We published USDJPY’s next highest target months ago with the caveat that it would mean completing a large IH&S that targeted much higher levels and was, thus, far from certain. With inflation already rising sharply, would the BoJ willingly inflict even higher prices on Japanese citizens and businesses just to keep the yen carry trade going?  Wonder no more. In the past month, USDJPY has completed three separate IH&S Patterns. Unlike other central banks which are acting to reduce inflation, the BoJ is guaranteeing even more. It will certainly mitigate stocks’ downside potential to some extent, but at what cost?

Wonder no more. In the past month, USDJPY has completed three separate IH&S Patterns. Unlike other central banks which are acting to reduce inflation, the BoJ is guaranteeing even more. It will certainly mitigate stocks’ downside potential to some extent, but at what cost?

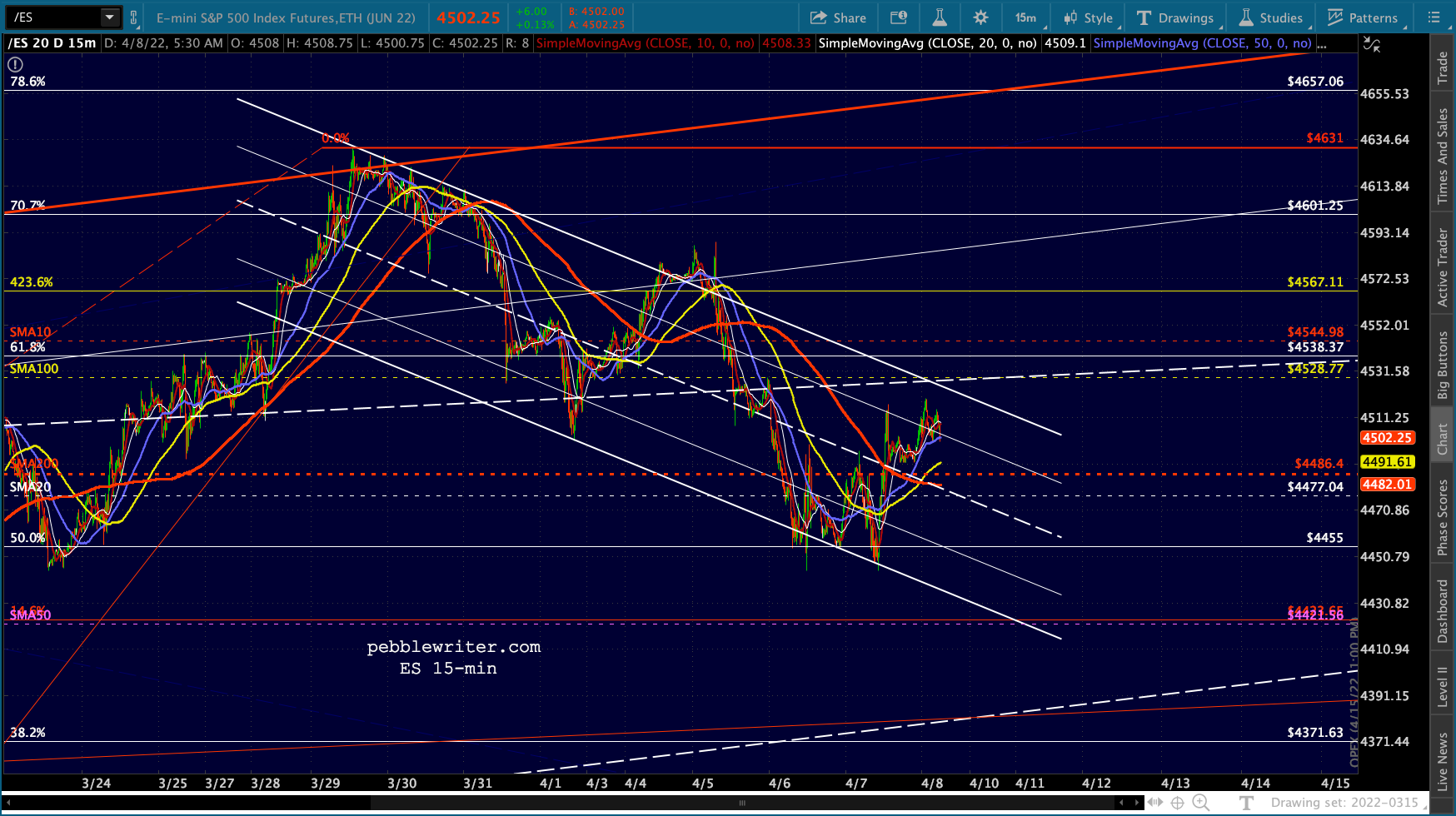

continued for members… (more…)