Seemingly every great Western has a scene when a bunch of cowboys are riding nonchalantly through an obvious place for an ambush when one of them (the dimwit) optimistically mutters, “purdy quiet.” Our hero knowingly replies, “yeah…too quiet” at which point all hell breaks loose. The dimwit is the first one to bite the dust. This week could be a lot like that.

There are scads of economic data due out this week, many of which could move markets.

But, a few of them could result in all hell breaking loose: tomorrow’s CPI data, Powell’s testimony to Congress Wednesday and Thursday, and retail sales on Friday.

But, a few of them could result in all hell breaking loose: tomorrow’s CPI data, Powell’s testimony to Congress Wednesday and Thursday, and retail sales on Friday.

continued for members…Futures are off slightly.

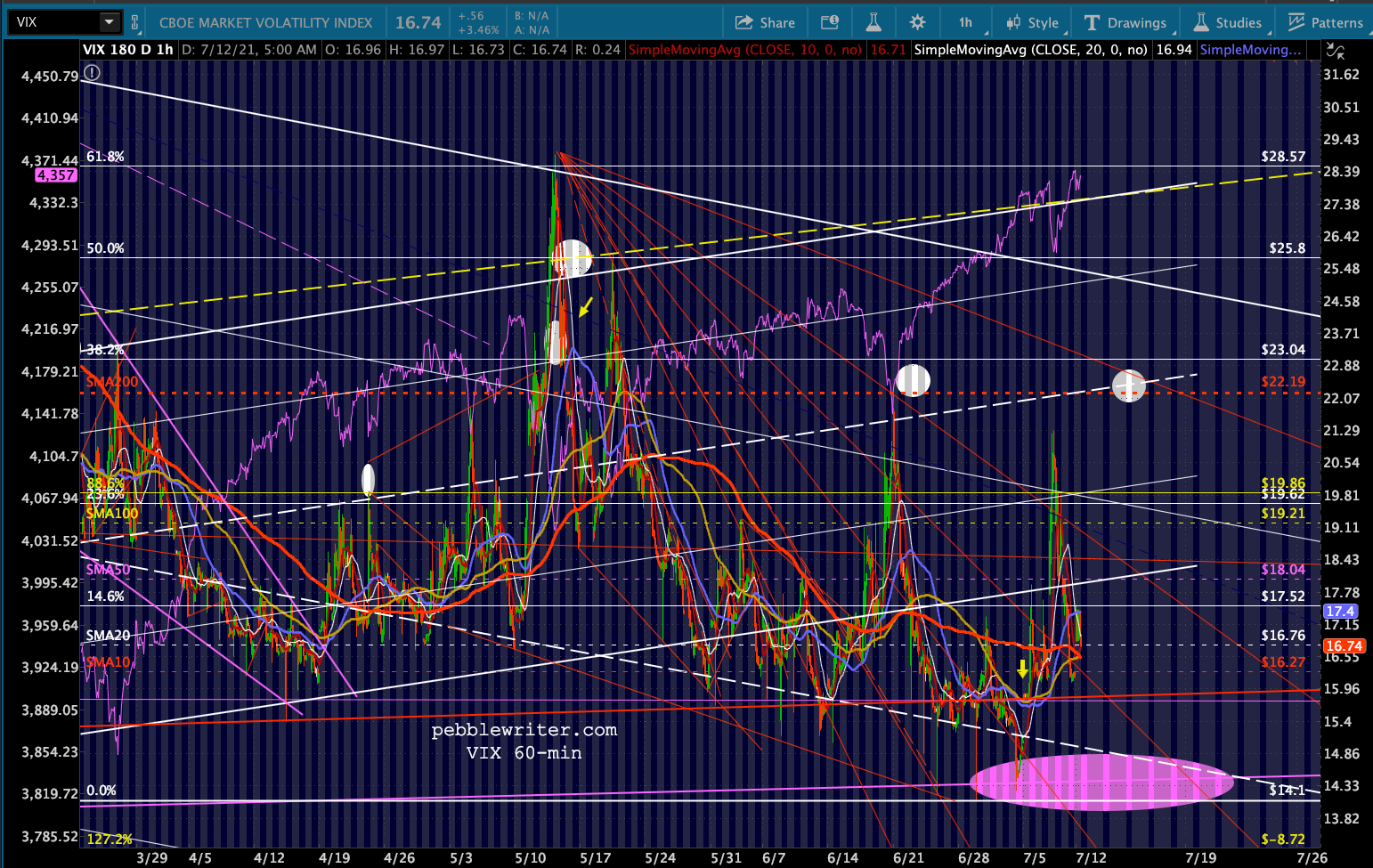

VIX popped up over the SMA10 overnight, but is not surprisingly headed back toward it.

VIX popped up over the SMA10 overnight, but is not surprisingly headed back toward it.

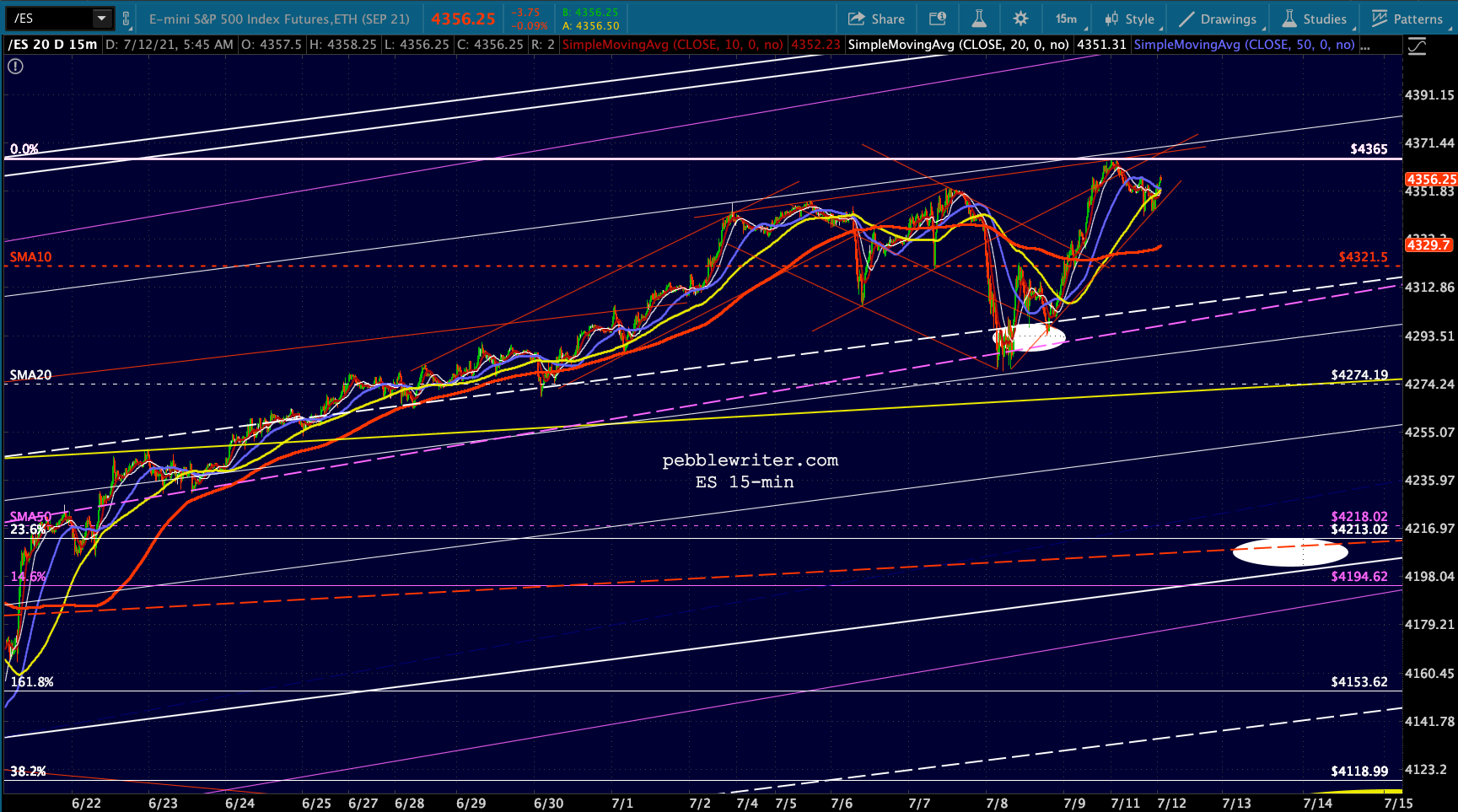

Pretty much everything else is on hold – in position to react to mitigate a big drop in equities if tomorrow’s CPI is alarming. CL and RB are in position to break out.

Pretty much everything else is on hold – in position to react to mitigate a big drop in equities if tomorrow’s CPI is alarming. CL and RB are in position to break out.

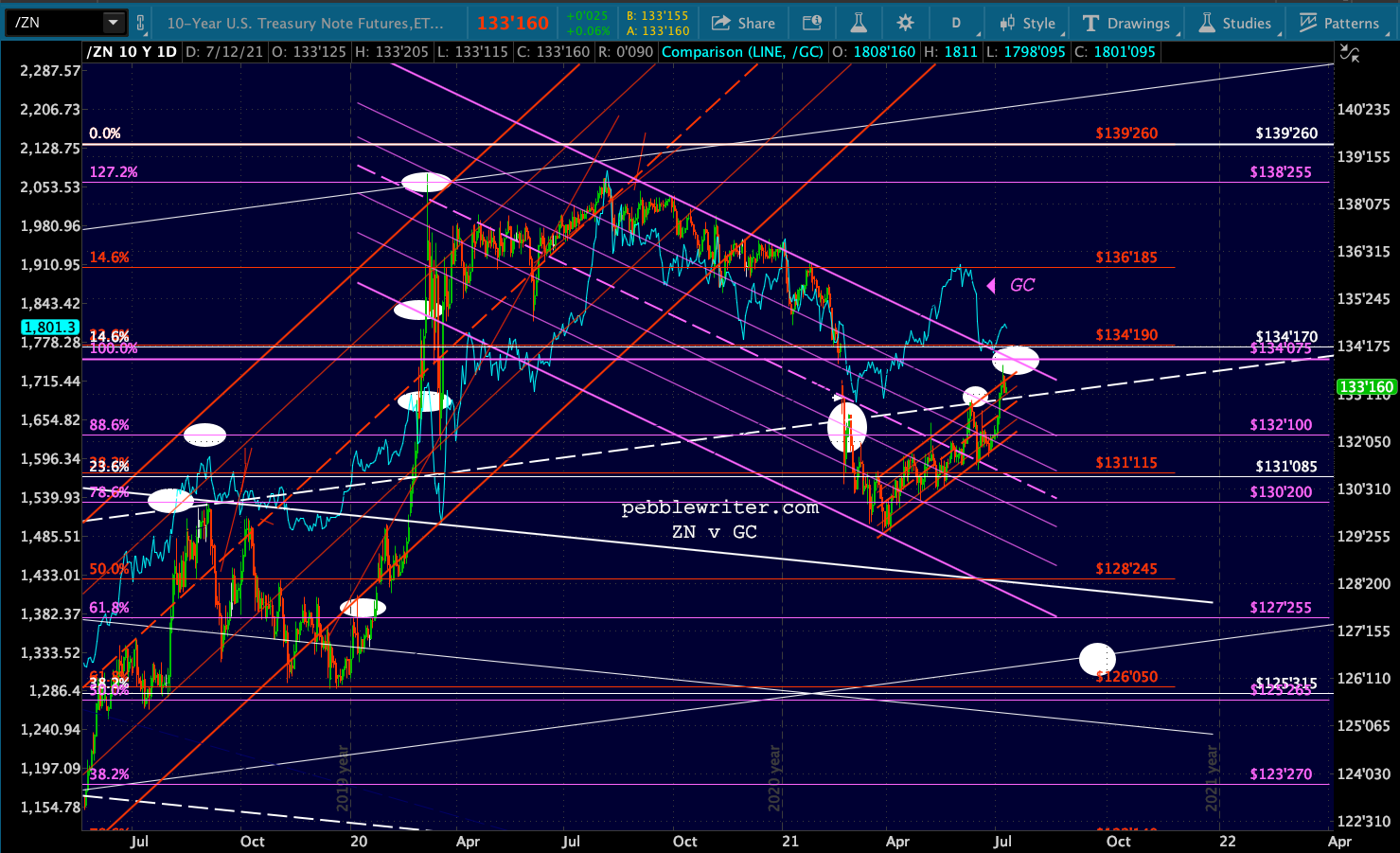

While USDJPY is hinting at a break back above its recently broken TL and bounce off that white channel line we talked about last week.

While USDJPY is hinting at a break back above its recently broken TL and bounce off that white channel line we talked about last week. EURUSD is getting a counter-trend bounce.

EURUSD is getting a counter-trend bounce. Meaning DXY is pausing.

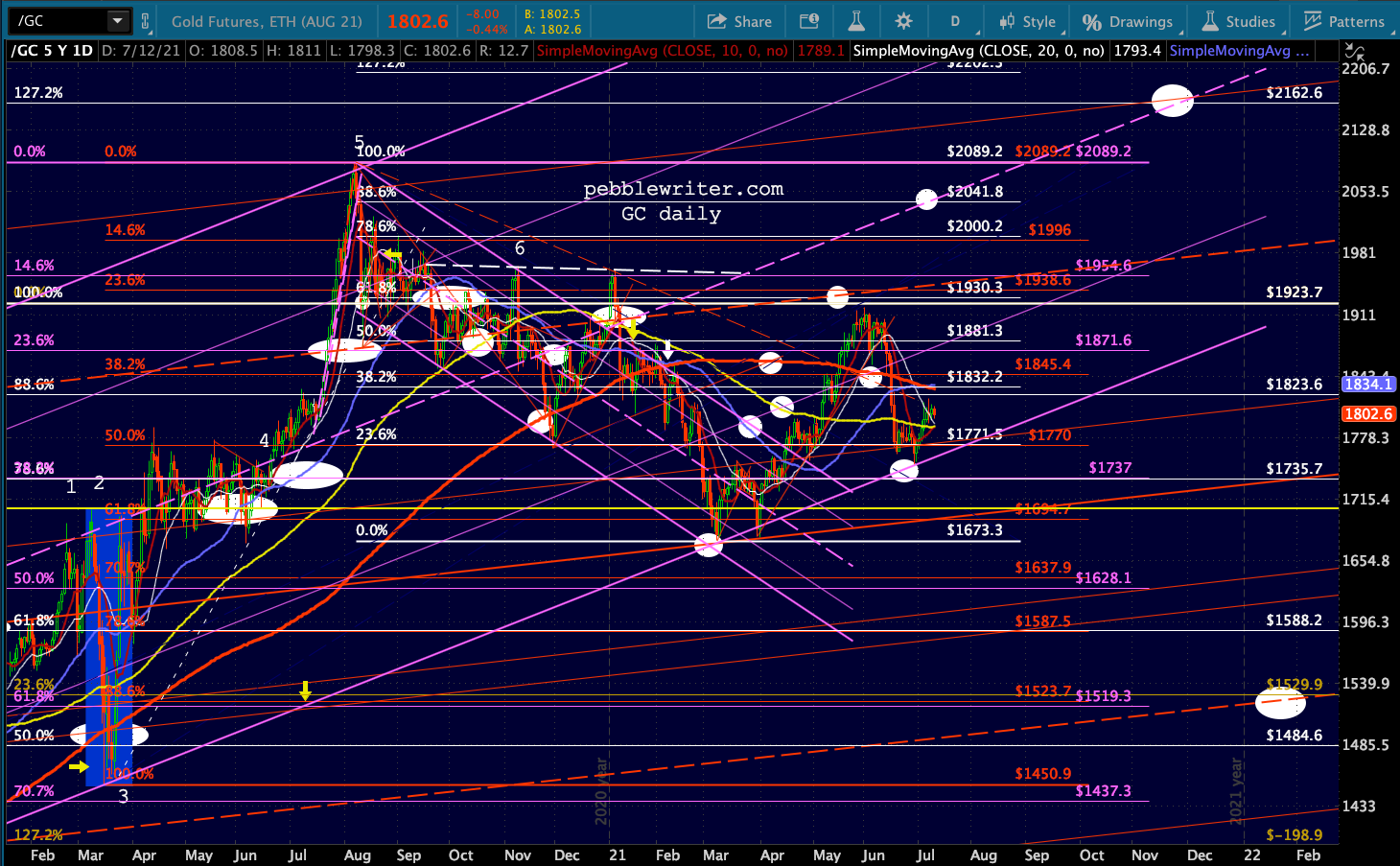

Meaning DXY is pausing.  GC and SI are still treading water.

GC and SI are still treading water.

And, TNX is bouncing off last weeks lows.

And, TNX is bouncing off last weeks lows.

And, BTC is still slipping lower. The downside case makes more sense at this point.

And, BTC is still slipping lower. The downside case makes more sense at this point. I have several conference calls lined up this morning. I’ll post updated CPI estimates in a couple of hours.

I have several conference calls lined up this morning. I’ll post updated CPI estimates in a couple of hours.

UPDATE: 3:30 PM

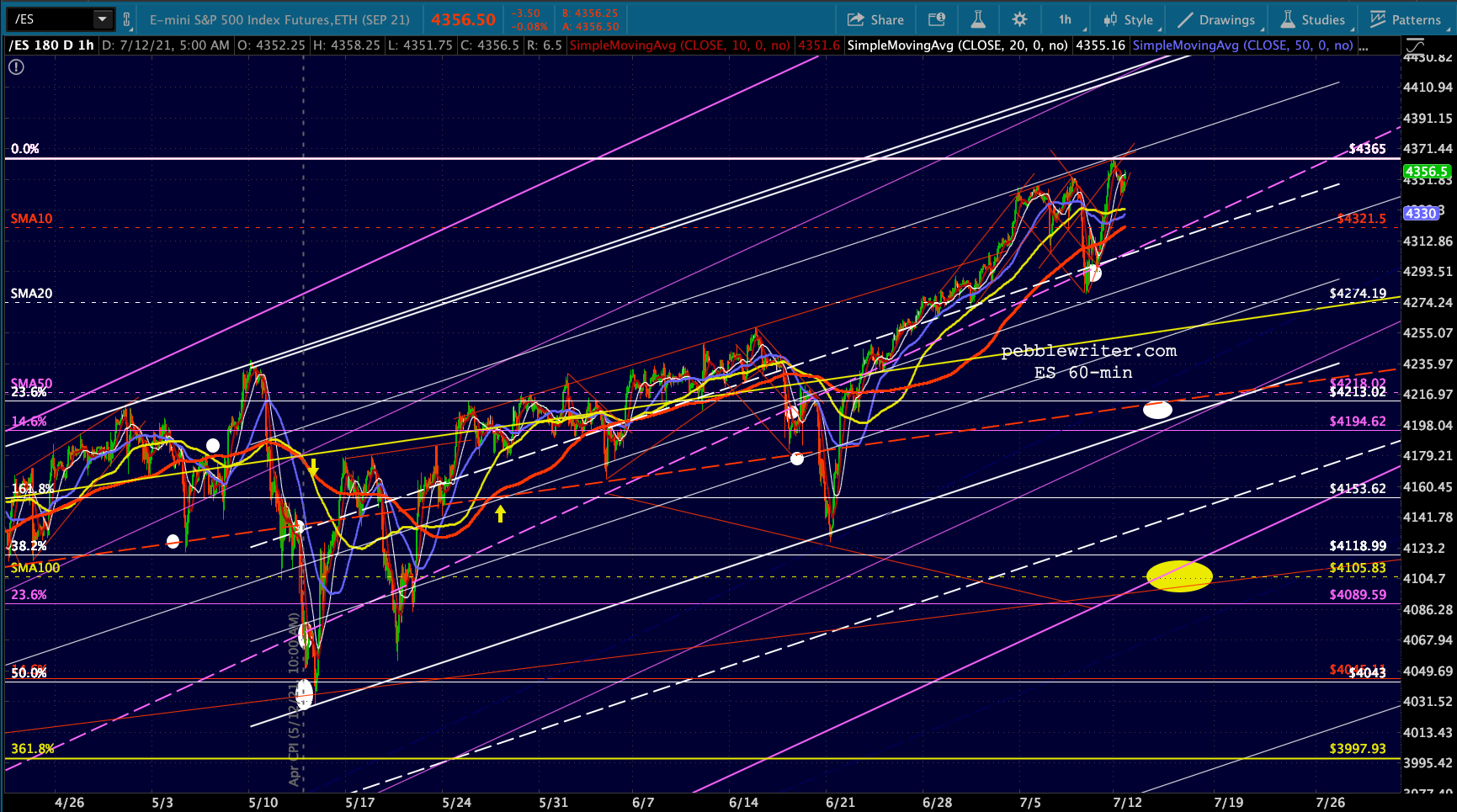

Still purdy quiet, but that hasn’t stopped VIX from drifting back down to the SMA10 (4th time in the last 5 sessions) and ES from scampering up to new all-time highs.

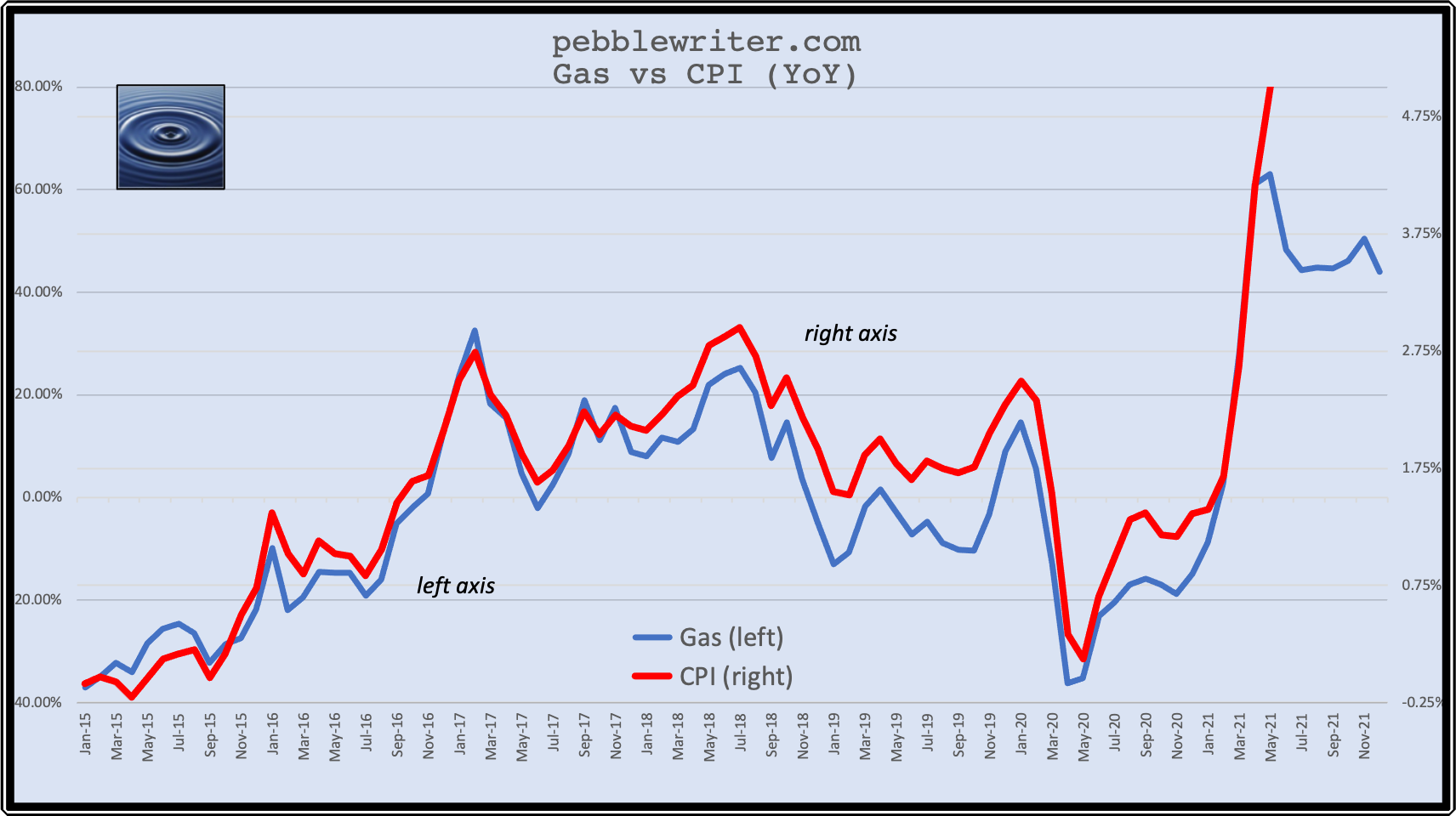

About tomorrow’s CPI…I can see two potential outcomes. We discussed last month, when May CPI hit 5%, that it soared even more than was explainable by the YoY gas price increase.

About tomorrow’s CPI…I can see two potential outcomes. We discussed last month, when May CPI hit 5%, that it soared even more than was explainable by the YoY gas price increase.  This was due to the other categories, some related to energy prices and some not, which also experienced stronger inflation. Almost all other categories – especially other commodities, food away from home, gas service, apparel and transportation – rose faster than usual…

This was due to the other categories, some related to energy prices and some not, which also experienced stronger inflation. Almost all other categories – especially other commodities, food away from home, gas service, apparel and transportation – rose faster than usual…

… and significantly faster than in April.

… and significantly faster than in April.

Since the YoY gasoline price increase has leveled off and will – unless prices suddenly shoot higher this month – drop somewhat over the coming months (at least through October) then it will be up to these other categories to keep the rate of inflation at 5% if it’s in the cards.

Since the YoY gasoline price increase has leveled off and will – unless prices suddenly shoot higher this month – drop somewhat over the coming months (at least through October) then it will be up to these other categories to keep the rate of inflation at 5% if it’s in the cards.

The two scenarios, then, are that the other categories moderate some and CPI pulls back from 5% or the other categories continue to increase just as rapidly and push CPI even higher. As we’ve discussed many times before, several of these data points are just hogwash. Shelter, for instance, is growing much faster than 2.2% annually. So, in a sense, the whole calculation is an exercise in hoodwinkery.

By essentially buying up all the Treasury’s new issues, the Fed has been able to very effectively suppress interest rates – leading inflation watchers to wonder whether inflation even matters any more. Fair question. I see the data more as an indication of what the Fed wants people to believe and what expectations it hopes to establish.

On that basis, I’ll be surprised if CPI doesn’t pull back at least a little, say 4.4-4.6%. It’s still a robust number but will allay fears that inflation is running away to the upside. Stay tuned.