On May 16, we adopted the position that weak inflation – driven primarily by oil prices that we expected to plunge after a brief rally – would lead the EURUSD to rally sharply [see: May 16 Update on EURUSD.]

Our forecast, shown below, also required DXY to make new lows — which most analysts derided as unlikely in a rising interest rate environment.

Sure enough, WTI spiked for about a week, then plunged right to our downside target over the following month. This took the wind out of inflation’s sails, leaving the Fed’s rate hike argument looking more than a little iffy.

This took the wind out of inflation’s sails, leaving the Fed’s rate hike argument looking more than a little iffy. The net effect? Yesterday, EURUSD nailed our upside target.

The net effect? Yesterday, EURUSD nailed our upside target.

With Yellen’s testimony coming up, it’s an opportune time to review the overall currency picture and its likely effect on equity prices – and, by that, I’m not talking about the latest VIX-driven ramp job.

With Yellen’s testimony coming up, it’s an opportune time to review the overall currency picture and its likely effect on equity prices – and, by that, I’m not talking about the latest VIX-driven ramp job. I’ve been promising a turning point for the past several weeks, and it’s finally here.

I’ve been promising a turning point for the past several weeks, and it’s finally here.

continued for members…

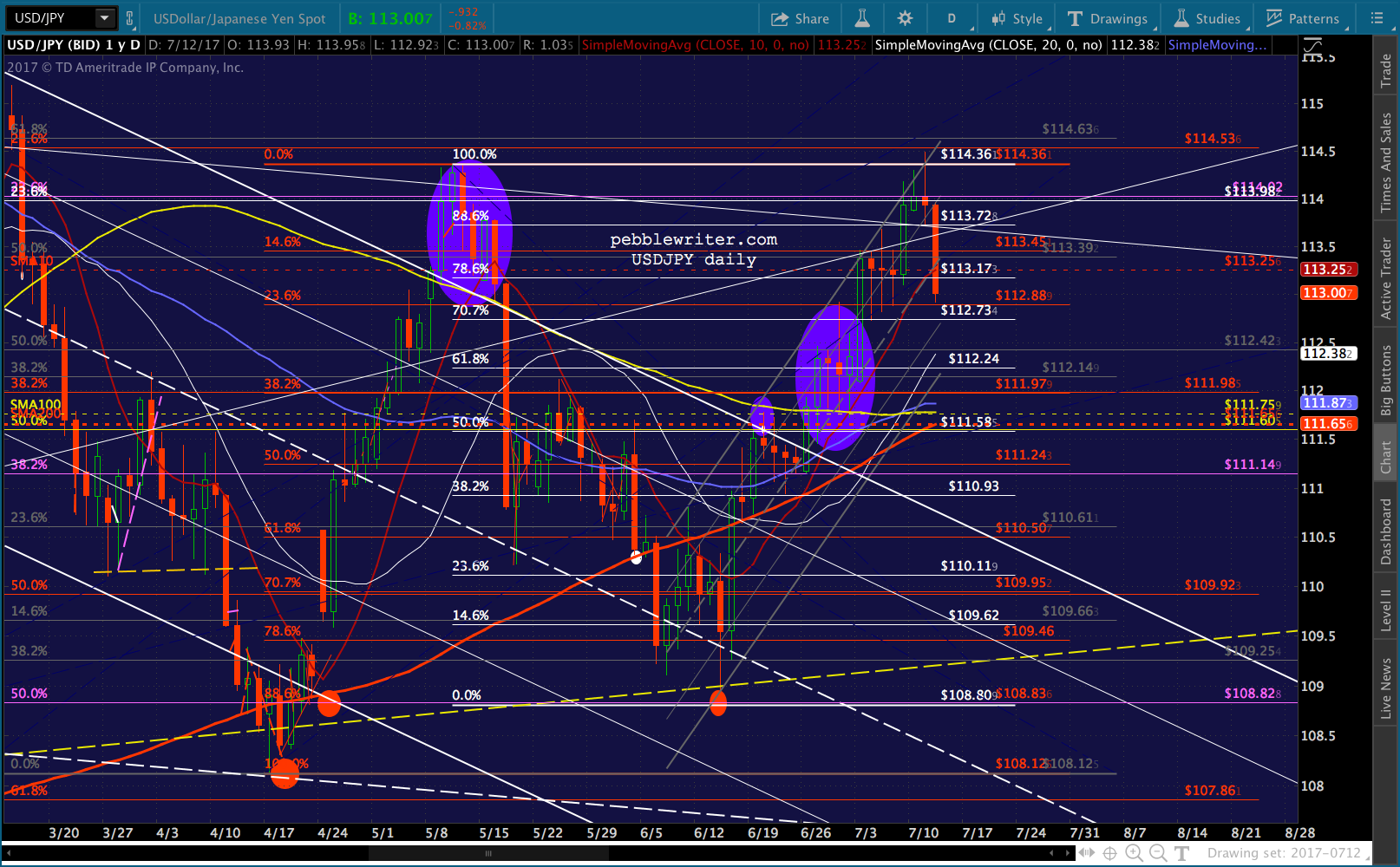

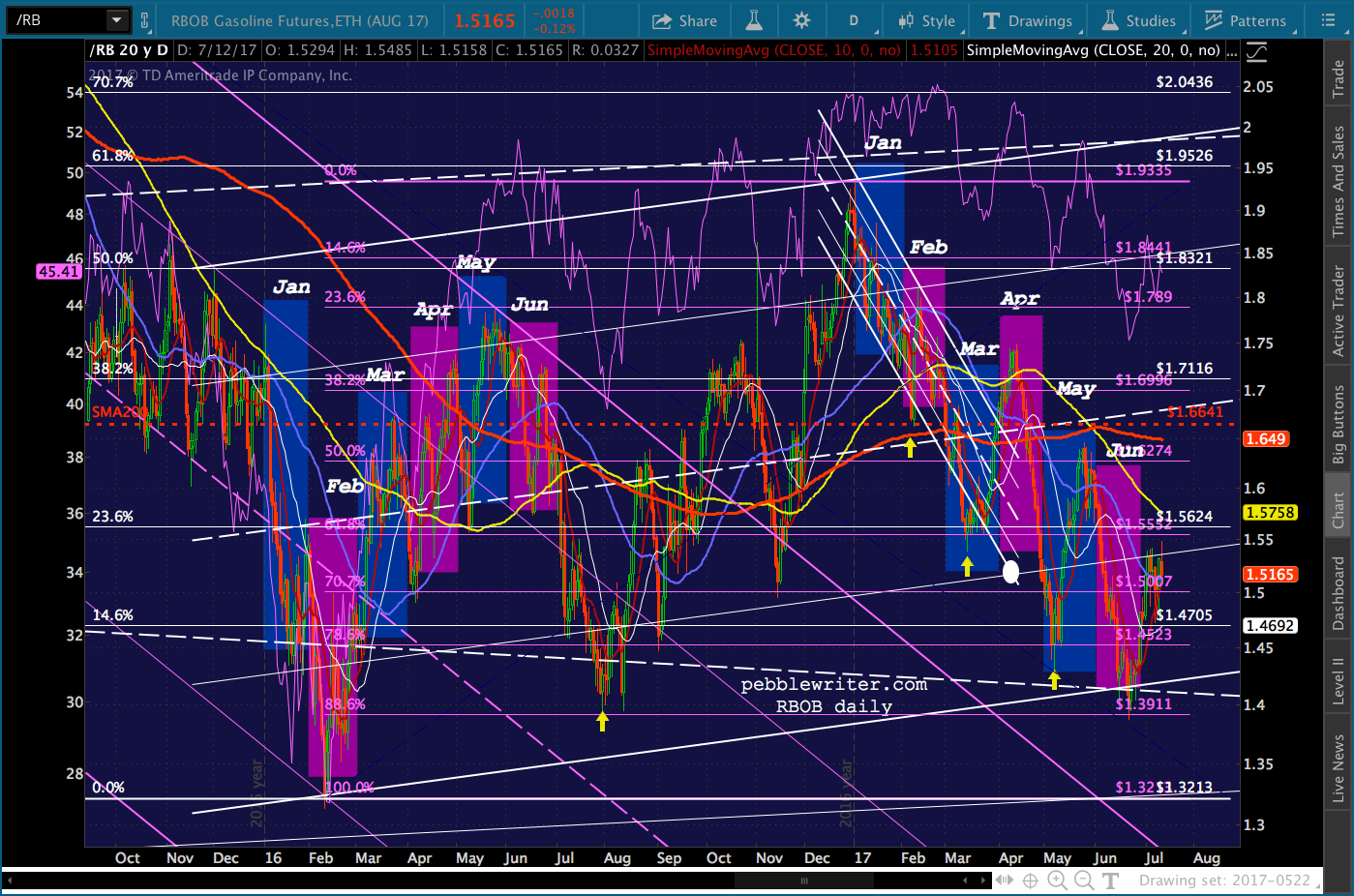

Note that USDJPY, having helped keep stocks afloat even as DXY faltered, is finally coming back to earth. CL is in “whatever it takes” mode.

CL is in “whatever it takes” mode. While DXY put in a slightly lower low — a truncated 5th, I believe. This should represent a nice buying opportunity, especially against the EUR if not the JPY.

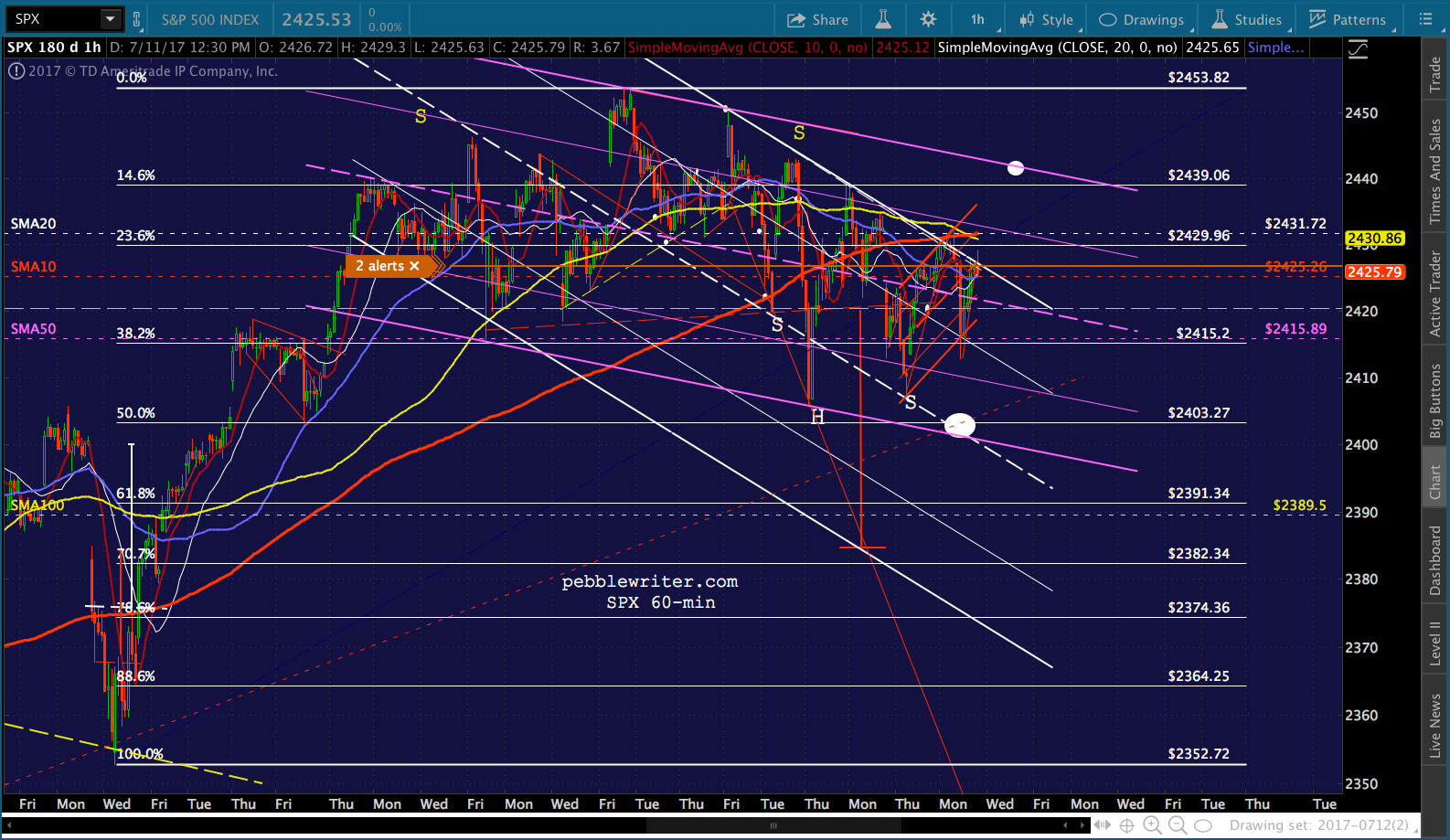

While DXY put in a slightly lower low — a truncated 5th, I believe. This should represent a nice buying opportunity, especially against the EUR if not the JPY. We should find out what’s in store for equities fairly quickly, as DX strength should translate into equity strength. If ES is able to break out of its falling white channel at 2438ish…

We should find out what’s in store for equities fairly quickly, as DX strength should translate into equity strength. If ES is able to break out of its falling white channel at 2438ish…  …SPX has a crack at doing the same with its falling purple channel at 2442.80.

…SPX has a crack at doing the same with its falling purple channel at 2442.80.

As we discussed last week, if DXY can’t catch a bounce here, it’ll be a real headwind for equities.

UPDATE: 9:52 AM

SPX just reached and briefly topped its purple channel top. This is probably a good spot for anyone riding the initial bump to take profits. UPDATE: 3:25 PM

UPDATE: 3:25 PM

I’ve been sitting here for hours, digesting what Yellen said and trying to make sense of everything. Here’s where I am.

First, I thought Yellen’s statement and Q&A came off dovish. I think it was meant to sound hawkish enough to support the USD, but dovish enough not to scare the children. And, I think she nailed it.

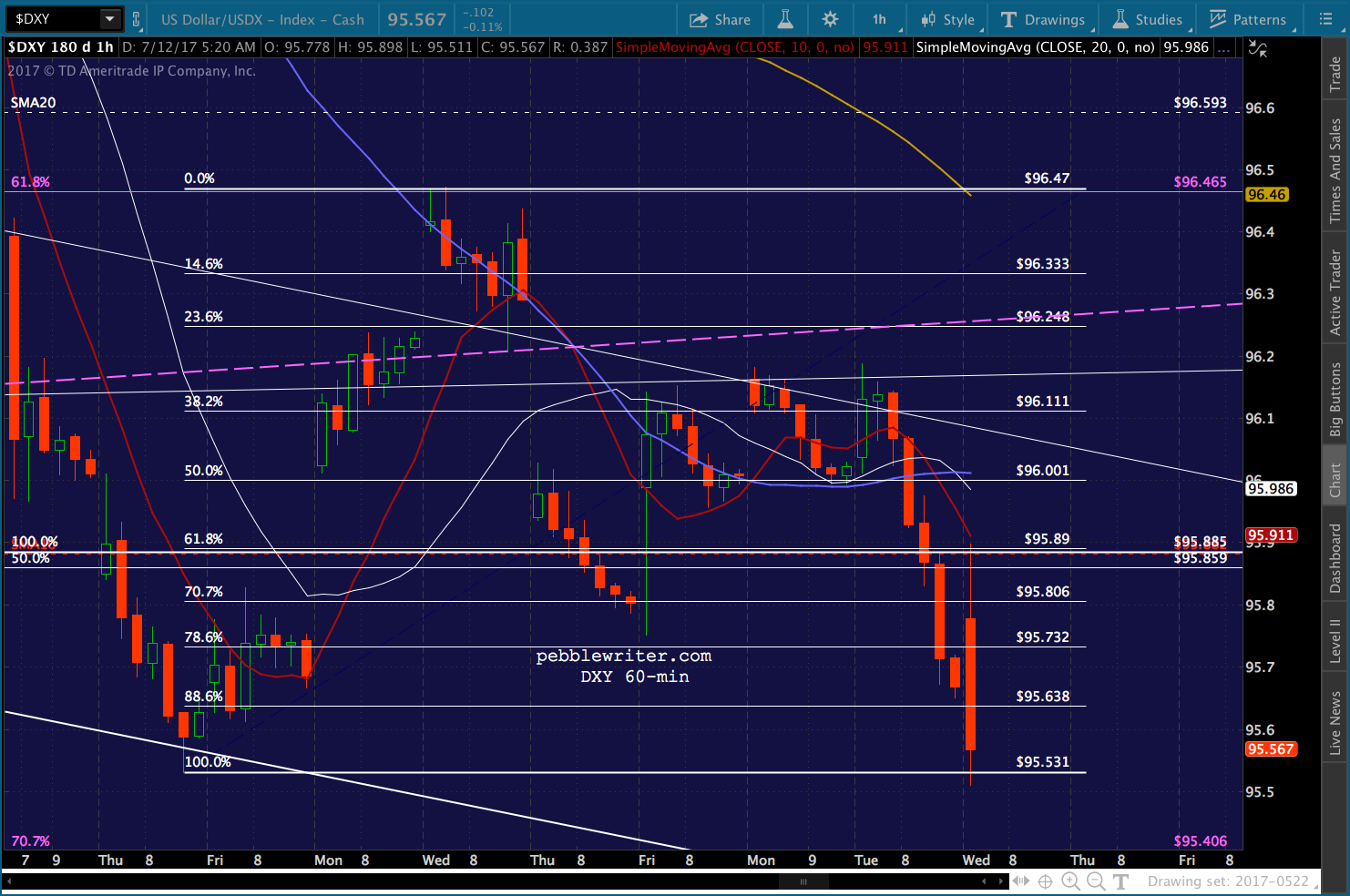

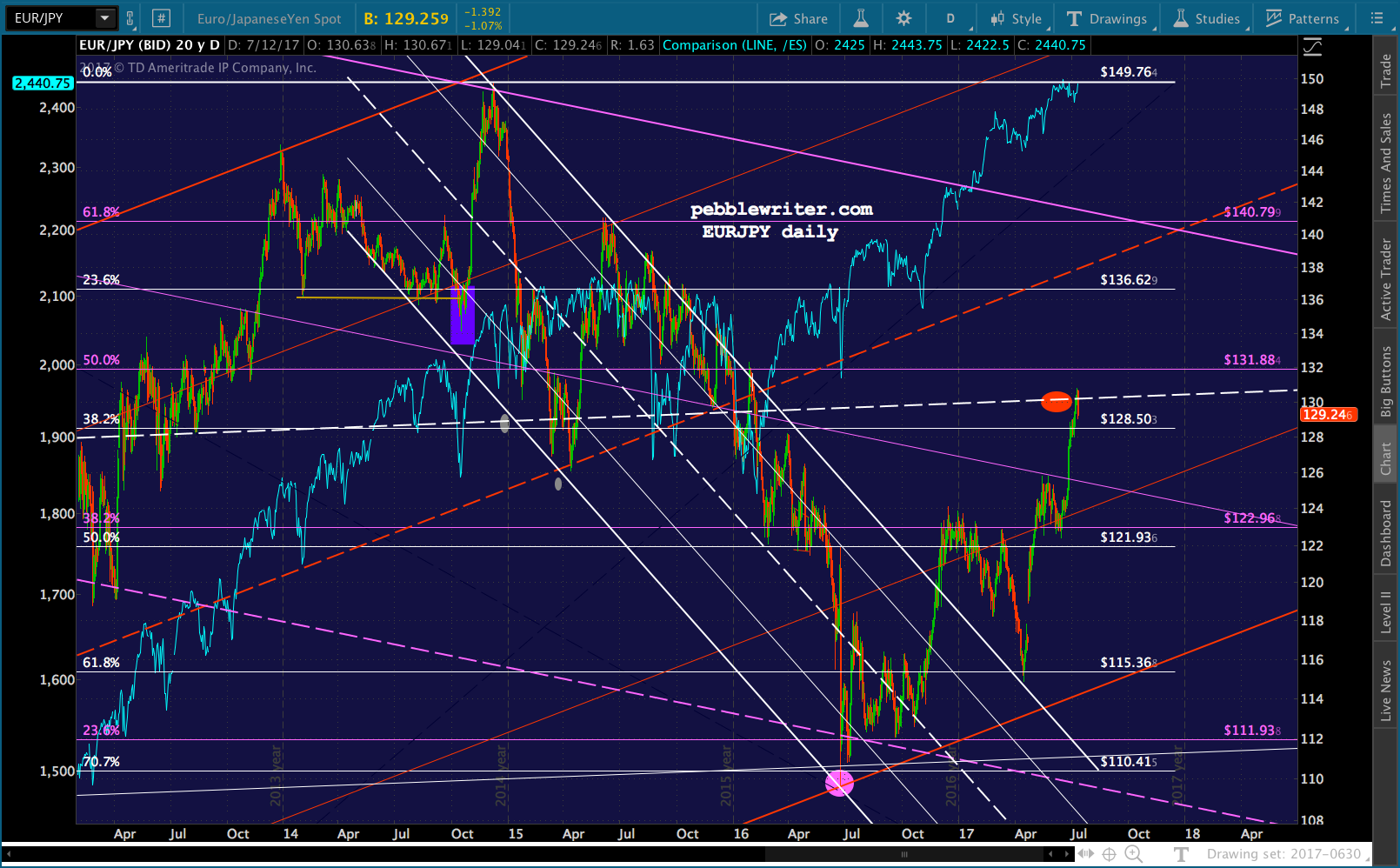

USDJPY is still falling… …but, EURUSD is, too.

…but, EURUSD is, too. As a result, DXY is mostly waffling (but, still off its lows.)

As a result, DXY is mostly waffling (but, still off its lows.) Other than the 17% VIX smackdown, there’s very little technical reason for stocks to be higher today. Fundamentally, I suppose you could make an argument that being slightly dovish means the possibility of skipping a rate hike or two. But, frankly, I think they’ll hike as much and as often as they think they can get away with without affecting stocks.

Other than the 17% VIX smackdown, there’s very little technical reason for stocks to be higher today. Fundamentally, I suppose you could make an argument that being slightly dovish means the possibility of skipping a rate hike or two. But, frankly, I think they’ll hike as much and as often as they think they can get away with without affecting stocks.

It has been amusing hearing the Fed blame cell phone and RX prices for lower inflation, when it’s perfectly obvious that oil is the biggest “transitory” factor.

As we’ve discussed many times, June’s YoY comp is going to be atrocious — every bit as bad as May’s. I don’t see any way rates will be increased in July — though there might be plenty of talk. This means DXY will likely continue fighting an uphill battle — unless EUR makes it possible for DXY look good by comparison. If the economic news coming out of Europe is so bad that the ECB doubles down on dovishness, it could tip the scales in favor of the USD.

This means DXY will likely continue fighting an uphill battle — unless EUR makes it possible for DXY look good by comparison. If the economic news coming out of Europe is so bad that the ECB doubles down on dovishness, it could tip the scales in favor of the USD.

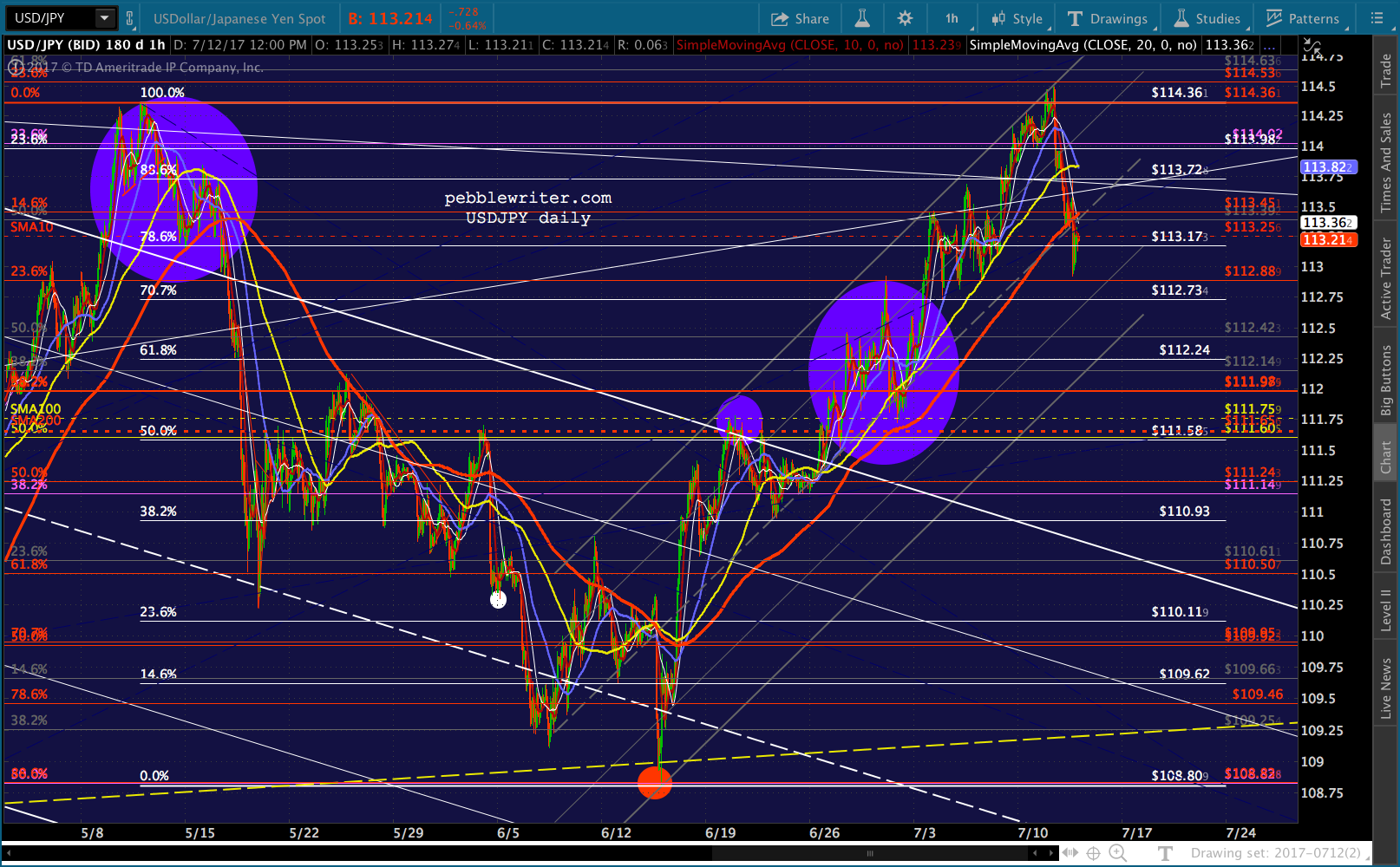

Given that JPY got so out of whack, though, in supporting the USD while the EUR was depressing it, I’d take a different tack in trading the currencies and consider shorting the EURJPY. It’s up against a channel midline — probably as a backtest — and, the whole thing should unwind. If I’m wrong, there’s a pretty clean stop level at 131ish. Eurozone CPI comes out tomorrow, while US comes out on Friday.

Eurozone CPI comes out tomorrow, while US comes out on Friday.

GTLA.