Algos popped in the past hour on a larger than expected increase in initial jobless claims with the more important NFP due out tomorrow.

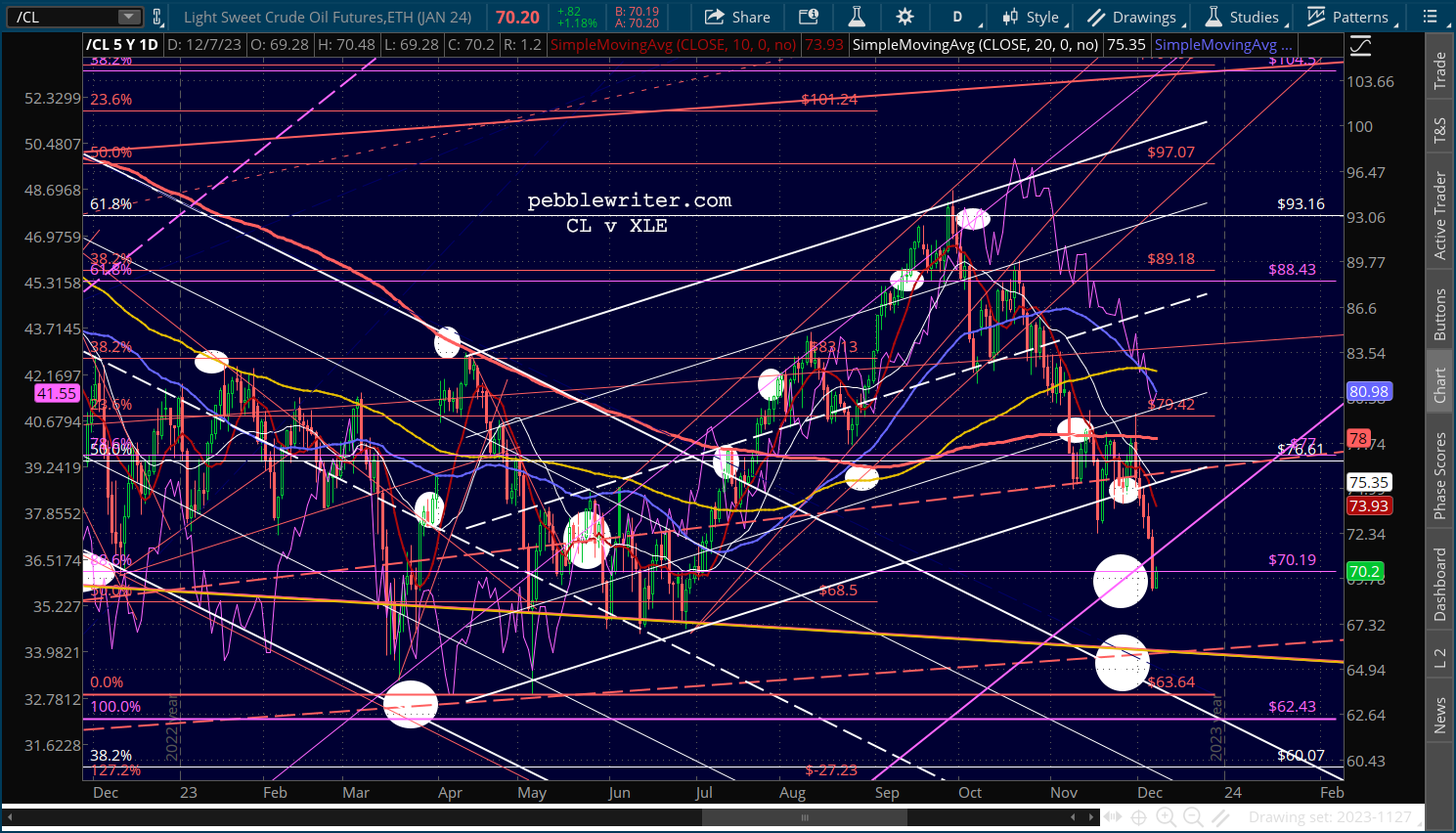

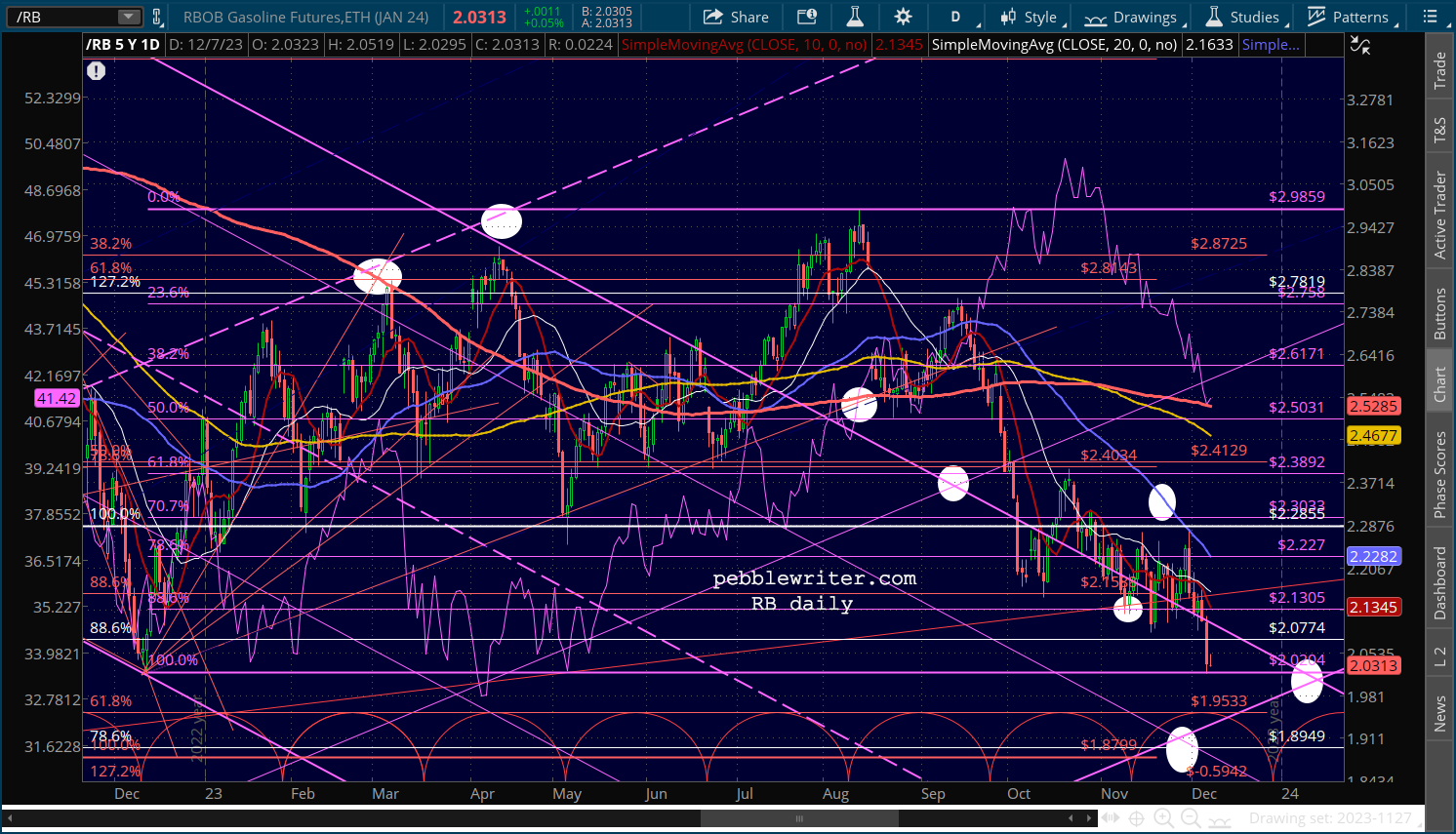

But, the more dramatic move has been in oil, with CL reaching our next downside target and RB well on its way to its own.

But, the more dramatic move has been in oil, with CL reaching our next downside target and RB well on its way to its own.

continued for members…

continued for members…

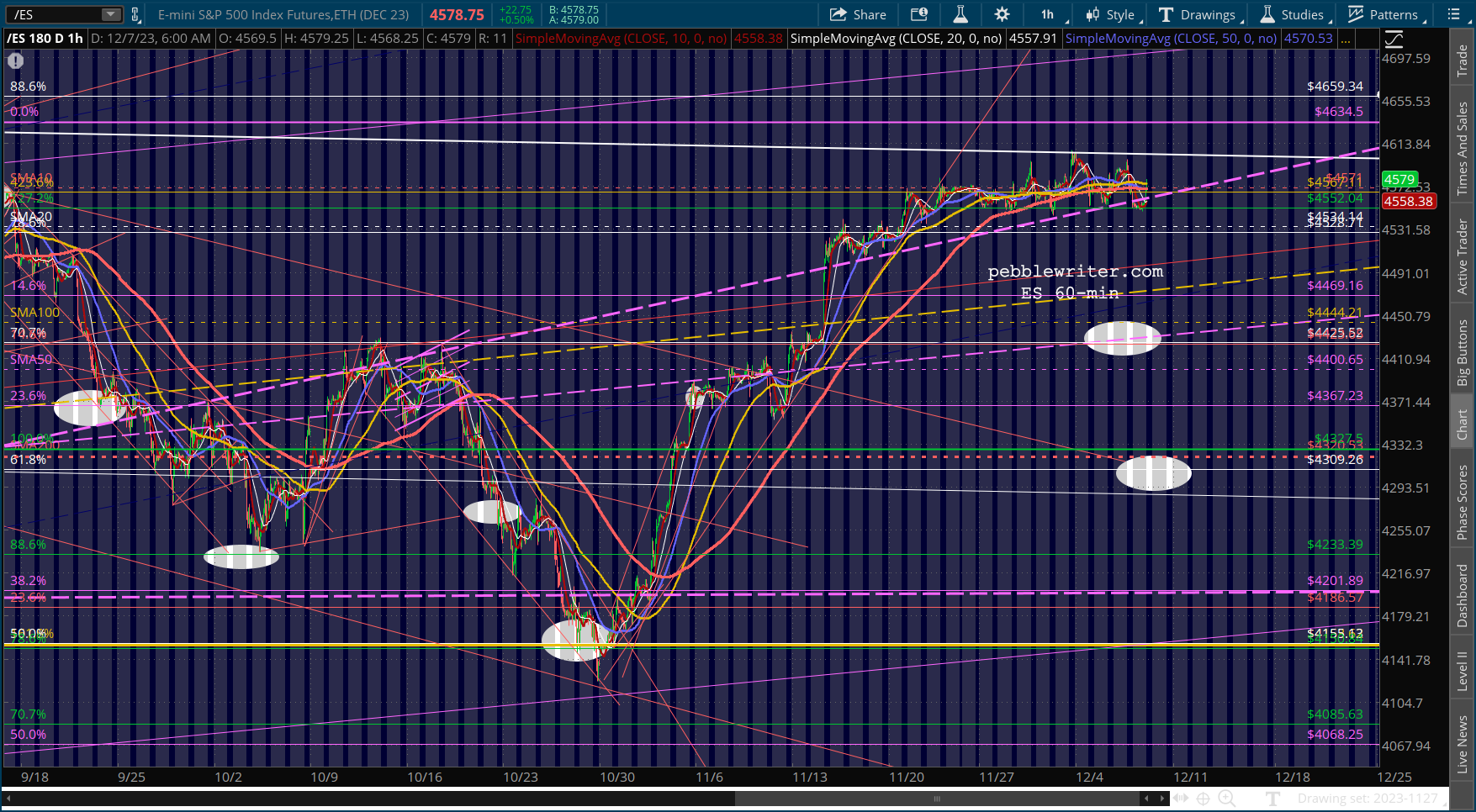

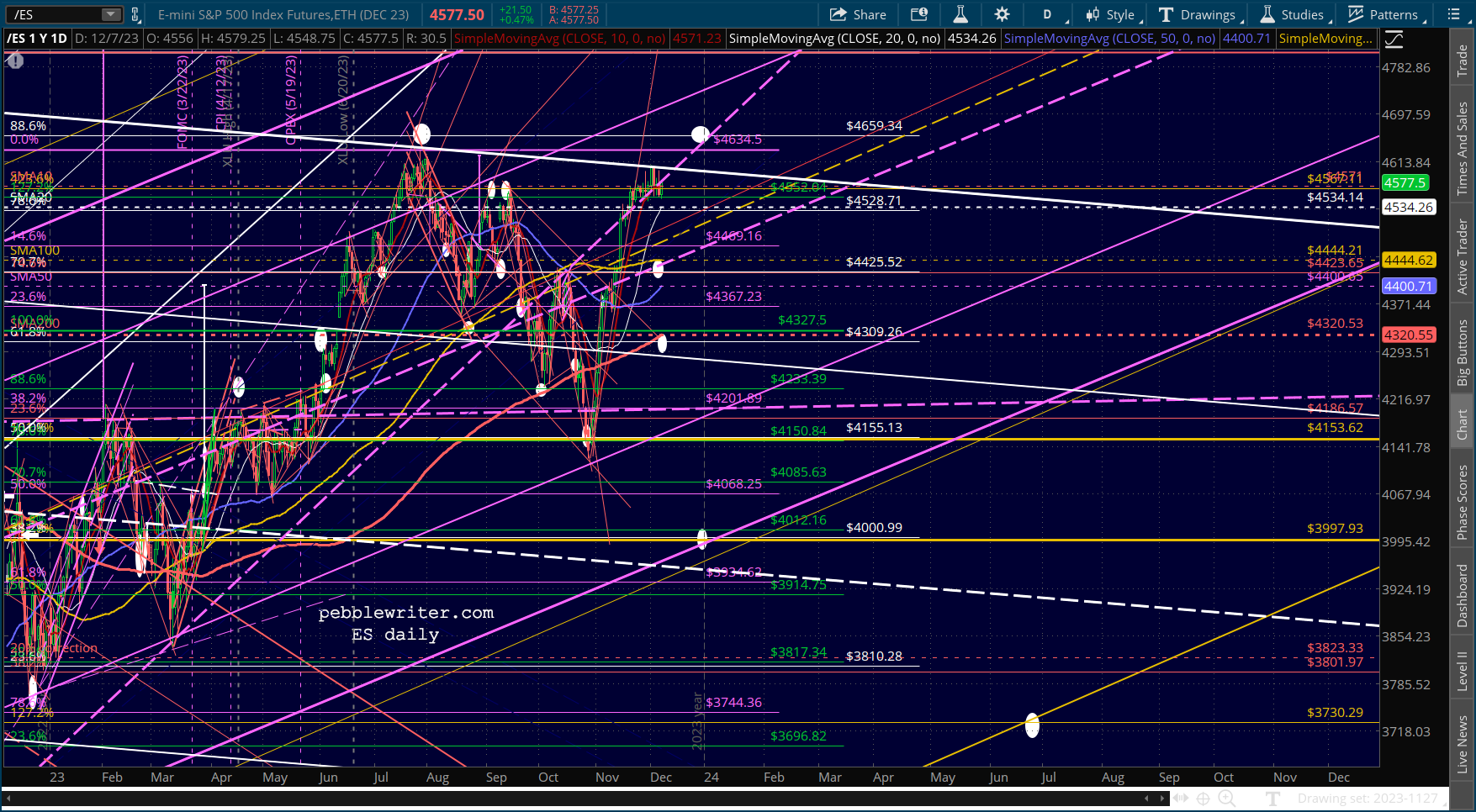

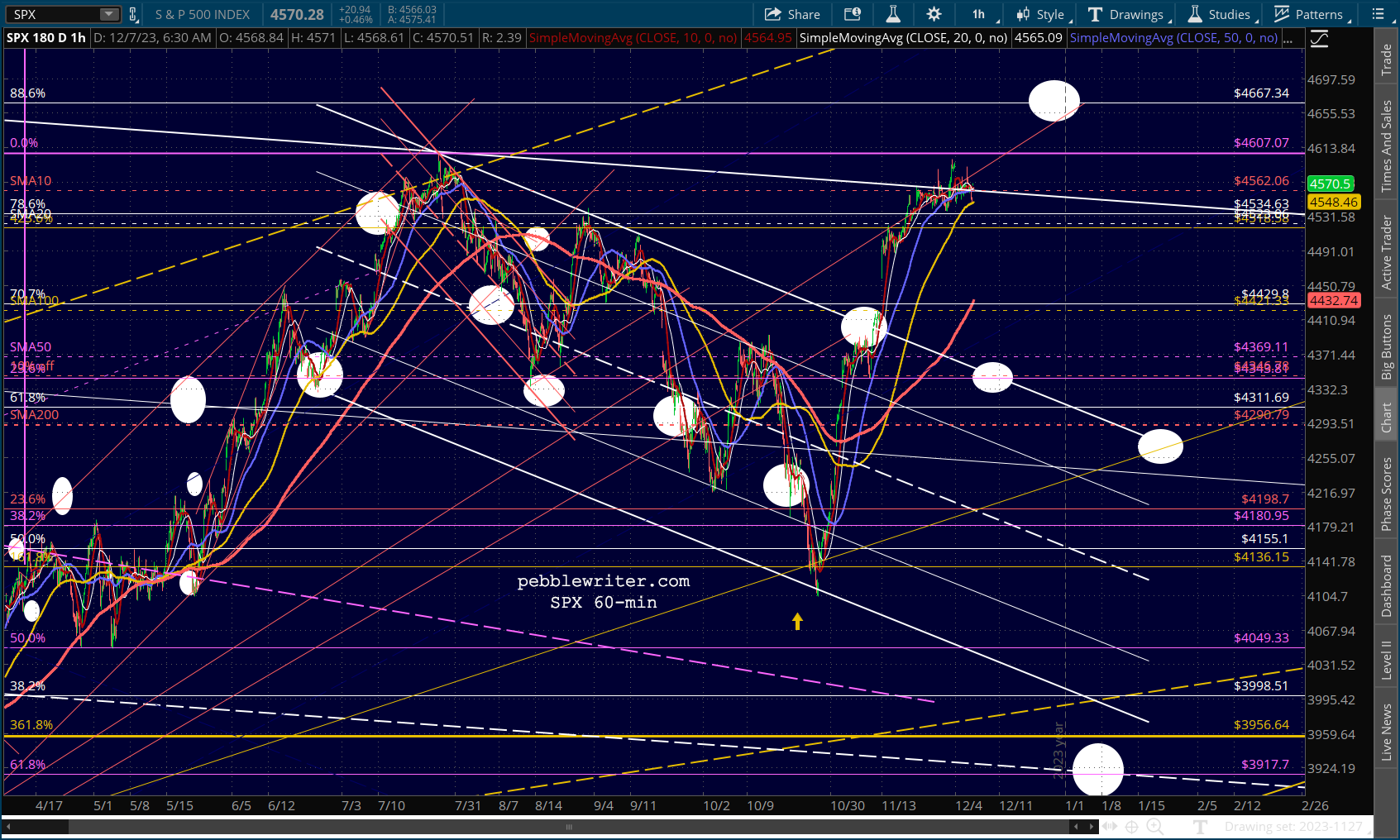

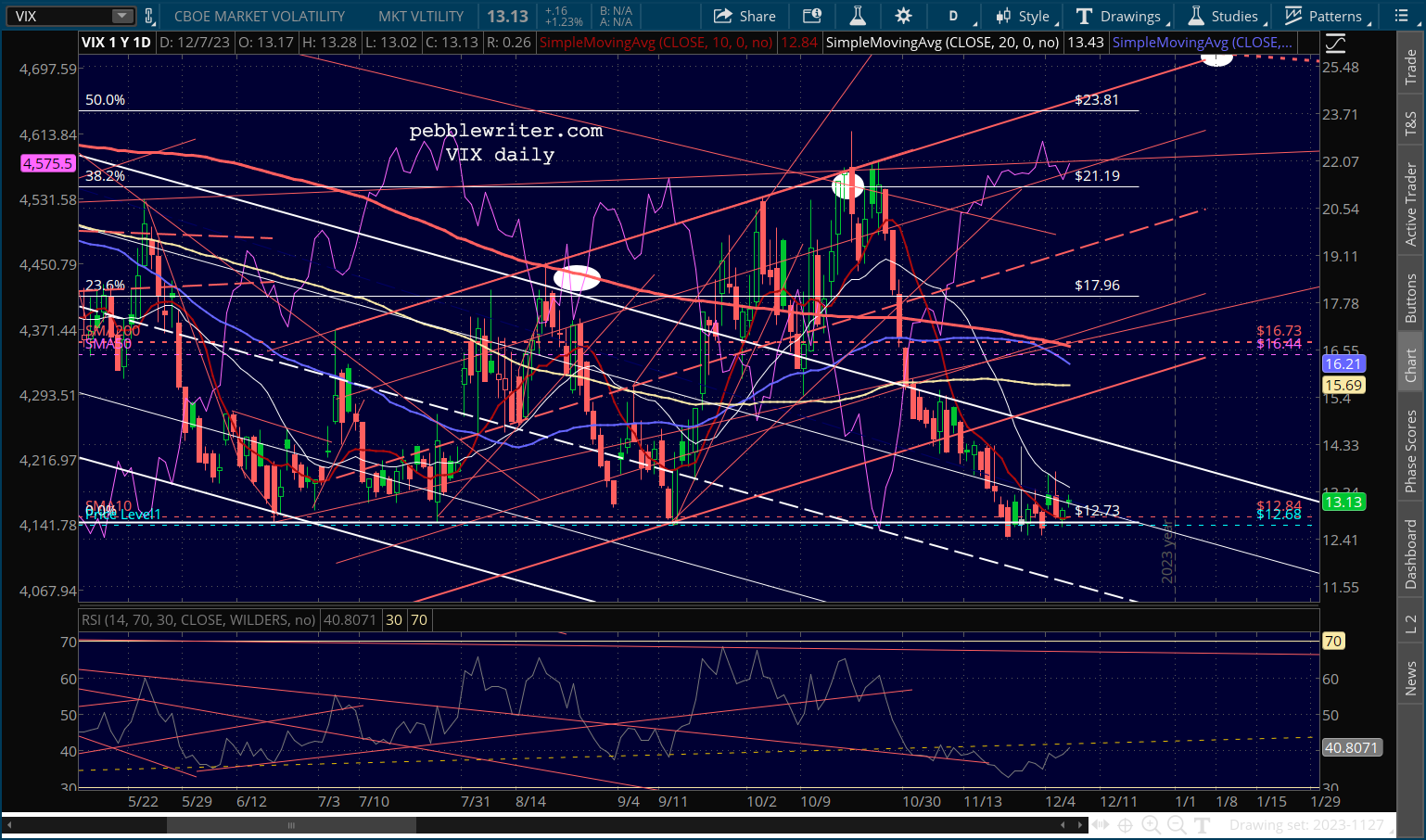

First a wrapup of the markets…

VIX continues its games, but is back above its SMA10.

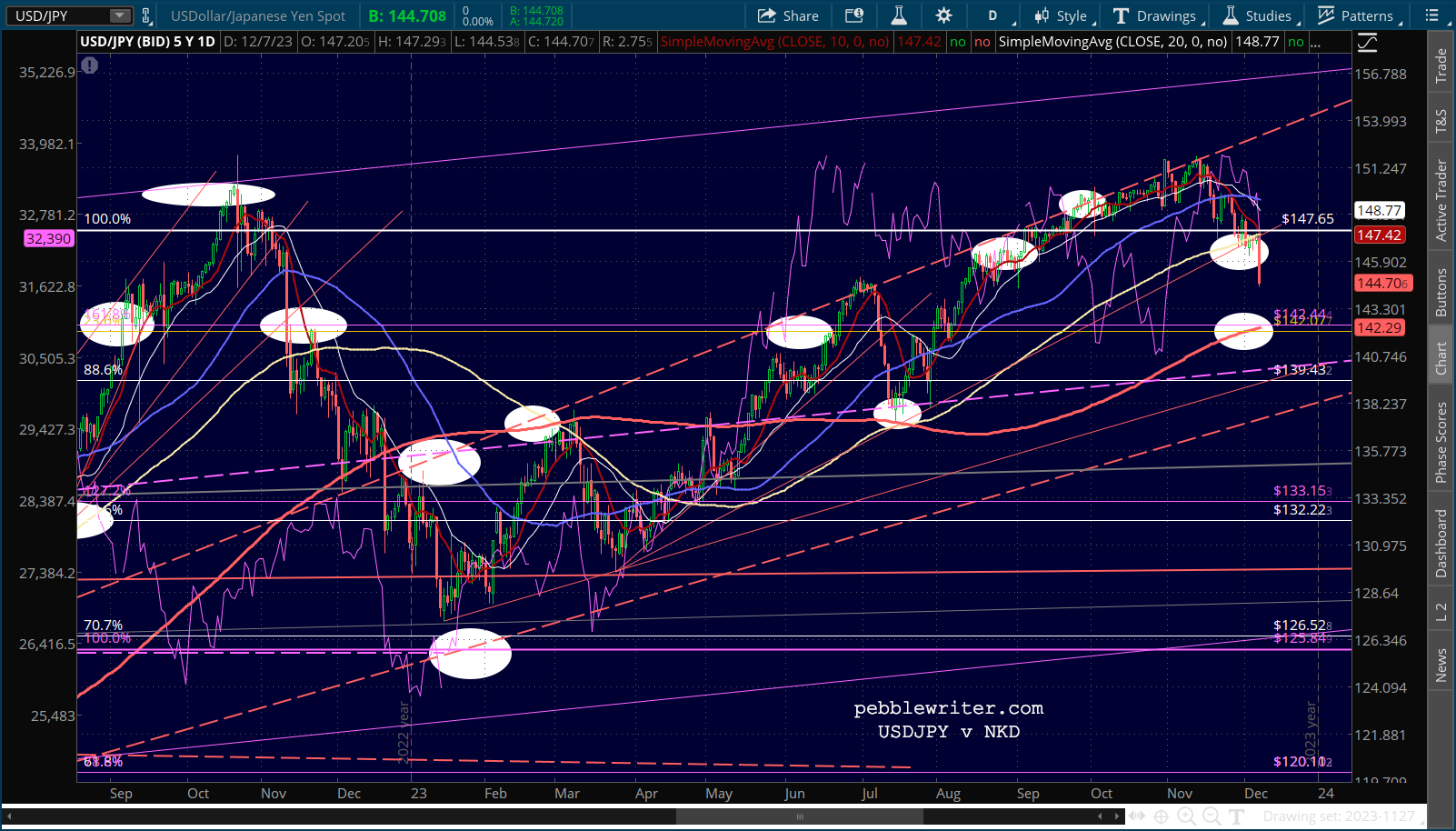

VIX continues its games, but is back above its SMA10. USDJPY has finally broken down and is approaching our SMA200- target – a net negative for stocks until it bounces on the SMA200 itself.

USDJPY has finally broken down and is approaching our SMA200- target – a net negative for stocks until it bounces on the SMA200 itself.

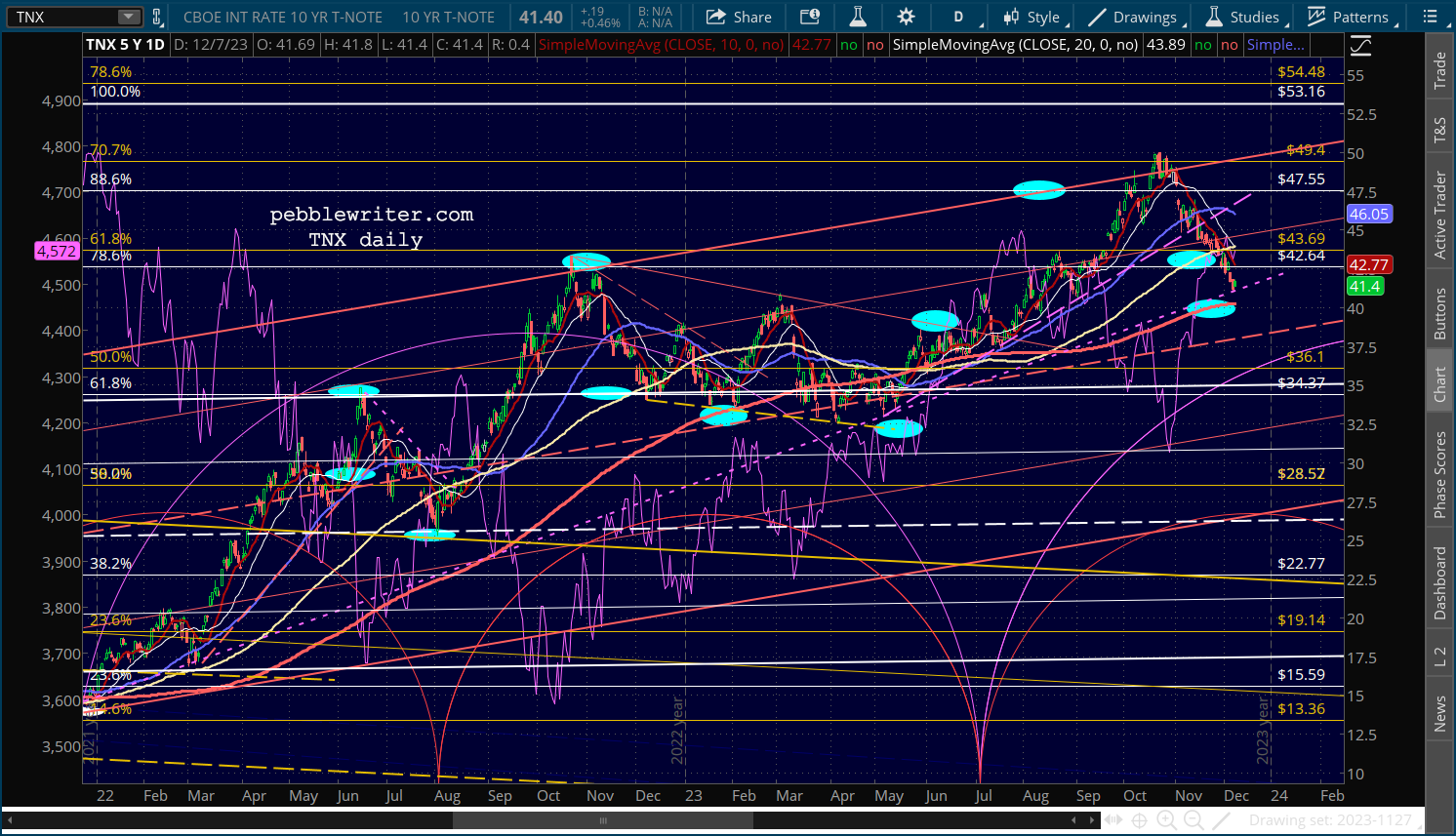

The decline in oil and gas continues to keep the pressure up on interest rates…

The decline in oil and gas continues to keep the pressure up on interest rates…

…driving TNX to within a whisper of its SMA200 at 4.027. Needless to say, dropping below 4% would be a very big deal for the markets.

…driving TNX to within a whisper of its SMA200 at 4.027. Needless to say, dropping below 4% would be a very big deal for the markets. If the 10Y breaks down below its purple TL below, it could cause the 2s10s to also break down. It appears to already be doing so – a negative for stocks.

If the 10Y breaks down below its purple TL below, it could cause the 2s10s to also break down. It appears to already be doing so – a negative for stocks.

But, the psychological boost of seeing rates drop through a key level will likely offset the move by the 2s10s.

But, the psychological boost of seeing rates drop through a key level will likely offset the move by the 2s10s.

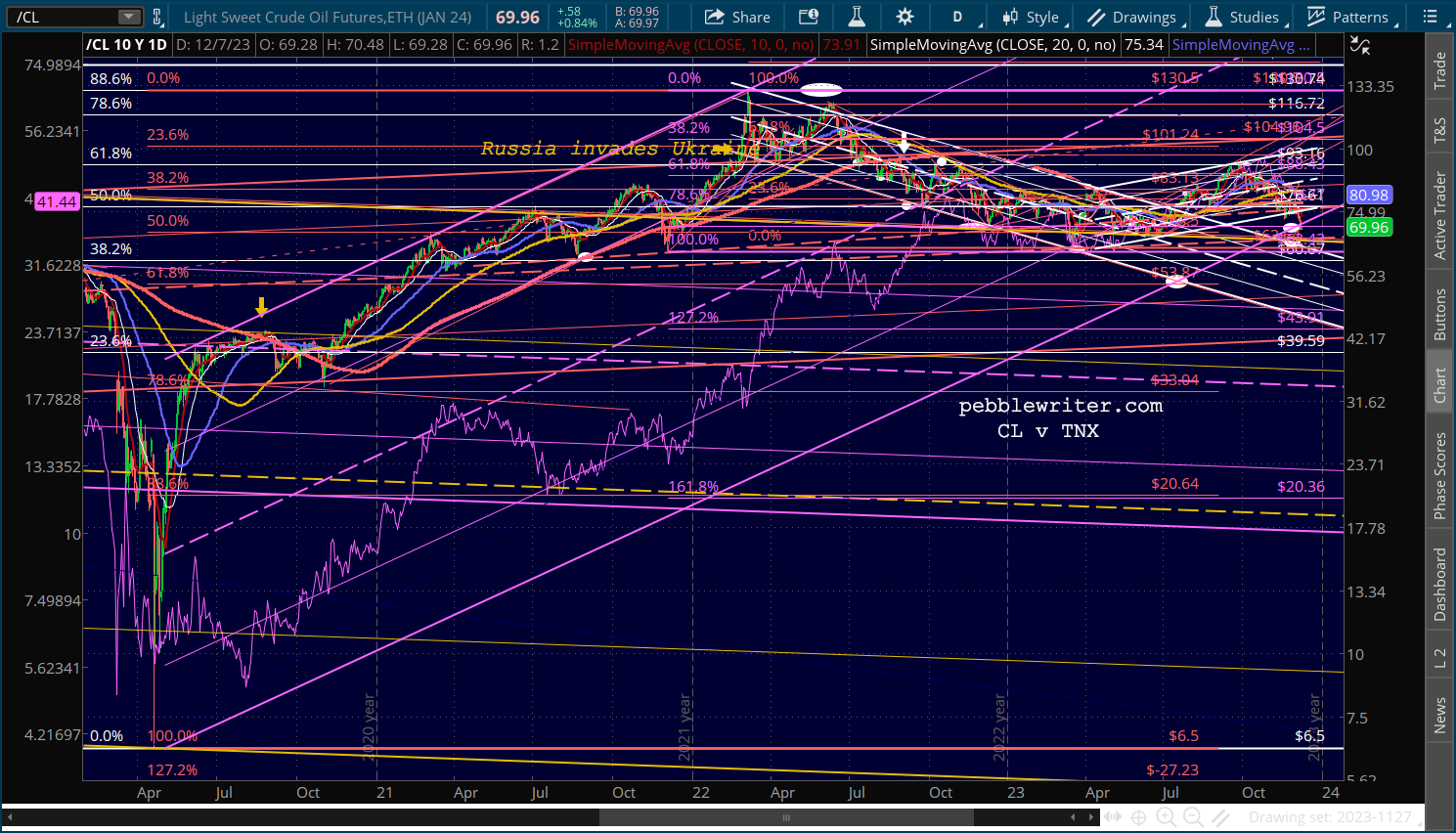

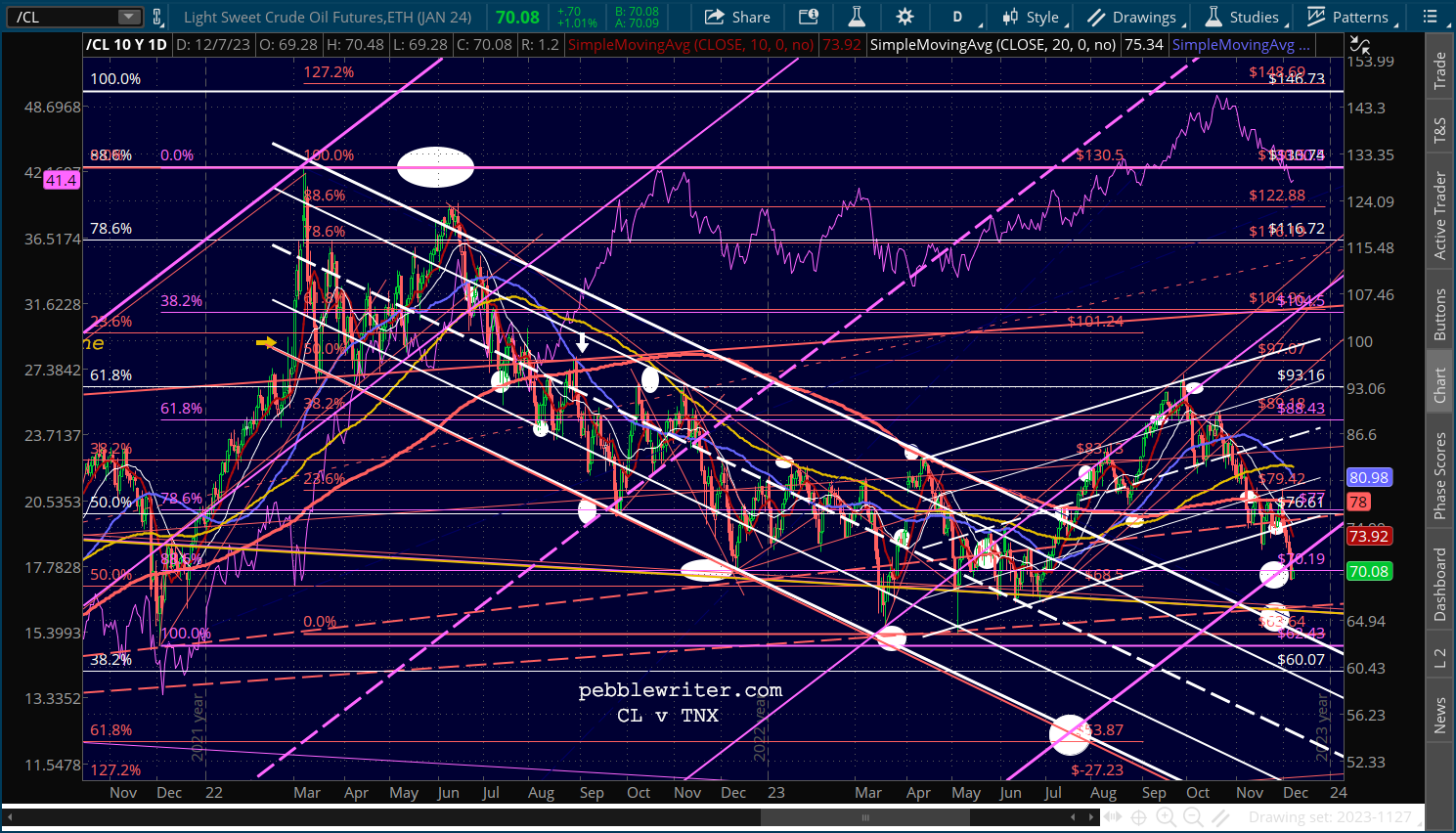

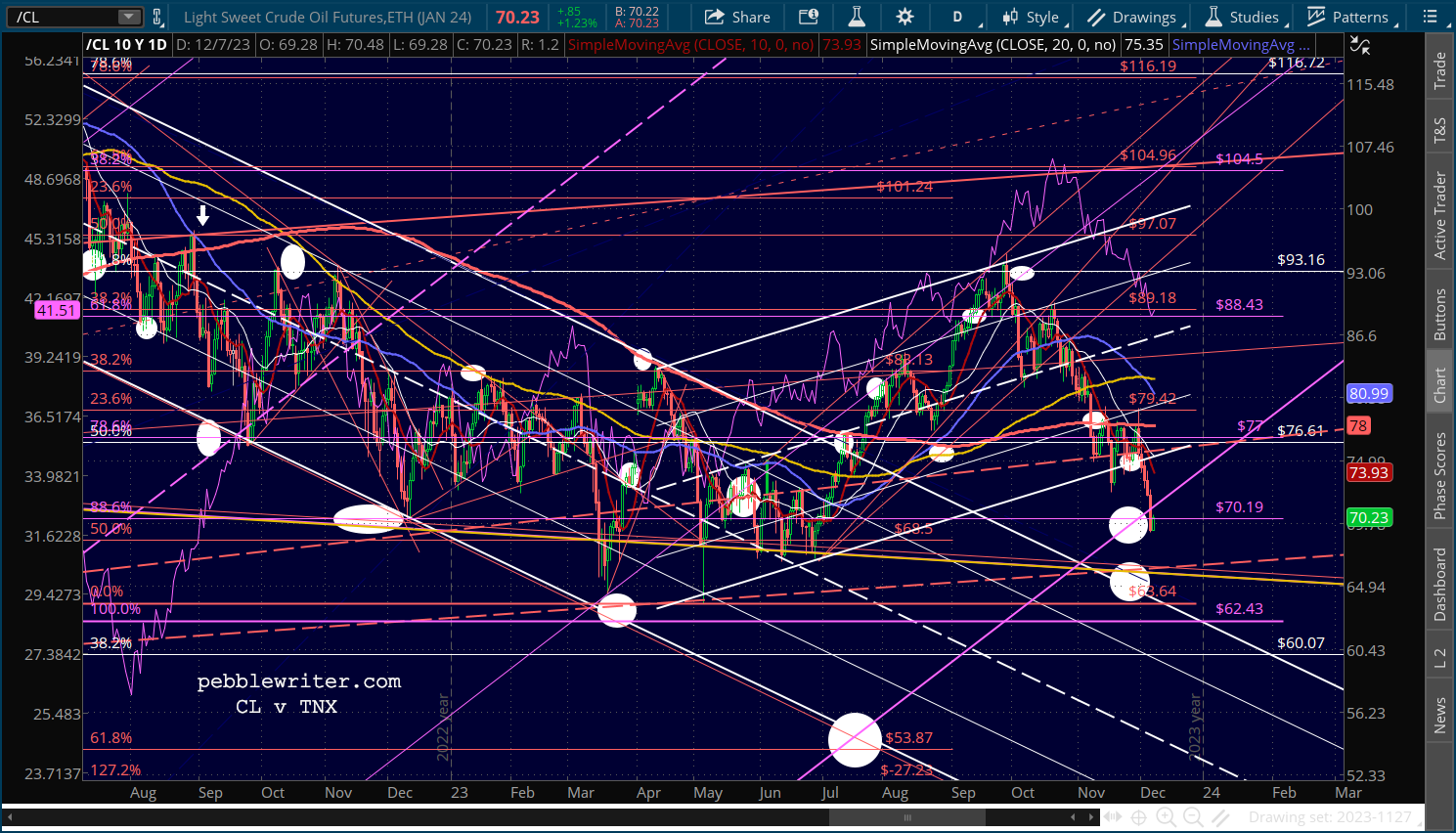

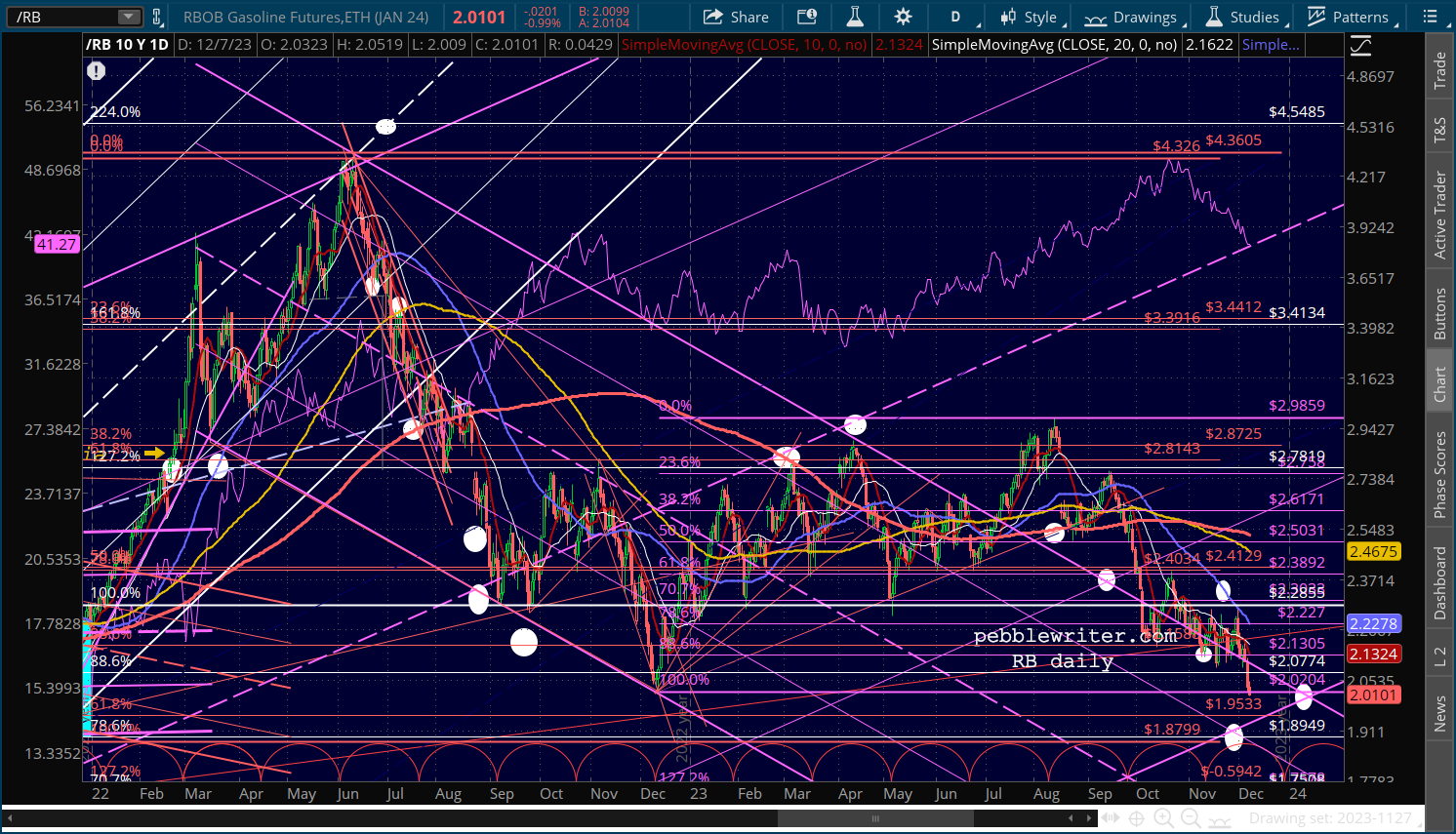

In looking at a longer term chart of CL, we can see that this latest drop puts it at the bottom of the large purple channel from April 2020.

The charts initially targeted the red .618 at 53.87 in July, but the well-formed falling white channel dating back to the Russian invasion of Ukraine.

The charts initially targeted the red .618 at 53.87 in July, but the well-formed falling white channel dating back to the Russian invasion of Ukraine. But, the May 4 plunge to new lows touched off a 6-month rally that saw a breakout of the channel that ultimately drove the 10Y up over 5%.

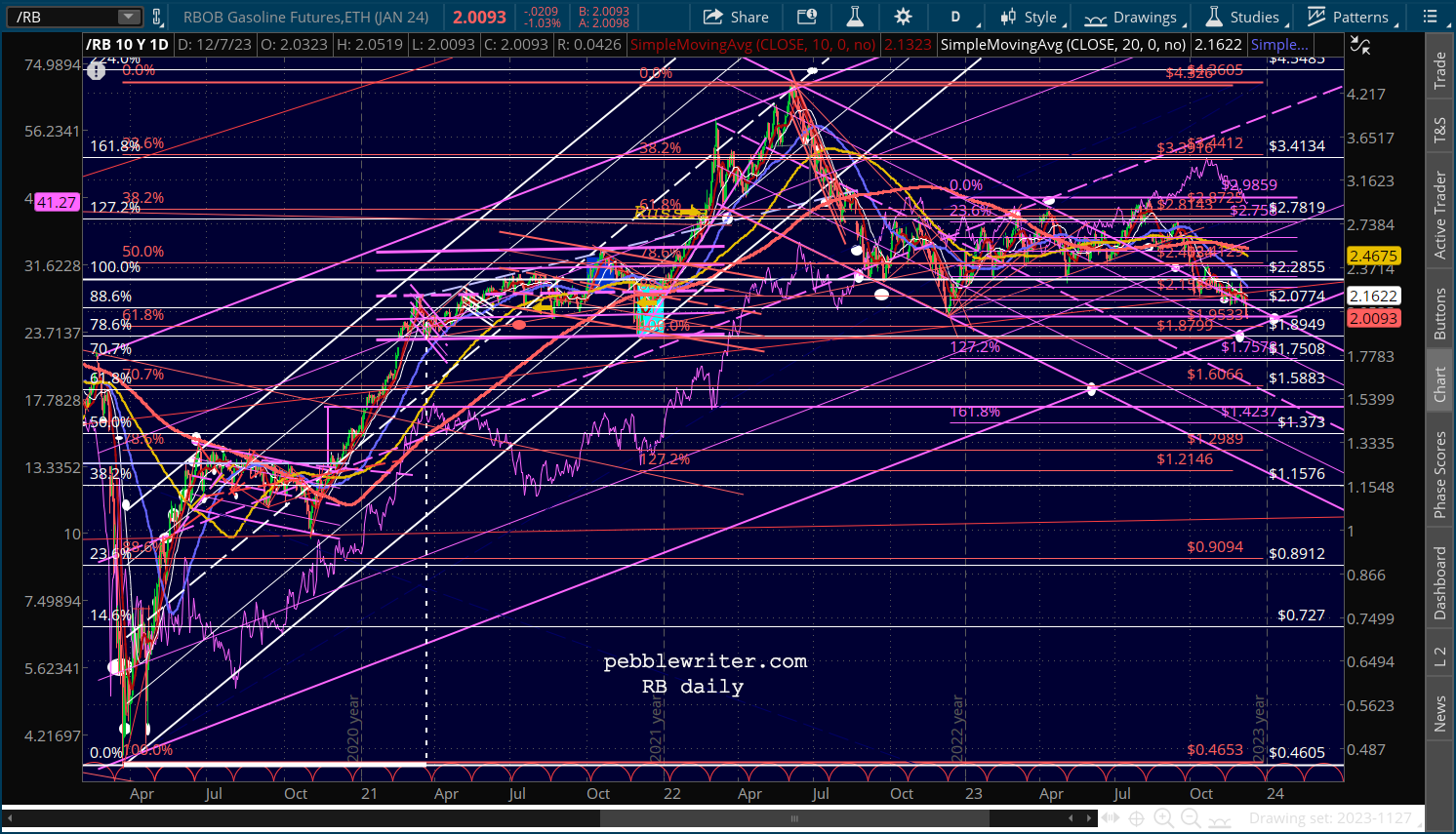

But, the May 4 plunge to new lows touched off a 6-month rally that saw a breakout of the channel that ultimately drove the 10Y up over 5%. We’ve focused more on gasoline prices, as there is a large and immediate impact on CPI. RB saw a similar pattern to CL, also possessing a positive correlation with the 10Y and a breakout of the falling purple channel in July.

We’ve focused more on gasoline prices, as there is a large and immediate impact on CPI. RB saw a similar pattern to CL, also possessing a positive correlation with the 10Y and a breakout of the falling purple channel in July.

The most recent drop puts it within striking distance of the purple channel bottom at 1.89ish – hence our downside target there.

The most recent drop puts it within striking distance of the purple channel bottom at 1.89ish – hence our downside target there. Since the YoY changes in CL and RB help CPI, and CPI drives the 10Y, it’s important to note that the recent trends in gas prices suggest continuing pressure on the 10Y.

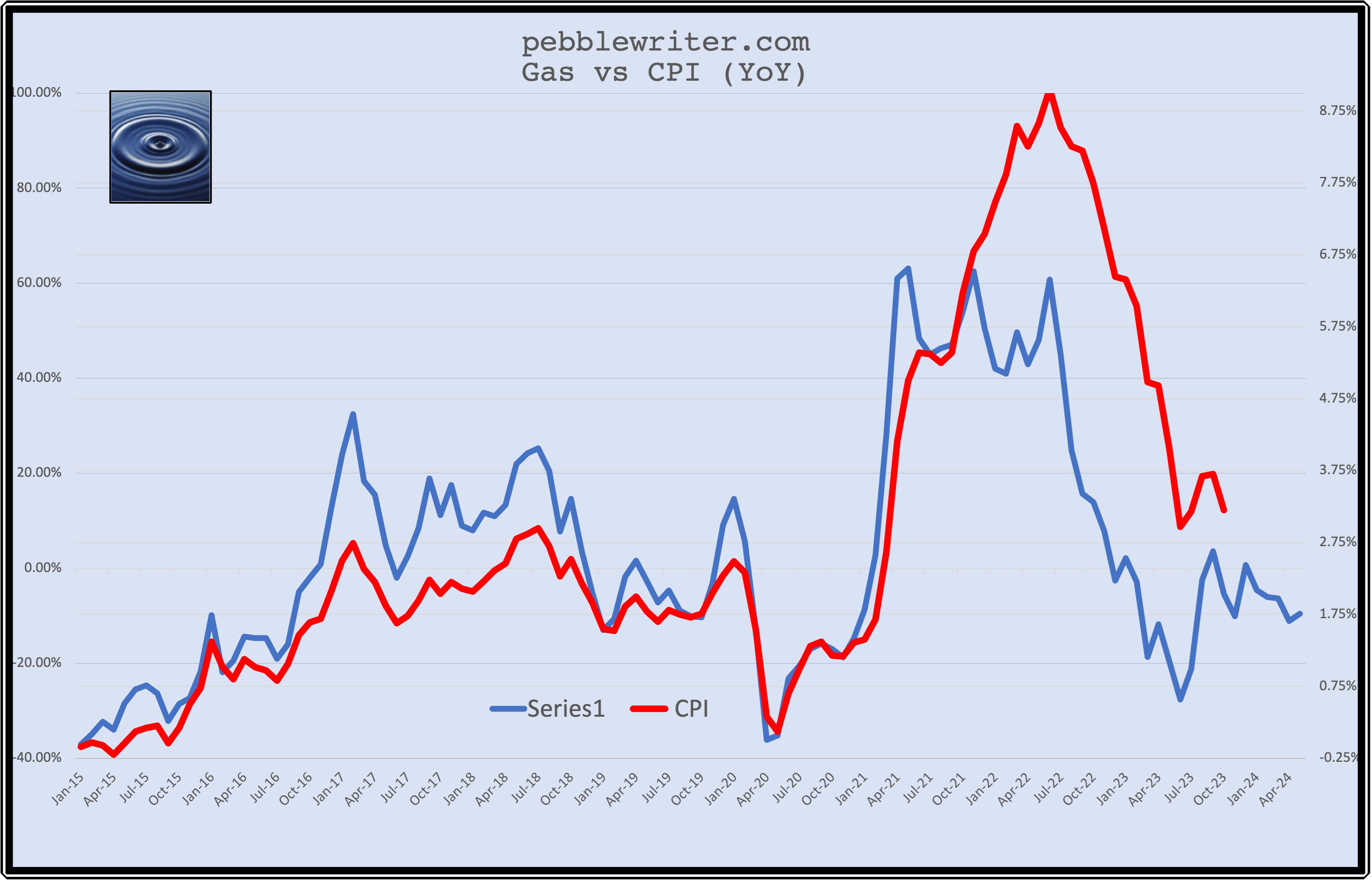

Since the YoY changes in CL and RB help CPI, and CPI drives the 10Y, it’s important to note that the recent trends in gas prices suggest continuing pressure on the 10Y.

If gas prices (the blue line) were to remain at the current level, CPI would continue to remain under pressure. The obvious divergence between gas and CPI beginning in late 2021 reflects the fact that other components of CPI began to join the inflation bandwagon. Those components remain a factor, but the spread is beginning to narrow as their YoY price deltas fall.

Does the FOMC want the 10Y to drop below 4%? I suspect they do, especially with an election coming up. While some members might not love Biden, they likely fear what life under a second Trump presidency would look like. If so, they are very likely to keep the pressure on gas prices, inflation, and interest rates until at least next November.

Does the FOMC want the 10Y to drop below 4%? I suspect they do, especially with an election coming up. While some members might not love Biden, they likely fear what life under a second Trump presidency would look like. If so, they are very likely to keep the pressure on gas prices, inflation, and interest rates until at least next November.

The tricky part, of course, is how to do so without lowering the value of the US dollar, which is at least partly reliant on a positive interest rate margin above the other dominant currencies. A lower dollar means more costly goods from overseas and higher inflation for a net importer such as the US.

This strengthens the argument for oil/gas prices going sideways or lower – unless, of course, the situation in the Middle East or in Ukraine get demonstrably worse.

Stay tuned…