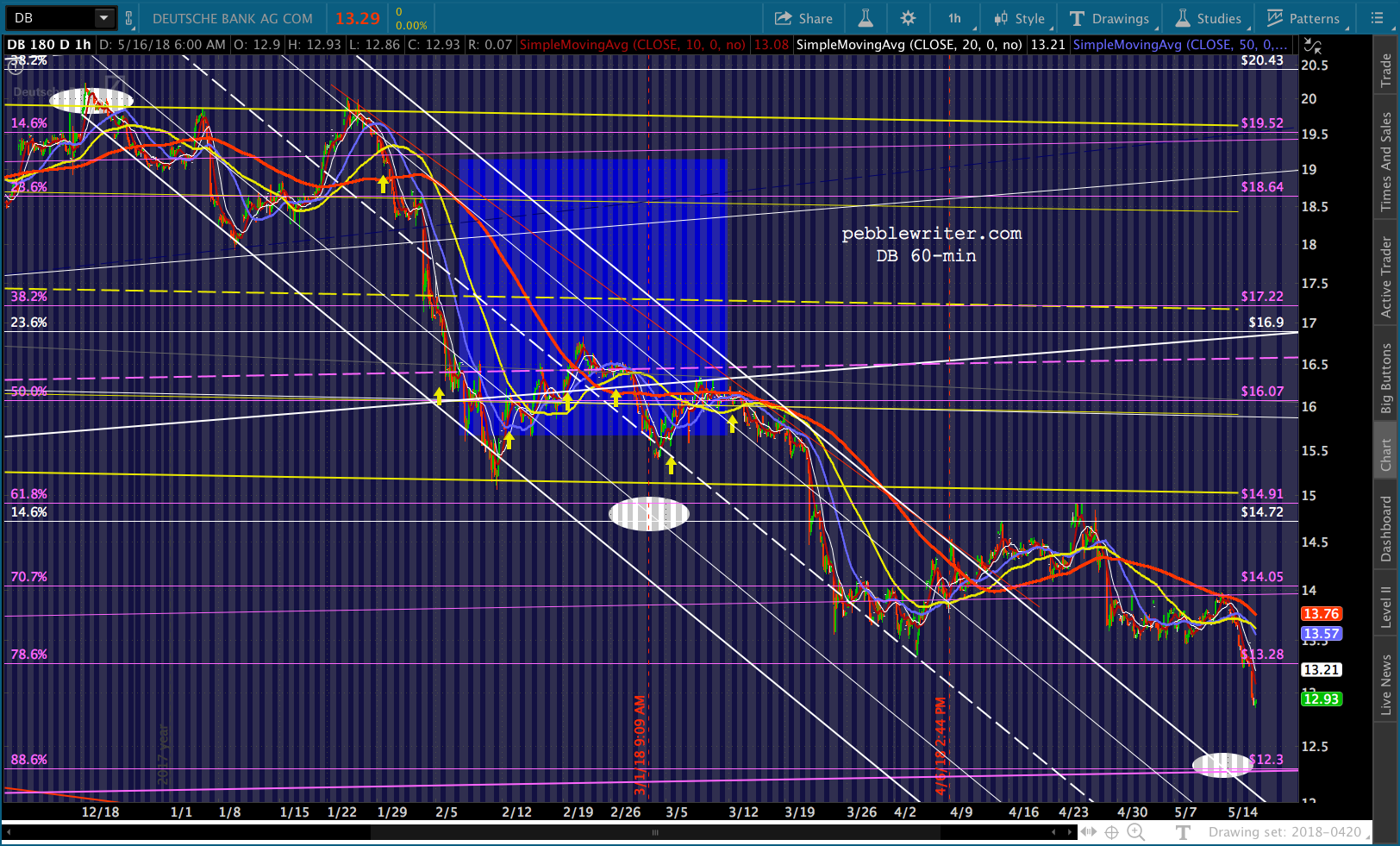

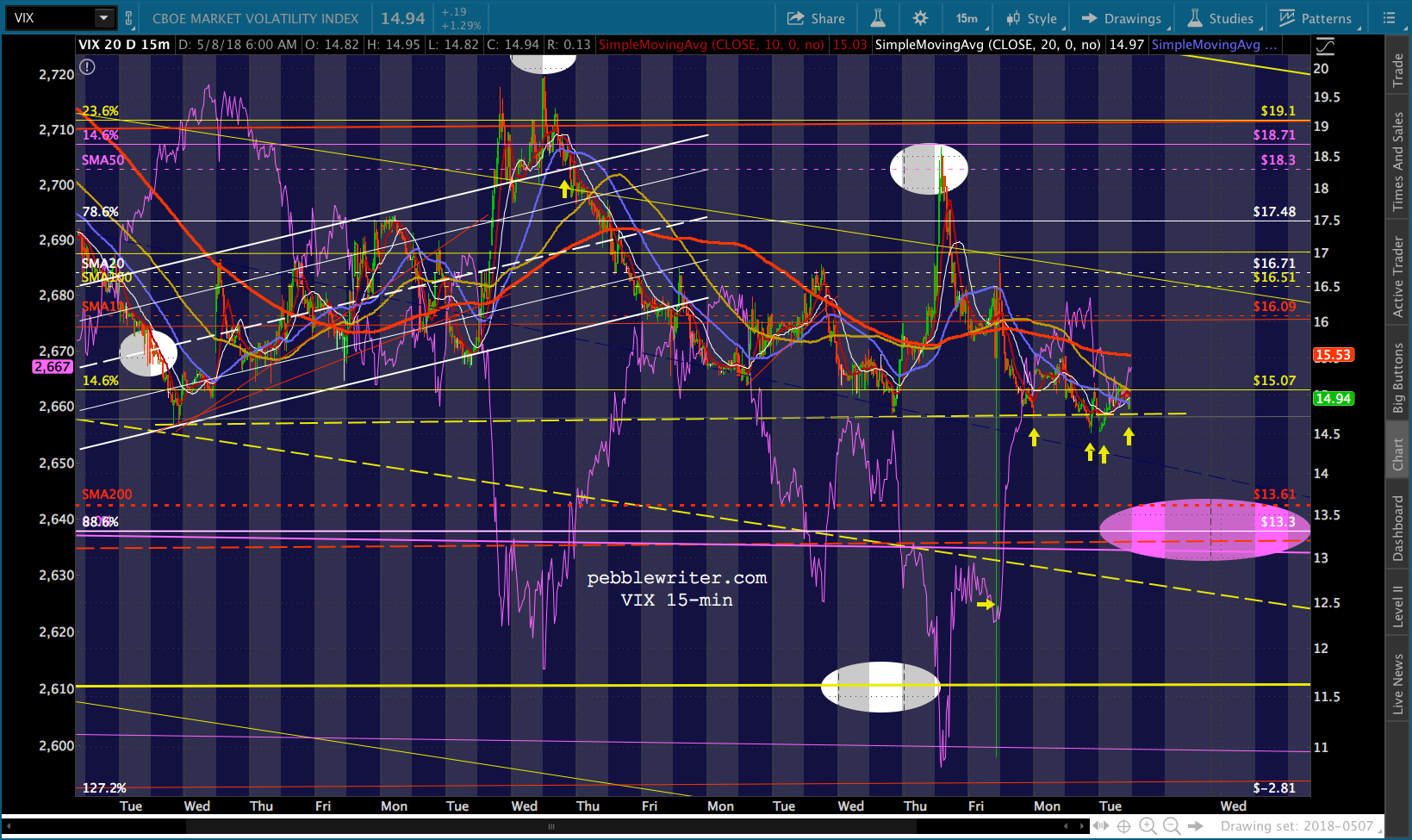

Yesterday’s late-day reversal was a minor victory for the bears — even if it came on the heels of an algo-driven melt-up which still threatens a break out. How do we know when the algos have free rein? A quick glance at VIX offered one pretty nice clue. Every dip below horizontal support (the yellow line at roughly 14.76) prompts SPX to rally; while, every rise above it prompts a sell off.

How do we know when the algos have free rein? A quick glance at VIX offered one pretty nice clue. Every dip below horizontal support (the yellow line at roughly 14.76) prompts SPX to rally; while, every rise above it prompts a sell off.

And, like the past three days, we saw a rally overnight that could facilitate another intraday decline. In the past 2 hours, its almost imperceptible dip (except to the machines) was enough to erase almost 10 points off ES’ overnight decline. But, the real story today is oil — meaning what Trump decides about the Iran nuclear deal. Now, to talk about Iran, we really have to talk about Iraq. It wasn’t that long ago that our leaders decided Saddam Hussein was such a threat to our existence that we sacrificed $2.4 trillion, 4,424 American lives, and perhaps over a million Iraqi lives.

But, the real story today is oil — meaning what Trump decides about the Iran nuclear deal. Now, to talk about Iran, we really have to talk about Iraq. It wasn’t that long ago that our leaders decided Saddam Hussein was such a threat to our existence that we sacrificed $2.4 trillion, 4,424 American lives, and perhaps over a million Iraqi lives.

Volumes have been written on the other costs: destabilization in the Middle East, loss of global unity reached in the wake of 9/11, the rise in terrorism, etc.

Most now accept that the Iraq War was about oil and, by extension, regime change — a conclusion that’s difficult to fault given that no weapons of mass destruction or evidence of collusion with al-Qaeda were ever found. From a 2013 CNN article:

“Of course it’s about oil; we can’t really deny that,” said Gen. John Abizaid, former head of U.S. Central Command and Military Operations in Iraq, in 2007. Former Federal Reserve Chairman Alan Greenspan agreed, writing in his memoir, “I am saddened that it is politically inconvenient to acknowledge what everyone knows: the Iraq war is largely about oil.” Then-Sen. and now Defense Secretary Chuck Hagel said the same in 2007: “People say we’re not fighting for oil. Of course we are.”

It’s this thread I’d like to explore a bit. I think our experiences in Iraq are relevant to the current situation in Iran. This became more clear on Saturday, when newly minted Trump mouthpiece Rudy Giuliani declared “we have a president who is as committed to regime change [in Iran] as we are.” SecState Pompeo and National Security Adviser Bolton have made similar comments.

I’ve heard it said that taking control of Iraq’s oil fields somehow benefited Americans by reducing the price of oil — a statement which is pure fantasy. Oil prices increased rapidly as the war escalated, and fell sharply only after negotiation of the Status of Forces Agreement (SOFA) which effectively spelled the end of US control. If that’s the case, then what did the US gain by invading Iraq, taking control of its oil fields and negotiating sweetheart deals? The real benefactors of the Iraq War were military contractors and oil companies. Halliburton’s performance was fairly typical.

If that’s the case, then what did the US gain by invading Iraq, taking control of its oil fields and negotiating sweetheart deals? The real benefactors of the Iraq War were military contractors and oil companies. Halliburton’s performance was fairly typical. Aside from the obvious benefits to the stock market, where did this leave the US economy? CPI averaged 1.59% in 2002, as the US was trying to recover from the Tech Bust. In 2003, when the US invaded Iraq, it averaged 2.27%.

Aside from the obvious benefits to the stock market, where did this leave the US economy? CPI averaged 1.59% in 2002, as the US was trying to recover from the Tech Bust. In 2003, when the US invaded Iraq, it averaged 2.27%.

CPI peaked at 3.62% in 2004, 4.69% in 2005, 4.32% in 2006, 4.31% in 2007, and 5.60% in July 2008. The 2008 figure is all the more impressive given that the Great Financial Crisis was taking hold. It dropped to 0.09% by December.

Of course, inflation is just part of the story. With higher inflation, we get higher interest rates. And, because the war cost so much, those interest rates were being paid on an ever growing pile of debt. Annual interest expense exploded from $318 billion in 2003 to $451 billion in 2008. That kind of expense was unsustainable. Interest rates had to come down, which meant inflation had to come down — which, in turn, meant that oil and gas prices had to come down. Of course, that’s exactly what happened.

That kind of expense was unsustainable. Interest rates had to come down, which meant inflation had to come down — which, in turn, meant that oil and gas prices had to come down. Of course, that’s exactly what happened.

By the time CPI hit 0.09% in December 2008, the 10-year — which had peaked at 5.26% in June 2007 — had fallen to 2.13%. It was possible because oil fell from $147/barrel in July 2008 to $33/barrel by Jan 2009. Gas prices fell from $4.00 to $1.67 per gallon between July and December 2008.

Although we haven’t started a new major war yet, it’s important to recognize that a military confrontation in Iran would be much greater in scale than the Iraq War. With Trump’s top advisors advocating regime change, the chances of a shooting war don’t seem nearly as remote as when candidate Trump declared he would “stop racing to topple foreign regimes.”

Although we haven’t started a new major war yet, it’s important to recognize that a military confrontation in Iran would be much greater in scale than the Iraq War. With Trump’s top advisors advocating regime change, the chances of a shooting war don’t seem nearly as remote as when candidate Trump declared he would “stop racing to topple foreign regimes.”

The 10-year is currently hovering just shy of 3%, and CPI has pushed well above 2%. Annual interest expense is expected to reach about $500 billion in 2018. If oil and gas prices don’t come down quickly, the 10-year will soon top 3%.

Bottom line: we can’t afford current oil and gas prices, let alone those which an escalation in the Middle East would produce. Something for Trump to think about as he scrambles for a distraction from the domestic storms in which he’s embroiled.

For more on the current status of oil and gas prices, and the effect they’re having on inflation, interest rates and equities, see: Oil & Gas, Inflation and Interest Rates – A Delicate Balance or Goal Seeking?

Now, on to today’s charts.

continued for members… (more…)

We asked rhetorically, yesterday, whether “

We asked rhetorically, yesterday, whether “ USDJPY, meanwhile, is taking the opportunity to rally on higher interest rates and is nearing our next upside target. And, RBOB and CL hit new highs. Are the algos really so easily fooled? Have carbon-based investors — who have certainly done the math on the economic damage higher rates and rising inflation are already doing — become irrelevant?

USDJPY, meanwhile, is taking the opportunity to rally on higher interest rates and is nearing our next upside target. And, RBOB and CL hit new highs. Are the algos really so easily fooled? Have carbon-based investors — who have certainly done the math on the economic damage higher rates and rising inflation are already doing — become irrelevant?