I’ll admit it, I’m pissed. I don’t often hop on my digital soapbox, but after this morning’s outrageous jobs report it’s just too hard to keep it to myself.

I’ve taken the opportunity to speak to numerous business owners over the past month about their reaction to Trump’s tariff nonsense. They have uniformly been extremely negative, with many wondering if they’ll be able to stay in business when tariffs erase their already slim profit margins.

So, it’s surprise that virtually all of the hiring surveys since tariffs were announced have looked like this.

It was therefore quite shocking to see the Bureau of Labor Statistics, a division of the Department of Labor, release a jobs report that was much more positive than virtually anyone on Wall Street or in academia had forecast.

It was therefore quite shocking to see the Bureau of Labor Statistics, a division of the Department of Labor, release a jobs report that was much more positive than virtually anyone on Wall Street or in academia had forecast.

It so shocked the markets that futures soared up to new highs despite very disappointing earnings outlooks from both AAPL and AMZN after the close yesterday. Truly a WTF moment, until you think back to January 25.

It so shocked the markets that futures soared up to new highs despite very disappointing earnings outlooks from both AAPL and AMZN after the close yesterday. Truly a WTF moment, until you think back to January 25.

Trump was inaugurated on Jan 20. Five days later, in one of his first acts as president, Trump fired multiple inspectors general via Friday night emails. These are the people who are supposed to ensure that the government plays by the rules. The person who oversaw the Department of Labor and thus the BLS was this guy.

Thus, the person who might have raised the alarm about DOGE’s chainsaw firings, labor related crimes, or, say, artificially inflating the jobs numbers, was dismissed. Never mind that he had an exemplary military and civilian career, succeeding Scott Dahl who was forced out in 2020 after warning Congress about massive fraud related to the pandemic handouts during Trump’s first presidency.

Thus, the person who might have raised the alarm about DOGE’s chainsaw firings, labor related crimes, or, say, artificially inflating the jobs numbers, was dismissed. Never mind that he had an exemplary military and civilian career, succeeding Scott Dahl who was forced out in 2020 after warning Congress about massive fraud related to the pandemic handouts during Trump’s first presidency.

But, hey, all’s fair in love and politics – a world where the veracity of economic data just became more questionable than ever. The irony is that even if this data were true, which it is definitely not, it would suggest that the economy is doing just fine and that inflation is a more serious concern than employment. It’s the sort of scenario that would suggest the Fed not cut interest rates.

Naturally, Trump renewed his criticism of the Fed for not cutting rates.

Why would anyone be pissed about this? After all, a rising stock market is great for the country – or at least stockholders. But, a market that relies on falsified data is not a legitimate market at all. Such illegitimate markets seriously distort the feedback loop determining hiring and capital allocation. It also moves us that much closer to the kind of banana republic BS that the US used to oppose.

Why would anyone be pissed about this? After all, a rising stock market is great for the country – or at least stockholders. But, a market that relies on falsified data is not a legitimate market at all. Such illegitimate markets seriously distort the feedback loop determining hiring and capital allocation. It also moves us that much closer to the kind of banana republic BS that the US used to oppose.

For example, a business owner who relies on the bullish message the market is sending might be inclined to expand their workforce or operations as the economy is entering a recession – thus compounding the negative impacts to his business and increasing the risk that the recession is even worse.

A market which is easily manipulated is also, obviously, going to be more frequently manipulated – enabling those at the controls to bend it to their own purposes instead of serving the intended purpose of markets – to facilitate the exchange of financial assets on a free and fair basis.

continued for members… (more…)

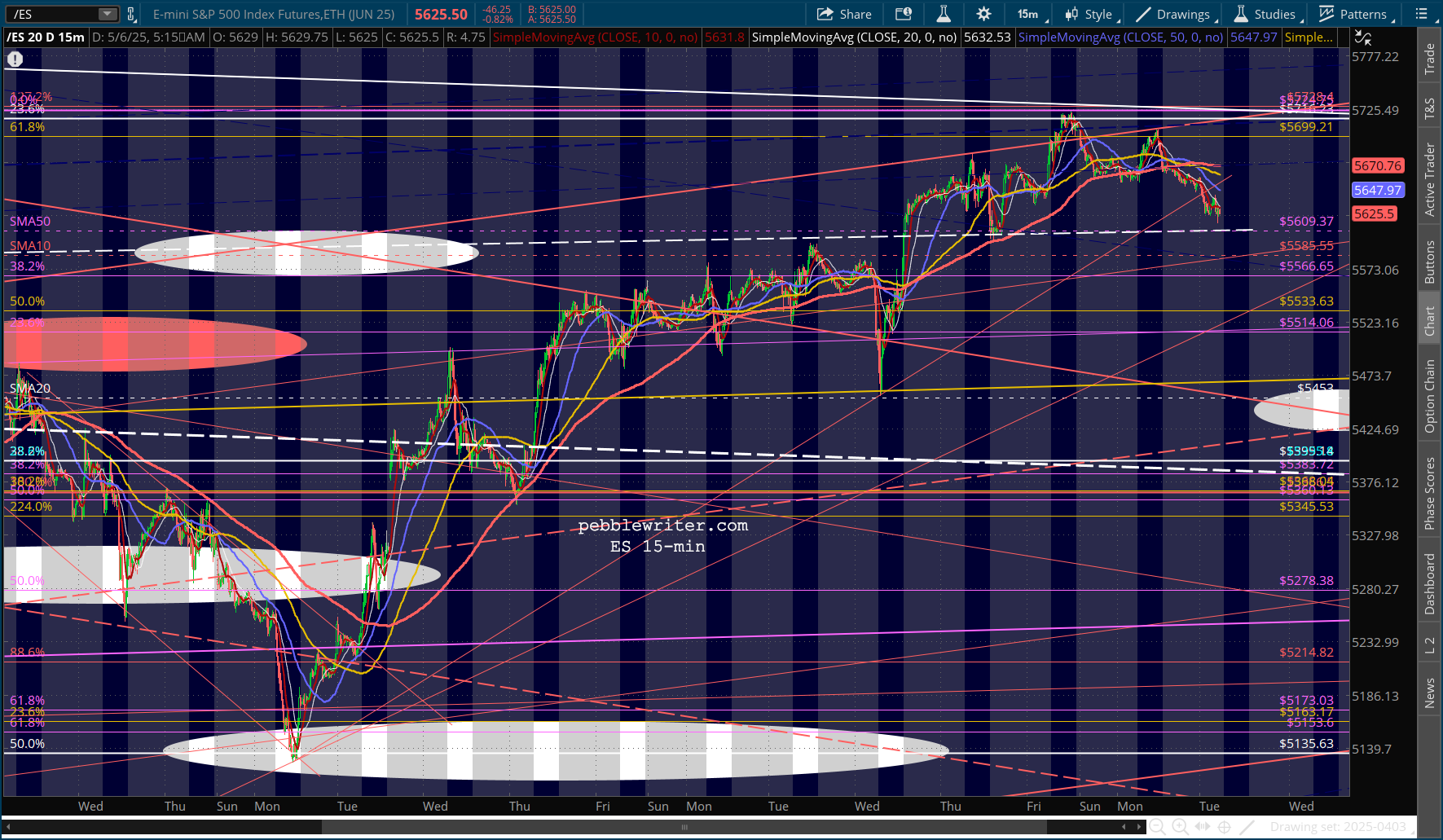

Our charts turned bearish almost a week ago, though there has been less clarity on the extent of a pullback.

Our charts turned bearish almost a week ago, though there has been less clarity on the extent of a pullback.