With the 10Y having broken out, the 2Y threatening new highs and the 2s10s threatening new lows, should investors really be letting their guard down?

continued for members…

continued for members…

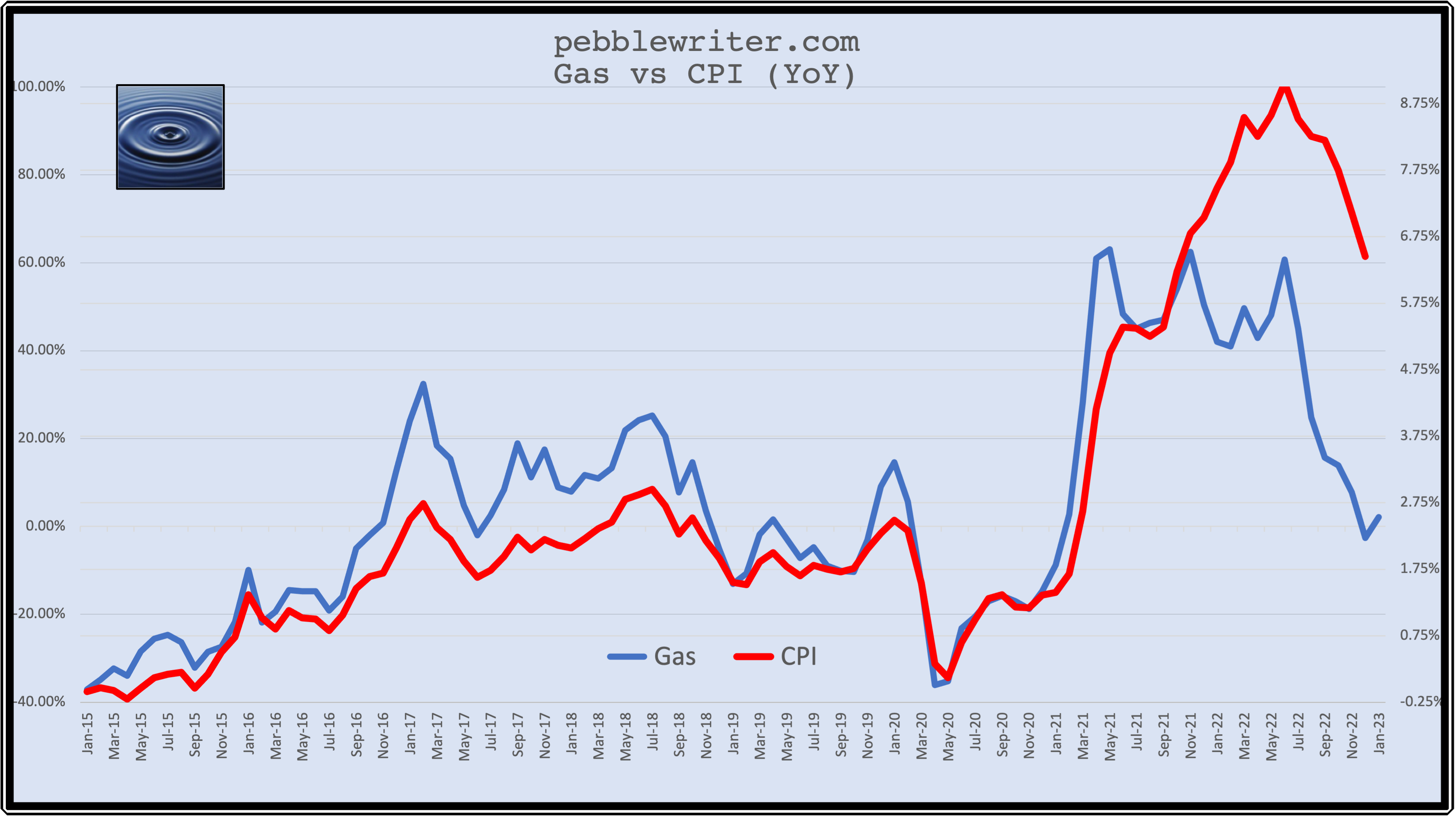

Our favorite inflation indicator reaffirms that oil/gas prices aren’t as well correlated with inflation as they once were – which echoes economists’ sentiment that services have taken the inflation mantle. Note that YoY gas prices did tick up in January. Ticks higher has always resulted in similar moves for CPI…

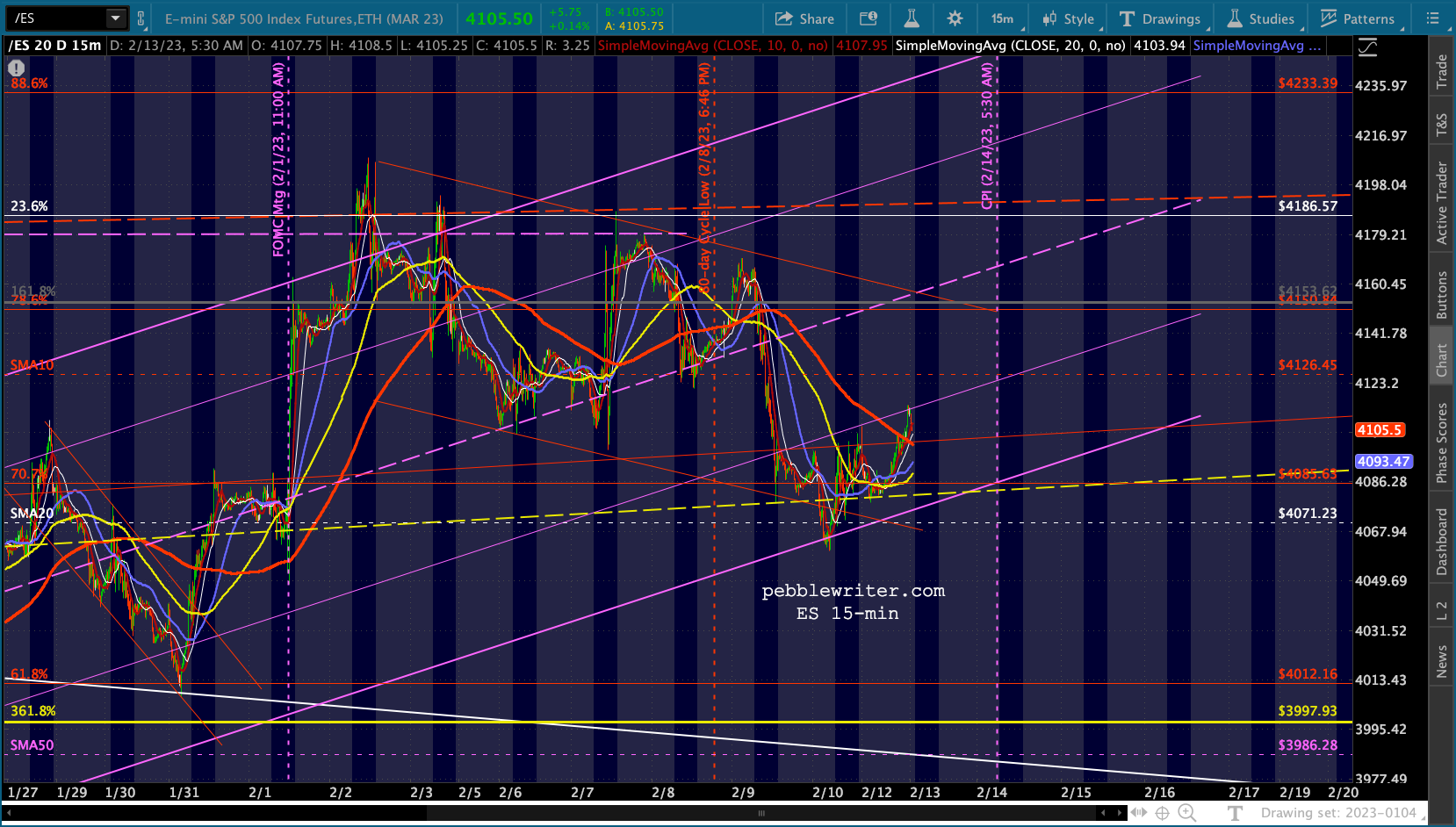

Equities have run up these past few weeks on the assumption that the Fed will take its foot off the brake pedal and either pause or pivot soon. If we get a strong MoM CPI number (0.5%?) tomorrow, however, it would be reason to reassess and equities could take it on the chin.

Equities have run up these past few weeks on the assumption that the Fed will take its foot off the brake pedal and either pause or pivot soon. If we get a strong MoM CPI number (0.5%?) tomorrow, however, it would be reason to reassess and equities could take it on the chin.

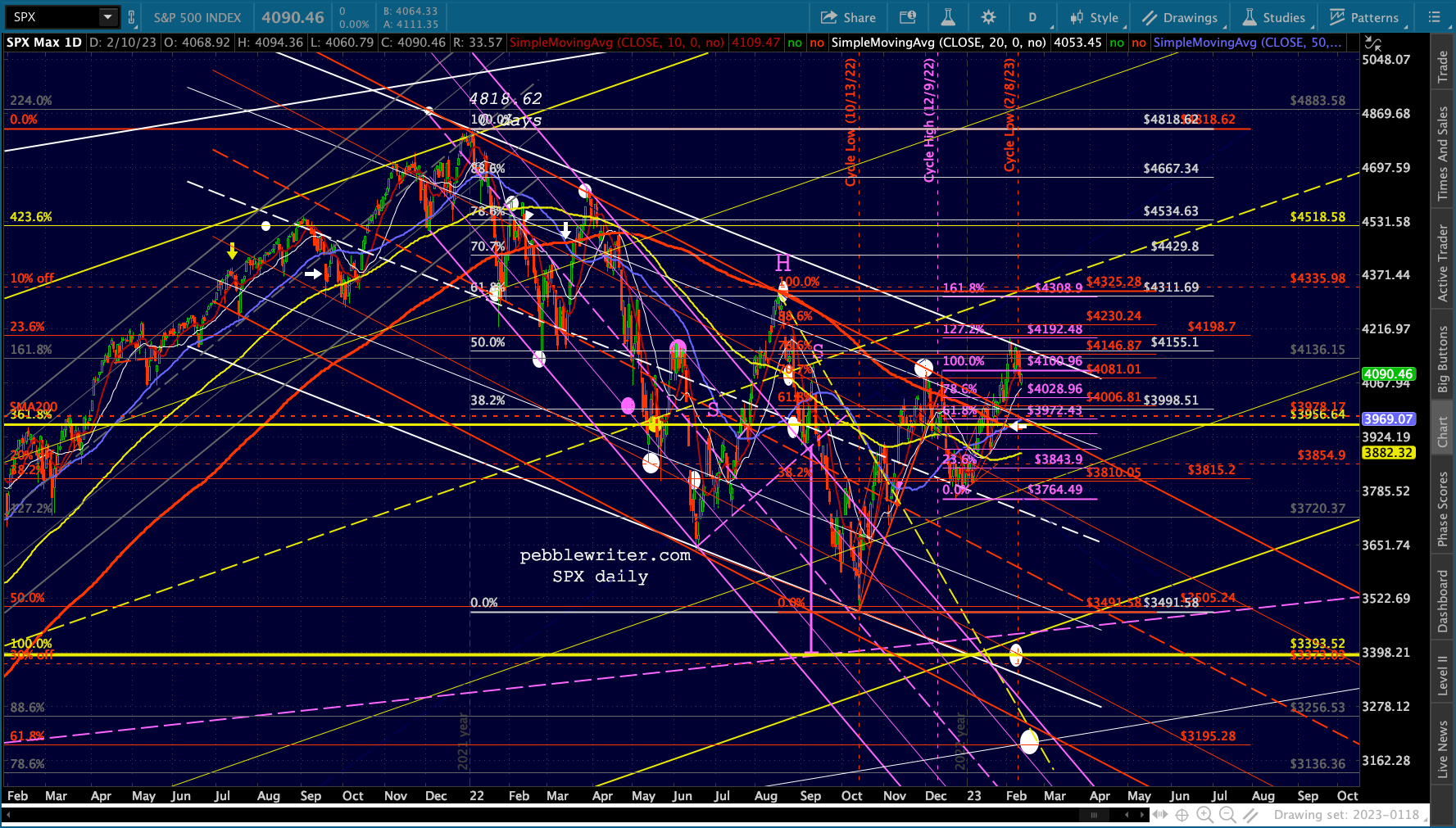

While SPX has apparently broken with the 80-session cycle, the XLU cycle indicates there is still another week to go before we can call it quits.

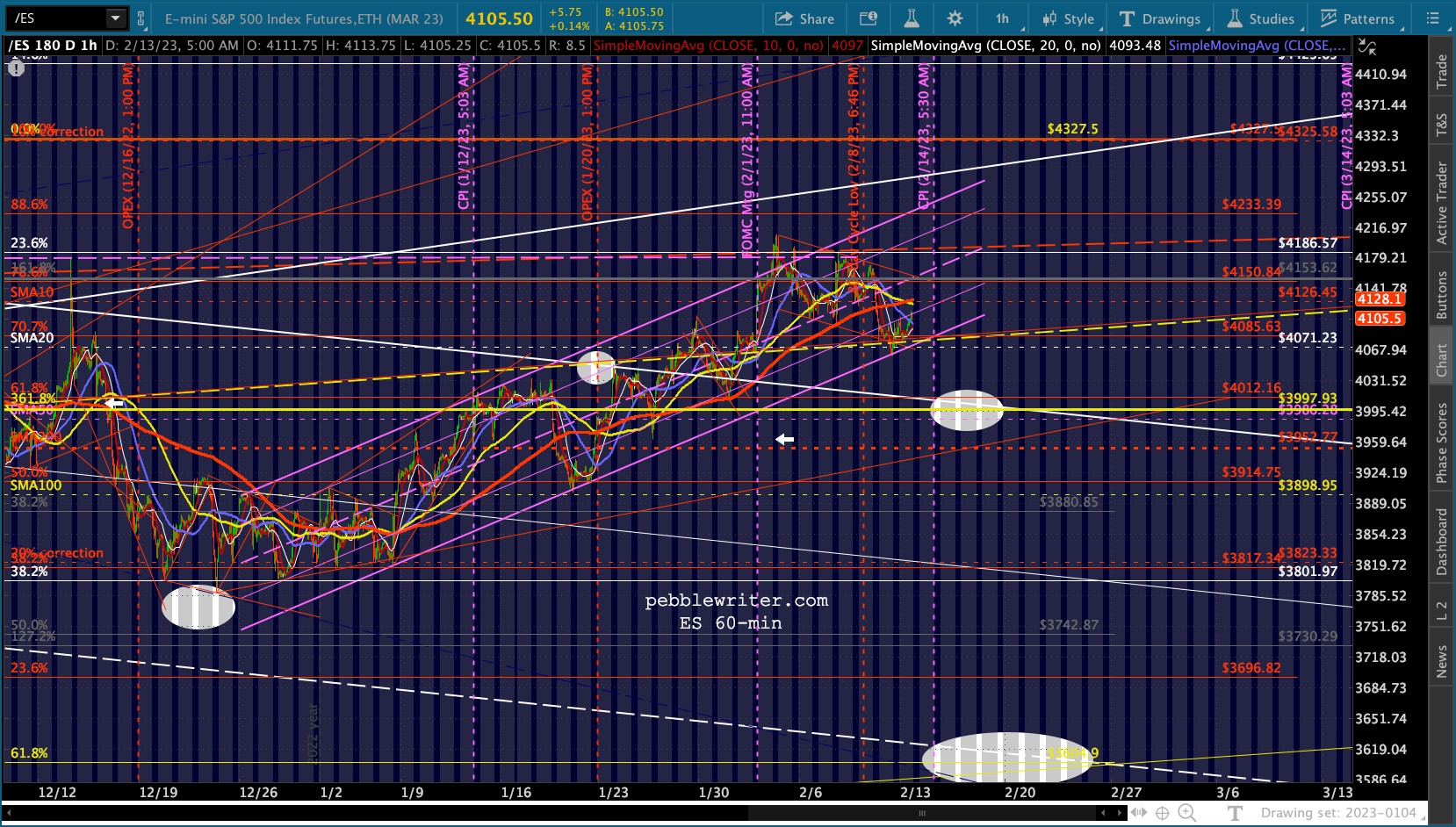

And, recent survey results indicate an very high level of bullishness. Yet, as we noted last week, equity indices have ignored opportunities to complete inverted H&S patterns – a very curious situation that suggests the latest runup was all about postponing the next leg down rather than preventing it.

And, recent survey results indicate an very high level of bullishness. Yet, as we noted last week, equity indices have ignored opportunities to complete inverted H&S patterns – a very curious situation that suggests the latest runup was all about postponing the next leg down rather than preventing it.

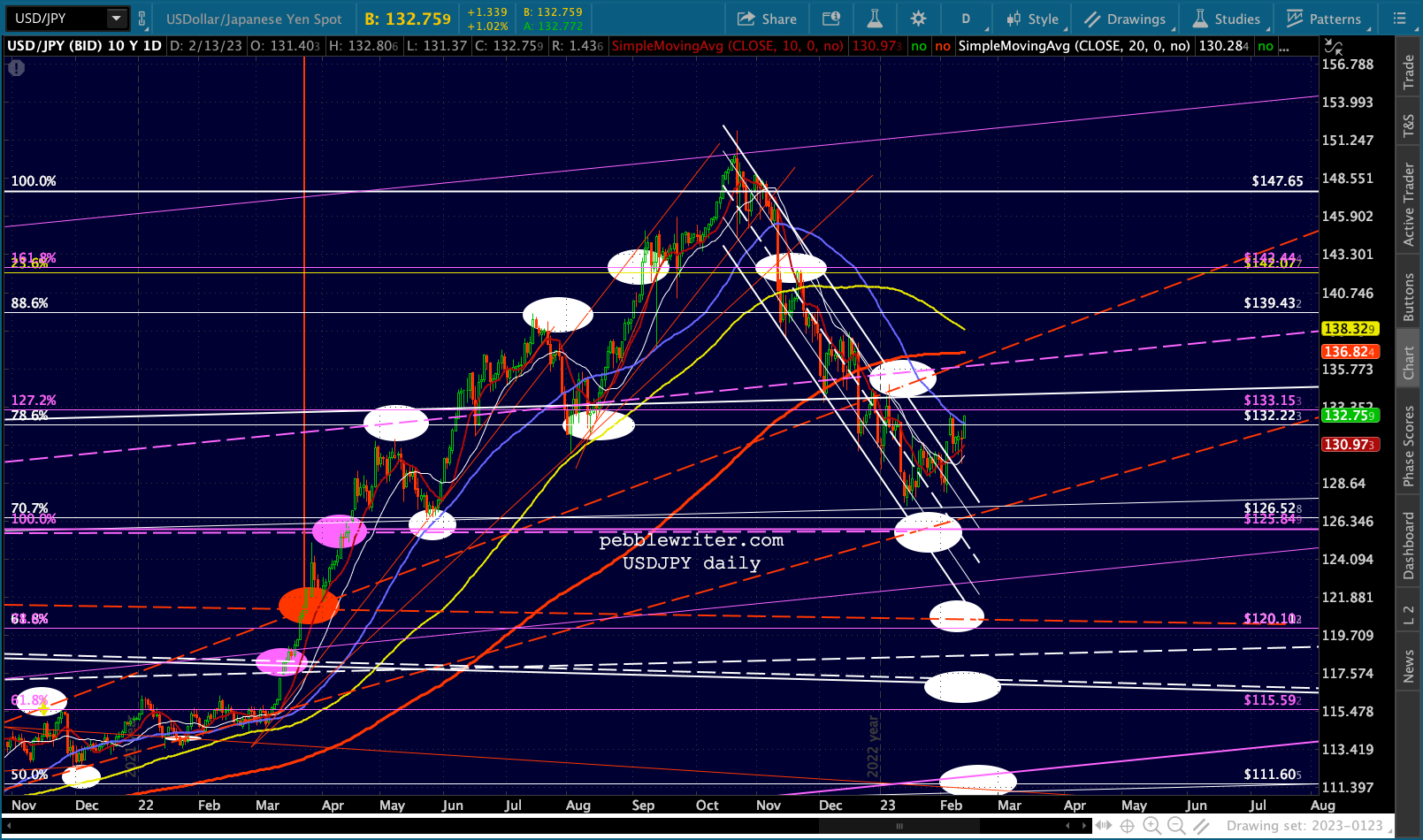

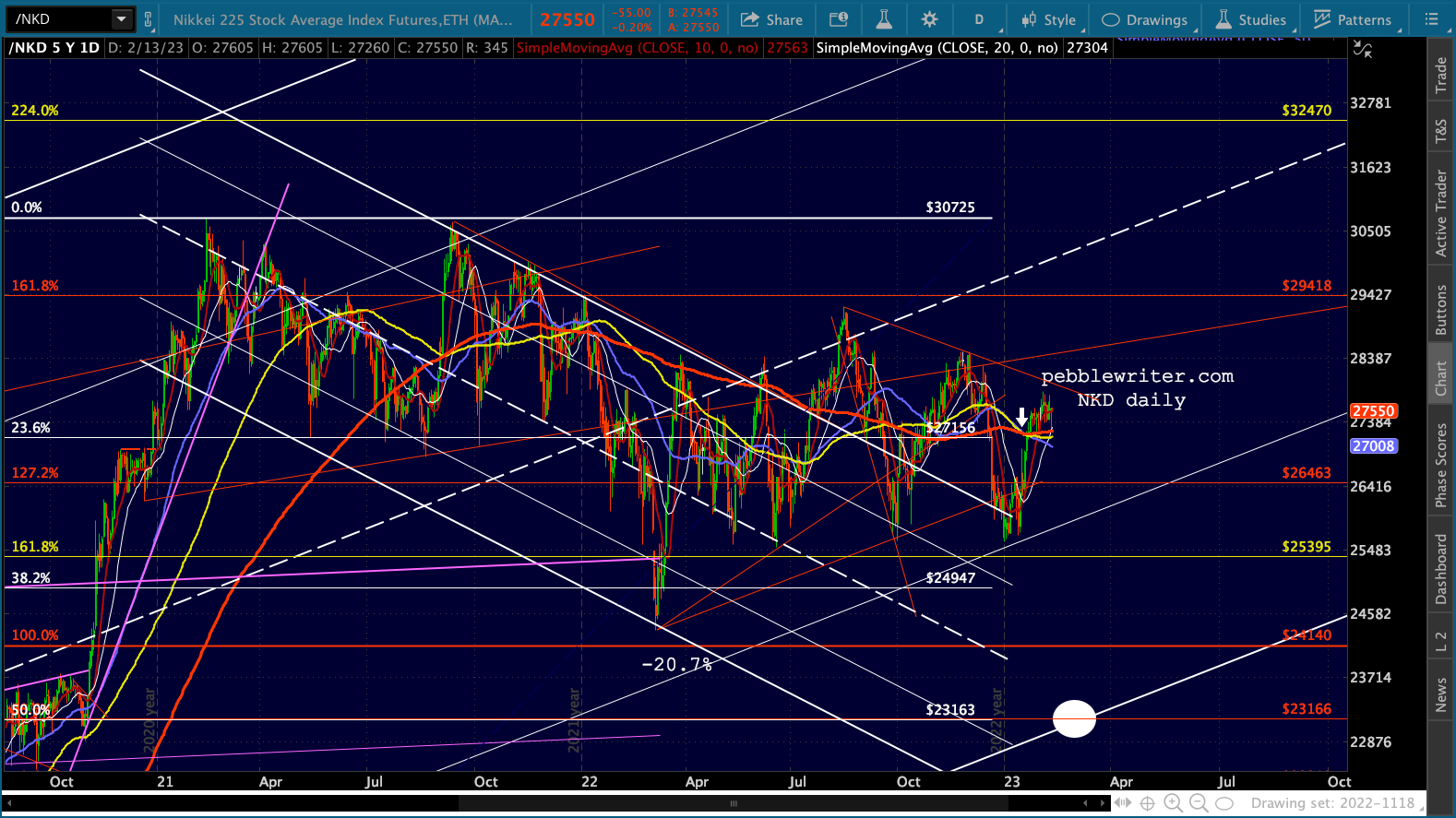

Currencies have continued their moves from last week, with USDJPY still broken out – the better to prop up NKD…

Currencies have continued their moves from last week, with USDJPY still broken out – the better to prop up NKD…

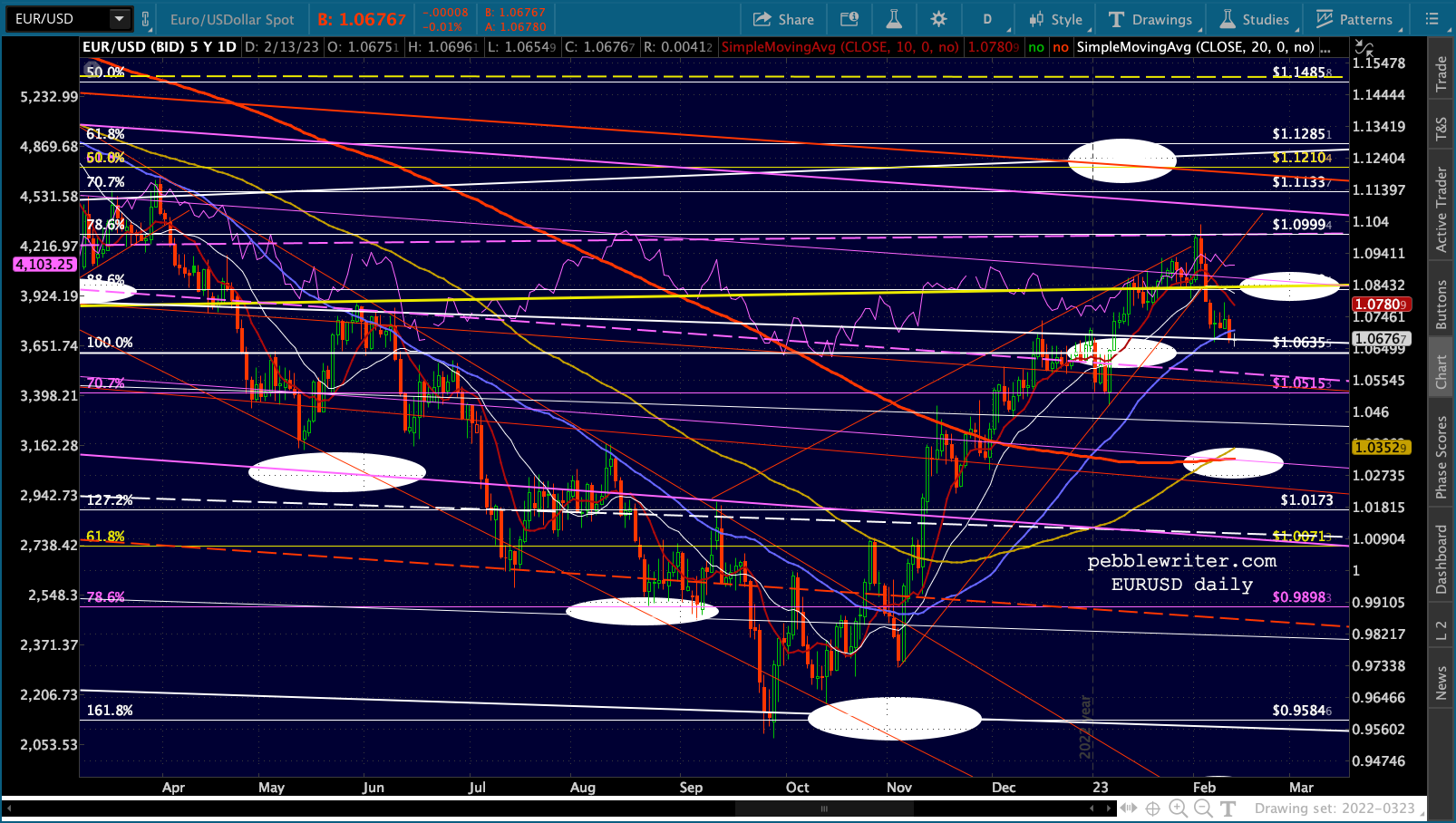

…and EURUSD still rolling over.

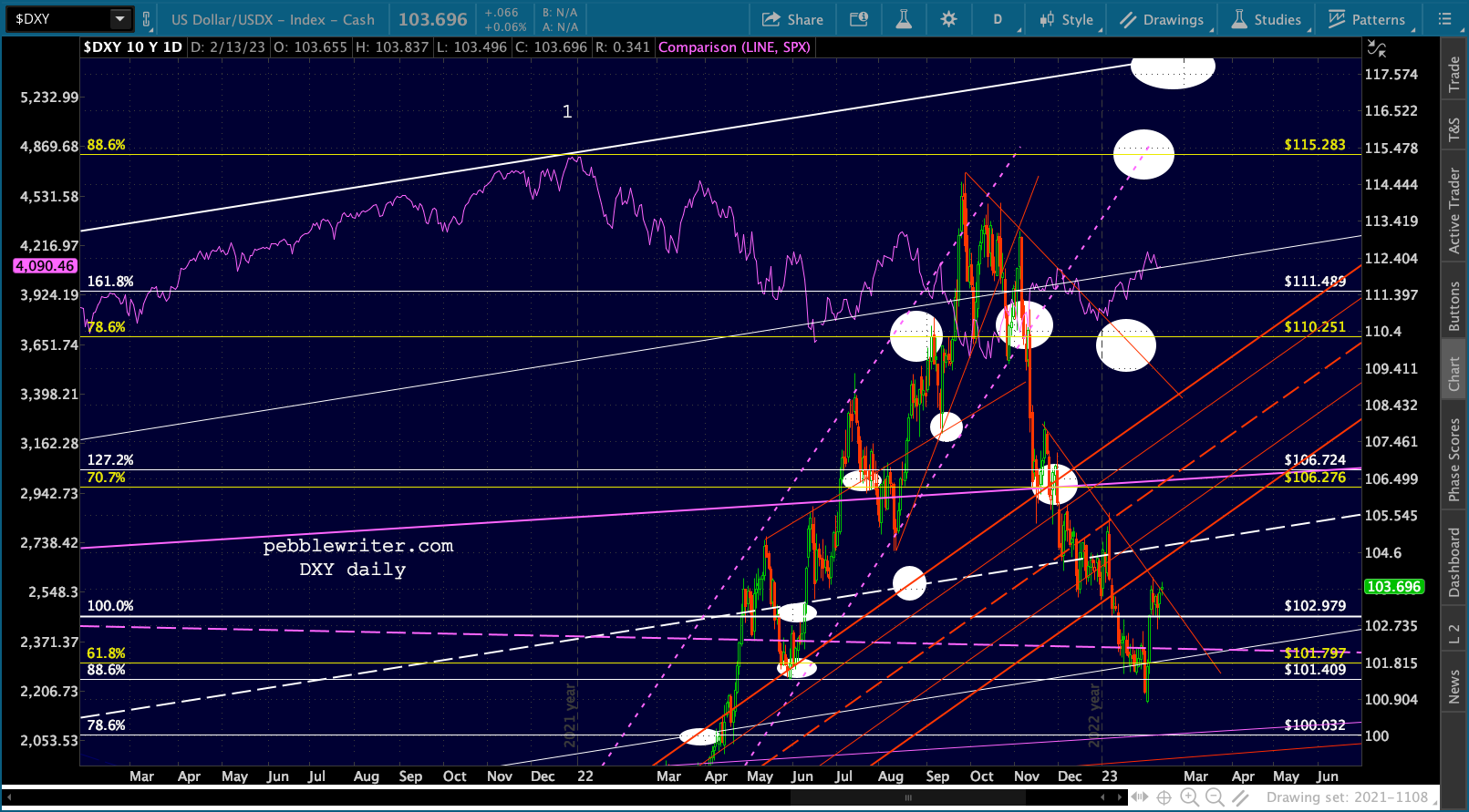

…and EURUSD still rolling over.  This still leaves DXY on the verge of a breakout – a near certainty if rates continue edging higher.

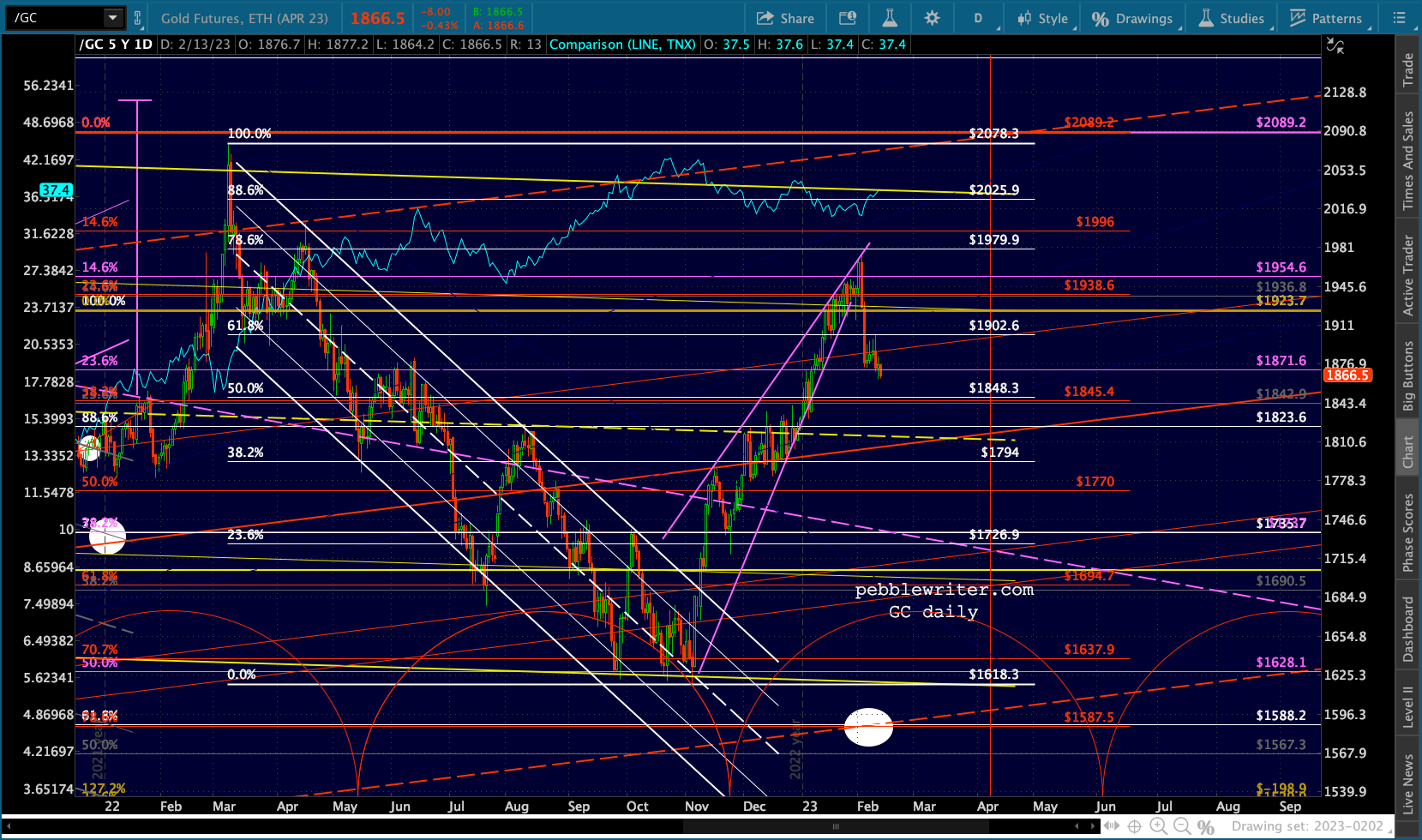

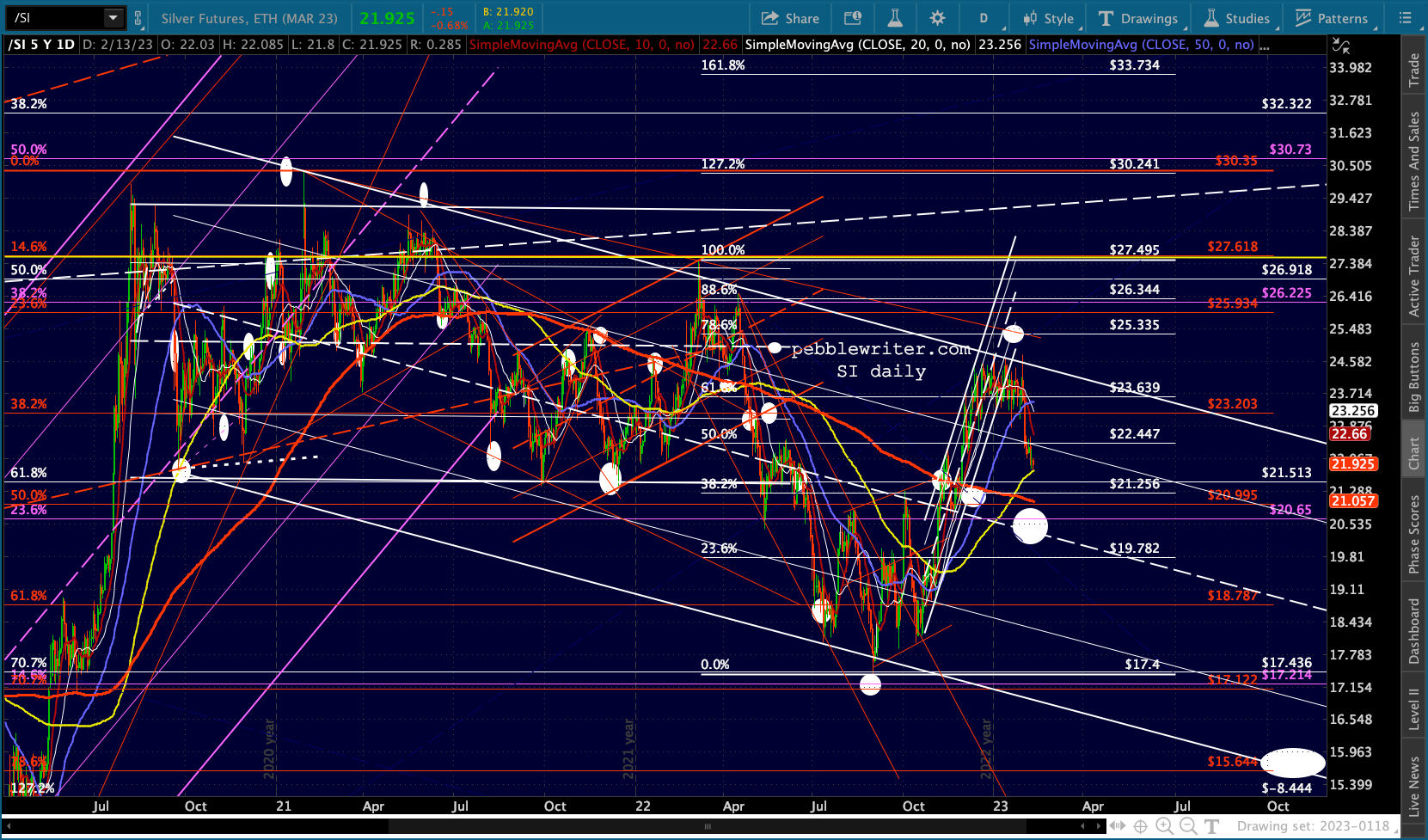

This still leaves DXY on the verge of a breakout – a near certainty if rates continue edging higher. GC and SI sure seem to recognize the potential for additional USD strength.

GC and SI sure seem to recognize the potential for additional USD strength.

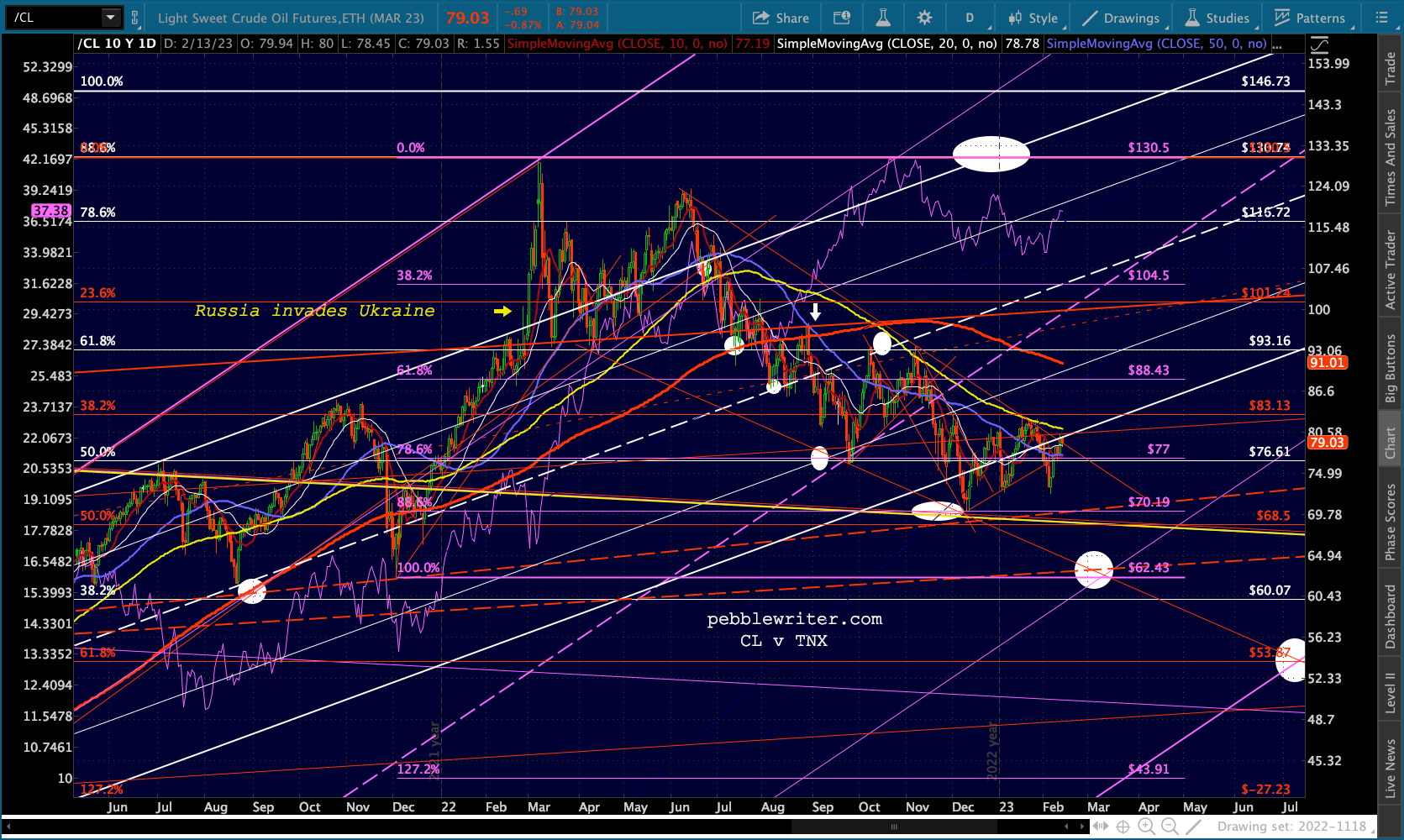

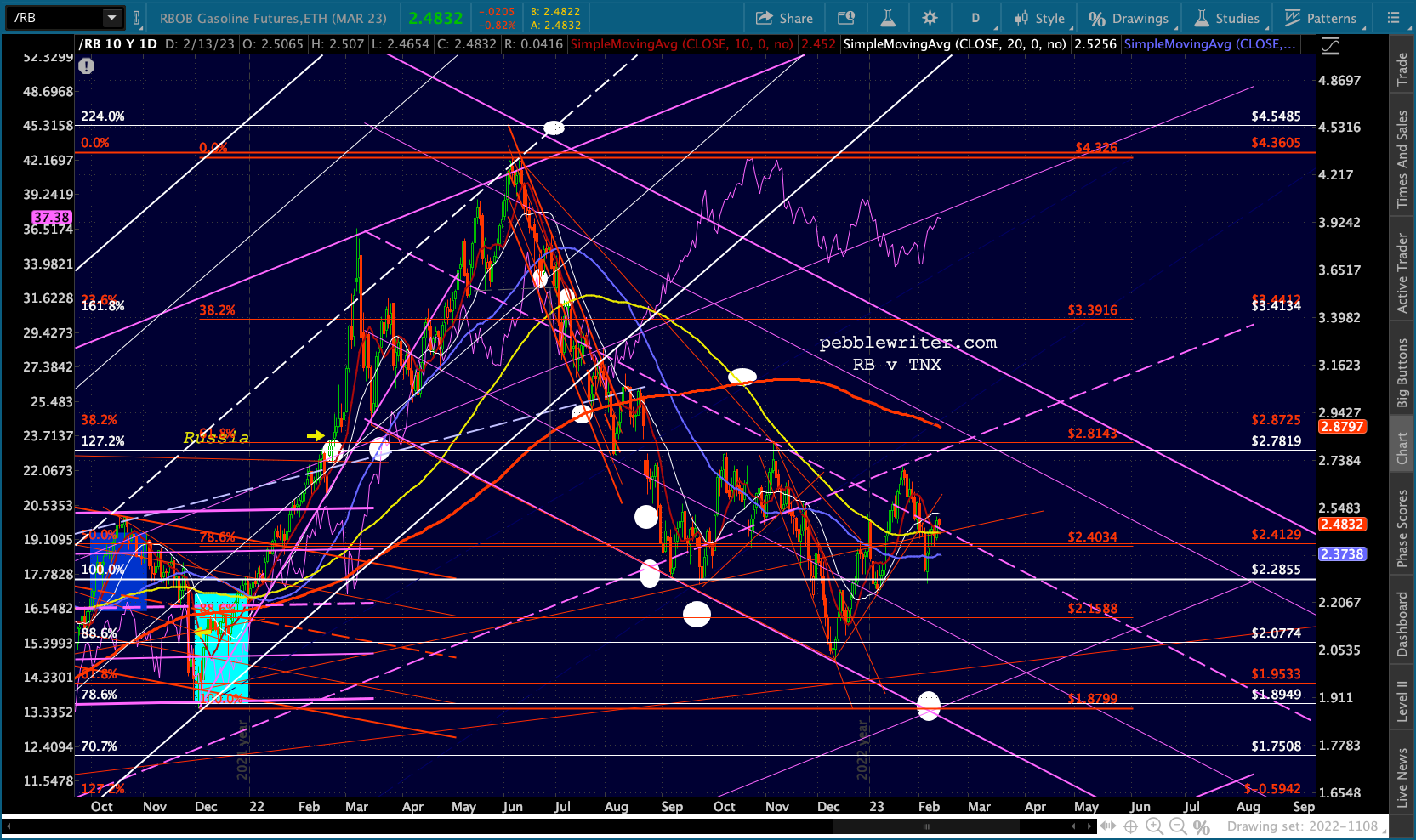

CL and RB are both still pushing up against overhead resistance – additional ammunition for the higher interest rate/CPI argument.

CL and RB are both still pushing up against overhead resistance – additional ammunition for the higher interest rate/CPI argument.

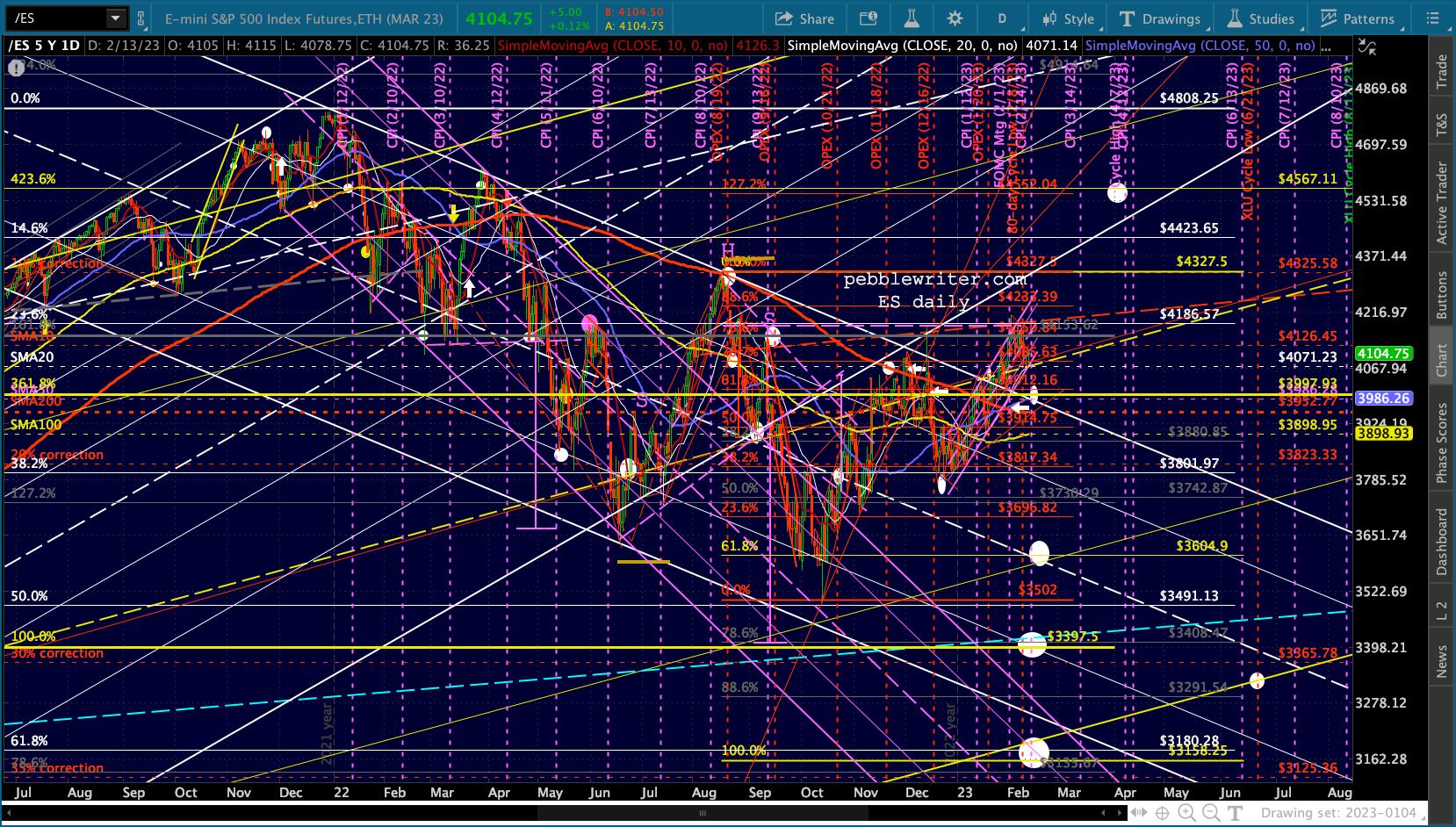

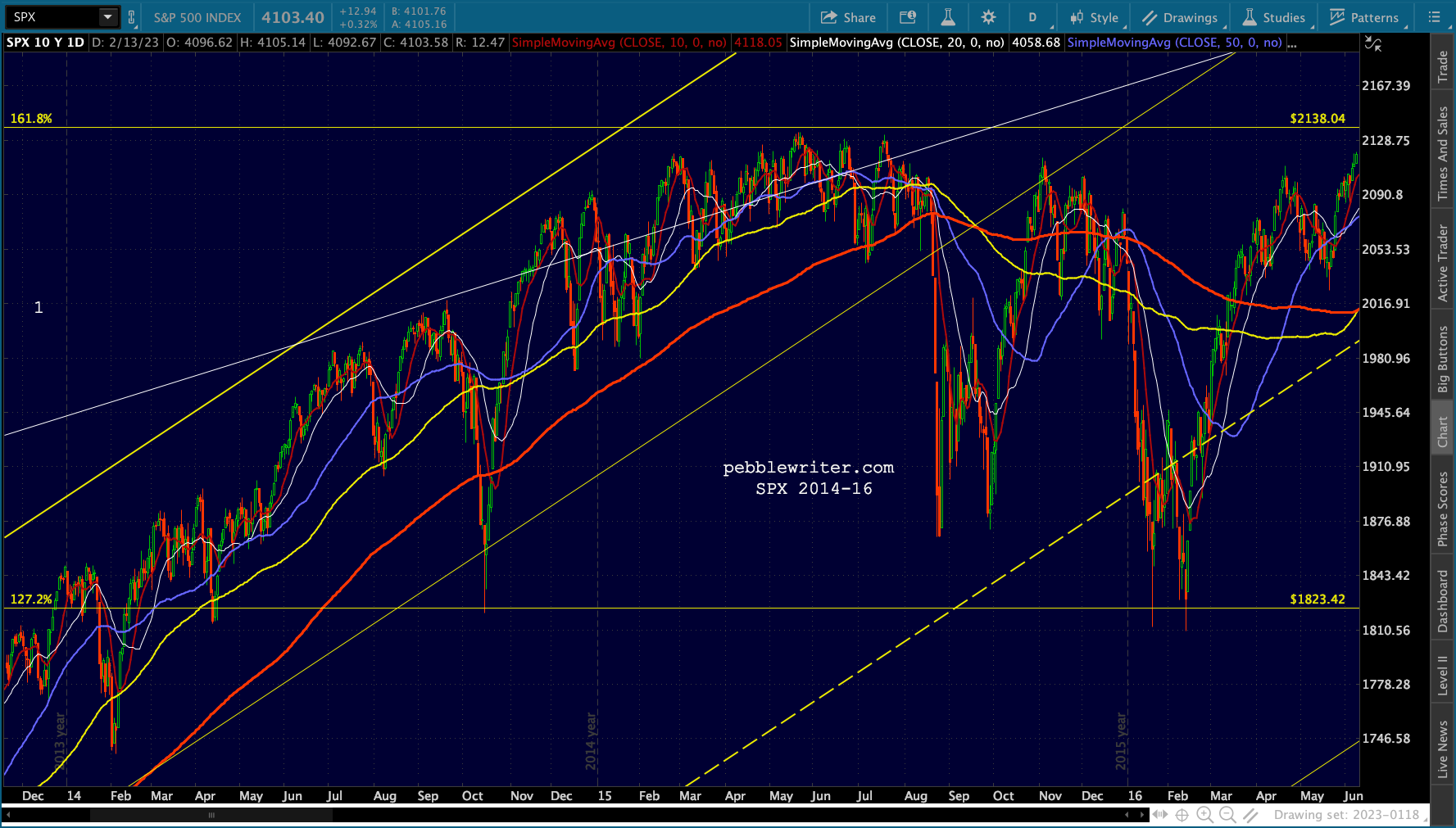

This sentiment reminds me a lot of 2015-2016, when the rebound off the initial drop was so strong it washed out a great many bears.

This sentiment reminds me a lot of 2015-2016, when the rebound off the initial drop was so strong it washed out a great many bears.

stay tuned…