There are lots of reasons for interest rates to decline. Inflation expectations could fall. Economic growth could slow. A central bank could pump trillions of dollars into buying up debt. They’re all effective, but they all take time and involve nasty consequences.

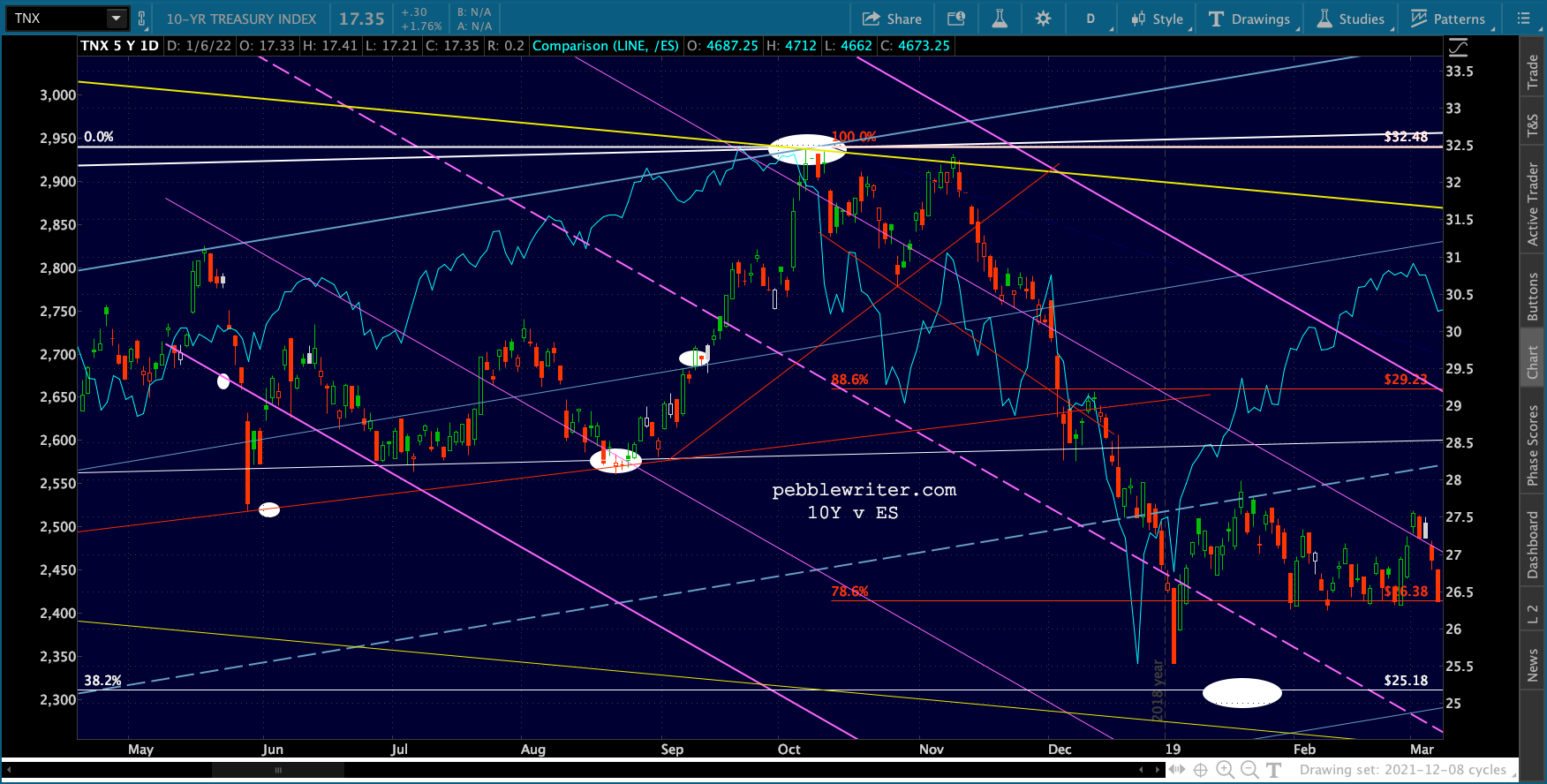

When it comes to a rapid response, nothing can hold a candle to an equity correction – the scarier the better – that sends equity investors running for the fixed-income hills. We saw this occur at the end of 2018 and in early 2020 – the scene of 21% and 35% corrections respectively.

In the first case, the 10Y fell from 3.25% to 2.55% during roughly the same period.  In 2020, the 10Y plunged from 1.64% to 0.4% in less than a month.

In 2020, the 10Y plunged from 1.64% to 0.4% in less than a month.

Following the 2020 plunge, economic activity was thought to be low enough to keep inflation expectations in the cellar. But, it’s difficult to distinguish between inflation expectations and the doubling of the Fed’s balance sheet from $4.3 to $8.6 trillion (as of Dec 2021.)

Following the 2020 plunge, economic activity was thought to be low enough to keep inflation expectations in the cellar. But, it’s difficult to distinguish between inflation expectations and the doubling of the Fed’s balance sheet from $4.3 to $8.6 trillion (as of Dec 2021.)

The 10Y followed rebounding inflation until topping out at 1.765% in March 2021 – about the same time the Fed began pounding the “transitory” drum. Since then, the 10Y has slumped as low as 1.13% before clawing its way back to today’s high of 1.74%. Conventional wisdom has it that rates will continue going higher, perhaps much higher, as the Fed employs its “tools” to combat inflation. This is a reasonable assumption, particularly since the Fed’s taper impacts its ability to buy up treasuries.

Conventional wisdom has it that rates will continue going higher, perhaps much higher, as the Fed employs its “tools” to combat inflation. This is a reasonable assumption, particularly since the Fed’s taper impacts its ability to buy up treasuries.

And, a timely decline in inflation such as we saw in late 2018 is thought to be unlikely [more a shortage of volunteer journalists rather than supply constraints.] Even if oil prices were to crash, it’s unclear whether other, stickier components of inflation would respond very quickly, if at all.

That leaves us with the interesting prospect of a market correction that’s scary enough to bring rates down off the ledge, but not so scary that real damage is done. The current taper schedule means QE will end in March. So, there’s plenty of time to to put such a plan into place before the Fed would be expected to start raising rates significantly.

Stay tuned.

Futures, which were already off sharply, legged down further on the news.

Futures, which were already off sharply, legged down further on the news. Our equity targets remain unchanged.

Our equity targets remain unchanged.