Futures are off about 20 points this morning, but it’s last week’s breakout that has us wondering whether the downside case is still intact.

continued for members… (more…)

Futures are off about 20 points this morning, but it’s last week’s breakout that has us wondering whether the downside case is still intact.

continued for members… (more…)

I didn’t set out to be an FX analyst. About the only time I ever focused on currencies was when planning a trip abroad, which seemed to always line up with USD lows. Eight dollars for a croissant? Really?

Ten years ago, however, I began to notice how closely aligned equity performance was with moves in the USDJPY and EURUSD. That curiosity blossomed into a robust appreciation of the fact that many currency moves have become tools for central bankers to support equity markets.

On April 23 [see: A New Catalyst] despite the fact that USDJPY had been locked in a falling channel since November 2016 and was seemingly breaking down, I added the breakout target shown below due to what I reasoned was stocks’ vulnerability at the time.

This morning, USDJPY reached that very target for precisely that same reason.

This morning, USDJPY reached that very target for precisely that same reason.

Likewise, EURUSD was seemingly breaking out of a downtrend. I expected the breakout to ultimately fail and for EURUSD to very gradually backtest the channel from which it had broken out. This would be the least disruptive outcome for stocks.

Likewise, EURUSD was seemingly breaking out of a downtrend. I expected the breakout to ultimately fail and for EURUSD to very gradually backtest the channel from which it had broken out. This would be the least disruptive outcome for stocks. A few days ago, EURUSD completed that backtest – after several more headfakes along the way of course.

A few days ago, EURUSD completed that backtest – after several more headfakes along the way of course. My point isn’t that I’m any smarter than other FX analysts. It’s simply that we can usually count on central bankers to manipulate whatever is handy (interest rates, currency exchange rates, vol, etc.) to prop up stocks.

My point isn’t that I’m any smarter than other FX analysts. It’s simply that we can usually count on central bankers to manipulate whatever is handy (interest rates, currency exchange rates, vol, etc.) to prop up stocks.

This morning’s move was fairly predictable only because it was apparent that the BoJ (the reigning world’s best market manipulators) wouldn’t be satisfied with NKD’s backtest and reversal at its 200-day moving average. Thanks to USDJPY’s strong overnight move, the Nikkei had no trouble spiking through that particular overhead “resistance.”

At no time does the manipulation get more frenzied than around options expiration day. Today is one of those days and, as usual, stocks have gone hog wild in an effort to cause as many of the puts purchased over the past month as possible to expire worthless.

At no time does the manipulation get more frenzied than around options expiration day. Today is one of those days and, as usual, stocks have gone hog wild in an effort to cause as many of the puts purchased over the past month as possible to expire worthless.

The falling channel which has faithfully guided stocks lower since our correction call in early September has seemingly been busted.  Of course, that was also the case on September 16 after ES had popped through the yellow trend line and was apparently breaking out of the falling white channel going into the close.

Of course, that was also the case on September 16 after ES had popped through the yellow trend line and was apparently breaking out of the falling white channel going into the close.

The ruse continued into options expiration on Sep 17, at which point the bottom fell out and stocks suffered their worst two day plunge in months.

The ruse continued into options expiration on Sep 17, at which point the bottom fell out and stocks suffered their worst two day plunge in months.

Why does it matter, you ask? Because we’re in a very similar situation all over again. Based on the market action yesterday and today, you’d be crazy to short stocks. Which is exactly what the market makers want you to think.

Why does it matter, you ask? Because we’re in a very similar situation all over again. Based on the market action yesterday and today, you’d be crazy to short stocks. Which is exactly what the market makers want you to think.

continued for members… (more…)

If you’re looking for producer prices to level off and take the pressure off consumer prices, don’t hold your breath. If anything, September’s print should serve as a strong reminder that something’s gotta give. Either consumers or retailers will bear the brunt of rising prices, and neither is all that positive for markets.

Speaking of markets, futures have completed their trip to the falling channel top just in time for OPEX tomorrow. Absent a world class head fake, this should be the hopping off point for the latest algo-driven bounce.

Speaking of markets, futures have completed their trip to the falling channel top just in time for OPEX tomorrow. Absent a world class head fake, this should be the hopping off point for the latest algo-driven bounce. It’s been 5 weeks since we announced a correction watch, with SPX having given up a little less than 6% at its worst. Should there be another leg down, it should be about ready to get started.

It’s been 5 weeks since we announced a correction watch, with SPX having given up a little less than 6% at its worst. Should there be another leg down, it should be about ready to get started.

continued for members…

(more…)

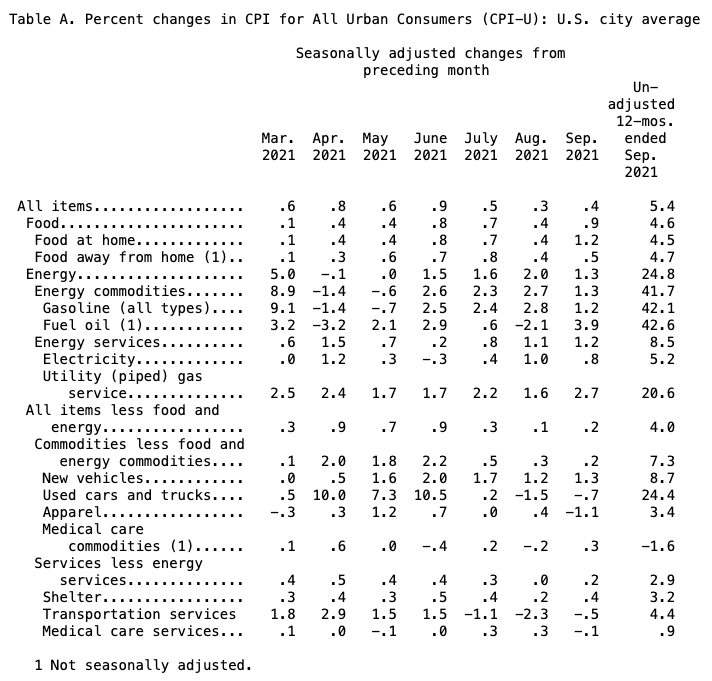

It’s almost like a line from a vintage SNL weekend update.

See if you can find a category in Table A below which is susceptible to price decreases.

Blame it on supply chain shortages rather than trillions in stimulus if you like, but the current inflation spike is likely to be with us for quite some time. Only the BLS’s cooked books prevented a new 20-year high.  It goes without saying that the uncooked numbers are much worse. Take this chart, for instance, comparing actual apartment rental rates to the BLS’ fictional OER.

It goes without saying that the uncooked numbers are much worse. Take this chart, for instance, comparing actual apartment rental rates to the BLS’ fictional OER.

Futures dipped back to UNCH on the news, looking as though they might even turn negative. But, the algos were transfixed by VIX’s daily pre-opening dip below its SMA200 and, well, we all know how that works.

Futures dipped back to UNCH on the news, looking as though they might even turn negative. But, the algos were transfixed by VIX’s daily pre-opening dip below its SMA200 and, well, we all know how that works.

continued for members… (more…)

continued for members… (more…)

This little article on Reuters caught my eye this morning.

Japan’s new Prime Minister Fumio Kishida noted that a weaker yen would exacerbate Japan’s spiraling wholesale prices (+6.3% last month.)

Japan’s new Prime Minister Fumio Kishida noted that a weaker yen would exacerbate Japan’s spiraling wholesale prices (+6.3% last month.)

Of course, the weaker yen – a result of the yen carry trade – is a big reason why stocks are so high.

As we’ve discussed many times in the past, the trade has its limits. When the yen weakens significantly at the same time that oil/gas prices are rising rapidly, something has to give.

Otherwise, you end up with untenable price increases…

…which lead to untenable inflation…

…which lead to untenable inflation… …which in turn lead to untenable interest rates (in Japan, anything above 0%.)

…which in turn lead to untenable interest rates (in Japan, anything above 0%.) Now, Japan’s bond market is even more broken than the US bond market. The journey to NIRP has been going on for a long, long time.

Now, Japan’s bond market is even more broken than the US bond market. The journey to NIRP has been going on for a long, long time.  Given Japan’s 272% debt to GDP ratio, it’s been necessary.

Given Japan’s 272% debt to GDP ratio, it’s been necessary.

[The US is expected to exceed that ratio by 2029, but I digress.] The last time Japan’s producer prices increased this rapidly was in 2014…

[The US is expected to exceed that ratio by 2029, but I digress.] The last time Japan’s producer prices increased this rapidly was in 2014… …when CPI also neared 4%. It wasn’t a good look for a central bank which required negative interest rates in order to avoid the appearance of technical default.

…when CPI also neared 4%. It wasn’t a good look for a central bank which required negative interest rates in order to avoid the appearance of technical default.

Then, as now, it was largely a function of sharply rising oil prices. Clearly, oil prices needed to come down.

Then, as now, it was largely a function of sharply rising oil prices. Clearly, oil prices needed to come down.  But, how could they do that without killing off the rally from 2011’s Fukushima lows? Easy. The yen carry trade, which had helped the Nikkei almost double in the two years since Fukushima…

But, how could they do that without killing off the rally from 2011’s Fukushima lows? Easy. The yen carry trade, which had helped the Nikkei almost double in the two years since Fukushima… …came to the rescue. Not coincidentally, USDJPY broke out on the exact same day that WTI broke down.

…came to the rescue. Not coincidentally, USDJPY broke out on the exact same day that WTI broke down.

The carry trade’s influence on the algos prevented crashing oil prices from also crashing stocks. And, cratering oil prices prevented the crashing yen from exacerbating inflation. It was a win-win. By the end of the 2014 CPI was down below 0%, 10Y yields were slashed in half, and the Nikkei had risen an additional 20%.

The carry trade’s influence on the algos prevented crashing oil prices from also crashing stocks. And, cratering oil prices prevented the crashing yen from exacerbating inflation. It was a win-win. By the end of the 2014 CPI was down below 0%, 10Y yields were slashed in half, and the Nikkei had risen an additional 20%.

What if USDJPY hadn’t broken out to offset oil’s breakdown? We got a taste of that in October 2018 when oil/gas reversed lower following Jamal Khashoggi’s murder. WTI plunged 45% in a little over 11 weeks, while USDJPY shed about 8.7% and stocks swooned by 21%.

Why does this matter? We can see from the 10Y chart that rates are testing 0% again, even though the BoJ continues to suppress interest rates. It’s no wonder that rates are breaking out given that broad-based inflation is on the rise.

Rates are threatening to break out in the US and the euro zone as well.

The most expeditious way to get inflation under control is to hammer oil/gas prices lower. But, how to keep stocks from following suit if, as PM Kishida intimates, the yen carry trade is off the table? How indeed.

The most expeditious way to get inflation under control is to hammer oil/gas prices lower. But, how to keep stocks from following suit if, as PM Kishida intimates, the yen carry trade is off the table? How indeed.

continued for members…

(more…)

The latest Fed speaker, Mary Daly, implied on Face The Nation that the inflationary pressures facing the country are a function of a lack of supply caused primarily by COVID.

Well, right now, Americans are feeling it in their pocketbooks. Everyone’s feeling the rising prices for energy, food, basic services, and that’s painful because they- they aren’t- we aren’t used to seeing it. It’s eye popping in some categories. And of course, that’s challenging, especially for low- and moderate-income families who were- they spend most of their money on food and energy. So, this is really hard.

And it’s also really directly related to COVID. It’s related to the supply bottlenecks, to the disruptions. That we can’t get in the global economy people fully back to work. We can’t in the US get people fully back to work. We have these really anxious to get out there and spend consumers hitting the wall of supply constraints and of course, the prices are going to- to rise. But I don’t see this as a long-term phenomena. And the issue again comes back to, if we can get through COVID, we’ll get back to the normal conditions where we’re more used to and the ones we all want.

No mention whatsoever of the $120 billion being pumped into markets every single month – money that’s sloshing around in virtually every commodity, inflating prices out of proportion to underlying demand. The bubble is especially apparent in energy prices.

The link between YoY gas price increases and CPI have been well documented here and elsewhere. Perhaps the Fed was counting on a decline in the YoY change in oil/gas prices moderating CPI as they’ve continued to insist that inflation was transitory. We should get a better idea on Wednesday, when CPI for September is released.

We’ve focused a great deal this past year on energy, as increasing oil and gas prices quickly permeate nearly every category of production and spending. Note that oil prices have broken out above the top of a channel that dates back 20+ years – which means that the expense of producing and transporting many other categories have also broken out.

We’ve focused a great deal this past year on energy, as increasing oil and gas prices quickly permeate nearly every category of production and spending. Note that oil prices have broken out above the top of a channel that dates back 20+ years – which means that the expense of producing and transporting many other categories have also broken out.

Prices need not come back down in order for CPI to moderate. They only need to slow their rate of change. Slowing the ROC, however, doesn’t necessarily leave consumers in a place where necessities are any more affordable.

Prices need not come back down in order for CPI to moderate. They only need to slow their rate of change. Slowing the ROC, however, doesn’t necessarily leave consumers in a place where necessities are any more affordable.

Gas prices, for instance, are much more expensive than at any time over the past seven years and are also threatening to break out.  Food price inflation is equally problematic.

Food price inflation is equally problematic.

While food and gas expenditures only account for 6-7% of income for top earners, they can top 50% for those in lower income categories — meaning most of the pain imposed by the Fed’s policies are felt by those least able to afford it. The bulk of the benefits – e.g. soaring stock prices – are enjoyed by those who least need them.

While food and gas expenditures only account for 6-7% of income for top earners, they can top 50% for those in lower income categories — meaning most of the pain imposed by the Fed’s policies are felt by those least able to afford it. The bulk of the benefits – e.g. soaring stock prices – are enjoyed by those who least need them.

Mary Daly tells us that “everyone’s feeling the rising prices for energy, food, basic services, and that’s painful because they- they aren’t- we aren’t used to seeing it.” This is dead wrong on at least two counts. Not everyone is feeling it – only those who eat and drive and are barely squeaking by. And, the pain has nothing to do with seeing something unusual. It’s the very real function of not being able to pay the rent or feed your family.

Mary Daly tells us that “everyone’s feeling the rising prices for energy, food, basic services, and that’s painful because they- they aren’t- we aren’t used to seeing it.” This is dead wrong on at least two counts. Not everyone is feeling it – only those who eat and drive and are barely squeaking by. And, the pain has nothing to do with seeing something unusual. It’s the very real function of not being able to pay the rent or feed your family.

* * *

Futures are off modestly this morning, but then again VIX hasn’t yet begun its pre-opening nosedive.

continued for members… (more…)

Futures are up modestly on a truly dreadful Sept jobs print (+194K vs 500K consensus.) But, it was really the collapse in VIX that ensured a green open.

VIX is now back below the SMA200 and channel top and is testing its SMA50 — all the algos needed to know.

VIX is now back below the SMA200 and channel top and is testing its SMA50 — all the algos needed to know.

continued for members… (more…)

ES’ triangle has evolved into a flag patttern, piling on another 30 points of meltup thanks to VIX’s timely meltdown.

continued for members… (more…)

continued for members… (more…)

ADP payrolls beat this morning, while mortgage applications were off. The biggest economic data of the day/week as far as stocks are concerned, though, is EIA oil inventories.

Algos have been riding the reflation trade as indicated by WTI ever since April 2020. Downturns have been very few and far between, meaning significant equity corrections have been non-existent.  As we’ve expected, however, markets are finally focusing on the impact rising oil/gas prices have had on inflation, and that’s irritating the few remaining non-Fed bond investors to the point that a (very tiny) bit of price discovery has snuck back into the market.

As we’ve expected, however, markets are finally focusing on the impact rising oil/gas prices have had on inflation, and that’s irritating the few remaining non-Fed bond investors to the point that a (very tiny) bit of price discovery has snuck back into the market.

If the Fed should ever actually taper, the risk of a reunion between economic reality and bond yields will increase. And, that’s a scenario the Fed would very much like to avoid.

Meanwhile, the holding pattern continues.

OPEX issues again?

OPEX issues again?

continued for members… (more…)

It’s the third day in a row of backtesting a bearish Head & Shoulders Pattern. Futures are up moderately, but haven’t broken out despite the algo factors’ best efforts.

Remember, only a lasting breakout busts the pattern. Backtesting only postpones the inevitable.

Remember, only a lasting breakout busts the pattern. Backtesting only postpones the inevitable.

continued for members…