Unless something dramatic happens in the next 24 hours, November CPI will top 2% again. This obviously lends credence to the overwhelming market expectation for a rate hike in December. – even though PCE is still languishing well below target. Yet, there are still two events in the coming days that could give the Fed pause: the tax bill (due for a vote in the Senate tomorrow) and the debt ceiling (will be reached next Friday.) If either isn’t successfully navigated, will the Fed still have the nerve to raise rates? And, if they don’t, what would that do to markets?

Yet, there are still two events in the coming days that could give the Fed pause: the tax bill (due for a vote in the Senate tomorrow) and the debt ceiling (will be reached next Friday.) If either isn’t successfully navigated, will the Fed still have the nerve to raise rates? And, if they don’t, what would that do to markets?

continued for members…

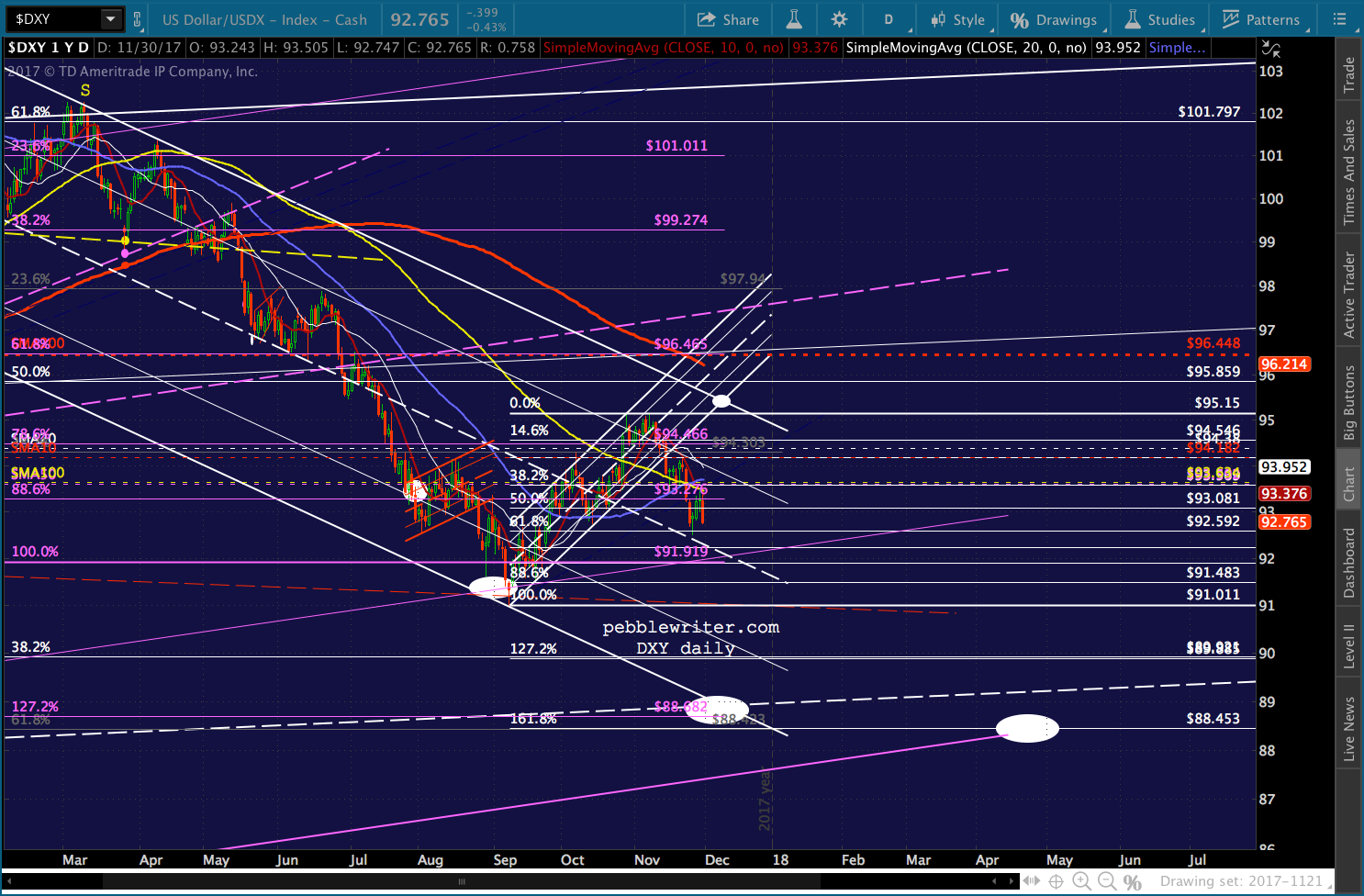

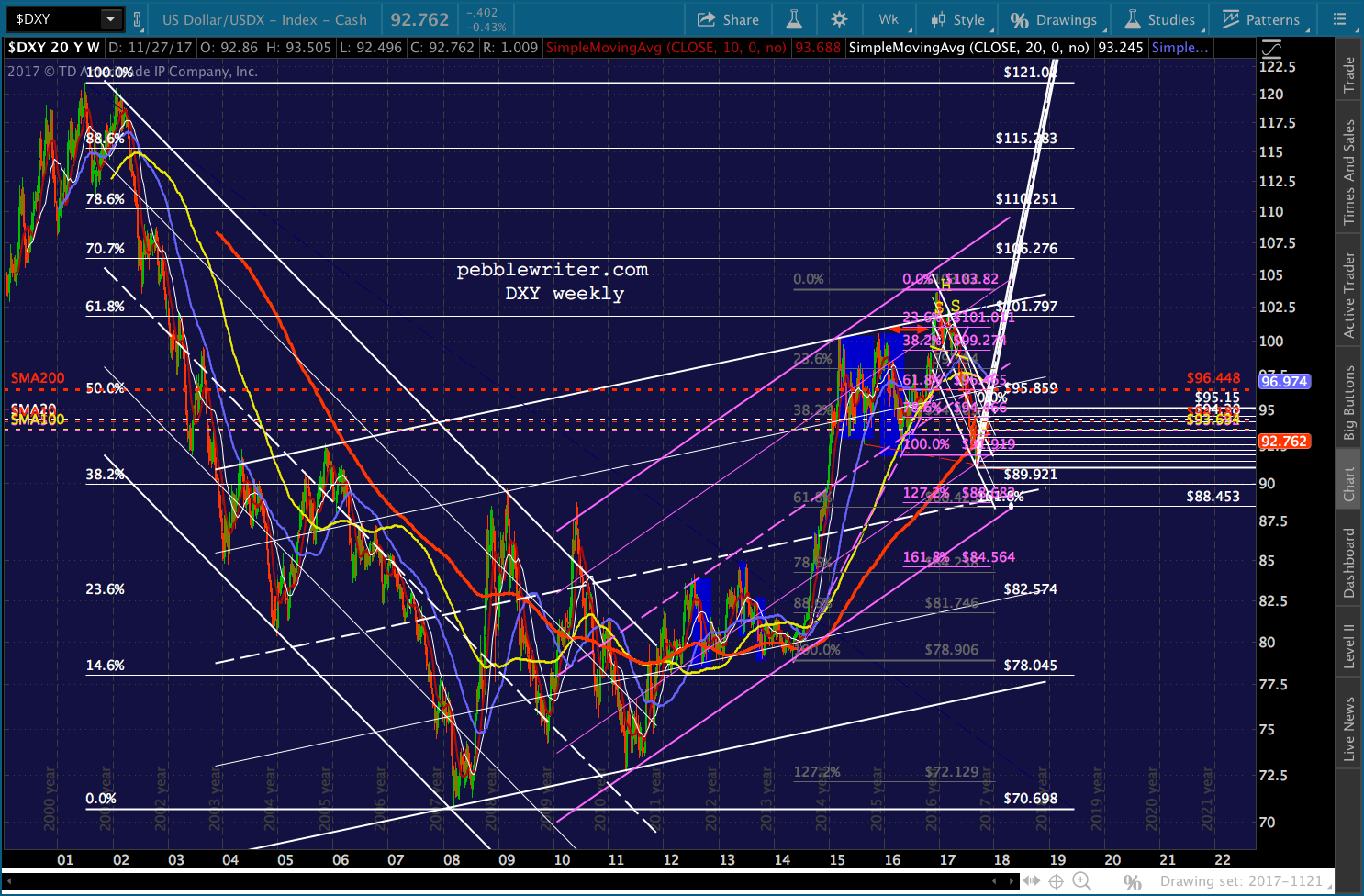

The DXY has spent the past few days acting as though it believes, but the chart hints at potential weakness. Obviously, the rising white channel’s breakdown is problematic. But, the subsequent drop was arrested at the falling white channel midline – providing grist for the bounce that’s taken place this week.

The insinuation is that DXY will continue bouncing up to the top of the large white channel. But, a backtest of the broken rising channel would need to happen very quickly. The two channels intersect on Dec 7, almost a week before the FOMC’s Dec 12-13 meeting. Consider the alternative: if DXY didn’t continue bouncing up to the top of the falling white channel and the SMA200. Note that the falling white channel intersects with the huge white channel midline at 88.88ish around that same time frame: Dec 7. And the 1.272 extension at 88.682 and newly formed 1.618 extension at 88.453 offer attractive targets.

Consider the alternative: if DXY didn’t continue bouncing up to the top of the falling white channel and the SMA200. Note that the falling white channel intersects with the huge white channel midline at 88.88ish around that same time frame: Dec 7. And the 1.272 extension at 88.682 and newly formed 1.618 extension at 88.453 offer attractive targets.

Which one is more likely? Hard to say. I’m not sure it’s as binary as it seems. Some of our previous rate hikes have been followed by sharp declines in DXY. The fact that it’s exhibiting such weakness when “everything is going so well” suggests this might be the case this time as well.

Which one is more likely? Hard to say. I’m not sure it’s as binary as it seems. Some of our previous rate hikes have been followed by sharp declines in DXY. The fact that it’s exhibiting such weakness when “everything is going so well” suggests this might be the case this time as well.

That is, we could get a bounce between now and Dec 7-13 based on political developments and expected Fed actions that, then, unwinds after year-end. That way, USDJPY would be under less pressure and stocks would get all the help they need.

The white .618 (92.592) that was tagged on Nov 27 could be setting up a Gartley at 91.897. If it drops any further, I’d say it’s game on for the dollar bears, with additional support at 91.483, 91, 89.9 and 88.5-90. I’d be willing to let my short position run as long as it closes below the SMA10 and SMA100. Anything above that, and I’d be inclined to ditch it.

Of course, dollar weakness means a higher EURUSD — likely leading to a breakout of the falling white channel that would otherwise be heading for the SMA200 (now at 1.1371) and/or white channel bottom around 1.13-1.14.

Should be interesting.

Now, on to the oil and gas sector…

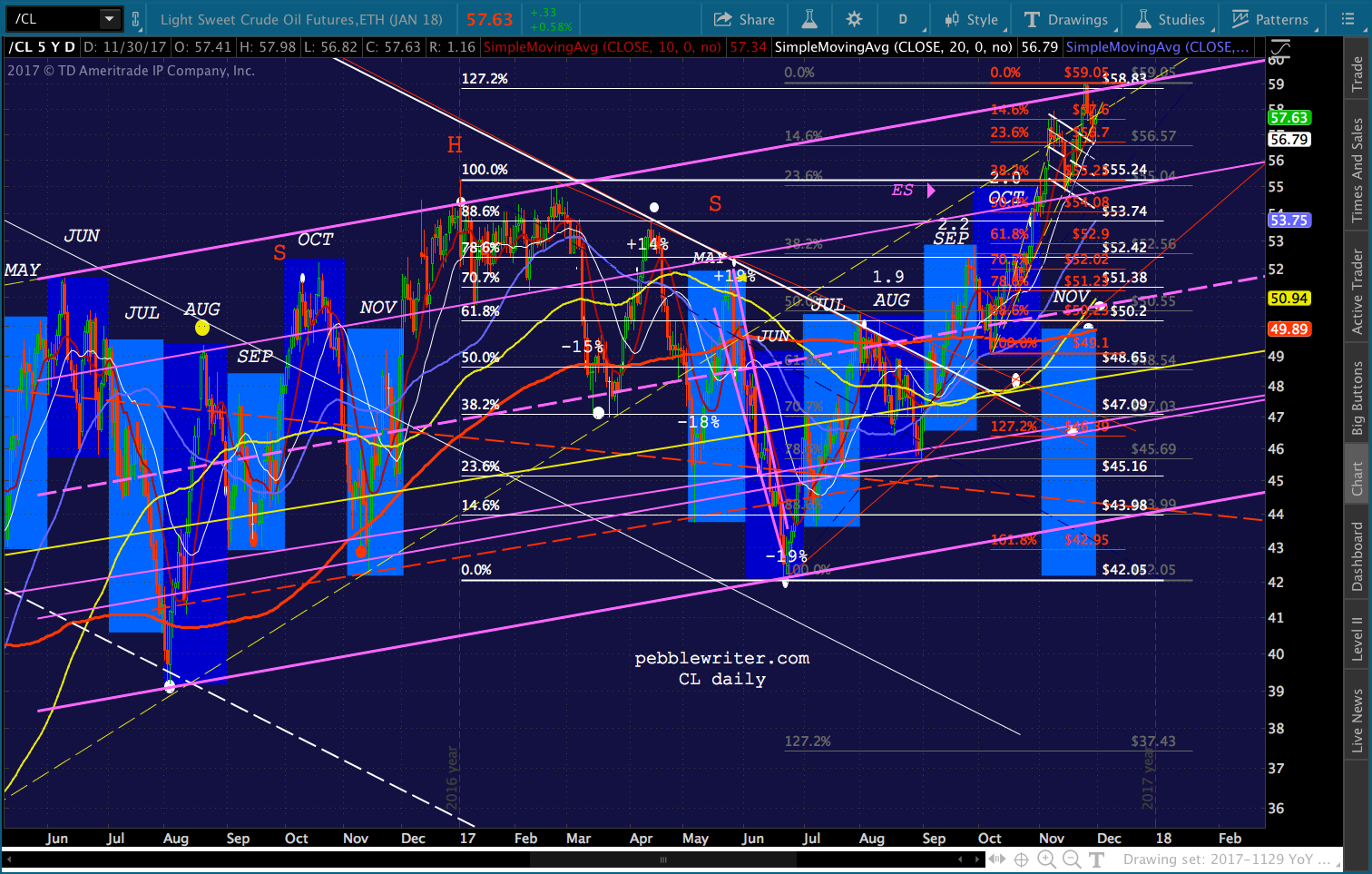

Needless to say, I’m disappointed that we didn’t have more follow through to yesterday’s sharp declines. OPEC announced an extension of the current output deal (details to follow…) and RB is currently up .20% and CL is up .51% on the day.

Unless it tumbles in the next 12 hours, it looks like CL is going to have a huge gap over Nov 2016’s range. Whether or not the BLS includes those numbers in their headline CPI release, who knows. But, it’s substantial and, if no games were played with the numbers, would result in a big increase in YoY CPI and PPI.

Unless it tumbles in the next 12 hours, it looks like CL is going to have a huge gap over Nov 2016’s range. Whether or not the BLS includes those numbers in their headline CPI release, who knows. But, it’s substantial and, if no games were played with the numbers, would result in a big increase in YoY CPI and PPI.

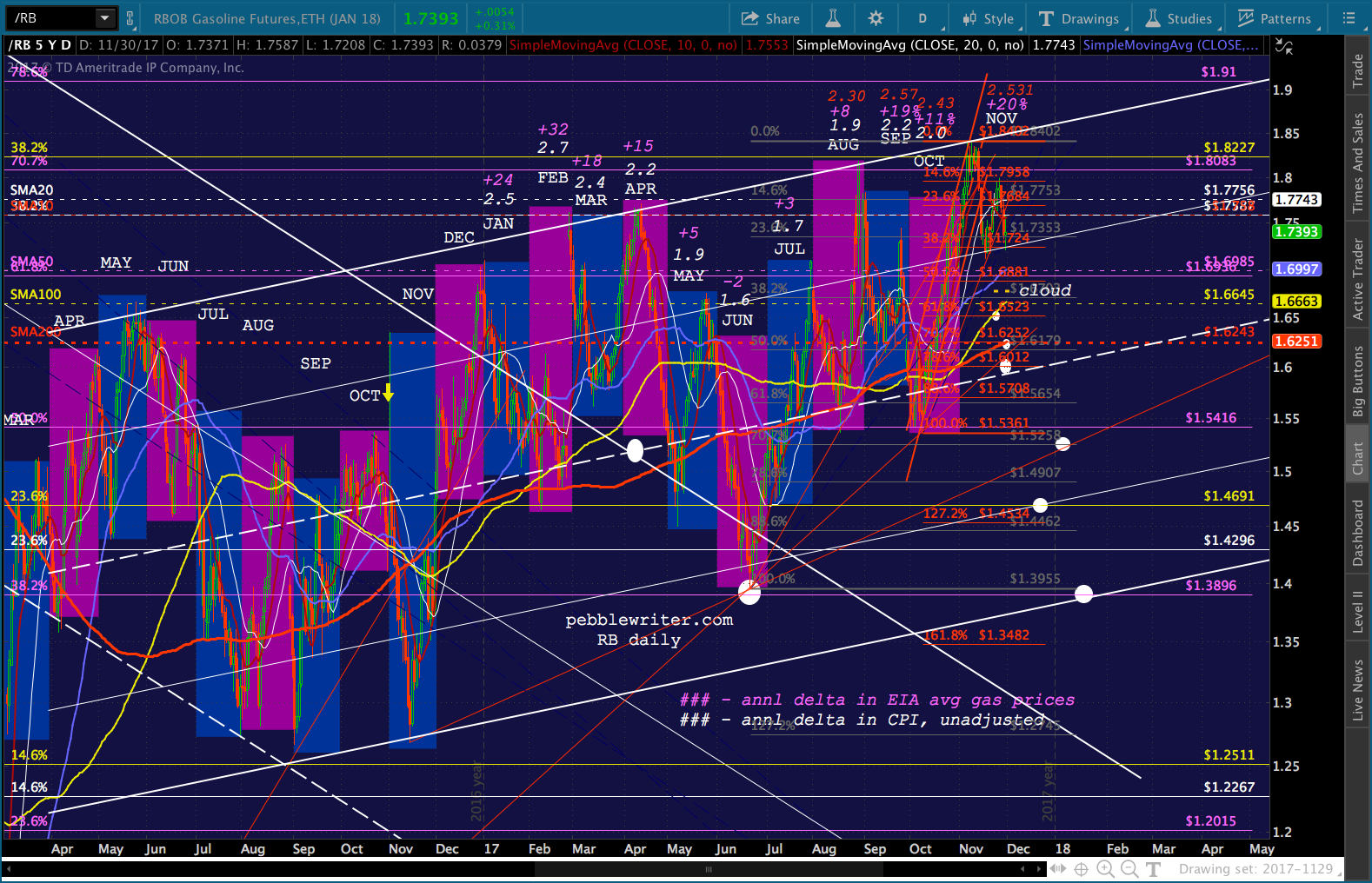

It’s a little easier to gauge the effect of gasoline prices on inflation — though the BLS has been playing games with the timing and, therefore, pricing of the data they input. I track prices daily, and can say that the average price in November has been 2.531 versus 2.105 in November 2016. It’s a 20.3% increase — which, based on past experience, should equate to a 2.3-2.4% CPI print.

RBOB itself has averaged 1.77 during November 2017 versus 1.38 in November 2016 (closing prices.) This was a 28.92% increase, meaning only 2/3 of it was passed along to consumers at the pump.

Remember, however, that there was a big intraday spike on Nov 1 2016 (1.44 – 1.63) that, if the BLS so chose, could be emphasized in the historic data — resulting in a much smaller reported increase (e.g. from 1.63 to 1.72 is only 5.5%.)

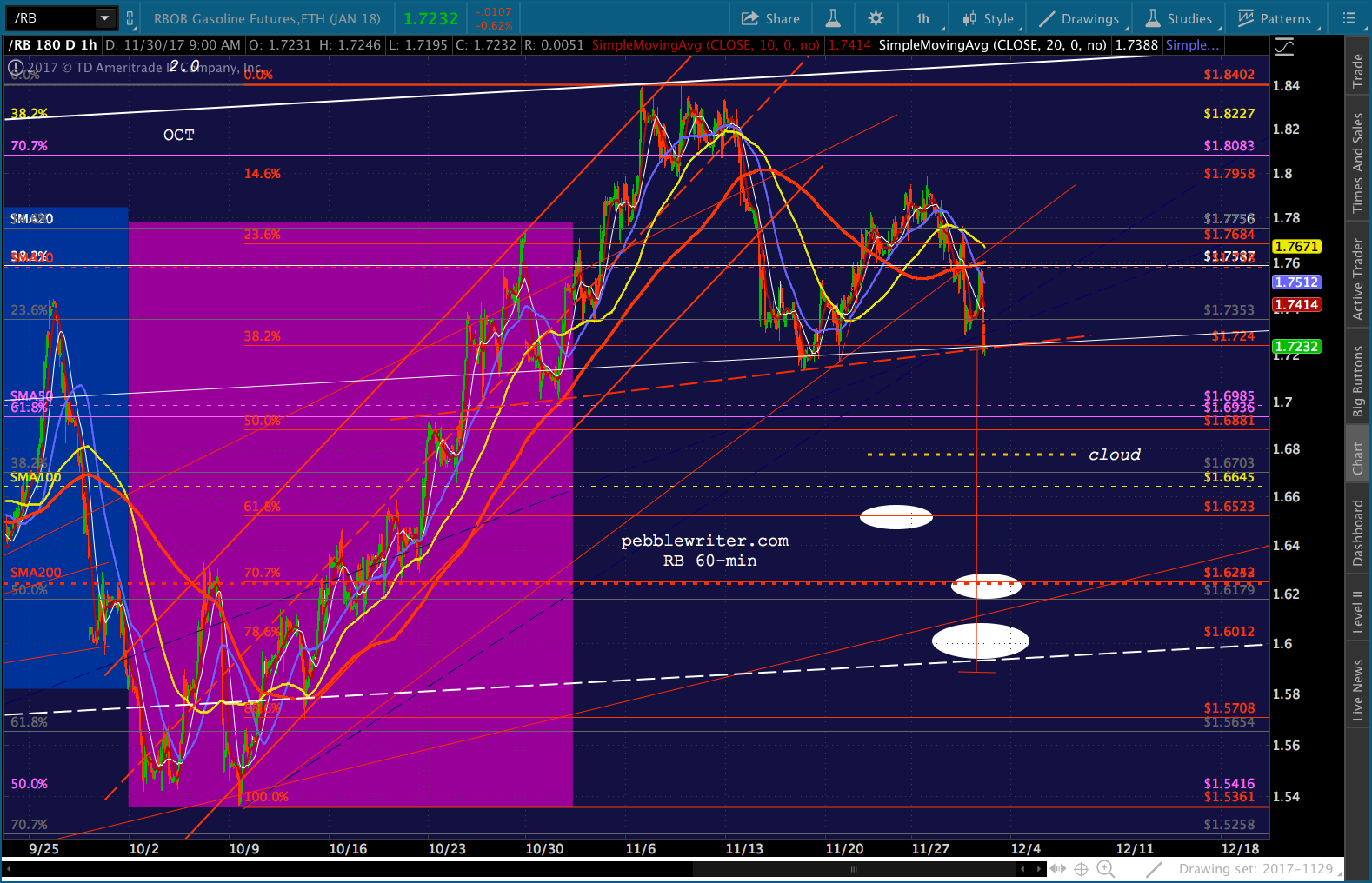

While I’ve been writing this, RB has given up all its gains and is currently down to 1.72 — a small 3.3% gain given our 1.78 short. That gain would expand to 5.6% at the cloud top of 1.68, and over 10% if it fell to the H&S target of 1.6ish. Caution is warranted.

If RB bounces here, CL certainly will. I’d want to remain long above the TL, currently around 57. Just know that the upside might be limited, and the OPEC deal doesn’t exactly make me bullish. Past deals have been followed by selloffs.

If RB bounces here, CL certainly will. I’d want to remain long above the TL, currently around 57. Just know that the upside might be limited, and the OPEC deal doesn’t exactly make me bullish. Past deals have been followed by selloffs.

GLTA.

Comments

2 responses to “The December Rate Hike: A Sure Thing?”

In the beginning of the year, you had a possible target in the S&P at 2750 I believe? Do you remember when that was posted?

Hmmm, I can’t recall that particular number. But, I’ll put a chart on the 12/5 post that shows where it might come in.