January 2023 headline CPI came in at 6.41% versus 6.45% for December 2022. It increased 0.8% month-over-month, though this was reduced to 0.5% after the usual government massaging (aka seasonal adjustment.)

Core CPI also dropped – from 5.71% in December to 5.58% in January. Despite all that massaging, some of the recent gains in energy prices made it into January’s data. But, a win’s a win, right? In this case, the data wasn’t far from most expectations, so the market is holding up so far.

But, a win’s a win, right? In this case, the data wasn’t far from most expectations, so the market is holding up so far.

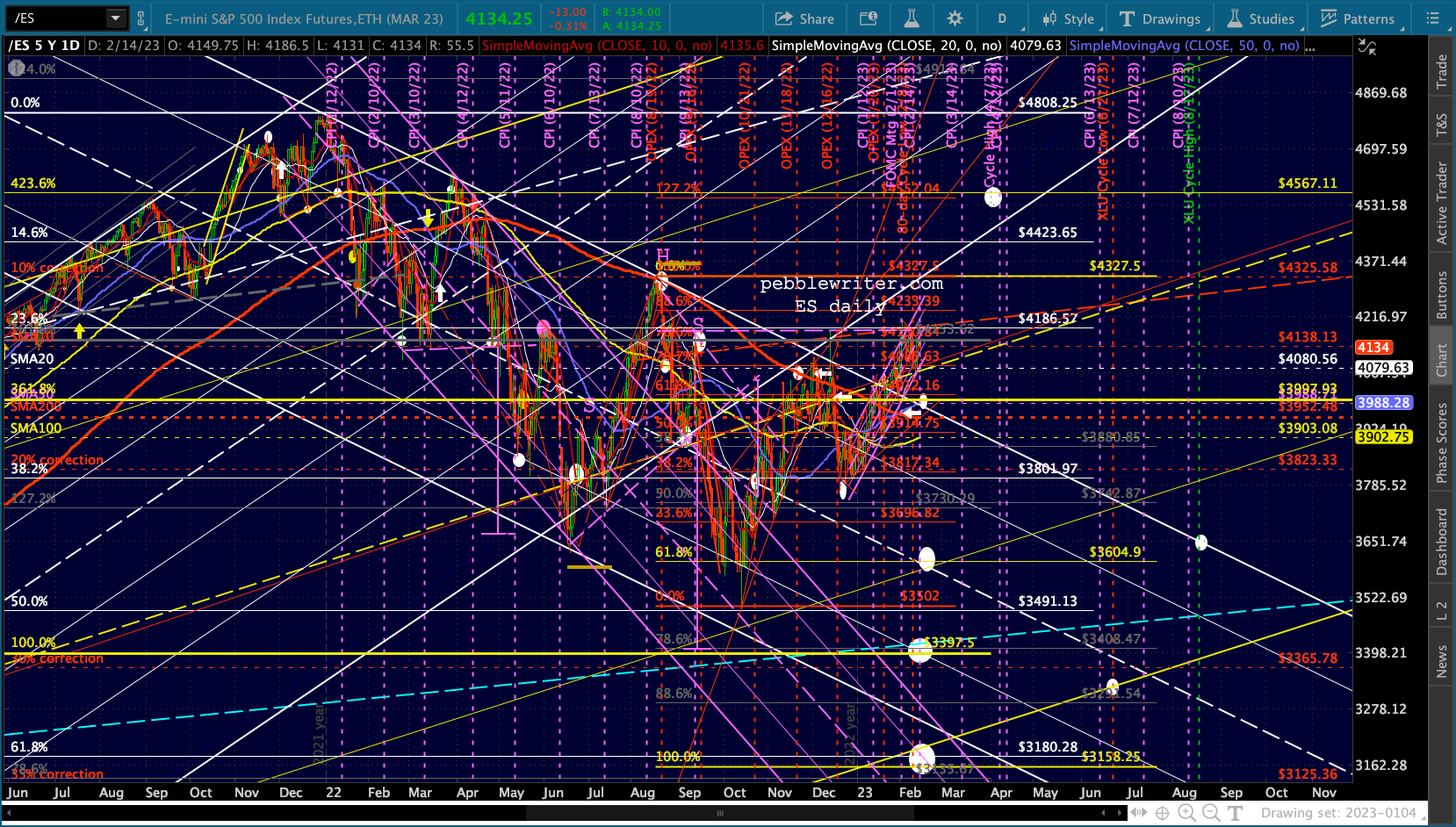

Purely by coincidence (not) it seems that VIX was clobbered by 7% – over 14% from Friday’s highs.

Purely by coincidence (not) it seems that VIX was clobbered by 7% – over 14% from Friday’s highs. If you look closely, though, you’ll notice that VIX merely backtested the channel from which it broke out last Thursday – meaning that the latest rally might finally be over.

If you look closely, though, you’ll notice that VIX merely backtested the channel from which it broke out last Thursday – meaning that the latest rally might finally be over.

continued for members… Of course, it remains to be seen whether the channel and SMA200 backtest targets will hold.

Of course, it remains to be seen whether the channel and SMA200 backtest targets will hold.

Much will depend on whether the VIX backtest can hold.

Much will depend on whether the VIX backtest can hold.

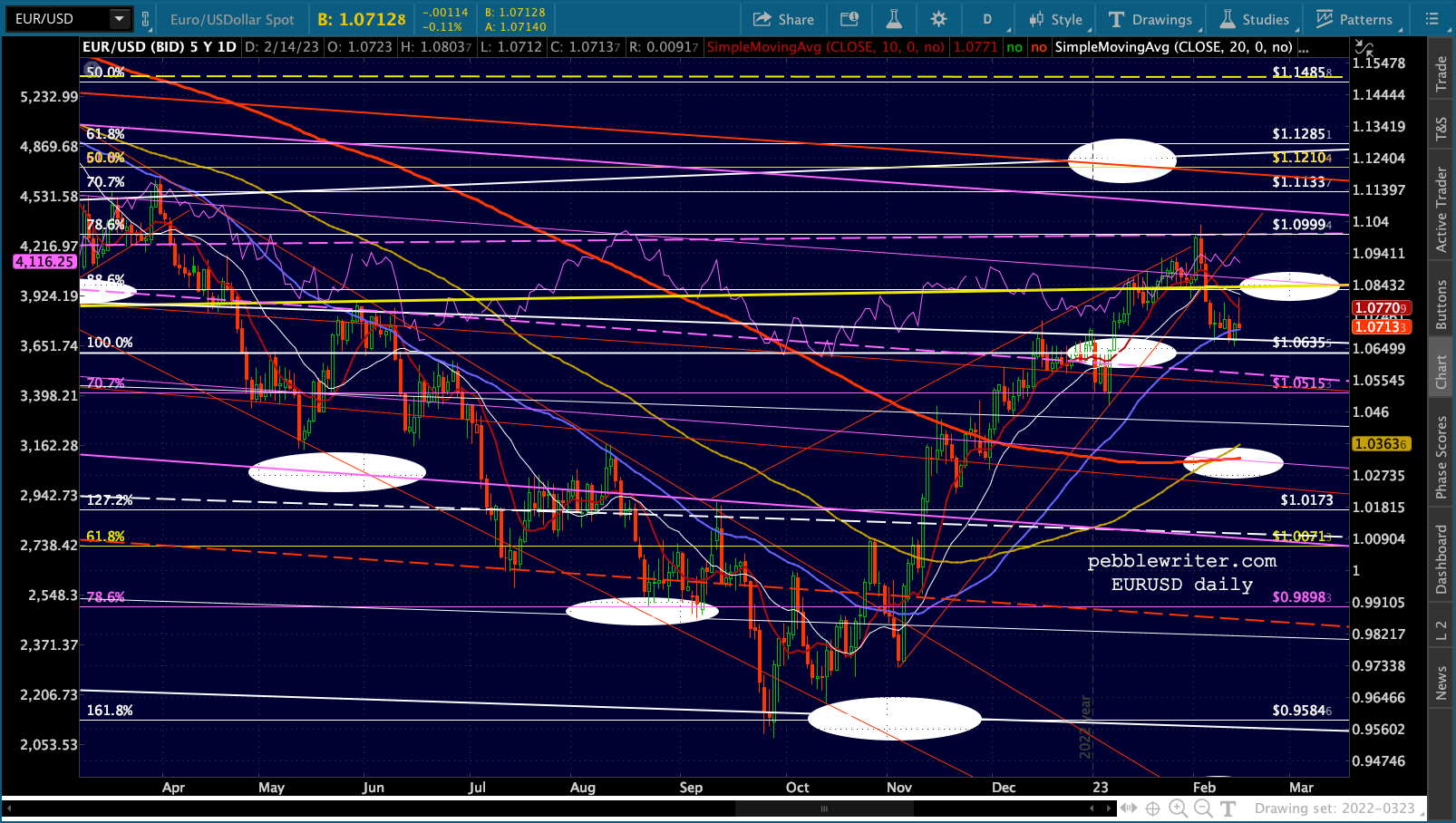

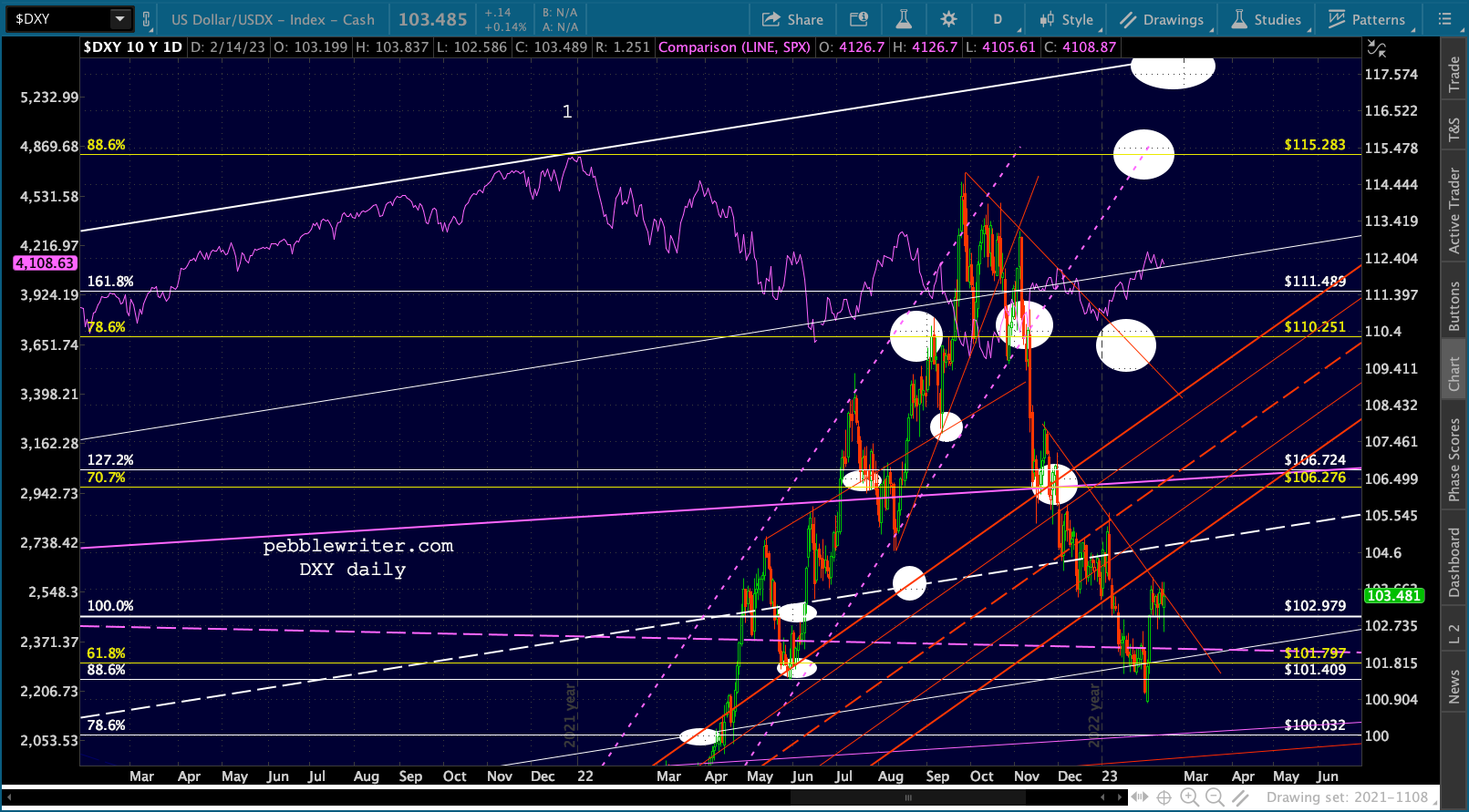

Currencies are letting equities slide – at least for the time being. EURUSD’s initial pop has faded. Combined with USDJPY’s rally already in process, this has DXY chomping at the bit. GC, SI and BTC continue to slump.

Currencies are letting equities slide – at least for the time being. EURUSD’s initial pop has faded. Combined with USDJPY’s rally already in process, this has DXY chomping at the bit. GC, SI and BTC continue to slump.

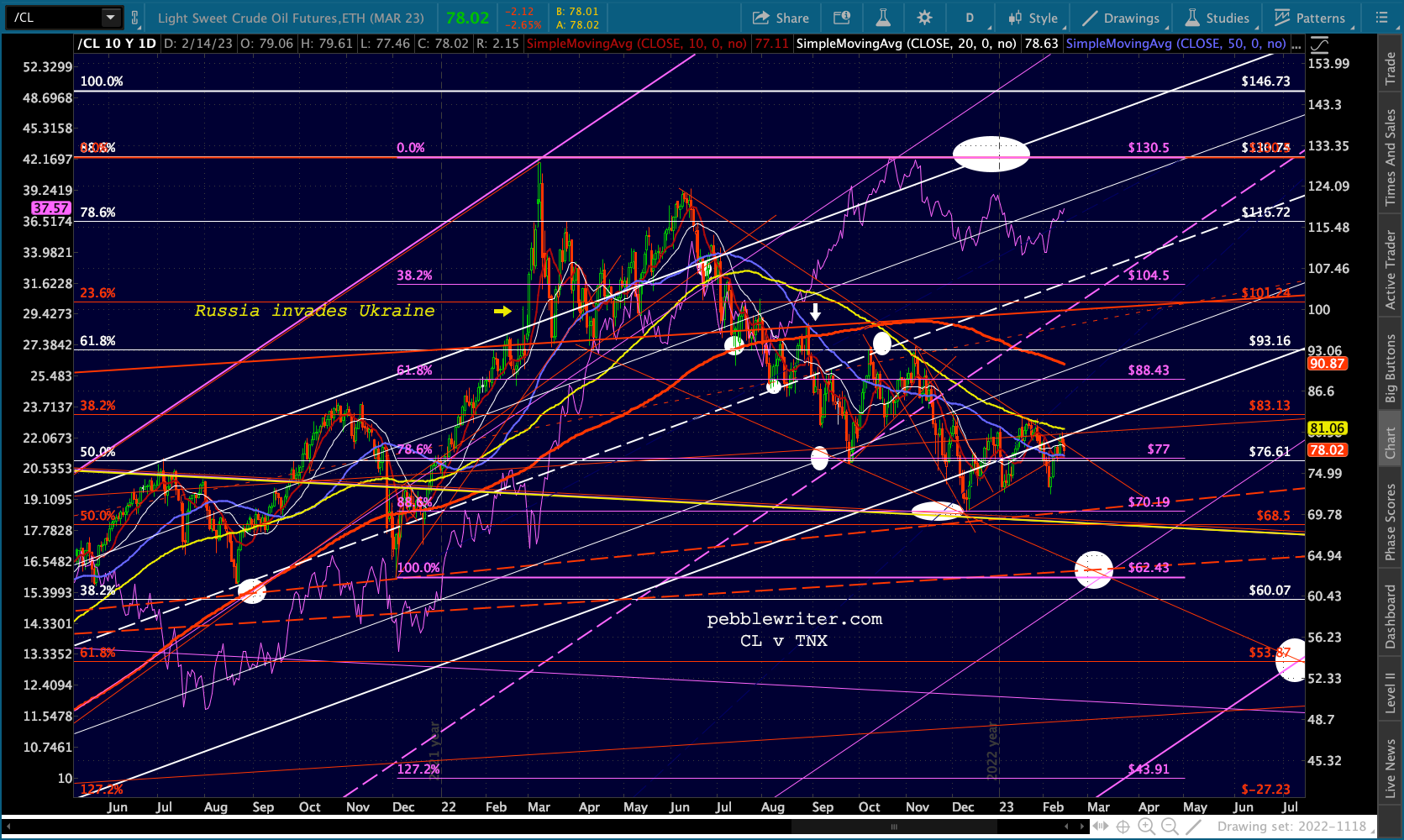

CL and RB are back to Friday’s lows…

CL and RB are back to Friday’s lows…

…which makes TNX’s continuing breakout even more impressive.

…which makes TNX’s continuing breakout even more impressive. Stay tuned…

Stay tuned…