Wildfire is a common occurrence in many parts of California. But, unlike earthquakes, mudslides and bad plastic surgery, The Powers That Be seem to feel they can prevent it.

Wildfire is a common occurrence in many parts of California. But, unlike earthquakes, mudslides and bad plastic surgery, The Powers That Be seem to feel they can prevent it.

If you live in fire country, you’re awfully glad that Cal Fire is quick to respond when things go south. In financial terms, it’s like having a protective put.

Long before Man arrived on the scene, however, Mother Nature had her own way of responding to periodic wildfires: let ’em burn until the available fuel was consumed and/or a timely downpour came along. And, it wasn’t necessarily a bad thing.

The negative effects of wildfires are often outweighed by ecological benefits such as the removal of non-native plants and insects and the release of nutrients from older vegetation into the soil to support new growth.

And, there’s a bonus. If much of the dry, combustible underbrush is consumed by periodic smaller fires, the next wildfire won’t be anywhere near as bad.

The economy is much like nature in that downturns are both natural and cyclical. As any econ student knows, business cycles entail periods of expansion and contraction, punctuated by peaks and troughs.

Throughout modern history, financial wizards have tried various methods to prevent or at least smooth out the peaks and troughs (especially the troughs.) But, the real economy rarely cooperates.

Throughout modern history, financial wizards have tried various methods to prevent or at least smooth out the peaks and troughs (especially the troughs.) But, the real economy rarely cooperates.

For starters, excess optimism and pessimism are baked into human nature — both the cause of and the antidote for one another. Behavioral yin and yang, if you will.

And, there’s also what could be called the “wildfire principle.” When a central banker acts to prevent the occasional financial wildfire, the cycle might be delayed or interrupted — but, not eliminated. And, delaying or interrupting it is likely to only make the next one worse. As we discovered (but, have apparently forgotten) in the last financial crisis, prices do eventually revert to the mean.

Even along the way, the negative effects can greatly outweigh the benefits. When the Fed forced “risk free” interest rates to historically low levels, for instance, they increased the present value of streams of cash flow (earnings, dividends, rents or whatever.) This ratcheted up the price of things without increasing their utility (i.e. created asset bubbles.)

And, by rendering bonds relatively useless from a cash flow standpoint, central bankers encouraged investors to pile into overpriced assets without regard to the historical risks. They’ve even taken extraordinary steps to reassure investors that these assets are risk free. It’s the equivalent of building wood-framed houses on fire-prone prairies and then offering interest-free loans and move-in specials. What could go wrong?

Perhaps the most egregious example of central banker interference has been the yen carry trade [see: Yen Carry Trade Explained.] I believe most of equities’ gains since 2011 are attributable to this effective, but ill-advised scheme.

Perhaps the most egregious example of central banker interference has been the yen carry trade [see: Yen Carry Trade Explained.] I believe most of equities’ gains since 2011 are attributable to this effective, but ill-advised scheme.

Large investors can borrow in yen at near 0%, invest in equities certain to rise, and repay their debt with yen guaranteed to have declined. It works because the BoJ has been willing to ignore the negative effects on the Japanese people in order to keep stocks rising.

Like a forest that never burns, Nikkei 225 has gained about 140% since its Fukushima lows. The chart below shows how QQE and stock purchase programs extinguished various flare ups along the way, while the falling yen (rising USDJPY) essentially acted as fertilizer. [Note: the BoJ and GPIF purchase stocks directly and are currently the largest shareholders of Japanese stocks — amounting to $666 billion, about 14% of Japan’s GDP and the NKD’s market cap.]

After such rapid, uninterrupted gains, the Nikkei was an ideal target for arsonists. But, the BoJ kept it growing by: (a) constantly debasing the yen; and, (b) buying every dip that came along. So, it’s no surprise that, nearly a year after QQE and USDJPY flatlined, NKD has actually lost value. If USDJPY ever actually suffered a meaningful decline, the gains of the past four years would no doubt go up in smoke.

The FOMC’s recent non-rate increase was evocative of the BoJ’s behavior. In a stunning impression of a forest that should have been thinned long ago, Yellen & Co. deemed a 1/4% increase in the Fed Funds rate too great a threat!

Furthermore, the Fed — like the BoJ — has been fundamentally deceitful regarding its reasons for holding rates near zero for over seven years. It has nothing to do with reaching a desirable rate of inflation (if it ever did.) There’s plenty of inflation to be found if it were properly recognized and acknowledged. The reason is much more straightforward. We can’t afford it.

The US spent seven long years landscaping its economy, budget and stock market with unnaturally low rates. A return to normal rates now would bankrupt borrowers who built business plans around ZIRP and slash the value of investments whose prices are based on cash flow.

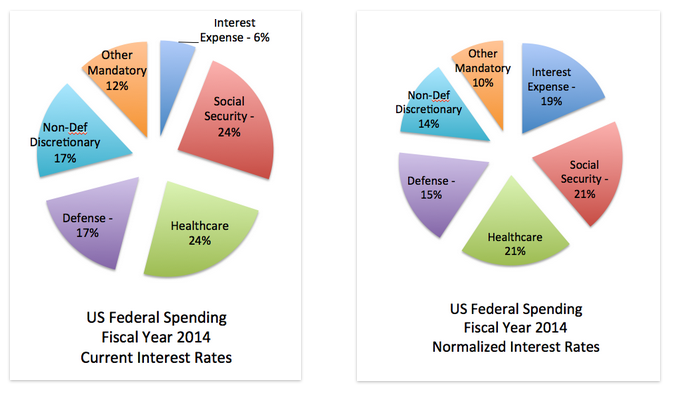

It would also triple the US’s annual interest expense, boosting it from last place to third in the race to waste the most taxpayer money.

As the Fed Governors so aptly demonstrated last week, it’s probably too late to attempt a controlled burn. Their only choice, now, is to remain hyper-vigilant, hoping against hope that the ultimate reversion to the mean won’t come during their tenure.

The hapless ECB is content to sit in Franfurt with their fingers crossed, secure in the knowledge that while they don’t know how to fix the euro zone’s problems, no one else does either. Their trillion euro experiment has produced negative interest rates, which allows overindebted countries to continue to appear solvent. But, they’re not really fooling anyone. Like Japan, only ECB-funded banks and the ECB itself are buying those bonds.

The BoJ, after watching 2015’s gains go down in flames over the past three weeks, will no doubt throw more fuel on the fire in the form of expanded QQE and/or additional yen debasement. In fact, since last March [see: A New Analog], my market forecasts have presumed that TPTB would tank stocks if necessary in order to “help” the BoJ make the right decision. They’re in an equity trap of their own making.

The late-August conflagration was a good start. The flames currently racing towards us just might do the trick.

Stay tuned.