I remember Oct 15, 2014 like it was yesterday. SPX had risen sharply on the back of the yen carry trade, popping through important Fib resistance at 1823. But, it had just broken trend line and channel support. To make matters worse, it had just dropped through its SMA200 at 1905. The culprits? USDJPY had reversed off heavy resistance and its 10-week rising channel had broken down. And, equally concerning, the bond market signaled more stock carnage to come.

The culprits? USDJPY had reversed off heavy resistance and its 10-week rising channel had broken down. And, equally concerning, the bond market signaled more stock carnage to come.

As we noted at the time:

The more troubling development for Mr. Market is the bond market. The 10-yr note futures shot through the previous high overnight, complicating the prospects of a quick resolution to the market’s correction.

Note that while we might see a reversal today on the white Fibonacci grid — the .786, .886 or the 1.272 itself — we still have to deal with the grey grid, which suggests the possibility of a drop to the .786 at 1798 or the .886 at 1770.

A drop to 1800 would have meant giving up that important Fib support at 1823. More importantly, a 10% correction would occur with a drop to 1817.33 or lower. Who needed those headlines in the middle of spectacular rally to new all-time highs?

The solution?

SPX’s plunge halted at 1820.66 — 3.33 points above what would have been an official correction. No fuss, no muss. The Fib line which had once loomed as formidable resistance could now be reclassified as support.

What has been is what will be,

and what has been done is what will be done,

and there is nothing new under the sun.

Ecclesiastes 1:4-11

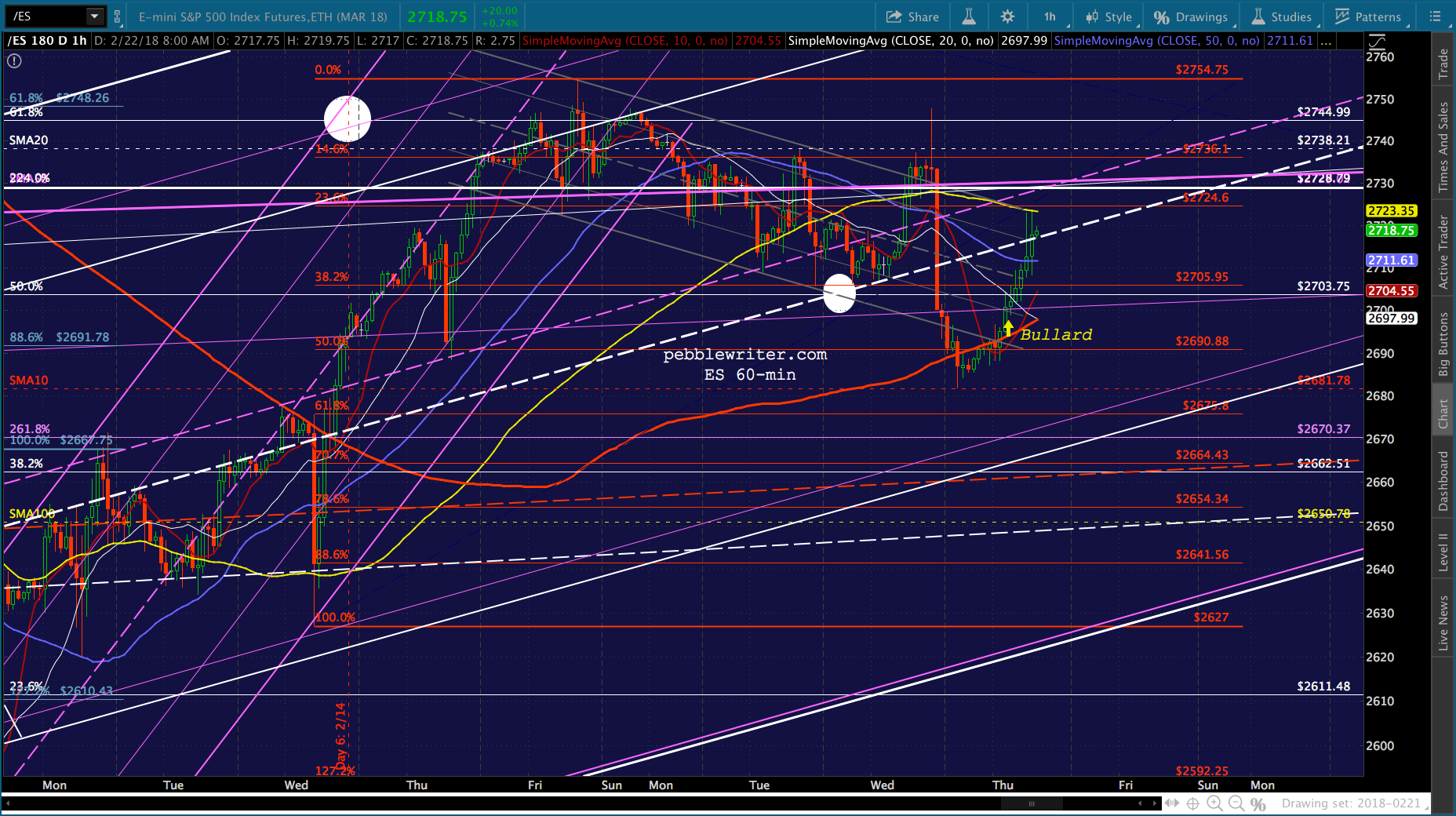

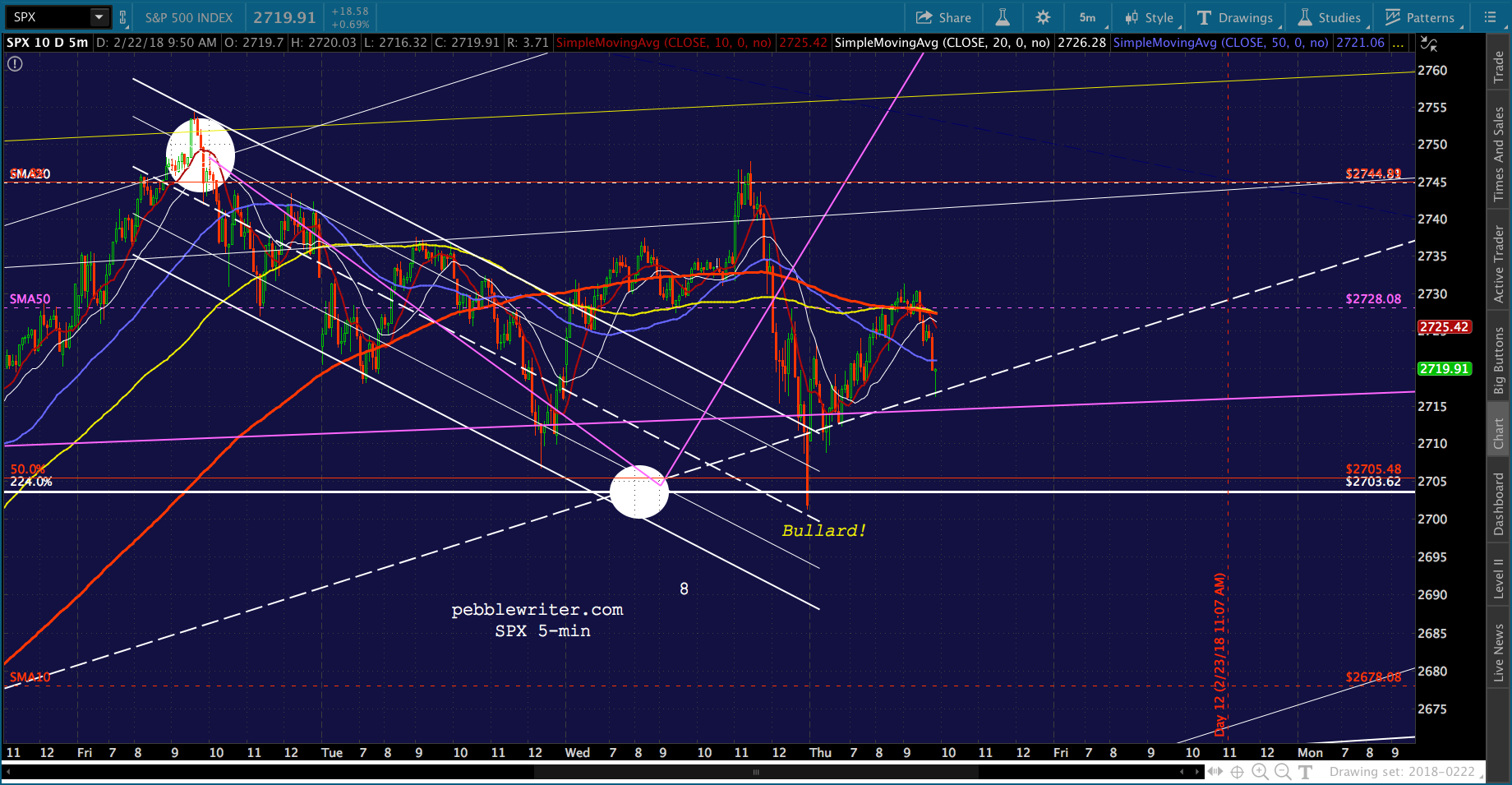

As I went to sleep last night, marveling at how SPX had taken a rather circuitous path to our 2703.62 target,I wondered whether the 2.24 Fib would hold.

I found myself thinking back to 2014. Maybe Fed President Bullard would make another appearance. I didn’t have long to wait.

I found myself thinking back to 2014. Maybe Fed President Bullard would make another appearance. I didn’t have long to wait.

On CNBC this morning…

Futures are currently up 27 points off their overnight lows (bounced at the 10-day moving average, probably about 60 seconds after Bullard was booked on CNBC.) At least we weren’t kept in suspense too long!

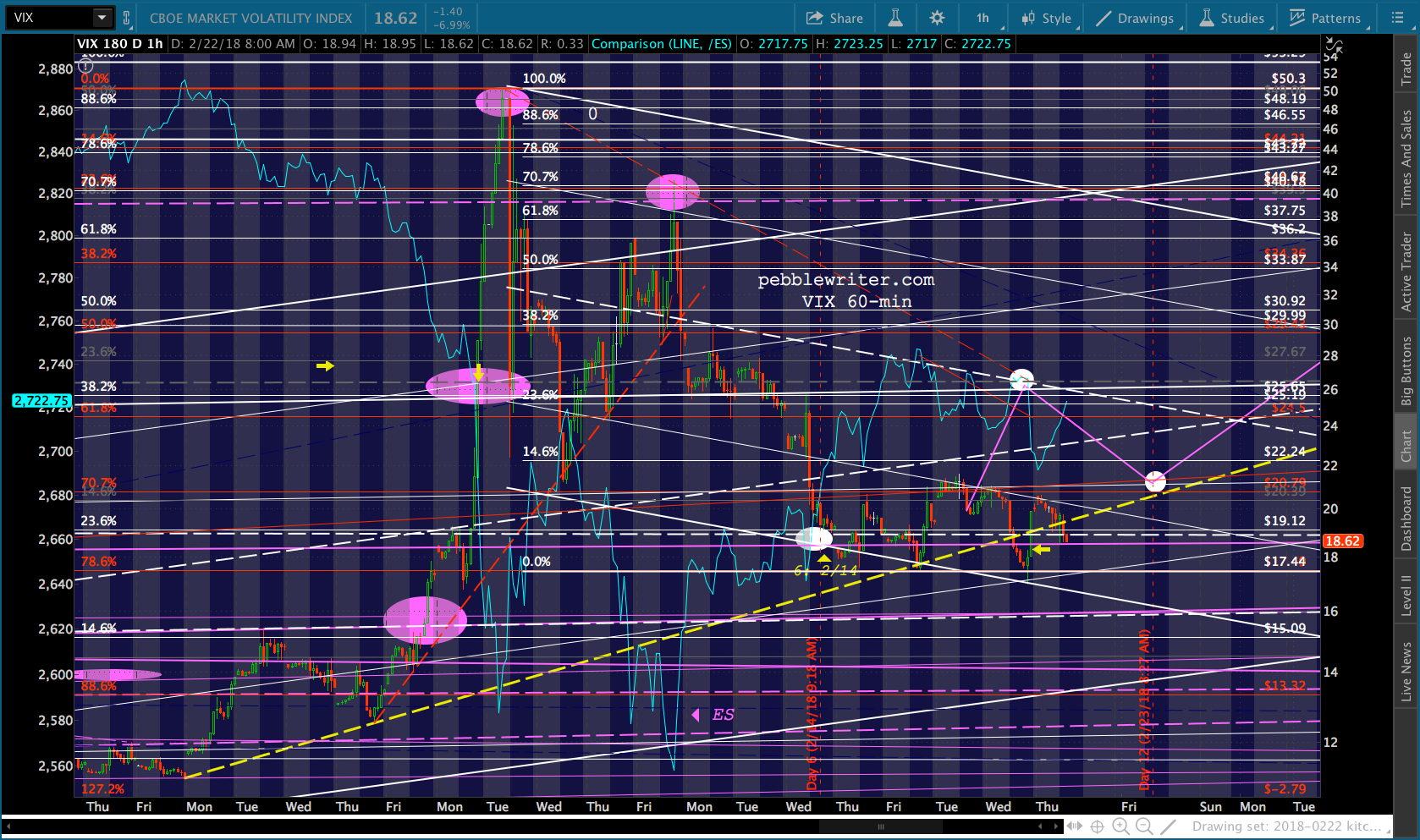

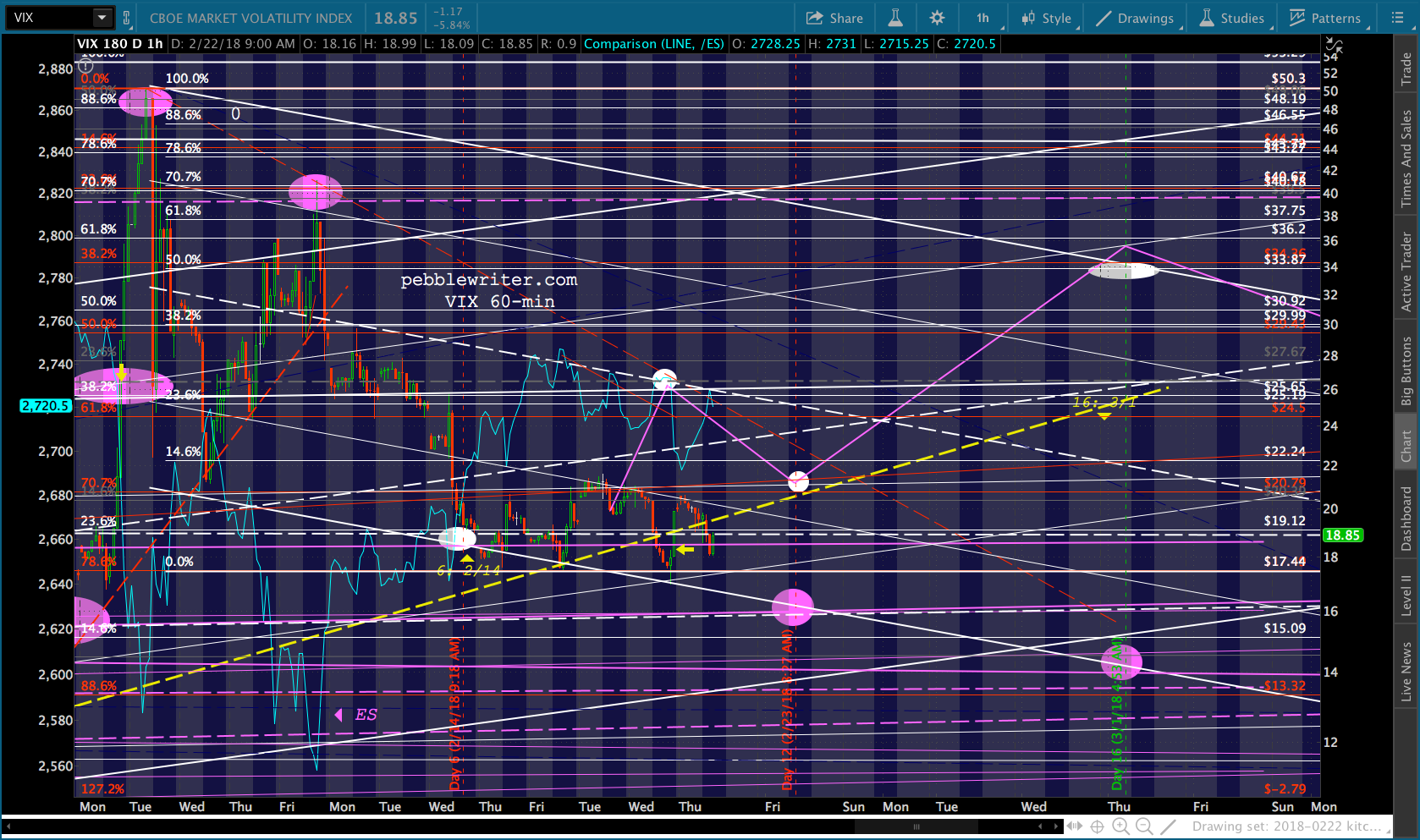

Oh, and for those wondering why/how yesterday unfolded as it did, take a look at VIX. See that little dip (yellow arrow) below the trend line from Jan 26? Yep, that’s all it took.

When VIX climbed back above the yellow trend line, SPX promptly gave up all its pre-minutes ramp job. VIX has obviously proven it’s still incredibly powerful. Who needs a 40% spike when a 20% one can put on the brakes so effectively? The flipside, of course: if VIX decides to pop up to 26 anyway, SPX will likely ignore Bullard and also test its SMA10.

VIX has obviously proven it’s still incredibly powerful. Who needs a 40% spike when a 20% one can put on the brakes so effectively? The flipside, of course: if VIX decides to pop up to 26 anyway, SPX will likely ignore Bullard and also test its SMA10.

Bullard might be able to divert attention from the interest rate problem. But, it clearly hasn’t gone away.

This time, it’s a spike in rates rather than a plunge. So it’s a different kind of interest rate problem. As a result, this one might be tougher to rectify. And, the implications for the overall economy are much more serious.

This time, it’s a spike in rates rather than a plunge. So it’s a different kind of interest rate problem. As a result, this one might be tougher to rectify. And, the implications for the overall economy are much more serious.

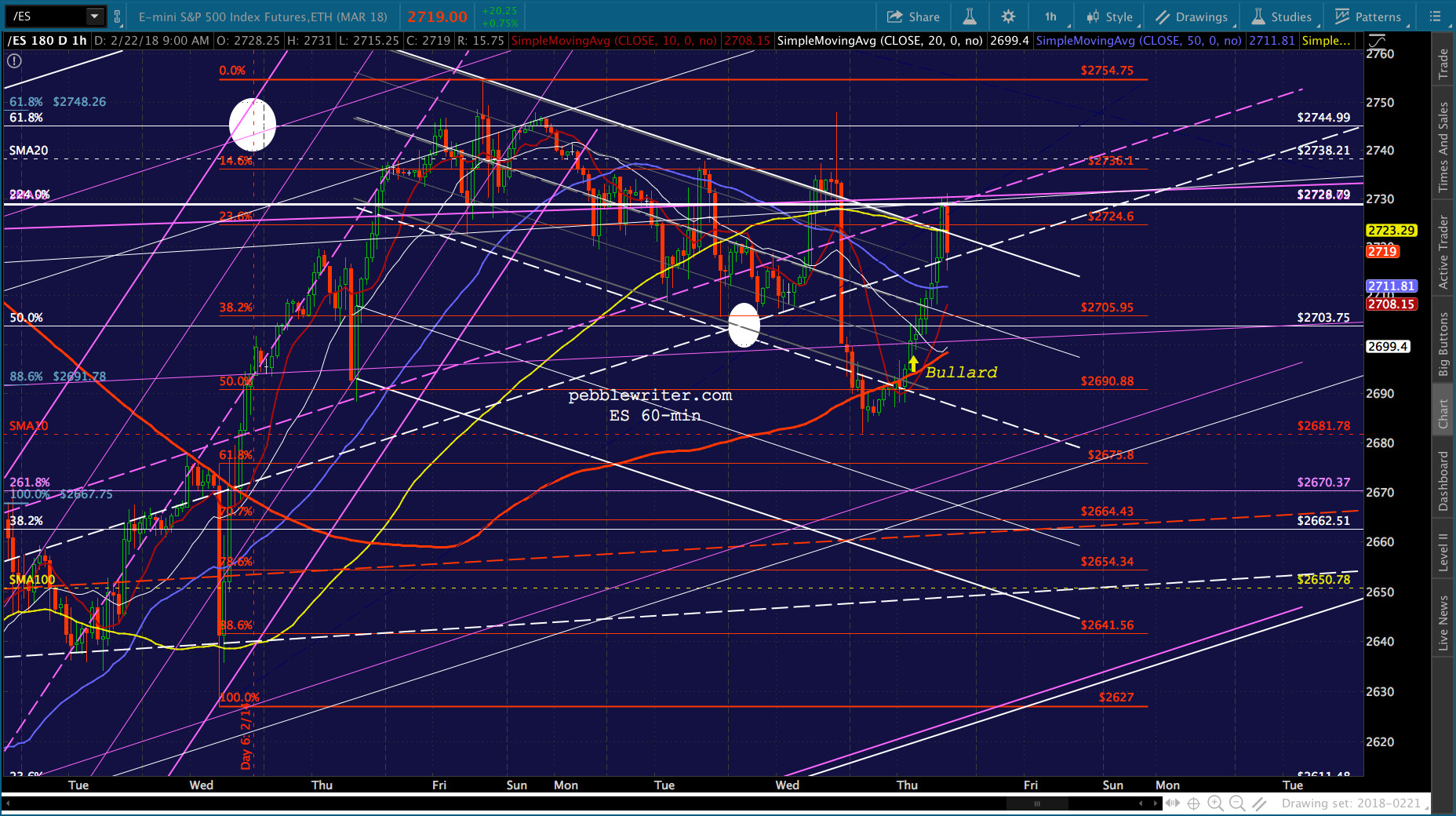

continued for members…ES is testing the top of the falling gray channel in place over the past 4 sessions. This also means a test of the rising white channel midline. A rise above 2724 should leave the bulls in the clear, with only ES’ 2.24 at 2728.79 to contend with. Will VIX accommodate?

Will VIX accommodate?

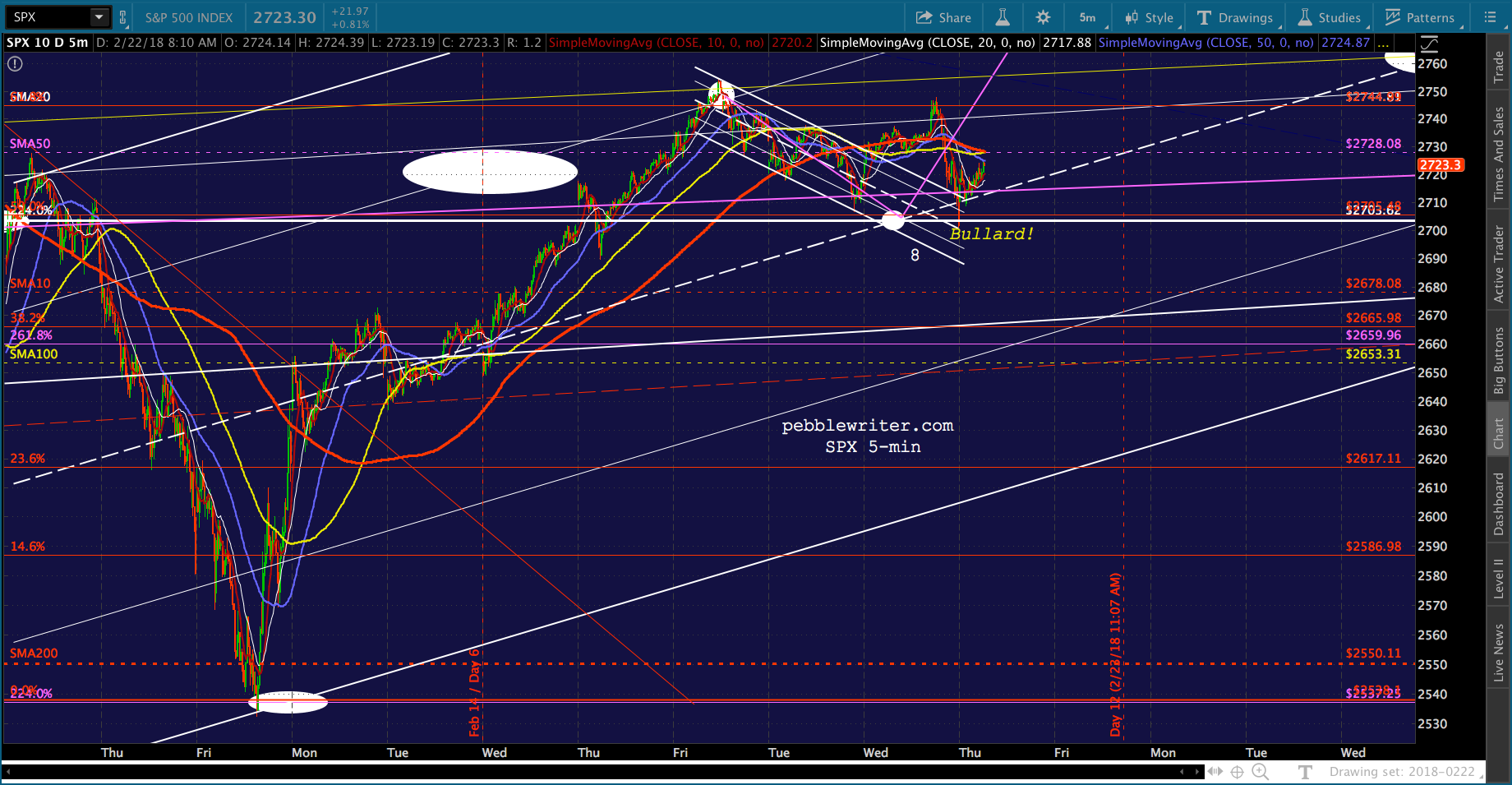

The view from SPX:

The view from SPX:

UPDATE: 1:00 PM

UPDATE: 1:00 PM

ES reversed off its 2.24 on the lack of (algo) leadership. So far, it is holding at the rising white channel midline, but it’s hard to imagine it shooting higher unless VIX gets into gear. Likewise for SPX, which just backtested its white midline at 2716. Watch out if it drops through it.

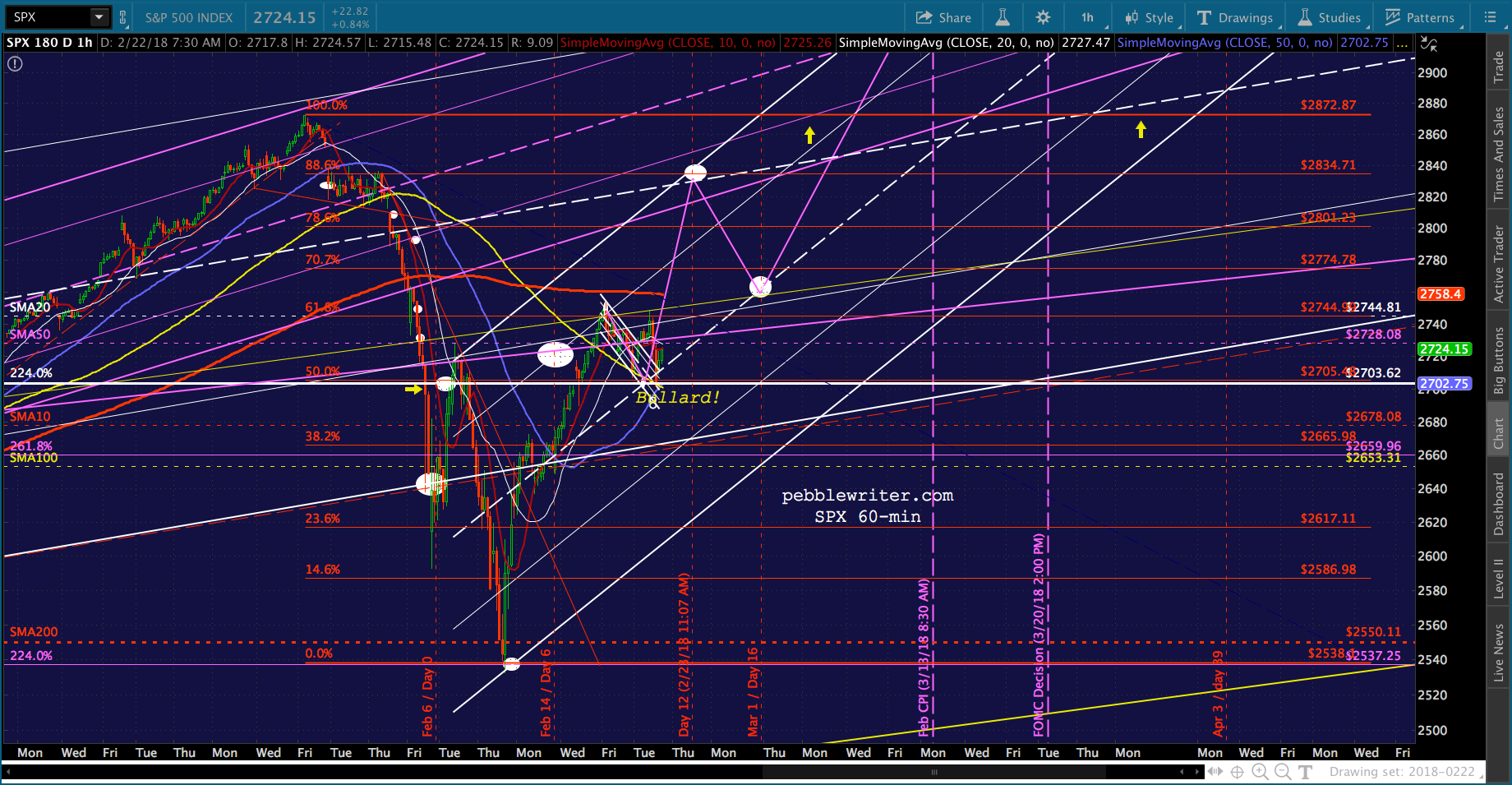

By expanding ES’ falling white channel, we can see a path to, say, the red .886 at 2641.56. If VIX were to pop up to 26, I think it’d be fairly likely to occur.

By expanding ES’ falling white channel, we can see a path to, say, the red .886 at 2641.56. If VIX were to pop up to 26, I think it’d be fairly likely to occur.

This raises the question about the analog, which called for some pretty strong moves from VIX in order to manipulate SPX higher one last time.

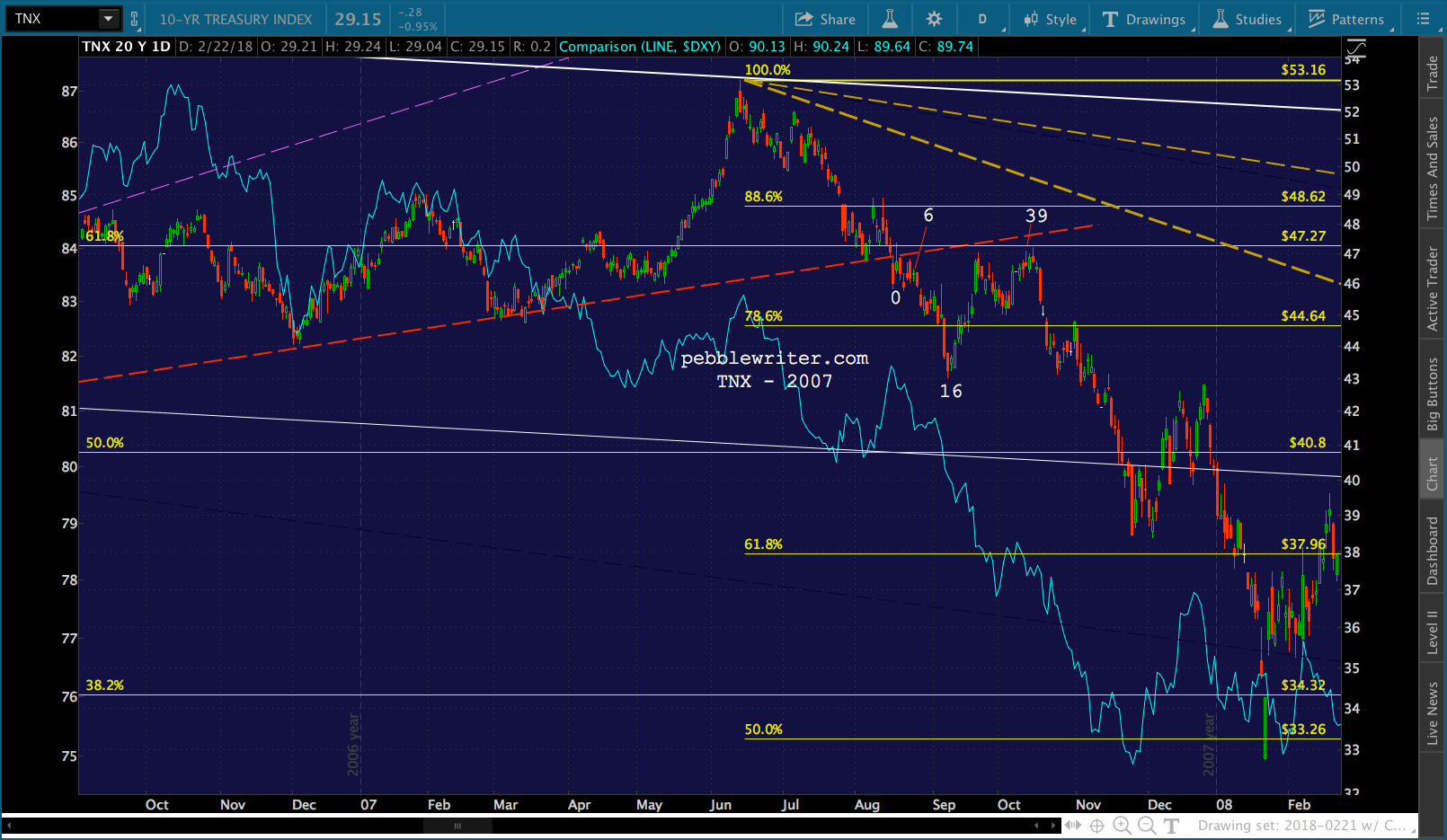

The bullish argument: if we focus on what VIX did in 2007 rather than how it did it, it’s not that hard to see the analog still holding up — at least as far as its effect on stocks. That is, the whole point of those zig-zags in VIX was to ratchet SPX higher — which it did.

VIX moved to exactly where it needed to in order to string together some legit-looking higher highs and higher lows. Today, a pop up to 26 would create more of a drop in SPX than TPTB wish to see play out. So, instead, the rise in VIX took SPX to backtest the 2.24 at 2703 and then stopped.

Right now, the most prominent algo trigger for VIX is the yellow TL. If VIX moves back toward it or above it, stocks will drop. If, instead, it continues to follow the falling white channel bottom, dipping below 16 in the next day or two, then SPX and ES can break out.

We know the analog is off by some measure of time because SPX didn’t bottom on the same day that VIX peaked. ES did, tagging nice support at its SMA200. So, there’s a little uncertainty around that. If VIX’s spike were to occur today, for instance, instead of yesterday, SPX could tag 2678 and we could move on.

The other uncertainty concerns interest rates. As mentioned earlier, the recent rate rise is opposite from and has consequences far exceeding Oct 2014’s. It’s also opposite the move that was made around the 2007 analog period — when rates had spiked two months earlier and had just broken support when the VIX spike occurred. Interest rates were slumping in 2007 and 2014 because equity investors were getting nervous and putting equity money into treasuries instead. In 2007, TNX broke below trend because people were panicking. Today, we need interest rates to decline in order to keep people from panicking.

Interest rates were slumping in 2007 and 2014 because equity investors were getting nervous and putting equity money into treasuries instead. In 2007, TNX broke below trend because people were panicking. Today, we need interest rates to decline in order to keep people from panicking.

But, rates are unlikely to decline as long as there’s a perception that inflation is on the rise. Bonds investors simply don’t believe it’s not going to be a problem, and are demanding to be paid for that risk. When might that perception change?

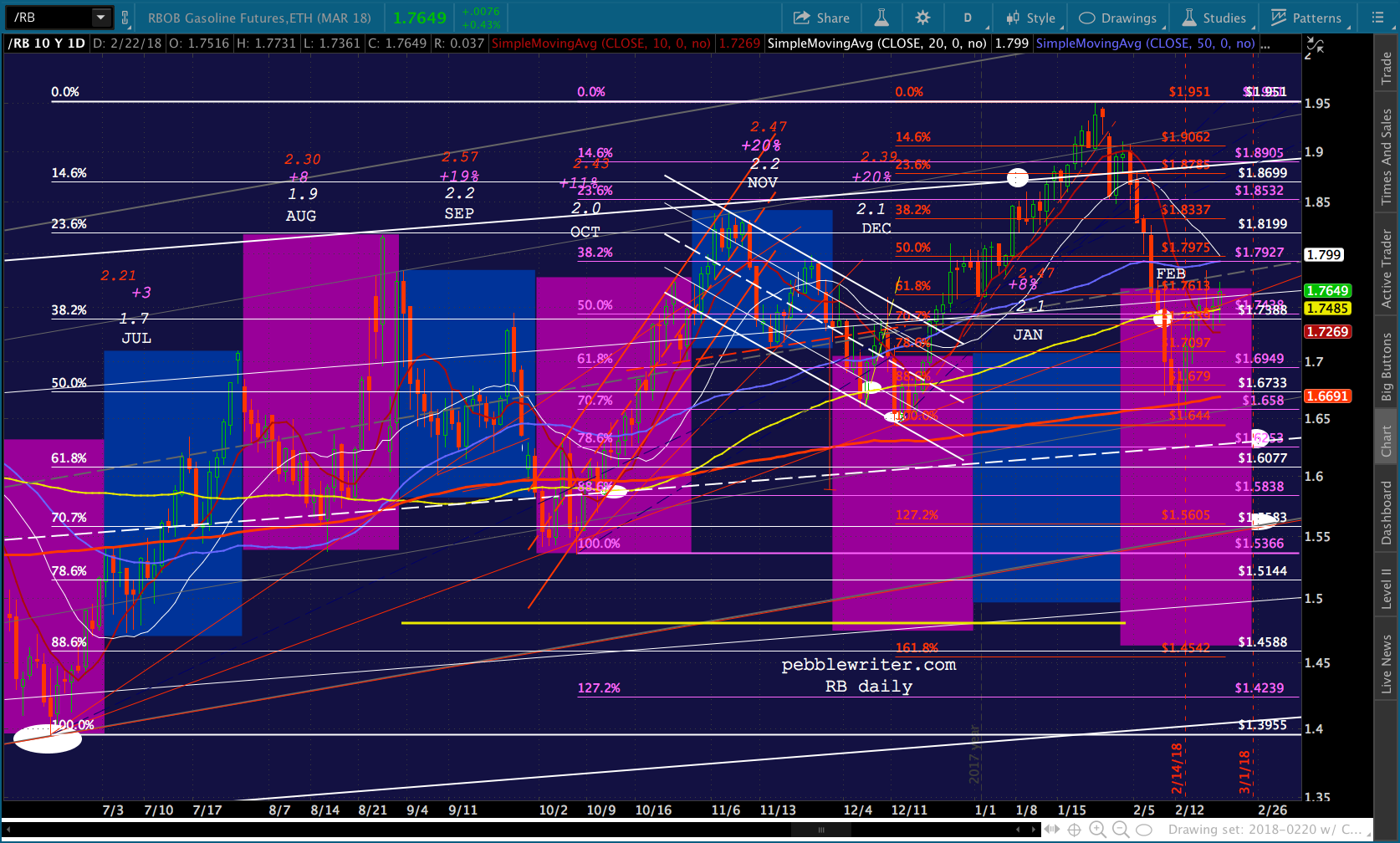

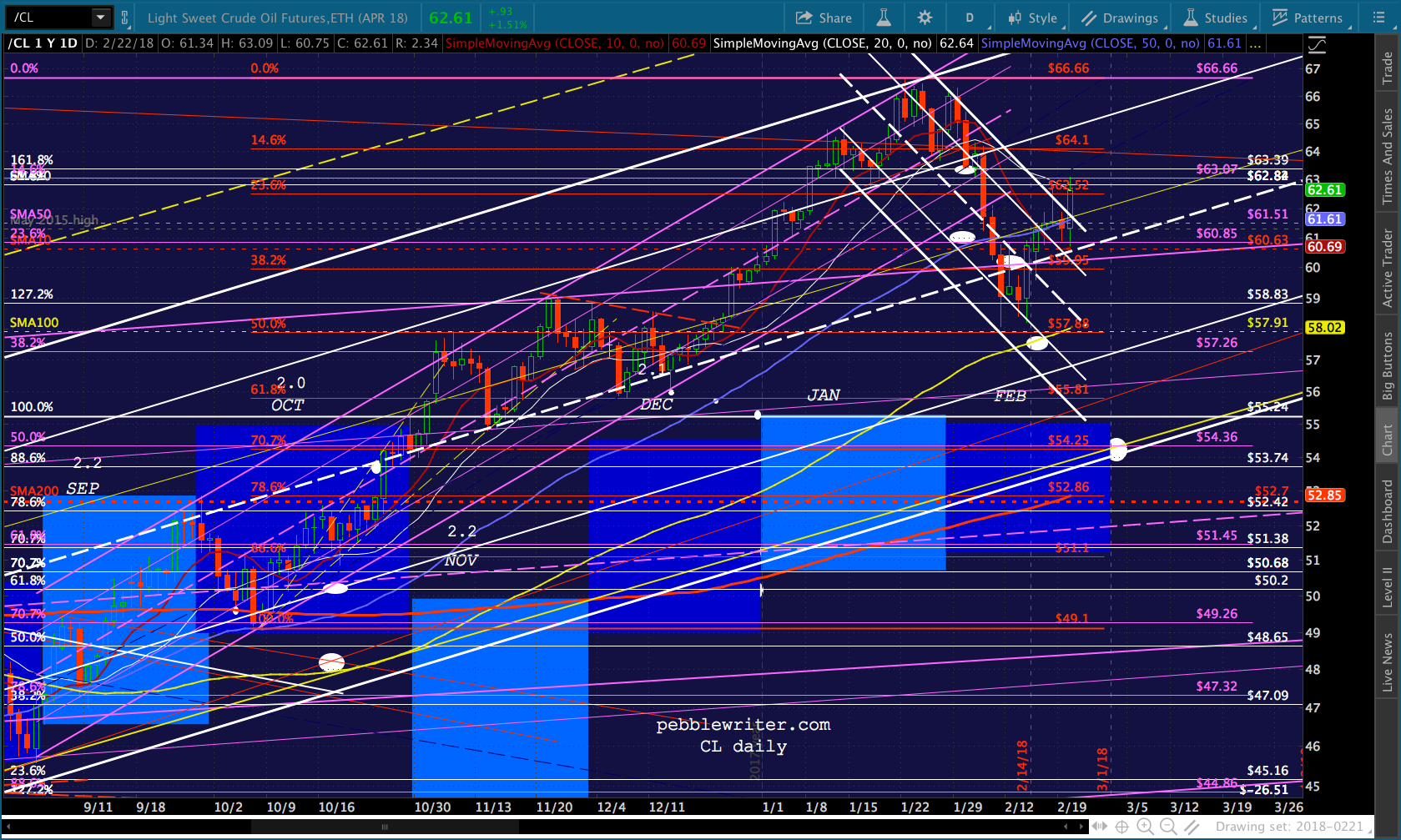

It would help if oil and gas prices were to drop further; but, that doesn’t appear likely. RB has come down significantly from its year-end ramp job, but shows no signs of reversing after bouncing at its SMA200. CL is still working its way higher in order to help stocks. With SPX on the precipice here, I’d expect both to head higher.

If both could plunge on the 28th (the day EIA reports inventory), then BLS would find a way to report very low inflation numbers for Feb when they report on March 13.

Mar 1 is day 16 of our analog, when VIX was supposed to spike higher — enabling a dip in SPX. What if instead of VIX spiking (too dangerous!!!) we saw CL plunge to 53-54 and RB to 1.61? We’d get the dip (backtest) in stocks without the risk of another big VIX spike. Wishful thinking.