December retail sales disappointed, slumping 1.9% MoM and capping off a week of economic data which provided growing evidence of stagflation. The data were before nominal, meaning inflation-adjusted data were even worse. This is hardly surprising given that ever greater portions of Americans’ incomes are being consumed by rapidly rising prices.

Futures, which were already off sharply, legged down further on the news.

Futures, which were already off sharply, legged down further on the news.

Our equity targets remain unchanged.

Our equity targets remain unchanged.

continued for members…

With the IH&S officially busted, our downside targets just became more likely.

A drop by COMP through its SMA200 would generate a lot of bearish attention.

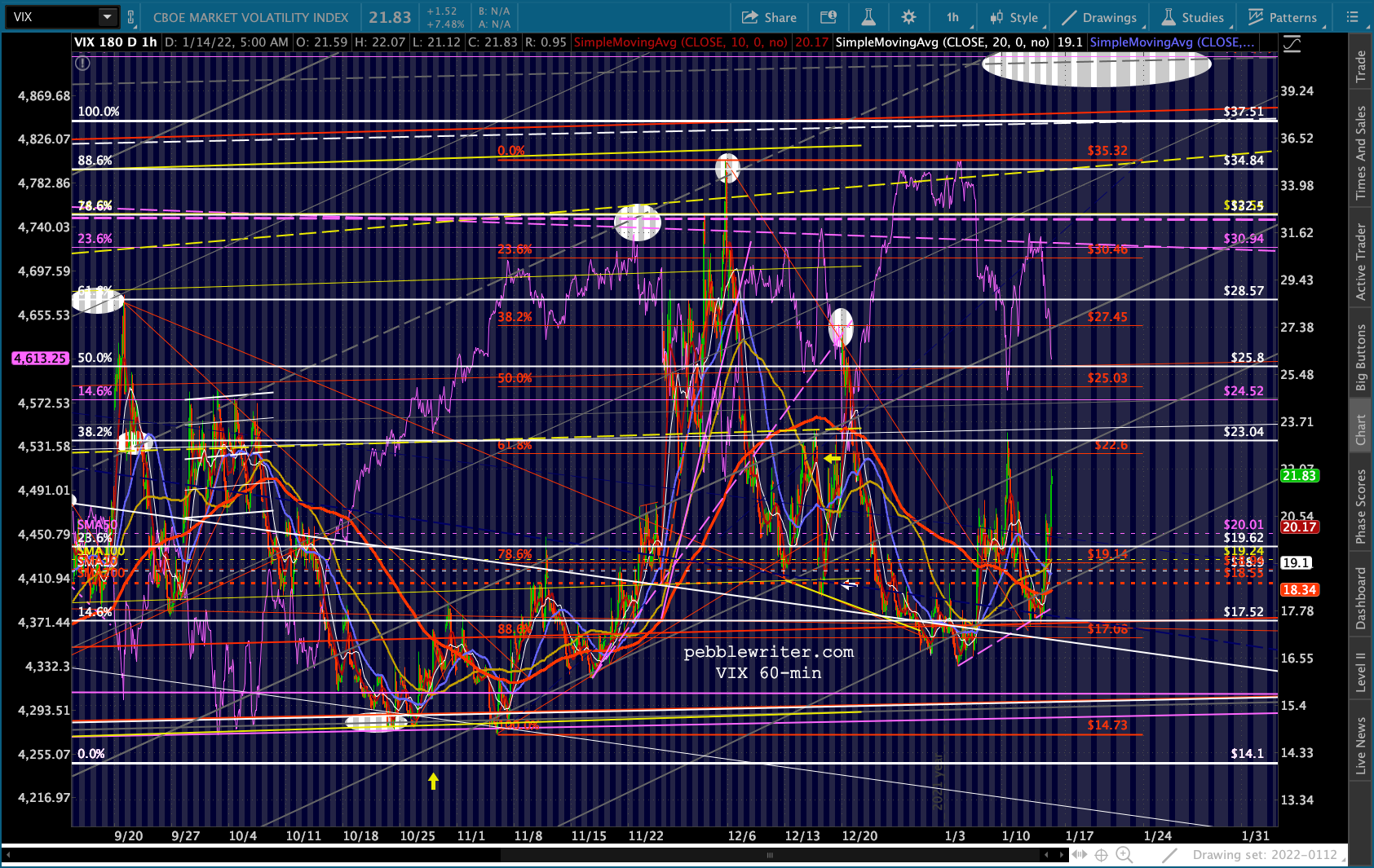

A drop by COMP through its SMA200 would generate a lot of bearish attention. VIX is back on top of all of its SMAs…

VIX is back on top of all of its SMAs…  …and is on the brink of a bullish (bearish for stocks) 10/20 cross.

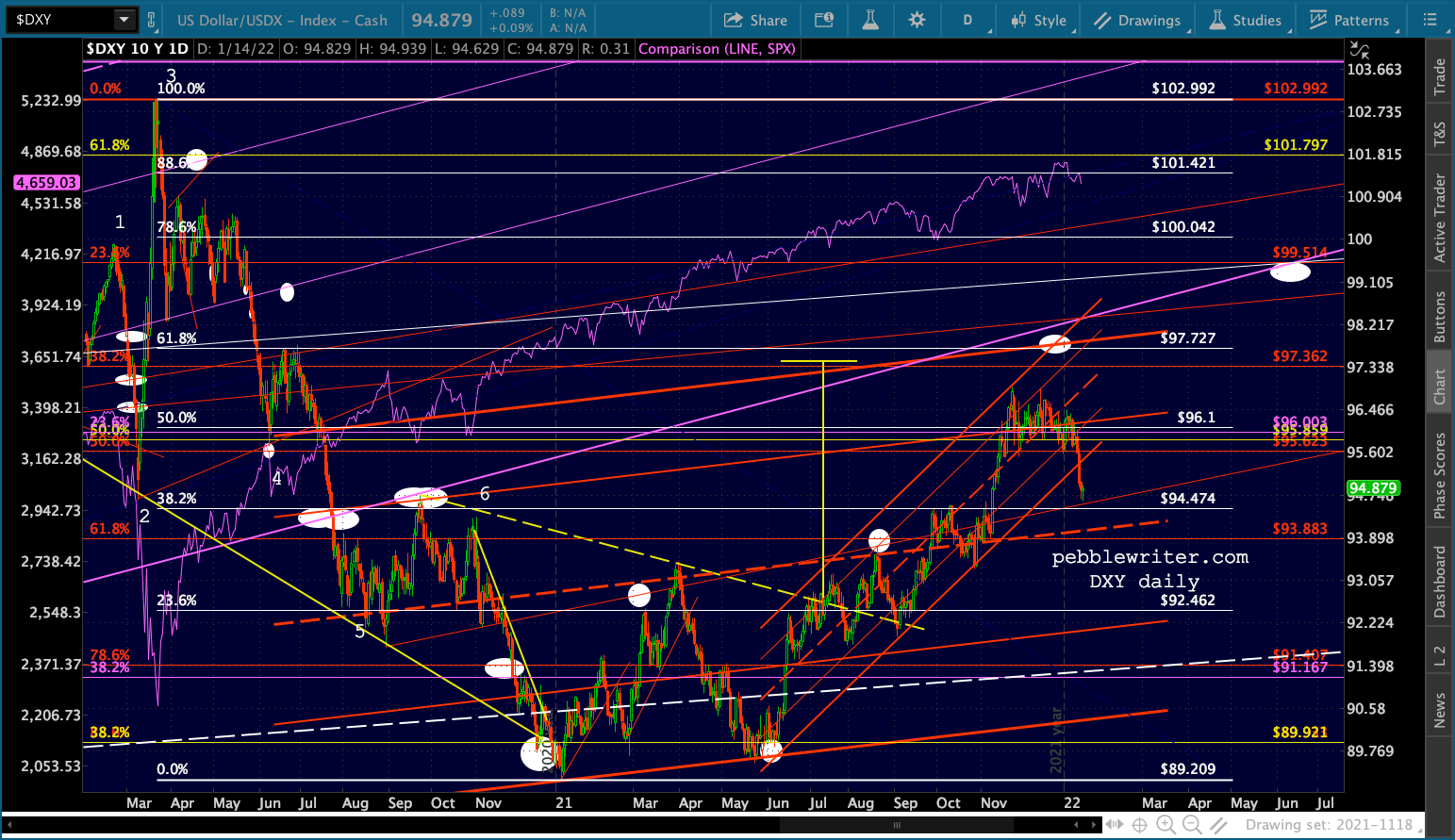

…and is on the brink of a bullish (bearish for stocks) 10/20 cross.  USDJPY is endorsing an equity downturn, breaking below the red TL and closing the gap with the SMA200.

USDJPY is endorsing an equity downturn, breaking below the red TL and closing the gap with the SMA200. We’re also seeing the dollar strengthen against the euro with a reversal at that TL we discussed yesterday.

We’re also seeing the dollar strengthen against the euro with a reversal at that TL we discussed yesterday.  The net effect on DXY is a modest bounce…so far.

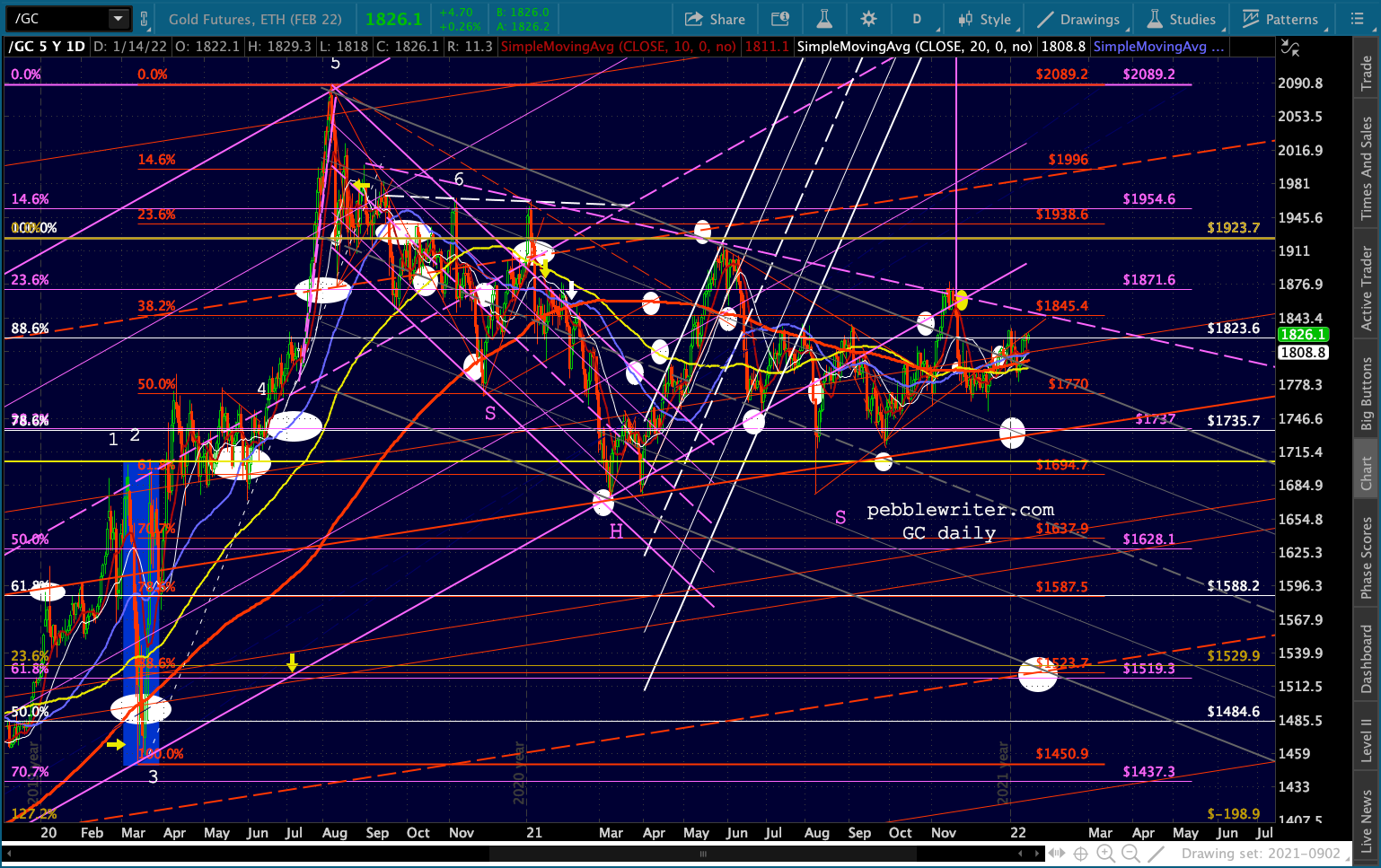

The net effect on DXY is a modest bounce…so far.  Gold and silver are relatively unchanged…

Gold and silver are relatively unchanged…

…while BTC is clinging to its SMA10.

…while BTC is clinging to its SMA10.  Oil and gas are largely on the sidelines with both mostly erasing yesterday’s small losses.

Oil and gas are largely on the sidelines with both mostly erasing yesterday’s small losses.

Though NG has given up its intrusion into the red channel from which it broke down in early December. As long as 4.20 resistance holds, we’ll continue to call that a head fake.

Though NG has given up its intrusion into the red channel from which it broke down in early December. As long as 4.20 resistance holds, we’ll continue to call that a head fake.

The small correction we’ve had so far has put a damper on higher rates. Over the last two days, the 10Y fell from a high of 1.808% to 1.706%. It’s bouncing a bit today on the growing certainty of multiple rate hikes in 2022.

The small correction we’ve had so far has put a damper on higher rates. Over the last two days, the 10Y fell from a high of 1.808% to 1.706%. It’s bouncing a bit today on the growing certainty of multiple rate hikes in 2022.

But, if markets crash hard and fast enough – say, SPX crash through its SMA200 to our 4340 target on Tuesday – then I believe we’d see a significant effect on flows and yields could head back down below the neckline.

The problem with that scenario, of course, is oil and gas. It would be a lot easier to accomplish a rate reset if they would participate in the downside.

The problem with that scenario, of course, is oil and gas. It would be a lot easier to accomplish a rate reset if they would participate in the downside.