While a higher dollar might help mitigate inflation, higher interest rates are starting to bite. Both mortgage refinancing and housing starts and permits tumbled in April.

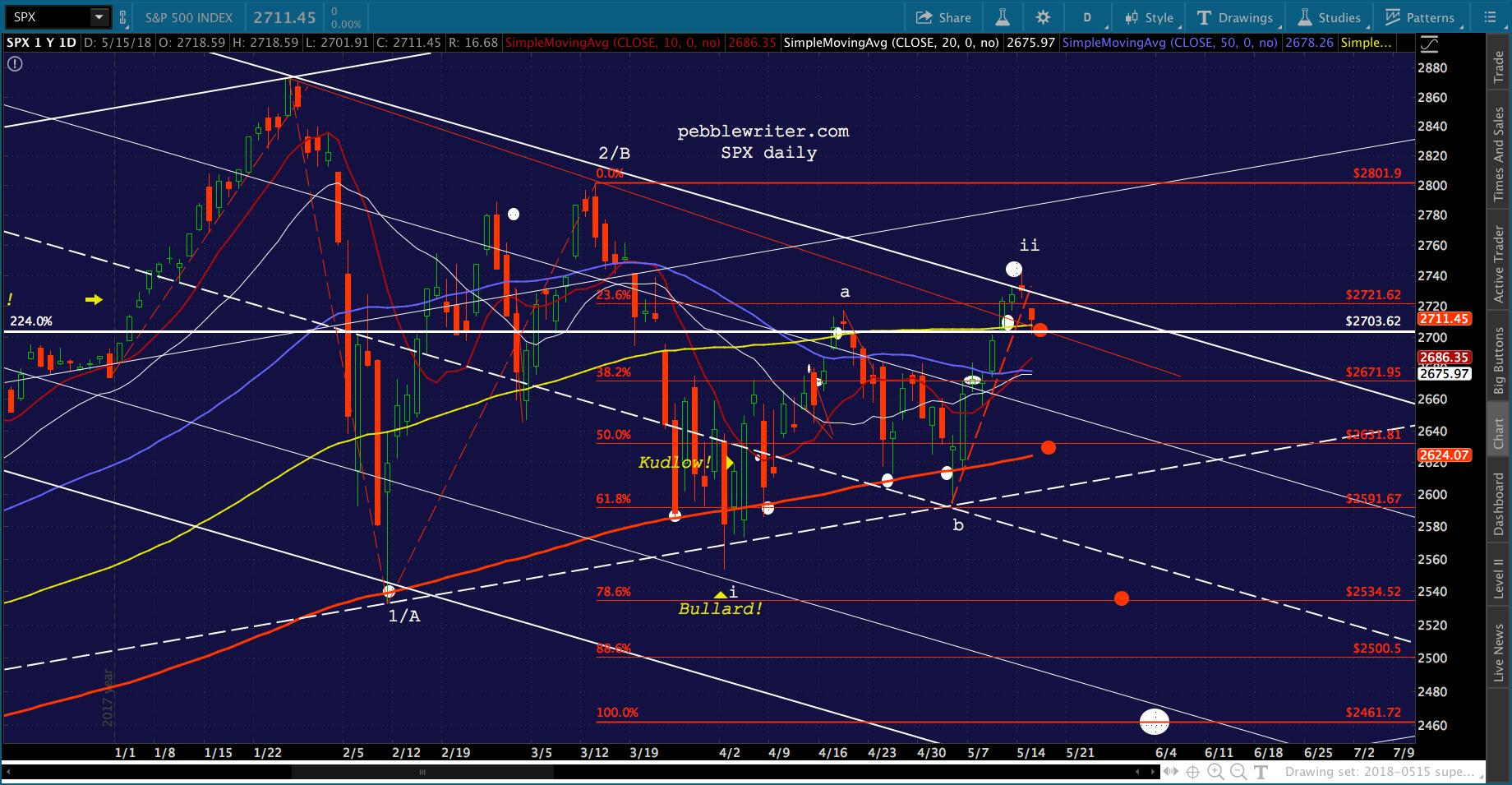

Futures tumbled about 5 points on the news. But, even that was a problem, as SPX is perched precariously atop the critical support of its 2.24 Fib extension at 2703.62 (not exactly a random walk…)

Futures tumbled about 5 points on the news. But, even that was a problem, as SPX is perched precariously atop the critical support of its 2.24 Fib extension at 2703.62 (not exactly a random walk…) It should come as no surprise to readers that VIX has already begun its nosedive.

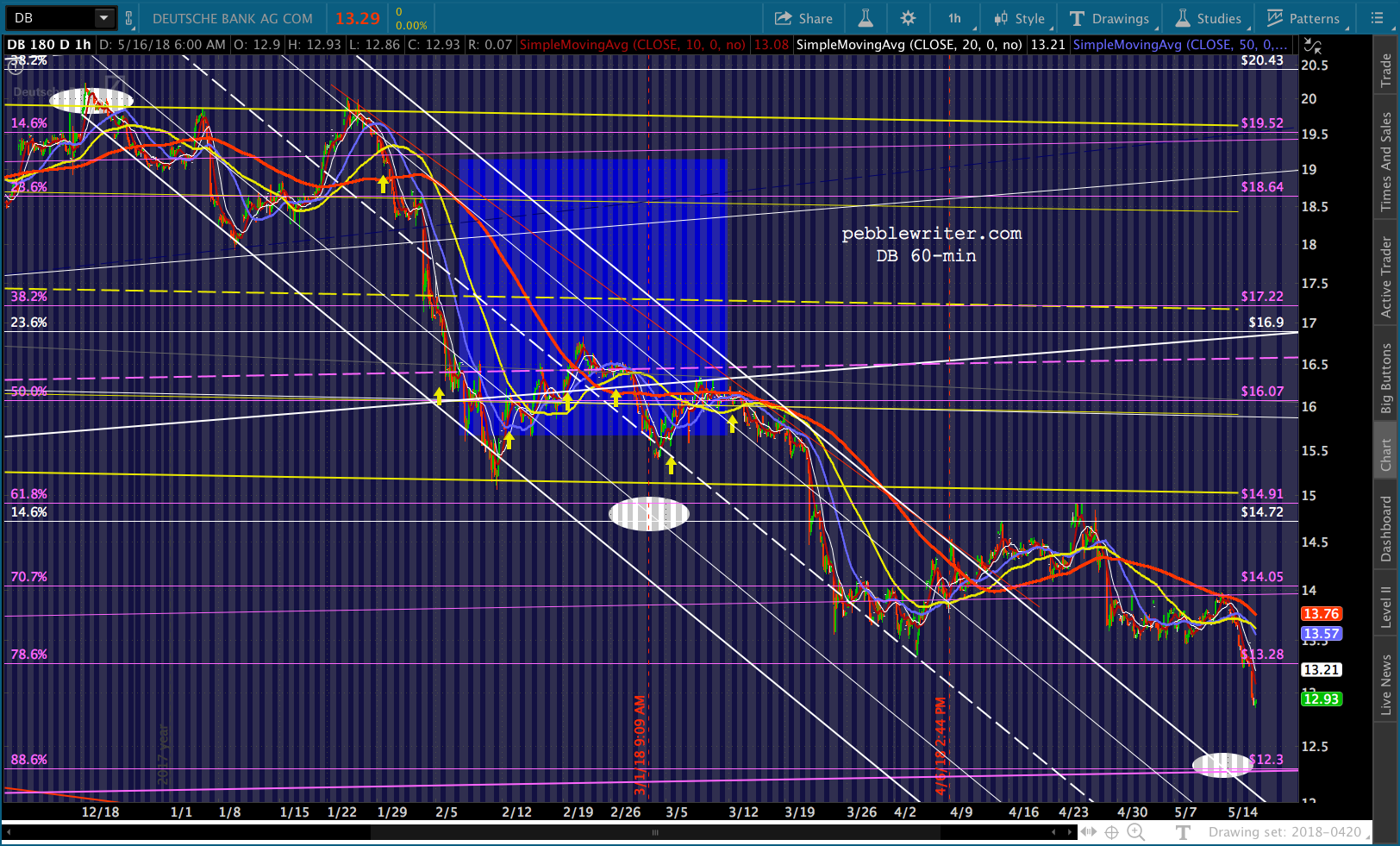

It should come as no surprise to readers that VIX has already begun its nosedive. Meanwhile, Deutsche Bank — the third largest bank in the eurozone with $1.8 trillion in assets and $40 trillion in derivatives — continues its meltdown, closing in on our target from Feb 7 [see: What is Deutsche Bank Trying to Tell Us?]

Meanwhile, Deutsche Bank — the third largest bank in the eurozone with $1.8 trillion in assets and $40 trillion in derivatives — continues its meltdown, closing in on our target from Feb 7 [see: What is Deutsche Bank Trying to Tell Us?]  But, hey, VIX is off 8%! Everything must be awesome!

But, hey, VIX is off 8%! Everything must be awesome!

Will investors algos even care about the stagnation which, abetted by inflation-driven higher interest rates, has ensnared the economy in its razor sharp talons? Or, will a tumbling “risk indicator” and copious share buybacks be enough to ward off a correction?

continued for members…

SPX is in limbo until VIX declares its intentions regarding rejoining the purple channel.

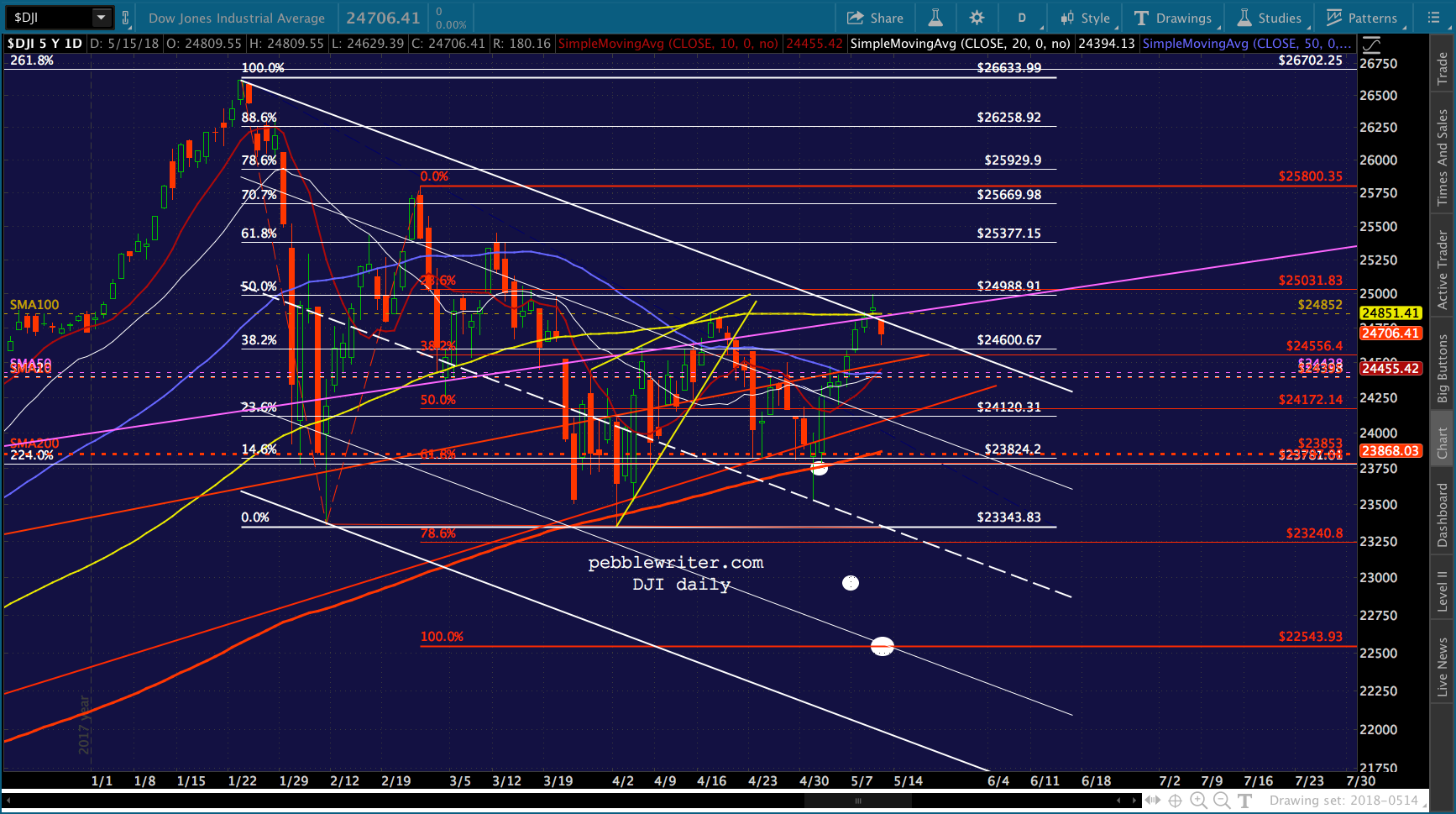

Ditto for DJIA.

Ditto for DJIA.

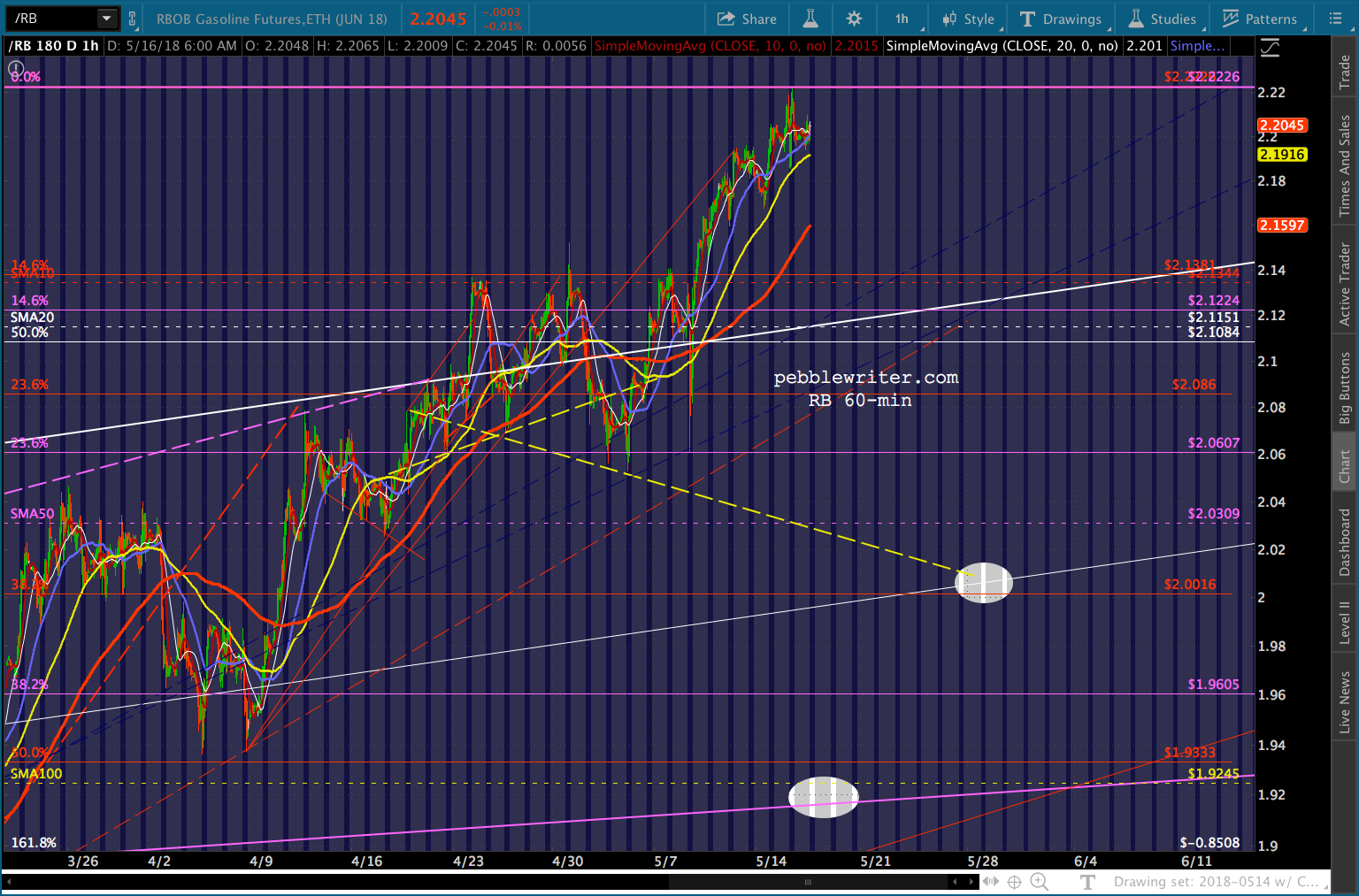

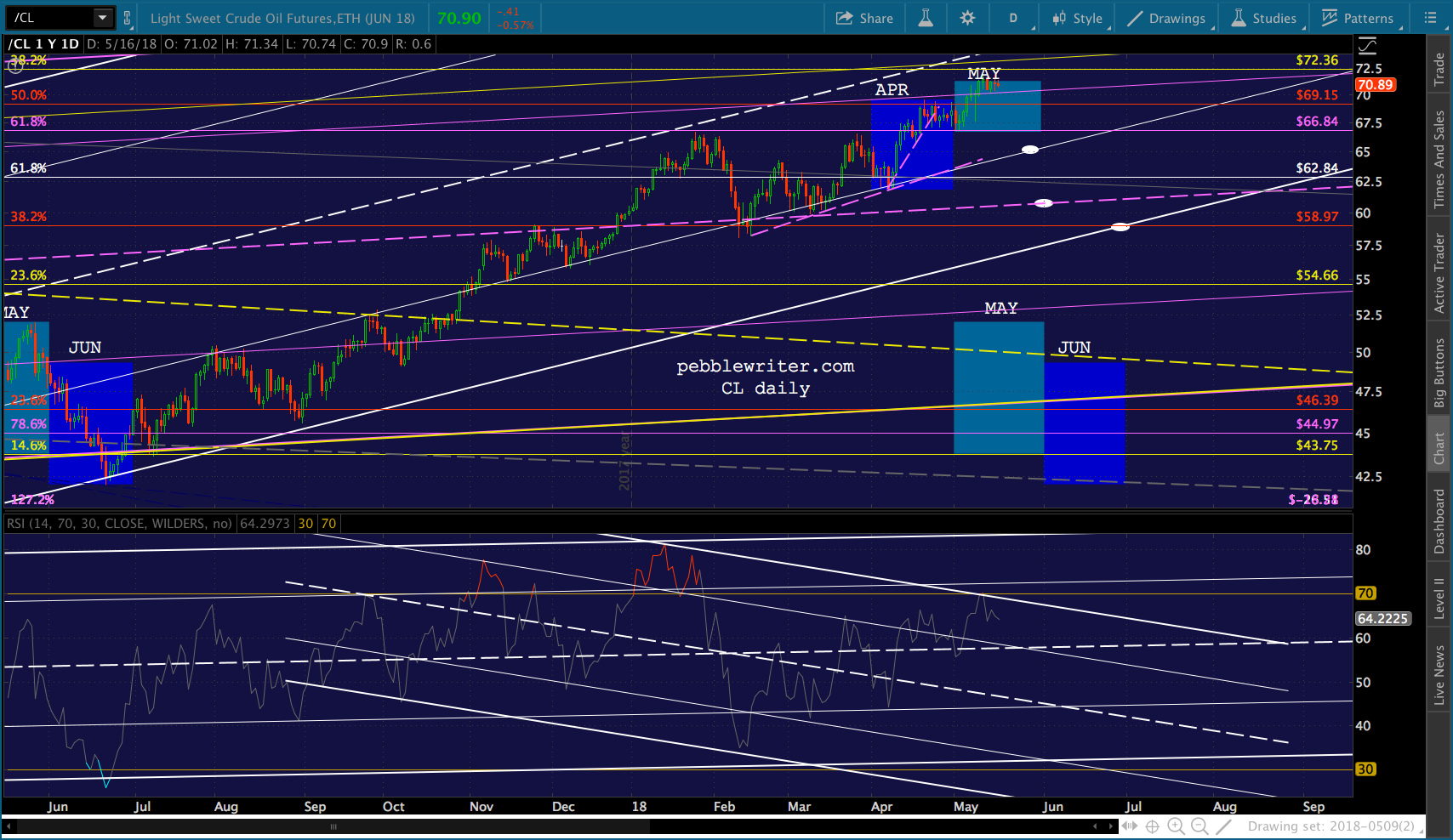

CL remains way higher than its YoY comps — meaning May Inflation will be higher and June’s higher still. Translation – higher rates unless oil/gas come back down. From a fundamental standpoint, the IEA says demand is falling off and API reported a crude inventory build.

CL remains way higher than its YoY comps — meaning May Inflation will be higher and June’s higher still. Translation – higher rates unless oil/gas come back down. From a fundamental standpoint, the IEA says demand is falling off and API reported a crude inventory build.