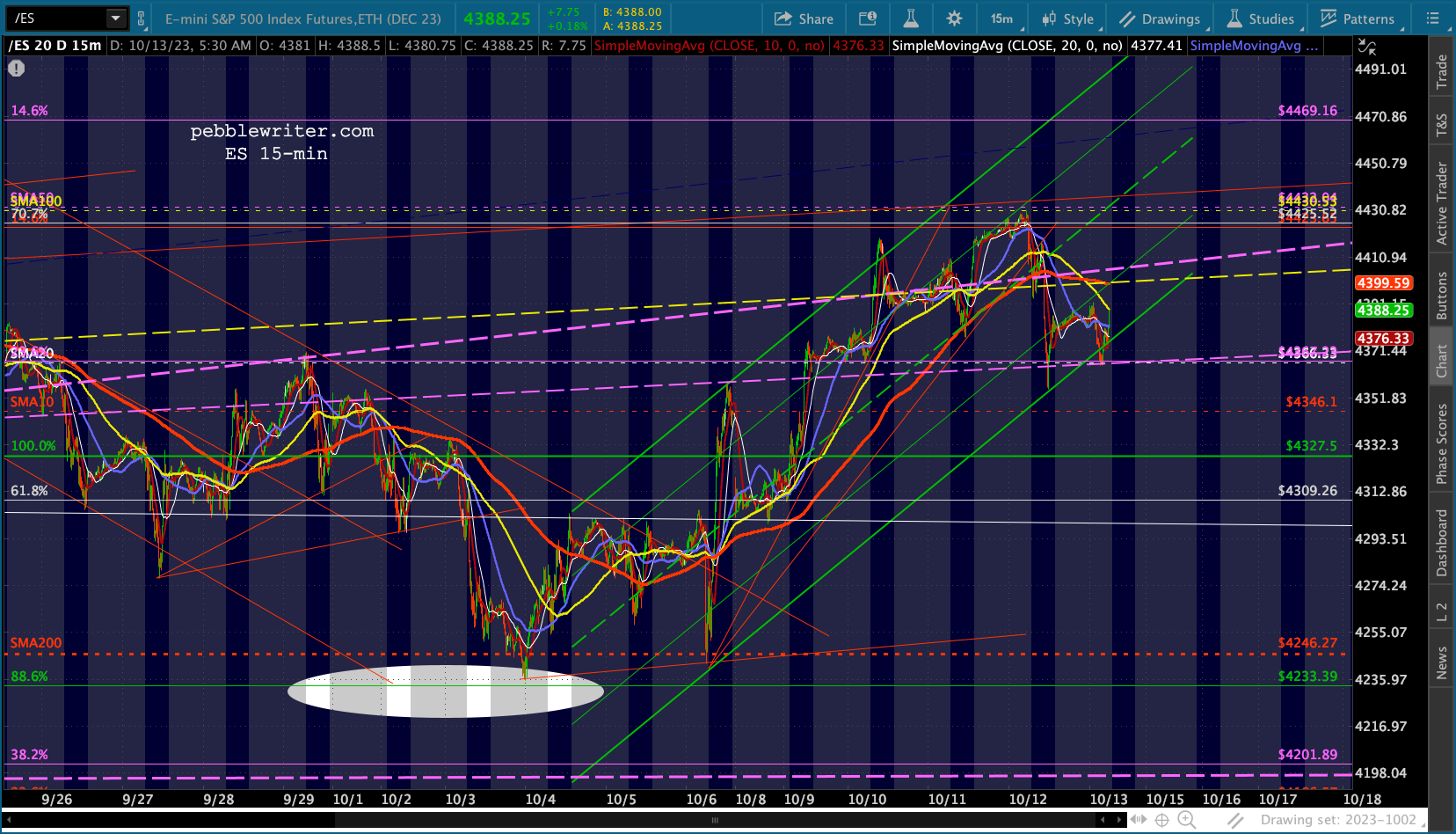

Futures are up moderately, running into their own channel top following VIX’s recent retreat from resistance,

continued for members… (more…)

Futures are up moderately, running into their own channel top following VIX’s recent retreat from resistance,

continued for members… (more…)

Futures are up modestly following establishment of a new rising channel.

continued for members… (more…)

continued for members… (more…)

September CPI came in higher than expected, at 0.4% MoM and 3.7% YoY versus estimates of 0.3% and 3.6%. Core CPI (less food and energy) remained elevated at 4.1%.

The details reveal continuing challenges with shelter, food and energy.

While the YoY print has trended lower…

While the YoY print has trended lower…  …the last two monthly prints suggest that inflation might be leveling out at elevated levels.

…the last two monthly prints suggest that inflation might be leveling out at elevated levels. Bottom line, the YoY trend is of little benefit to consumers who are tapped out, with depleted savings and higher expenses including the resumption of student loan payments. We don’t see a significant drop in CPI in the months ahead unless oil/gas prices collapse – a scenario that seems unlikely given recent events in the Middle East.

Bottom line, the YoY trend is of little benefit to consumers who are tapped out, with depleted savings and higher expenses including the resumption of student loan payments. We don’t see a significant drop in CPI in the months ahead unless oil/gas prices collapse – a scenario that seems unlikely given recent events in the Middle East.

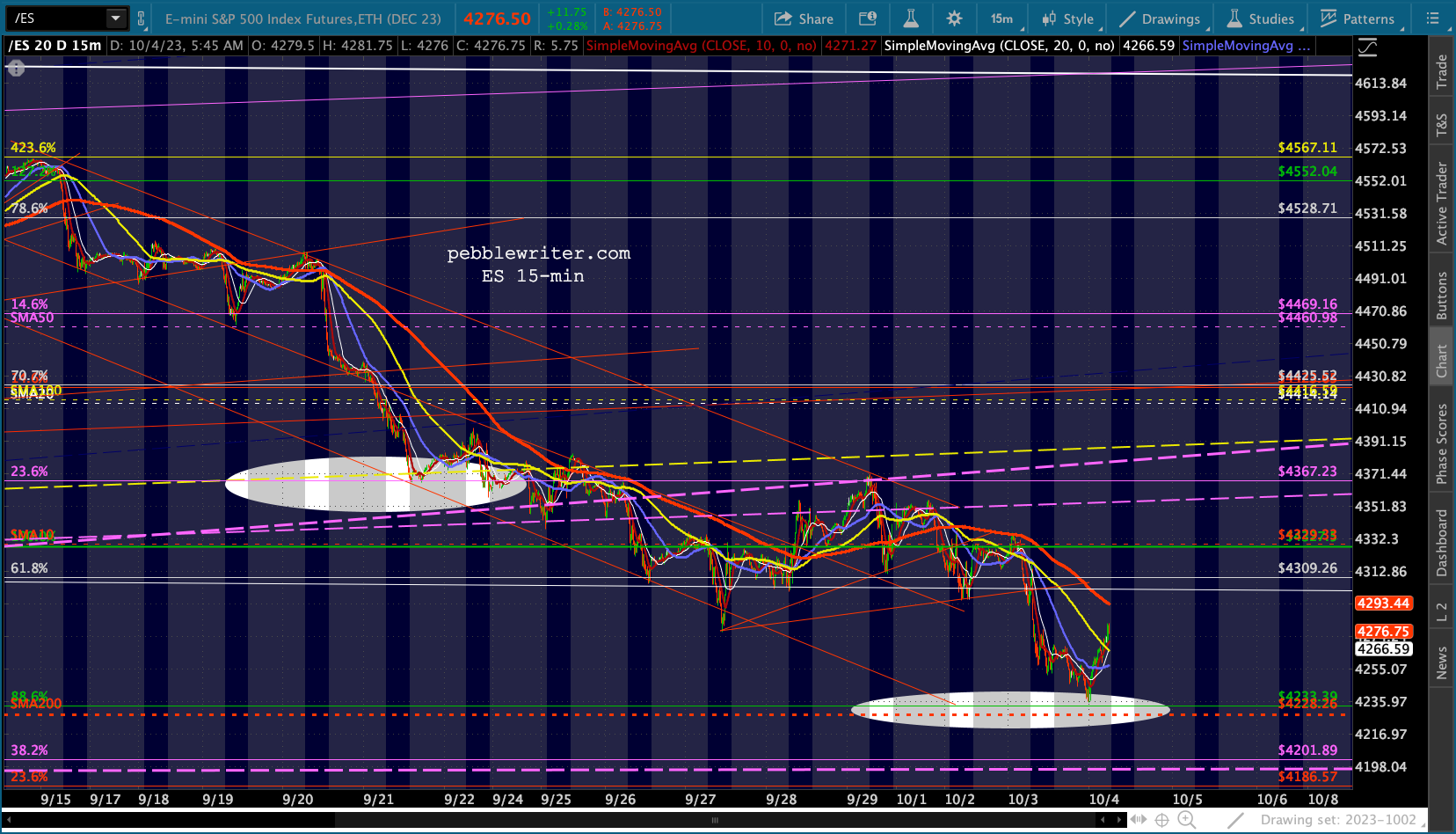

Futures have lost most of their overnight ramp and are almost back to flat.

Futures have lost most of their overnight ramp and are almost back to flat.

continued for members… (more…)

continued for members… (more…)

September PPI came in at 0.5% versus 0.3% expectations, briefly driving down futures prices…until VIX was hammered back down. Its 200-day moving average continues to be the critical threshold for algos.

It remains to be seen whether tomorrow’s CPI print can also be ignored.

It remains to be seen whether tomorrow’s CPI print can also be ignored.

continued for members… (more…)

Futures are up slightly as the bond market reopens and attempts to take stock of the geopolitical situation in the Middle East.

Meanwhile, ES is making an important backtest.

Meanwhile, ES is making an important backtest.

continued for members… (more…)

Equity markets are tumbling following the Hamas attack on Israel this weekend. This comes on the heels of a strong surge off 200-day averages on Friday amid what had been a selloff in oil and gas.

So far, the surge in oil/gas has been held to less than 4%. But, it’s not difficult to imagine the conflict drawing in additional MENA players and unleashing much higher oil prices.

So far, the surge in oil/gas has been held to less than 4%. But, it’s not difficult to imagine the conflict drawing in additional MENA players and unleashing much higher oil prices.

continued for members… (more…)

Employment unexpectedly surged in September, supporting the case for another Fed rate hike. Futures were not amused and are taking another swipe at their 200-day moving average.

continued for members… (more…)

continued for members… (more…)

Futures are testing the upper bounds of the channel from Sep 14. Judging from VIX, currencies and the commodities we watch, ES won’t break out just yet – thus allowing SPX to fully backtest its 200-day moving average.

continued for members… (more…)

continued for members… (more…)

Futures came within 7 points of our 200-day moving average target overnight, begging the question: was that close enough for a legitimate backtest? SPX itself is still 15 points away, close enough by Aug-Oct 2019 standards but nowhere near the overshoot experienced this past March.

The more important question is whether the factors driving stocks lower haven’t yet finished? As we discussed yesterday, the bearish fundamental case has been building momentum lately. What if investors started to care?

The more important question is whether the factors driving stocks lower haven’t yet finished? As we discussed yesterday, the bearish fundamental case has been building momentum lately. What if investors started to care?

continued for members… (more…)

We’ve had a 4.75% target for the 10Y for almost 2 years – reasoning that the breakout in oil/gas prices would eventually force inflation and interest rates higher [see: The 10Y Breaks Out] and equity prices lower.

Sure, the Fed was able to postpone it with the usual misleading jawboning. But, the bill has finally come due.

Higher interest rates, coupled with high energy, housing, and grocery bills and the resumption of student loan payments, present a considerable challenge to the American consumer and economy alike.

Now that the 10Y has reached our target, what does the future hold?

Can the damage to stocks be limited to just a backtest of the 200-day moving average?

Can the damage to stocks be limited to just a backtest of the 200-day moving average? continued for members… (more…)

continued for members… (more…)