I have long looked at interest rates, inflation and politics as at least as important as supply and demand in forecasting oil and gas prices. After July’s 2.95% CPI print and subsequent spike in interest rates, it seemed obvious that the Fed faced a dilemma. From Currency Crisis on the Horizon:

…the rise of inflation — caused primarily by rising oil and gas prices — is a problem. If oil and gas prices decline, inflation is reduced by quite a bit. But, the latest rally in stocks was greatly bolstered by the breakout in oil and gas. If the breakout goes away, would the rally?

Oil dropped nicely over the next week, but began a sharp rally that lasted from from mid-Aug to early October. Gas put in another leg lower through Sep 6 before joining in the rally. Sure enough, stocks responded positively. SPX gained 5%. But, the 10Y soared from 2.80 to 3.25%. Ouch.

It was obvious that oil and gas needed to come back down lest inflation and interest rates get out of control. CL (WTI futures) reached 76.9 and RB (gasoline futures) 2.15 on Oct 3 when we pulled the plug in VIX Takes The Plunge:

…CL and RB, which not only reached overhead resistance by our measure, but must deal with bearish API data, another round of Trump tweeting, and a large build in EIA inventory. I think the time has finally come to revert to short, but with tight stops in case this is a head fake.

We delved further into motives on Oct 16 in Appearances:

…since Trump is desperate to reverse the rise in gas prices, inflation, and interest rates between now and November 6 (and, to salvage billions in arms sales) don’t be surprised if we get that next leg down in oil prices very soon.

And, a few days later in Oil & Gas Come Through Again:

While baffling those who focus on fundamentals and various geopolitical risks, these price moves made perfect sense when viewed through our favored prism: “what do TPTB need them to do?”

That equation, my friends, boils down to a few essential elements: inflation, stock market support, politics and chart patterns. We know the administration craves lower inflation and interest rates and has been agitating for lower oil prices in order to accomplish this.

The following week, I added our current lower targets for oil in Time to Panic and gas in Interesting Days Ahead. And, in Coincidences and Consequences, I touched on how the Khashoggi murder likely played a role in Saudi Arabia’s sudden acquiescence.

It’s interesting how Khashoggi’s murder top-ticked oil and gas prices – and, so soon after Trump’s latest demand that OPEC lower oil prices.

I’ve received more than a few sideways glances over the past month, especially from those focused solely on fundamentals who felt it was ludicrous to suggest that Trump might be manipulating oil and gas prices in order to achieve his political goals.

Yesterday, Trump came to my defense.

“If you look at oil prices they’ve come down very substantially over the last couple of months,” Trump said. “That’s because of me. Because you have a monopoly called OPEC, and I don’t like that monopoly.”

Translated: “Voters were becoming increasingly agitated about soaring gas prices and I needed to get them back down prior to the midterm elections. I’d also like some ammunition at my disposal to keep a lid on further FOMC rate hikes.”

Touting his success in bringing prices down, of course, is specious at best. Current WTI prices are actually higher than they were before Trump’s “provocative actions” response to the February Israeli-Syria-Iran conflict laid the groundwork for his subsequent withdrawal from the JCPOA which sent prices soaring.

Touting his success in bringing prices down, of course, is specious at best. Current WTI prices are actually higher than they were before Trump’s “provocative actions” response to the February Israeli-Syria-Iran conflict laid the groundwork for his subsequent withdrawal from the JCPOA which sent prices soaring.

* * *

CL and RB have reached every downside target we’ve set for them so far, with one potential last leg down looking fairly likely. Our Oct 3 short call has produced a 20.5% gain in CL and 23.7% in RB.

But, my point isn’t to toot my own horn — though we have enjoyed a string of nice results [OIL and GAS].

I simply think it would be wise for analysts to consider central bankers’ and politicians’ objectives whilst laying out their forecasts.

continued for members…

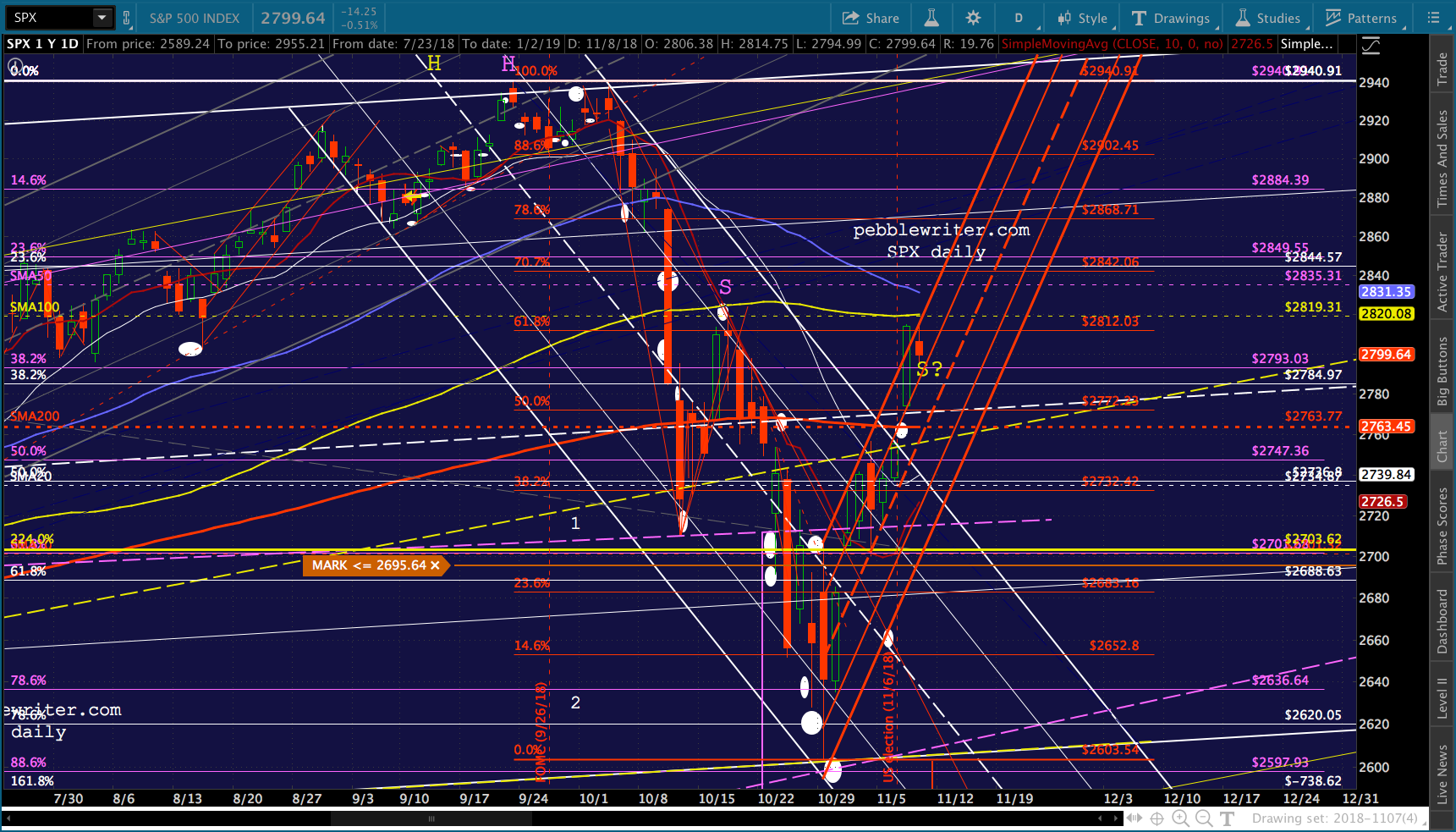

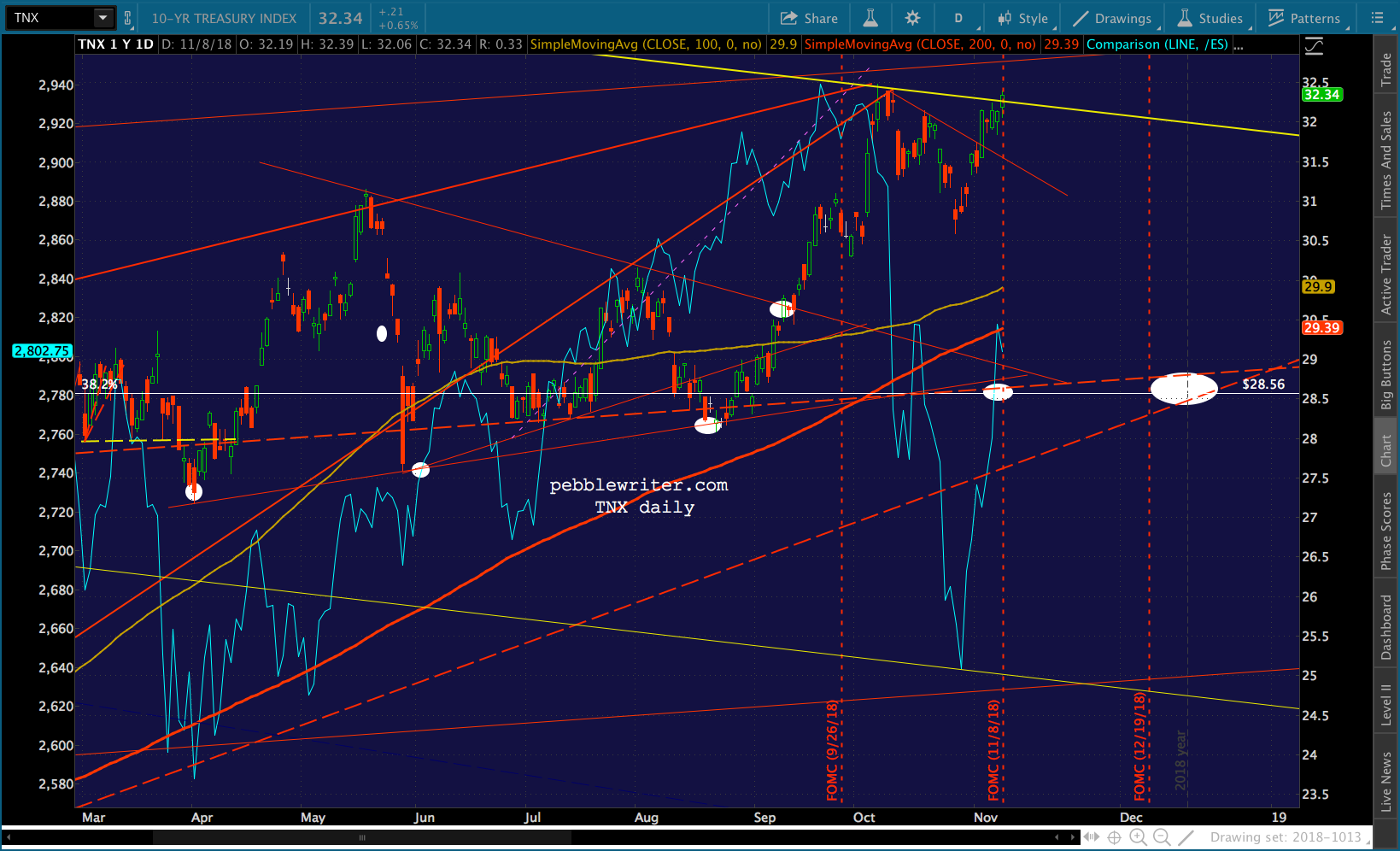

VIX is still sitting just above its SMA200, so we’ll know soon enough whether or not stocks have topped out.  USDJPY continues ramping higher.

USDJPY continues ramping higher. As such, stocks are in limbo – waiting to hear what the Fed has to say, which could potentially be damaging, but with the usual downside protection.

As such, stocks are in limbo – waiting to hear what the Fed has to say, which could potentially be damaging, but with the usual downside protection.

Note that even COMP is sitting atop its SMA200.

Note that even COMP is sitting atop its SMA200. I have to run out for a meeting, will post more later.

I have to run out for a meeting, will post more later.

UPDATE: 2:00 PM

The FOMC statement…

UPDATE: 2:45 PM

UPDATE: 2:45 PM

Nice downturn, so far. VIX is bouncing, so this reversal might have legs.

UPDATE: 3:20 PM

UPDATE: 3:20 PM

I suppose the minutes weren’t dovish enough. TNX, DXY and USDJPY are pushing higher…

…while EURUSD is headed lower.

…while EURUSD is headed lower. ES and SPX are still clinging to 2800.

ES and SPX are still clinging to 2800.

And, interestingly, COMP is back below its SMA200.

And, interestingly, COMP is back below its SMA200. If we can just get a nice bounce of of VIX’s SMA200, we should see SPX back down to its SMA200. Again, if it can’t hold, we have a slew of targets ranging from 2600 to 2703 that would align nicely with our COMP target. More on this later.

If we can just get a nice bounce of of VIX’s SMA200, we should see SPX back down to its SMA200. Again, if it can’t hold, we have a slew of targets ranging from 2600 to 2703 that would align nicely with our COMP target. More on this later. CL is soldiering on toward our downside target. When it stops, RB should too. The latest catalyst is almost laughable. Now, Saudi Arabia is considering disbanding OPEC. Riiiiight.

CL is soldiering on toward our downside target. When it stops, RB should too. The latest catalyst is almost laughable. Now, Saudi Arabia is considering disbanding OPEC. Riiiiight.

Comments

2 responses to “Trump: “Falling oil prices…that was me.””

Hello PW, while CL is going down(implying “low” inflation), the 10 year treasury yield is higher still.

It does not make sense.

Sorry I didn’t see this sooner, Tommy. The admin has been working CL lower, trying to appease consumers and get inflation low enough to prevent additional rate hikes. The Fed, meanwhile, does not want to invert the yield curve in the process of raising short-term rates. So, the 10Y has to increase enough to avoid flattening or inverting. Plus, they get the benefit of a strong dollar which mitigates inflation.