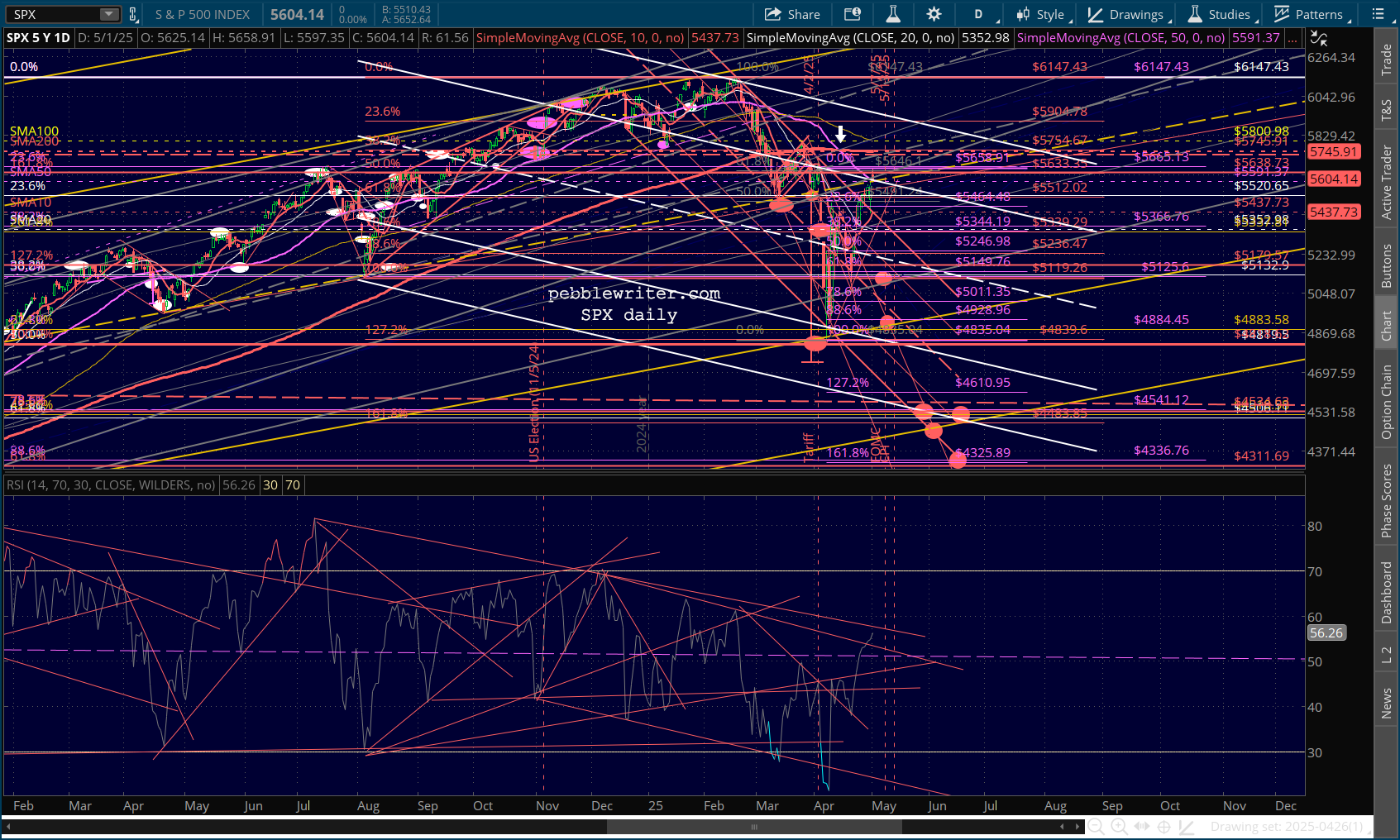

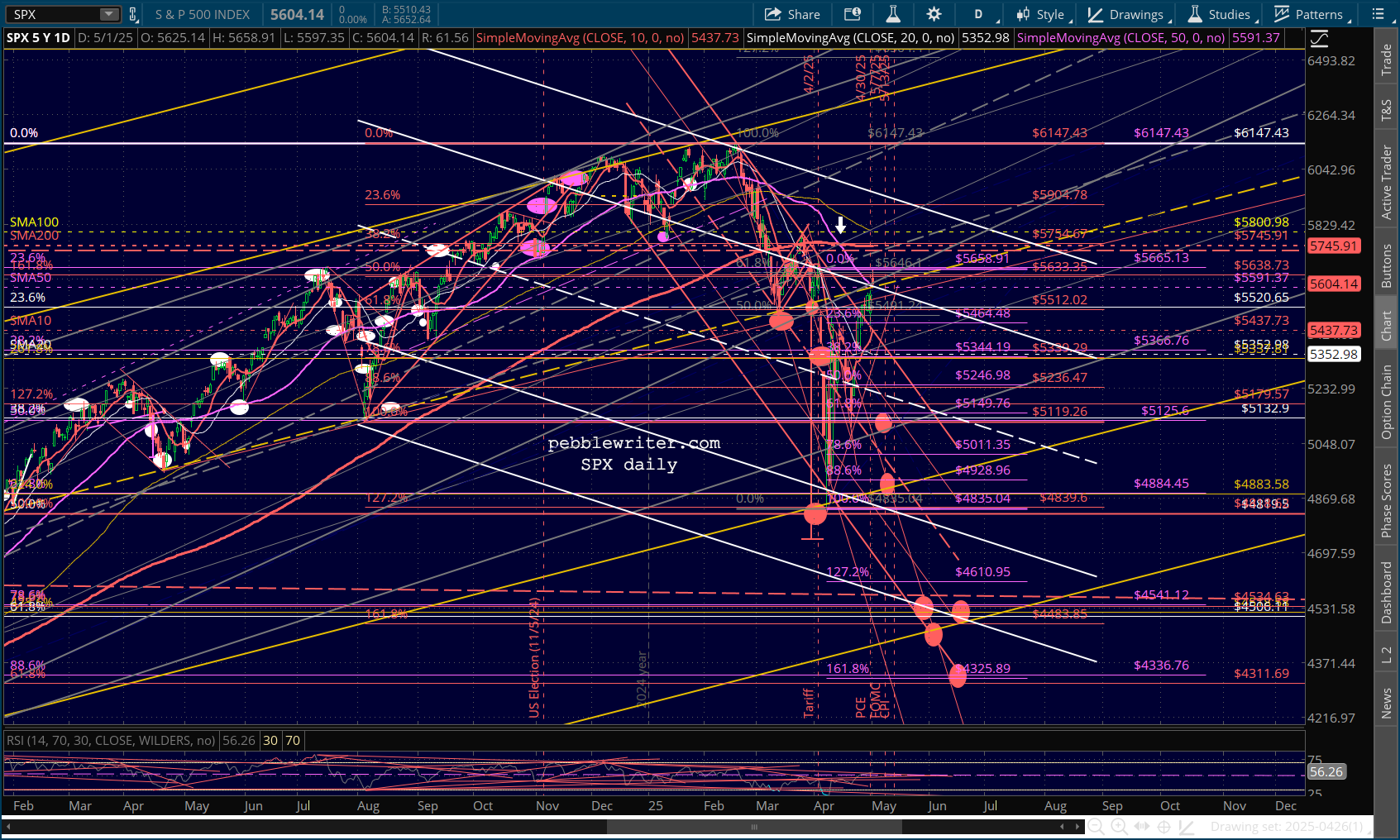

While the SPX was oversold at its April lows, there was a reason for the selloff. That reason, Trump’s disastrous trade war, is still with us. Yet, the market is back to where it was when the tariffs were announced after nine straight daily gains, the longest winning streak in more than 20 years.

Friday’s rally was especially dubious as it was based, in our opinion, on falsified employment data. We’ll get ISM services data (watch the employment component, which fell from 52.1 in Feb to 46.2 in Mar) and an FOMC meeting and rate decision this week. We’ll soon see whether or not the rally’s longevity is warranted.

continued for members…

Note that employment already did a nosedive in March.

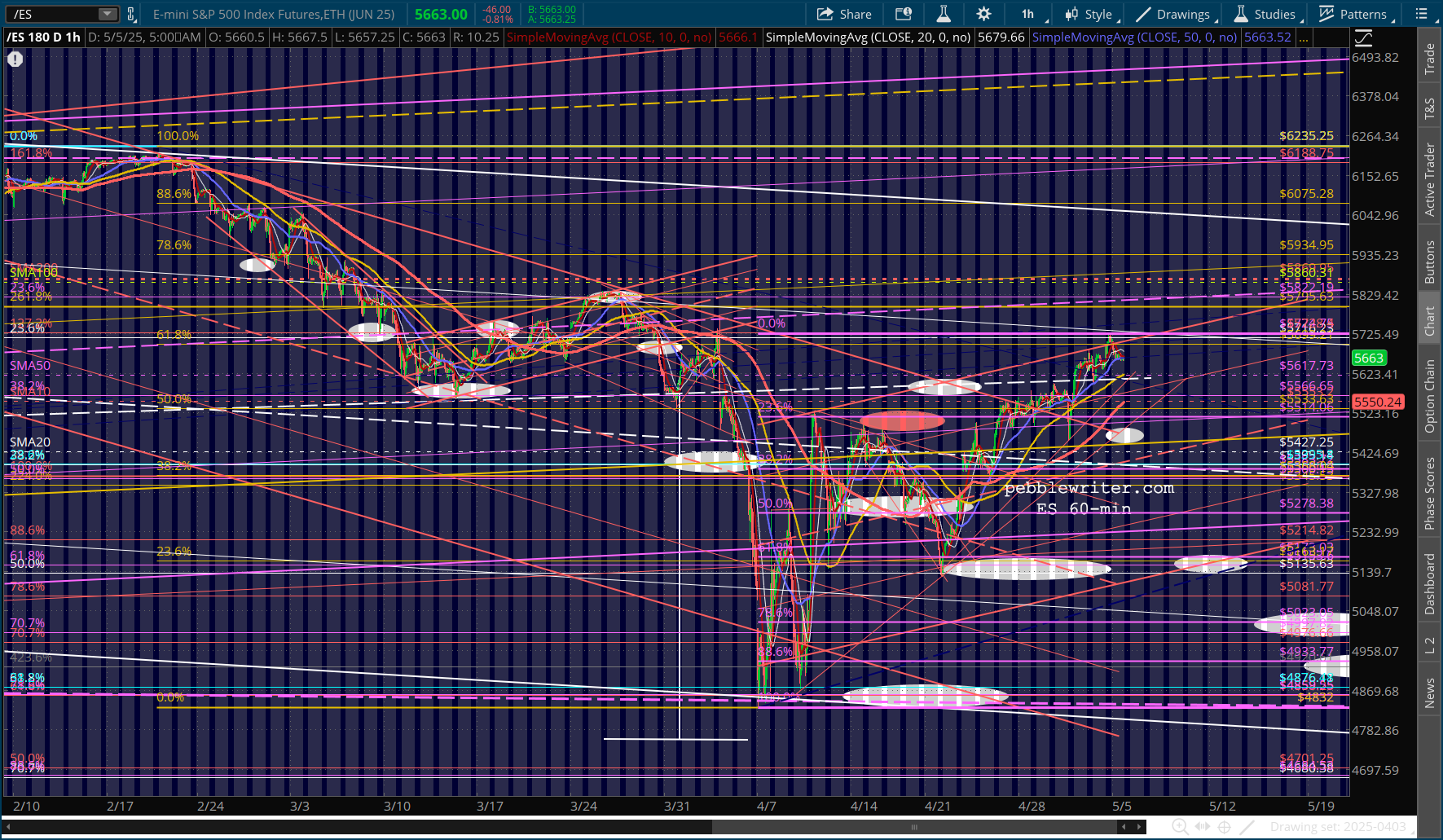

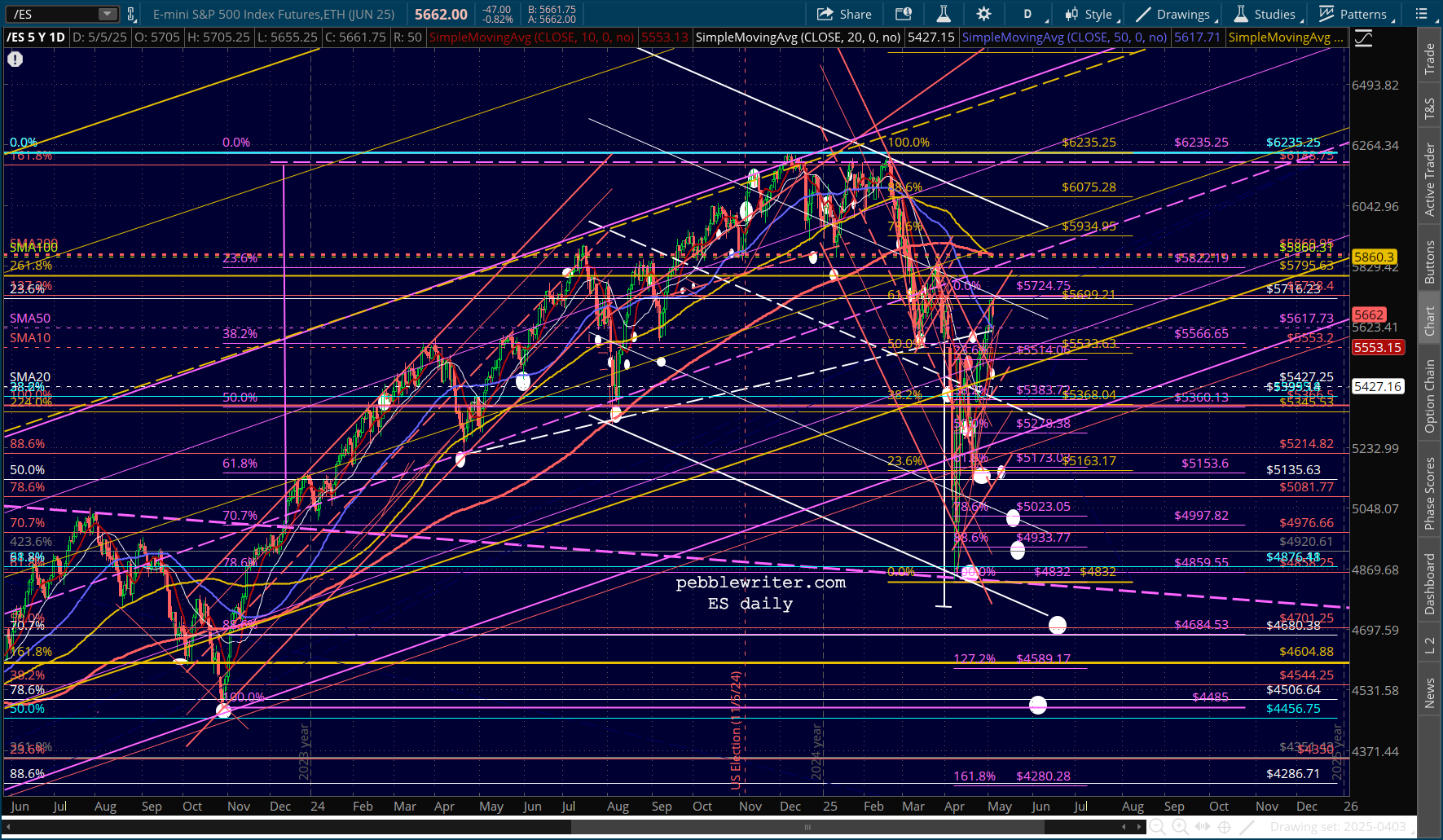

ES has clearly broken out of the falling red channel…

ES has clearly broken out of the falling red channel… …but the falling white channel still holds. If the neckline at 5600 doesn’t hold, then ES has immediate downside to the backtest at 5470ish. If it falls back into the red channel, then we’re talking at least 4933-5278.

…but the falling white channel still holds. If the neckline at 5600 doesn’t hold, then ES has immediate downside to the backtest at 5470ish. If it falls back into the red channel, then we’re talking at least 4933-5278.

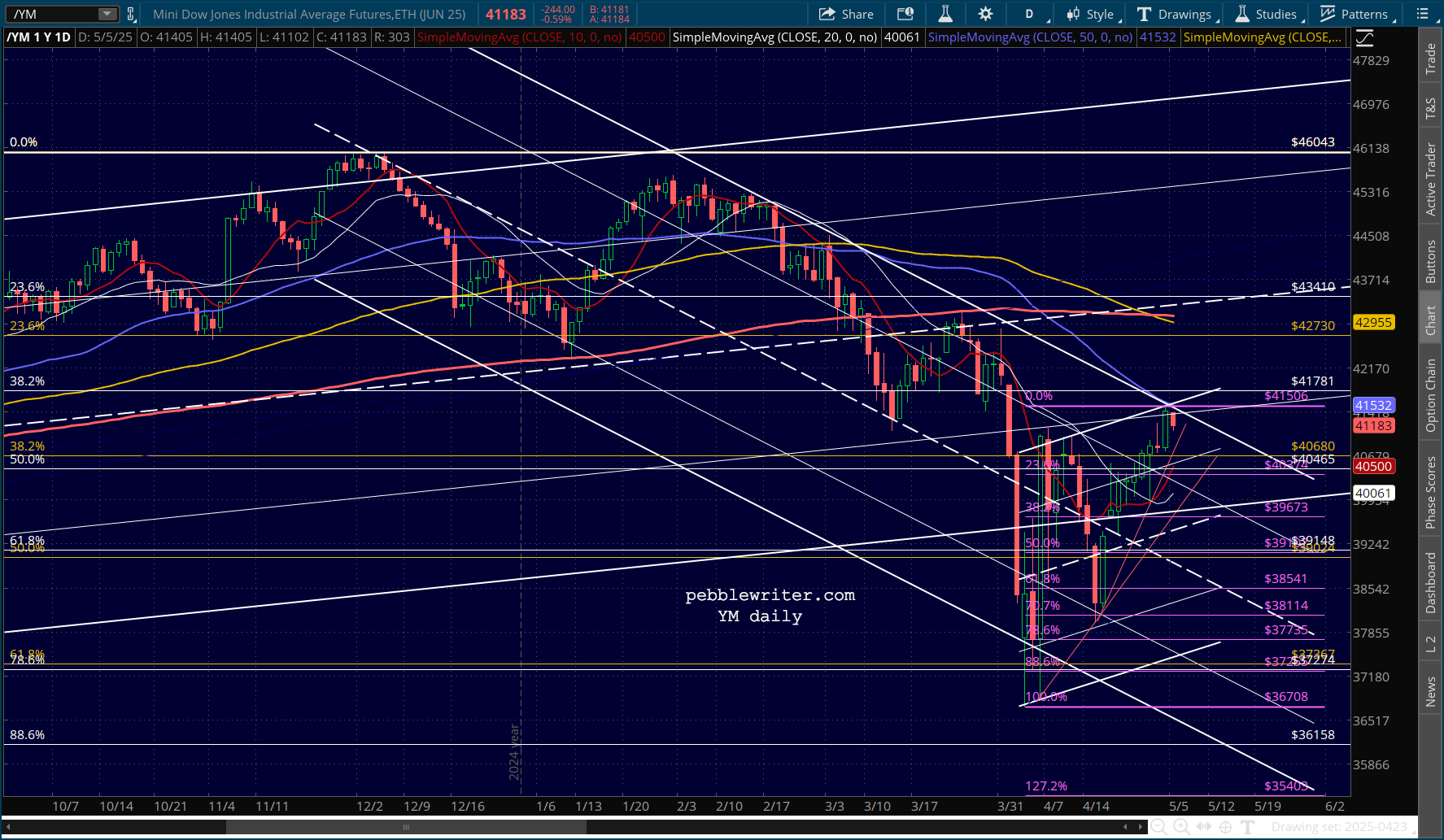

Interestingly, the Dow’s falling white channel and its SMA50 could provide a serious impediment to additional upside.

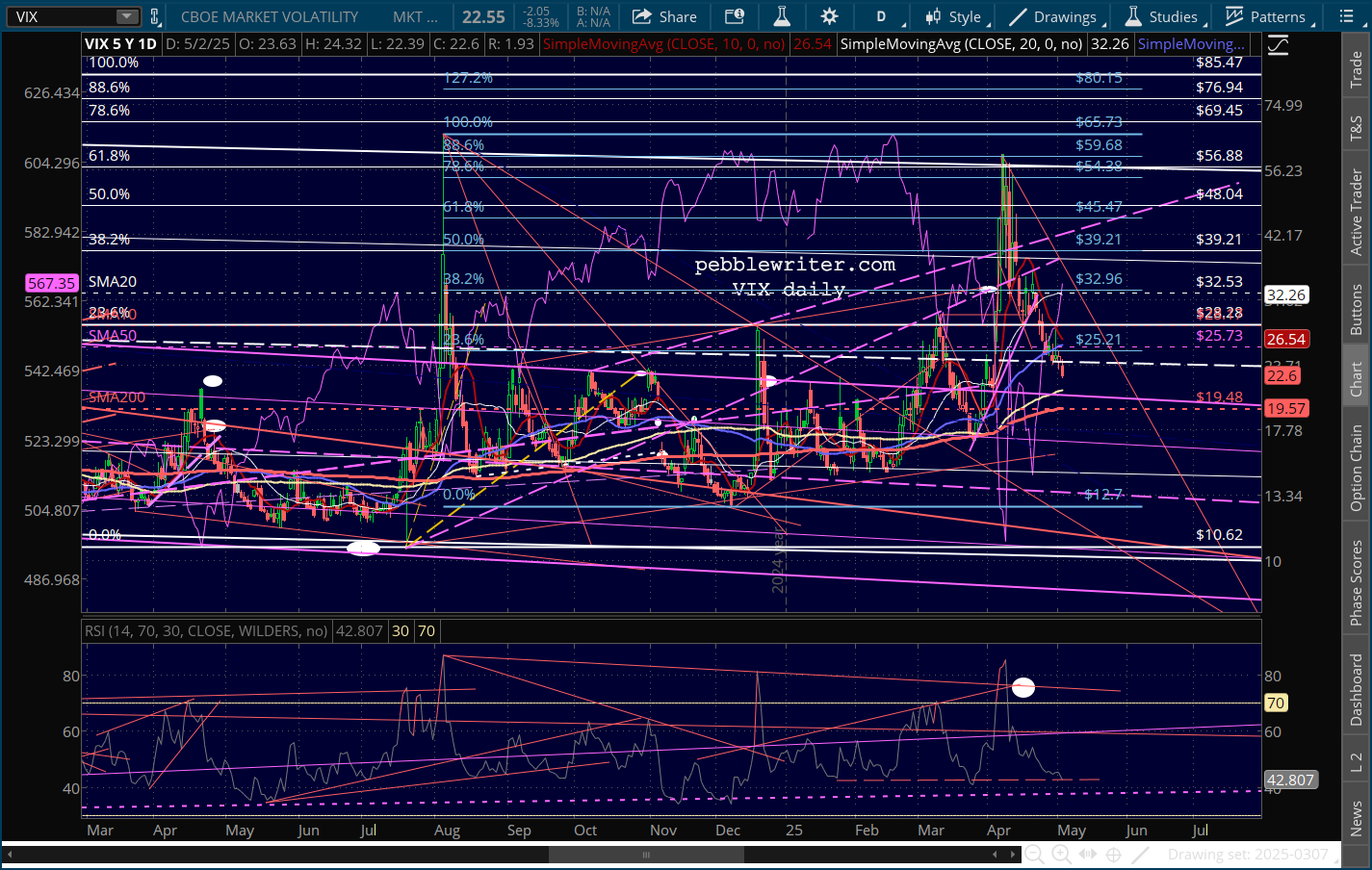

Interestingly, the Dow’s falling white channel and its SMA50 could provide a serious impediment to additional upside. And, VIX and VX both have substantial support here.

And, VIX and VX both have substantial support here.

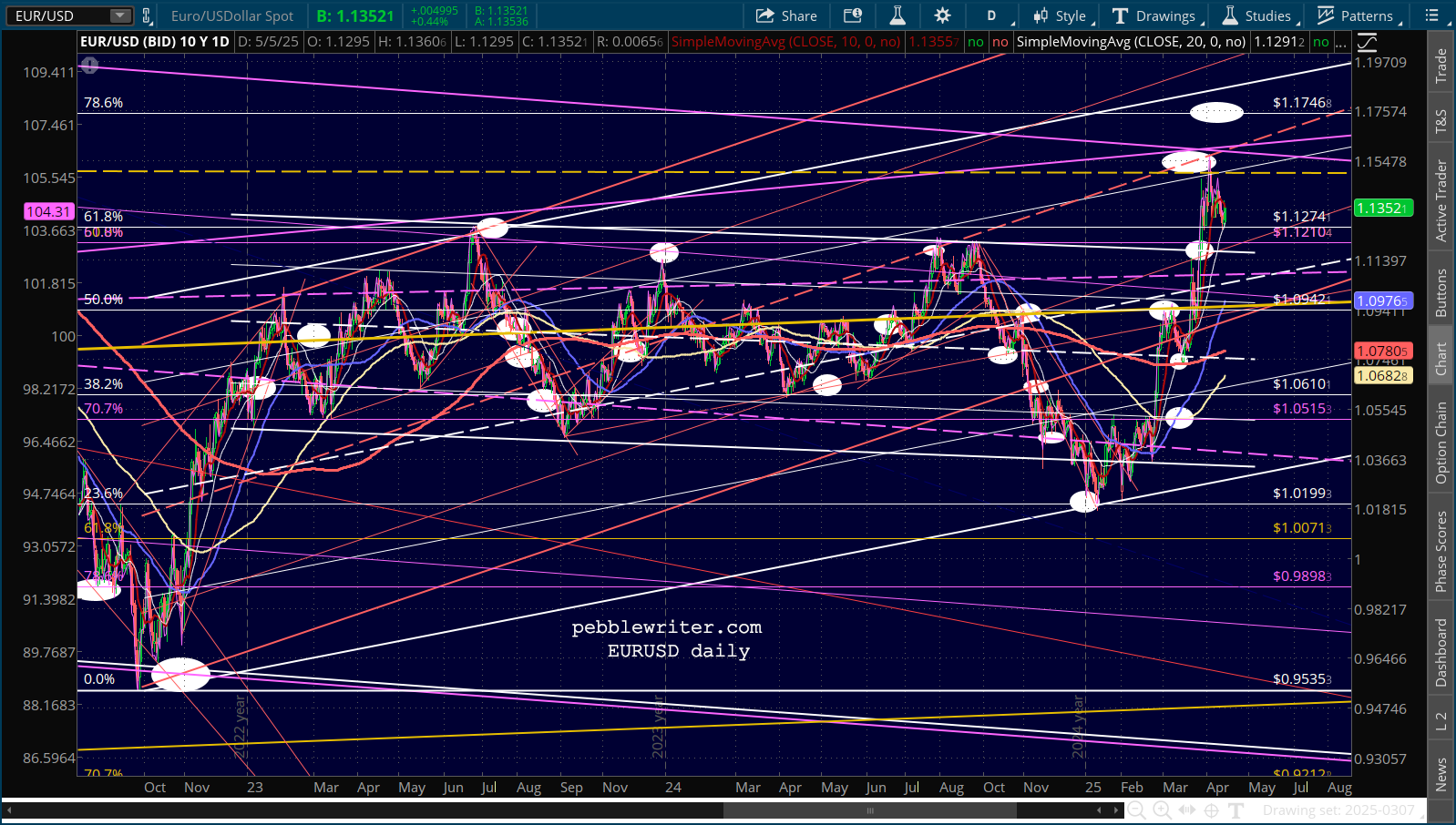

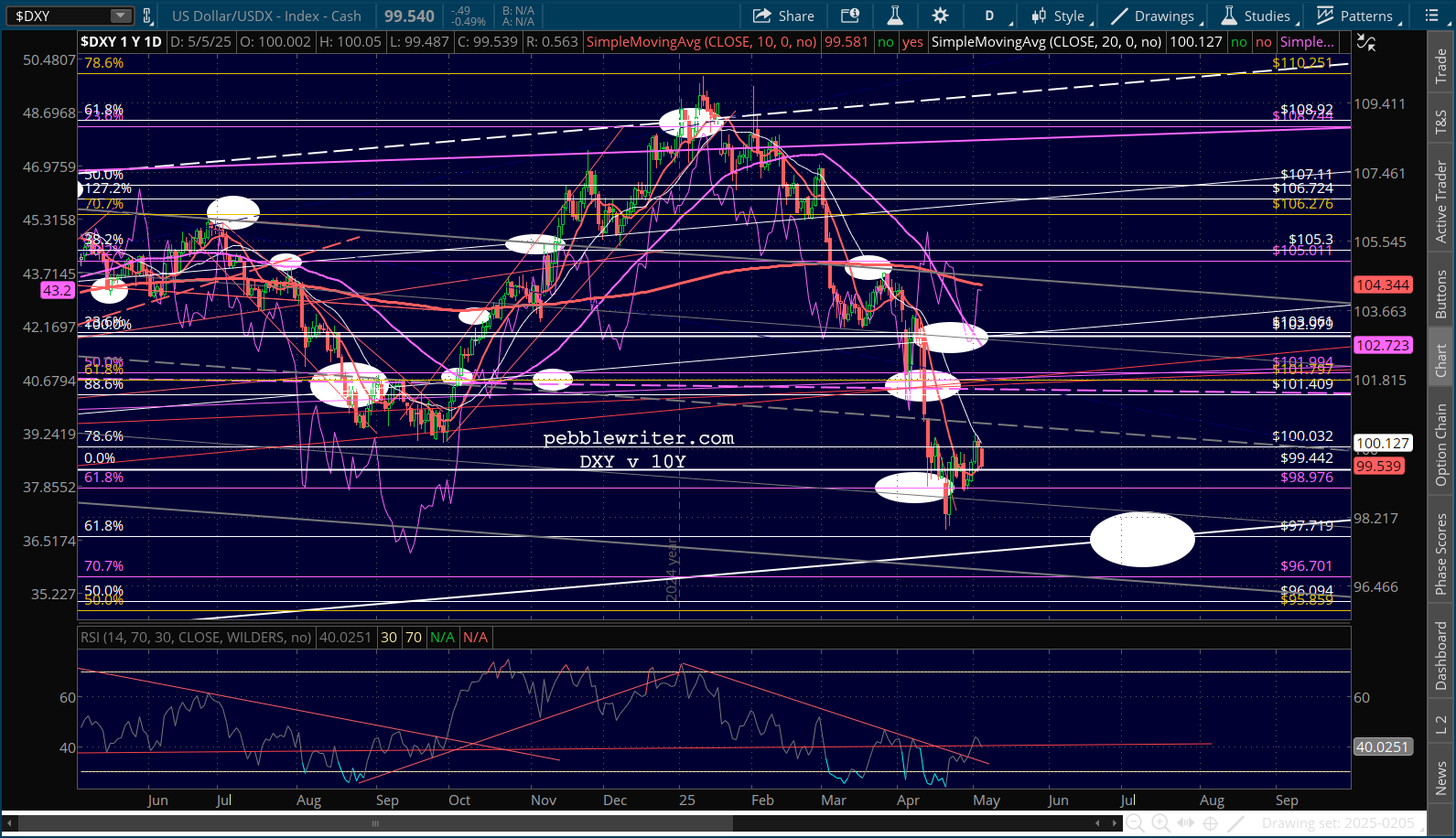

Currencies are also set to impede stocks’ gains…

Currencies are also set to impede stocks’ gains… …with the DXY faltering again.

…with the DXY faltering again.

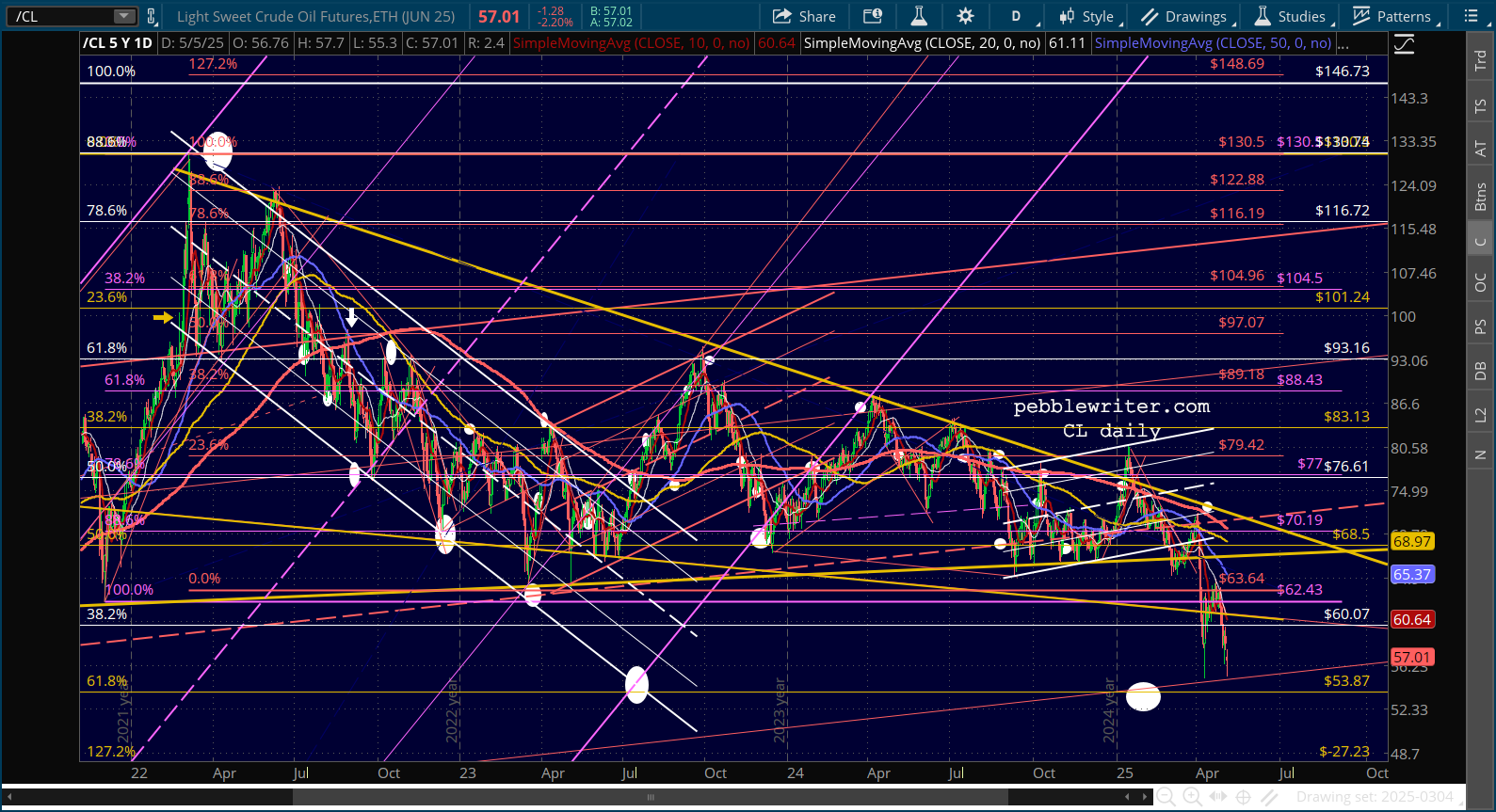

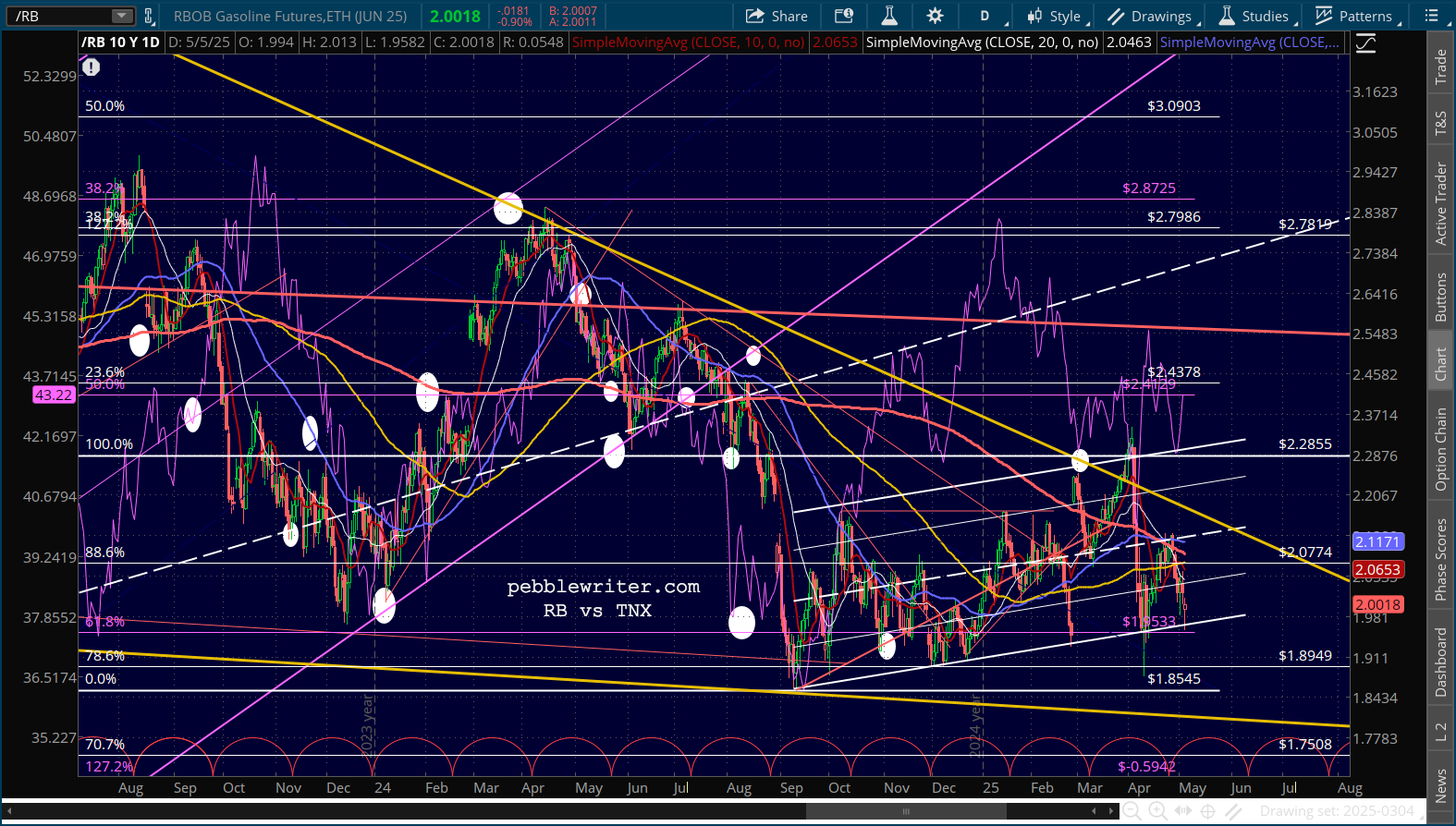

Though, this time, it’s being suppressed by the falling inflationary inputs in oil and gas.

Though, this time, it’s being suppressed by the falling inflationary inputs in oil and gas.

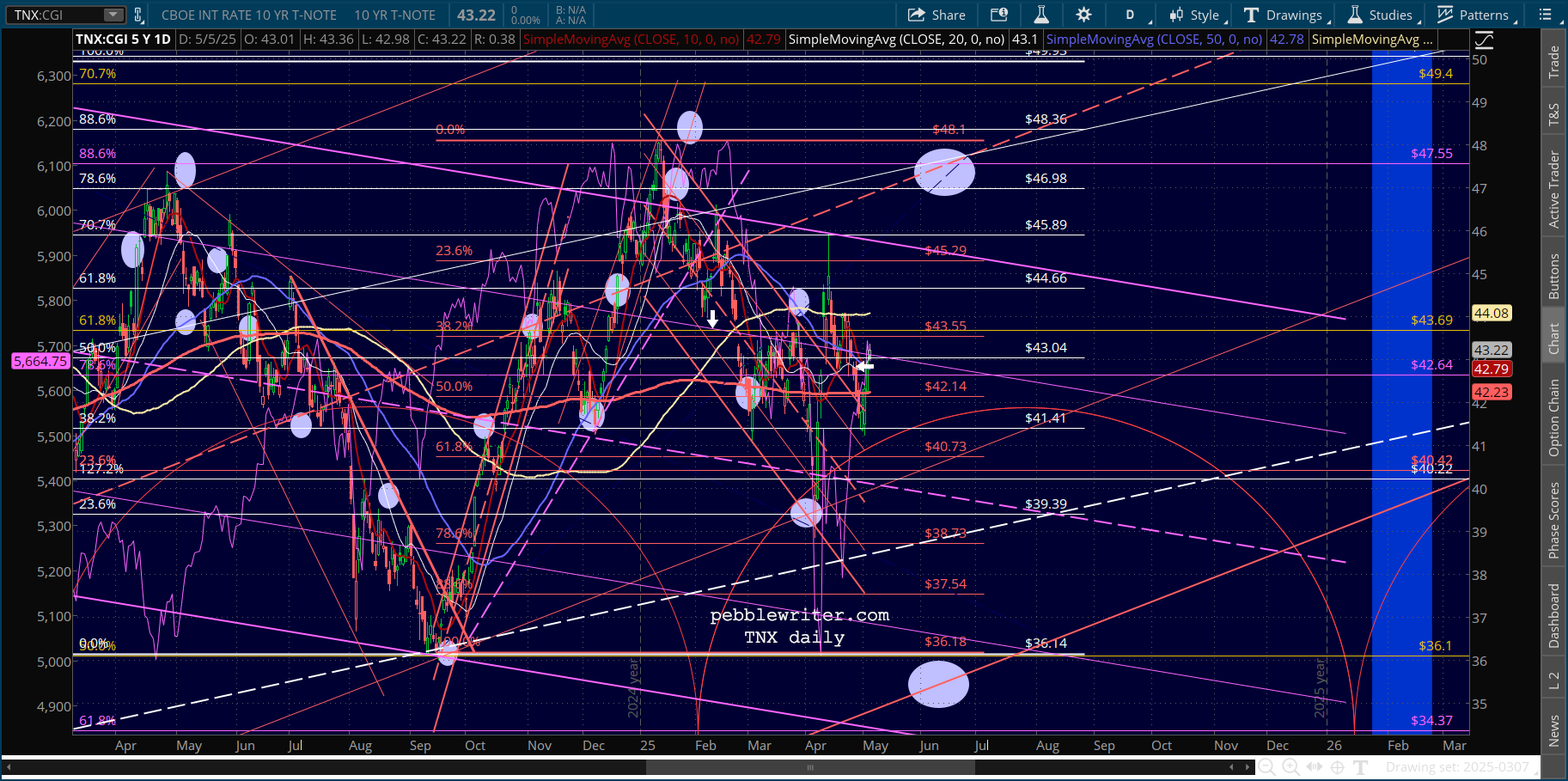

But, note that the 10Y is still rising.

But, note that the 10Y is still rising. …which is preventing the 2s10s from dropping back through the channel top. Not good for equities.

…which is preventing the 2s10s from dropping back through the channel top. Not good for equities.