In The Unavoidable Crash published on Project Syndicate’s website, economist Nouriel Roubini asserts that “years of ultra-loose fiscal, monetary, and credit policies and the onset of major negative supply shocks, stagflationary pressures are now putting the squeeze on a massive mountain of public- and private-sector debt. The mother of all economic crises looms, and there will be little that policymakers can do about it.”

Noting that debt as a share of GDP has risen from 200% in 1999 to over 420% in “advanced” economies, he argues that the “explosion of unsustainable debt” has created insolvent zombies that survived only due to ZIRP and NIRP.

I’ve been of the same mind for years, suggesting very early on in these pages that the excessive liquidity being shoveled into markets by central banks would ultimately usher in destructive stagflation. Yet, year after year, the economy continued to putter along and stocks continued to rally as interest rates were seemingly immune to building economic risks.

That immunity was manufactured, of course, by central banks themselves. They intervened in bond markets, scooping up with abandon the debt their host countries issued. The resulting all-time low interest rates perpetuated the impression that risk was also at an all-time low.

In the US, the 10Y continued to ratchet lower, reversing on right on cue every time it threatened to break out of the channel that has been in place for much longer than the average trader on Wall Street. This was possible because inflation would fortuitously top out, reversing in the nick of time, whereupon interest rates would dutifully follow. There’s always been a strong correlation…

This was possible because inflation would fortuitously top out, reversing in the nick of time, whereupon interest rates would dutifully follow. There’s always been a strong correlation…

…but it’s been particularly obvious over the past 22 years, with CPI nosediving every time the 10Y came close to breaking out.

…but it’s been particularly obvious over the past 22 years, with CPI nosediving every time the 10Y came close to breaking out.

CPI has consistently obliged because oil and gas prices have consistently obliged – until they didn’t.

CPI has consistently obliged because oil and gas prices have consistently obliged – until they didn’t.

It would be easy to blame the departure entirely on Russia’s invasion of Ukraine. But, the breakout began five months earlier in September 2021…

It would be easy to blame the departure entirely on Russia’s invasion of Ukraine. But, the breakout began five months earlier in September 2021… …several months after the FOMC started using the word “transitory” to describe inflation that was too high instead of inflation that was too low. We pointed out how ludicrous the notion was at the time [see: Not Transitory, Not Even Close.] Given the Fed’s access to reams of data and scores of PhDs, I have to assume that they knew it, too.

…several months after the FOMC started using the word “transitory” to describe inflation that was too high instead of inflation that was too low. We pointed out how ludicrous the notion was at the time [see: Not Transitory, Not Even Close.] Given the Fed’s access to reams of data and scores of PhDs, I have to assume that they knew it, too.

But, the Fed was more concerned about the market making new highs every other day. So, the transitory story stuck, as did the term “reflation trade.” The return of inflation [5% in May 2021, on its way to 7% in December] was supposedly a good thing as it was evidence of surging demand and ample liquidity.

That 7% print seemed to finally rattle some cages – but only because Powell finally admitted that “transitory” probably wasn’t the best word to describe inflation and because the FOMC finally promised to scale back its $120 billion/month bond buying binge.

Although WTI dropped back into its falling channel in November, the lead up to Russia’s invasion soon sent oil prices soaring again – up 80% between Dec 23 and Mar 7. Though the YoY delta in gas prices was limited to 63%, inflation was leaking through to other categories. Between Mar 2021 and Aug 2022, food prices rose from an annual rate of 3.5% to 11.4%. Shelter more than tripled from 1.7% to 6.2%. And, vehicles soared from 1.5% to 7.6%.

CPI continued its ascent, reaching 9.1% in Jun 2022. At current prices, the YoY increase in gas prices is running at about 2% – about the same as in Mar 2021 when CPI was only 2.62%. But, there is literally no chance of reaching those levels any time in the near future.

CPI continued its ascent, reaching 9.1% in Jun 2022. At current prices, the YoY increase in gas prices is running at about 2% – about the same as in Mar 2021 when CPI was only 2.62%. But, there is literally no chance of reaching those levels any time in the near future.

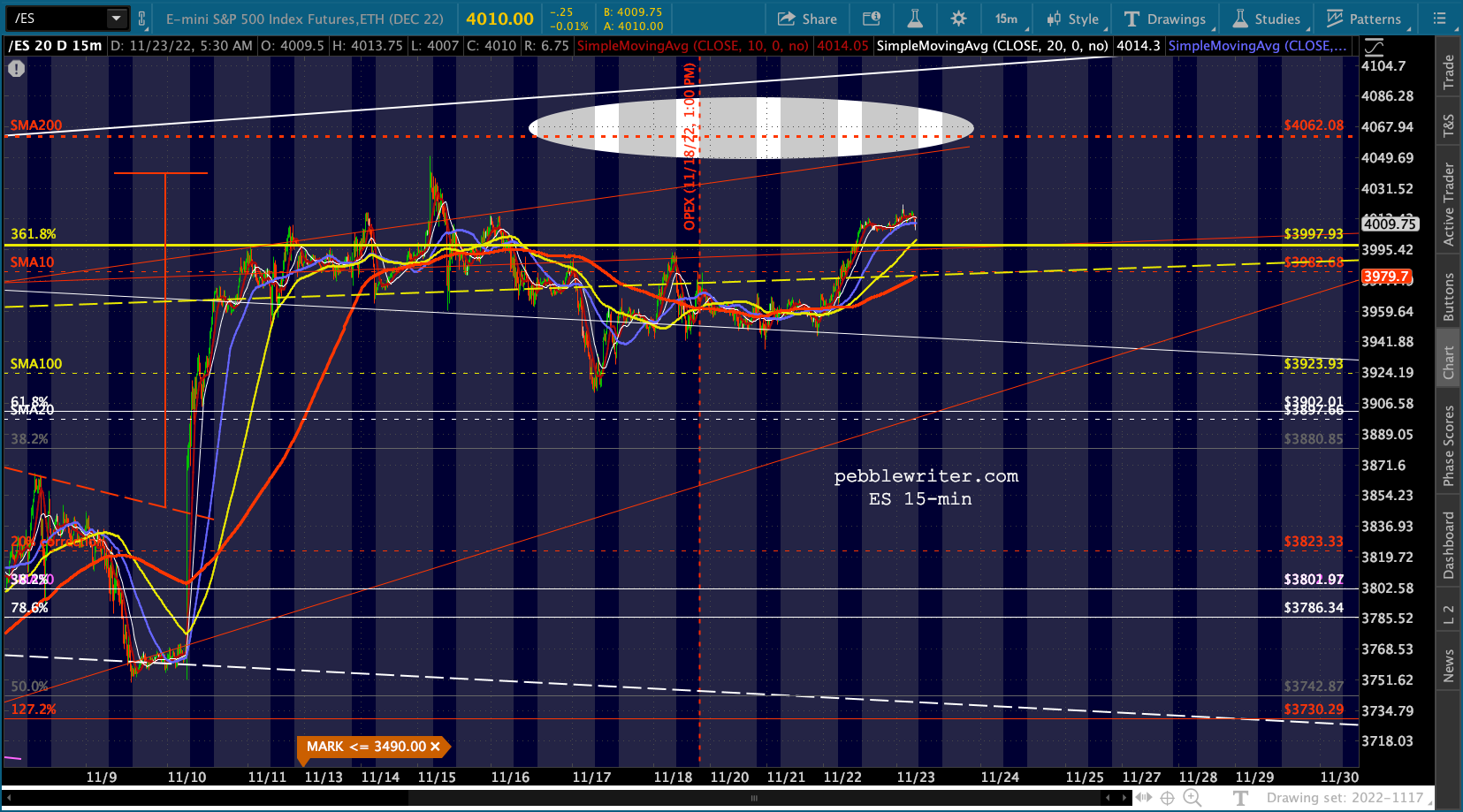

Last week’s BLS report that average hourly wages rose 5.1% YoY was a stark reminder of how “sticky” many inflation categories can be. With PPI due out on Friday and CPI next Tuesday, it will be interesting to see if the recent excitement over a Fed taper is justified.

continued for members… (more…)