Jerome Powell gave a good news/bad news speech to the Economic Club of New York. He noted that employment is still 10 million below February 2020 levels and that a broader range of unemployment would put the current rate at 10%, adding, “We are still very far from a strong labor market whose benefits are broadly shared.”

As the algos were spinning up their sell orders, he delivered the good news upon which the market relies: “Achieving and sustaining maximum employment will require more than supportive monetary policy.” He added that it could take “many years” to overcome the effects of long-term unemployment and scoffed at the idea of problematic inflation.

As the algos were spinning up their sell orders, he delivered the good news upon which the market relies: “Achieving and sustaining maximum employment will require more than supportive monetary policy.” He added that it could take “many years” to overcome the effects of long-term unemployment and scoffed at the idea of problematic inflation.

From my vantage point, he’s right and he’s wrong. The strong earnings and cheerleading from pandemic lockdown beneficiaries have drowned out the wails from the pandemic’s have-nots: those who find that even a $1,400 stimulus check won’t pay the rent, the millions of small businesses and self-employed who couldn’t qualify for PPP loans, the millions for whom unemployment benefits are unobtainable or inadequate.

But, make no mistake about inflation. Yesterday’s CPI data reiterates our long-held conviction that, although official core inflation is mild, actual inflation is much higher. Even the understated official CPI will soon soar to levels not seen since before the pandemic (when 10Y yields topped 2%) unless the manufactured rebound in oil and gas prices unwinds posthaste.

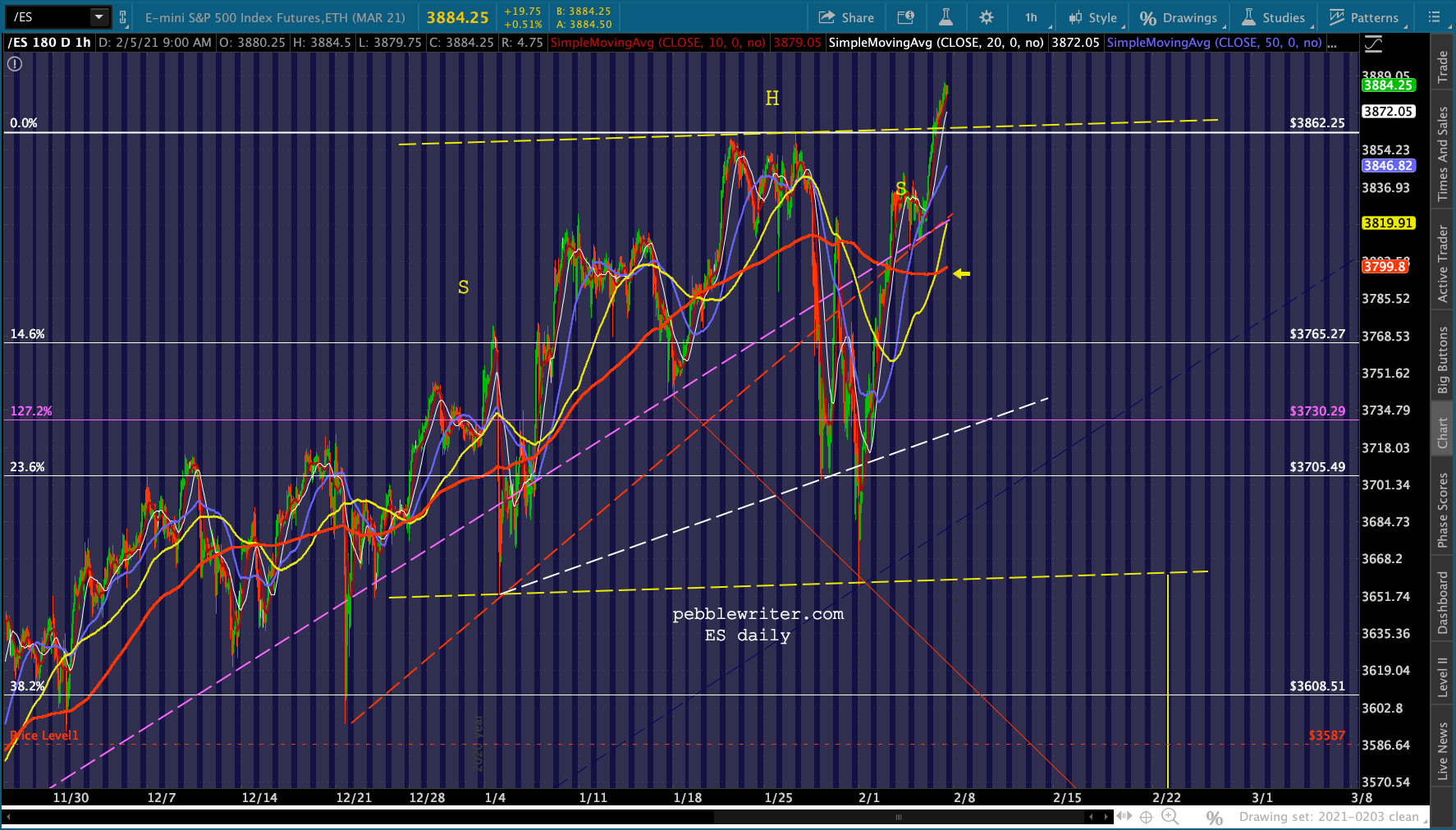

The morning after, futures have regained most of their losses and are again knocking on the door of the 1.272 Fibonacci extension…

The morning after, futures have regained most of their losses and are again knocking on the door of the 1.272 Fibonacci extension… …thanks primarily to yet another VIX “breakdown” from its rising channel which, as we discussed yesterday, has produced another bearish (bullish for stocks) 10/20 SMA cross.

…thanks primarily to yet another VIX “breakdown” from its rising channel which, as we discussed yesterday, has produced another bearish (bullish for stocks) 10/20 SMA cross. Will it be enough to offset the cold water with which Powell just drenched the reinflation trade?

Will it be enough to offset the cold water with which Powell just drenched the reinflation trade?

continued for members… (more…)

continued for members… (more…)

continued for members… (more…)

T

T