Where did March go? If you’re anything like me, it was a blur. I was in the process of recovering from knee replacement surgery when the crash began [being under the influence of some very strong pain killers was probably the best way to weather the storm.]

On February 3, the day before I went under the knife, I pulled together a forecast on everything I chart: stocks, bonds, currency pairs, commodities, etc. I try to update the Current Forecast page at least every month. But, between the pain and the global pandemic which threatened to trap my daughter in Rome, I was a little preoccupied.

I had been fairly bearish when penning that Feb 3 forecast and was still lucid enough in the following weeks to warn of the coming storm, writing on Feb 18 in When Will News Begin to Matter Again…

…be very careful in chasing this breakout. It is built on a very weak algo-driven foundation which, given the coming moves in CL, DXY, USDJPY and TNX, cannot stand. When it cracks, it could be quite violent.

…and, again on Feb 20 in Buckle Up:

…the major downside support levels such as the yellow 2.618 at 3047 – which was never backtested – and 2.24 at 2703 will soon disappear from the path of the existing rising channels… All I know is that when important support breaks down, it’s time to short – especially when the usual central bank tricks aren’t working.

As it turned out, Feb 20 was the all-time high. A month later, SPX had fallen further and faster than ever before. Needless to say, the targets mentioned in the forecast were reached and exceeded in almost every case – more than reversing the excesses of the breakout above SPX 3047.

My favorite downside targets over the past six months have been ES 2155 and SPX 2138. ES came close, dropping within 19 points of its target on Mar 23 before all hell broke loose.

My favorite downside targets over the past six months have been ES 2155 and SPX 2138. ES came close, dropping within 19 points of its target on Mar 23 before all hell broke loose.

The Fed began an extraordinary response which was expanded again by $2.3 trillion at 8:30:01 this morning. Not coincidentally, it was announced seconds after jobless claims of 6.6 million (also not coincidentally, which tied the worst ever prior continuing claims number) were announced.

Futures responded as planned — taking us another step past the line where price discovery used to be. The Fed might as well have named it the Prop Up the Market Program, as it lends new import to the expression “don’t fight the Fed.”

Oh, and just in case the market doesn’t understand the Fed’s intentions, Jerome Powell will give another presser at 10AM.

Just for fun, here’s a quick peek at where things stood on February 3…

Just for fun, here’s a quick peek at where things stood on February 3…

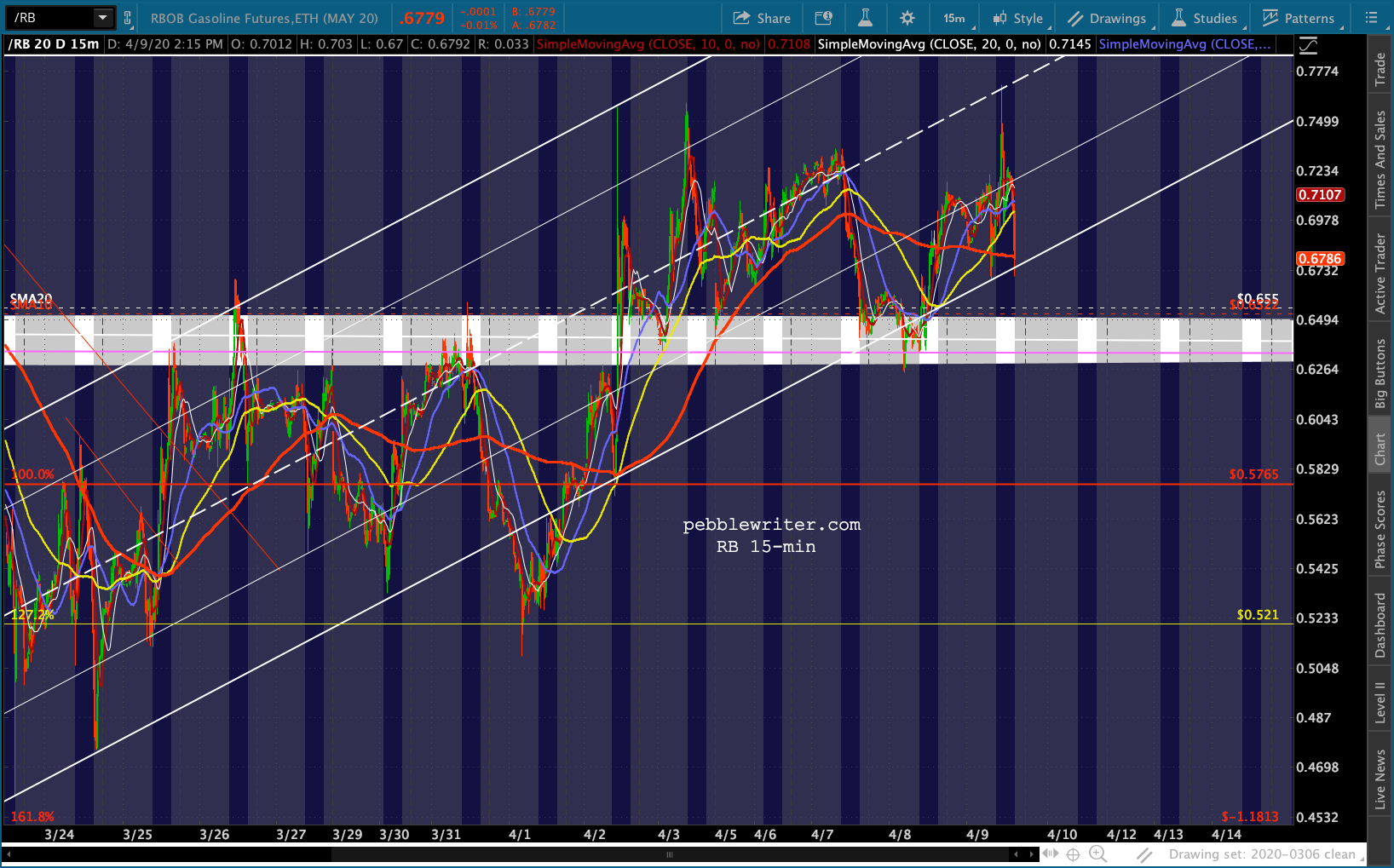

Short RB: 2/3/20 – Shorted near target on 4/24, back to long on 6/5, shorted again at backtest targets on 7/11 and back to long on 9/5. Back to short on 9/16 and back to long on 10/3. Shorted on 11/4 with tight stops, target of 1.35. Broke down on 11/19, but buy triggered on 11/20. Back to short on 11/22, long on Dec 4 and short on Dec 27. Targets are 1.44, 1.41 and 1.349.

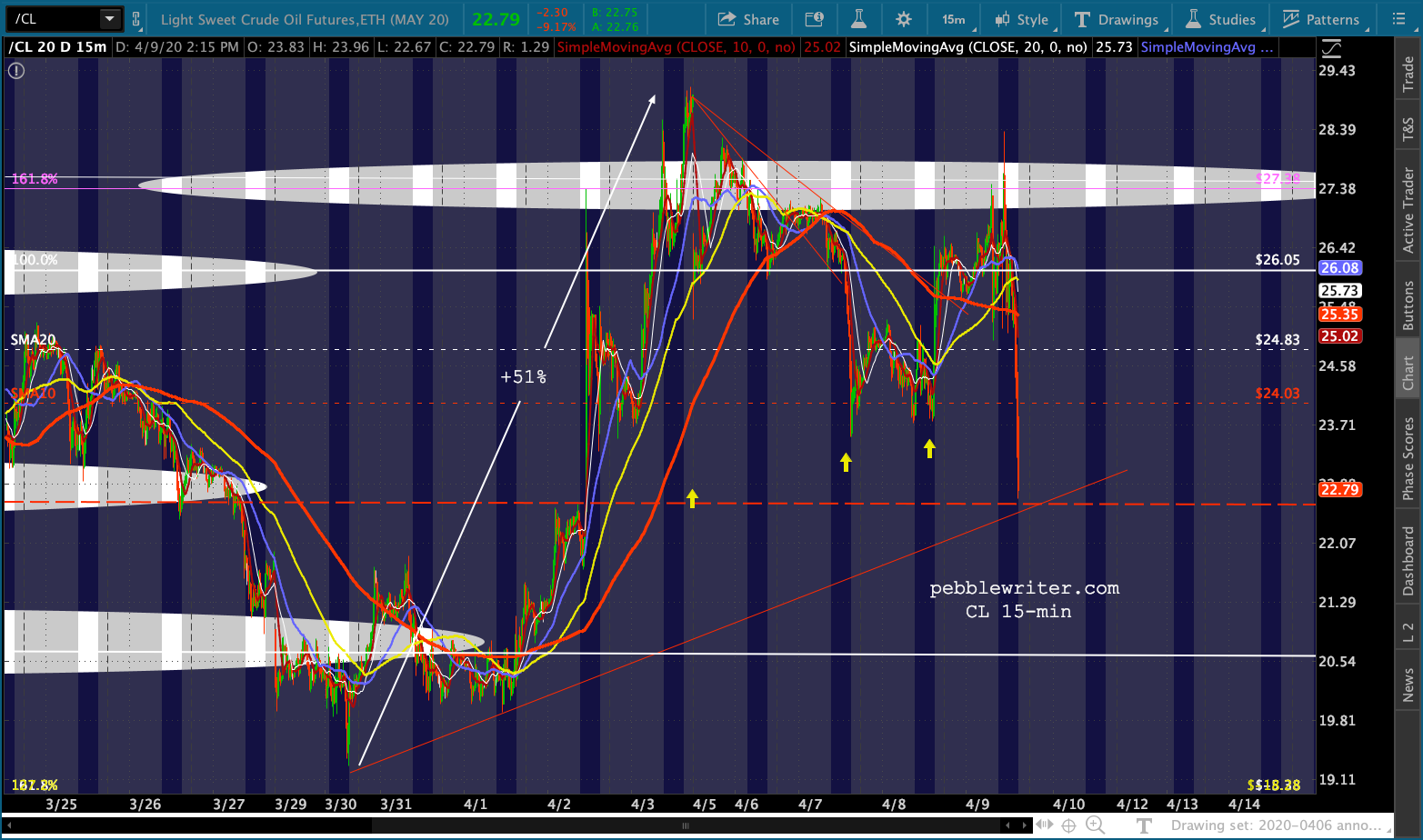

Short CL: 2/3/20 – Shorted near target on 4/24, back to long at target on 6/5, shorted at backtest target on 7/11, breakouts on 9/16 and .886 target on Jan 8. Targets delayed by Aramco IPO in Dec and Al Asad spike in January. 54.55 target reached on Jan 24, breakdown yielded targets of 51.62 (reached Jan 31), 49.46, 47.55 and 46.

Neutral DXY: 2/3/20 – We were long from 88.253 on Feb 16, 2018. Came close enough to our 97.873 target on Nov 12 and again on Dec 14 where we shorted at 97. Multiple breakdowns have bounced back, leaving DXY in trading range between 97-99 since Aug 2019. Essentially jerking algos around with signalling rises and dips. Don’t see it as a viable trading vehicle until at least March 2020, when inflation pressures should ease and make a decline possible.

Short USDJPY: 2/3/20 – Has been consolidating since June 2016, making lower highs and lows in the 104.74 area. Highs have followed a falling channel top, with the latest tag of our upside target on Jan 17. Since then, USDJPY has accommodated stocks’ weakness, with even lower downside targets of 107.94 and 107.64.a 107.64. The range remains tight (only 3 points, 107-110ish) so – like DXY – it has offered very modest trading opportunities.

Short EURUSD: 2/3/20 – Has been in a gently falling channel since July 2018, seems destined to remain in it for the foreseeable future. Recently backtested the latest rising corrective channel it broke down from. A nice drop to 1.0592 is possible, but the ECB is being careful to avoid big drops. Next downside target is 1.0813.

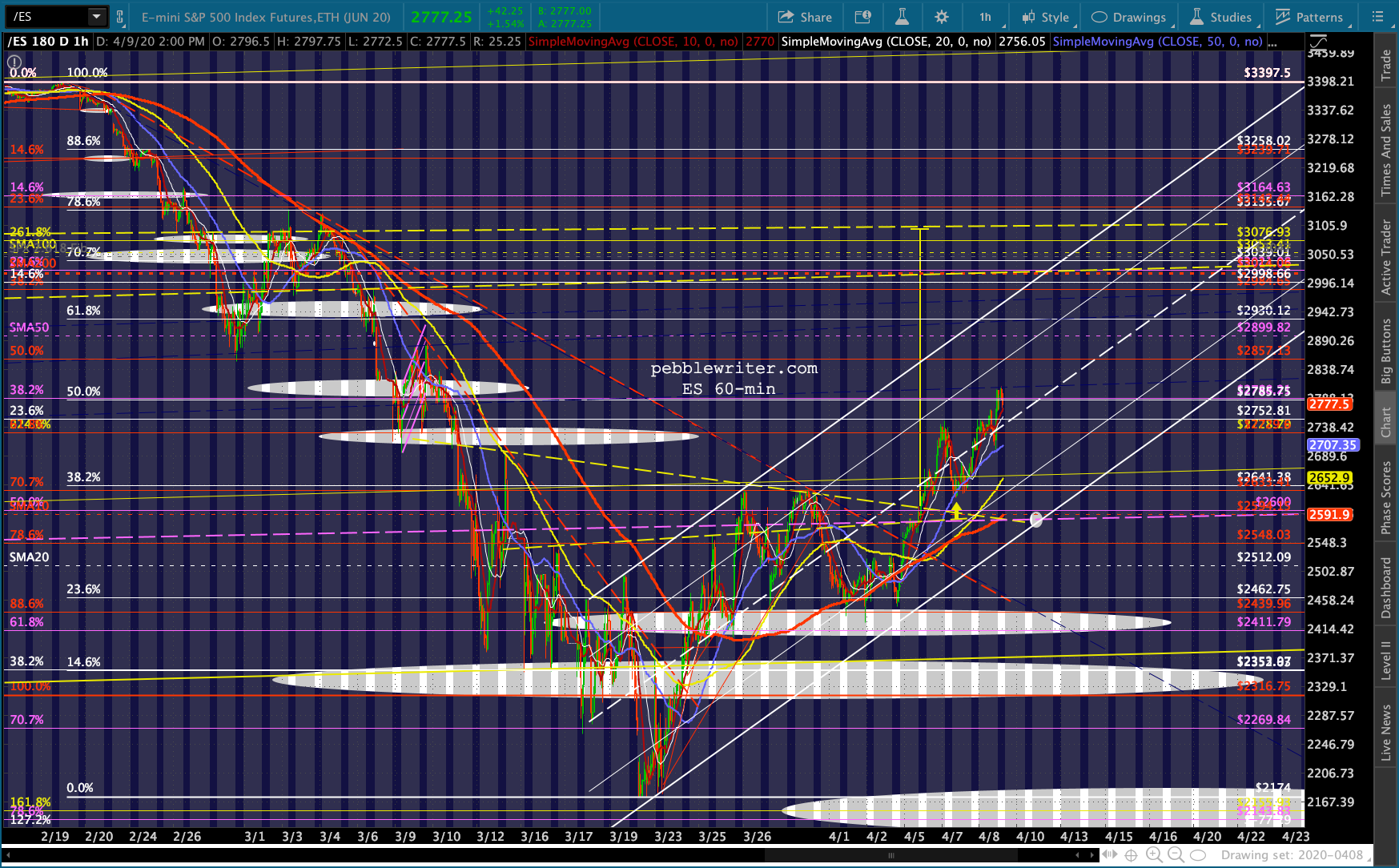

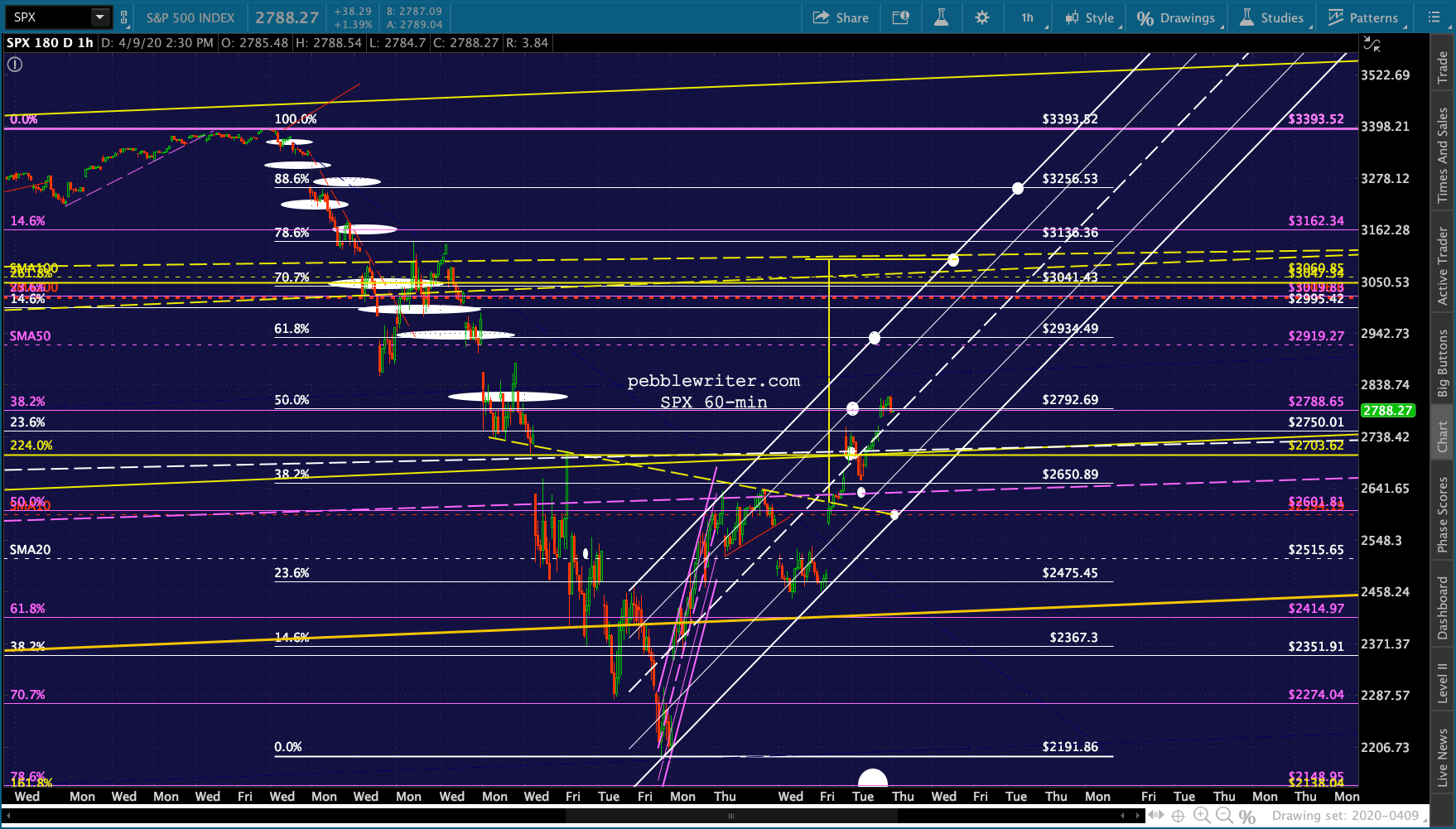

Short SPX/ES: 2/3/20 – formed an inverted H&S Pattern from Jan 2018, breaking out in Oct 2019 and racing higher in an acceleration channel to 1.618 Fib at SPX 3306.51/ ES 3336.49, at which point we started looking for a backtest of the acceleration channel/SMA50 around 3200 and, if that fails, the IH&S around SPX 3100. Major support below that include SPX’s 2.618 at 3047 and the 2.24 at 2703. If SPX should break out of its current correction, the IH&S targets 3673.

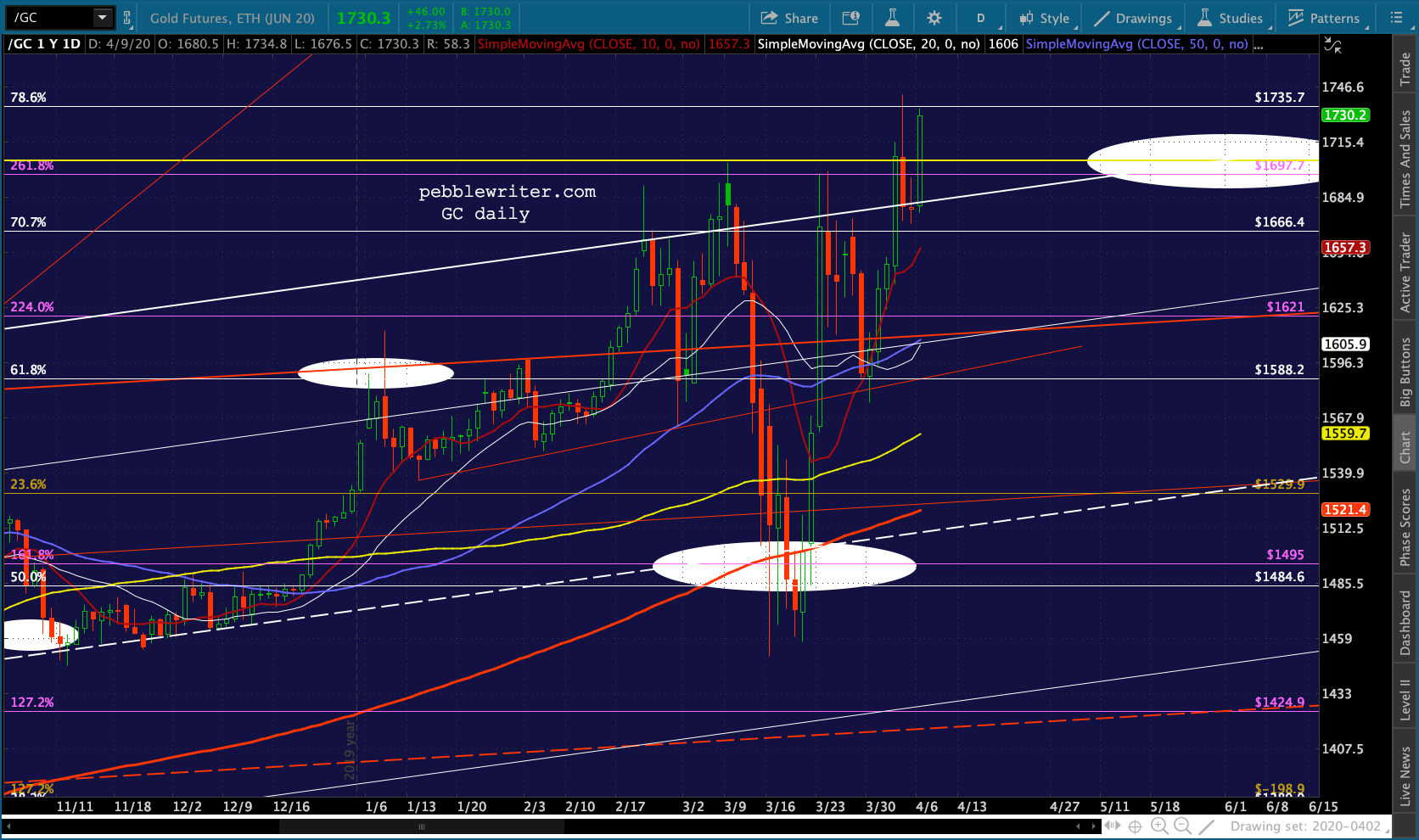

Long Gold: 2/3/20 – went back to long on rise through yellow TL at 1195 in August 2018. Completed IH&S, reaching 1370 target (again) in June 2019, then channel top in Aug 2019 and again on Jan 8, 2020. Backtested rising channel midline target on Nov 12, 2019 and back to red channel top where it is threatening a breakout. If it doesn’t, it has downside risk to 1490ish, 1424 and 1380. If it does, upside targets include IH&S target at 1308 and .786 Fib at 1735.70.

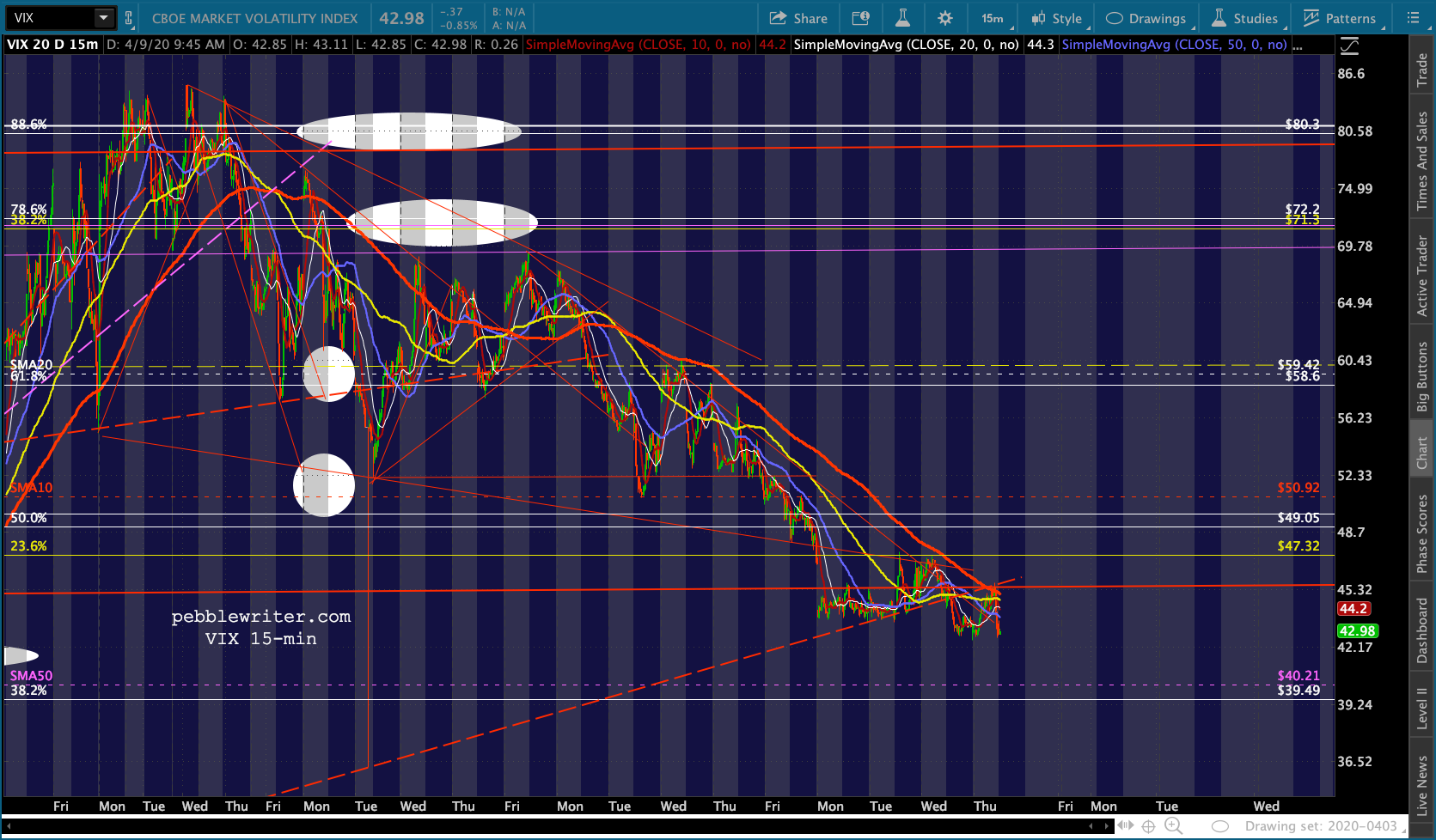

Long VIX: 2/3/20 – Went long in Jan 2020 after survived test of TL from Nov 2017. Has run into resistance at successively lower points on a falling TL from Aug 5, finally breaking out on Jan 27, 2020. Upside targets now include the TL from Dec 24, 2018, favoring 23.38. A breakout above it would open up 25.50 and 33.33.

Short COMP: 2/3/20 – Spent Apr 2 through Oct 25, 2019 trying to break out of falling channels and make new highs. Oct Oct 25 2019, finally broke out for good, testing 1.618 at 9334.14 on Jan 16, 2020. Anything below 9334 opens the door to 8953, 8661 and potentially 8133. But, stops are warranted as COMP has ignored reality time and time again.

Long Bonds: 2/3/20 – ZN reached our downside target of 117’135 on Oct 8, 2018, has since bounced to our successively higher targets, reaching the .886 at 132’100 on Sep 3, 2019. Almost backtested the SMA200 on Dec 19, has since broken out, back to near its Sep high. Targeting 133’070, followed by 134’075 and 135’155.

Shorted TNX in Oct 2018 and have seen it tag successively lower targets until reaching 15.54 on Aug 15, 2019. Long, drawn out series of bounces until Jan 21, 2020 when it broke down again. Reached 1.636 target on Jan 27, 15.54 on Jan 30 and is approaching 14.91 target. If it breaks lower, targets include 14.46 and 14.29. Longer-term, see the 10Y reaching 8.16 around May 2020 and approaching 0.0 in Jun-October 2020.

We’ll continue with a roundup of where we are two months later.

continued for members…

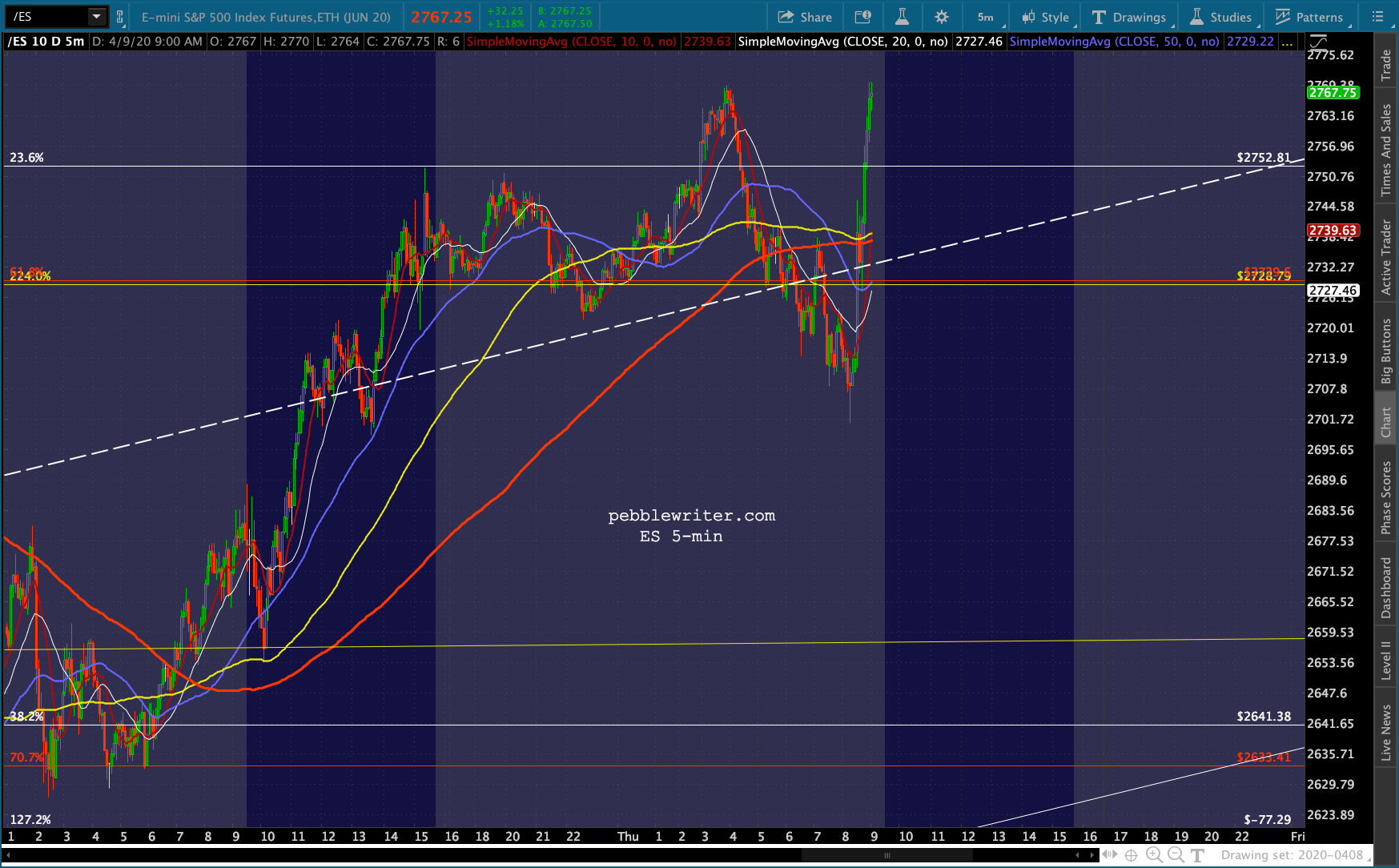

First, our usual daily charts…

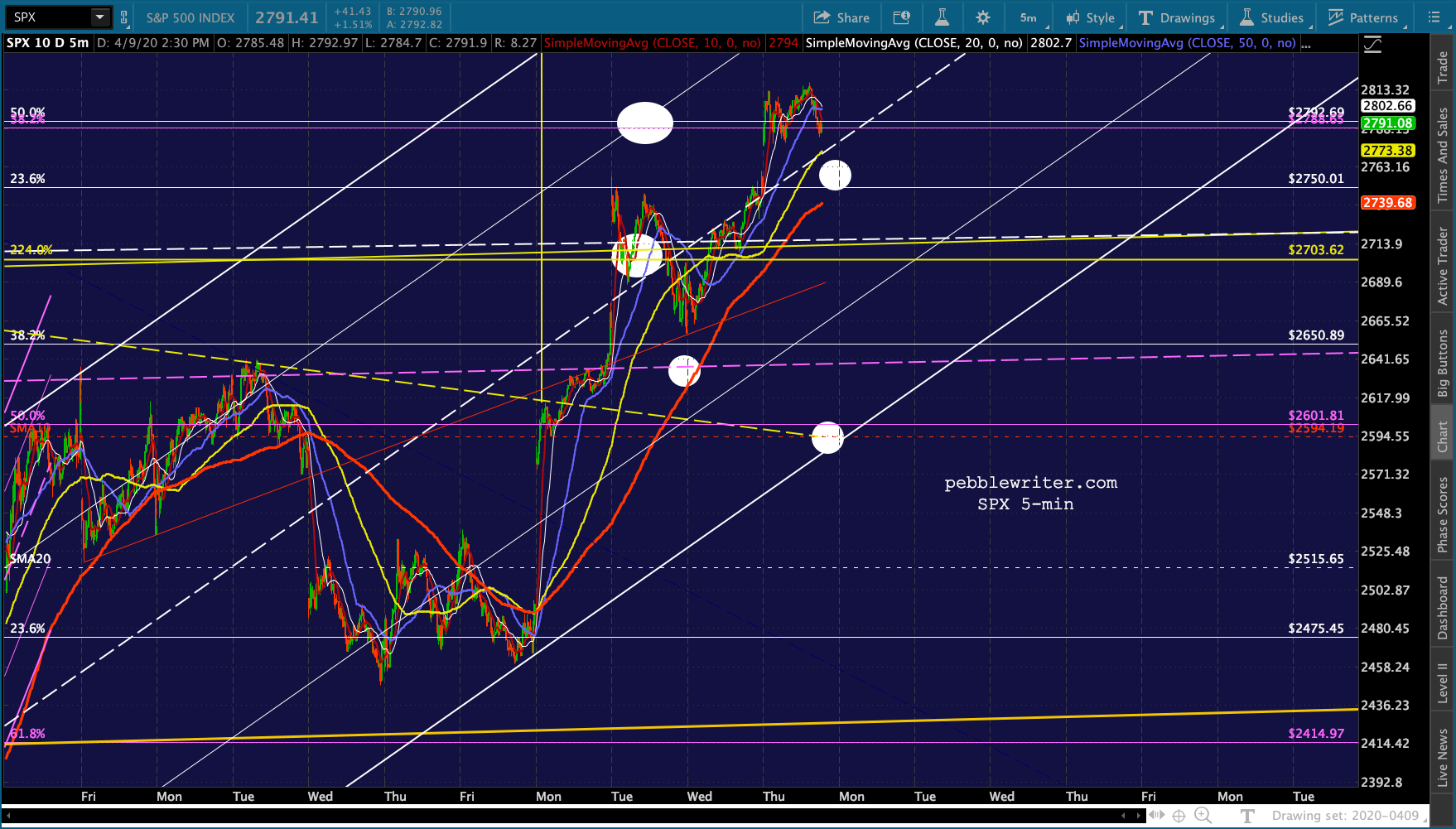

It appears we are not going to get that neckline backtest for SPX/ES – not if the Fed can help it. We’re 84 points off the overnight lows and ES and SPX are now well above their 2.24 Fibs. I probably don’t need to remind anyone that the markets puked – at least initially – the last time Powell spoke.

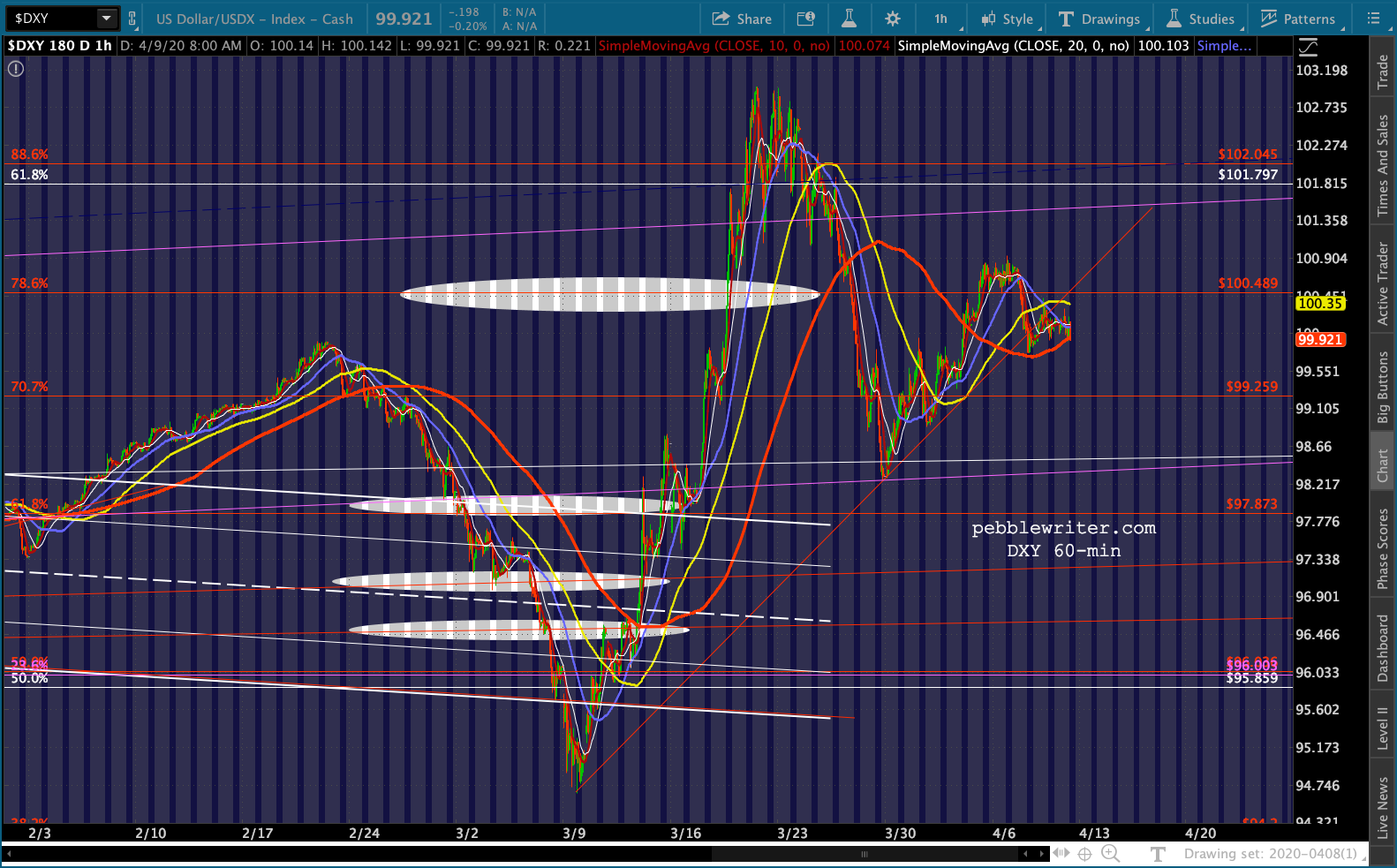

Not surprisingly, the dollar is breaking down this morning. I guess you can print too much money.

Not surprisingly, the dollar is breaking down this morning. I guess you can print too much money. As we discussed yesterday afternoon, this is a signal to stay long on gold, though with tight stops just in case the Fed decides to plug this particular hole in the dike over the long weekend.

As we discussed yesterday afternoon, this is a signal to stay long on gold, though with tight stops just in case the Fed decides to plug this particular hole in the dike over the long weekend.

EURUSD is getting a bounce that probably won’t last. The ECB will obviously have to follow suit now that the Fed has one-upped them.

EURUSD is getting a bounce that probably won’t last. The ECB will obviously have to follow suit now that the Fed has one-upped them.

USDJPY has been oddly quiet – still on the brink of breaking down without actually doing it.

USDJPY has been oddly quiet – still on the brink of breaking down without actually doing it. The big news today was supposed to be the OPEC/Russia virtual meeting where they would announce a huge drop in production that would send oil much higher. The futures aren’t waiting, getting a jump start at 7:30AM.

The big news today was supposed to be the OPEC/Russia virtual meeting where they would announce a huge drop in production that would send oil much higher. The futures aren’t waiting, getting a jump start at 7:30AM.

The odds of a meaningful announcement have not changed. But, that doesn’t mean the futures won’t be ramped higher anyway. Note that CL has coincidentally remained above its SMA10 every day.

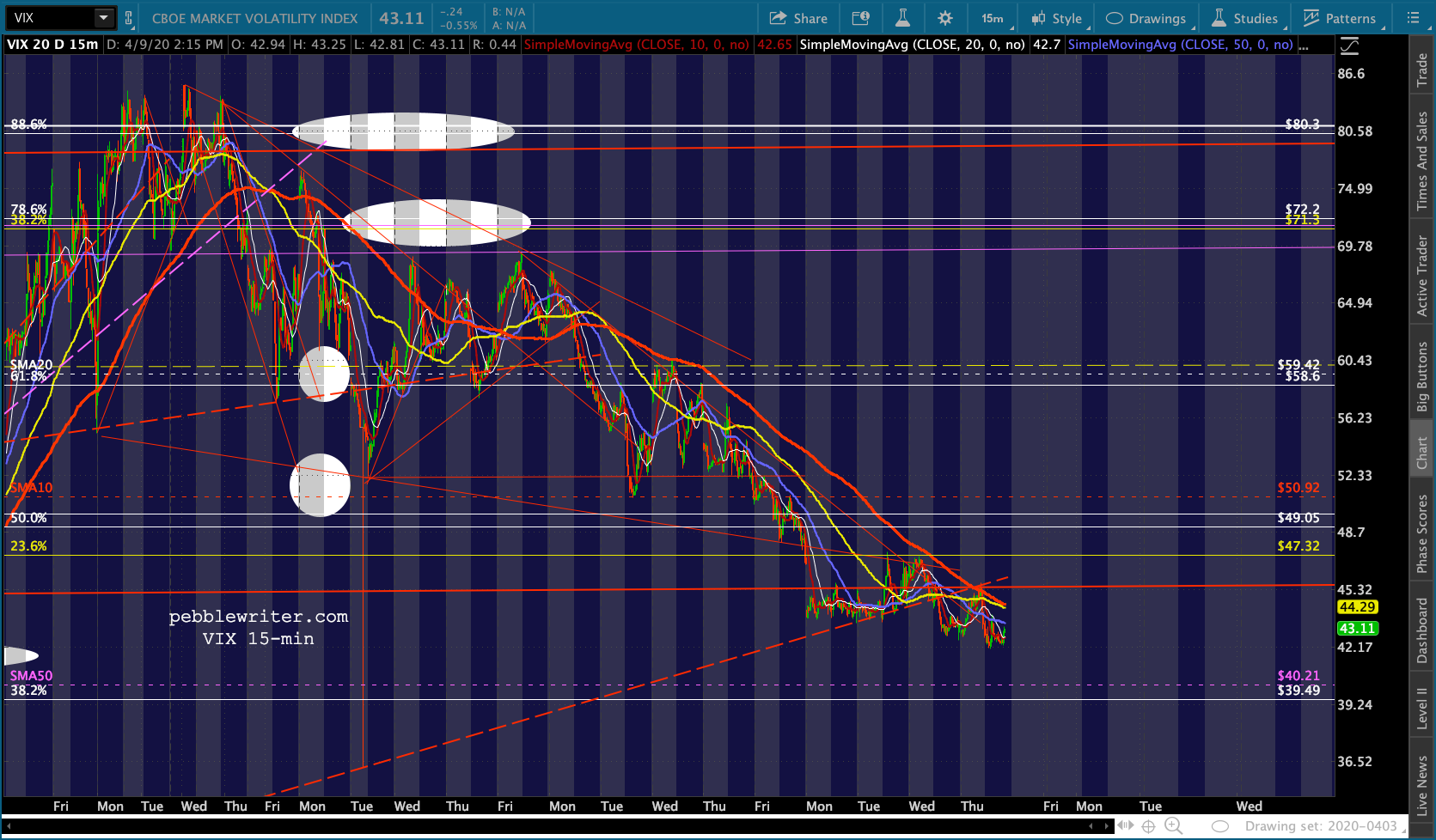

No surprise, but VIX is off this morning. The only surprise is that it hasn’t been hammered any lower. At this level, though, it can easily make new lows if stocks start to backslide – or if they’re simply not rising fast enough.

No surprise, but VIX is off this morning. The only surprise is that it hasn’t been hammered any lower. At this level, though, it can easily make new lows if stocks start to backslide – or if they’re simply not rising fast enough. Last, the 10Y yield predictably shot higher with the Fed’s announcement…

Last, the 10Y yield predictably shot higher with the Fed’s announcement… …which, combined with the 2Y slipping slightly lower…

…which, combined with the 2Y slipping slightly lower…

…has widened the 2s10s beyond the 48 bps threshold where a breakout technically happens. Along with the dollar breaking down (and, the obvious Fed desperation) this is about the only glaringly negative factor for the markets this morning.

…has widened the 2s10s beyond the 48 bps threshold where a breakout technically happens. Along with the dollar breaking down (and, the obvious Fed desperation) this is about the only glaringly negative factor for the markets this morning. A reminder, staying above that white TL is bearish. Rising above the prior highs at 68 bps would be quite bearish.

A reminder, staying above that white TL is bearish. Rising above the prior highs at 68 bps would be quite bearish. I’m going to take a break to listen to Powell and then have a few conference calls. I should be back to finish this post by 1 or 2pm.

I’m going to take a break to listen to Powell and then have a few conference calls. I should be back to finish this post by 1 or 2pm.

UPDATE: 2:30 PM

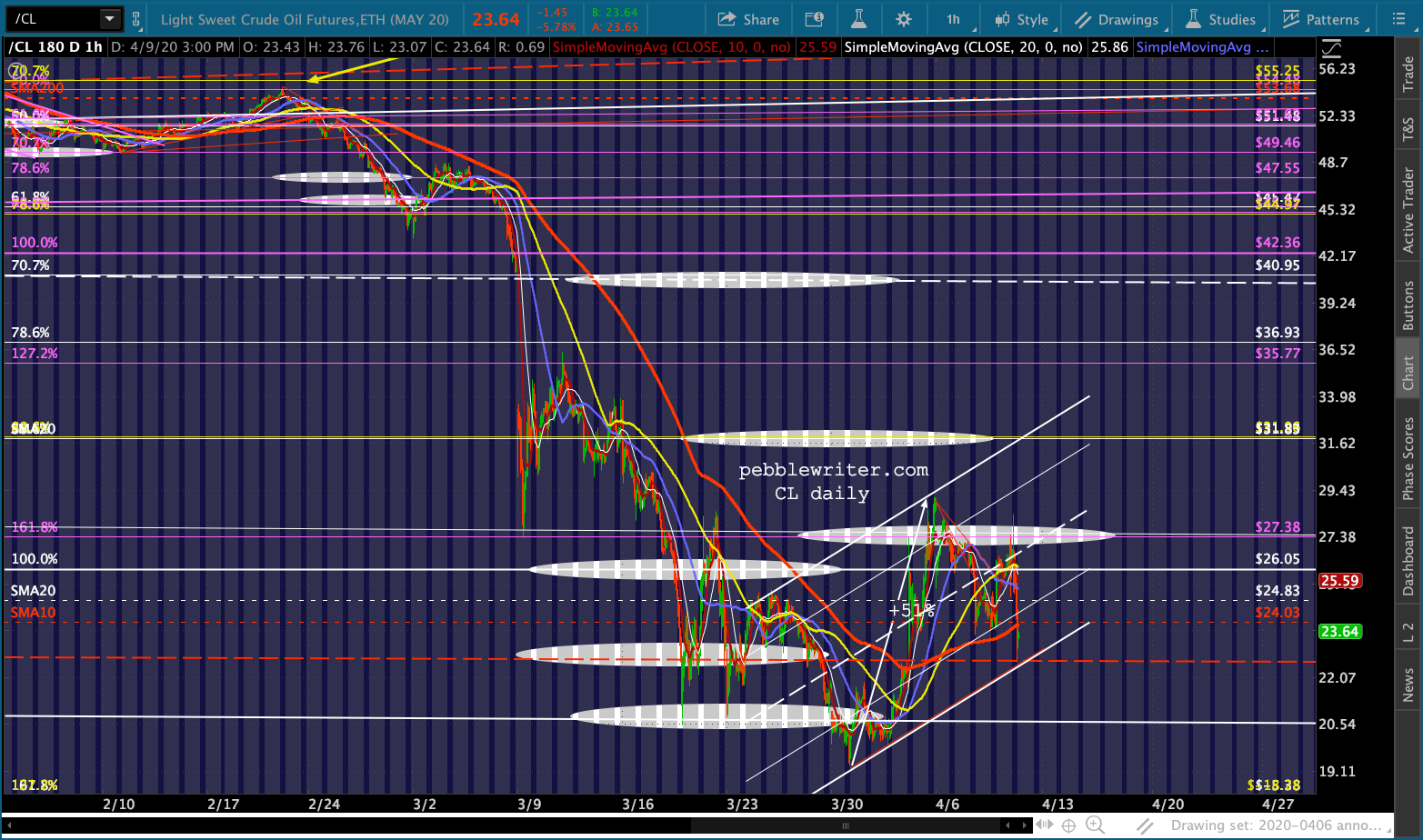

Let’s start with oil and gas, as that’s where the action is following the 10mm bpd cut by OPEC+ which, as we’ve discussed before, won’t make a dent. Since this is a 3-day weekend, the odds are CL and RB will bounce at their TL support here until after cash equities are closed. I expect them to go lower afterwards — but am still looking for CL to remain in the 20-26 range for the time being.

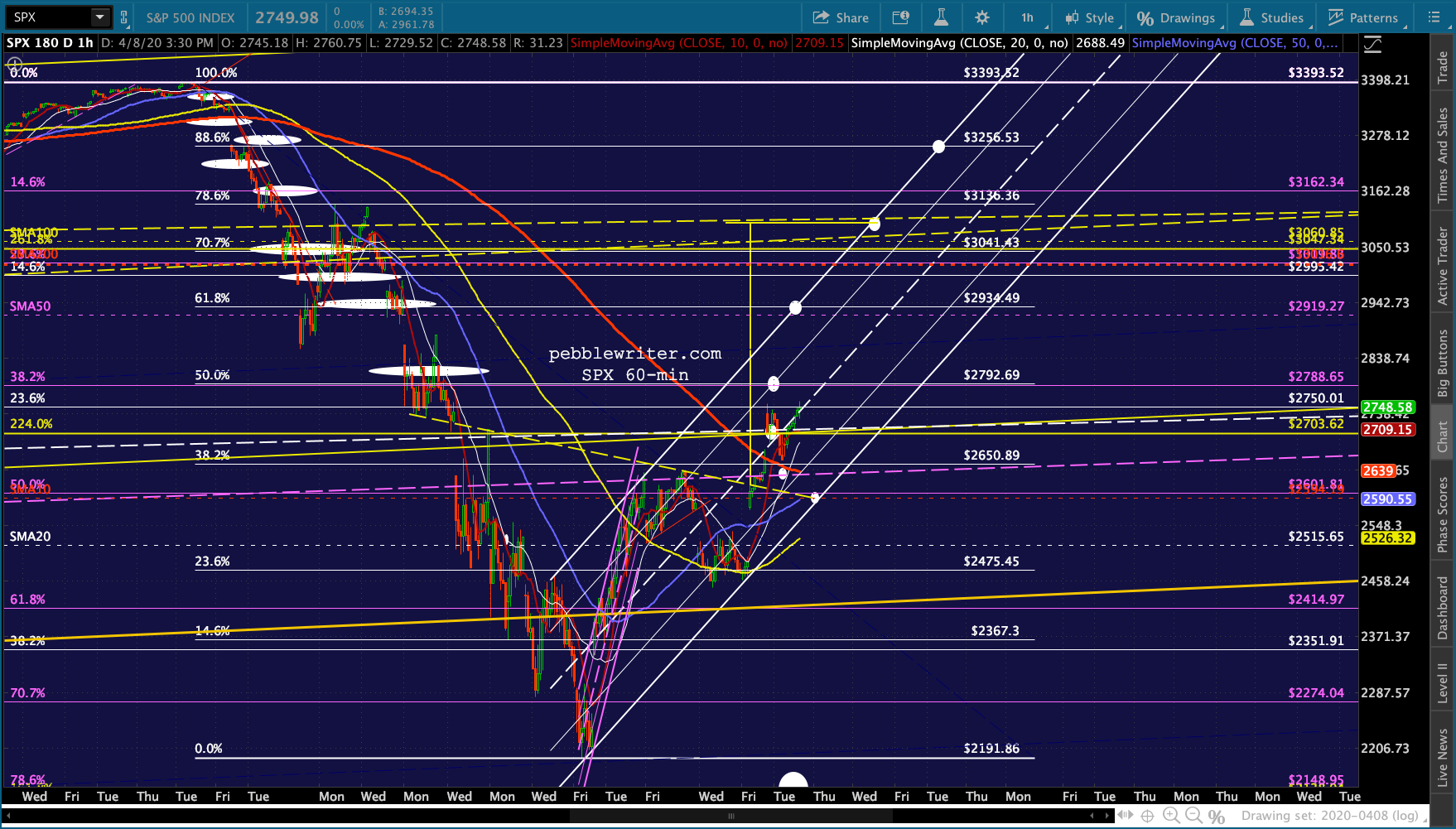

This has taken quite a bit of the bloom of SPX/ES’ rose. Those backtests are looking better by the minute.

This has taken quite a bit of the bloom of SPX/ES’ rose. Those backtests are looking better by the minute.

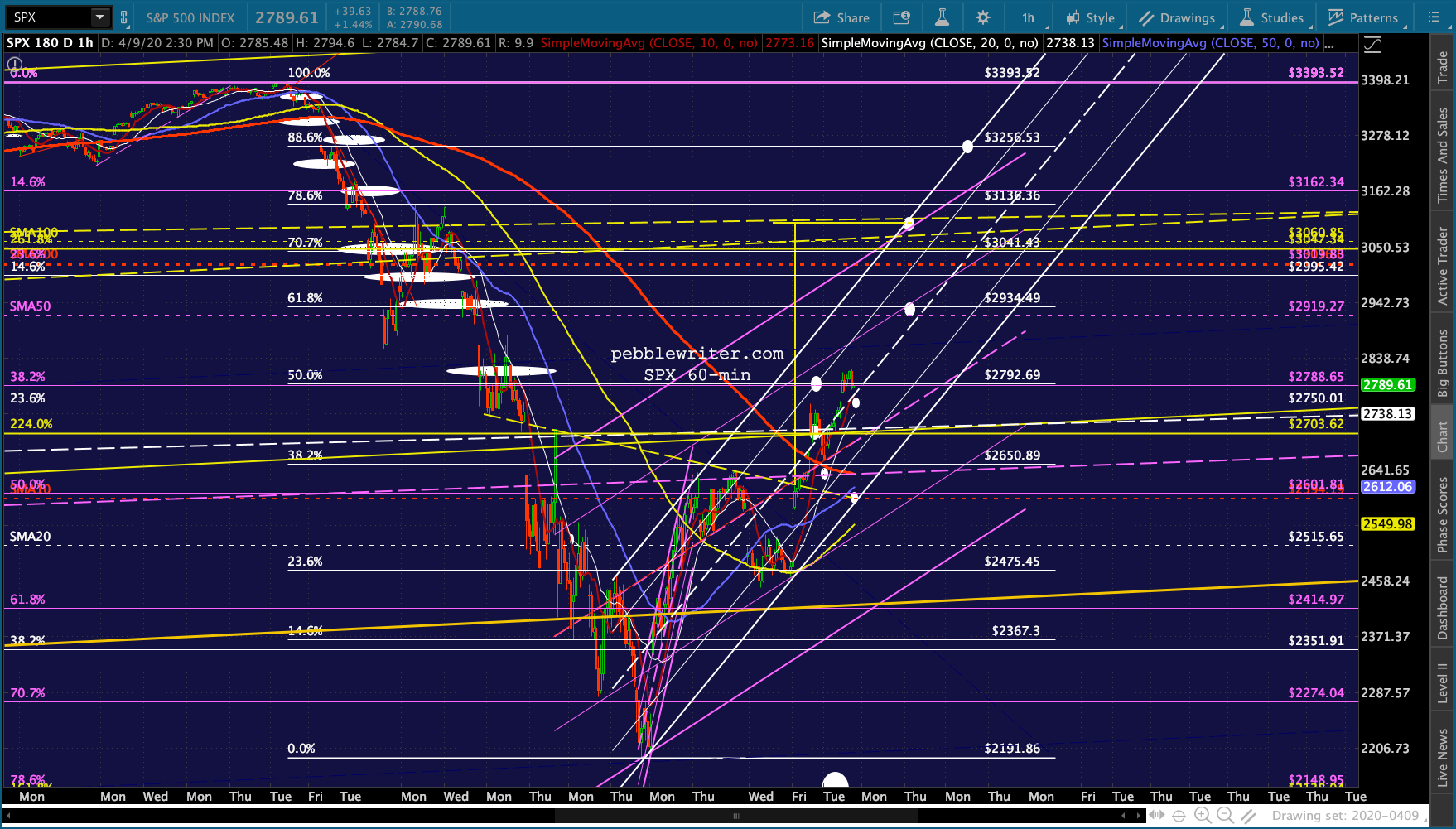

I just noticed this red internal TL on the SPX chart above. If we slap a channel on it, we get something like the purple channel below.

I just noticed this red internal TL on the SPX chart above. If we slap a channel on it, we get something like the purple channel below.

It doesn’t necessarily mean the top of the channel will be tagged up at 3100 – or even that the .618 will be tagged at 2934. But, it might well be what TPTB had in mind as a fallback position in case the Fed’s bazooka misfired – which looks like it might have.

It doesn’t necessarily mean the top of the channel will be tagged up at 3100 – or even that the .618 will be tagged at 2934. But, it might well be what TPTB had in mind as a fallback position in case the Fed’s bazooka misfired – which looks like it might have.

VIX is still in a position to help, but it is slipping higher as we approach the final hour of trading.

$2.3 trillion and Powell’s personal promise to do more if necessary wasn’t enough to raise SPX at least 1% in the face of the OPEC+ disappointment. This is a very bad sign for the bulls. What’s next, equity ETFs?

$2.3 trillion and Powell’s personal promise to do more if necessary wasn’t enough to raise SPX at least 1% in the face of the OPEC+ disappointment. This is a very bad sign for the bulls. What’s next, equity ETFs?

Okay, on to the big picture.

Oil should try but fail to hold the red TL at 22.72. It could drop as low as 20 with a deeper .886 retracement. Anything lower than 19.27 and we’re looking at the 17.12 lows from 2001. Anything above 26 should be followed only with tight trailing stops.

BTW, the TL translates into a rising channel which TPTB will certainly try to keep going if possible.

RB should try to hold .6322 and, failing that, .5765 — assuming the little white channel breaks down. Below that, there’s very little support anywhere. For now, it should remain in the trading range of .5765 and 0.79. Any push above .79 should be followed only with tight trailing stops.

The currencies are a tough case, as we discussed yesterday in the gold post.

The currencies are a tough case, as we discussed yesterday in the gold post.

I suspect today’s Fed action will weigh on DXY, meaning USDJPY could finally drop back below its SMA200 and tag the channel bottom currently at 99ish. But, I just don’t trust the BoJ to leave well enough alone. So, I’d be short USDJPY only on a drop through its SMA200.

If it holds the SMA200, and especially if stocks lose their mojo, I’d look for the BoJ try to outdo the Fed and grind the yen into the dirt — with that upside target at 118.60 still looking good.

EURUSD really should have tagged 1.0592 when it had the chance I still expect it to but would be willing to play along on the upside if it pushed through its SMA200.

This leaves DXY in no man’s land, with a nice downside target at 94.20 and upside target at 103.82. For now, I believe the momentum is to the downside with a backtest of its SMA200 at 98.08 the most likely near-term target. A drop through it would mean stay short, while a bounce should be played with tight trailing stops.

IMO, the bond market is dead for the time being. ZN still has upside potential to 144’195 and TNX downside to 1.54 – that’s .154% and ultimately zero. With debt piling up so fast, it’s no longer an option. It has to happen, and the Fed will make sure it does.

Now, the easy part: stocks. Just kidding. There’s nothing easy about the equity picture because we just don’t know how crazy the Fed might get if they don’t get the rally they so desperately want. And, speaking of unknowables, what about COVID-19?

Now, the easy part: stocks. Just kidding. There’s nothing easy about the equity picture because we just don’t know how crazy the Fed might get if they don’t get the rally they so desperately want. And, speaking of unknowables, what about COVID-19?

The daily growth rate in both cases and deaths has declined: a 10-DMA of 11.8% in cases and 19.2% in deaths. This means we’re only going to hit 500,000 cases by Easter instead of nearing 1,000,000. Deaths probably won’t reach 20,000 until Monday the 13th and might not reach 100,000 until late April – if then.

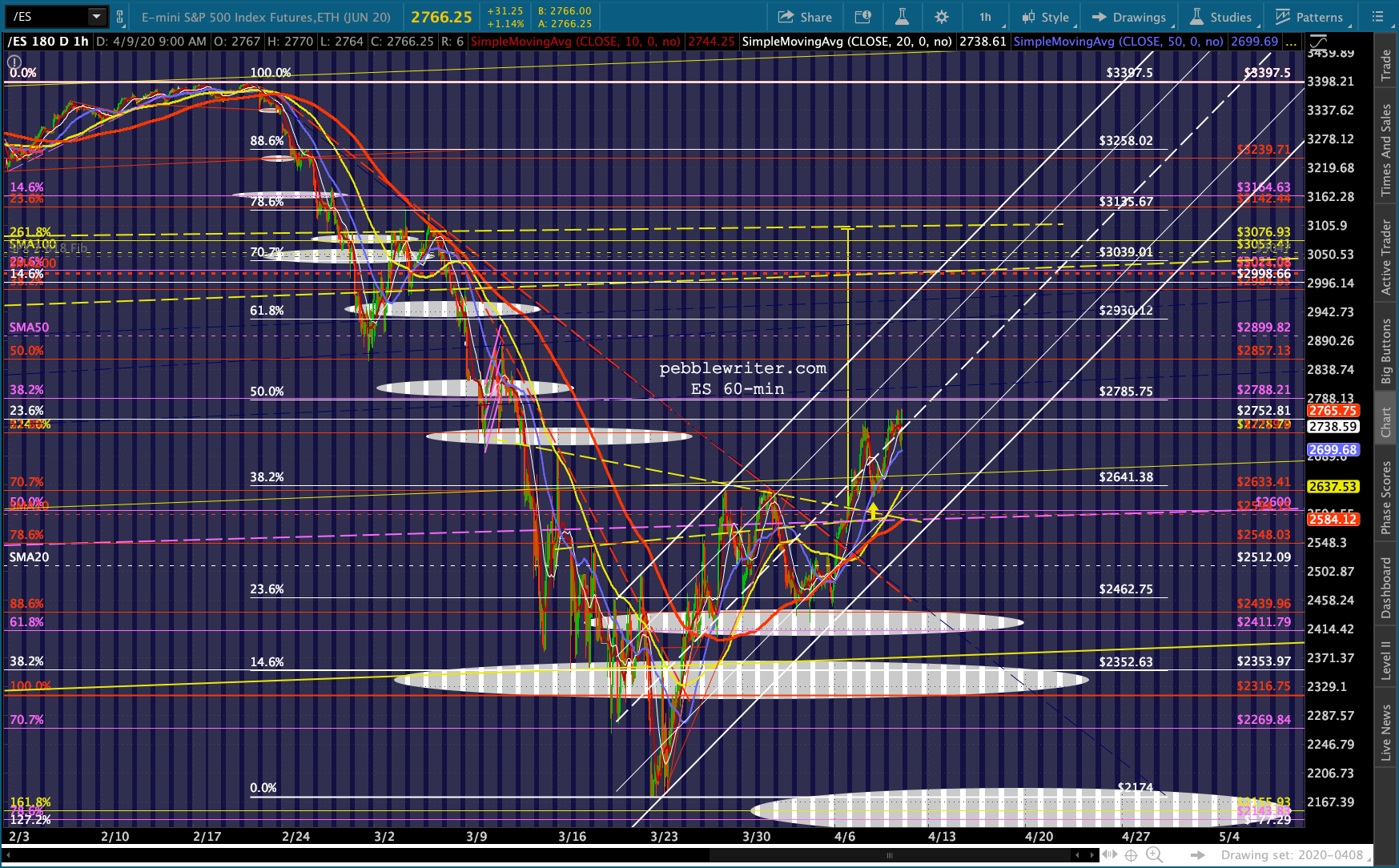

I still like the idea of ES 2155 and SPX 2138, but if the slowdown in COVID-19 deaths holds, it’s going to be hard to overcome Fed actions. I suppose I’ll hedge here — wanting to be short below the purple TL at SPX 2640 (ES 2585) and long above it.

As far as the upside goes, its the .618s at ES 2930.12 and SPX 2934.49 and the IH&S targets at ES and SPX 3100. If I had to take a position going into the weekend, I’d be short. But, I’d rather sit on the sidelines and see how things shake out.

Note that the DJIA has backtested its own 2.24 and, for now, failed to retake it. This is technically bearish. But, the DJIA is the all-time champion of manipulation. So, short it if you like but don’t be surprised if we get a gap up above 23781 at some point. I’ll translate the above onto the Current Forecast page tomorrow. Remember, markets are closed.

I’ll translate the above onto the Current Forecast page tomorrow. Remember, markets are closed.

Have a great weekend everyone. Stay healthy and enjoy a Happy Easter, Passover, or whatever you do to celebrate just being alive.