If you liked yesterday, today is shaping up as more of the same. But, there are still a few warning signs tugging at the market’s sleeve.

continued for members… (more…)

continued for members… (more…)

If you liked yesterday, today is shaping up as more of the same. But, there are still a few warning signs tugging at the market’s sleeve.

continued for members… (more…)

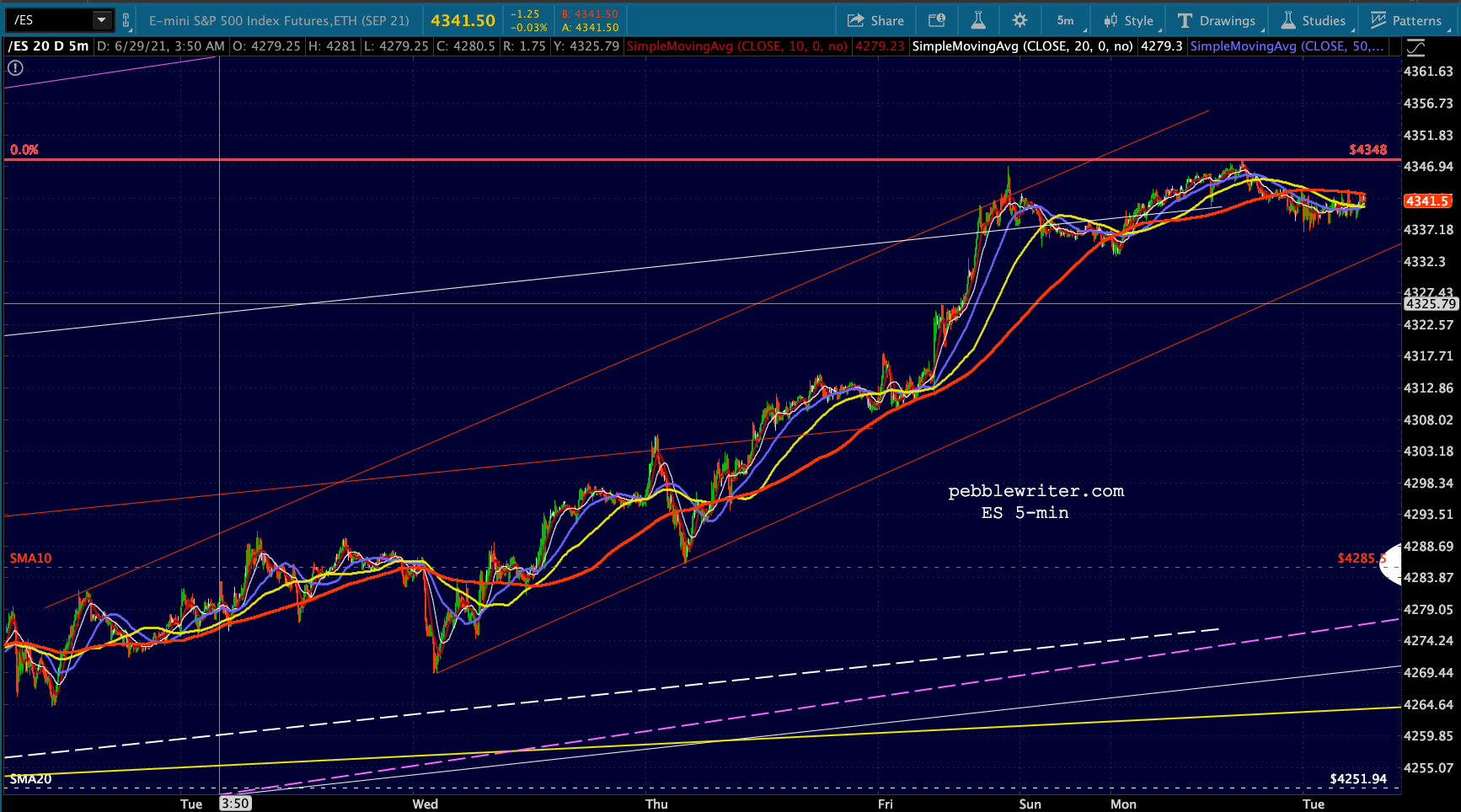

Futures are continuing their meltup in the pre-market on a 4% bounce in crude oil and the usual overnight slump in VIX.

continued for members… (more…)

continued for members… (more…)

COVID deaths continue to mount and the return to work pushes further into the future, a negative backdrop for equities at a time when they’re losing momentum from the reflation factors.

Futures are off mildly after bouncing off their overnight lows.

Futures are off mildly after bouncing off their overnight lows.

continued for members… (more…)

continued for members… (more…)

The correction is gathering steam, with ES off 40 points earlier this morning before getting a bounce. From a technical standpoint the culprit is VIX, which broke out of the falling channel which has guided stocks higher since March 2020.  Our downside targets remain unchanged.

Our downside targets remain unchanged.

continued for members… (more…)

July retail sales fell 1.1% versus -0.3% consensus, reflecting the impact of stimulus payments, Amazon’s Prime Day change, and the general apprehension surrounding the delta variant.

Yesterday’s bad news faded under heavy algo action, with VIX going into meltdown mode…

Yesterday’s bad news faded under heavy algo action, with VIX going into meltdown mode… …the instant SPX reached its SMA10.

…the instant SPX reached its SMA10.  The bears will get another shot today.

The bears will get another shot today.

continued for members… (more…)

Annual CPI remained at 5.4%, the highest in 30 years. And, that alarming number masks plenty of data which the BLS methodology simply ignores. Shelter, for instance, registered a 2.8% YoY increase per BLS’ survey-based calculation. Yet observed apartment rents increased at 9.2% in just the first six months of 2021. And, housing prices have been rising at the fastest rate in over 30 years.

Aside from the games played by the government, some non-transitory trends remain concerning: energy, vehicles and commodities all remain quite elevated. Combined with swiftly rising wages, it will be difficult to put this genie back in the bottle.

The algos are more concerned, however, with another overnight smackdown in VIX which sent S&P futures to new highs – for now. Pay attention to where that leaves some important Fib retracement levels.

The algos are more concerned, however, with another overnight smackdown in VIX which sent S&P futures to new highs – for now. Pay attention to where that leaves some important Fib retracement levels.

continued for members… (more…)

continued for members… (more…)

Stocks rarely drop over a 3-day weekend. This one was no exception. The miniscule decline we saw in the futures last night has been all but erased despite a conciliatory 5% bump in VIX to backtest its SMA10. No fuss, no muss.

continued for members… (more…)

continued for members… (more…)

As we noted yesterday, EURUSD is finally fulfilling our expectation of a breakdown from the trend established at the Mar 2020 lows. This move has been a long time coming and has potentially significant consequences for the DXY.

continued for members… (more…)

continued for members… (more…)

Under ordinary circumstances, a 2.3% MoM bump in Durable Goods orders would be very welcome – especially on the heels of last month’s -1.3% print. When inflation is a growing concern due to the Fed’s largesse, however, it complicates things. For instance, might it cause the Fed to take its foot off the gas?

Not to worry, VIX was hammered sharply lower for the fourth session in a row.  It’s now off 35% since Monday’s highs and has reached levels last seen on Feb 14, 2020, a few days before the market crashed. Note that this is the target we first charted back in early April [see: Irrational Exuberance and You]…

It’s now off 35% since Monday’s highs and has reached levels last seen on Feb 14, 2020, a few days before the market crashed. Note that this is the target we first charted back in early April [see: Irrational Exuberance and You]…

…when we observed that VIX was repeating a pattern seen many times over the years.

…when we observed that VIX was repeating a pattern seen many times over the years.

It should come as no surprise that VIX did break down and SPX did, indeed, rise above 3956. Like all the other breakdowns, this one has the potential to keep the party going long past curfew.

This time, it went a step further – breaking below a falling trend line – especially bearish for VIX and bullish for stocks. It now has the opportunity to break below the trend line from 2017 — all the reassurance algos would need in order to bid stocks even higher.

Along the same lines, RBOB futures just topped their May 2018 highs (CPI was 2.8%) and are now 27% higher than their Feb 2020 (2.33% CPI) peak – even though total miles driven in April 2021 were 10% lower than April 2020 and 11% lower than in May 2018. RBOB hasn’t been higher than this since Oct 2014 when CPI, now 5%, was retreating from its recent 2.13% highs.

Along the same lines, RBOB futures just topped their May 2018 highs (CPI was 2.8%) and are now 27% higher than their Feb 2020 (2.33% CPI) peak – even though total miles driven in April 2021 were 10% lower than April 2020 and 11% lower than in May 2018. RBOB hasn’t been higher than this since Oct 2014 when CPI, now 5%, was retreating from its recent 2.13% highs.

If this all seems a little overdone, you’re right. The economy has rebounded. But, few responsible economists would argue that things are better than in Feb 2020 when markets crashed as the pandemic roiled the global economy.

The obvious X-factor, of course, is the massive amount of money the Fed has thrown at markets. The less obvious factor is the ease with which the Fed can manipulate algos. The warning signs which used to cause correction-causing reversions to the mean — rapidly rising inflation and interest rates, rising volatility, etc. — are no longer legitimate concerns.

Why? Because the Fed has proven that stocks can keep rising even in the face of data that would otherwise be problematic. So what if inflation is out of control? Interest rates sure don’t reflect it. Below trend GDP? All the more reason for massive QE.  They haven’t learned how to cure the patient, let alone prevent him from getting sick. But, they’ve rigged the thermometer, the blood pressure cuff, and the stethoscope to indicate that everything is just fine.

They haven’t learned how to cure the patient, let alone prevent him from getting sick. But, they’ve rigged the thermometer, the blood pressure cuff, and the stethoscope to indicate that everything is just fine.

continued for members… (more…)

ES came within 9 points of our next downside target before getting a nice bounce motivated primarily by USDJPY, which was working flat out to save the NKD from a scary, and long overdue dive to its SMA200.

This bounce will be quite important to the bulls, who are no doubt hoping to avoid a bearish 10/20 cross.

This bounce will be quite important to the bulls, who are no doubt hoping to avoid a bearish 10/20 cross.

continued for members… (more…)