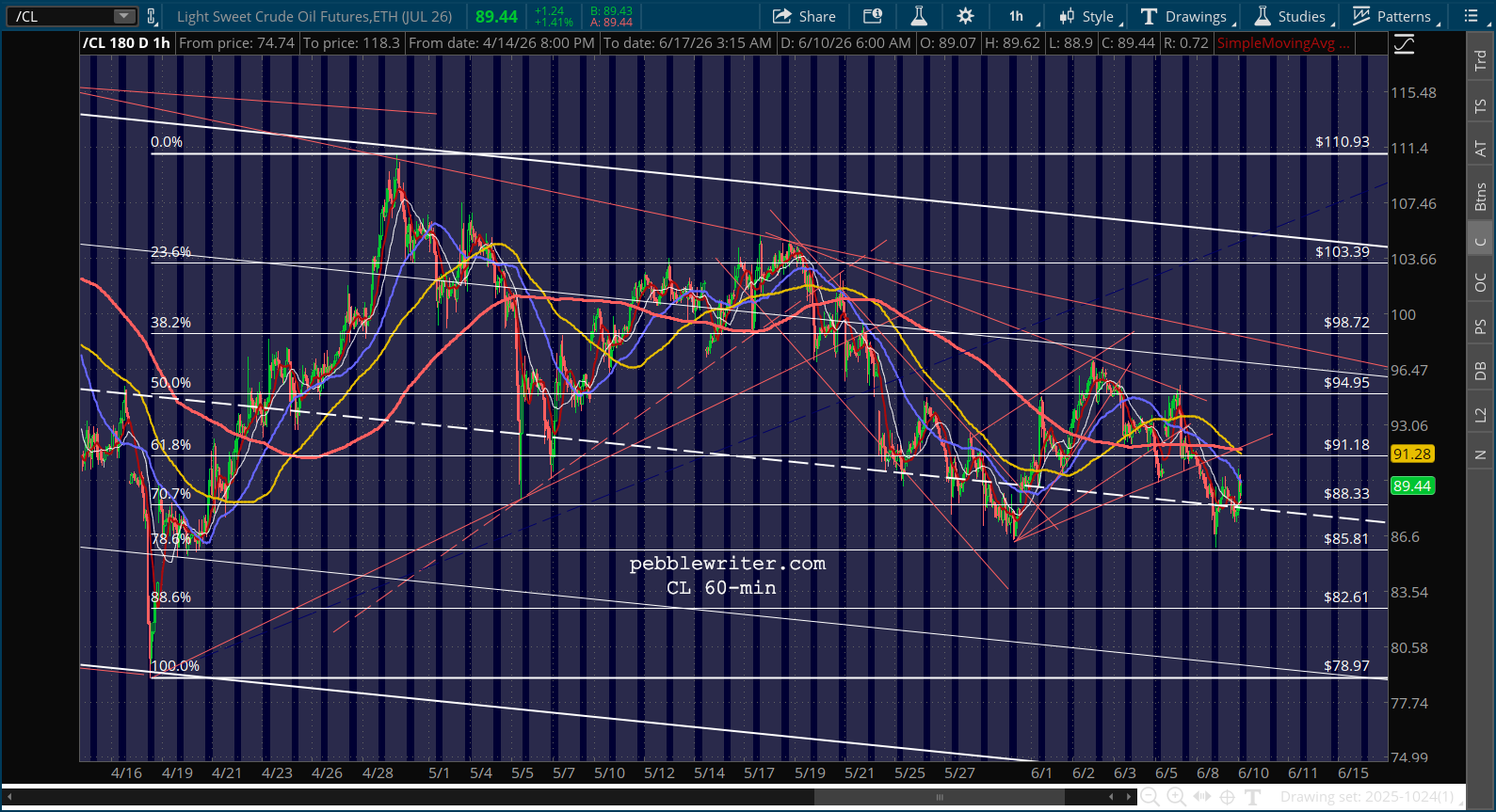

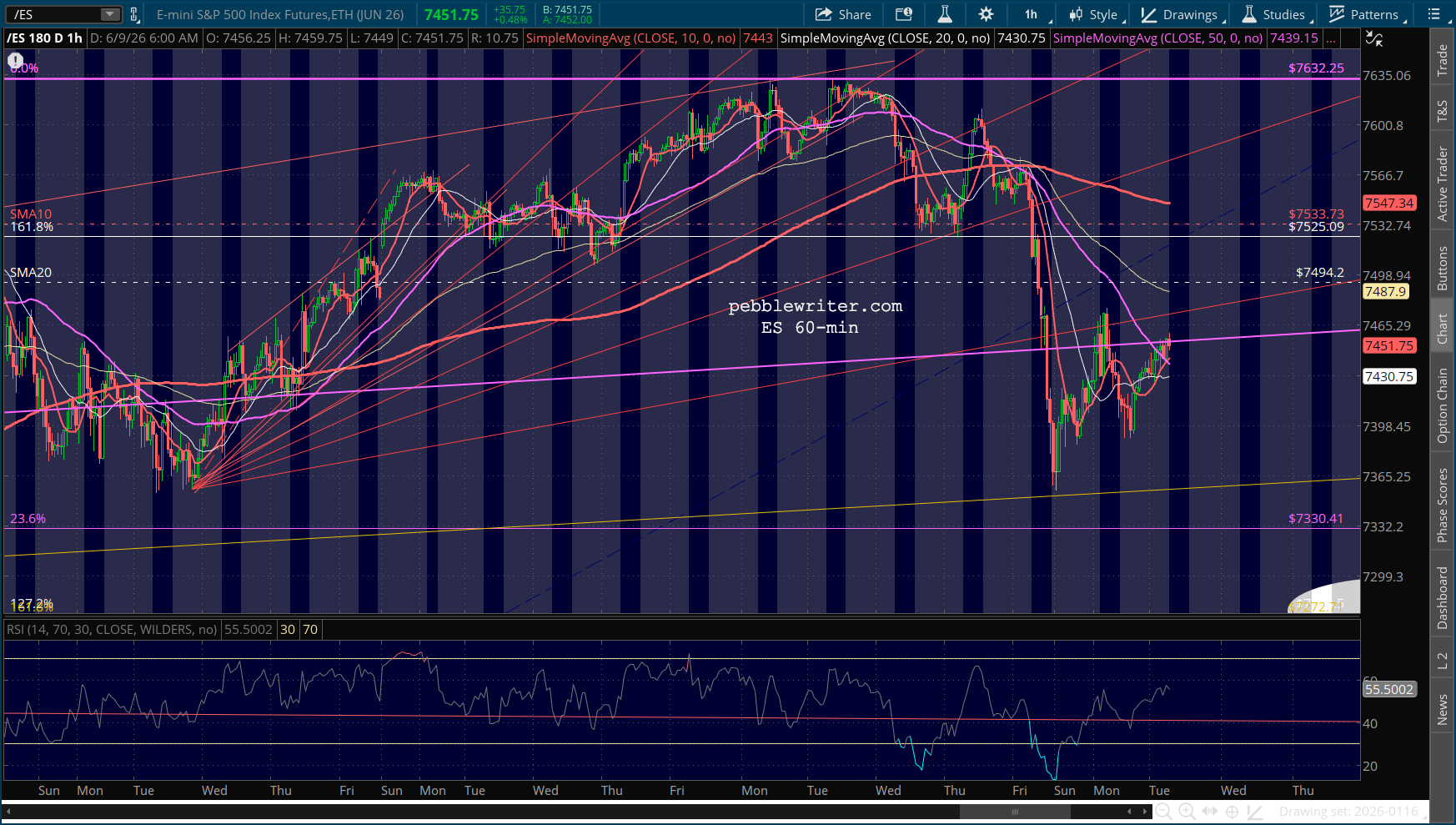

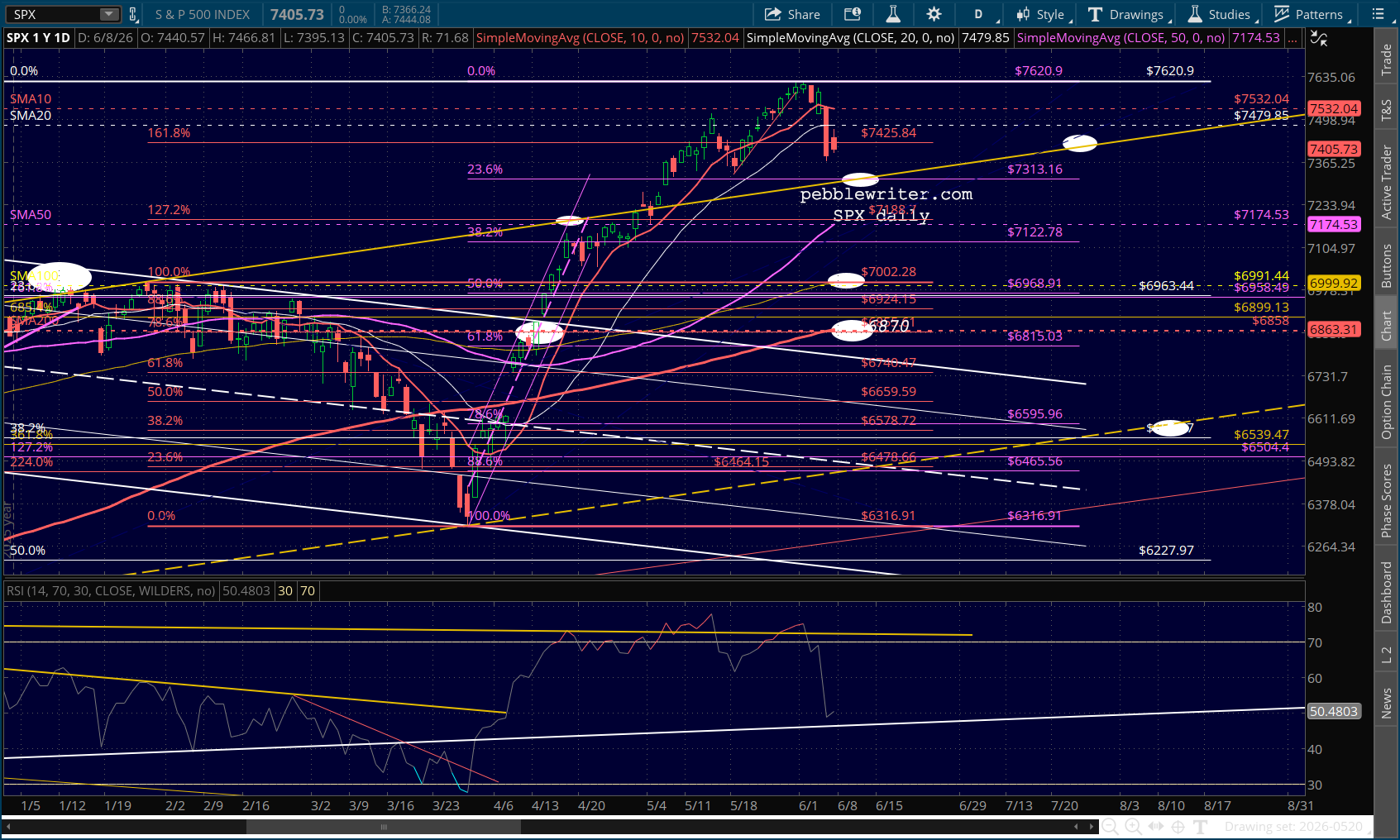

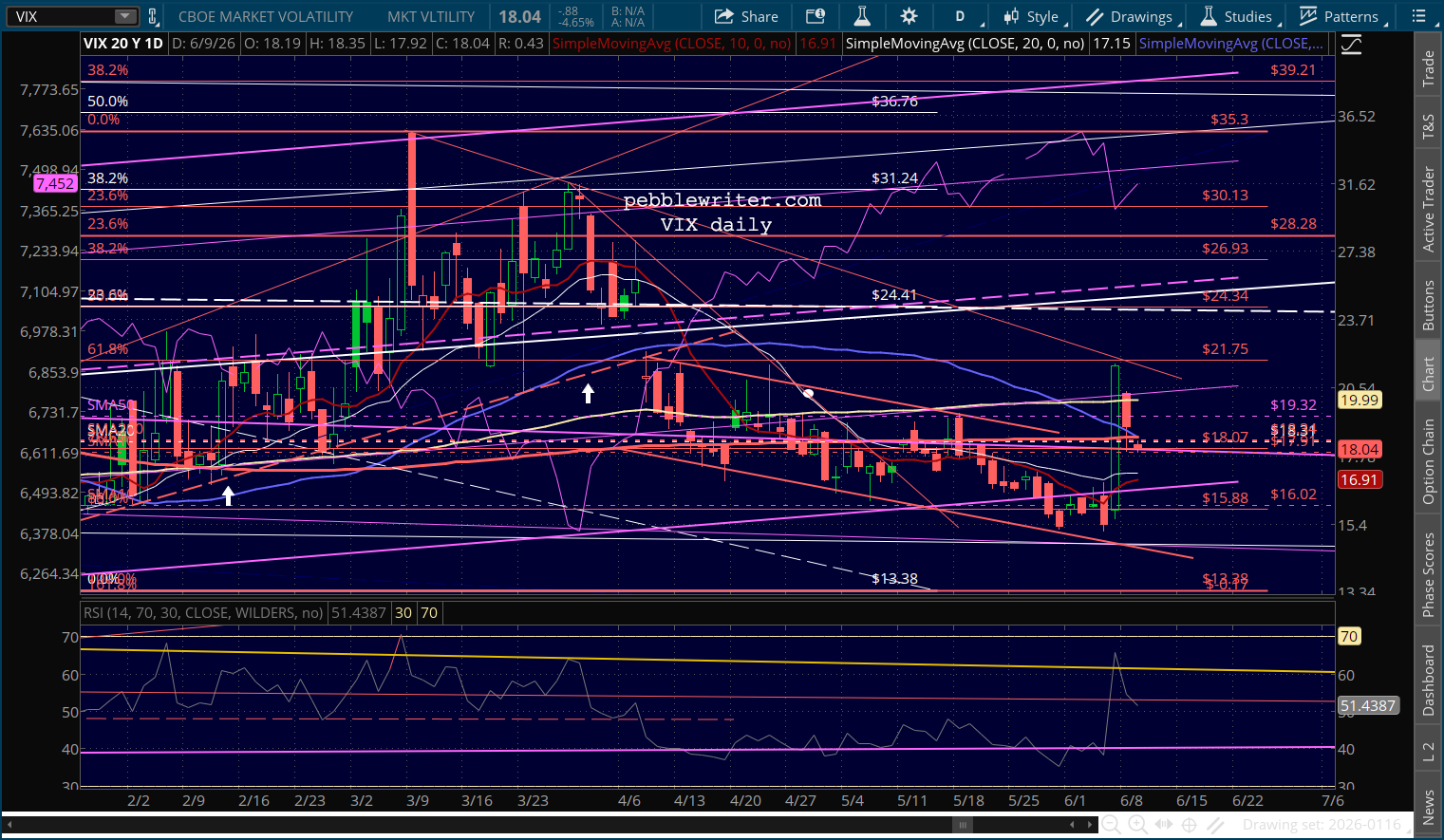

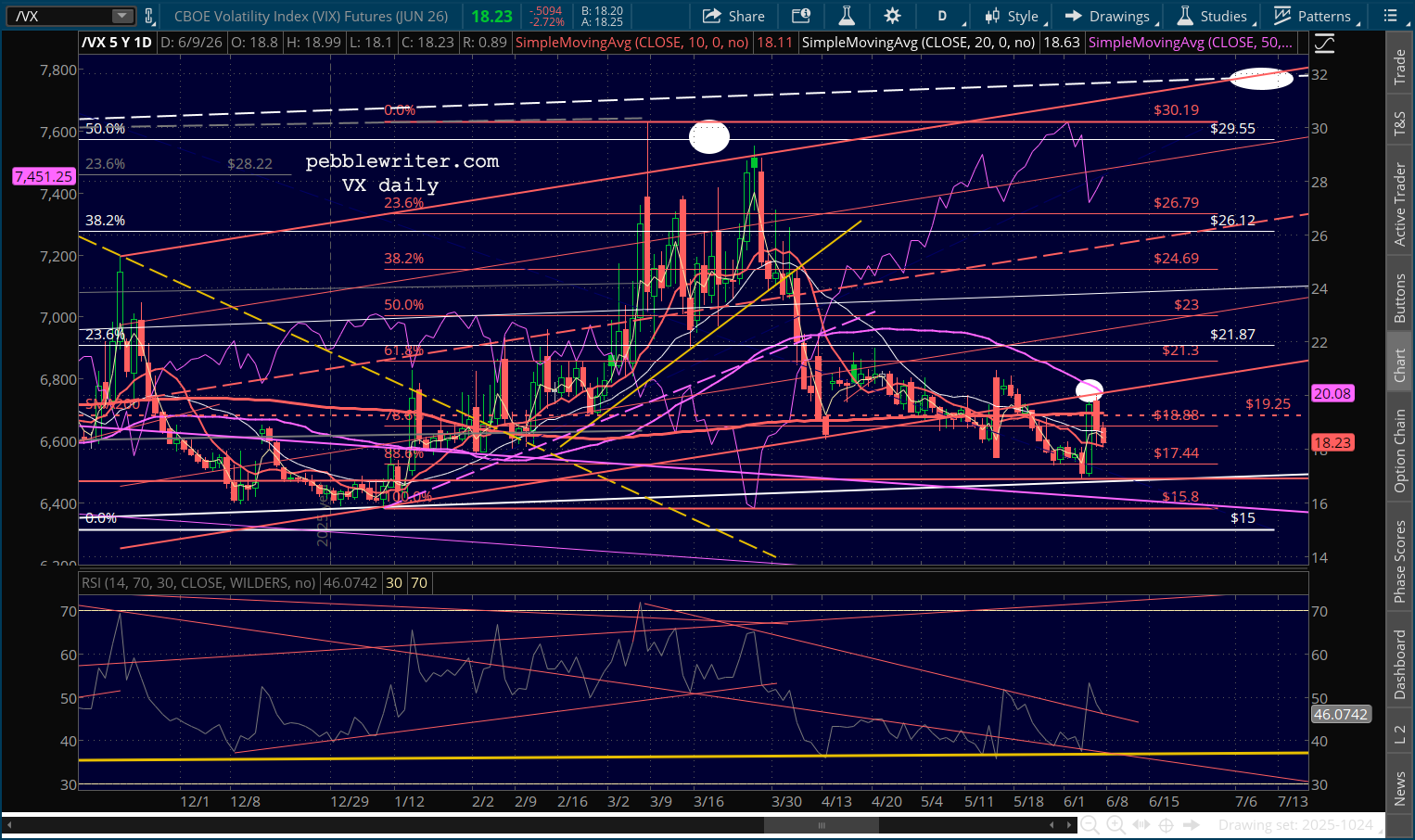

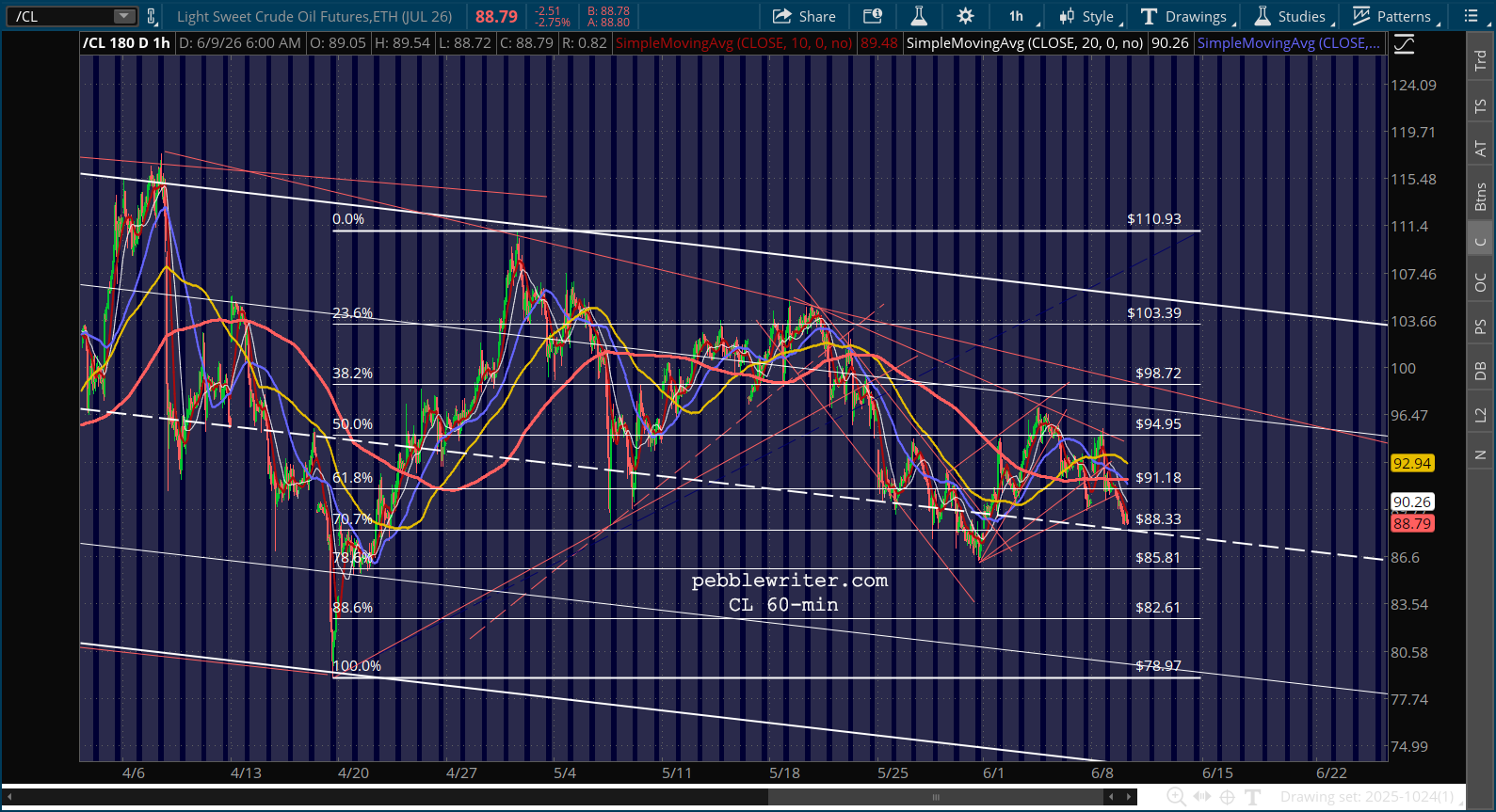

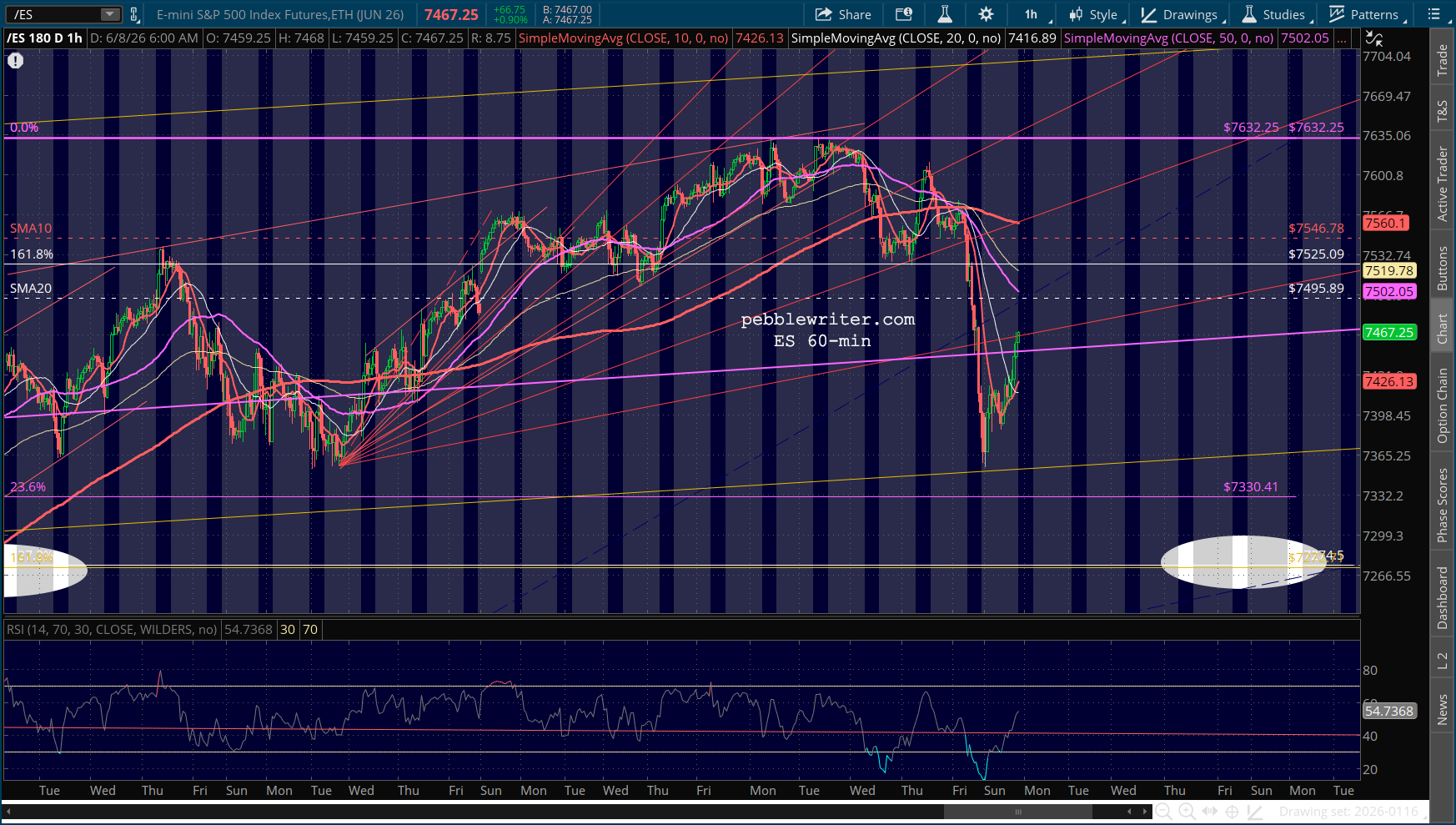

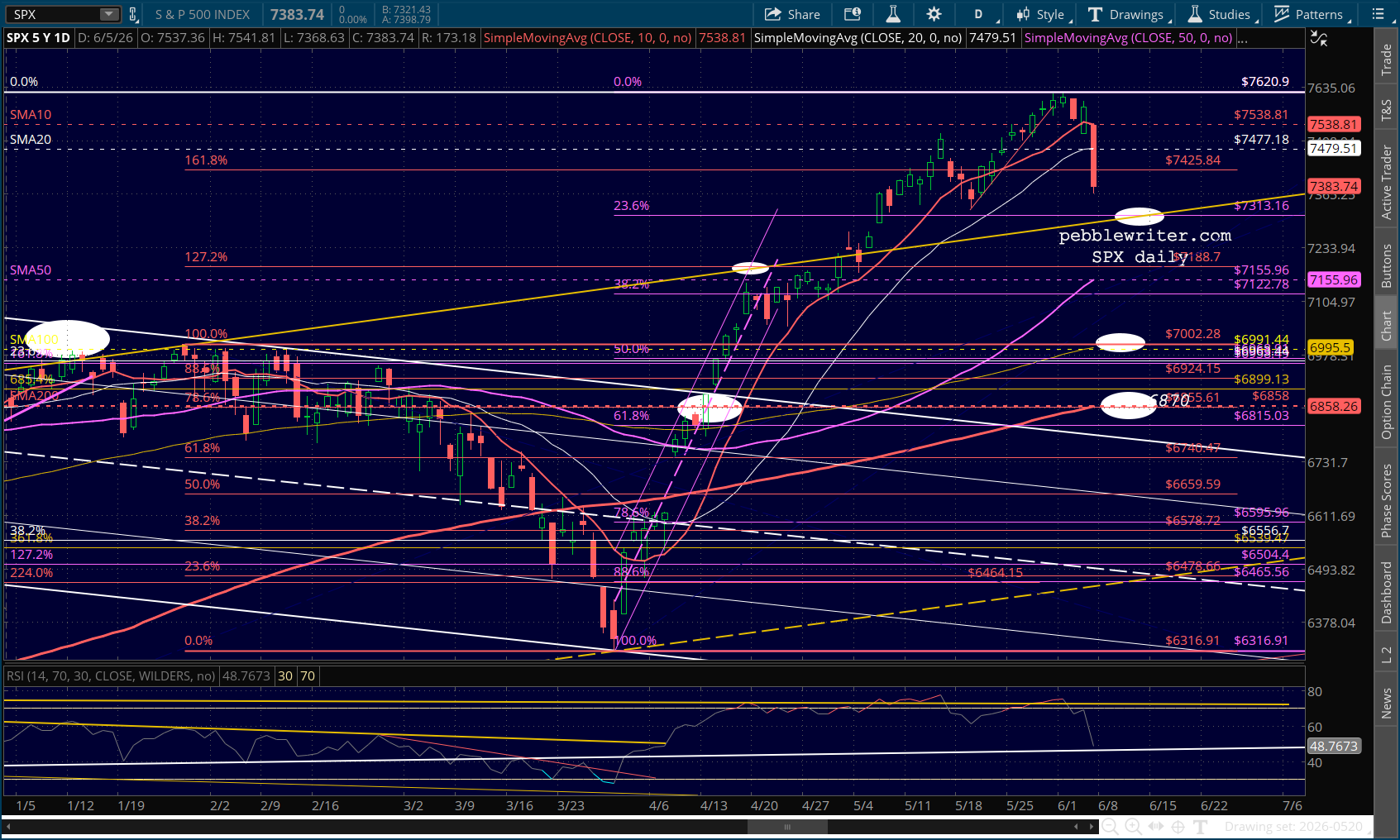

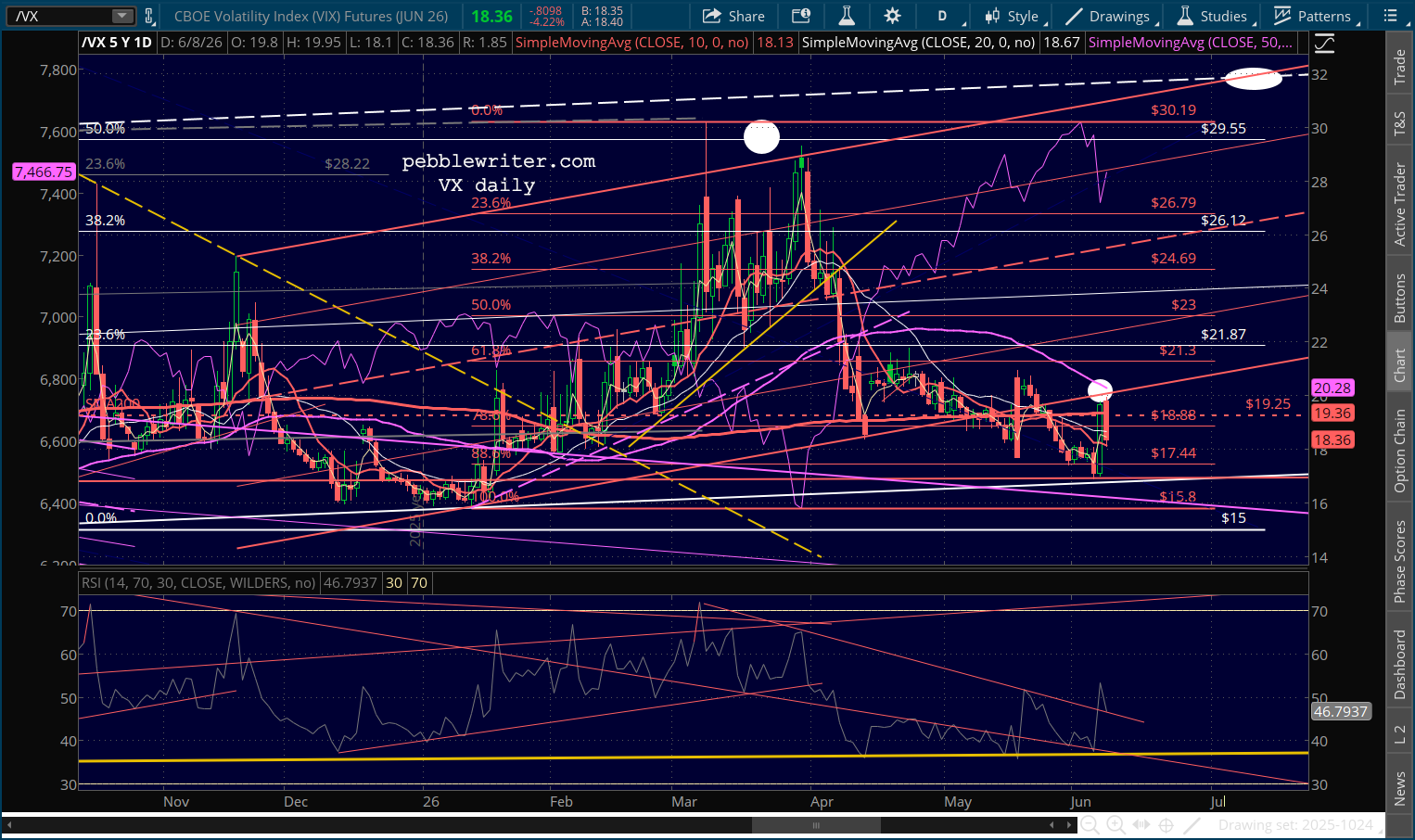

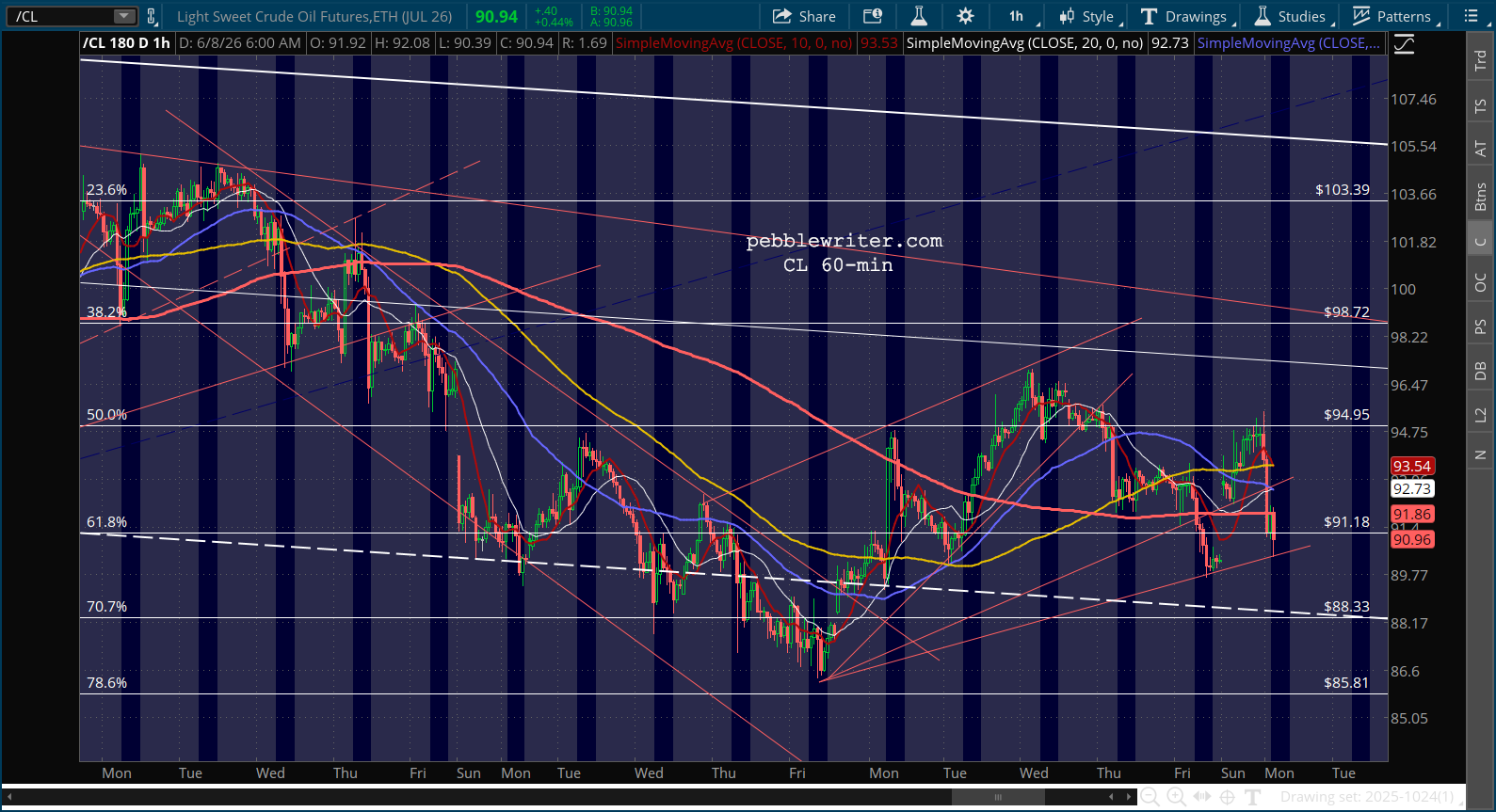

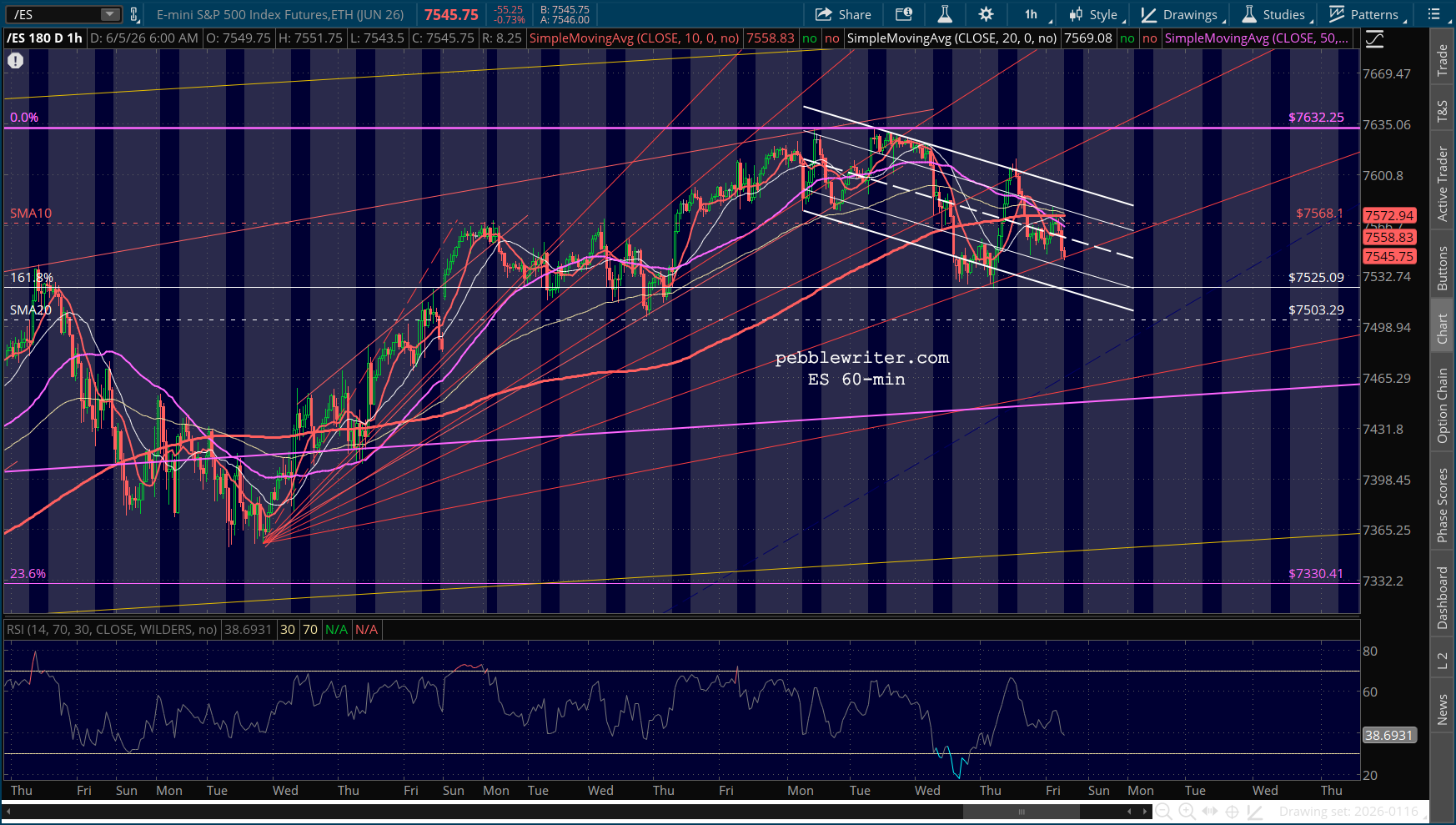

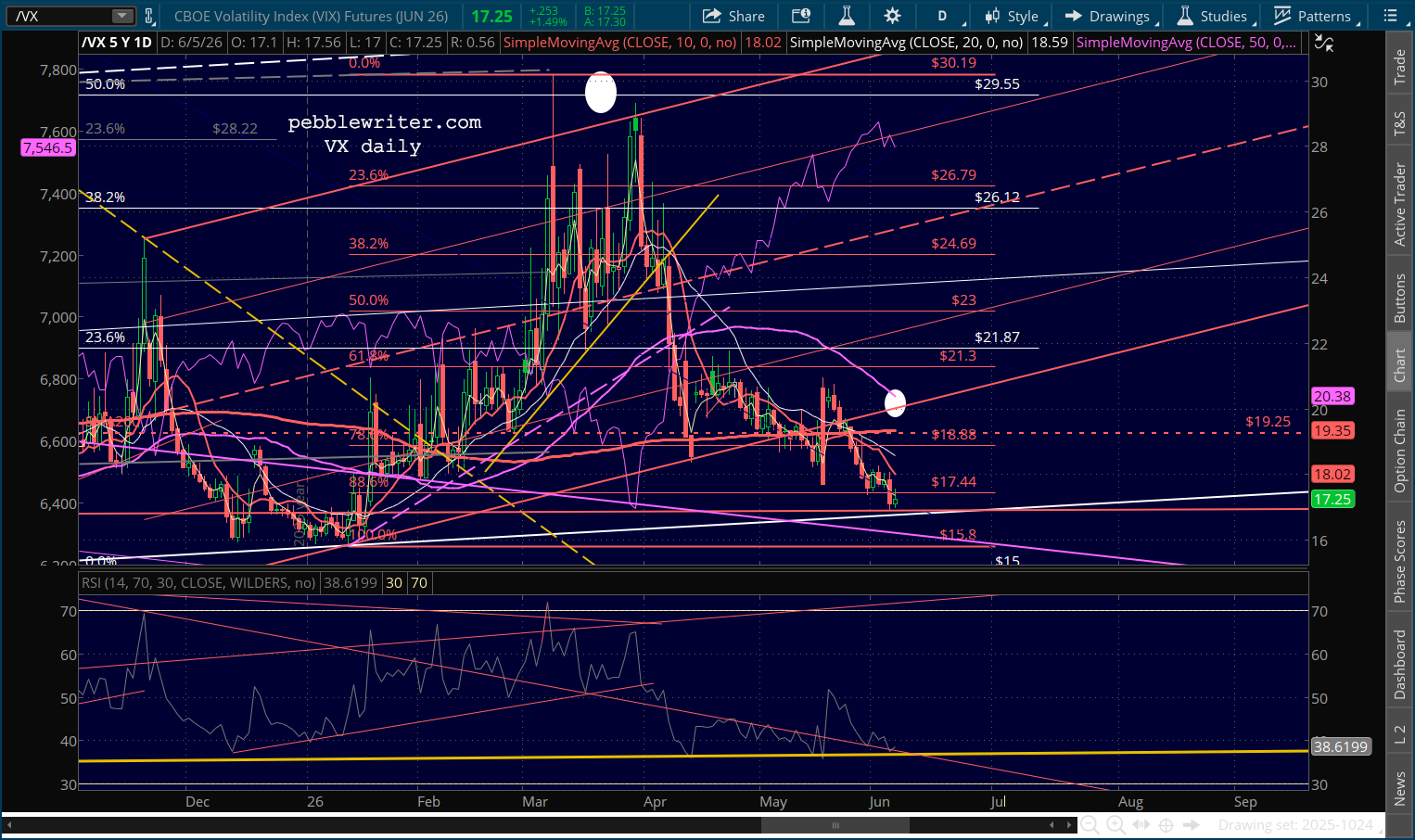

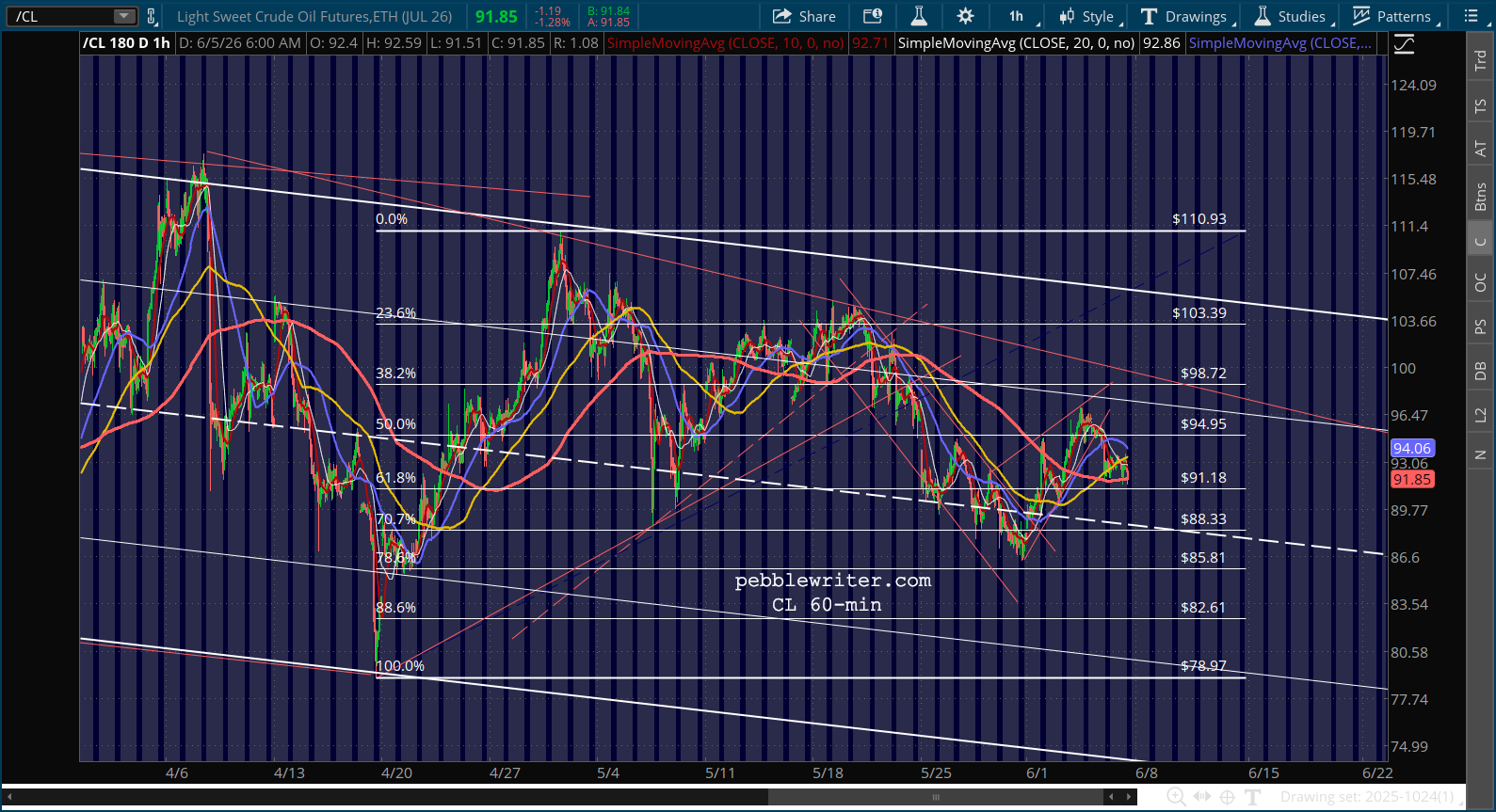

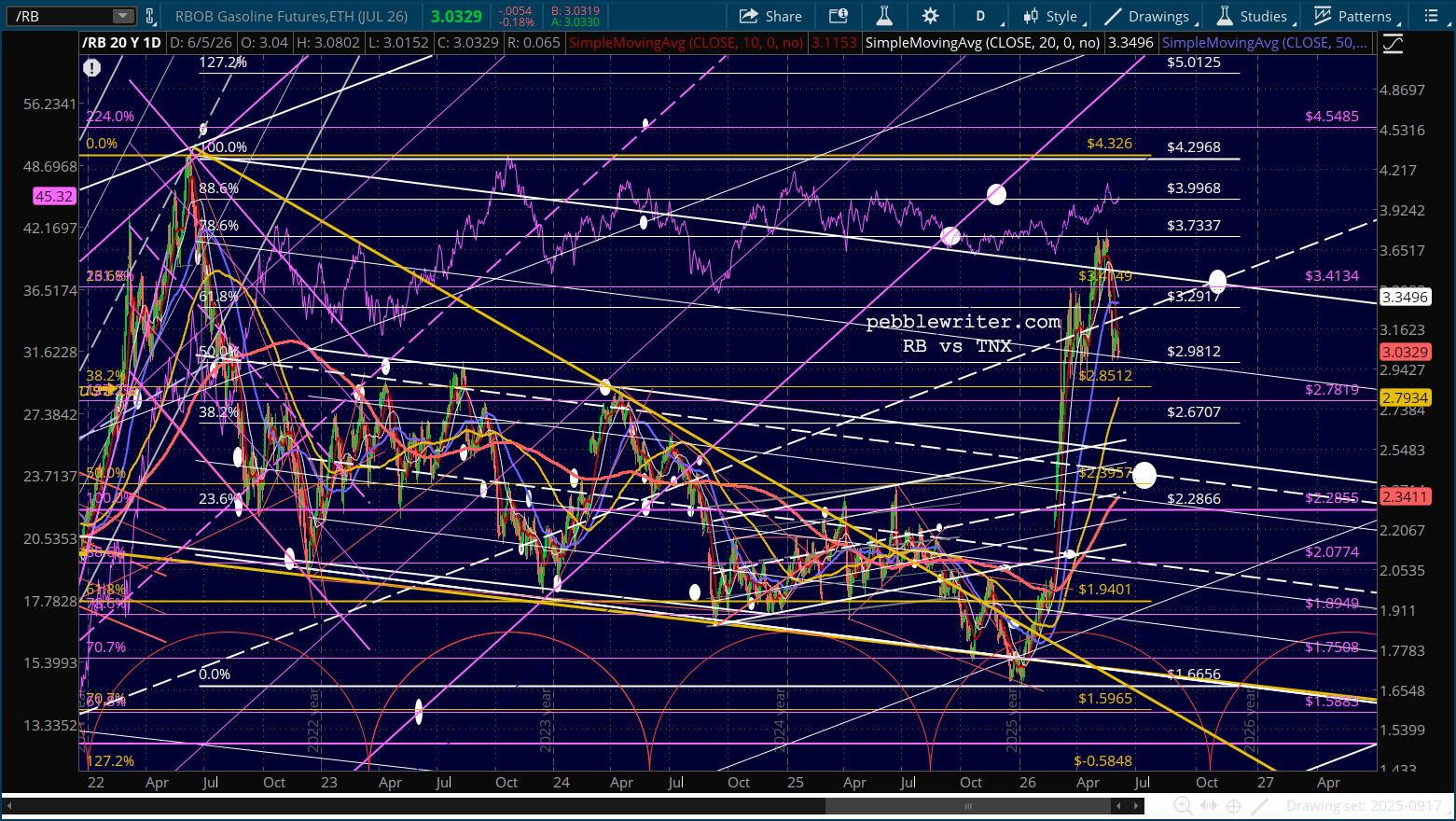

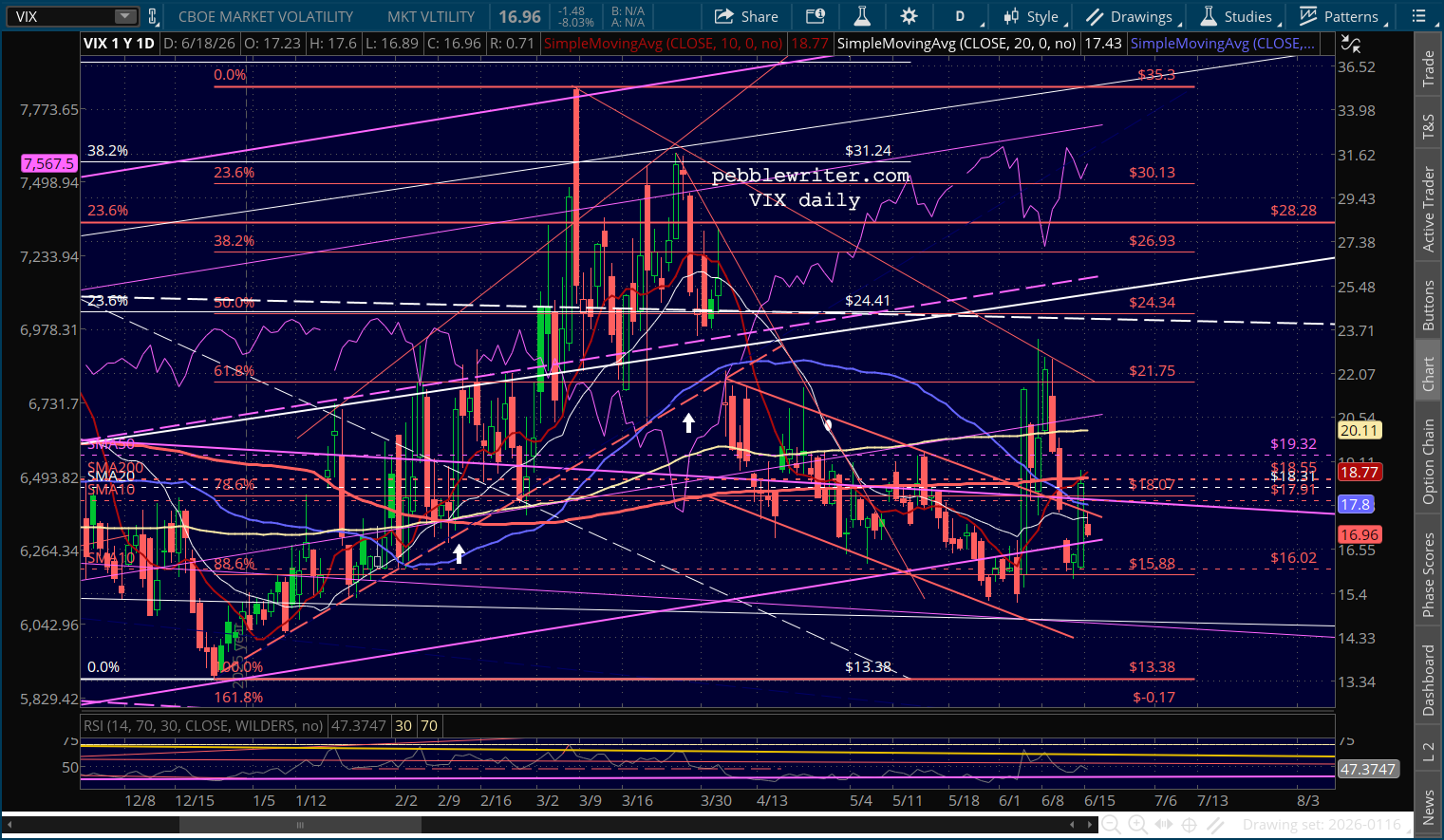

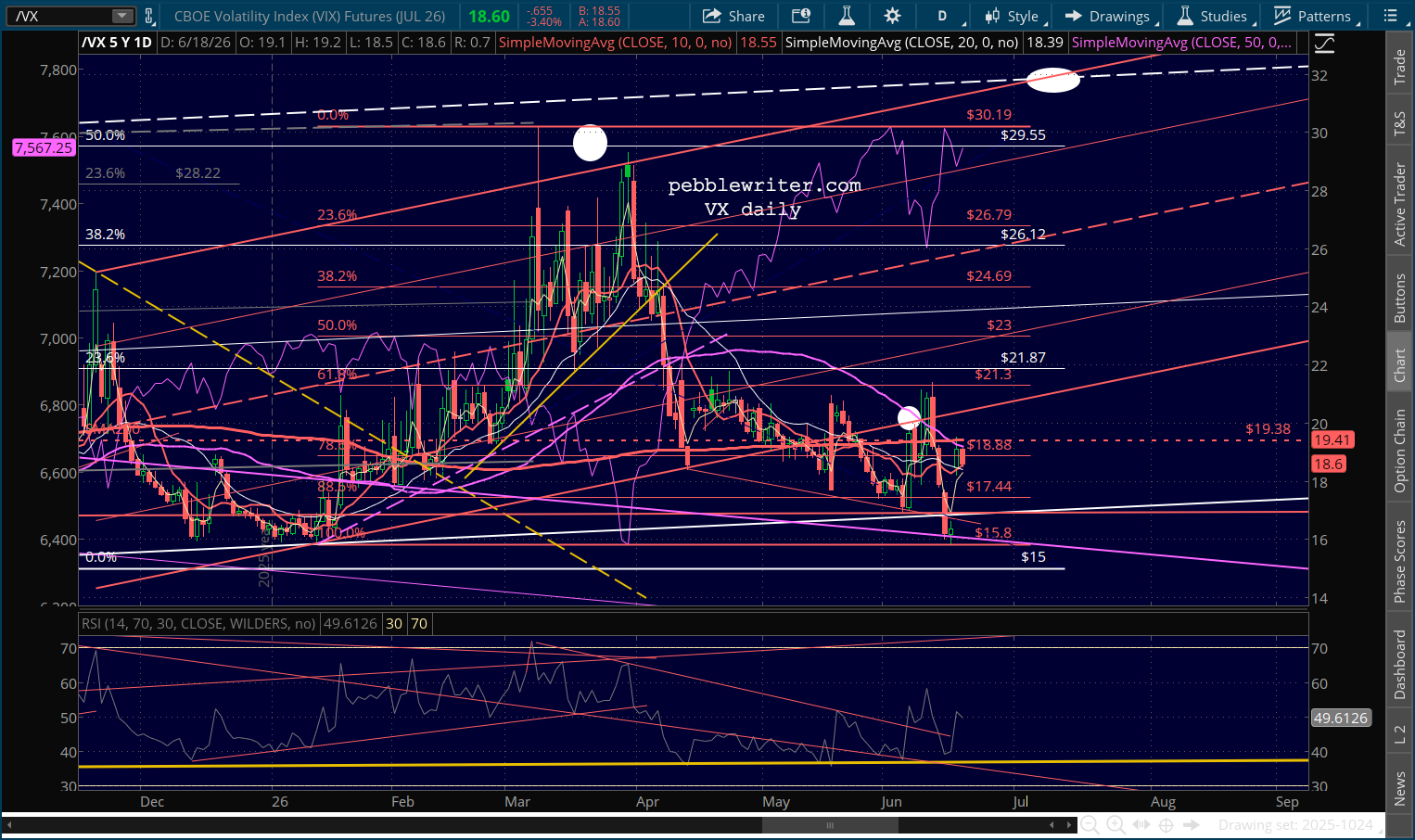

Anyone who watched Kevin Warsh’s hawkish comments about taming inflation yesterday is right to be skeptical about the market’s overnight action. It has everything to do with VIX/VX reversing at their SMA200s and oil slipping down to tag its SMA200 and very little to do with the substance of his comments.

Of course, Trump knew what was coming. Why else would he accelerate the signing of his deal with Iran, which even the Republicans are criticizing. Trump flat out admitted to the rationale behind the artless deal:

“I didn’t want to see economic catastrophe. If you kept this going, that could have happened…All I know is every time we talked about the possibility of peace, the stock market shot up like a rocket ship, Every time we said something negative, like, guess what, we’re not going to be able to settle, it would go down very big.”

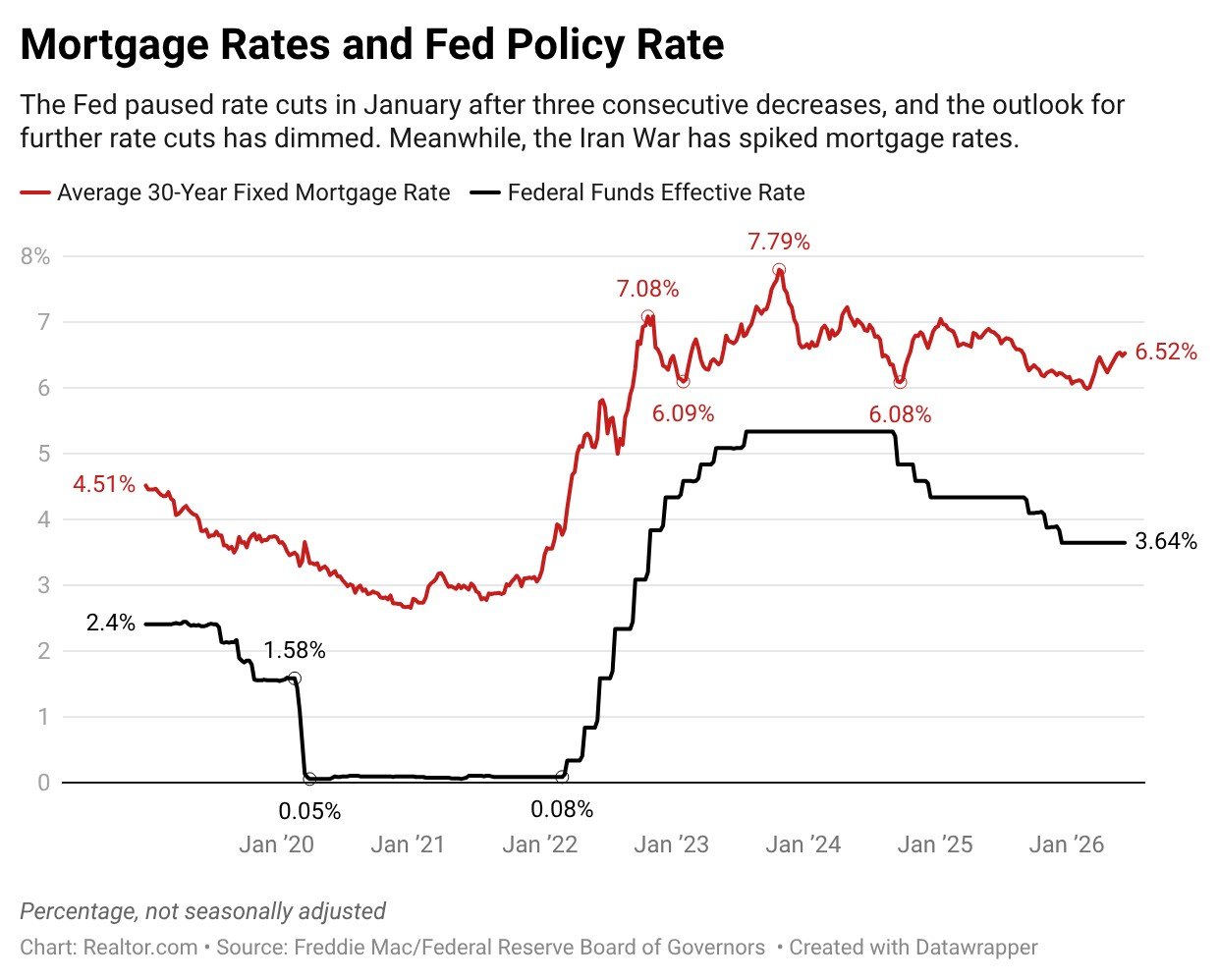

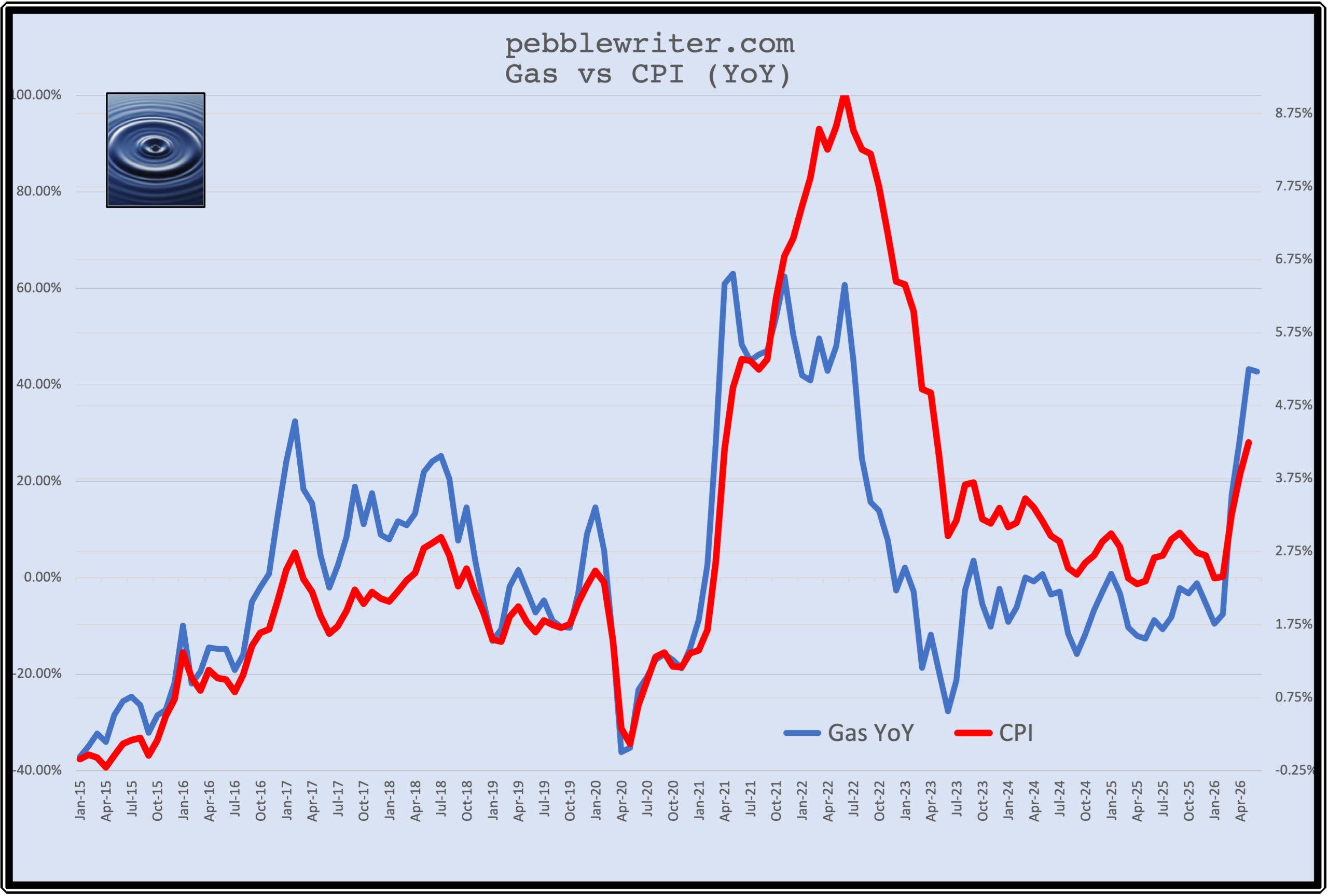

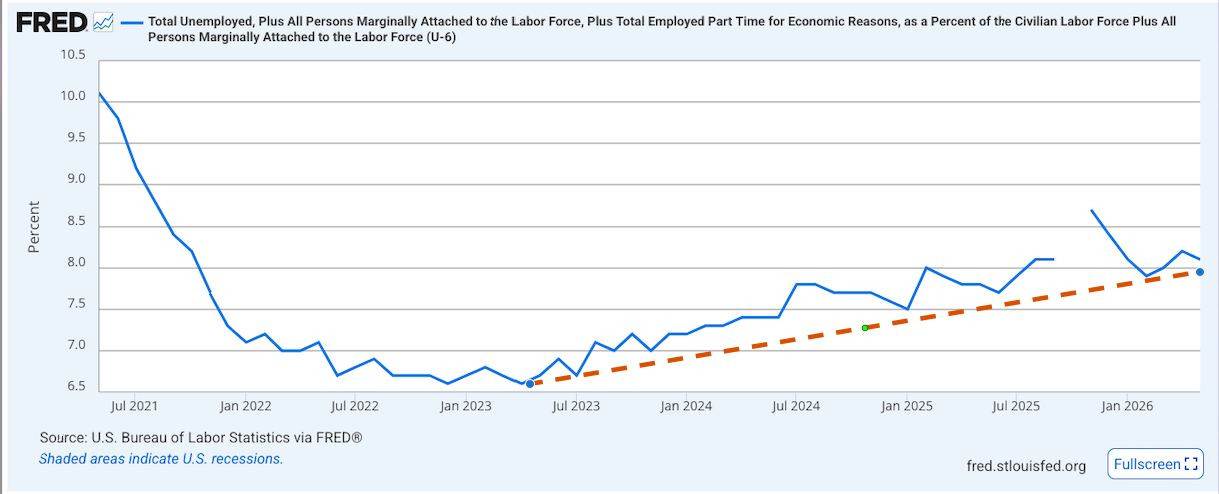

The Fed is unconcerned at this time about any economic weakness, but is very concerned about inflation which has remained above target for over five years. Even though gas price-driven CPI likely topped out in May at 4.25%, we’ve seen in the past that other expense categories (flights, groceries, consumer goods, etc.) can ramp up for several months afterwards. So, 4.25% might not be the last we see of Trump’s $200 billion “little excursion.”

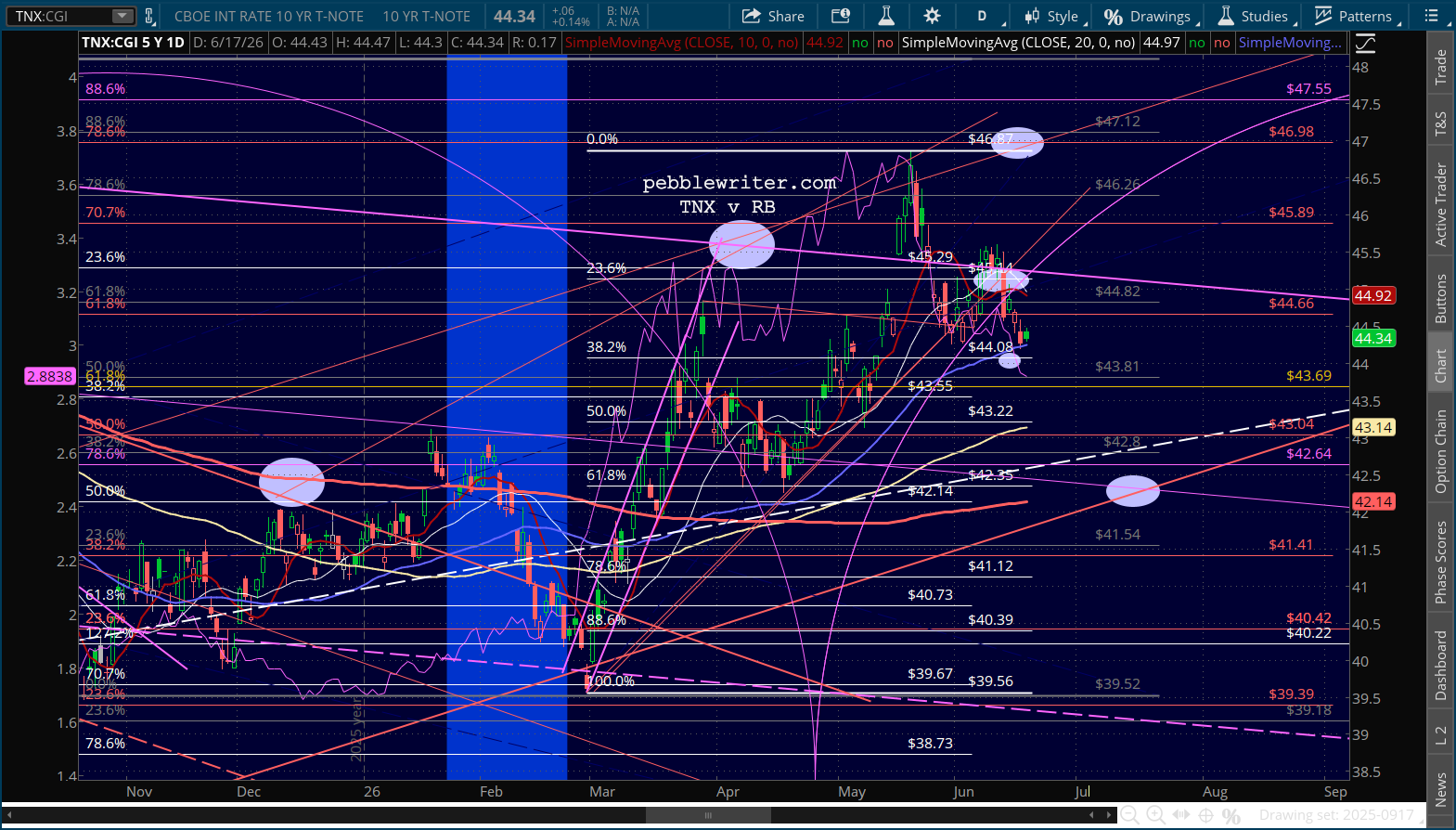

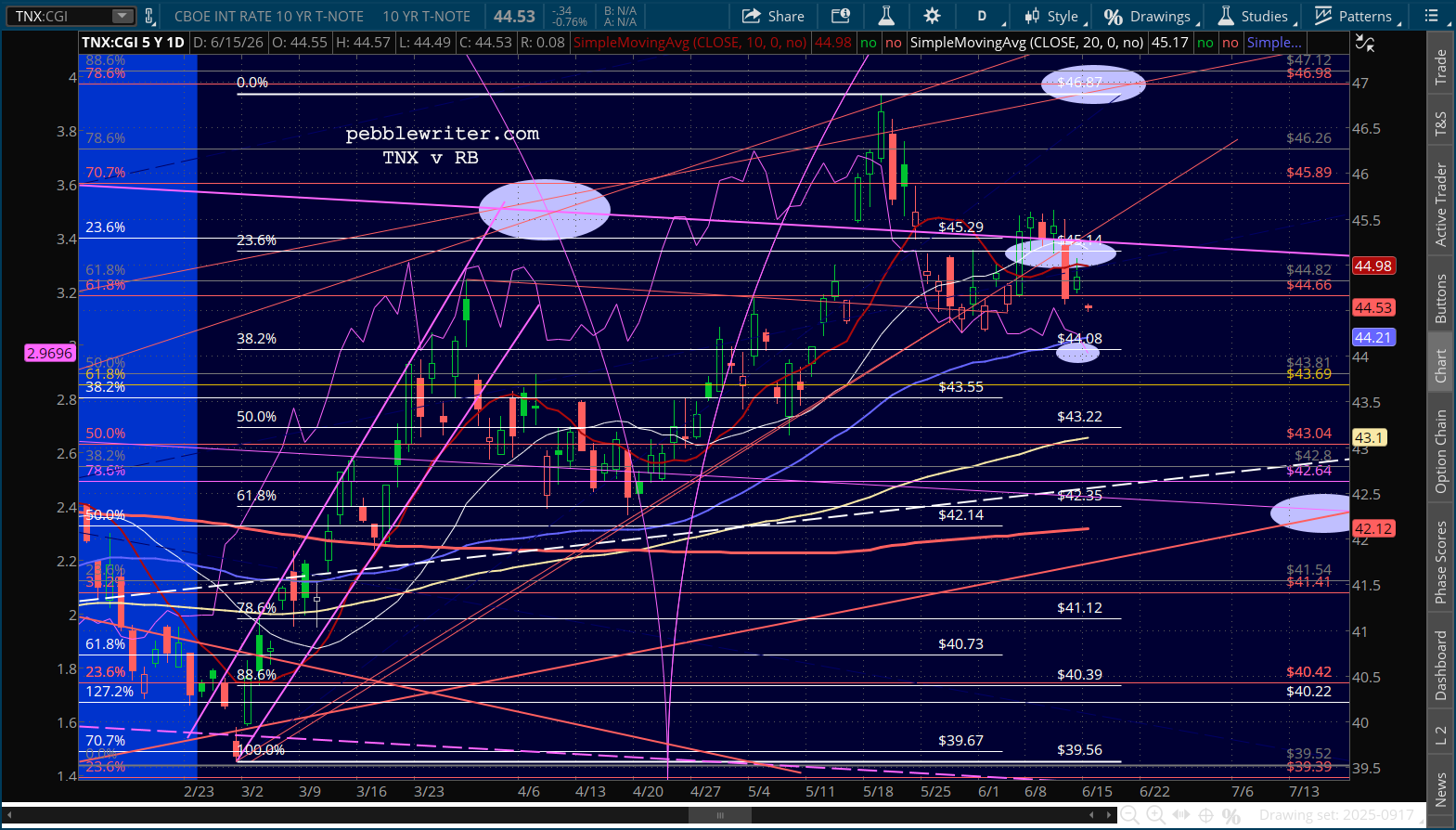

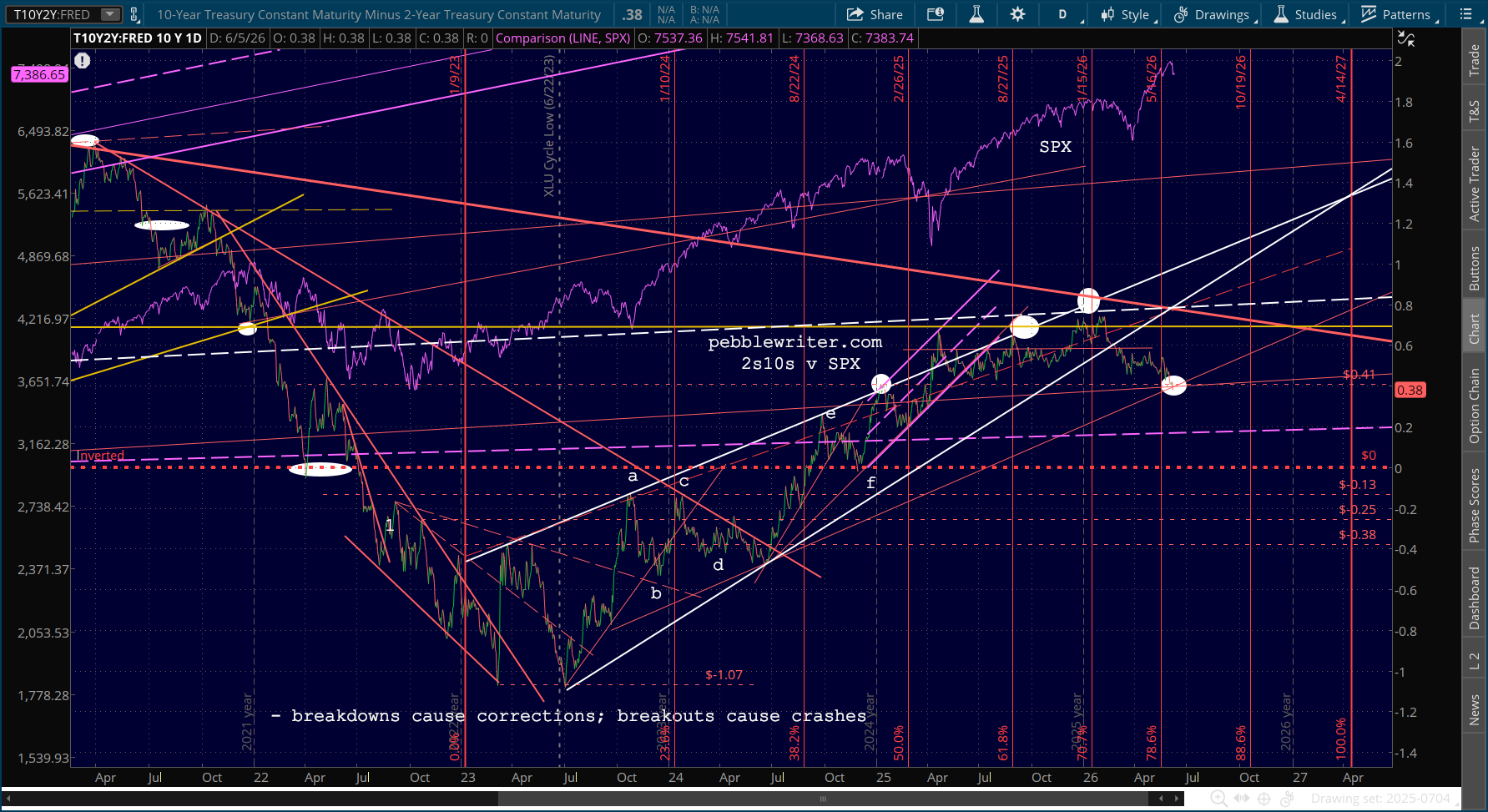

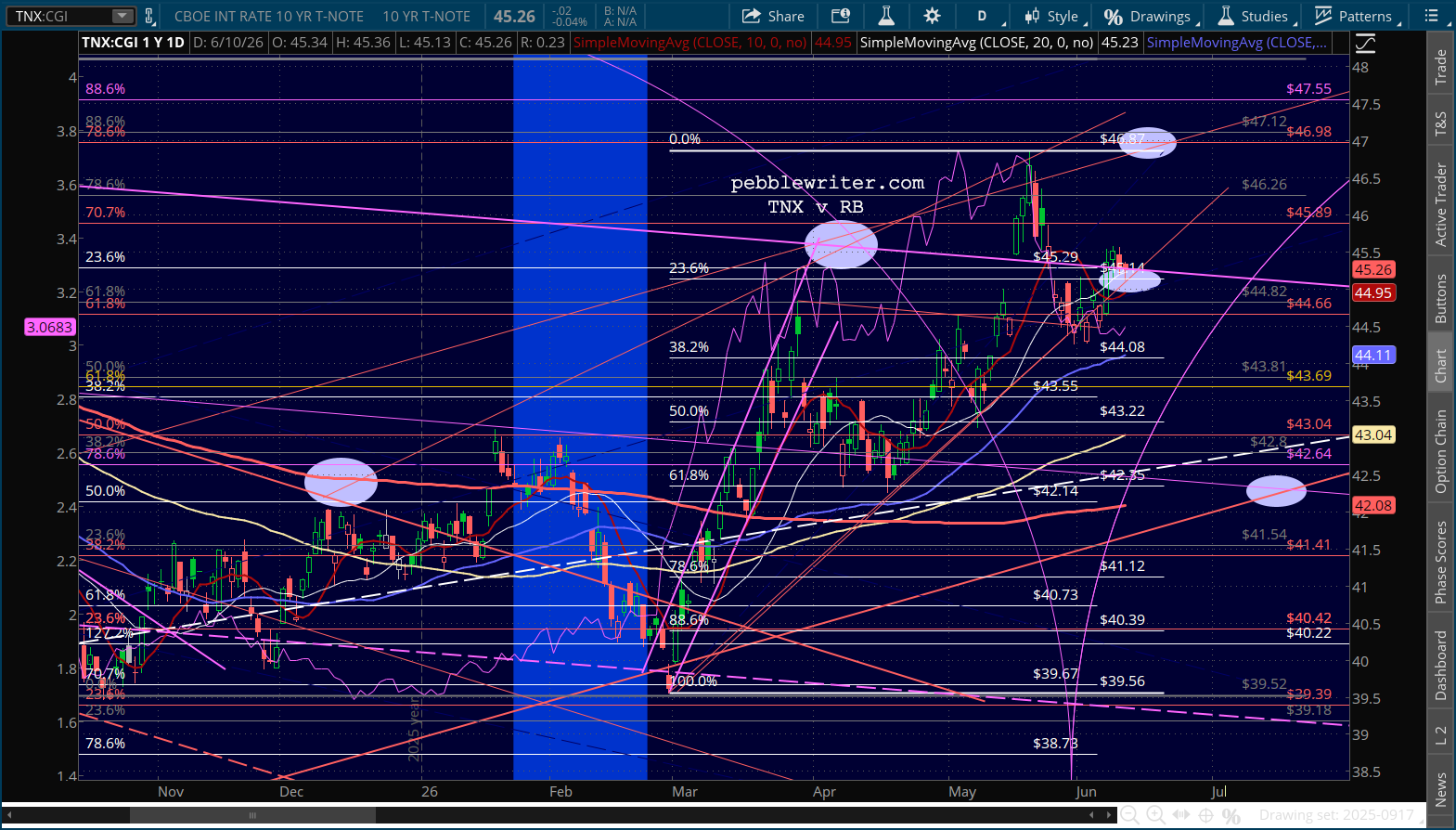

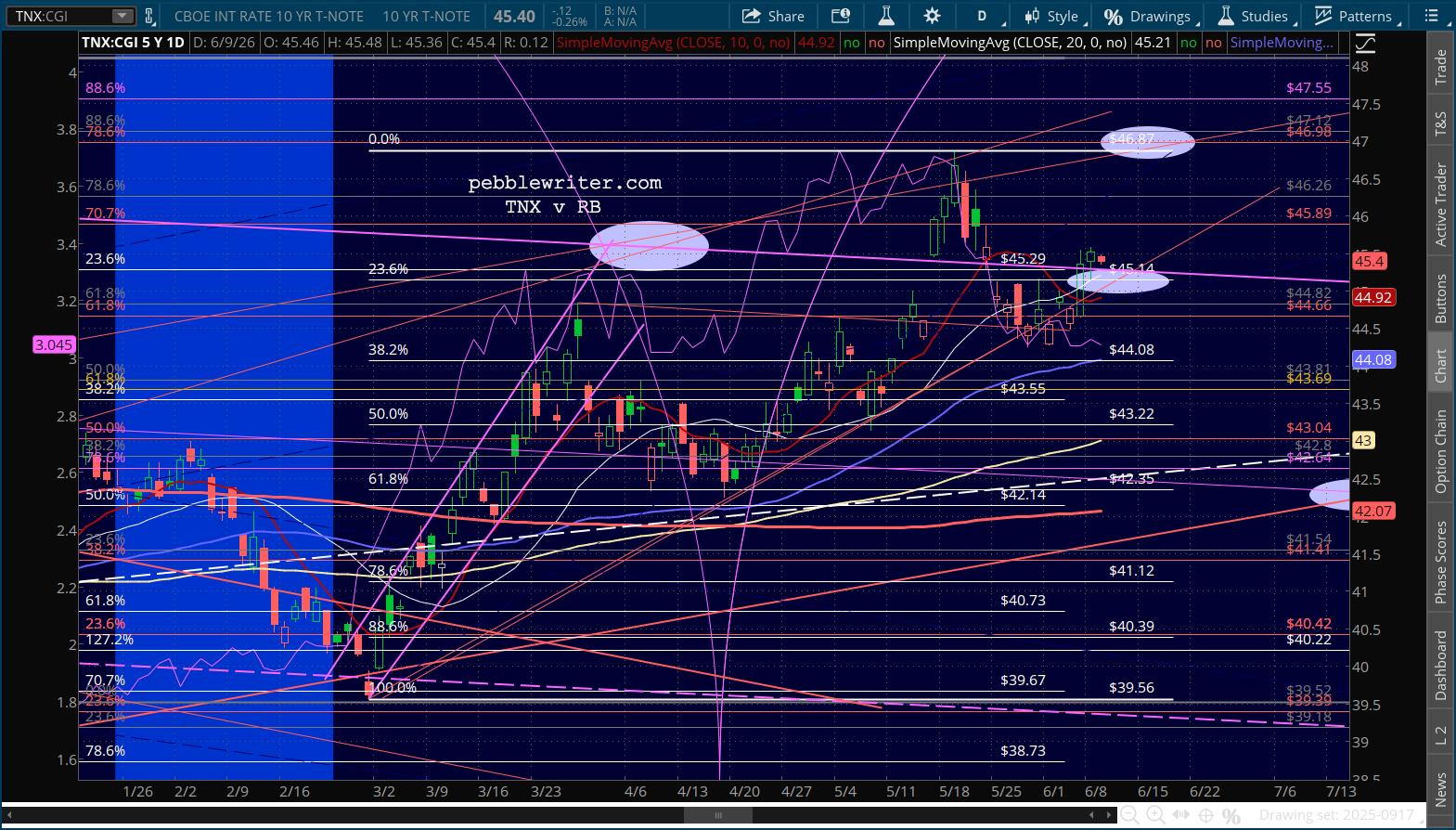

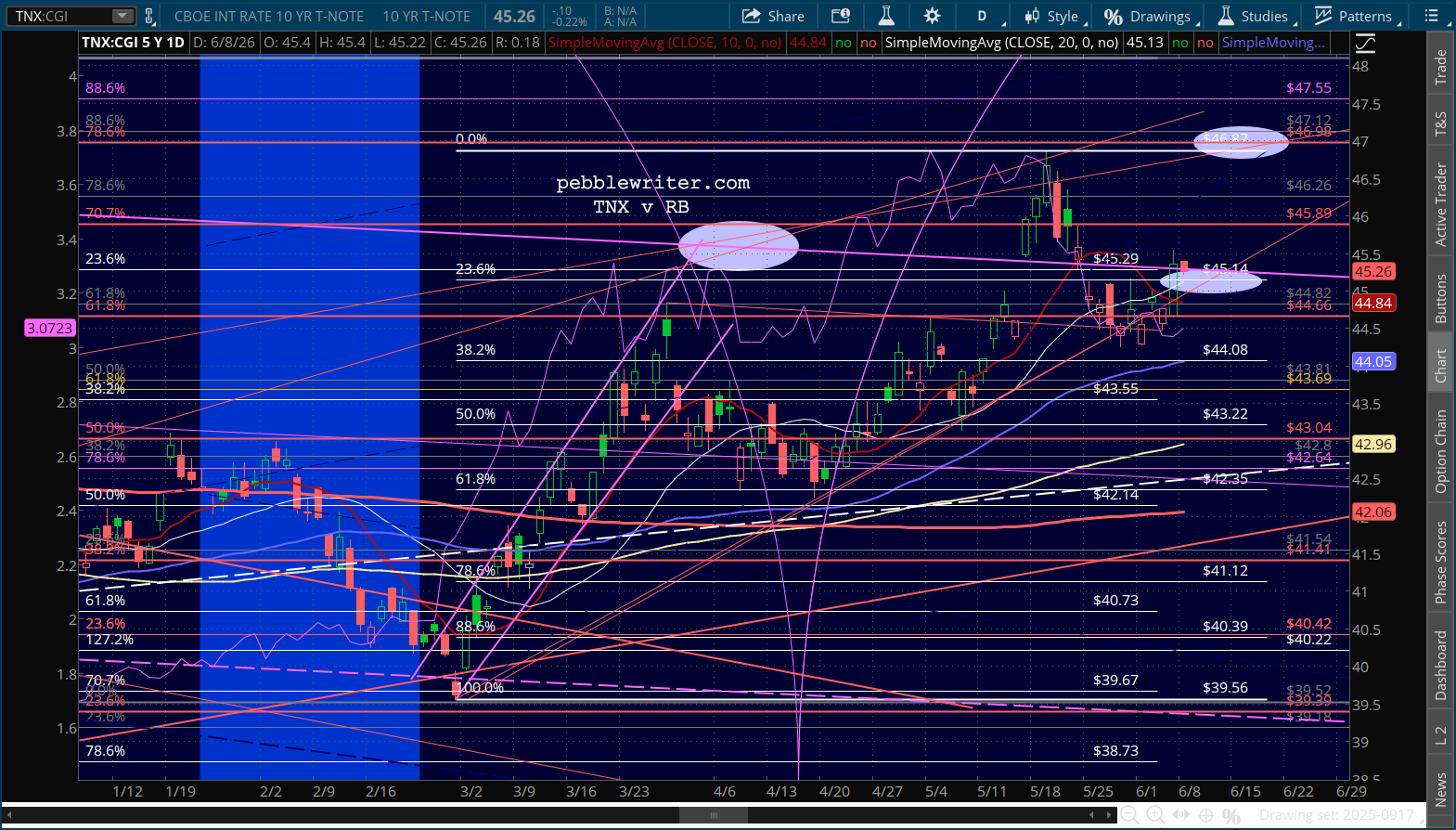

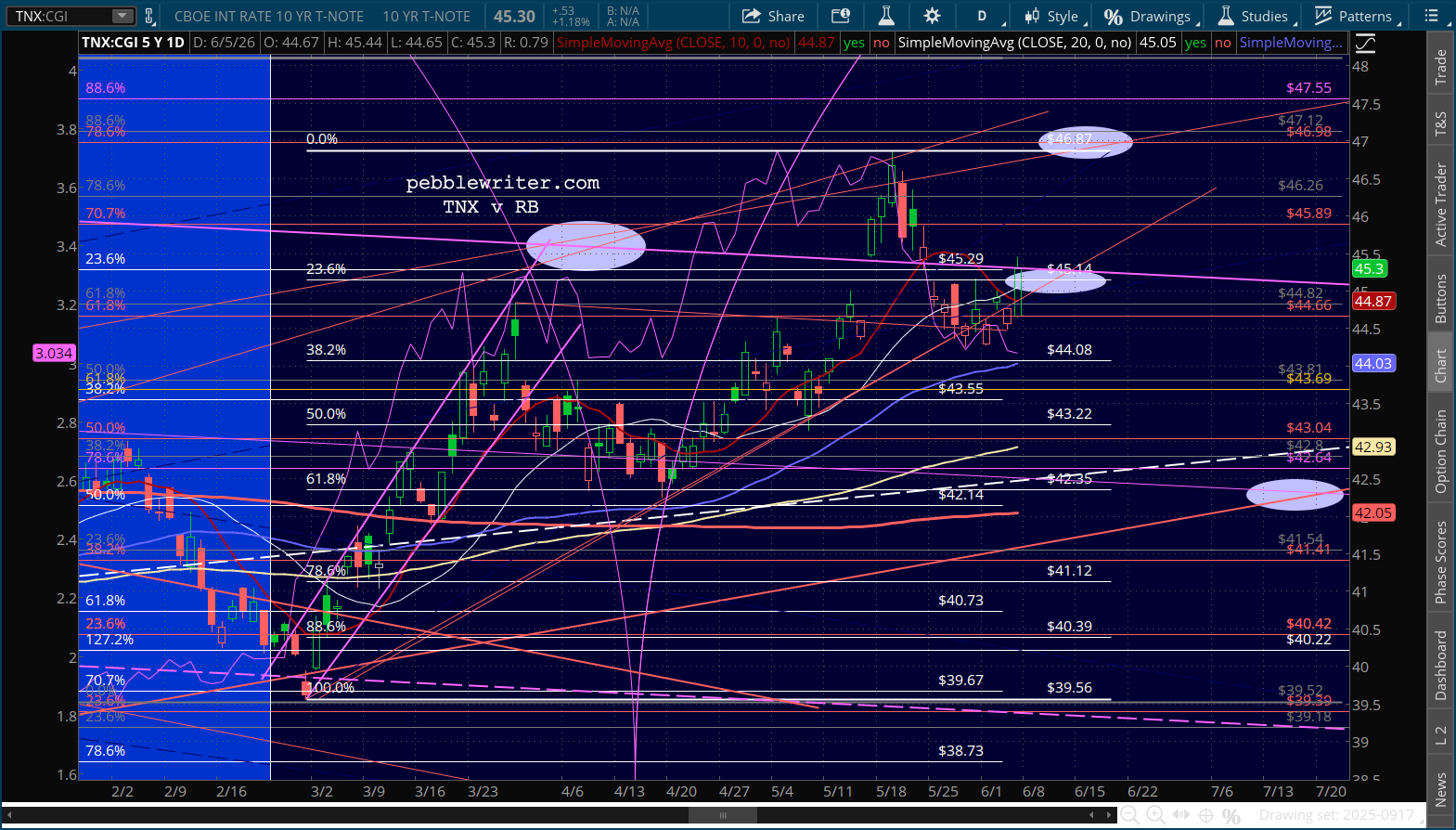

And, don’t forget that the war might well not be over. I suspect that if Iran thinks the Party of Trump is doing a little too well as we cruise into the midterms, there will be plenty of complications with the not-so-artful deal. Although the Fed is feeling hawkish, the 10Y is retreating – maybe some nerves?

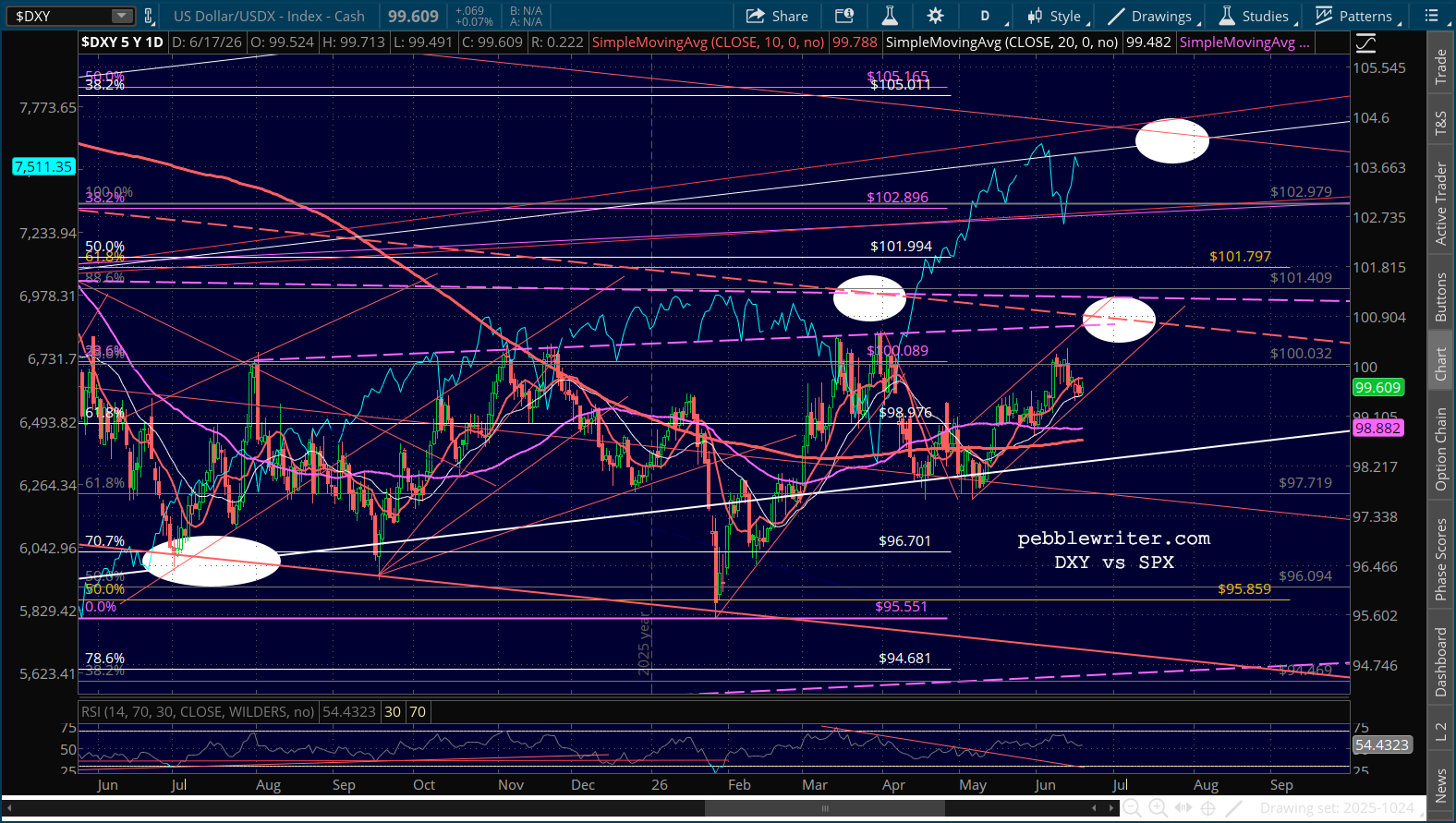

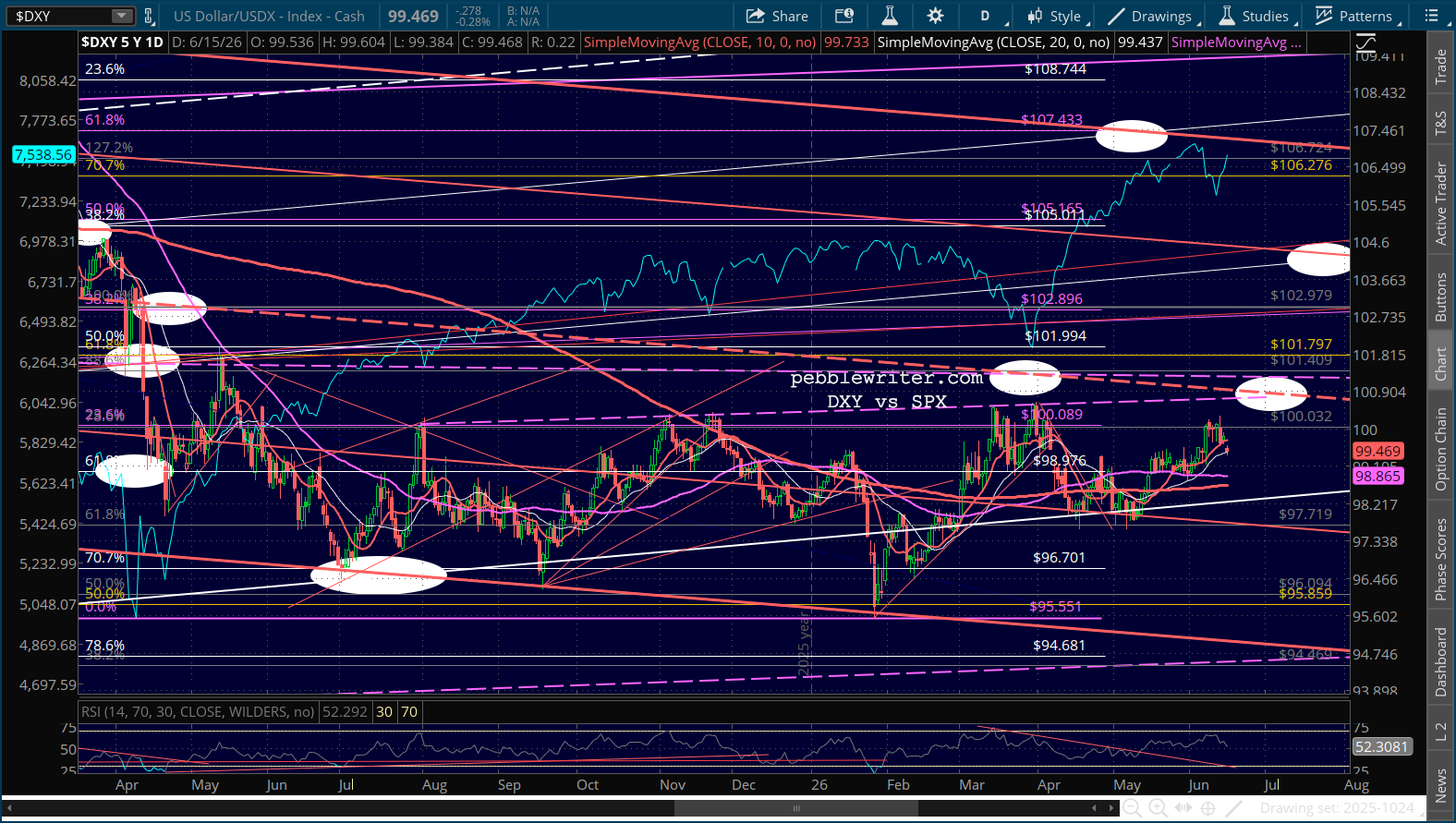

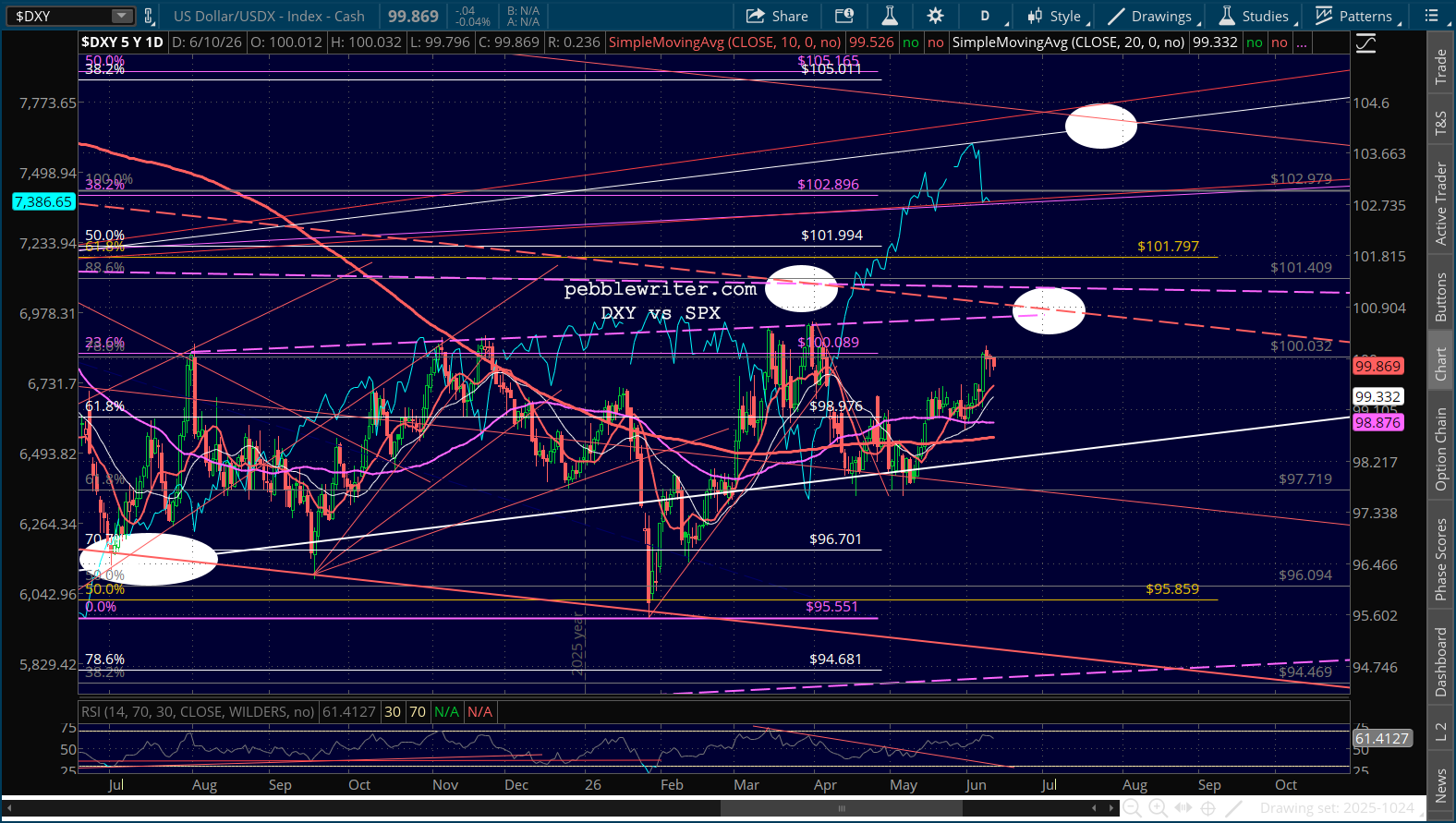

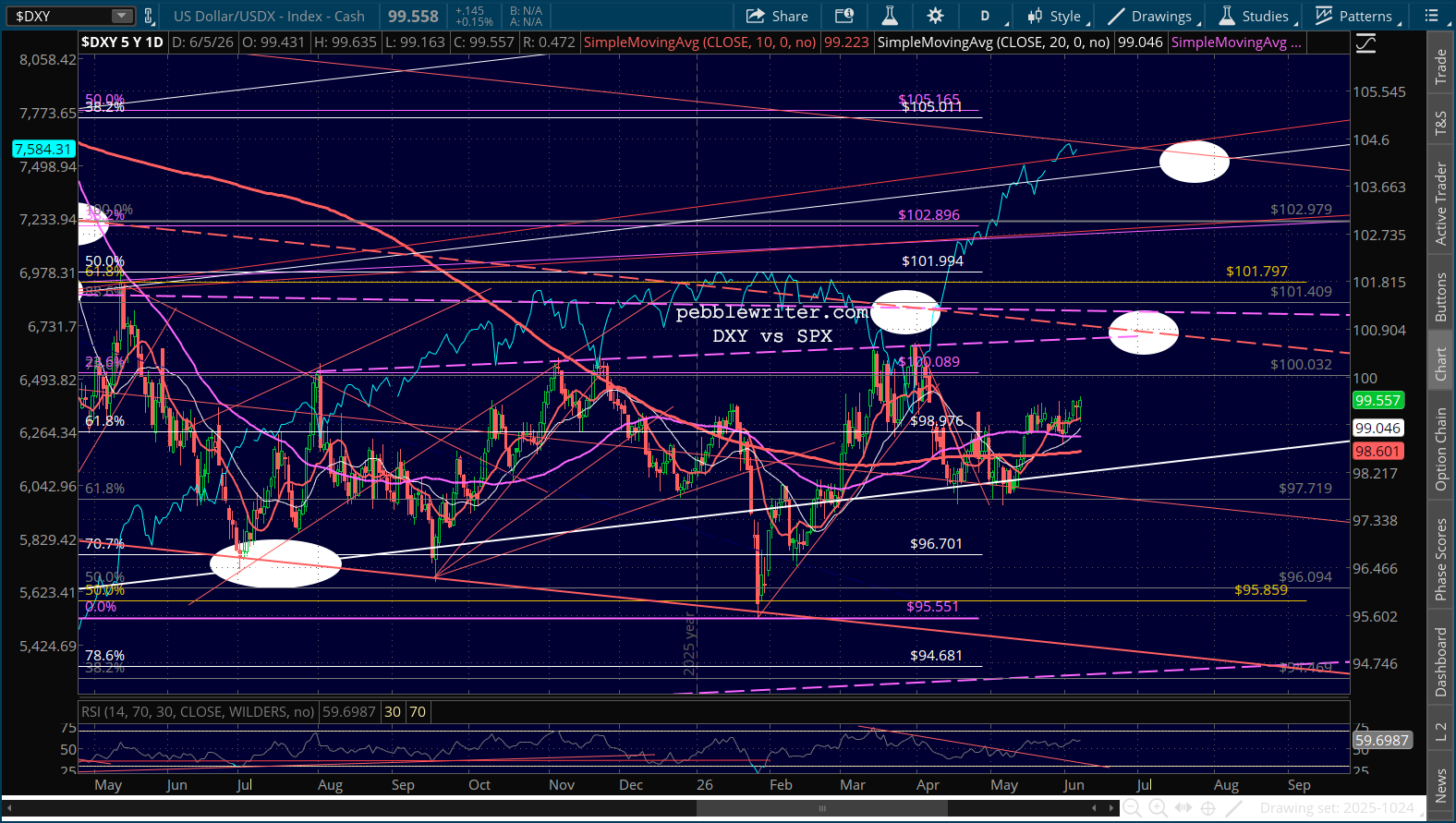

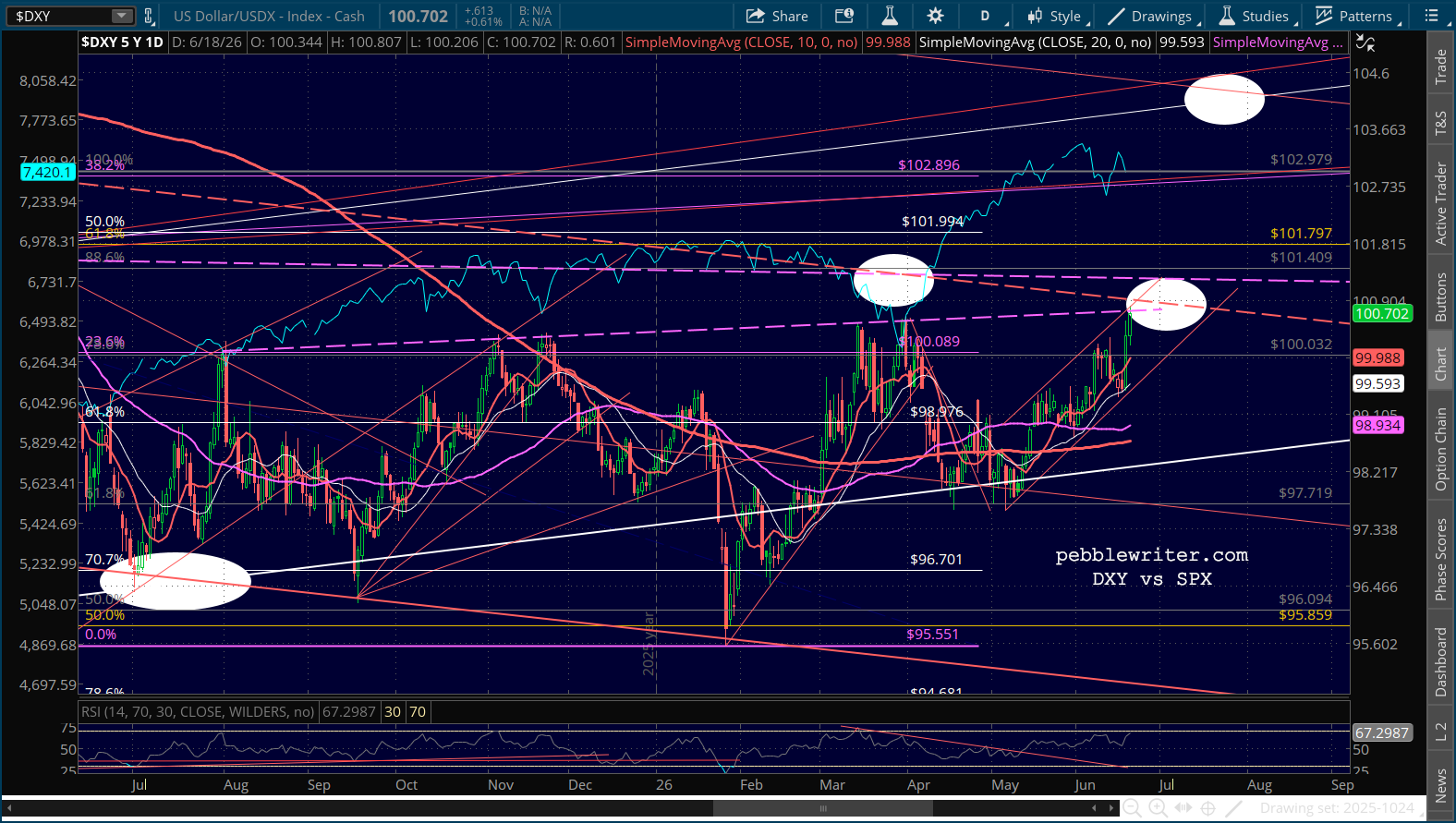

The bulls really need DXY to stop here at our 100.80 target.

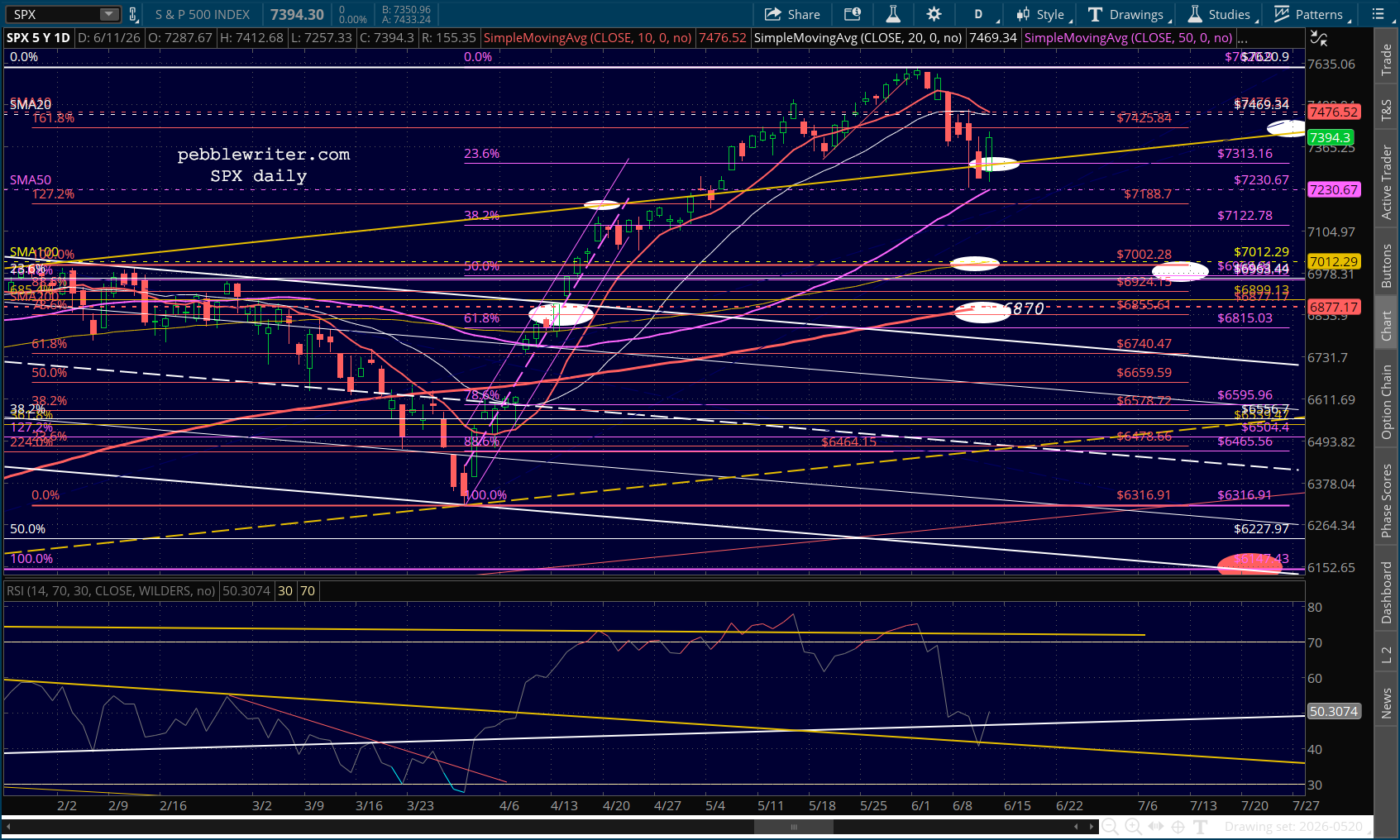

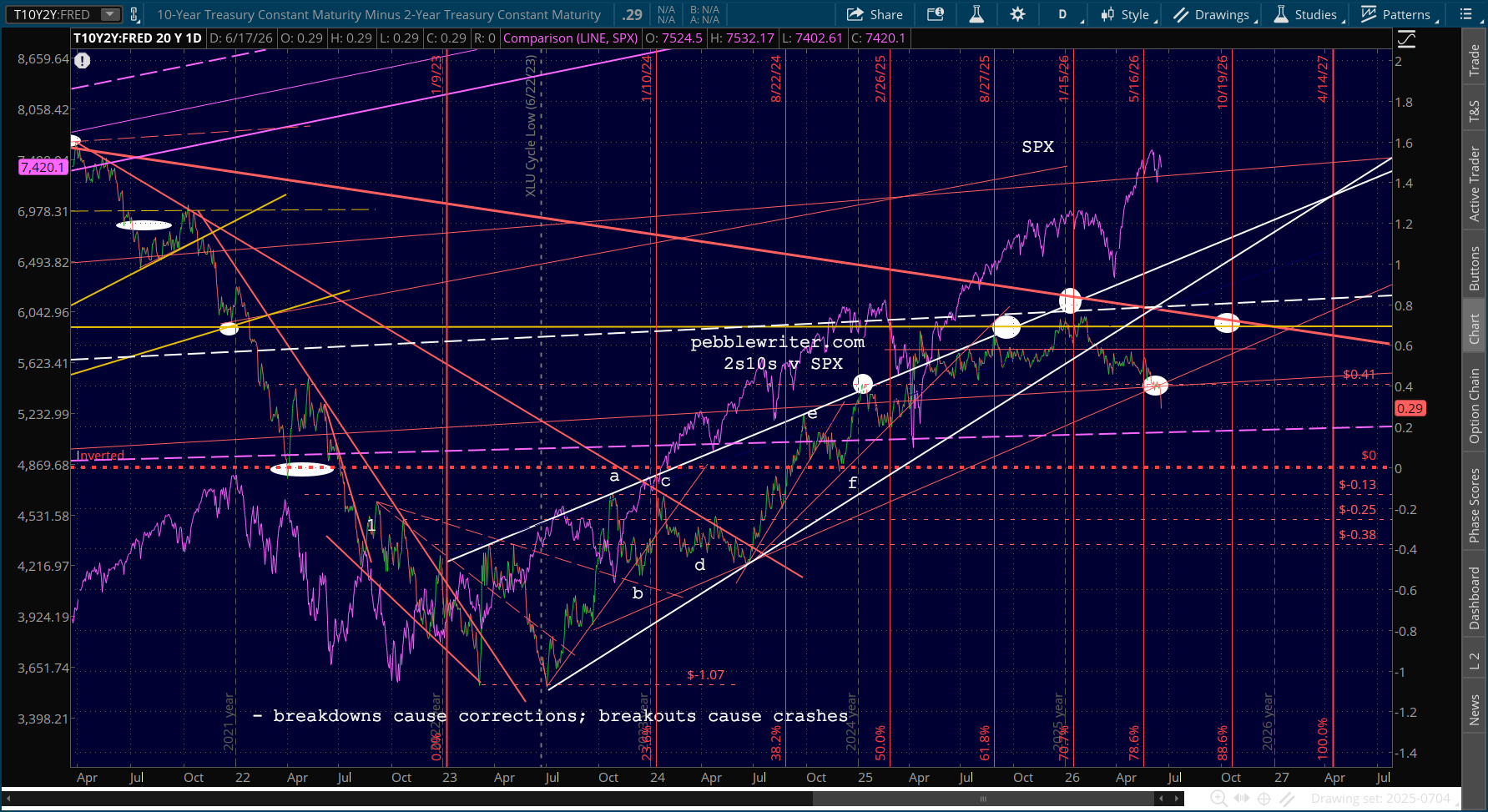

The breakdown of the 2s10s practically guarantees more downside.

Stay frosty…