Futures are flat as we approach the open, off from their overnight highs as VIX crept back above its SMA10 moments ago. At least the sharp rebound answered the question we had regarding the timing of this correction.

continued for members… (more…)

continued for members… (more…)

Futures are flat as we approach the open, off from their overnight highs as VIX crept back above its SMA10 moments ago. At least the sharp rebound answered the question we had regarding the timing of this correction.

continued for members… (more…)

In our last update [see: May 19 Update] we noted that BTC had reached our downside target of 30,108 months ahead of schedule and was due for a rebound.

The bigger picture indicates we should see a reversal here with at least a backtest of the SMA200 at 39,800ish.

As it turned out, BTC backtested the SMA200 the very next day – failing to break back above it and beginning a long, slow decline which continues to this day.  There are as many opinions about its future as there are billionaires blasting off into space. We’ll take a fresh look at what the charts, which have been incredibly accurate to date, have to say.

There are as many opinions about its future as there are billionaires blasting off into space. We’ll take a fresh look at what the charts, which have been incredibly accurate to date, have to say.

continued for members… (more…)

ES tagged our first downside target two sessions ahead of schedule yesterday. As my good friend (and brilliant trader) Ed put it…

All of our charts remain on track.

All of our charts remain on track.

The algos are trying to make up their “minds.” Is this one of those quick plunges which will be followed by an even quicker recovery, or is there more turbulence ahead?

The algos are trying to make up their “minds.” Is this one of those quick plunges which will be followed by an even quicker recovery, or is there more turbulence ahead?

I suspect most will be surprised.

continued for members… (more…)

We’re seeing a nice start to the correction we forecast last week.

We’ve reached our next downside target in the 10Y, which seems to finally have attracted attention from the algos. Remember, there’s still a gap to fill at 1.20%.

As expected, USDJPY, CL and RB have rolled over and broken down – leaving futures without much support at all. Our downside targets, essentially the same since May 26 [see: What’s the Holdup?], remain unchanged. The upshot: a wild ride ahead.

As expected, USDJPY, CL and RB have rolled over and broken down – leaving futures without much support at all. Our downside targets, essentially the same since May 26 [see: What’s the Holdup?], remain unchanged. The upshot: a wild ride ahead.

continued for members… (more…)

continued for members… (more…)

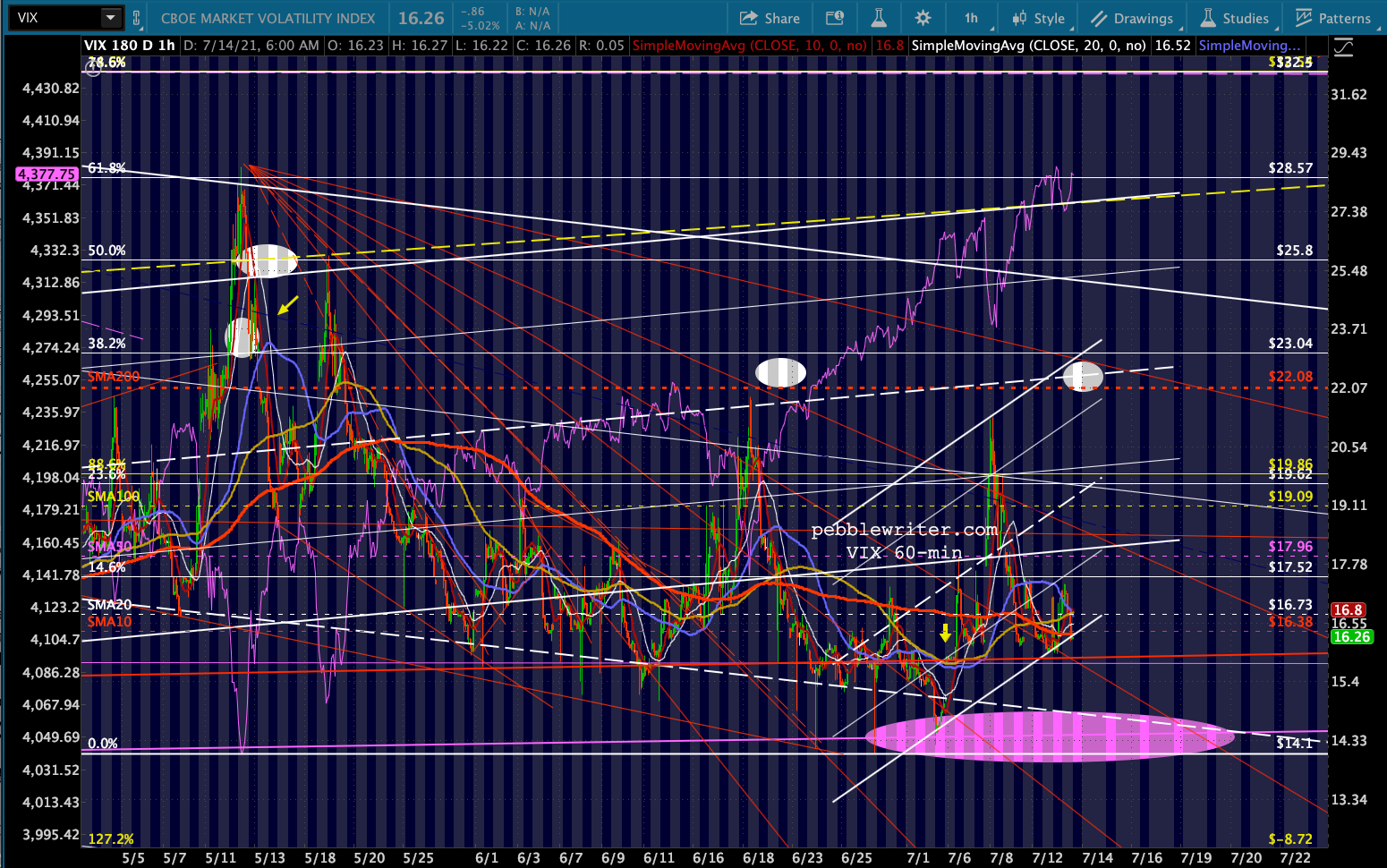

Another overnight session of VIX being hammered back below the SMA10 and melting up futures… Will it ever end?

ES spent hours bouncing at its SMA10 yesterday, finally breaking down – perhaps as carbon-based investors began contemplating the Fed’s dilemma. But, no surprise, VIX cratered into the close and got ES back above its SMA10 just in time.

ES spent hours bouncing at its SMA10 yesterday, finally breaking down – perhaps as carbon-based investors began contemplating the Fed’s dilemma. But, no surprise, VIX cratered into the close and got ES back above its SMA10 just in time.

SPX is on session #18 with a close above its own SMA10, with two of those coming late in the day on a VIX smackdown.

It appears that the algos are betting on VIX avoiding a bullish (bearish for stocks) 10/20 cross. I believe they’re wrong this time. I believe our 10% correction has finally arrived.

It appears that the algos are betting on VIX avoiding a bullish (bearish for stocks) 10/20 cross. I believe they’re wrong this time. I believe our 10% correction has finally arrived.

continued for members… (more…)

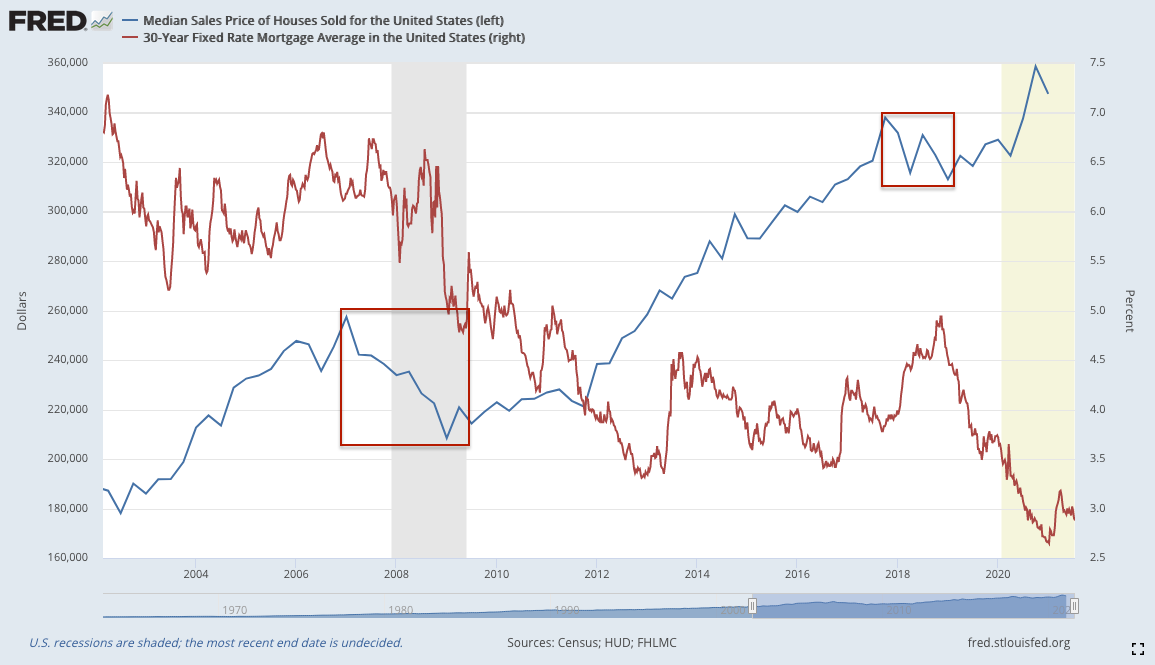

I’ve recently discussed this very issue with several friends who are a little nervous about the sharp runup in prices…and very nervous about the prospect of a selloff.

Most of us remember how ugly things got during the Great Financial Crisis: the sharp rise and the much sharper plunge when the bubble burst. According to HUD, the median sales price of a home fell about 20% from $257,400 in Q1:2007 to $208,400 in Q1:2009.  The fallout was both disastrous and widespread. Yet, years later, it appears modest compared to the subsequent reinflation. The median sales price reached $358,700 in Q4:2020.

The fallout was both disastrous and widespread. Yet, years later, it appears modest compared to the subsequent reinflation. The median sales price reached $358,700 in Q4:2020.  It’s the size and speed of the bubble’s reflation that has many worried – particularly given the Fed’s involvement. How so, you ask?

It’s the size and speed of the bubble’s reflation that has many worried – particularly given the Fed’s involvement. How so, you ask?

In the wake of the pandemic, the Fed cut short-term rates to zero and began large scale asset purchases which have been more than enough to purchase the entirety of Treasury’s monthly borrowings: $120 billion per month, including $40 billion in mortgages. The net effect was to drive interest rates to all-time lows and keep them there.

If you’re feeling pretty smart about all the money you’ve made in real estate over the past year, make sure you fire off a thank you note to Jerome Powell.

If you’re feeling pretty smart about all the money you’ve made in real estate over the past year, make sure you fire off a thank you note to Jerome Powell.

Most home buyers purchase as much house as their income will allow. That is, they focus more on the monthly payment than the purchase price. Lenders, likewise, use a formula to compare your monthly housing costs to your income.

These debt-to-income ratios vary. But, in this example, we’ll assume a 33% ratio – meaning the total house payment should be no more than 33% of your monthly gross income.

A home purchased for $1 million with a $200,000 down payment at the current jumbo mortgage rate of 2.6% would require a monthly payment of about $3,203. Toss in $1,000 per month for taxes and insurance, and you’d be looking at a total payment of $4,203. With a 33% ratio, the required annual income would be around $152,826.

If mortgage interest rates had been 6% instead of 2.6%, the monthly payment for that same $1 million house would have been much higher: about $5,796, requiring an income of $210,778 to qualify for an $800,000 mortgage.

And, there’s the rub. Cutting rates to all-time lows clearly reinflated real estate prices. People have been able to afford more and more expensive homes because the Fed kept cutting rates, keeping the payments super low even as the prices soared.

What happens if rates ever rise back to normal levels? The chart below shows the relationship between falling rates and rising prices. But, you can read it the other way around too. If rates rose, what would the price need to drop to in order to maintain the same monthly payment?

A rise in rates from 2.6% to 3.6% equates to a price drop from $1 million to $880,000. A rise to 4.6% would mean a drop to $780,000 – enough to wipe out your equity and leave you owing money at the closing.*

The Fed has managed to hold interest rates low by buying up all the bonds it sees. The flood of QE required to suppress rates has bid up not just real estate but most other categories of goods and services as well, thereby amping up the pressure to raise rates.

The Fed could mitigate inflation by raising rates or suppressing oil prices, but either would do some damage to stocks – another overinflated market. So, instead, they keep insisting that everything’s just fine, even as they paint themselves into a corner.

Is it time to sell your home? If you’re planning on it any time soon, consider the above and keep a very close eye on the market and on interest rates. It won’t necessarily happen tomorrow. In fact, sales/prices typically increase in the short run when rates begin to rise because buyers fear even higher mortgage rates to come.

But, spoiler alert: it will happen by this time next year. The Fed is playing a dangerous game – not because they love taking enormous risks but because, having reinflated all these bubbles, they have no other choice.

We all remember what happened the last time inflation reached these levels. From the July 2008 FOMC statement to Congress, the only time in the past 30 years that CPI has topped last month’s 5.4%:

We all remember what happened the last time inflation reached these levels. From the July 2008 FOMC statement to Congress, the only time in the past 30 years that CPI has topped last month’s 5.4%:

According to these projections, the economy is expected to expand slowly over the rest of this year. FOMC participants anticipate a gradual strengthening of economic growth over coming quarters as the lagged effects of past monetary policy actions, amid gradually improving financial market conditions, begin to provide additional lift to spending and as housing activity begins to stabilize.

Stocks crashed 50% over the next 8 months as the Great Financial Crisis decimated the economy.

* * *

* the spreadsheet below shows the effect on price of a change in mortgage rates, while holding payment and qualifying income steady.

No one laid a glove on Powell during his House testimony yesterday. His assertions regarding inflation and economic growth went largely unchallenged. In fact, 10Y yields are off this morning, testing 1.32 moments ago. Can he continue to fool most of the people most of the time? It’s worked out pretty well so far, with plenty of investors willing to ignore the inevitable outcome of the inflationary path we’re on.

Can he continue to fool most of the people most of the time? It’s worked out pretty well so far, with plenty of investors willing to ignore the inevitable outcome of the inflationary path we’re on.

continued for members… (more…)

Powell’s testimony to the House today should be informative, but it usually isn’t. By now he’s learned that it just doesn’t pay to be honest and forthright about what’s happening in the economy (e.g. “inflation isn’t a problem.”) Wouldn’t it be nice if someone called him on it, asking him how exactly spiraling inflation is supposed to help all the little people he claims to be so concerned about?

Nevertheless, the algos are prepped for a stick save should one be needed in the wake of reckless truthiness, with VIX predictably back below its SMA10 and positioned for a breakdown.

continued for members… (more…)

If you’re wondering what the noise was, it was the Fed’s “transitory” explanation doing a big fat face plant after June’s inflation data were released.

Headline annual CPI came in at 5.4%, the highest print since June 2008 and the second highest since Nov 1990. The 0.9% MoM print (headline and core) was also the highest since June 2008. Core CPI, at 4.5%, was the largest increase since November 1991.

Importantly, the data reveals that although energy prices might have led the charge to these lofty levels…

…inflation is now both widespread and endemic. Most categories increased by at least 4% YoY and nearly all categories increased in June at an annualized rate of over 4%.

…inflation is now both widespread and endemic. Most categories increased by at least 4% YoY and nearly all categories increased in June at an annualized rate of over 4%.

continued for members…

Seemingly every great Western has a scene when a bunch of cowboys are riding nonchalantly through an obvious place for an ambush when one of them (the dimwit) optimistically mutters, “purdy quiet.” Our hero knowingly replies, “yeah…too quiet” at which point all hell breaks loose. The dimwit is the first one to bite the dust. This week could be a lot like that.

There are scads of economic data due out this week, many of which could move markets.

But, a few of them could result in all hell breaking loose: tomorrow’s CPI data, Powell’s testimony to Congress Wednesday and Thursday, and retail sales on Friday.

But, a few of them could result in all hell breaking loose: tomorrow’s CPI data, Powell’s testimony to Congress Wednesday and Thursday, and retail sales on Friday.

continued for members… (more…)