UPDATE: Sunday night

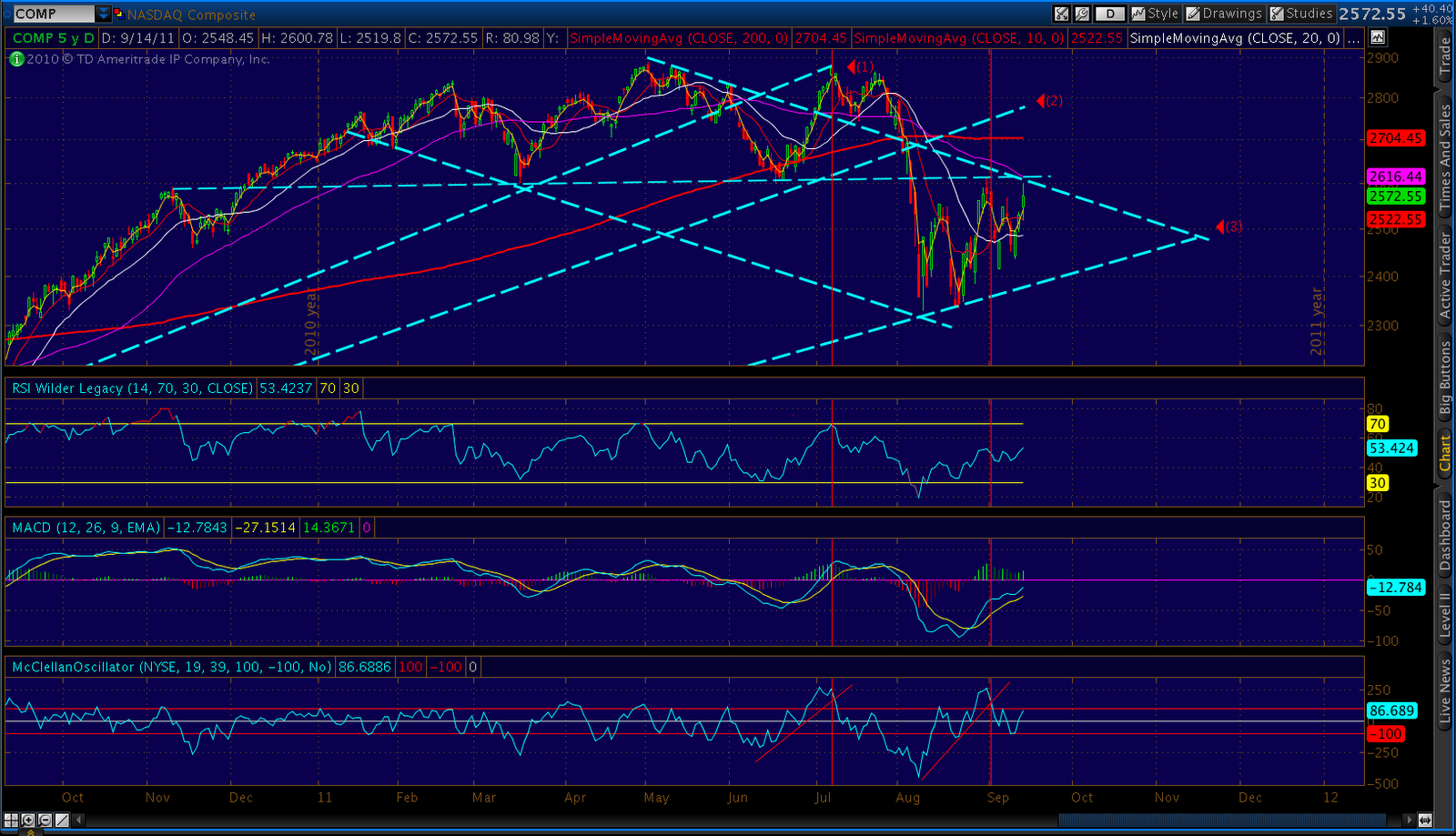

A quick update on our 2011 v 2007/8 comparison chart:

Here’s a close-up. On Feb 27, 2008,SPX had climbed 120 points off the bottom (24 days) and was 8 points away from establishing a new higher high. Instead, it fell 131 points over the next 13 trading days.

As of this past Friday, we have climbed 120 points off the bottom (27 days) and are 10 points away from establishing a new higher high. If this doesn’t mean anything to you, go back up and read the last paragraph again.

A 130 point drop from here, BTW, would take us to 1090. All we need is 1145, however, to complete the head and shoulders pattern discussed below with a 1040-1050 target.

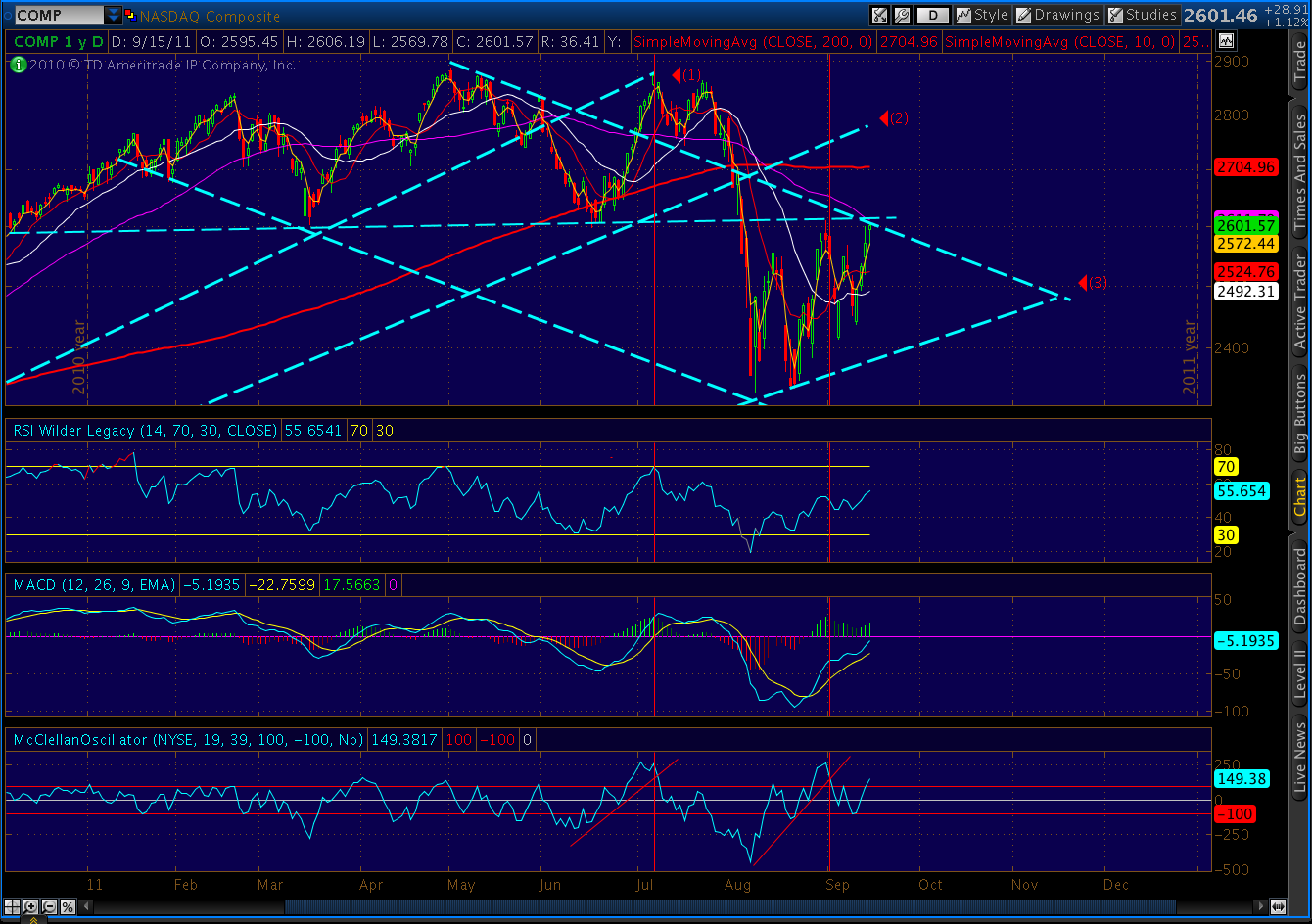

And my last chart for the weekend — the comparison between the past 5 weeks and the overall 2011 topping pattern. Eerily similar.

Some believe that Greece and EUR problems are baked into current prices, that we’ve seen the bottom. I say the problems are just beginning to get much worse. I think the only thing baked into prices is the belief that the Fed can wave its magic wand and bring back the bull. I believe there will be a lot of disappointment in the weeks ahead.

I think the huge rally engineered over the past 5 weeks was a do or die effort by market makers to salvage their books after massive losses sustained in the 250-point plunge. They got through OPEX alive, and will position themselves better in the coming leg down.

ONE LAST COMPARISON…

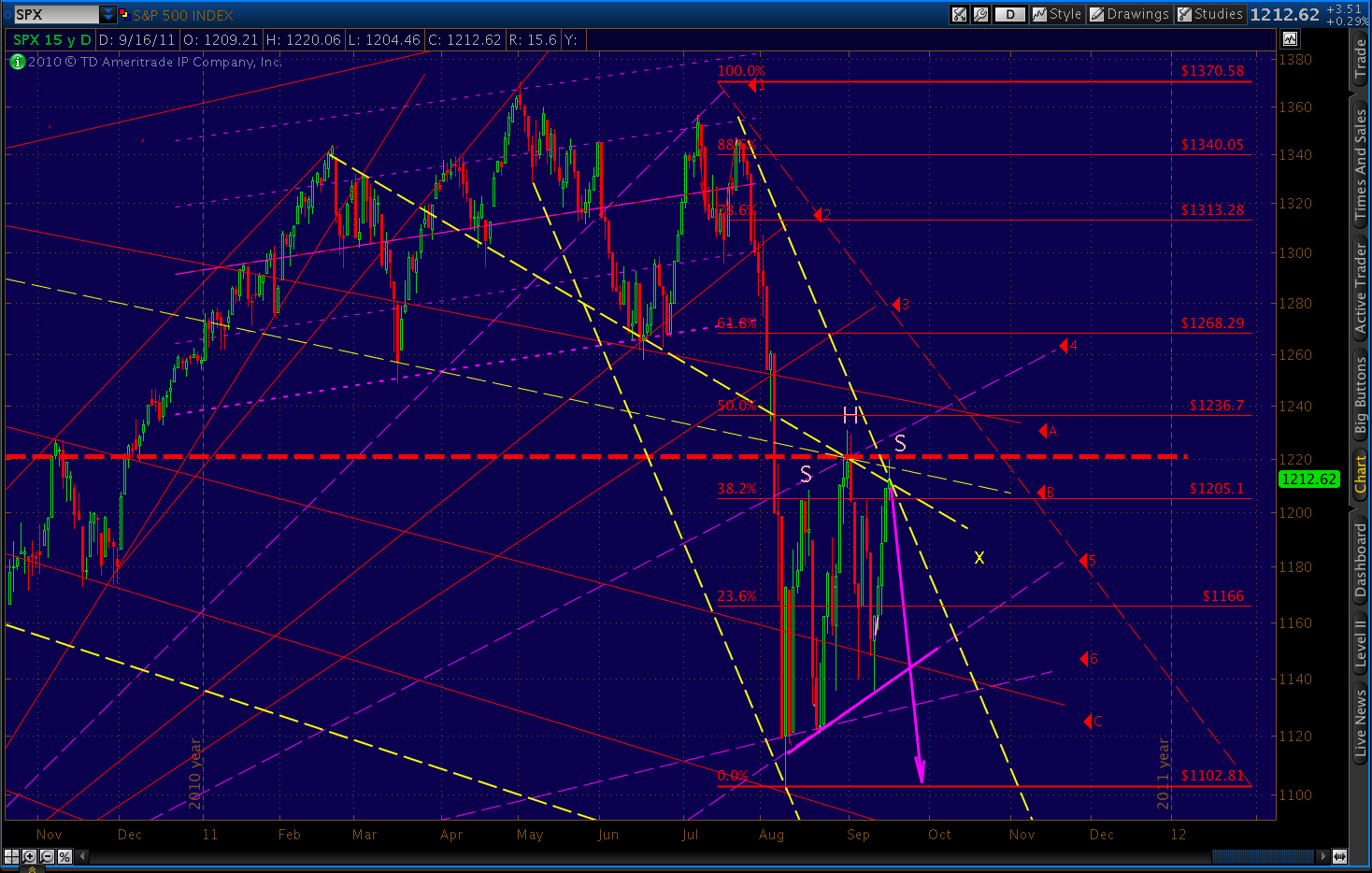

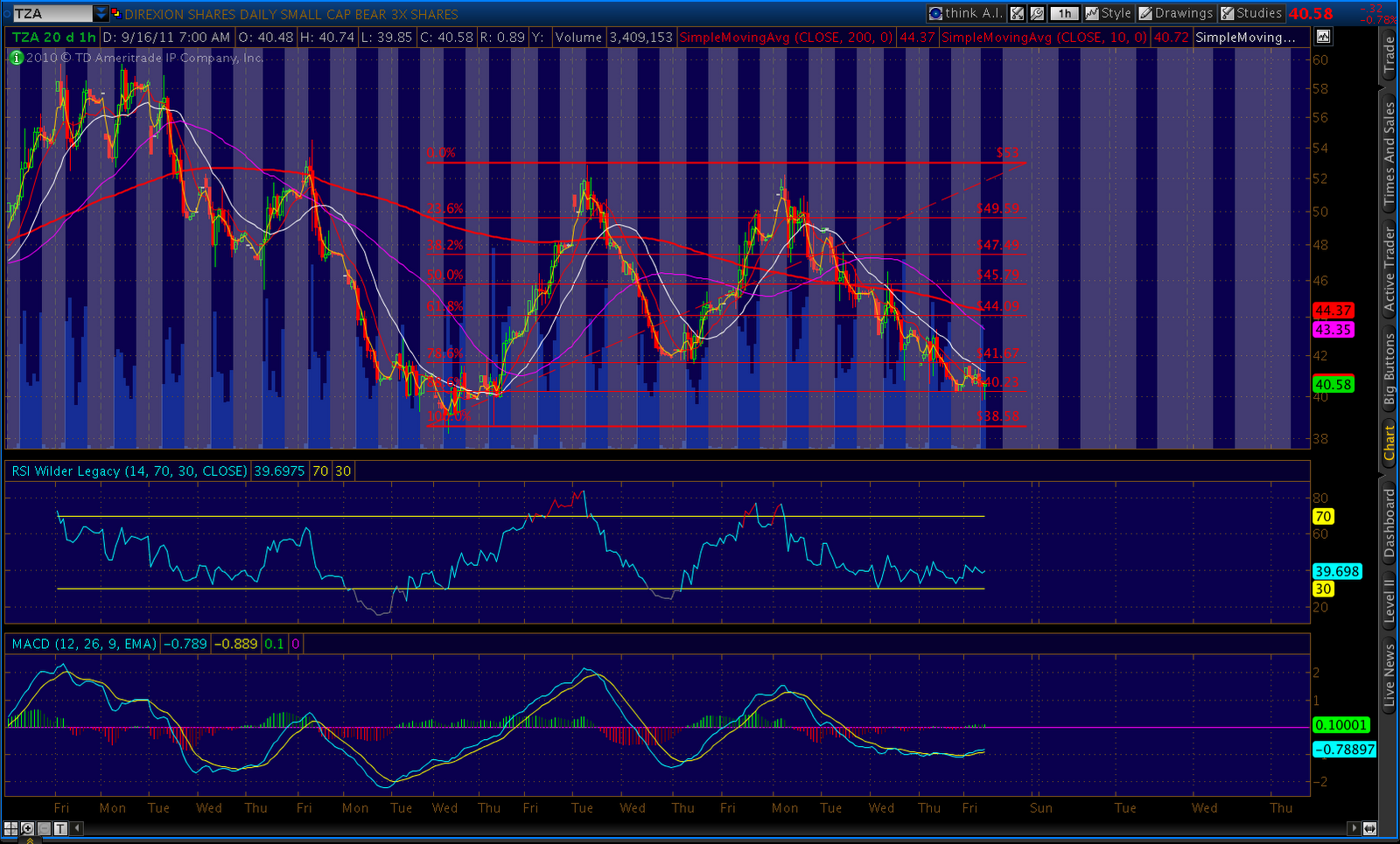

Sorry, couldn’t resist this one. Maybe it’s nothing, but the bearish Bat pattern we completed Friday reminded me of similar patterns I’d seen on dates I consider equivalent. The pattern shapes vary, but they all end with a .886 Fib retracement. You decide.

|

|||

| Bat completed 9/16/2011 |

|

|

| Bat completed Feb 26, 2008 |

|

| Bat completed July 21, 2011 |

FRIDAY – EOD:

Long, long week for us bears. But, the day went well. And, next week should be a lot more fun.

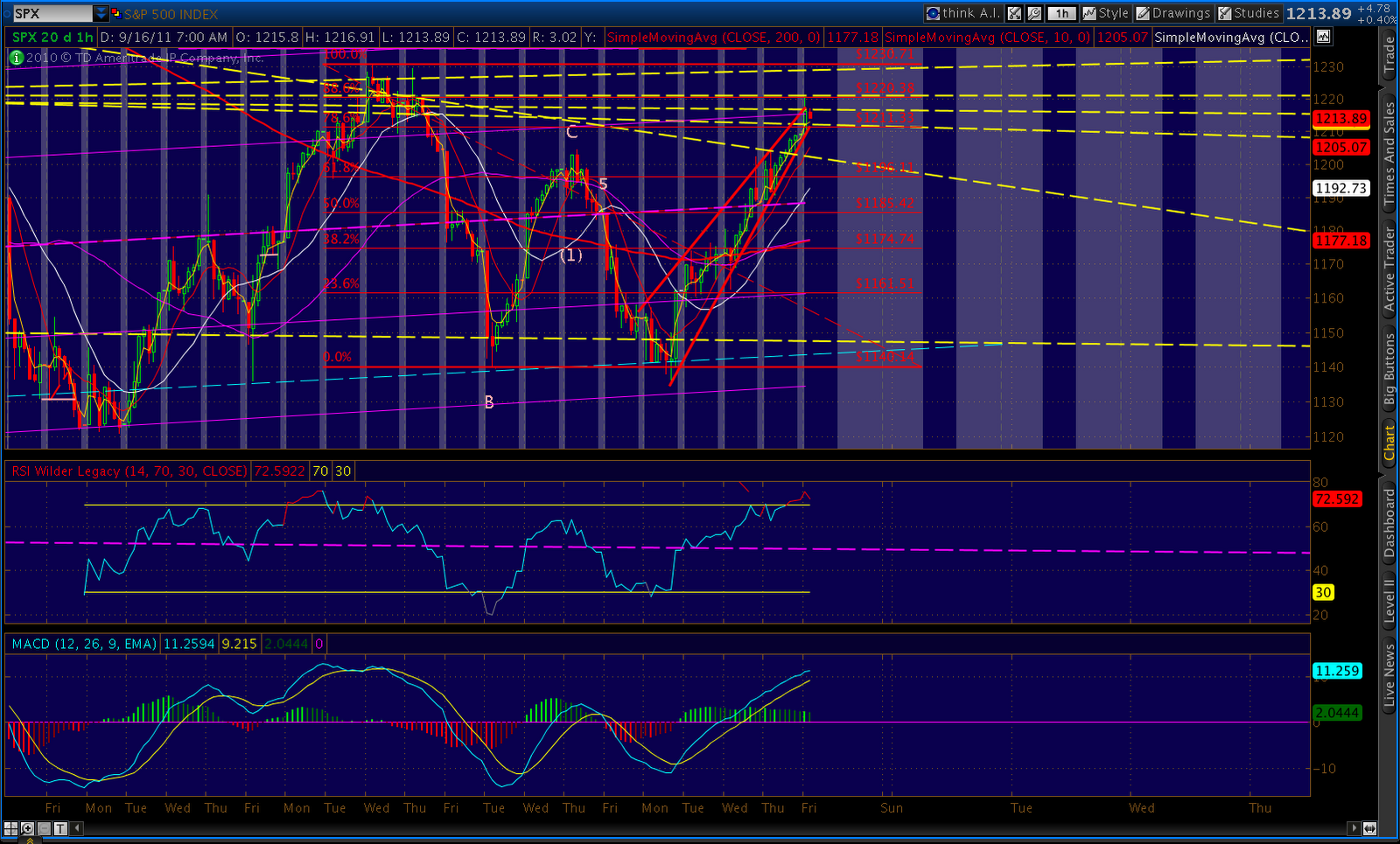

As someone recently told me, you can’t make this stuff up (no matter how often I try.) For instance, check out the 2 standard deviation regression channel from the Aug 9 low.

The 2nd line from the top is the +1 std dev line. It landed at 1220 today. As in…the high of the day. This would be easy to ignore if not for the fact that such a channel guided the Feb – Jul 2011 top. A final touch at the +1 std dev line on July 7 marked the beginning of the end.

UPDATE: 2:45 PM

A quick look at the big picture. Check out the Big Red Line. Looks like a backtest, no?

A closer look:

UPDATE: 12:50 PM

Very interesting Butterfly completing on Nasdaq 100 (NDX.)

The 5 year daily chart shows it’s backtesting a three-year trendline.

UPDATE: 12:40 PM

SPX just a couple bucks from an intra-day Gartley completing. The .786 is just over 1216.

UPDATE: 12:00 PM

ORIGINAL POST: 10:15 AM

SPX completed a Bat pattern at the .886 Fib level. It’s not terribly well-formed, with point B being too high and C too low. But, the .886 Fib retrace is right on the money. It roughly corresponds to the +1 regression channel line (dates back to Aug 8) as well as Trend Line B that saved the bears’ bacon back on Aug 31 and Sep 1.

This rally has gone 30 points past the highest level I thought it was capable of; so, I call this the top with a great deal of trepidation. However, similar reversal patterns are setting up across the market.

UPDATE: EOD

I’ve redrawn the channel to include today’s market action. The existing line (w/ shadows) would have accommodated yesterday’s rise, but not today’s. Channels can and do shift all the time, but this one caught me off guard.

I believe the MCO indicator I discussed last night is still in play. The indicator has risen above +100, which is typically a reversal signal.

Also, a fan line that didn’t even earn a label the last time I drew these appears to have come to the bears’ rescue. I’ll label it X for now.

I’m distressed (and poorer) at having called the top a few days early. This same thing happened at the end of the Feb – July topping pattern. On Jun 24, when seemingly everyone was calling for a flash crash, I called for a rally from 1267 to 1330 within the next 5 trading days. It happened in 4. I happily took my short position, only to see the market rally another 40 points before peaking.

In that case, too, the market rallied to the +1 regression channel line instead of the midline as I had been expecting (based on the 2007 analog.) We are within a point or two of the midline right now.

If you’ve read my stuff for very long, you know that I’m usually early. I’m not sure why. But, I’ll spend this weekend thinking about the comparisons between this miss and the one from July 7.

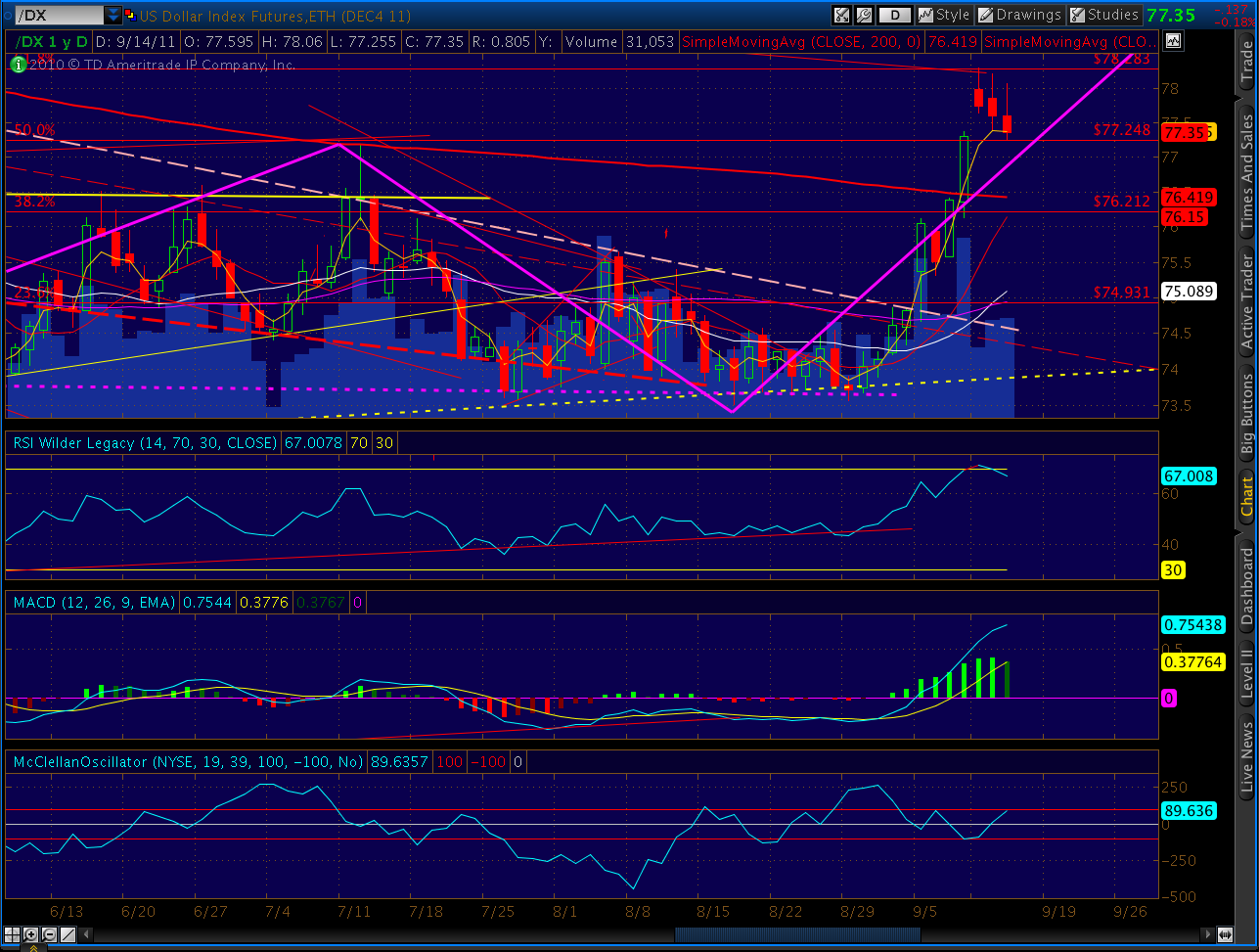

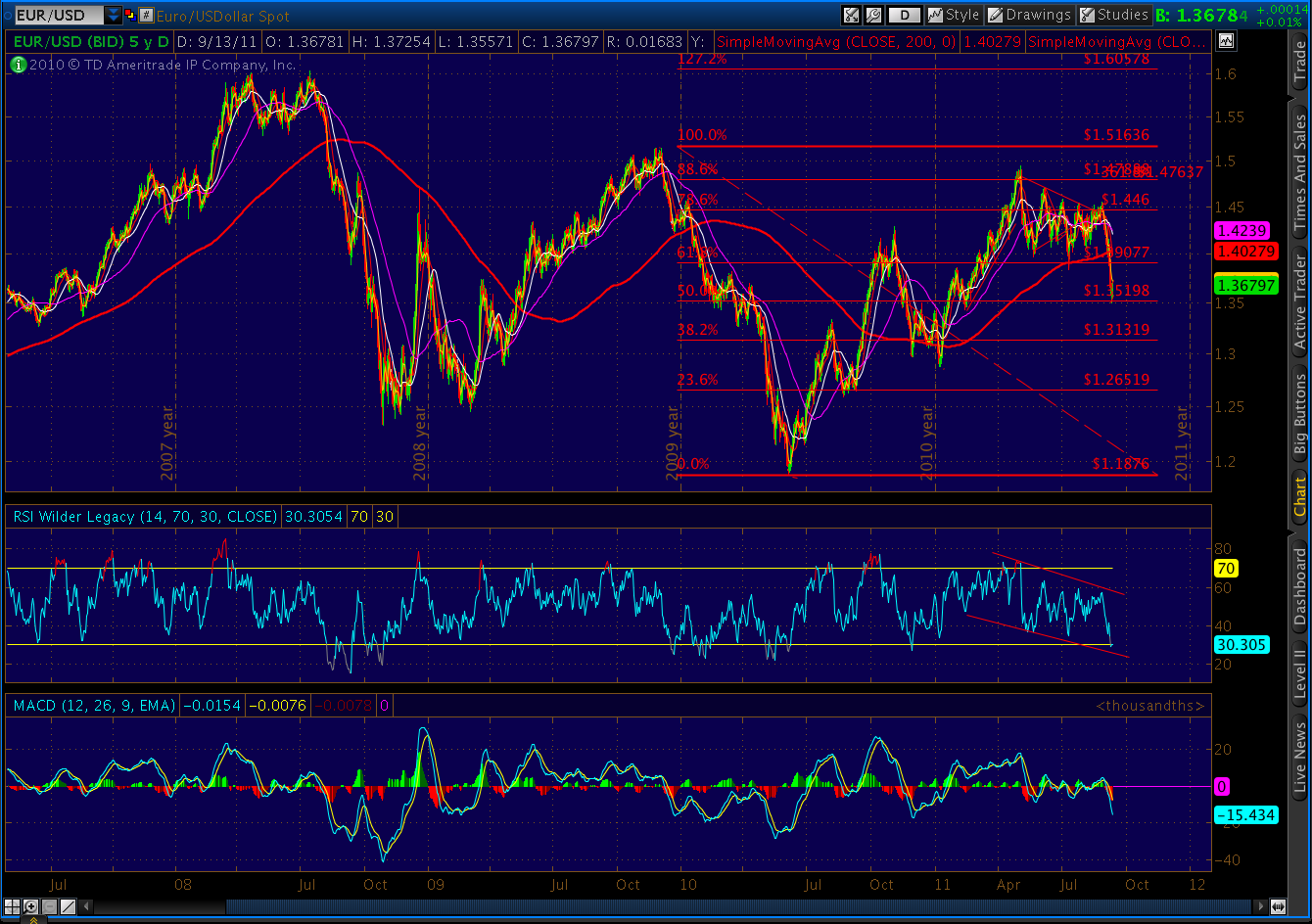

Last, DX is only .17 from its 200-day moving average. The .382 Fib level is only .19 below that. I see absolutely no possibility that we won’t get a huge bounce off one of those important support levels.

In closing, we are going down. OPEX (actually, quad-witching) might delay things a day or two. But it will be soon, and it will make your head spin.

ORIGINAL POST: 2:20 PM

Apparently, the channel I’ve been expecting to hold this advance wasn’t up to the task. I’m nominating a different candidate (the purple dashed line instead of the yellow.)

Compare it to the lines I drew on last night’s post for COMP.

Here’s how it’s done so far today:

We’ll discuss more later. Right now, I’m analyzing this Euro mess.

On a day when Marketwatch warns…

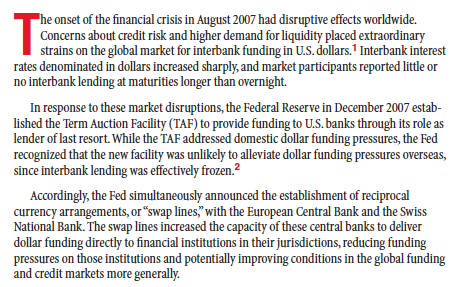

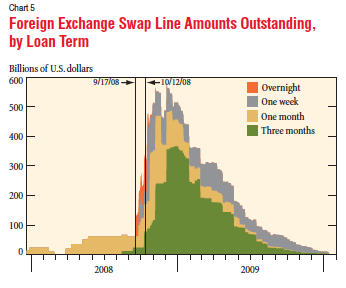

We first started this back on December 12, 2007. From the NY Fed’s research publication Current Issues in Economics and Finance, Apr 23, 2010:

We took Euros and Swiss Francs and Japanese Yen and NZ Dollars that no one wanted and gave them US Dollars in exchange. These central banks could loan these valuable greenbacks to their financial institutions who would (theoretically) lend them out to (theoretically) worthy borrowers — keeping liquidity alive and jumpstarting the economy. It would also (theoretically) put a floor under the foreign currencies’ values and keep them viable in the global finance marketplace.

Back then, financing had dried up because several large banks, investment banks and a hedge fund in insurance company clothing (AIG) had failed or were in the process of failing. They were failing because of a newly developed but widely circulated idea that loans ought to be backed by adequate collateral. Those that weren’t probably weren’t worth all that much.

Today, financing in the Euro zone has dried up because the Euro zone, itself, is in the process of failing. Some foreign and Euro-based investors are convinced that making loans there is throwing good money after bad. As I blogged a few days ago:

Deposits by financial institutions in Germany off 12% since Jan ’10, 24% since Sep ’08. France, oddly, not as bad at 6% and 14%. Italy off 1% in retail dep’s (serious money’s already gone), 13% ($100B) by financial insitutions. In other words, banks don’t trust each other.

Fitch says US Money Market funds cut lending to Euro banks 20% in last 3 months (Germany-42%, French-18%, Spain and Italy 97%.) At $1.5 Trillion, MMF’s are a vital source of funding.

The ECB can’t make up for all that, but it’s trying. Italy – EUR 85B in three months; Greek and Ireland – EUR 100B each in August; Portugal – EUR 46B in July; Spain – EUR 52B in July. Total lending so far = 7X Euro zone central banks’ combined capital.

Total exposure in loans from other Euro countries to PIGS: $1.7 Trillion. Lots more in guarantees and derivatives.

Total swaps outstanding under the 2007 program peaked at $580 billion in December 2008. At the time, this represented about 25% of the Fed’s total assets. The program was officially terminated in February, 2010. As the April 23 Fed article points out, market conditions had improved and financial strains had abated.

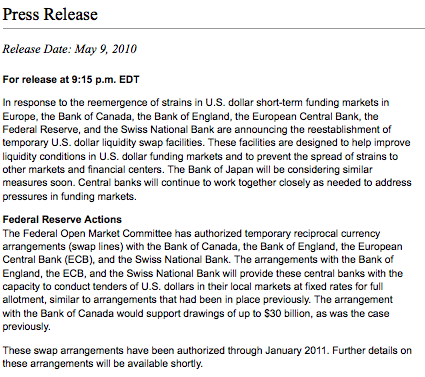

Two weeks later, on May 9, the Fed announced…

Apparently the system wasn’t quite ready to stop sucking the liquidity teat. The ECB immediately drew down $5.5B, bumping that to $500B in both August and October 2010 and finally zeroing it out in March 2011.

All was fine until last month, when the Swiss National Bank unexpectedly drew down $200B. It was followed the next week (Aug 24) by the ECB and another $500B.

Then, today’s news, and a 20-point SPX rally. Is this really that great a development? Let’s look at how both the dollar and the stock market performed following previous manipulations.

SPX DX

December 12, 2007 1512 75.92

low/high next 3 days 1445 77.49

low/high next 35 days 1270 77.85May 9, 2010 1164 83.07

low/high next 3 day 1156 85.57

low/high next 30 days 1011 88.91Aug 24, 2011 1208 73.72

low/high next 3 day 1121 74.55

low/high next 35 days 1121 78.30

(so far)

Bottom line, each intervention did diddly squat for stock investors. Today’s rally isn’t justified.

But, more importantly, we need to consider the more serious implications. The Euro zone is obviously on life support. The entire scheme is hanging by a thread, and we’ve been brought in to stitch it back together. We, who just last month were in danger of defaulting on our own debt.

The Fed’s balance sheet, only $885 billion in Dec 2007, has ballooned to nearly $3 trillion. And, every time we bail out another entity, whether it be Bank of America, General Motors or the ECB, we minimize the effect markets have on lending and borrowing and saving. We impose a rationale which, in the long run, not only delays the inevitable but exponentially raises the stakes.

And, what happens when one of these sterling borrowers goes under? The Fed article goes to great lengths to explain that we’re not taking crappy foreign loans as collateral. No, we’re simply taking the currency backed by lenders who make the crappy foreign loans — loans that no lender in his right mind would make. So much better, no?

The Fed Reserve article (published when the Fed thought the worst was behind us) details what happened the last time we did this.

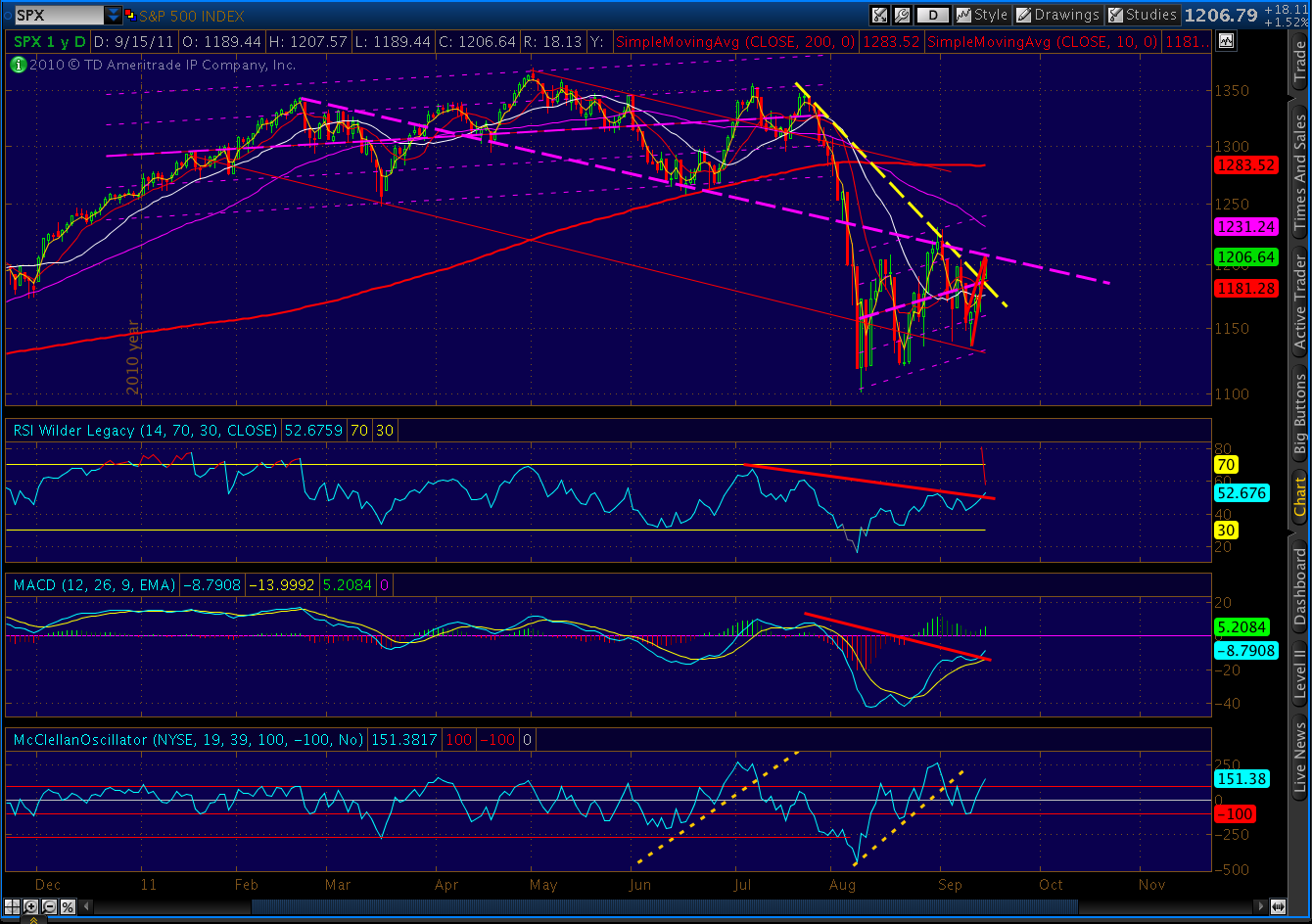

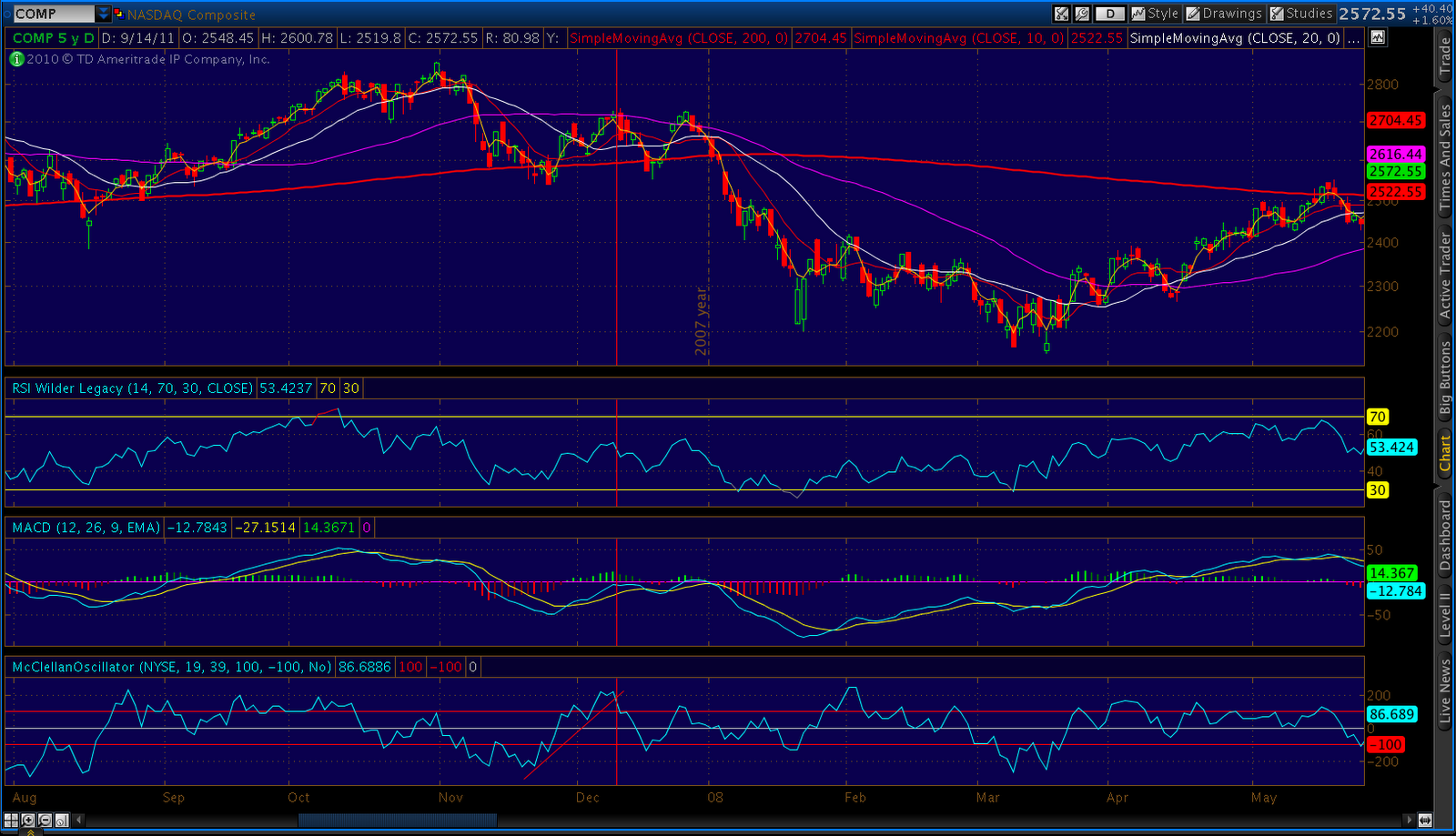

The McClellan Oscillator has been around for a while. As Stockcharts.com says, it puts momentum in the AD line. I first noticed a particular pattern while looking at the 2007 comparisons to 2011 in SPX.

In short, when the indicator bounces sharply higher after a distinct low, draw a trend line that connects the low to the subsequent dips. When it breaks that trend line, there’s a pretty good chance we’re putting in a high.

It works best when the starting point is relatively low, say -200, the number of touches is 3 or more, the shape of the indicator is very convex relative to the trend line, and the indicator makes it to +200 or so.

When each of these conditions is met, I’ve yet to see an instance where it didn’t result in a pretty healthy drop.

Here are a few examples from the past five years using COMP.

|

|||||||||

| Dec 07 |

|

|

| Nov & Dec 09 |

|

||

| Jun 10 |

And, the latest examples… Note the most recent case corresponds to the Aug 31 interim high. The previous one belongs to the Jul 8 high, which I view as the beginning of the end of the latest bull market.

In both cases, the market high was quickly followed by another slightly lower high that registers as a (post-trend line break) lower peak on the MCO indicator. It typically comes in at around 100.

|

| Jul and Sep 2011 |

In many previous cases, it’s this second, lower high which marks the start of the most dramatic phase of the downturn. It was certainly true in 2007 and in Jul 2011.

I’ve thrown a few other goodies in that last chart. I’ve drawn in another way of looking at the downward sloping channel. Beginning with the pattern high, it intersects with a horizontal support line which also happens to be the broken neckline for the gigantic head & shoulders pattern that just played out.

Here’s the view from 20,000 feet. Note that the three upward sloping TL’s are actually fan lines originating at the Mar 09 lows. The old adage with fan lines is “three strikes and you’re out” which means, the next drop below a fan line will be the most memorable.

|

| Fan Lines |

So, where does SPX stand with all this?

Should be a memorable next few days.

UPDATE: EOD

The Euro Mess is getting out of hand…

Deposits by financial institutions in Germany off 12% since Jan ’10, 24% since Sep ’08. France, oddly, not as bad at 6% and 14%. Italy off 1% in retail dep’s (serious money’s already gone), 13% ($100B) by financial insitutions. In other words, banks don’t trust each other.

Fitch says US Money Market funds cut lending to Euro banks 20% in last 3 months (Germany-42%, French-18%, Spain and Italy 97%.) At $1.5 Trillion, MMF’s are a vital source of funding.

The ECB can’t make up for all that, but it’s trying. Italy – EUR 85B in three months; Greek and Ireland – EUR 100B each in August; Portugal – EUR 46B in July; Spain – EUR 52B in July. Total lending so far = 7X Euro zone central banks’ combined capital.

Total exposure in loans from other Euro countries to PIGS: $1.7 Trillion. Lots more in guarantees and derivatives.

UPDATE: 4:05 PM

Whew! That was close, but we closed at 1188.67 — safely back within the descending channel. So, today’s action will go down as a shadow — a reversal at just past the .886 Fib level. Importantly, it leaves the completed H&S; pattern intact (or, we might get a new, larger one in the bargain.)

We did get a slight bump up in the MACD, but the same happened on July 22. The daily RSI trend line is intact, and MCO reached a new intra-day high today — an important indicator that I’ll hopefully have time to touch on later.

EOD for DX, with a reversal right at the lower Fib level. Keep an eye on news out of Euro zone through the night.

UPDATE: 3:55 PM

DX reversed where we thought it would, started the SPX reversal. Spitting distance from 1190…

UPDATE: 3:20 PM

We’ve overshot the .886 Fib level by a couple of points at 1198.63. It just happens to coincide with the descending channel line if redrawn to include the shadows from the Aug 31 and Sep 1 candles. Will today’s runup be a shadow? We have about 40 minutes to get back below 1190.

UPDATE: 3:00 PM

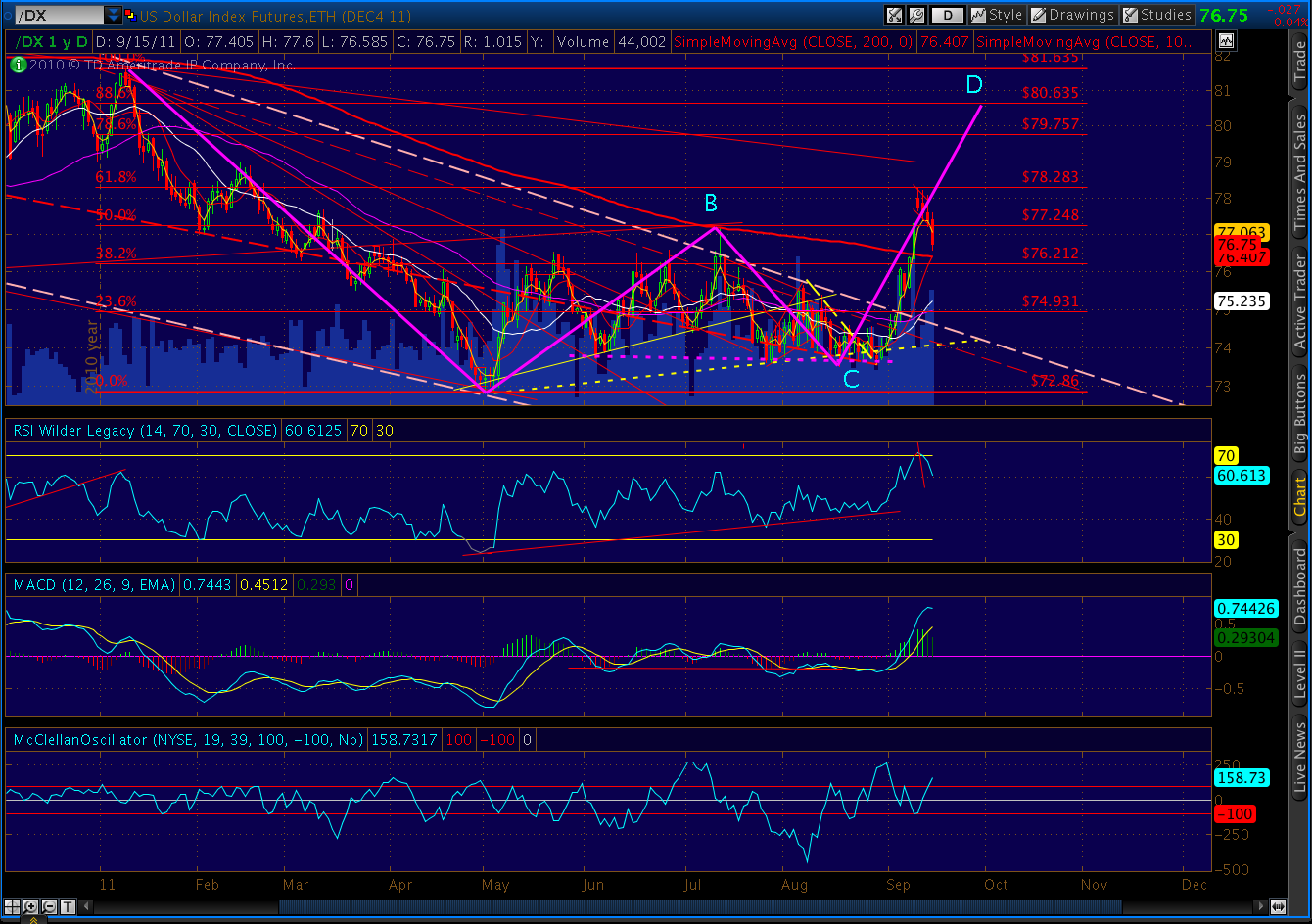

Check out DX. It’s working on a giant Bat pattern and recently stalled at the .618 level on its way to Point D at . Since then, it’s traced out a bullish flag, and is now within a heartbeat of the .50 level, which could very well signal the end of the retracement.

Here’s a closeup.

And, an even better look.

In a perfect world, the bounce off the .50 level will coincide with the SPX’s touch of the .886 Fib at 1196.61.

UPDATE: 1:55 PM

We got the gap fill, and then some. Don’ t be alarmed, as this is probably an overshoot — much better punctuation for the move ahead. Look at Aug 31 and Sep 1 for recent examples.

The .786 Fib is at 1189.78 and makes a great turning point from a harmonic standpoint. Even better, assuming this is a Bat pattern, is the .886 at 1196.61.

UPDATE: 1:15 PM

Moment of truth… I think it’s really cool that the rising wedge apex, gap fill and regression channel midline are all within .50 of each other. The descending channel could be right there, too; hard to draw it with absolute precision.

Take a look at the midline’s performance over the past several weeks.

UPDATE: 11:35 AM

This is the hardest part of calling every top, watching the backtest of the rising wedge. In this case, it could go up and close the gap at around 1184 as mentioned below. But, it doesn’t need to.

Here’s the 60-min chart:

And, the 5-minute:

The regression channel has been updated. The midline looks to be right where the gap fill is: 1183.4.

UPDATE: 10:55 AM

I won’t be surprised if we take one last stab at 1184 to close the gap and complete a better looking wave count. Also marks the SMA 10.

UPDATE: 10:00 AM

The McClellan Oscillator just flashed my favorite crash signal — the same as July 22, 2011 (but better) and December 26, 2007. It’s the dotted yellow line in the bottom study.

Here’s the same indicator on December 26, 2007.

The only question is whether the market makers can keep things afloat through OPEX this Friday. I think they let it peak a little early, which in itself is an indication of the downside pressure baked into this market.

Here’s an updated close up of the daily chart:

And, the five-minute chart, with the requisite other-shoe-dropping divergence.

ORIGINAL POST: 9:30 AM

While we’re waiting for the other shoe to drop, here are my leading candidates for the turn.

Take your pick, but I’m thinking 1181-1184 ought to do it.

UPDATE: 2:15 PM

Checking in on our regression channel and requisite rising wedge (the exclamation point!) So far, so good. Looks like we should get to 1182 – 1188 before the fun starts.

We should expect to see more divergence on the 5-min RSI and possibly the histogram soon.

UPDATE: 12:45 PM

Euro got a little bounce from Merkel’s interview this afternoon:

I see… we have nothing to fear but acknowledgement of the bloody, horrid reality itself.

Geithner is even taking the unprecedented step of attending Friday’s meeting of the EU finance ministers in Poland… ’cause nothing settles nerves like a guy who arranges train wrecks racing to the scene of the next train wreck.

Meanwhile, has anyone checked in with the people of Greece? Last I heard, they had no interest in yet more austerity so that the world’s bankers can limit their losses. I’ll say it again, the 2007-2009 crash (will we call it the mini-crash?) was the result of several failed companies. This time, we’re talking countries.

I remember something from a psychology class I once took. Kubler-Ross, the five stages of grief. I think it was: (1) denial, (2) anger, (3) bargaining… then… what was that next one?

Oh, yeah. Depression.

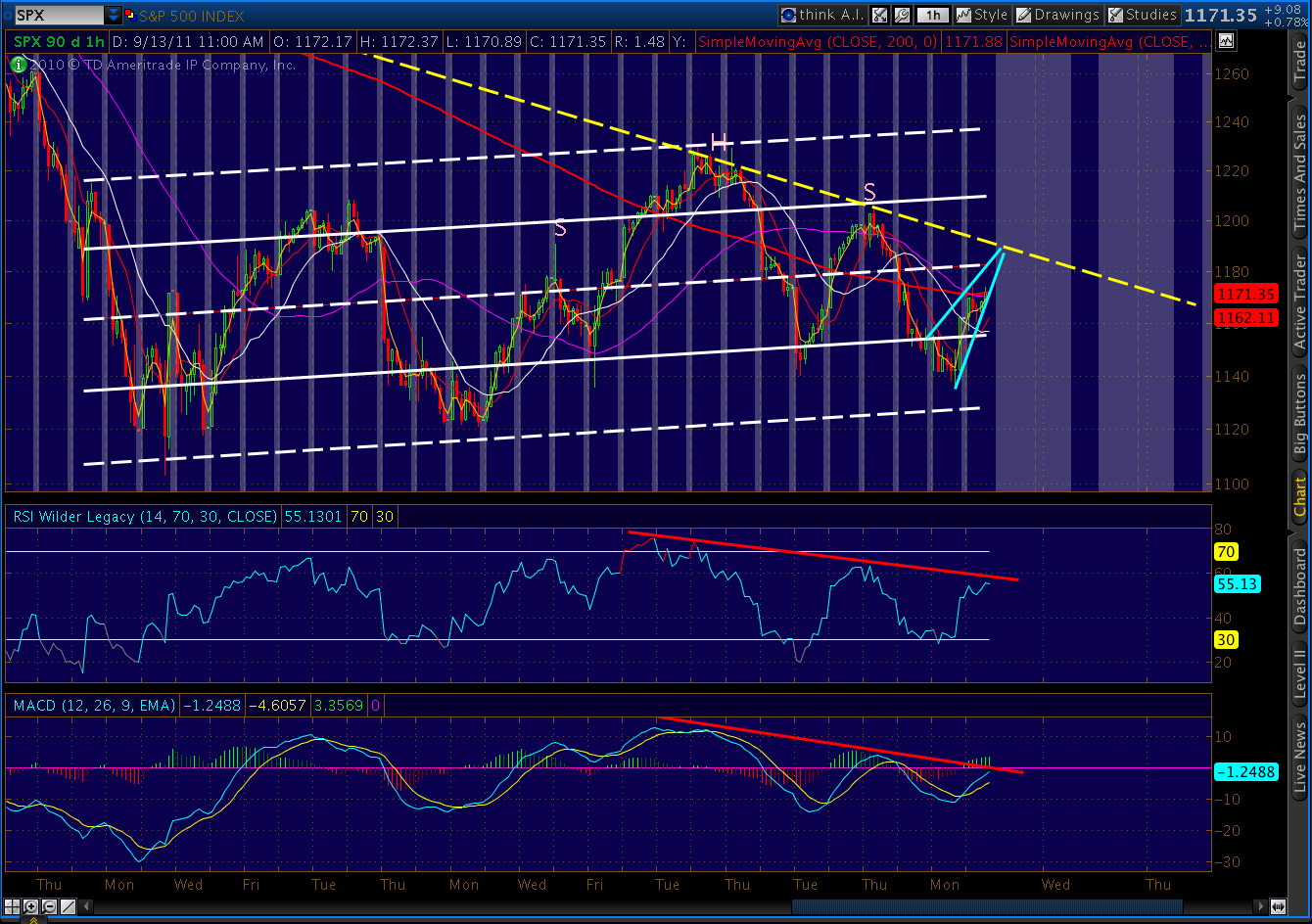

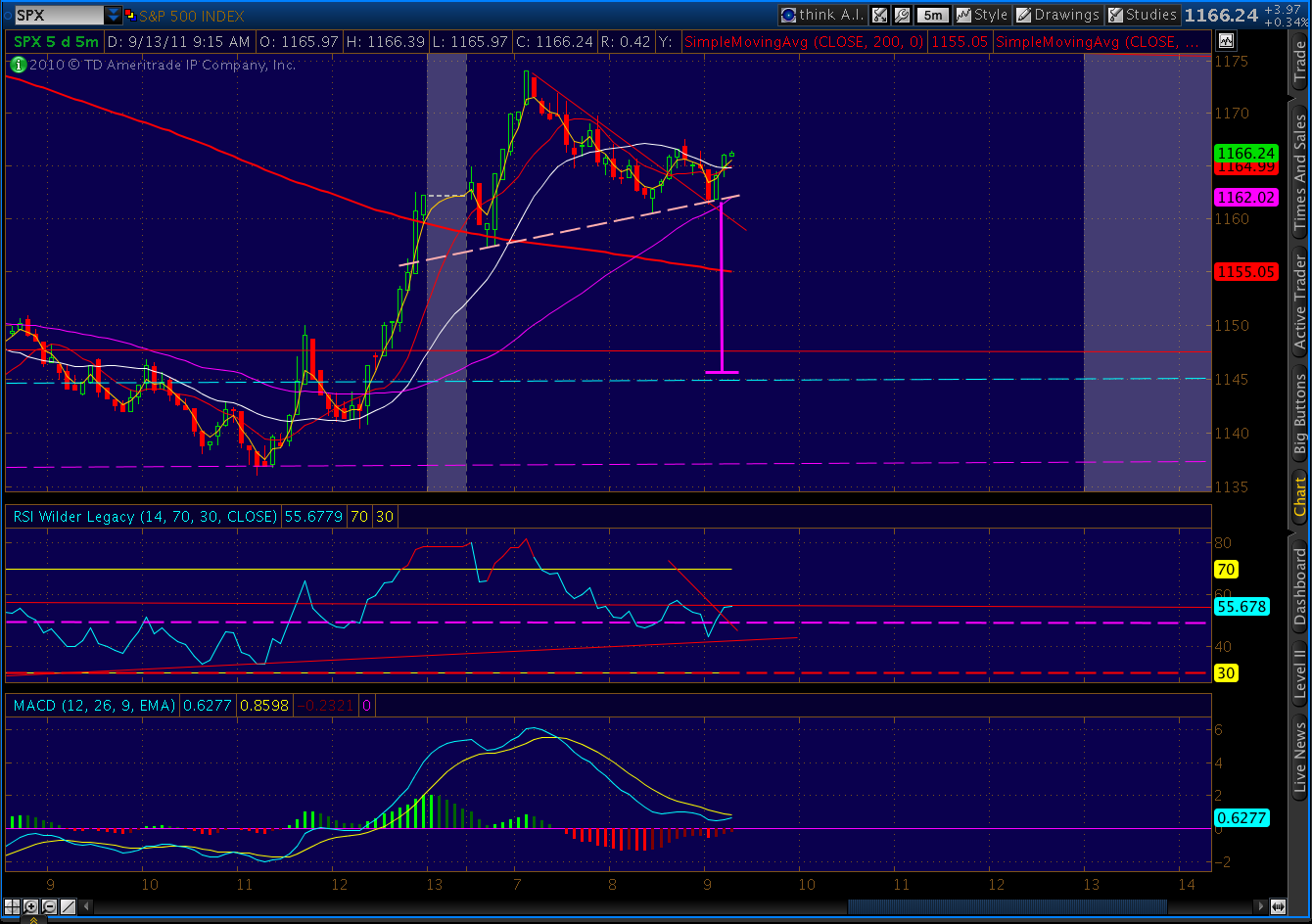

UPDATE: 12:15 PM

Little H&S; just completed on the 5-min chart… calls for a return to 1146-ish.

UPDATE: 11:30 AM

A closer look at the dollar… DX has traced out three points of a perfectly formed Bat pattern, which calls for an 88.6% retrace from the top. The bullish flag we’ve formed over the past couple of days is right at the .618 level. Our target is 80.635.

That might seem high, given how quickly DX has risen to its present height and the fact that its RSI looks overbought already. But, consider what happened the last time the stock market fell apart:

And, back then, the EUR was considered a great alternative to a sketchy dollar.

UPDATE: 10:30 AM

The daily RSI is drawing closer to the trend line that signals ongoing divergence. The next touch should mark the end of this rally, although it’s possible we’ll stop short. Also, note we’ve stalled at the SMA 20 at 1176 (the SMA 10 is at 1188, @ the upper channel line.) And, the histogram is also showing divergence — with a 4th shorter bar in a row to go with the two-day rally.

The 60 minute RSI has hit its TL and is working on a nice reversal candle. I think the rally is either over here or we might go up and tag 1188 first. Either way, the jig is just about up.

ORIGINAL POST: 9:00AM

I’m watching credit and currency markets this morning. Italy just auctioned EUR 6.5 billion at 5.60%, an all-time high since the Euro’s introduction. Bid to cover was a wretched 1.279.

Hopes that China would come to the Euro’s rescue appear unfounded. And, French banks continue to hit the windshield at high speed: asset sales all around, BNP rumored to draw no bids from money market funds, and Moody’s downgrades on the way.

Meanwhile, the dollar has traced out a bullish flag, to go with EUR’s bear flag:

UPDATE: 3:00 PM

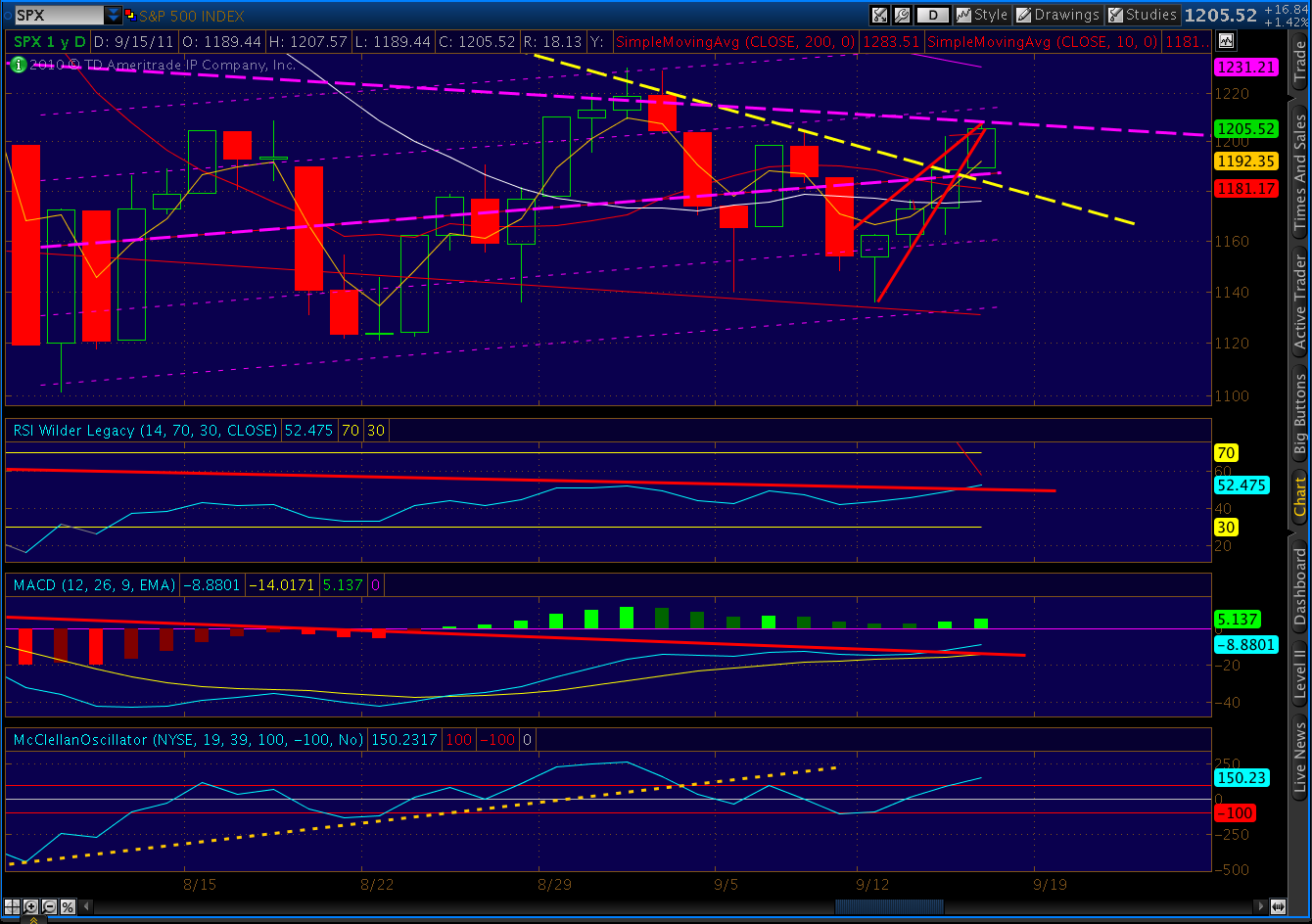

Had a little more time to study this… It’s open to interpretation, but here’s what I’m seeing. I’ve stacked the Feb – May 2011 top over this 5 week consolidation and compared them point by point.

There are a few discrepancies, but nothing that concerns me too much.

The biggest question is whether the channel down from Jul 22 should include the upper shadows from Aug 31 and Sep 1. If not, then Point 8 — when contained by the channel — will land around the regression channel midline at, say 1185.

If we include the shadows in drawing the channel, then Point 8 would be a little beyond the midline, at around 1200. In many past topping patterns such as 2001, the midline defines Point 8. In 2007 and 2011, however, the market overshot the midline. I suggest it will be largely a function of the momentum we have going once the reversal occurs.

Speaking of reversals, note that this little drama — which will no doubt draw a huge amount of attention due to its being “completely unexpected” — will fall short of the the Sep 8 high at 1204. This is significant, as once we reverse off Point 8, the subsequent drop will complete a new, larger H&S; pattern that points toward 1016.

And, the kicker — the Butterfly pattern we’ve been watching. The 1.618 extension is only a few points away at 1021.

UPDATE: 11:30 AM

I’m intrigued by the idea of the consolidation action we’ve seen since Aug 9 playing out as a fractal of the larger topping pattern from Feb 18 – July 22. First, a look back:

ORIGINAL POST: 9:30 AM

Global markets off, with the SPX plunging below Fan Line C as we discussed Friday. The H&S; pattern has been completed, and we’re well on our way to point D on the large Butterfly pattern.

We should see a backtest of Fan Line C, as the futures did yesterday. And, there’s the possibility that we’ll head back up for another test of the channel, but the next move of any substance is the mid-1000’s.

POSTED: 2:40 PM

This little pause brought to you by Fan Line C. Don’t worry, RSI and MCO promise plenty more downside to come.

The H&S; completion is up ahead at around 1146.