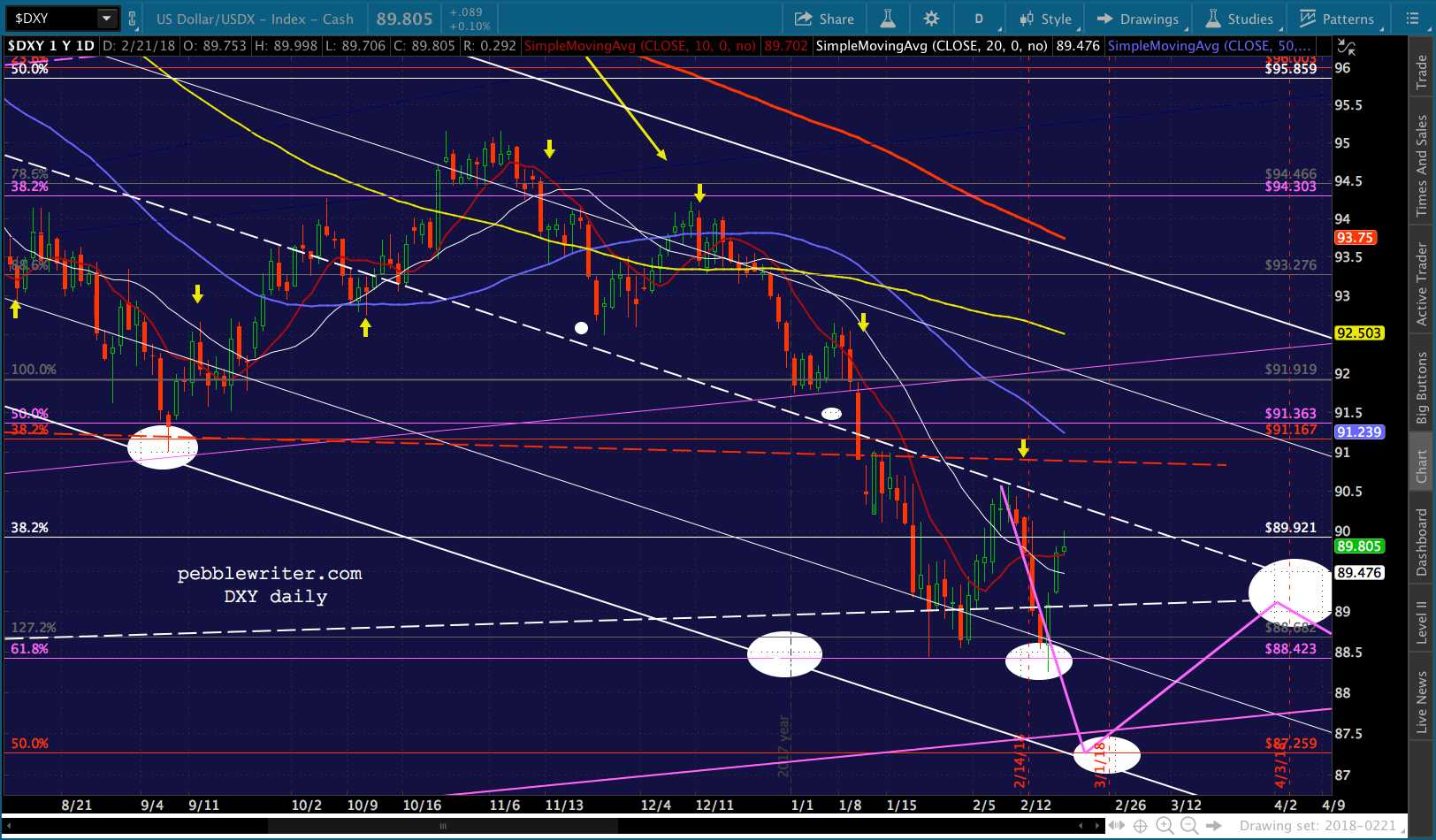

The last time the FOMC released minutes was Jan 3 [see: Will the FOMC Minutes Save the Dollar?] At the time, we looked at the effect of FOMC rate hikes on the dollar index (DXY.) The obvious conclusion was that rate hikes in 2017 had marked interim tops, while failures to hike rates has produced temporary bumps that lasted anywhere from 1-6 weeks.

Here’s the exact same chart, updated with January’s non-hike. In honor of today’s Fed minutes release, I’ve also added markers (the purple arrows) for previous releases.

Looking at each, you’d have to conclude that either: (1) the FOMC knew what they were doing, and wanted to talk the dollar down throughout 2017; or, (2) they had no clue how to prop it up.  What’s interesting to me, as a chartist, is how well the inflection points occasioned by the minutes releases tracked our falling white channel — allowing our forecast from last May [see: Update on US Dollar May 1, 2017] to play out very precisely.

What’s interesting to me, as a chartist, is how well the inflection points occasioned by the minutes releases tracked our falling white channel — allowing our forecast from last May [see: Update on US Dollar May 1, 2017] to play out very precisely. Our conclusion back on Jan 3 was that the minutes would not only not save the dollar, but its continued slide would present problems for stocks.

Our conclusion back on Jan 3 was that the minutes would not only not save the dollar, but its continued slide would present problems for stocks.

With TNX about to break out, we can expect continued weakness in DXY. Needless to say, this will present difficulties for the yen carry trade crowd and, ultimately, equities. I suspect the dollar’s slide isn’t over — with our targets at 88.423-88.682 the next major support when it breaks below September’s lows.

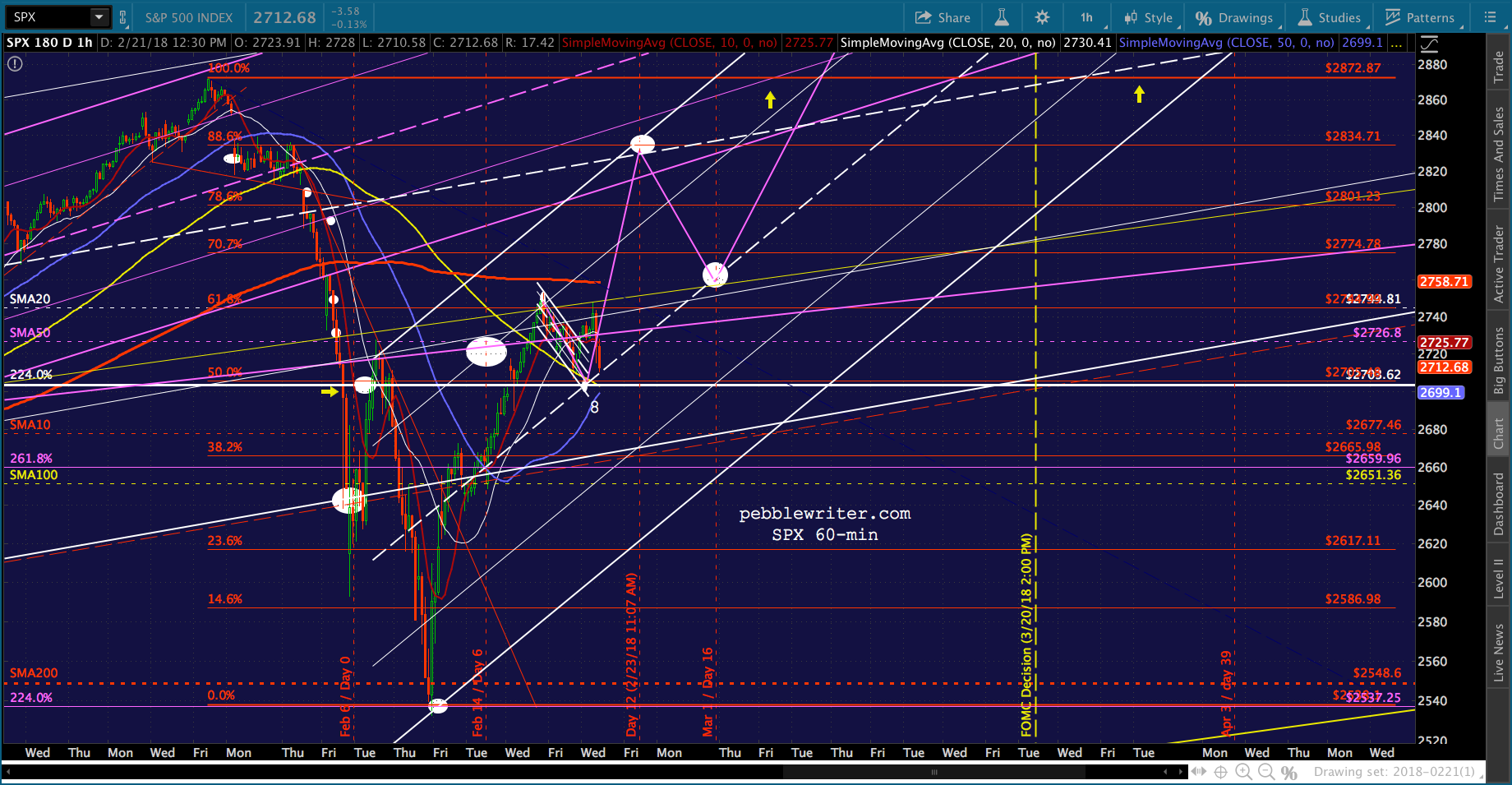

If [SPX can’t push through 2703] then the first real support is the bottom of the gray channel, currently around 2588. And, if that fails, then the SMA100 is currently around 2560 and the SMA200 is around 2485.

We all know what happened next. The minutes produced a momentary bump in DXY and USDJPY, safely escorting SPX through the resistance at 2703. At the same time, CL went on a month-long 11% tear and VIX continued to plunge when necessary. SPX didn’t look back until reaching 2872.

At that point, the rally ran out of steam. Obviously, it was overbought. But, DXY’s slide from 92 to 88 didn’t help. Nor did USDJPY’s plunge from 112.5 to 105.5.

The most intractable problem, however, was the sharp rise in interest rates. They reflected a growing recognition that the sharp spike in oil and gas prices which helped fuel algos throughout December and January would also produce inconveniently high inflation.

When the 10Y broke out on Jan 10 [see: China – It’s Not Me, It’s You] we slapped a 28.56 target on TNX — a target it reached on Feb 5. Not so coincidentally, Feb 5 was the day SPX plunged back below support (formerly resistance) at 2703. The next day, SPX plunged to within 5 points of our 2588 target. Three sessions later, it tagged the 200-day moving average.

When the 10Y broke out on Jan 10 [see: China – It’s Not Me, It’s You] we slapped a 28.56 target on TNX — a target it reached on Feb 5. Not so coincidentally, Feb 5 was the day SPX plunged back below support (formerly resistance) at 2703. The next day, SPX plunged to within 5 points of our 2588 target. Three sessions later, it tagged the 200-day moving average.

The rally off of 2532 has been impressive, following our analog [see: Analog Watch] very closely for the past two weeks. As we wait for word on whether to expect three or four rate hikes in 2018 (at least, so everyone says,) our analog suggests that the Fed will have to deal with the divergence between spreads and the 10Y itself. It might not be pretty.

It might not be pretty.

continued for members…

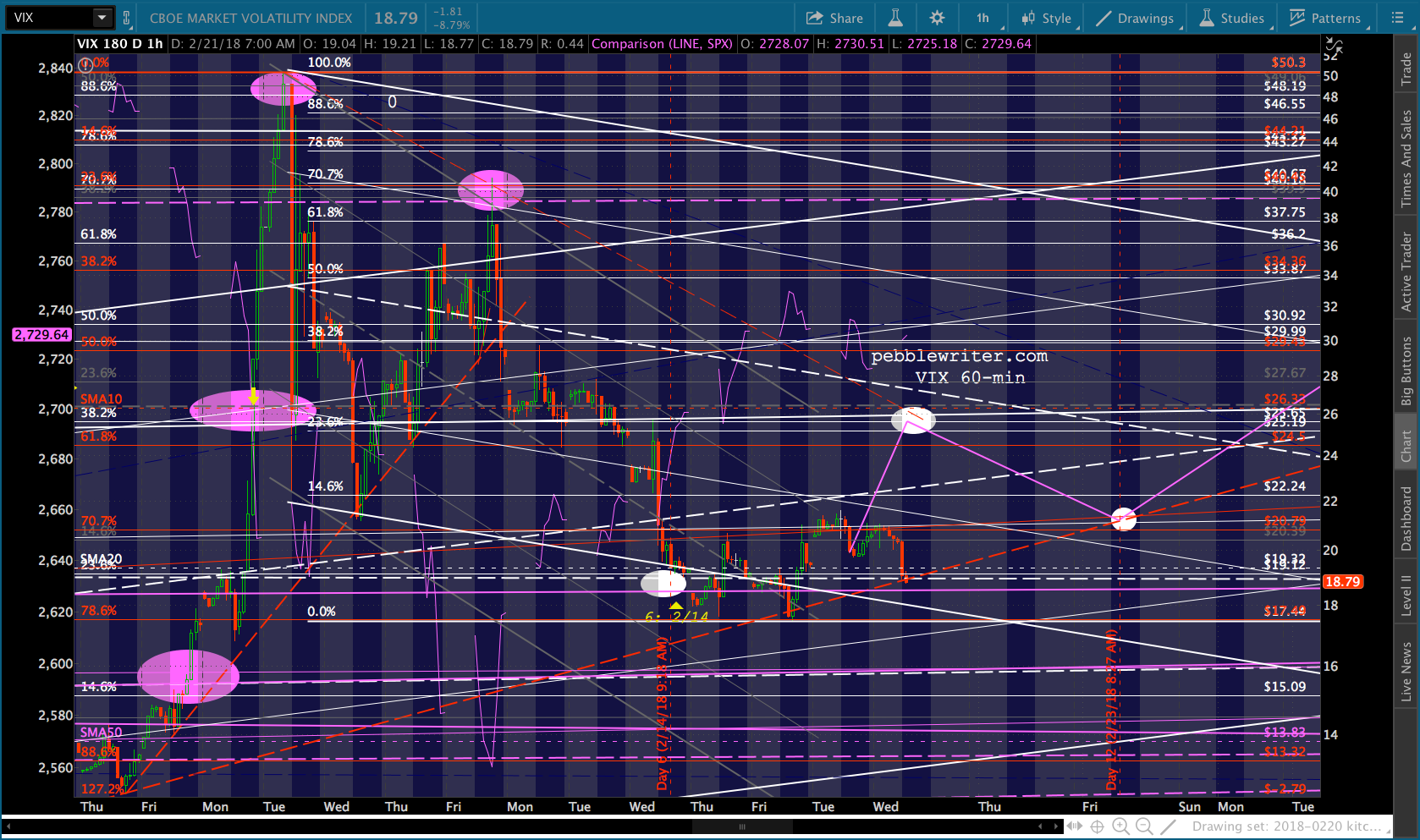

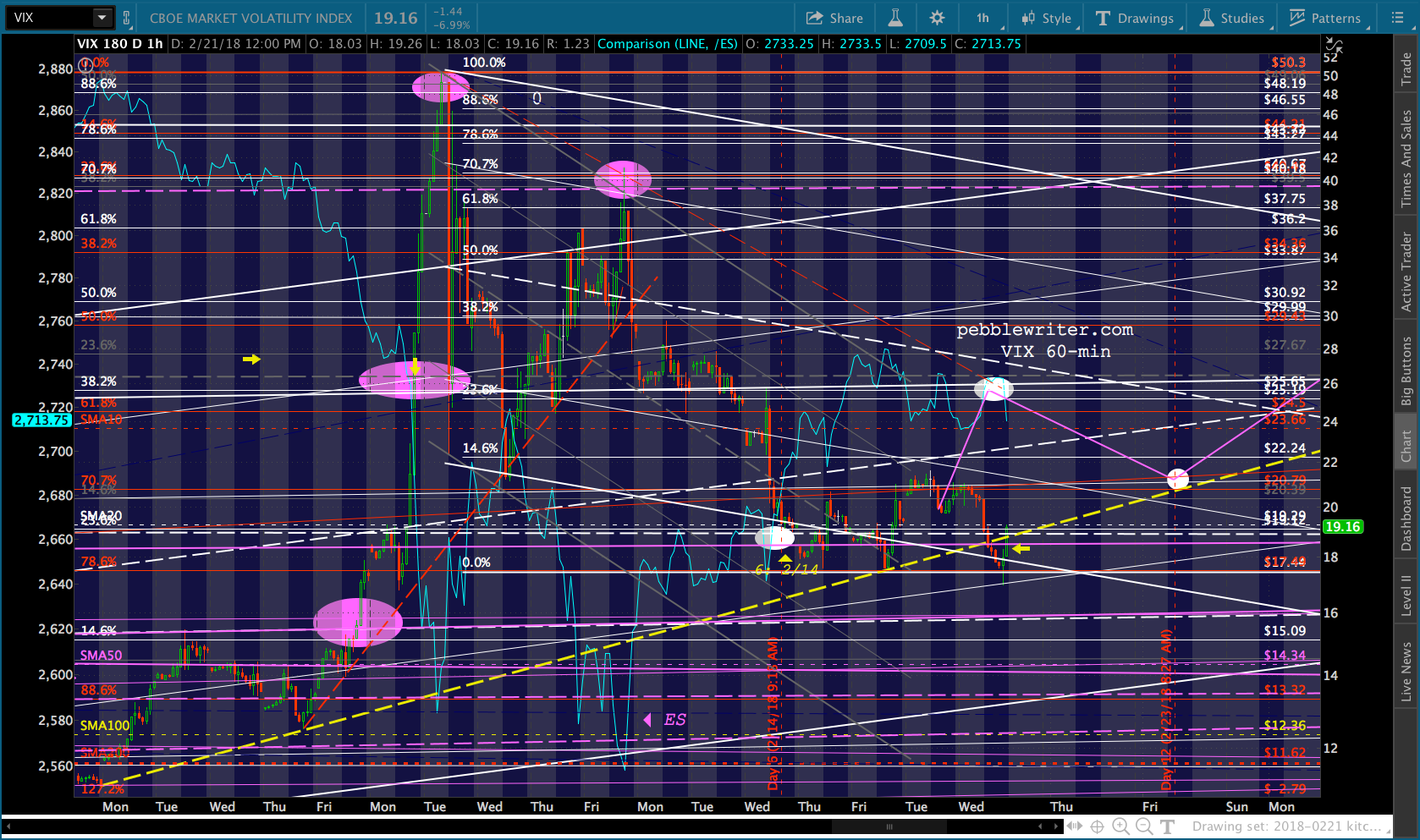

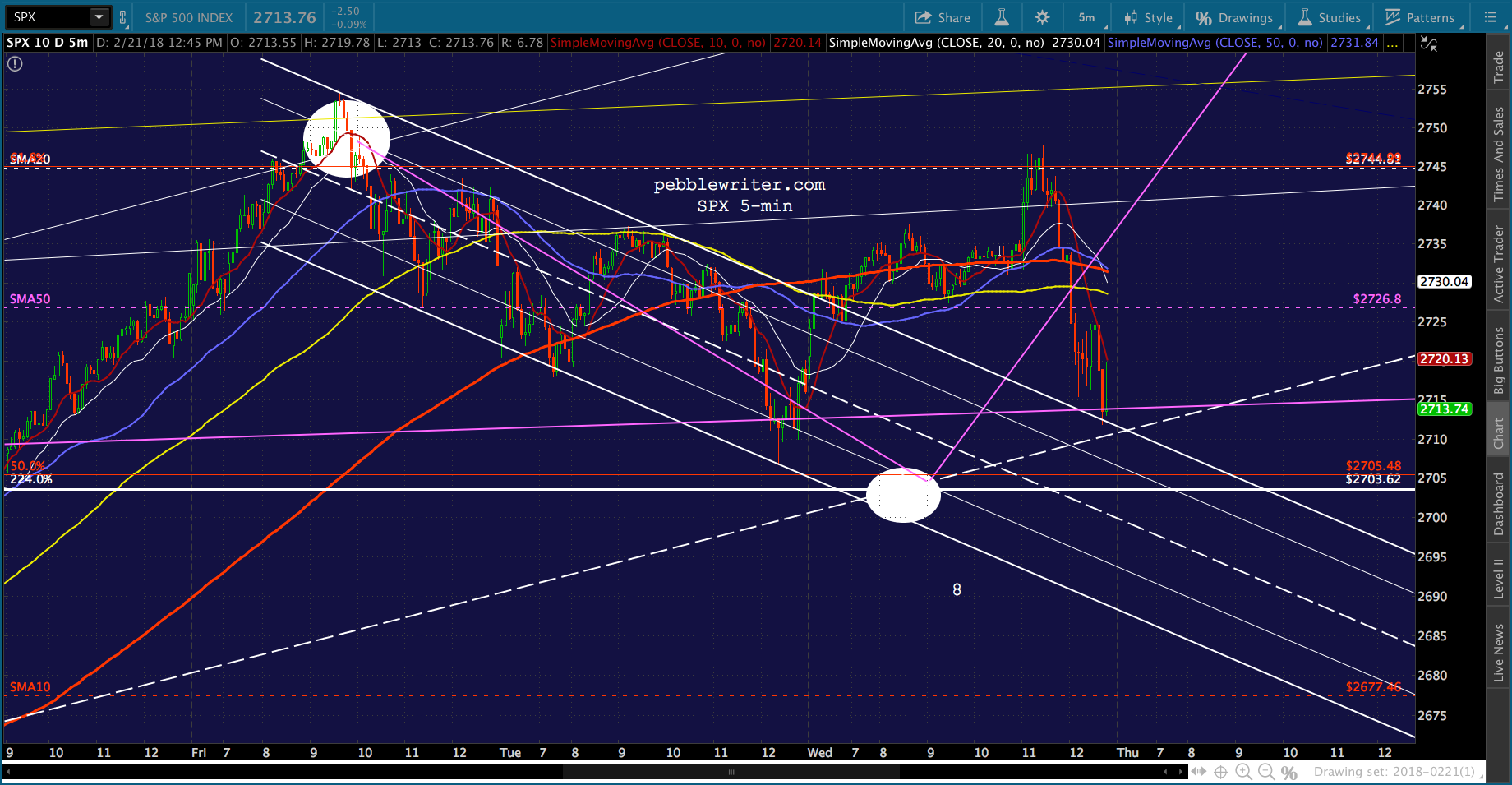

SPX came within 3 points of an actual backtest yesterday. The analog suggests VIX will pop higher today, meaning SPX isn’t necessarily out of the woods just yet.

VIX’s line in the sand is around 18.48. A drop through there would boost SPX up out of the small white channel shown above — at least temporarily. Watch for head fakes!

VIX’s line in the sand is around 18.48. A drop through there would boost SPX up out of the small white channel shown above — at least temporarily. Watch for head fakes!

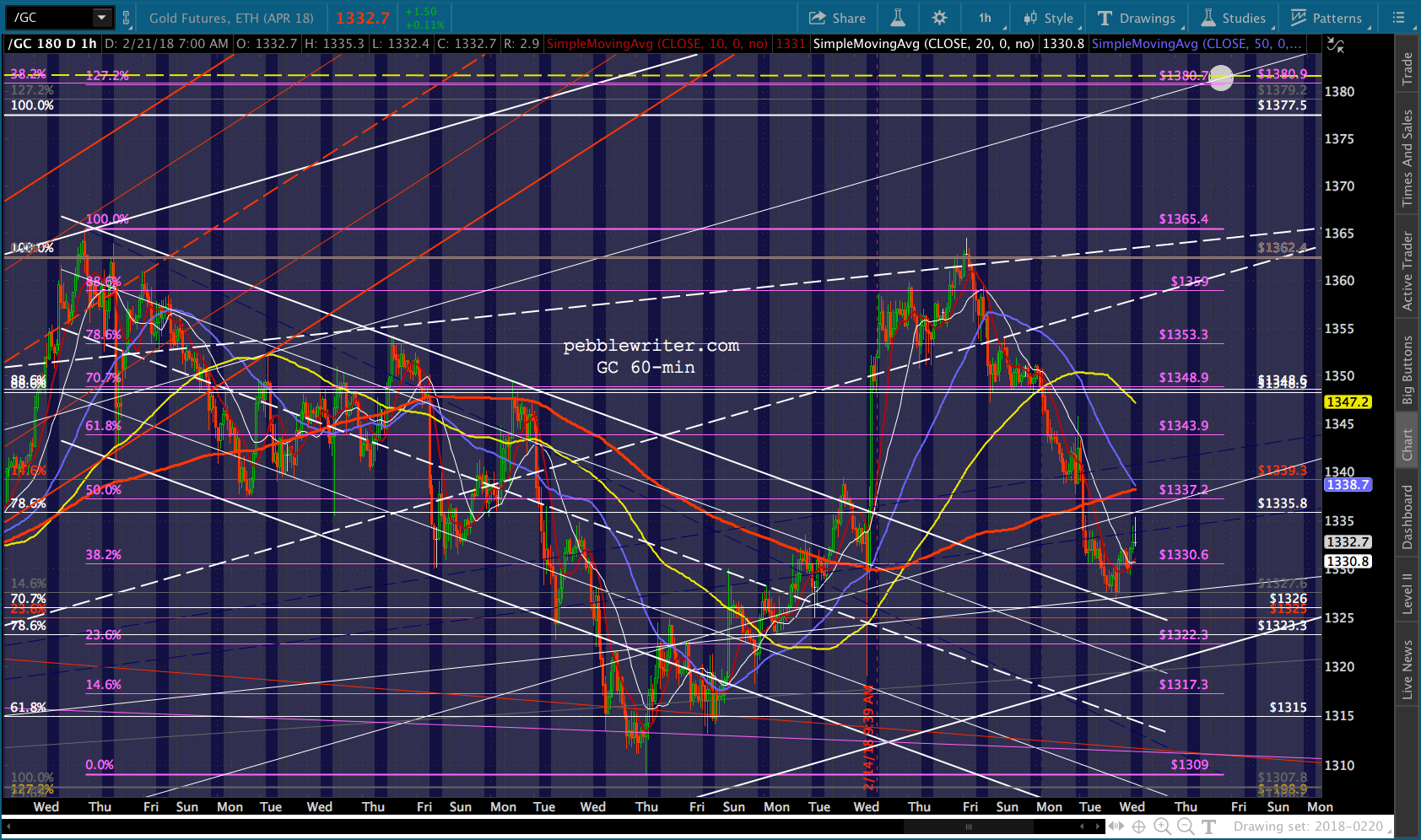

For those watching gold, note that it backtested its channel overnight and is well positioned for another run at 1380. Stops around the channel top are advised, just in case.

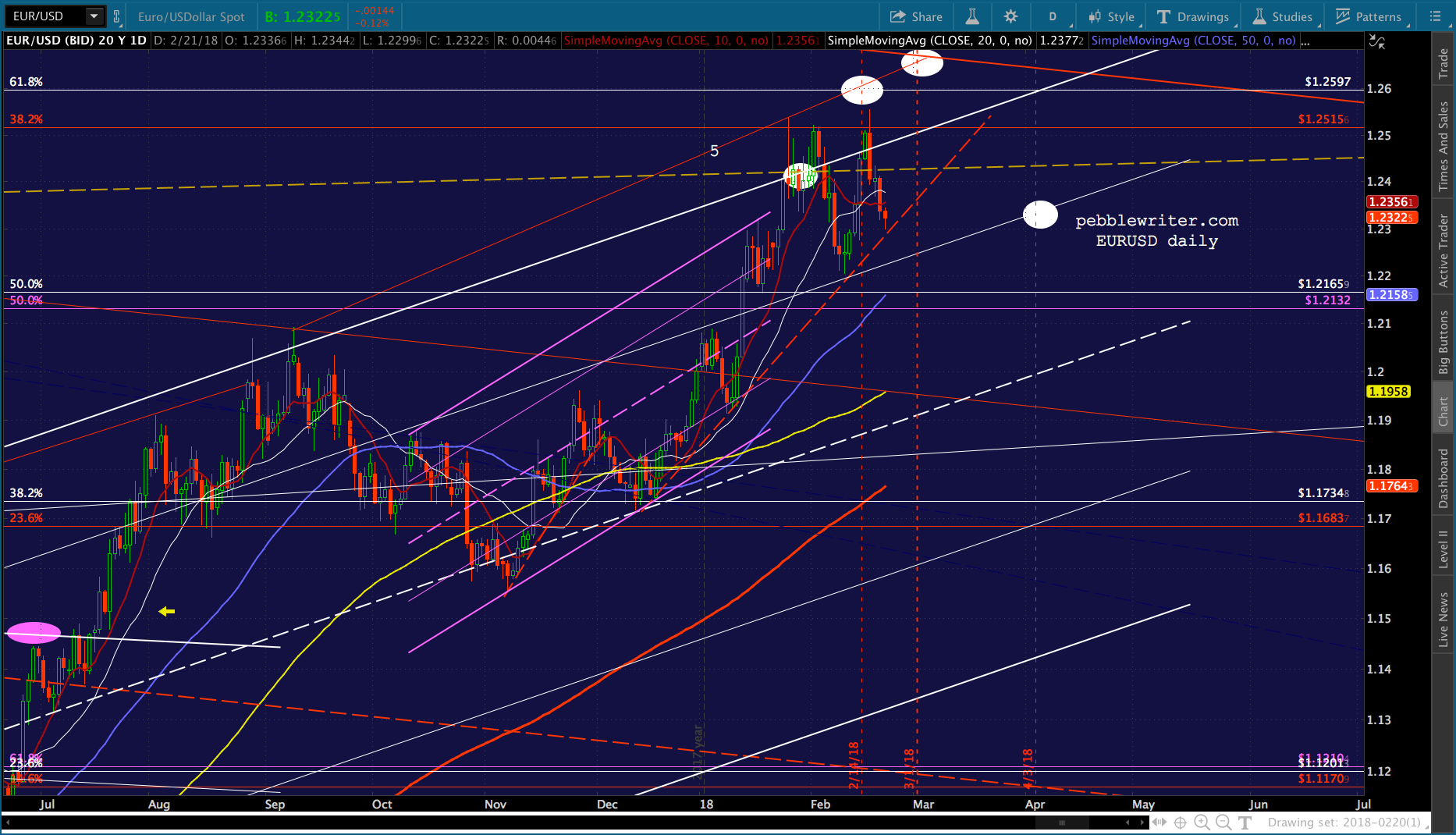

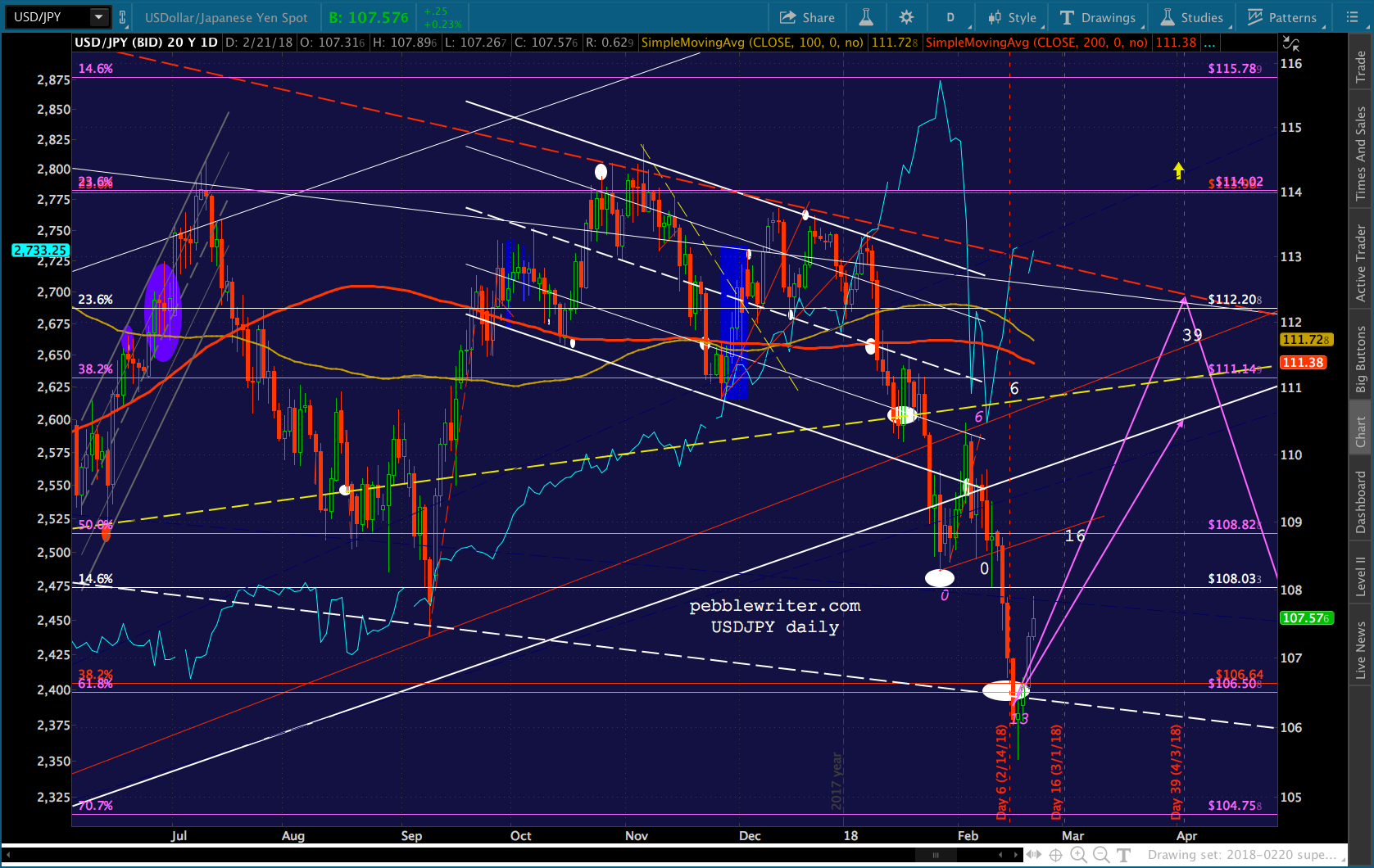

For those watching gold, note that it backtested its channel overnight and is well positioned for another run at 1380. Stops around the channel top are advised, just in case. All together, the charts suggest a continuing dovish tilt from the Fed — with a lower DXY into the end of the month, a combination of a pop in EURUSD partially offset by a rise in USDJPY.

All together, the charts suggest a continuing dovish tilt from the Fed — with a lower DXY into the end of the month, a combination of a pop in EURUSD partially offset by a rise in USDJPY.

As I mentioned yesterday, I have to be out of the office all day today. I hope to be able to check back in a few times, but it might not be until the end of the day.

As I mentioned yesterday, I have to be out of the office all day today. I hope to be able to check back in a few times, but it might not be until the end of the day.

GLTA.

UPDATE: 3:50 PM

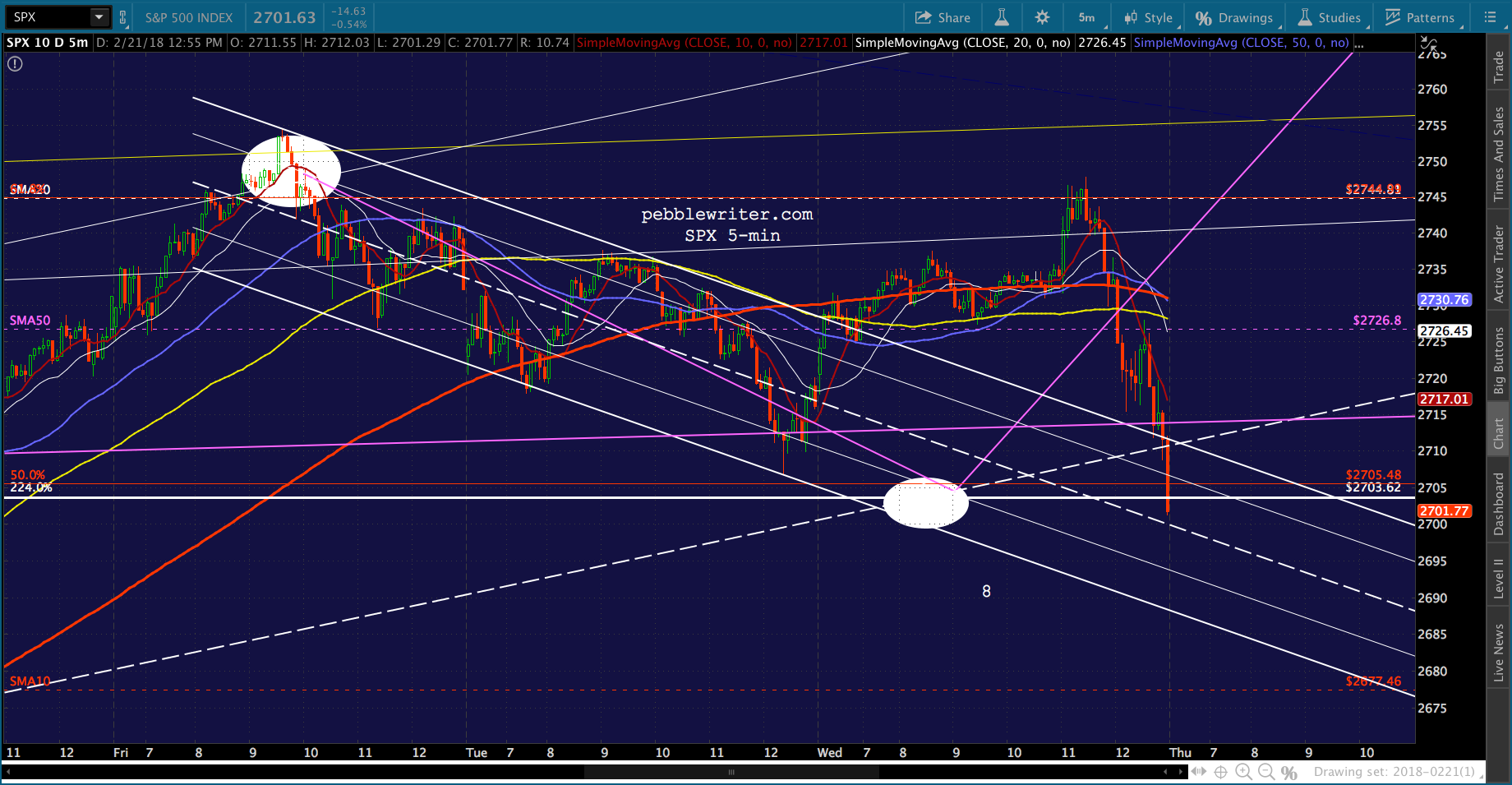

Been a wild ride, but SPX is almost back to 2703 — even without much of a move in VIX. It certainly doesn’t look like it’ll take much of a rise in VIX to get SPX on down to 2703, leaving me to wonder whether it might overshoot into the close in order to accommodate whatever move VIX has in mind.

If the analog is busted and we don’t get a spike in VIX, then we’ll know that rising rates (10Y pushing 2.94) have taken over the narrative. Even so, I expect it to be a headfake and that SPX will rally tomorrow. But, the SMA10 is down at 2677.46, so that’s always a possibility that it doesn’t stop at 2703.62ish but bounces off the SMA10 instead.

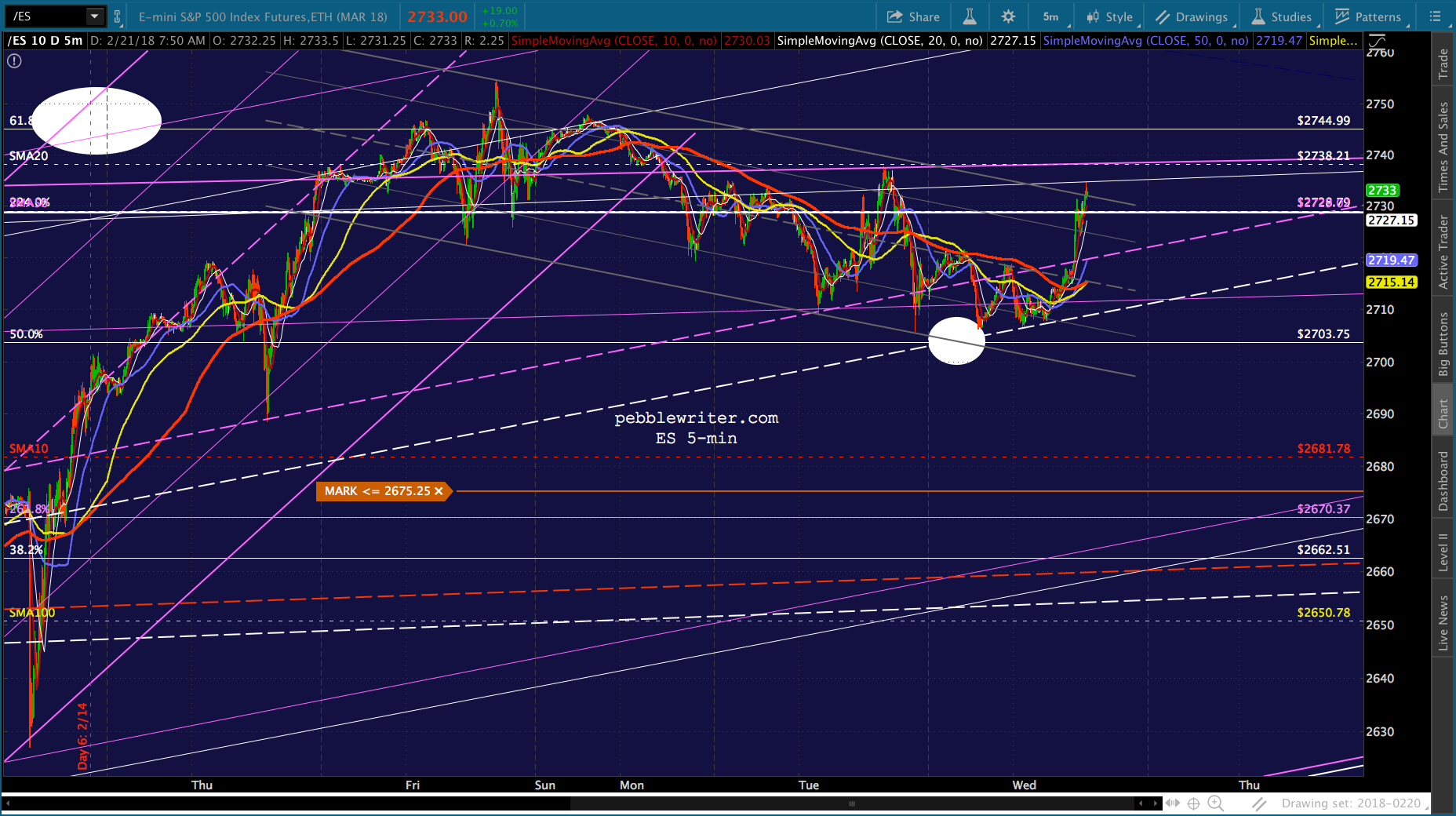

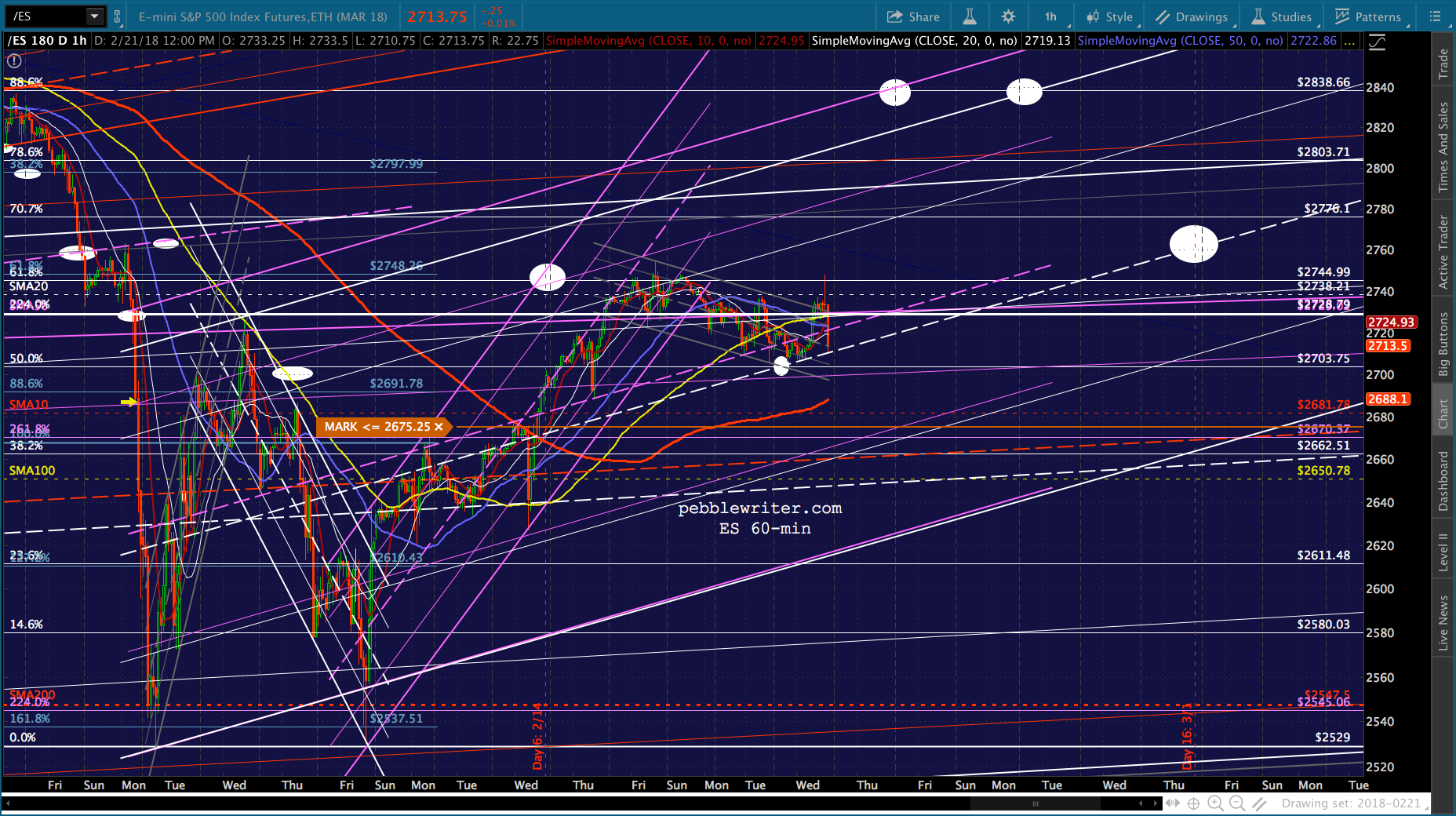

ES is sliding through the presumed midline, but that could always correct overnight.

UPDATE: 4:00 PM

UPDATE: 4:00 PM

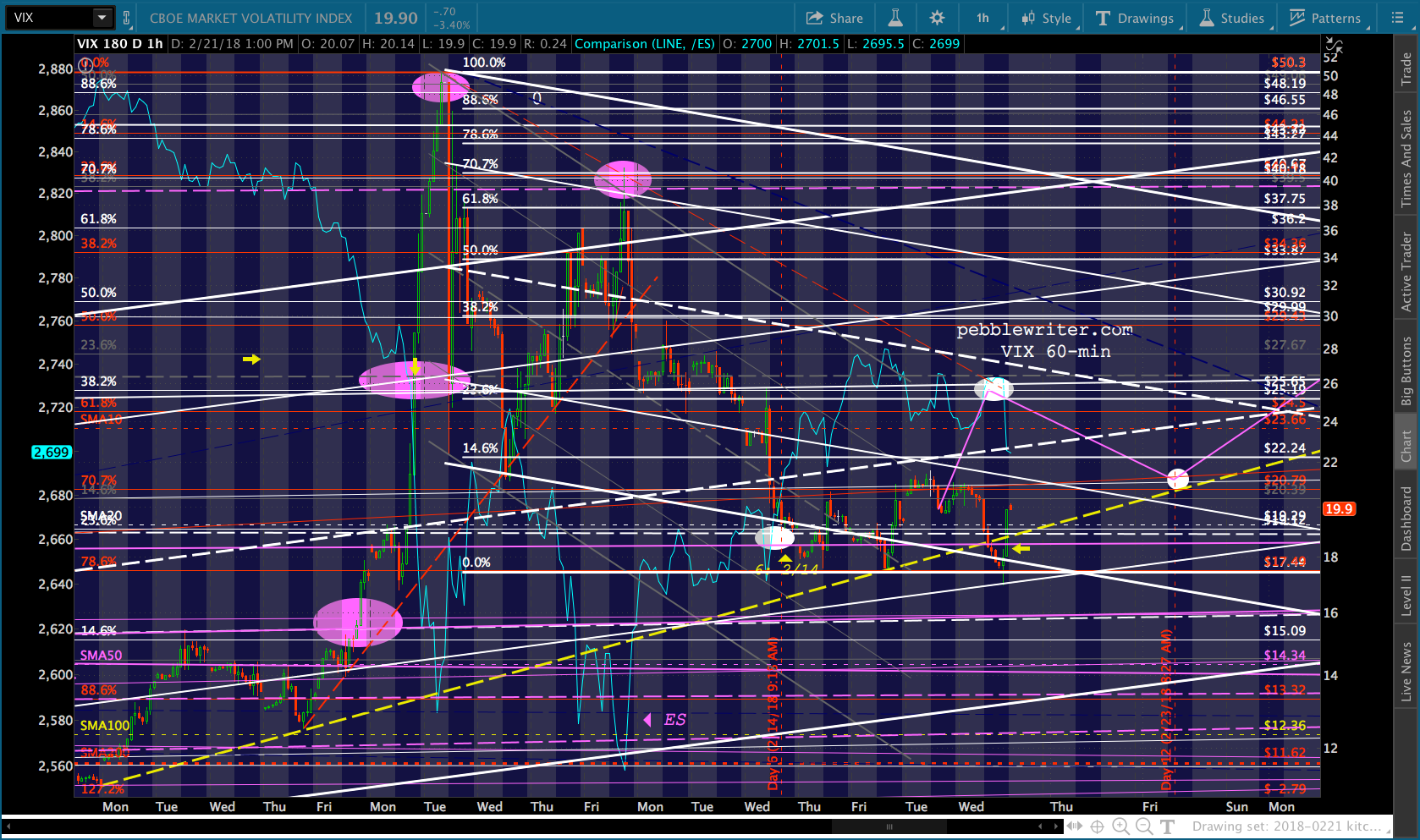

Tagged, but still slipping as VIX continues to slowly rise. Maybe some follow through on the futures and with VIX overnight? Having VIX rise up to 22-26 overnight would give it a higher perch from which to plunge in the morning. And, maybe ES could make it down to its SMA10 at 2681.78 and bounce back, much as it did when it tagged its SMA200 4 sessions ahead of SPX.

If you love head-fakes, you’re having a great time lately!

If you love head-fakes, you’re having a great time lately!