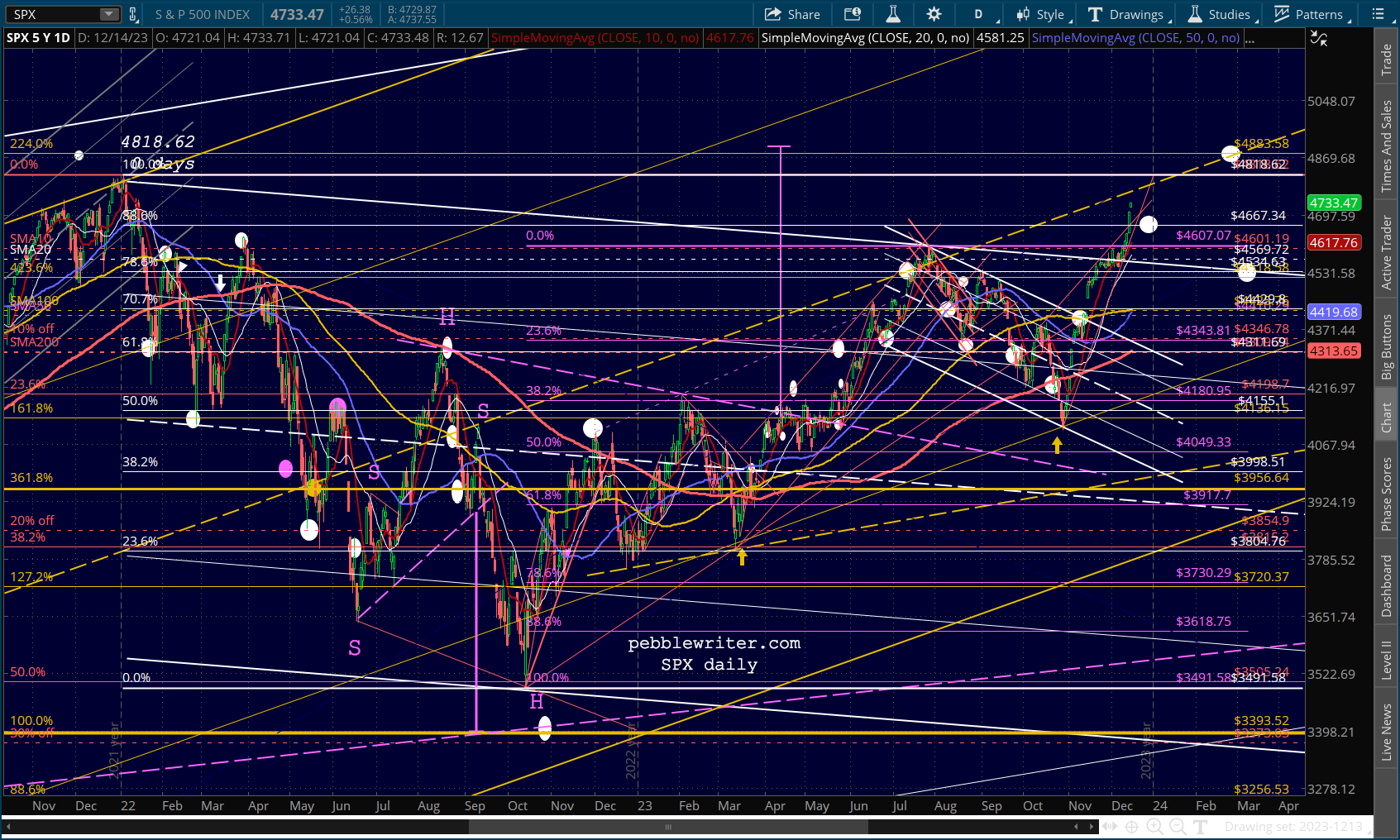

Okay, he didn’t actually say that. But, he might as well have. His latest press conference was completely devoid of any hawkish sentiment. Not only did SPX shoot up past our year-end target… …the 10Y plunged to our downside target.

…the 10Y plunged to our downside target. The message was clear. Interest rates are coming down and the Fed’s third mandate (higher stock prices) is officially in play, with all-time highs are right around the corner. But, are they?

The message was clear. Interest rates are coming down and the Fed’s third mandate (higher stock prices) is officially in play, with all-time highs are right around the corner. But, are they?

We don’t wish to sound negative, so we’ll let Goldman Sachs’ 2024 Equity Outlook do it for us. Stocks might be near record highs, but it’s really just the magnificent 7 which are reaching rarified air. The rest…not so much.

continued for members…

continued for members…

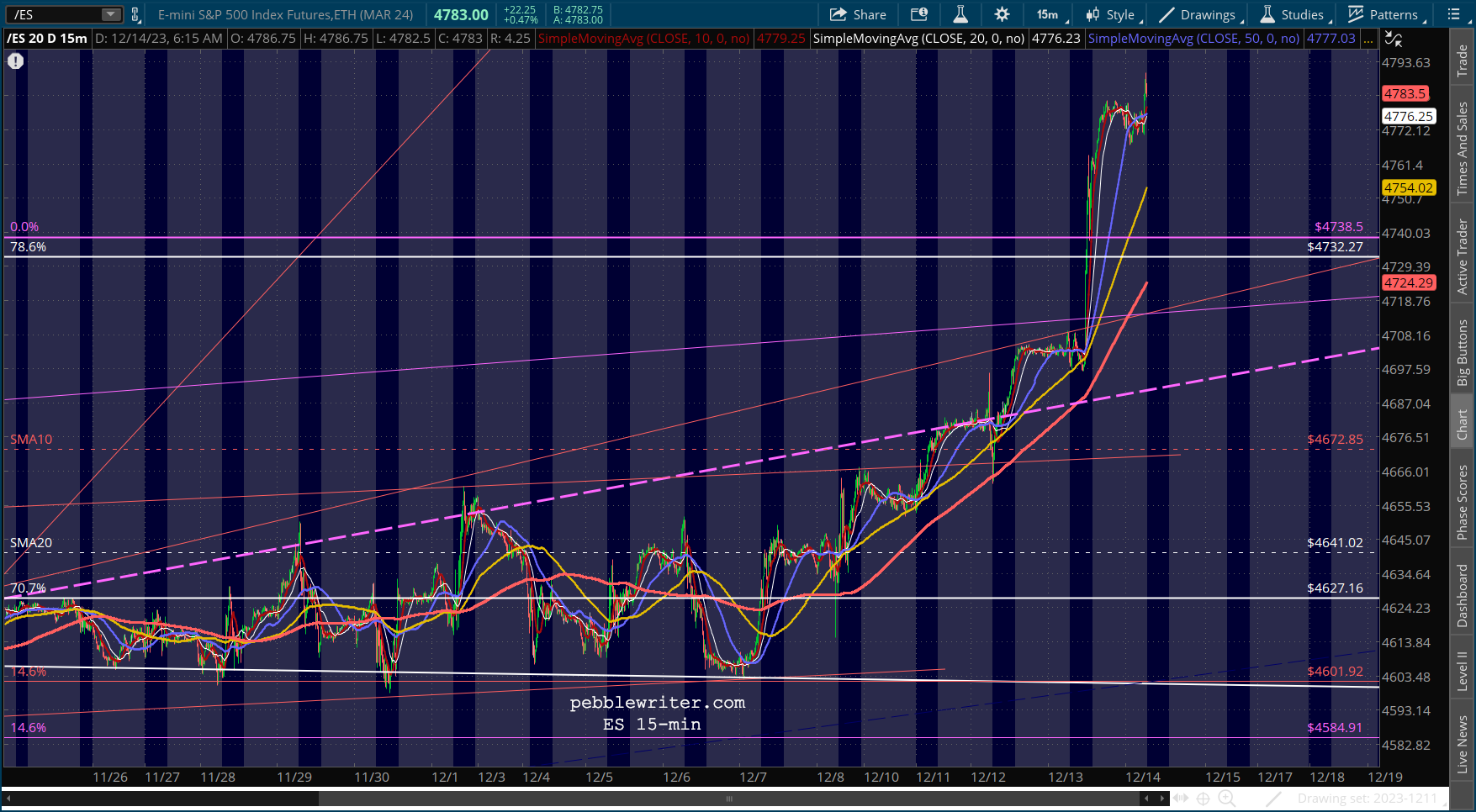

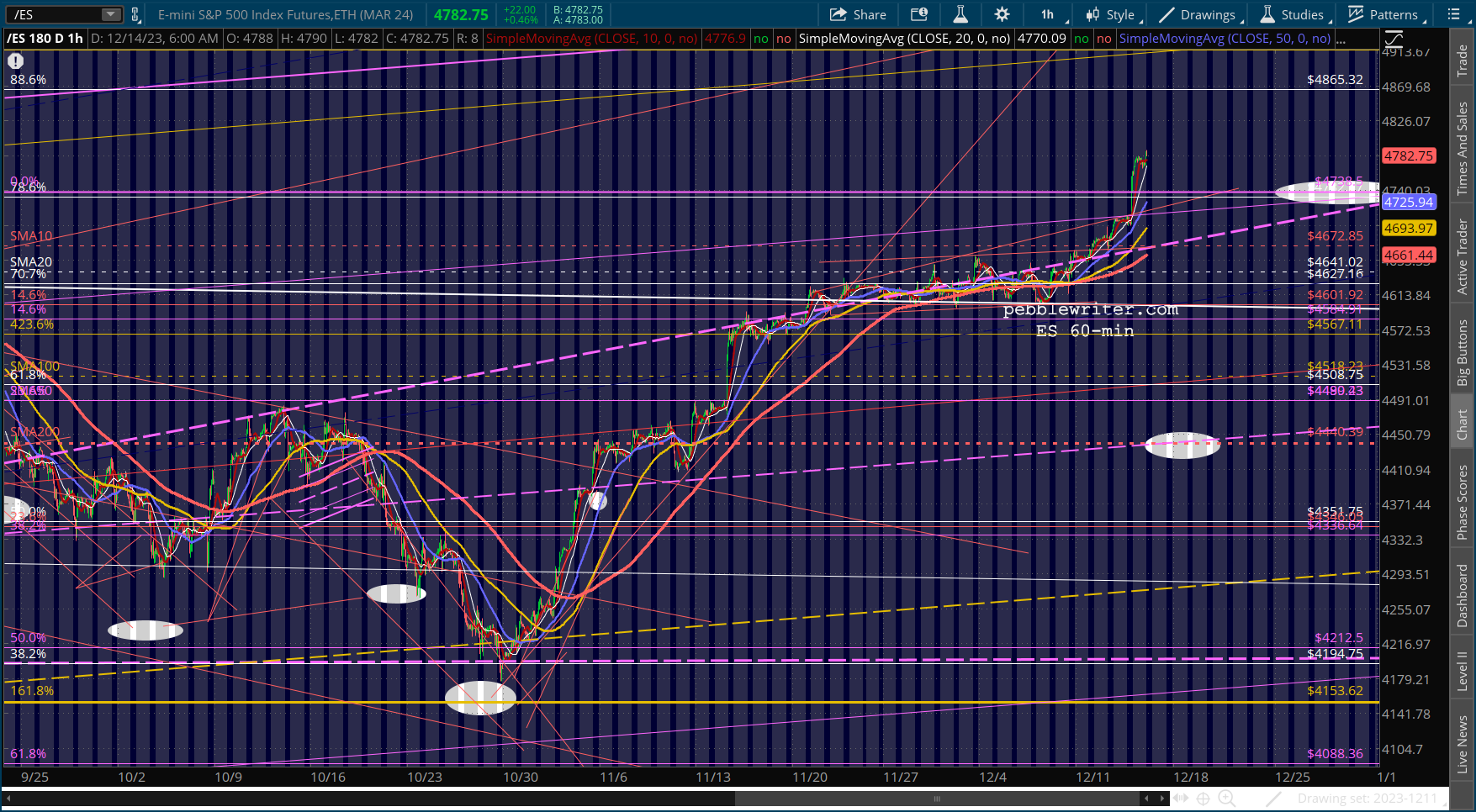

First, a quick overview of markets…

Although ES tagged its 2.24 extension (of the 2020 drop) back in Jan 2022…

Although ES tagged its 2.24 extension (of the 2020 drop) back in Jan 2022… …SPX never did. This puts SPX 4883 on the map – in addition to the former high of 4818.

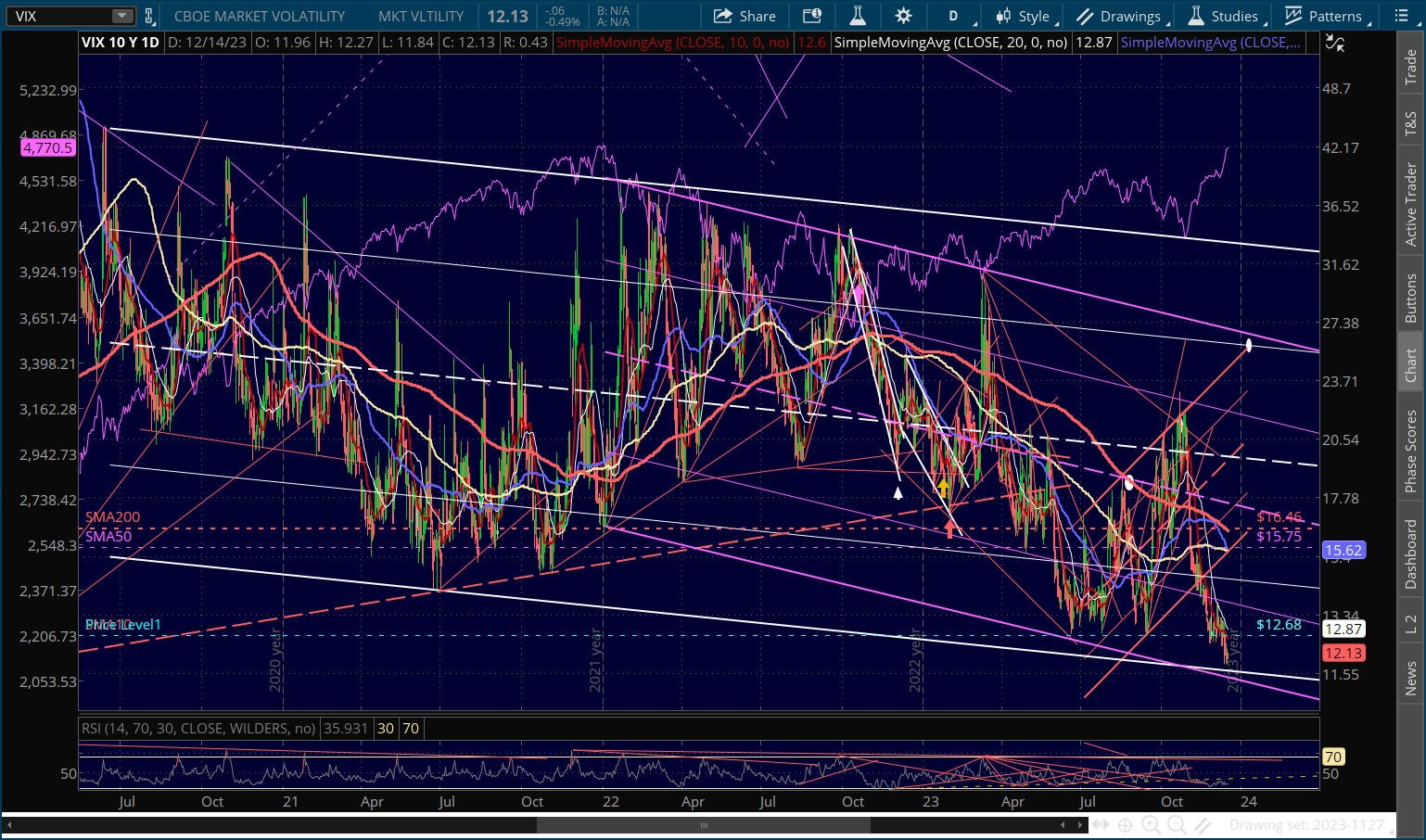

…SPX never did. This puts SPX 4883 on the map – in addition to the former high of 4818. Although VIX appears very close to the purple channel bottom…

Although VIX appears very close to the purple channel bottom…

…it has made a habit of pushing to new lows and breaking below trend line support in order to boost stocks past overhead resistance. The two most notable instances were in late 2015, when SPX needed to get up past its 1.618 extension (of the 2007-2009 crash) and again this past year in order to boost SPX out of its falling channel and above its SMA200.

…it has made a habit of pushing to new lows and breaking below trend line support in order to boost stocks past overhead resistance. The two most notable instances were in late 2015, when SPX needed to get up past its 1.618 extension (of the 2007-2009 crash) and again this past year in order to boost SPX out of its falling channel and above its SMA200.

Currencies are standing by, but there’s little for them to do at the moment. EURUSD moved very little after this morning’s ECB announcement that rates would be held steady. But, as soon as Legard took a somewhat more hawkish tone in her presser, EURUSD began edging higher. As expected, it held its SMA200, and is now pushing up against the top of a flag pattern.

Currencies are standing by, but there’s little for them to do at the moment. EURUSD moved very little after this morning’s ECB announcement that rates would be held steady. But, as soon as Legard took a somewhat more hawkish tone in her presser, EURUSD began edging higher. As expected, it held its SMA200, and is now pushing up against the top of a flag pattern.

USDJPY is playing cat and mouse with its own SMA200…

USDJPY is playing cat and mouse with its own SMA200…

…and, DXY is backtesting the white fan line from Jun 2021 again.

…and, DXY is backtesting the white fan line from Jun 2021 again.

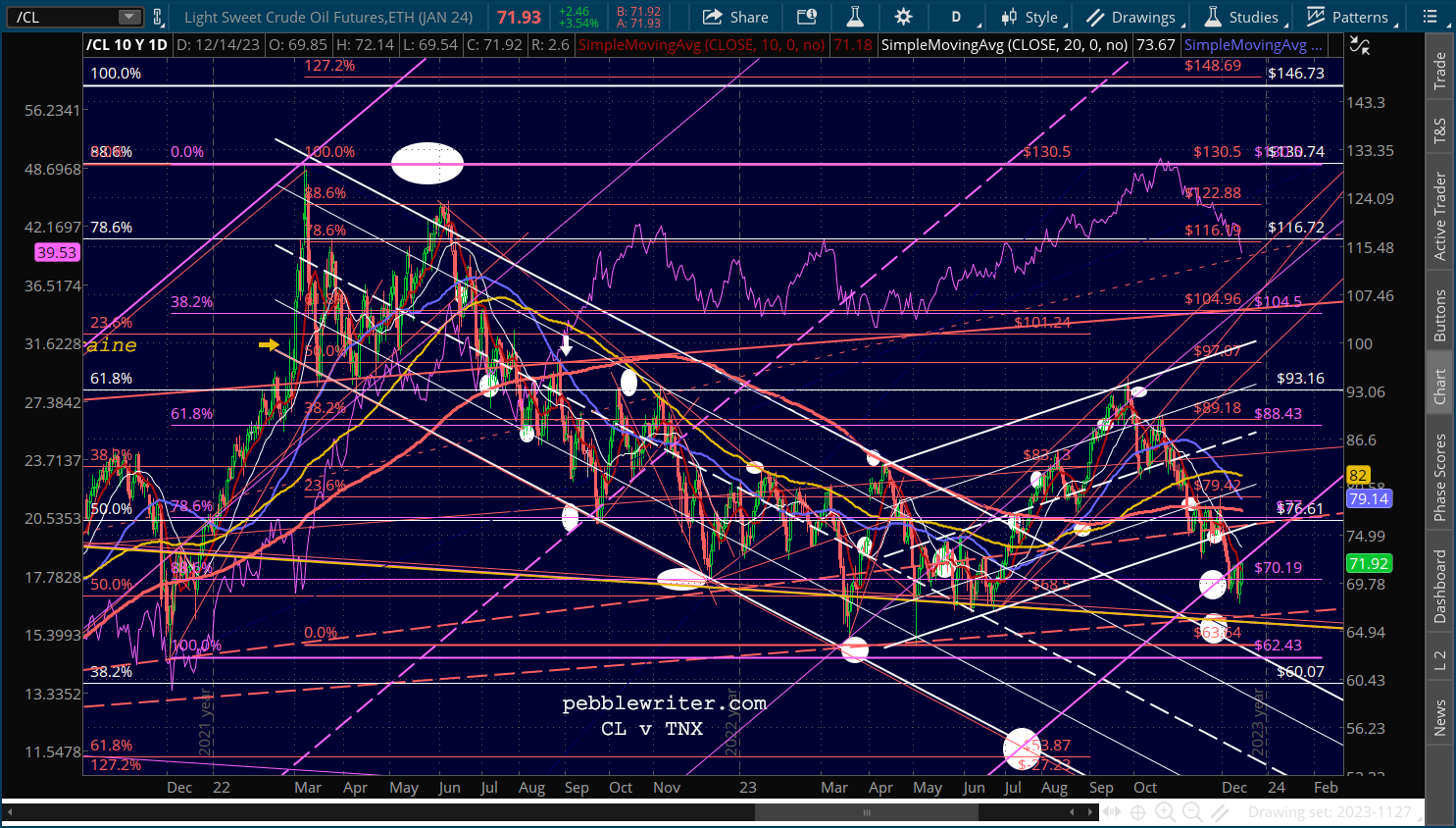

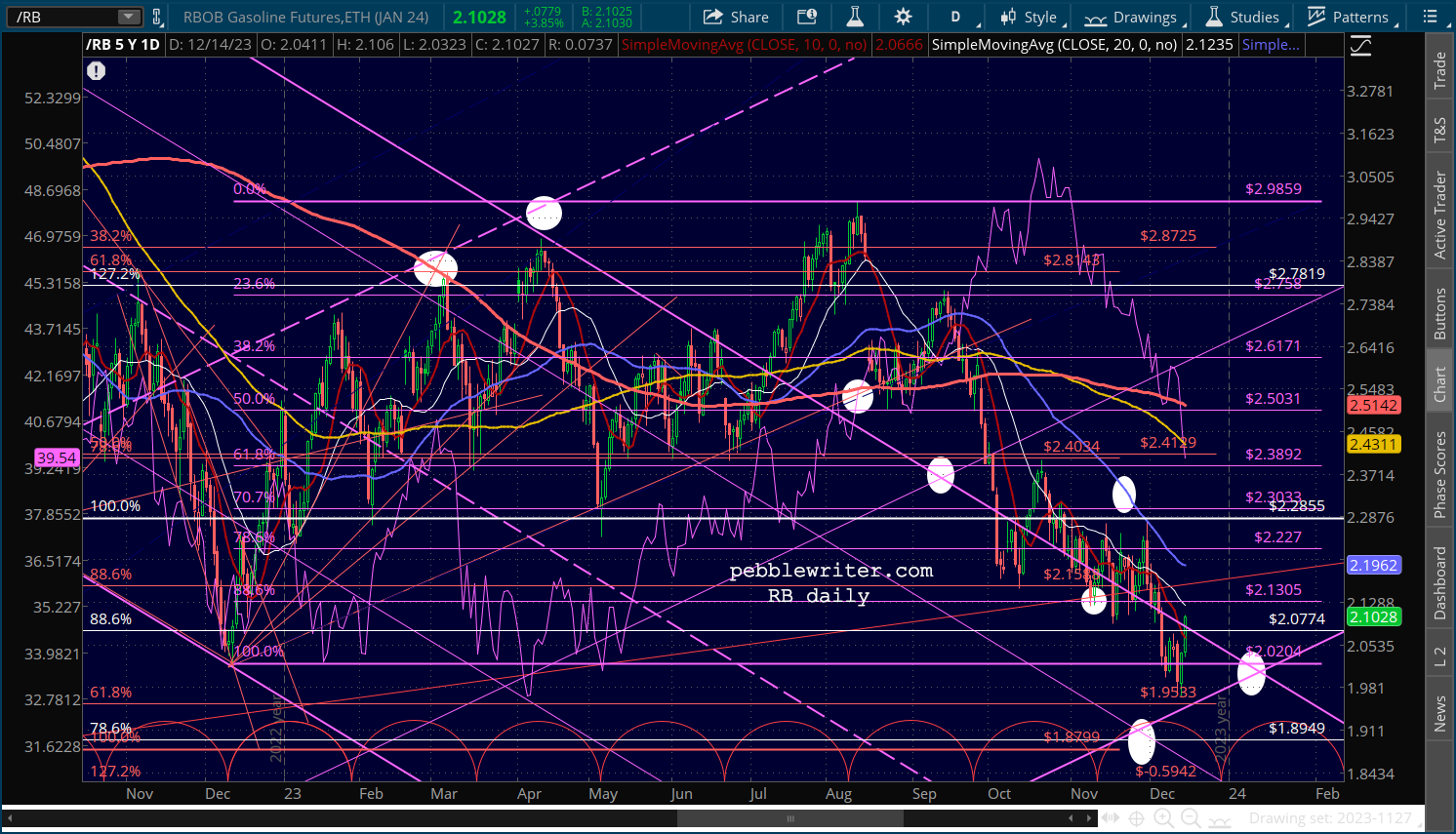

No longer needed in order to force rates lower (at least, today) CL and RB are getting a small relief bounce – a backtest, though – which has probably played out already.

No longer needed in order to force rates lower (at least, today) CL and RB are getting a small relief bounce – a backtest, though – which has probably played out already.

Aside from stocks, the big action this morning is in bonds. The 10Y finally broke down below the trend line from Dec 2021. This has been great support since May and it has remained our downside target until a few months ago when it became apparent that the SMA200 wasn’t going to quite make it up to the TL itself.

Aside from stocks, the big action this morning is in bonds. The 10Y finally broke down below the trend line from Dec 2021. This has been great support since May and it has remained our downside target until a few months ago when it became apparent that the SMA200 wasn’t going to quite make it up to the TL itself.  If the SMA200 doesn’t hold, that red channel midline just below current levels at about 3.80-3.88% is a very appealing target.

If the SMA200 doesn’t hold, that red channel midline just below current levels at about 3.80-3.88% is a very appealing target.

We’re likely to get a bounce here that backtests the SMA200 at 4.03 and potentially the purple fan line at 4.13.

We’re likely to get a bounce here that backtests the SMA200 at 4.03 and potentially the purple fan line at 4.13.

Ultimately, rates should move lower as long as inflation does. And, inflation should as long as oil and gas don’t bounce sharply. The other reason rates move lower, of course, is when equities run into trouble and funds move from stocks to bonds.

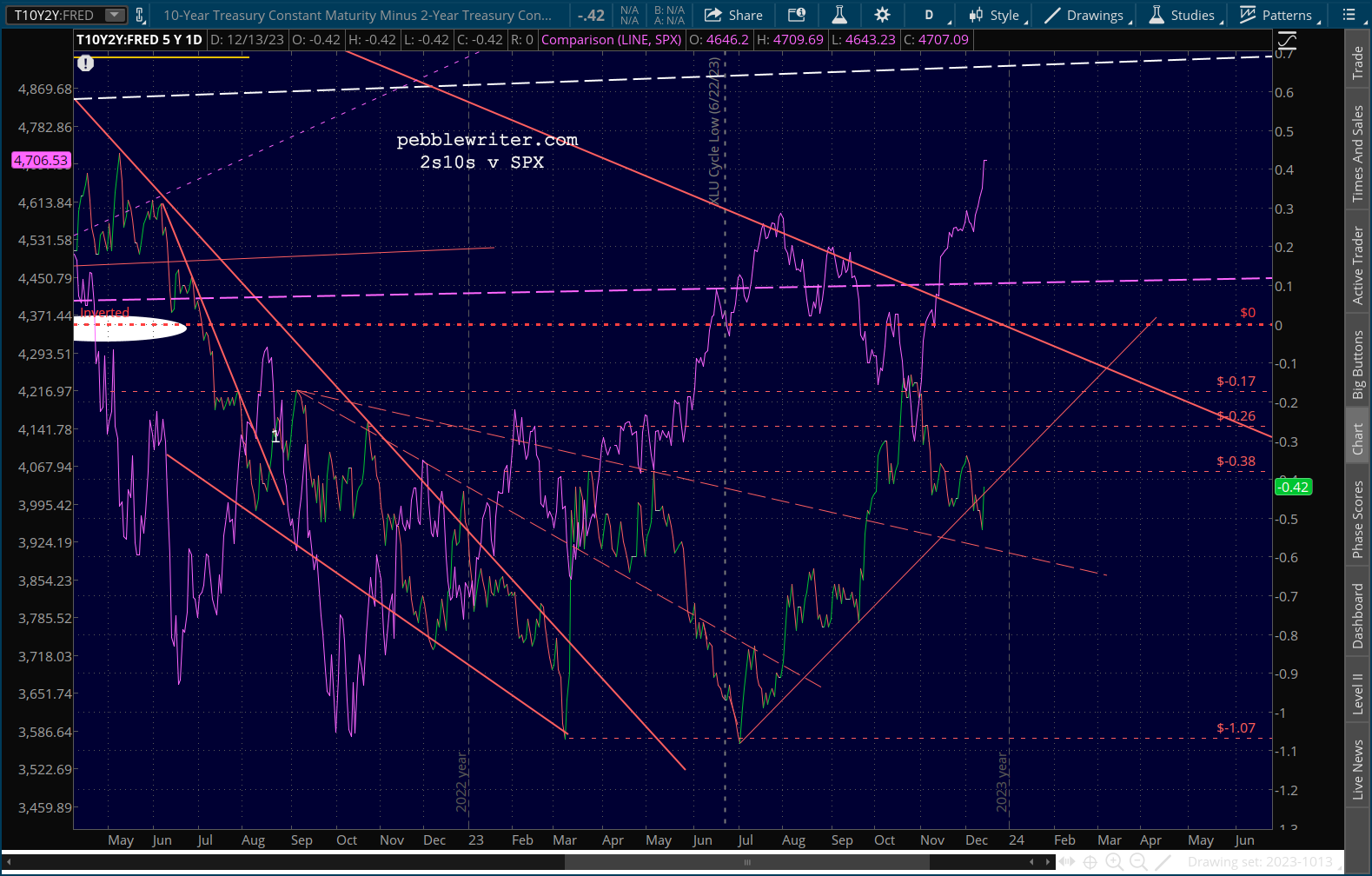

We’re already seeing the “breakdown” in the 2s10s reverse.  It should make bulls a little nervous as an unwinding of the inversion would be disastrous for stocks.

It should make bulls a little nervous as an unwinding of the inversion would be disastrous for stocks.

GLTA.