NYA reversed very close to our June 30 target (in yellow, below)…

…and has rebounded to backtest the broken red trend line a little sooner than expected. Do or die time for the index.

…and has rebounded to backtest the broken red trend line a little sooner than expected. Do or die time for the index.

NYA reversed very close to our June 30 target (in yellow, below)…

…and has rebounded to backtest the broken red trend line a little sooner than expected. Do or die time for the index.

As Draghi drones on, we’re reminded once again that central bankers abhor “markets” that dare fall while they’re pontificating.

The ECB? Swiss? It doesn’t really matter, as the eminis are up 10 points with 15 minutes to go till the cash open.

While EURUSD approaches our long-awaited downside target, the stage is being set for another gap opening for equities that will see them jump up past key resistance points.

While EURUSD approaches our long-awaited downside target, the stage is being set for another gap opening for equities that will see them jump up past key resistance points.

continued for members… (more…)

Yesterday’s algo-driven meltup went straight to our upside targets and sat there. So, our targets are essentially unchanged from yesterday morning, which are essentially unchanged from Monday.

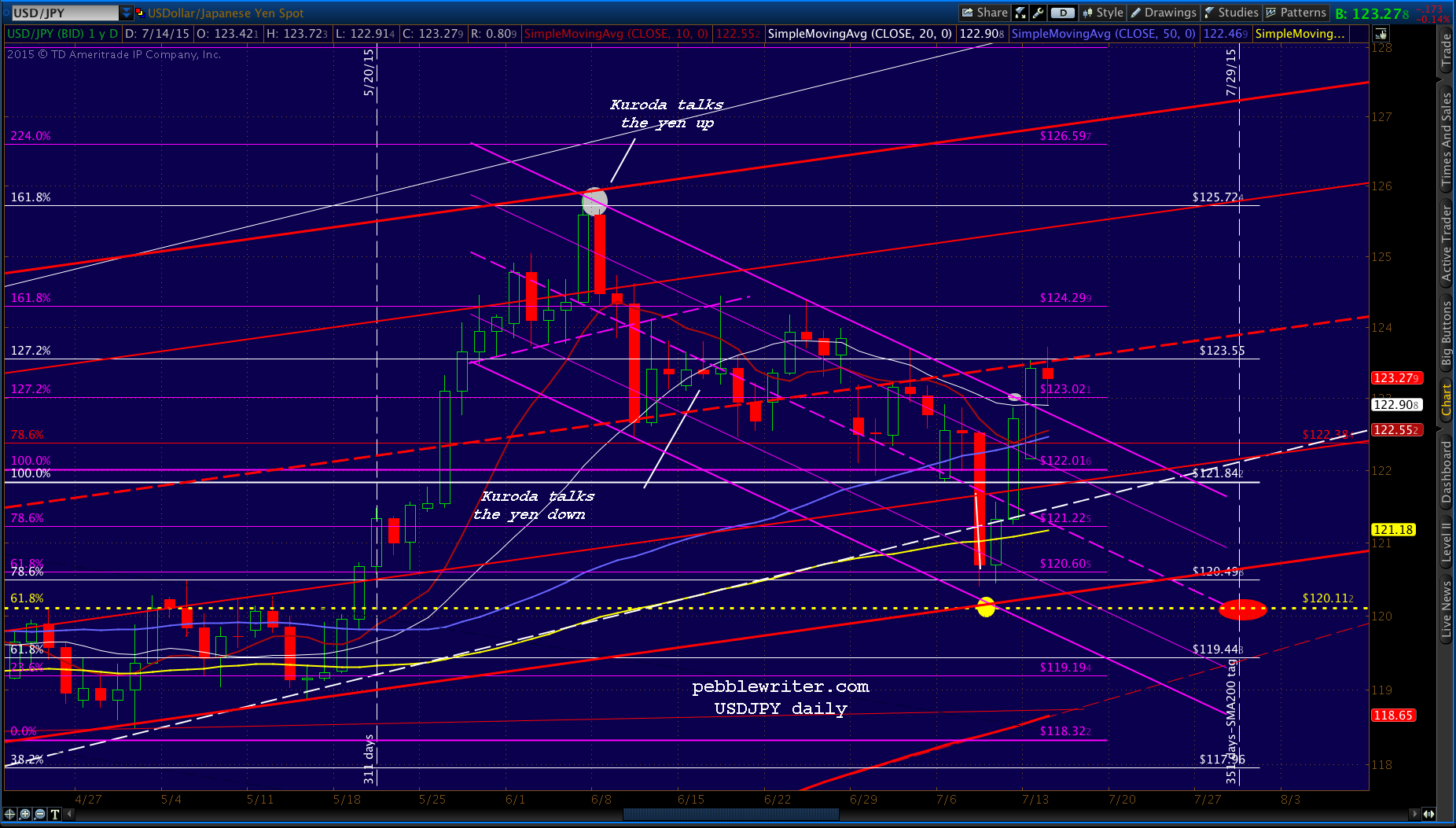

An hour ago, Janet Yellen confirmed the Fed’s plans to raise rates sometime later this year (they won’t.) And, this seems to have taken the bloom off the overnight ramp job just a bit — though USDJPY is more than making up for it.

An hour ago, Janet Yellen confirmed the Fed’s plans to raise rates sometime later this year (they won’t.) And, this seems to have taken the bloom off the overnight ramp job just a bit — though USDJPY is more than making up for it.

continued for members… (more…)

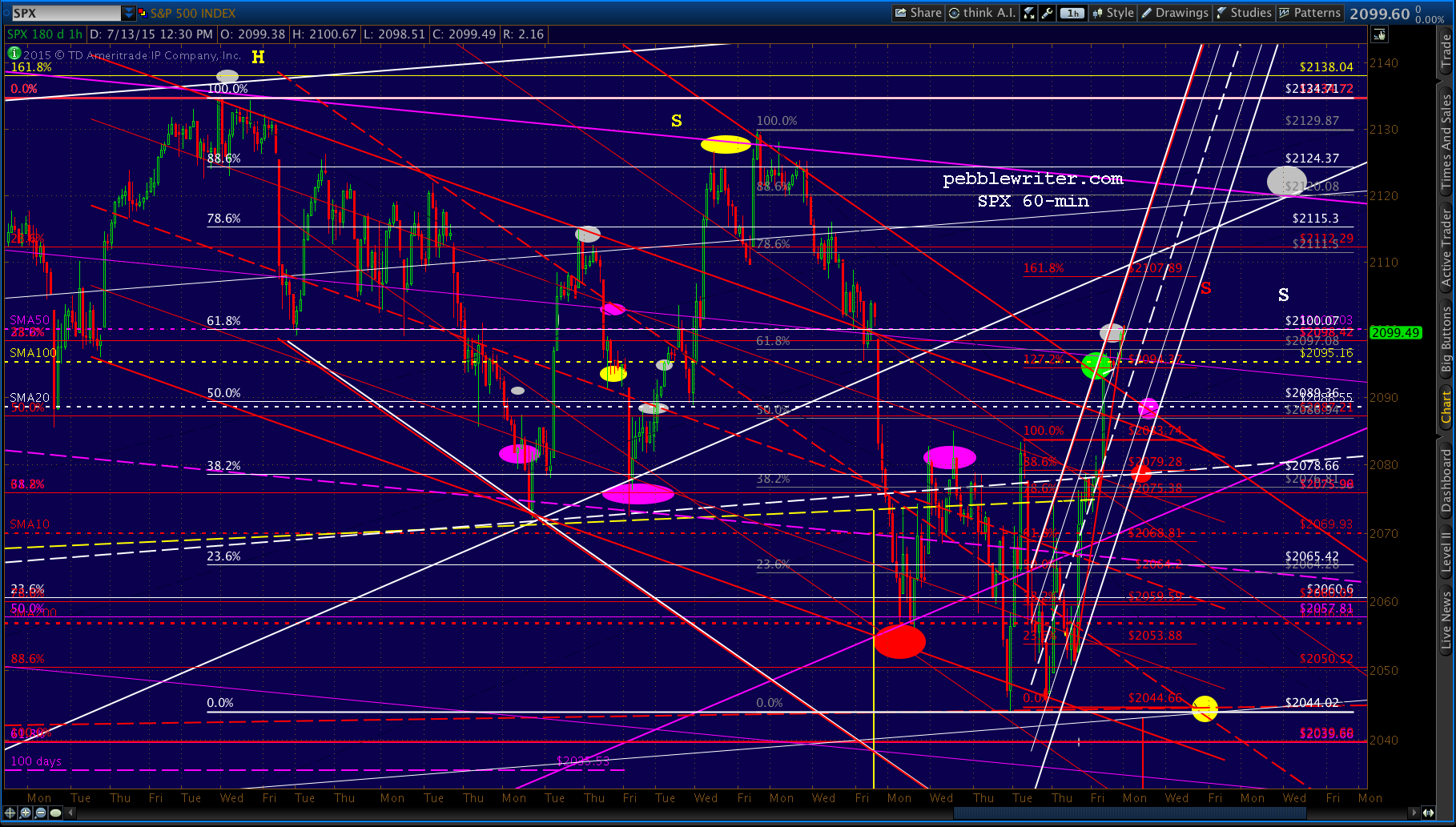

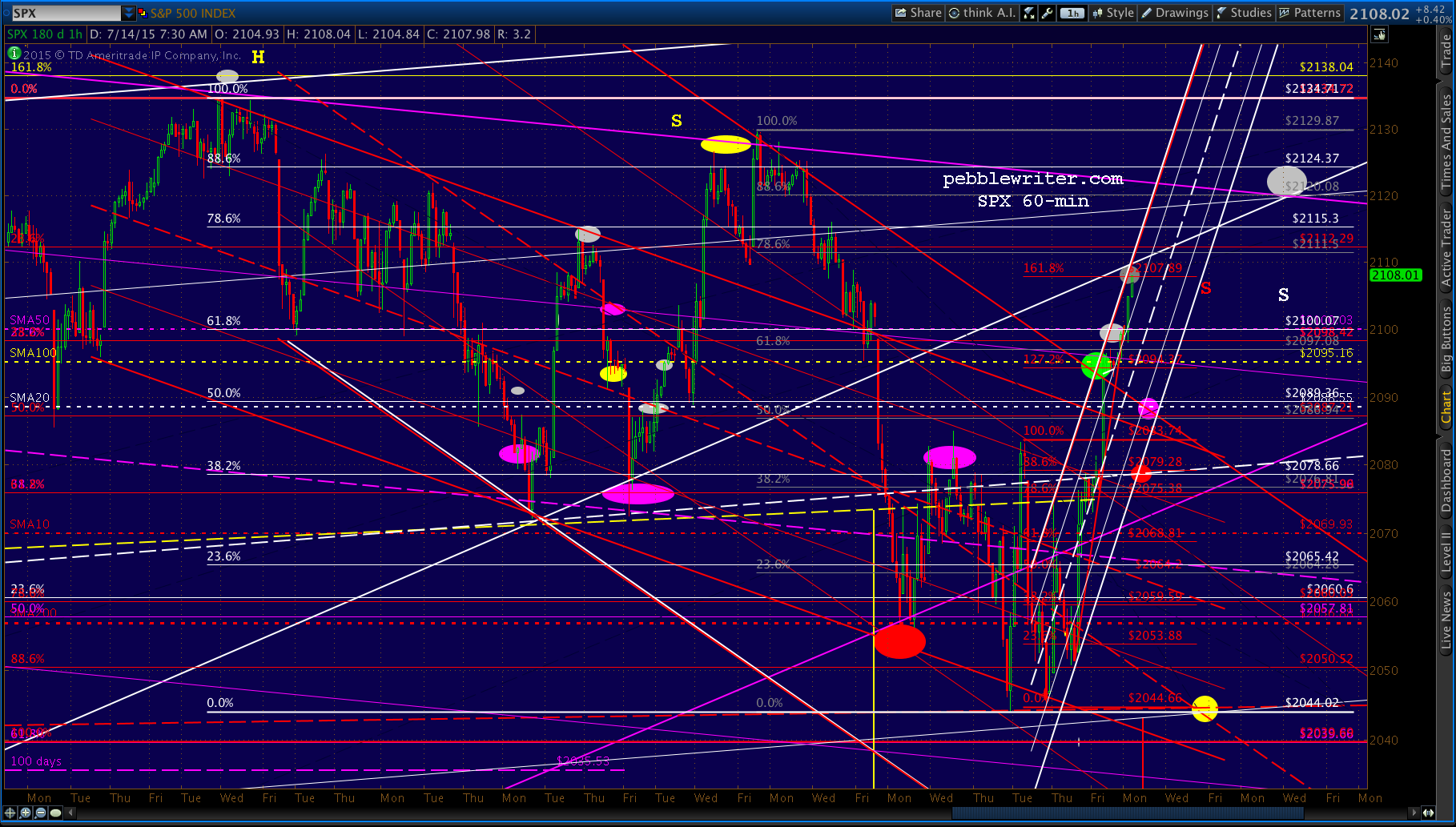

TPTB had two simple goals yesterday: get SPX back above its moving averages and bust the falling channel it’s been in since May 20. They succeeded on both counts.

We’ve seen this countless times over the past few years since algorithms and HFT took control of the “market.” Ramp the eminis an inordinate amount (usually on nominally bullish headlines) and, once the cash “market” opens, HFT the crap out of it — a nickel and a dime at a time — until a well-established pattern is busted and/or a moving average is topped.

It’s more subtle than the Chinese technique of prohibiting stock sales. But, in the end, it’s manipulation just the same. And, it has turned our normally functioning market into a “market” — where plunging retail sales don’t matter at all.

TPTB also succeeded in tagging both our upside targets — the most obvious on the chart. From yesterday’s members section:

The first hurdle will be the falling red channel top at 2094-2095 (also the SMA100 @ 2095.16) with a secondary target of the .618 at 2100 (also the SMA50 @ 2099.75.)

The important question we’re left with is whether yesterday’s algo-driven chart busting exercise will hold, or whether it’s more akin to the Jun 18 incident that began in much the same way but resulted in an 84-pt plunge.

The important question we’re left with is whether yesterday’s algo-driven chart busting exercise will hold, or whether it’s more akin to the Jun 18 incident that began in much the same way but resulted in an 84-pt plunge.

continued for members…

I’m looking for at least a small pullback, with the leading candidate a backtest of the SMA100 at 2095 and the secondary target the SMA20/red channel backtest at 2089.

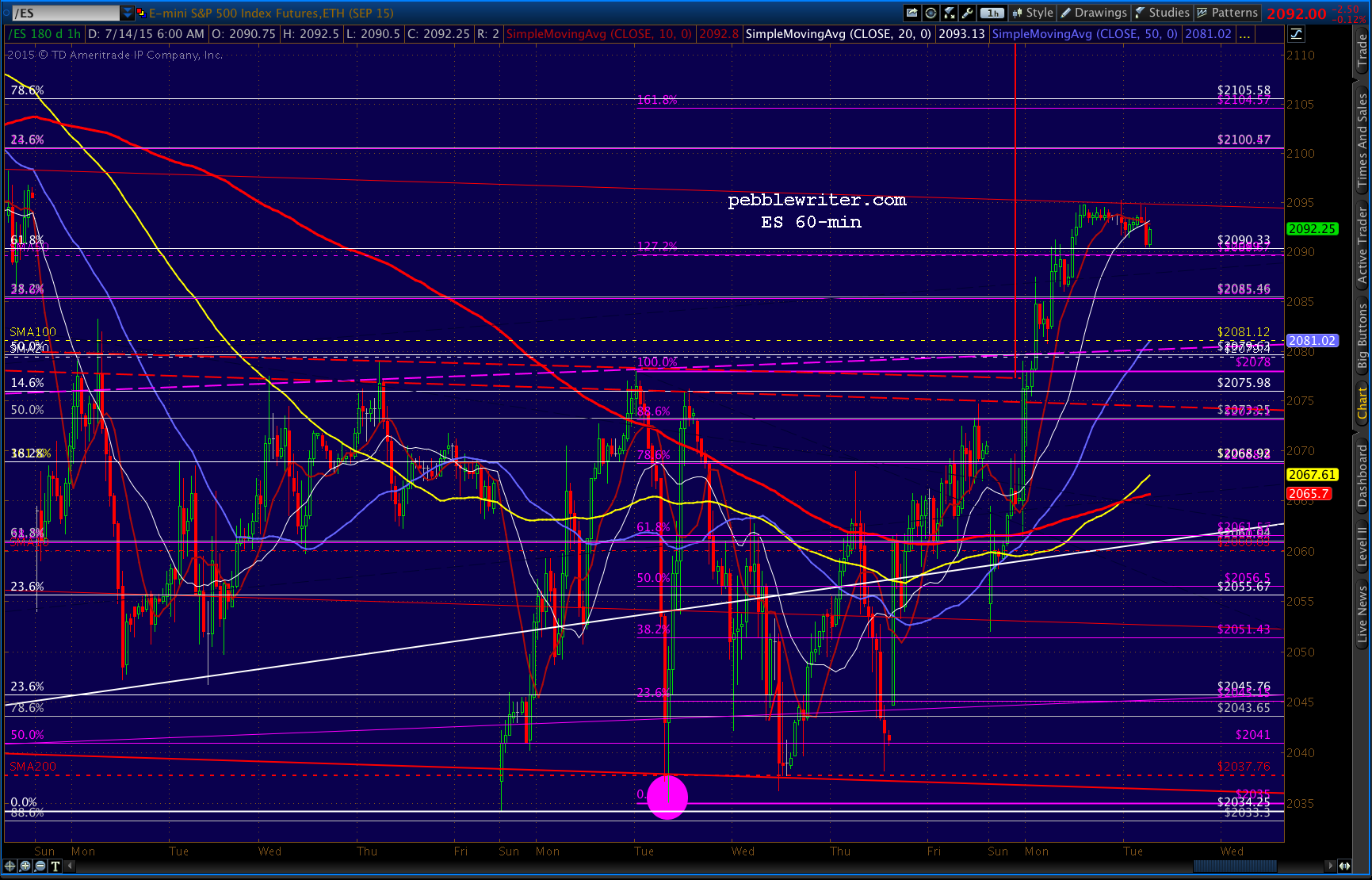

The eminis briefly and begrudgingly gave up a few points in order to backtest the .618 retrace from the May highs. They will try to hold the line, but that was a pretty awful retail sales report. There ought to be more fallout than a few points.

The eminis briefly and begrudgingly gave up a few points in order to backtest the .618 retrace from the May highs. They will try to hold the line, but that was a pretty awful retail sales report. There ought to be more fallout than a few points.

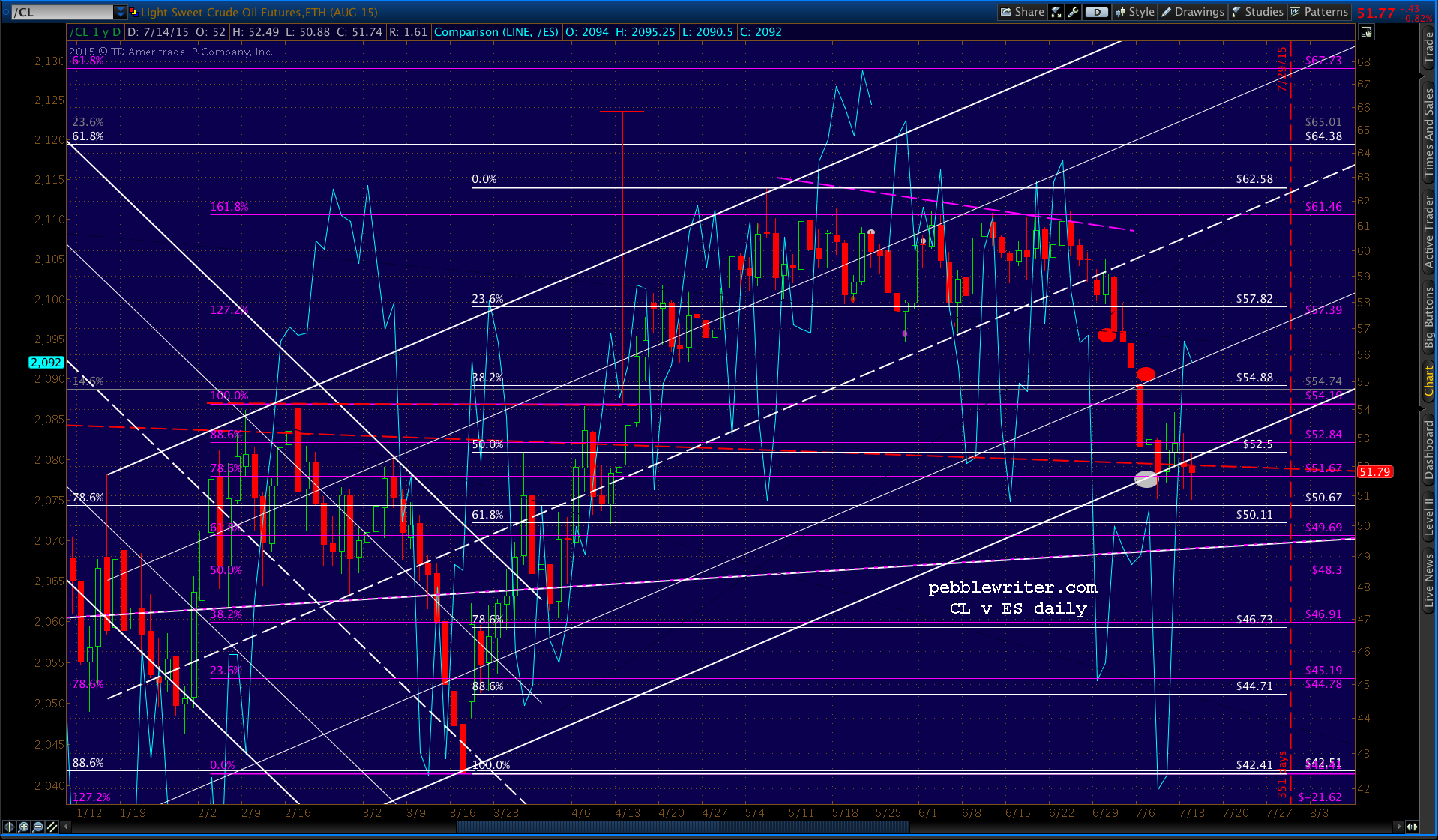

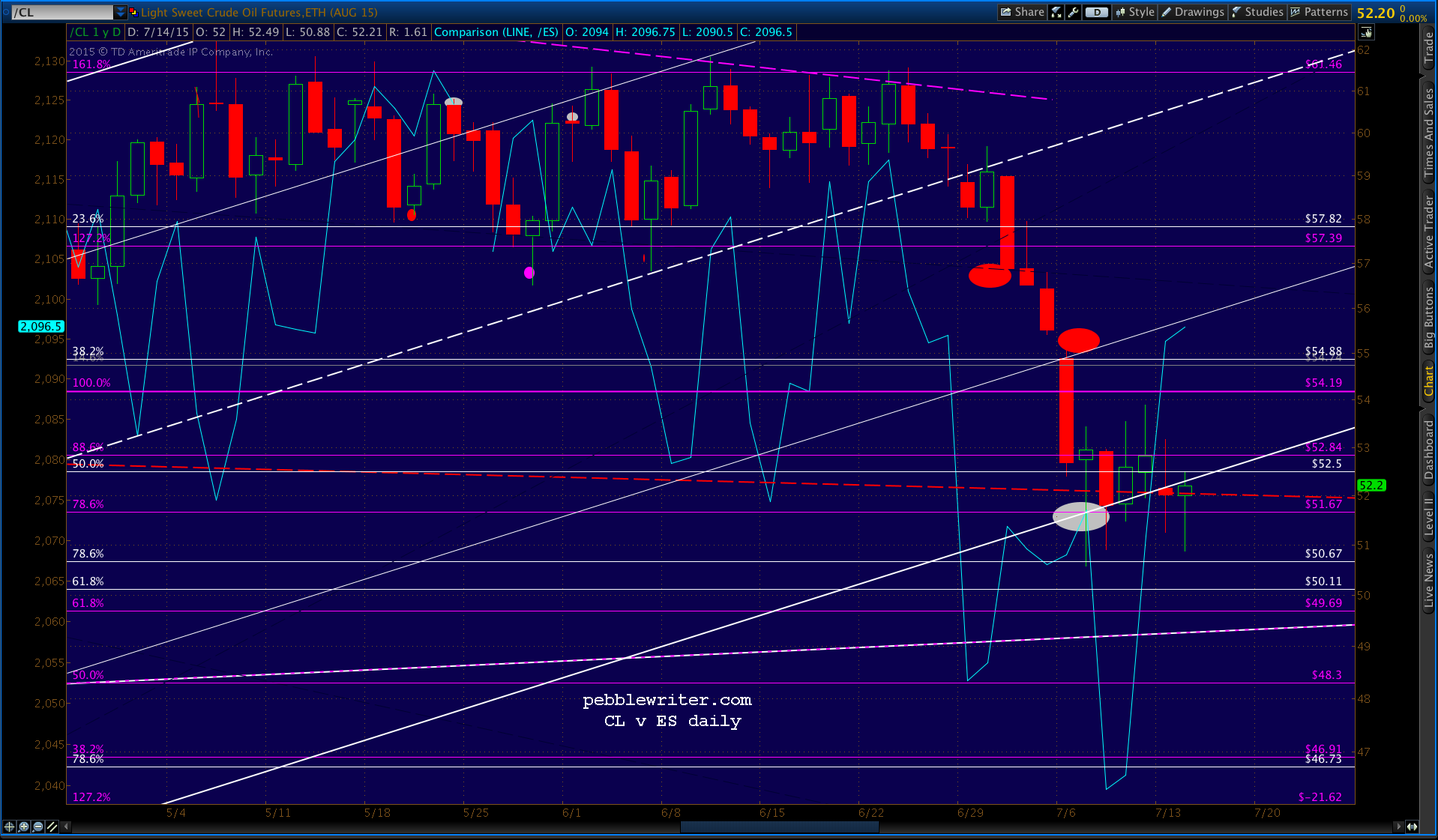

Note, also, that CL should provide some headwinds today as it might finally be allowed to test the .618 at 50.11. Unless it can regain its 10-day moving average (54.56) I’d want to be short for the next leg down.

Note, also, that CL should provide some headwinds today as it might finally be allowed to test the .618 at 50.11. Unless it can regain its 10-day moving average (54.56) I’d want to be short for the next leg down.

More after the open.

More after the open.

UPDATE: 9:46 AM

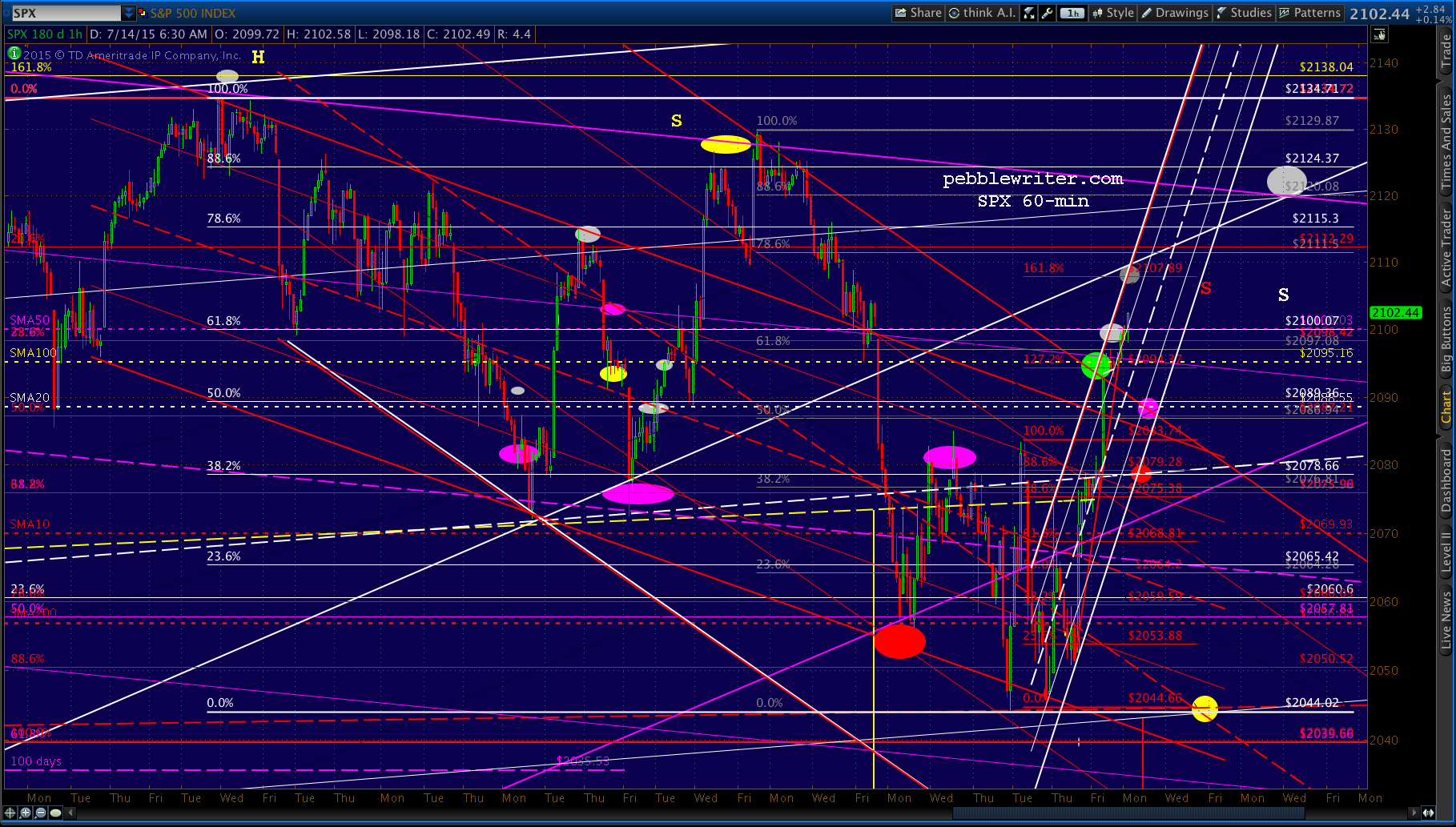

Note that 2107.89 will also effectively backtest the broken white channel bottom.

Thank CL for the reversal — even though it has failed to retake the white channel bottom or the SMA10, for that matter.

Thank CL for the reversal — even though it has failed to retake the white channel bottom or the SMA10, for that matter.

CL is rallying, of course, to cover for USDJPY — which, as we discussed yesterday, has run into resistance at the red channel midline. This, after trashing the perfectly-formed falling purple channel in order to effect yesterday’s “rally.”

CL is rallying, of course, to cover for USDJPY — which, as we discussed yesterday, has run into resistance at the red channel midline. This, after trashing the perfectly-formed falling purple channel in order to effect yesterday’s “rally.”

UPDATE: 11:16 AM

UPDATE: 11:16 AM

One of the more illuminating articles I’ve read on the Greece debacle comes from Harry Lambert at the NewStatesman. The article exposes the story behind the headlines: the methods Eurogroup bankers used to force the concessions they wanted.

The details haven’t yet been finalized, but at this point it appears the bulk of the funds Greece receives will go to repay its creditors, with most or all of the remainder going to its banks. $55 billion in Greek assets (banks, airports, infrastructure) will be escrowed to ensure its creditors are repaid (apparently for the funds they are loaning Greece to repay themselves.)

Those citizens of Greece who have suffered the most will continue to bear the brunt of onerous austerity measures. Those who caused the global financial crisis in the first place will continue to avoid any repercussions.

For anyone wondering what’s really happening in the eurozone — coming soon to your sovereign (for now) country — I strongly recommend taking the time to read the entire article and the full transcript. It’s a rare opportunity to peek behind the curtains.

Exclusive: Yanis Varoufakis opens up about his five month battle to save Greece

In his first interveiw since resigning, Greece’s former Finance Minister says the Eurogroup is “completely and utterly” controlled by Germany, Greece was “set up” and last week’s referendum was wasted.

A few highlights:

“This country must stop extending and pretending, we must stop taking on new loans pretending that we’ve solved the problem, when we haven’t; when we have made our debt even less sustainable on condition of further austerity that even further shrinks the economy; and shifts the burden further onto the have-nots, creating a humanitarian crisis.”

“The other side insisted on a ‘comprehensive agreement’, which meant they wanted to talk about everything. My interpretation is that when you want to talk about everything, you don’t want to talk about anything.” But a comprehensive agreement was impossible. “There were absolutely no [new] positions put forward on anything by them.”

“…there was point blank refusal to engage in economic arguments. Point blank. You put forward an argument that you’ve really worked on, to make sure it’s logically coherent, and you’re just faced with blank stares. It is as if you haven’t spoken. What you say is independent of what they say. You might as well have sung the Swedish national anthem – you’d have got the same reply.”

“What we have is a non-existent group [the Eurogroup] that has the greatest power to determine the lives of Europeans. It’s not answerable to anyone, given it doesn’t exist in law; no minutes are kept; and it’s confidential. No citizen ever knows what is said within . . . These are decisions of almost life and death, and no member has to answer to anybody.”

The entire article, along with a link to the transcript of the interview with Varoufakis, may be found HERE.

As in the old Rocky & Bullwinkle cartoons, the ECB might have pulled a rabbit out of their hats, or it might be something else entirely. The headlines will be very positive, and investors will no doubt breathe a sigh of relief. But, anyone with their eyes wide open will recognize the “solution” as nothing more than can kicking.

As in the old Rocky & Bullwinkle cartoons, the ECB might have pulled a rabbit out of their hats, or it might be something else entirely. The headlines will be very positive, and investors will no doubt breathe a sigh of relief. But, anyone with their eyes wide open will recognize the “solution” as nothing more than can kicking.

The futures have been predictably ramped to a very positive opening, with ES nearly back to the SMA50/.618 Fib combo at 2090.

As for SPX, our upside targets from Friday are unchanged.

As for SPX, our upside targets from Friday are unchanged.

continued for members… (more…)

We had a successful outing yesterday, with the decision to short at 2074 rewarded with a move to our first downside target of 2055 and even our second one at 2051. From yesterday’s members section 10 minutes into a very strong opening:

I’d try a short here at 2074 with an objective of the SMA200 at 2056 — also a .618 retrace from yesterday’s lows.

As for today, we had strong overnight moves in USDJPY… and EURUSD…

and EURUSD… …which have led to a 26-pt ramp job in the eminis. Look for SPX to easily reach yesterday’s upside targets.

…which have led to a 26-pt ramp job in the eminis. Look for SPX to easily reach yesterday’s upside targets.

continued for members… (more…)

If too much debt is a problem, it stands to reason that the best cure is more debt. Like curing a headache with a hammer, or alcoholism with a bottle of Wild Turkey, more debt will apparently enable the Fed to fix the economy once and for all. So suggests Federal Reserve Bank of Minneapolis President Narayana Kocherlakota.

If too much debt is a problem, it stands to reason that the best cure is more debt. Like curing a headache with a hammer, or alcoholism with a bottle of Wild Turkey, more debt will apparently enable the Fed to fix the economy once and for all. So suggests Federal Reserve Bank of Minneapolis President Narayana Kocherlakota.

In remarks prepared for a conference hosted by Germany’s Bundesbank, Kocherlakota maintains that increasing the nation’s borrowings “would push downward on debt prices, and so upward on the long-run neutral real interest rate.”

Raising the neutral rate would supposedly give the Fed more room to lower rates should the economy tank again (which it is arguable already doing.) In other words, higher interest rates would make it easier to further inflate those bubbles that have already been re-inflated. Brilliant!

Perhaps Mr Kocherlakota is suffering from jet lag, or ingested some bad kraut. Because, at $18.15 trillion in national debt, every 1% increase in rates amounts to another $181.5 billion in annual interest payments — over 5% of the US annual budget.

Perhaps Mr Kocherlakota is suffering from jet lag, or ingested some bad kraut. Because, at $18.15 trillion in national debt, every 1% increase in rates amounts to another $181.5 billion in annual interest payments — over 5% of the US annual budget.

A return to a historically average 6% would boost interest payments to over 20% of annual expenses — competing with social security and healthcare for the nation’s biggest expense category. Is there anyone out there who honestly believes spending more tax dollars on interest payments would help the disappearing middle class?

I’ve got a better idea. Let’s get a great big glass jar, and we’ll stick it in Washington D.C. — in the Mall right across Constitution Ave. from the Eccles Building.

I’ve got a better idea. Let’s get a great big glass jar, and we’ll stick it in Washington D.C. — in the Mall right across Constitution Ave. from the Eccles Building.

And, every time some Fed president or PhD economist comes up with a bone-headed idea like this, they’ll have to toddle across the street and toss a nickel in that jar.

I’ll bet it’s filled up in no time. It’ll pay off our national debt and end the financial crisis once and for all. Maybe Kocherlakota will run it by his pals in Frankfurt. Bet they could use a great big jar, too.

When markets are no longer free and open, it’s not that difficult for governments to mandate an outcome. The Chinese have graciously (and, clumsily) provided a thrilling front row seat to what’s been happening in a somewhat less blatant fashion in Western markets for nearly seven years.

SPX came within a few points of our 2039.66 target yesterday, despite a 4-hour seventh inning stretch that wasn’t enough to stem the selling pressure. Thank God for the overnight session, right Janet? Our last words from yesterday’s members’ section:

I like the idea of a close at 2039.60. That way, SPX closes below the SMA200, sucking in tons of bears who aren’t aware of the Fib picture just in time to sucker punch them with a big ramp job in the morning.

SPX only reached 2044.66, not 2039.60. But it closed below the SMA200, and no doubt sucker punched more than a few bears.

Overnight, the Nikkei [see yesterday’s update] got fixed…

…the USDJPY [see: yesterday’s update] got fixed…

…the USDJPY [see: yesterday’s update] got fixed…

…and, with a 26-pt ramp job overnight, the S&P 500 might appear to be fixed.

…and, with a 26-pt ramp job overnight, the S&P 500 might appear to be fixed.

It clearly closed below an important channel bottom yesterday. But, for years now, these things have been easily fixed in low-volume overnight sessions. SPX has a lot of backtesting to do, offering multiple bounce targets: the broken purple channel bottom from 2009 at 2070, the H&S neckline at 2075, the gray channel midline at 2087…the list goes on. But, will it stay fixed?

SPX has a lot of backtesting to do, offering multiple bounce targets: the broken purple channel bottom from 2009 at 2070, the H&S neckline at 2075, the gray channel midline at 2087…the list goes on. But, will it stay fixed?

continued for members… (more…)

As China melts down, seems there’s precious little being said about the Nikkei. The futures are off almost 5.5% today, and down nearly 8% since the Jun 24 highs. Look for the BOJ to start panicking any time now…