If we believe the narrative emanating from the White House, we might take the recent rally as a sign that the market is all better. Trump has softened his disastrous tariff rhetoric and is listening to his better angels (or at least the billionaires who got him reelected.) So is the coast actually clear?

It’s obviously a scary time to go long, given that the past several weeks are peppered with large drops. It’s also nerve-wracking to go long on the basis of a rally that’s the result of Trump’s offhand comments that he doesn’t plan to fire Jay Powell and that he will be very nice in his trade negotiations with China. Naturally, the rally began during the low-volume after hours when surprises can have much greater effect.

Can we really trust those comments or will Trump consider today’s market rally “money in the bank” for use in making questionable future policy decisions? Tariffs are obviously inflationary, but we won’t get inflation data that reflects the tariffs (announced Apr 2, after Q1 was over) until PCE on April 30 and CPI on May 13. Aside from employment and consumer confidence, we won’t get any significant April economic data until Apr 30.

The market’s 21.8% decline between Feb 19 and Apr 7 obviously earned Trump a great deal of criticism. The subsequent bounce might help his approval numbers, but it won’t necessarily heal relationships with our trading partners, restore the confidence of corporate CEO’s in terms of hiring and capital expenditures, or encourage foreign investors to buy US debt.

The highly unusual divergence between treasury yields and the US dollar is almost certainly due to the world losing its appetite for US-based assets due to high tariff rates – as well as the US stepping back from its military, economic and humanitarian leadership role. I question whether Trump squirting a little water on the fire that he started will restore the status quo.

The disruption in the bond market has caused a significant steepening of the yield curve, with the 2s10s breaking out and topping 60 bps on Tuesday. In my modeling, a breakout such as this following an inversion has always resulted in an equity selloff greater than the one we’ve already experienced. The 2000-2003 and 2007-2009 crashes are prime examples. These crashes were caused by a variety of economic circumstances in environments of overpriced equities. There’s an argument to be made that this time is different since it’s a self-inflicted wound (aka stagflation) that can be healed with a properly crafted tweet. But, it’s quite possible that the knock-on effects from Trump’s tariff policy – even if it’s modified to less drastic terms – could usher in a full on recession that can’t be tweeted away.

These crashes were caused by a variety of economic circumstances in environments of overpriced equities. There’s an argument to be made that this time is different since it’s a self-inflicted wound (aka stagflation) that can be healed with a properly crafted tweet. But, it’s quite possible that the knock-on effects from Trump’s tariff policy – even if it’s modified to less drastic terms – could usher in a full on recession that can’t be tweeted away.

Since the FOMC would be caught between a recessionary rock and an inflationary hard place, there is little chance that they would be able or willing to swoop in and rescue markets with an infusion of liquidity and/or massive rate cut. Could this be one of those situations where the market will need to experience a much bigger drop in order to reach a state of equilibrium?

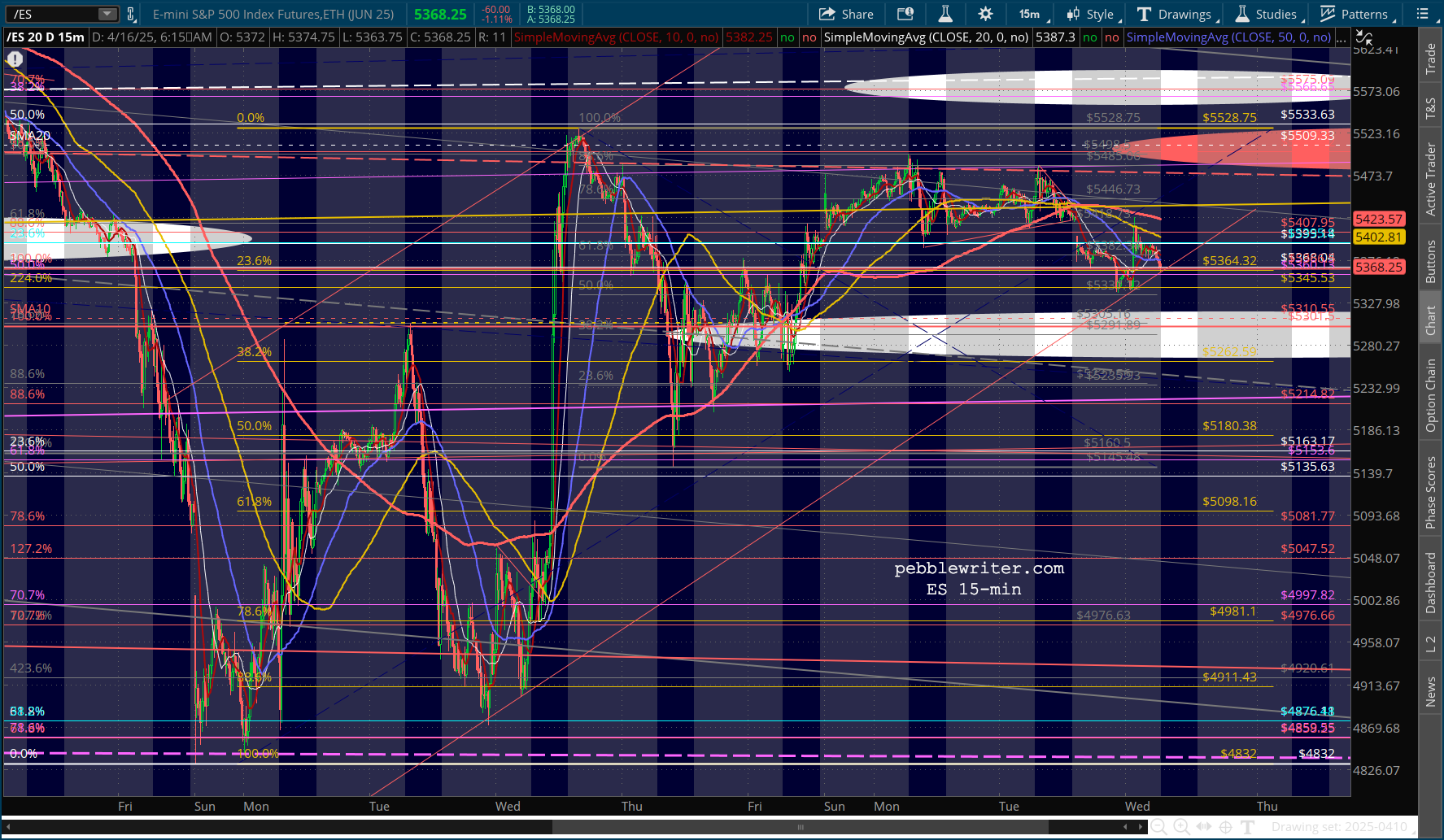

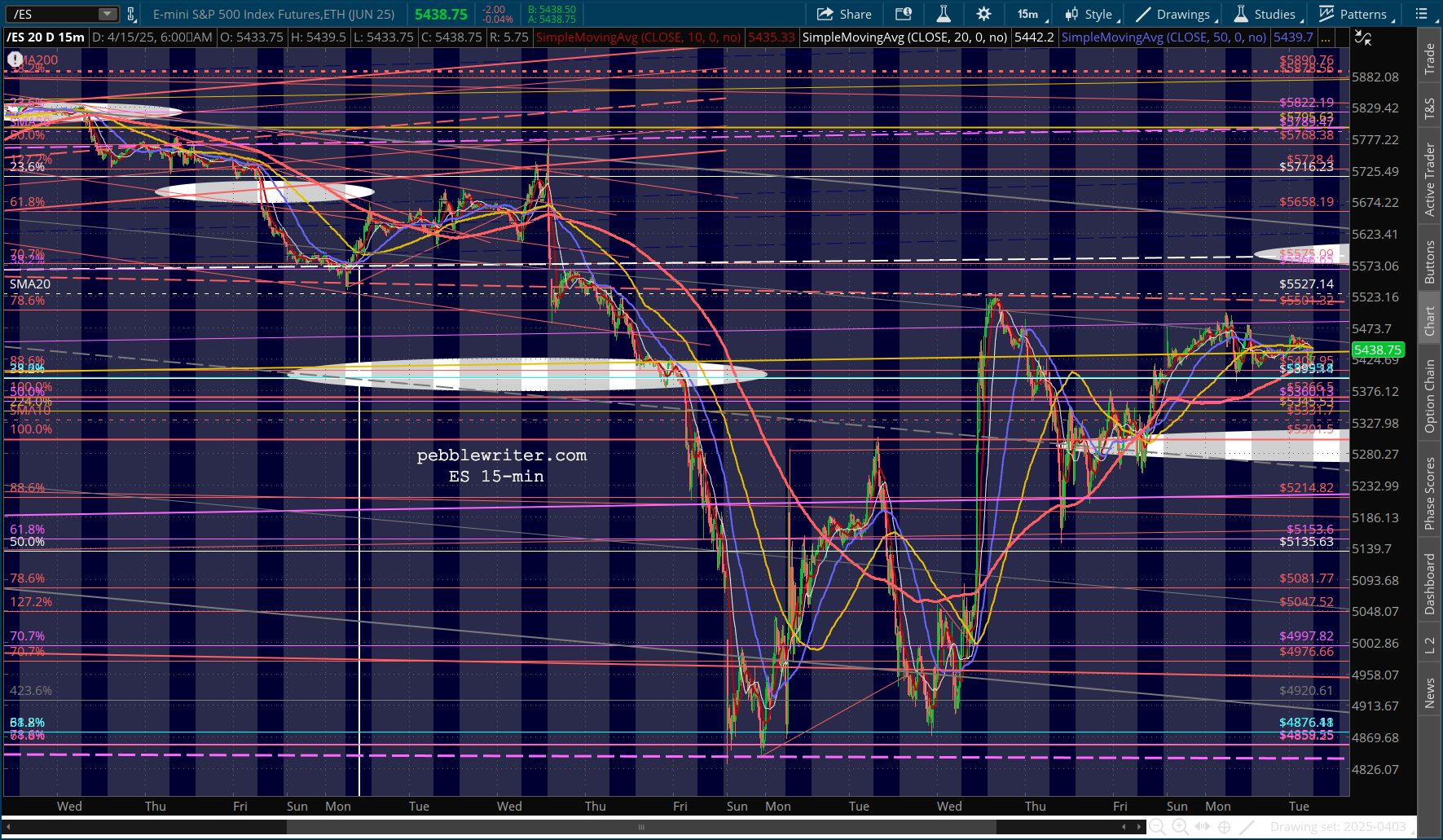

continued for members… (more…)