“There’s a world of difference between truth and facts. Facts can obscure the truth.”

— Maya Angelou

For over a year, now, the market’s rallies have been motivated by periodic announcements that the China trade dispute/war was resolved. When that particular narrative faltered, there was often a dovish FOMC-related news blurb of some sort.

At this juncture, neither appears likely to come to the rescue of an ailing market. Through a series of tactical errors, Trump has squandered any advantage he might have enjoyed in negotiations with China. And, investors loudly called BS on the latest report of a “very positive phone call.” Two of them, actually. Yeah, that’s the ticket.

Then, just yesterday, ex-Fed President of NY Bill Dudley suggested that the FOMC should avoid any rate cuts that might “bail out an administration that keeps making bad choices on trade policy.” I was astonished — not that Dudley felt this way, but to see it in print.

As long-time readers know, I have expected for quite some time that the global financial establishment, concerned about the uncertainty that four more years of a Trump administration would entail, would temper or even withdraw its “support” from the market since a correction back to November 2016 levels would neutralize some very important bragging rights.

Whether or not you support Trump or believe he’s on the right path with China, the truth is that a great deal of uncertainty has been injected into the market. Markets dislike uncertainty, as do business owners and managers who have to make decisions which could prove disastrous depending on what the next tweet says. All the “adjusted” earnings reports, massaged economic data and other convenient “facts” can’t change that simple truth.

Trump has a difficult choice to make: go to the Chinese, hat in hand, and beg for a deal that will allow him to announce a victory and save face with his base — many of whom have suffered enormously throughout the trade war — or, be prepared for another 14 months of economic water torture.

* * *

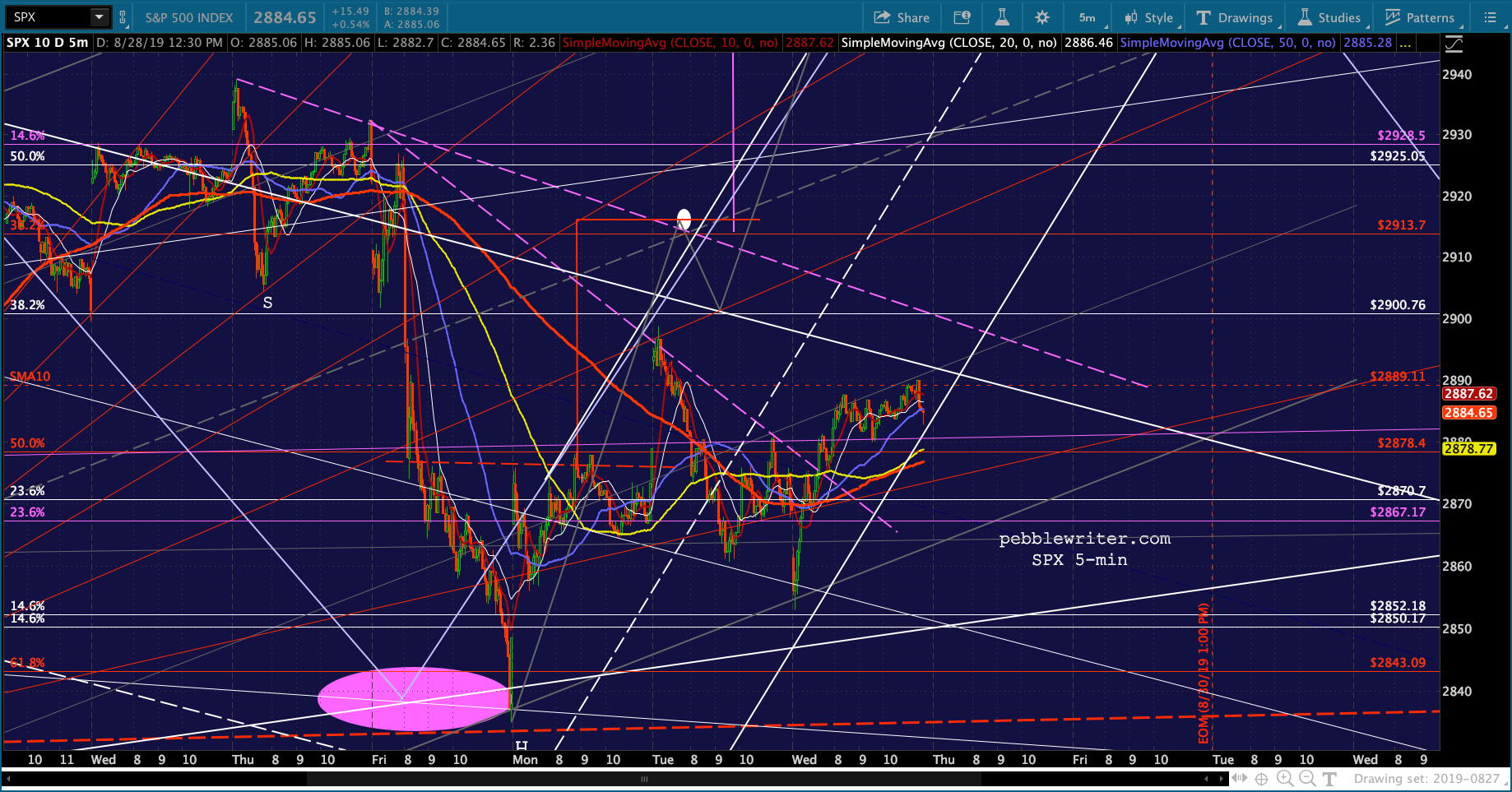

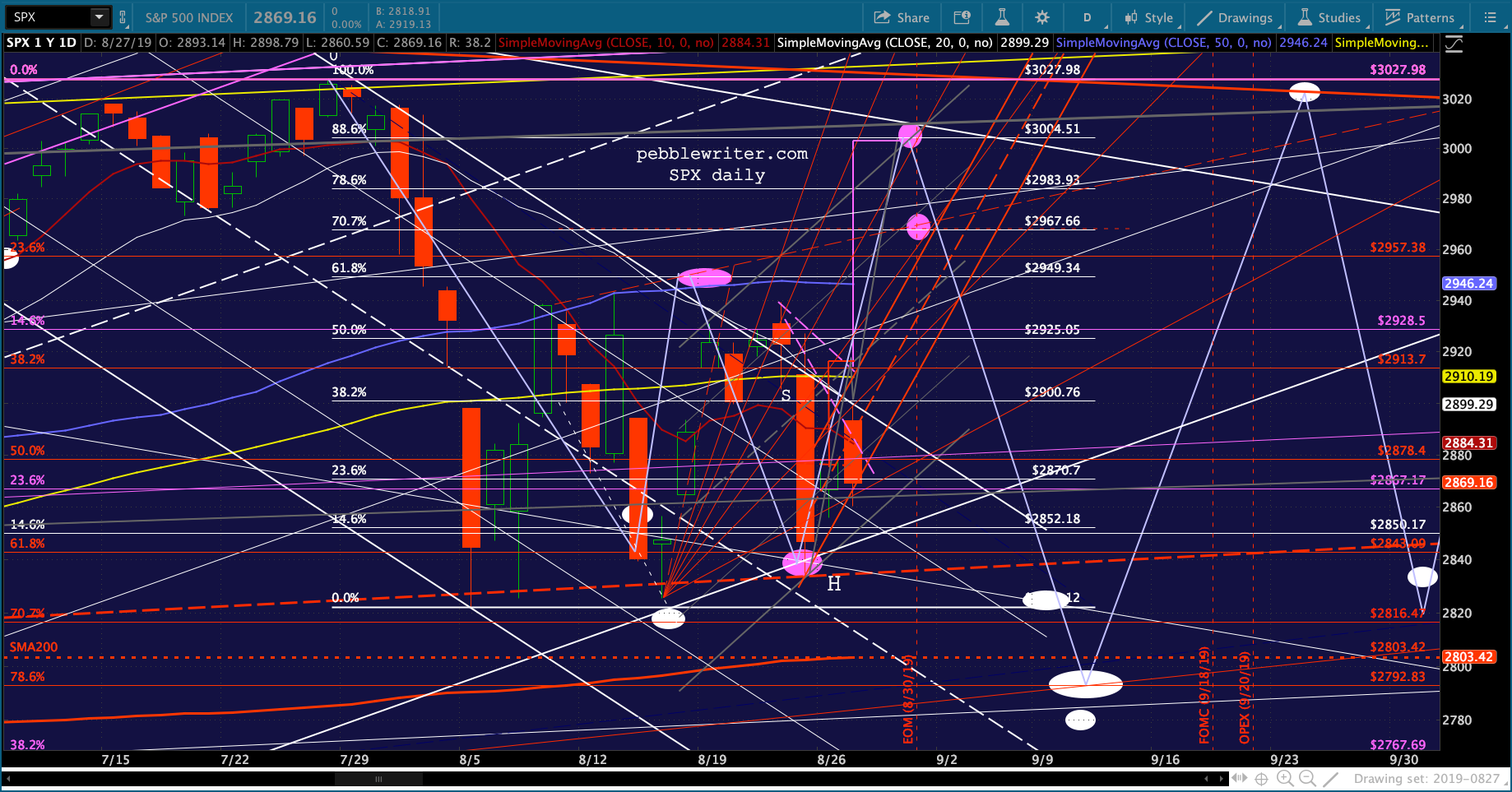

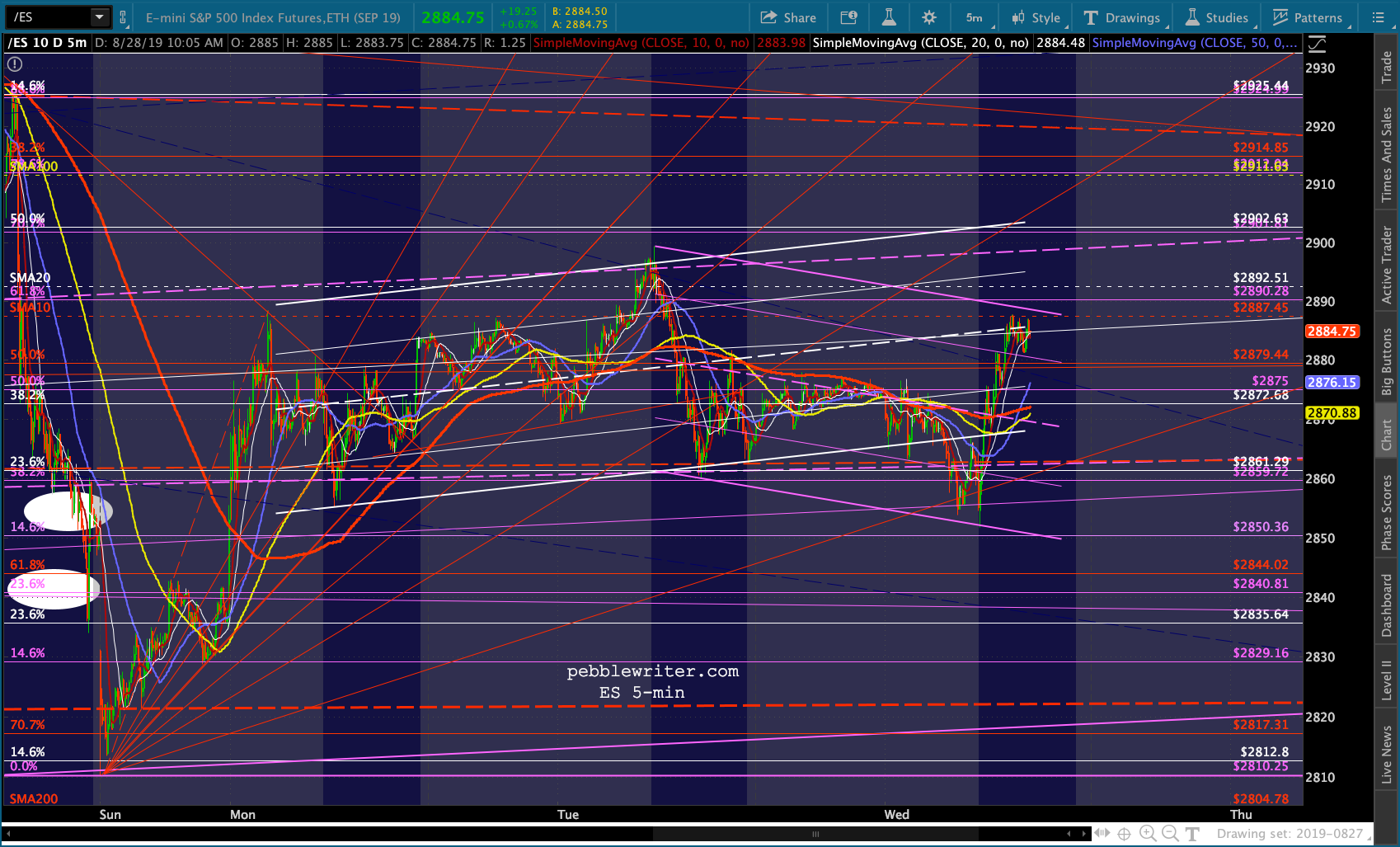

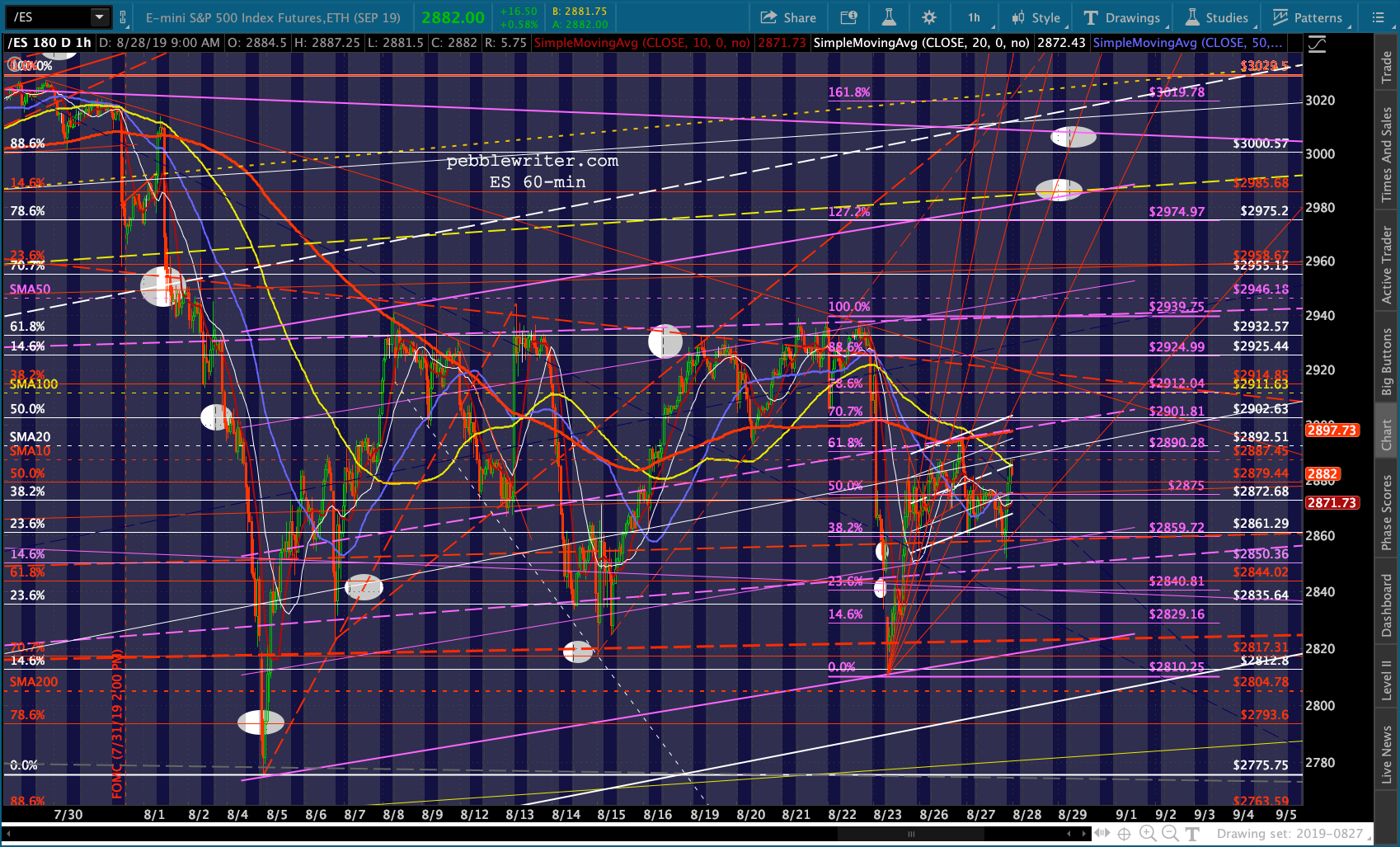

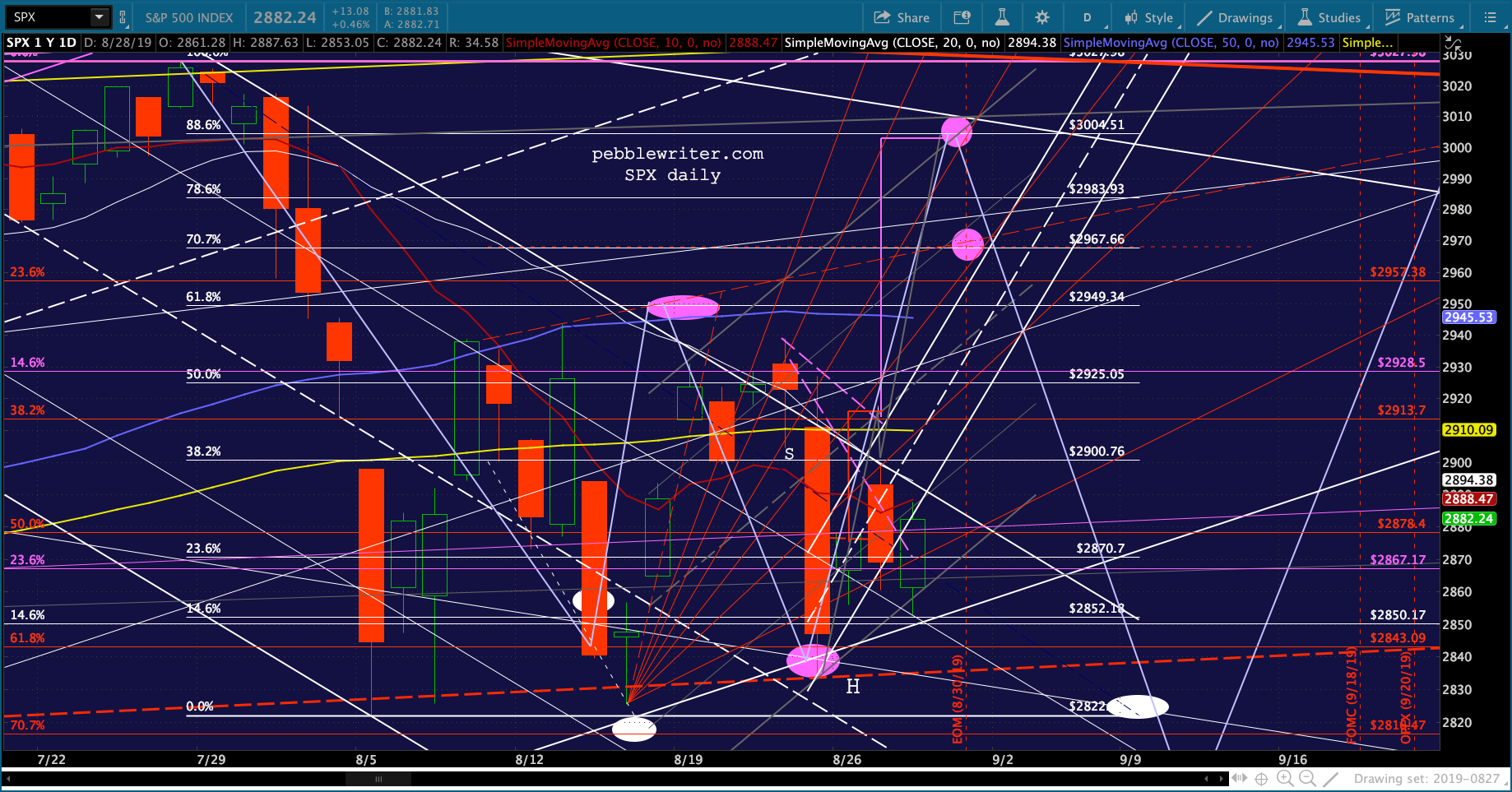

Our analog has been eerily accurate over the past month. When it wasn’t, it was because stocks fell short of upside targets and declined more sharply than expected. We should be in the midst of a multi-day bounce after bottoming where expected on Friday. But, yesterday was a struggle. Can the algos produce higher highs?

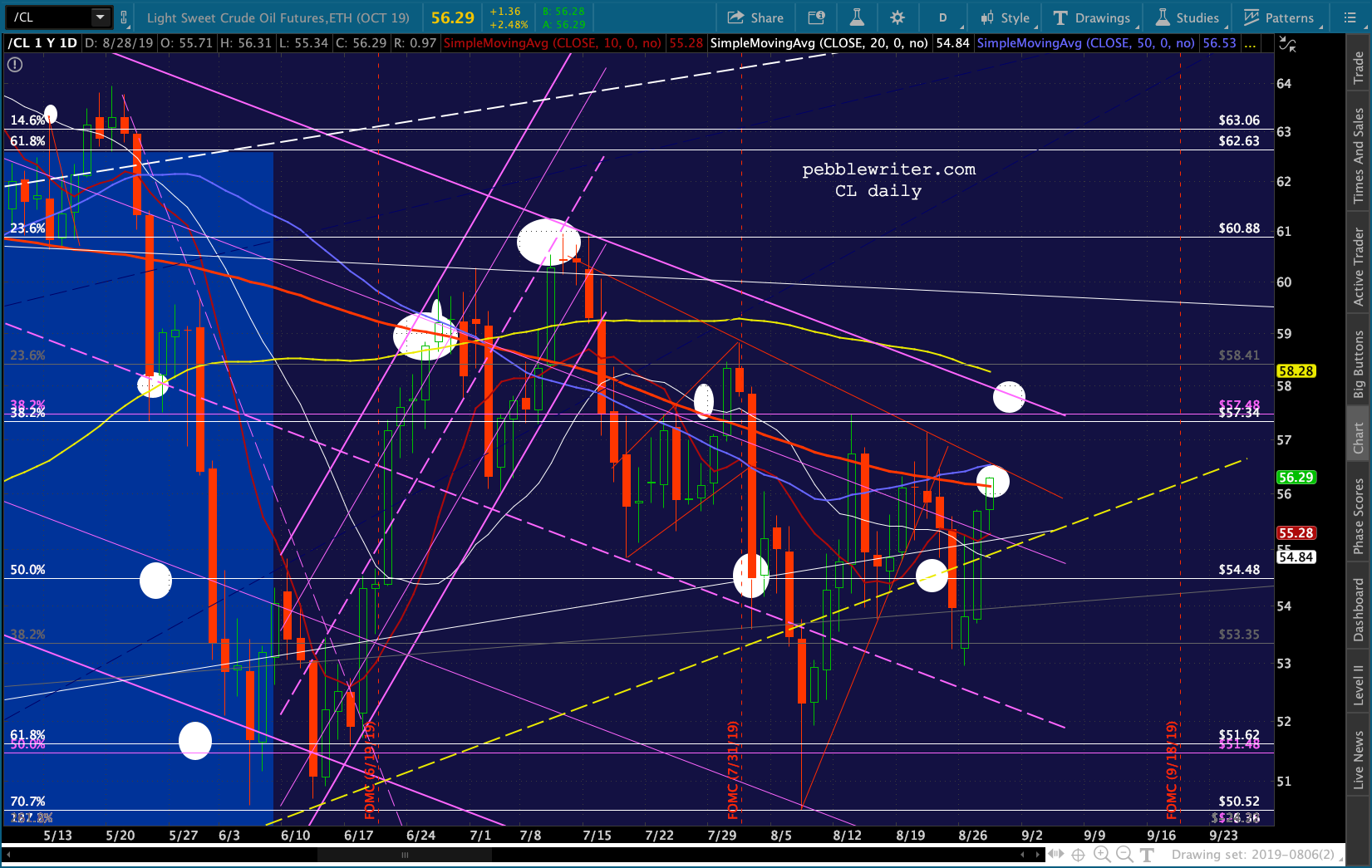

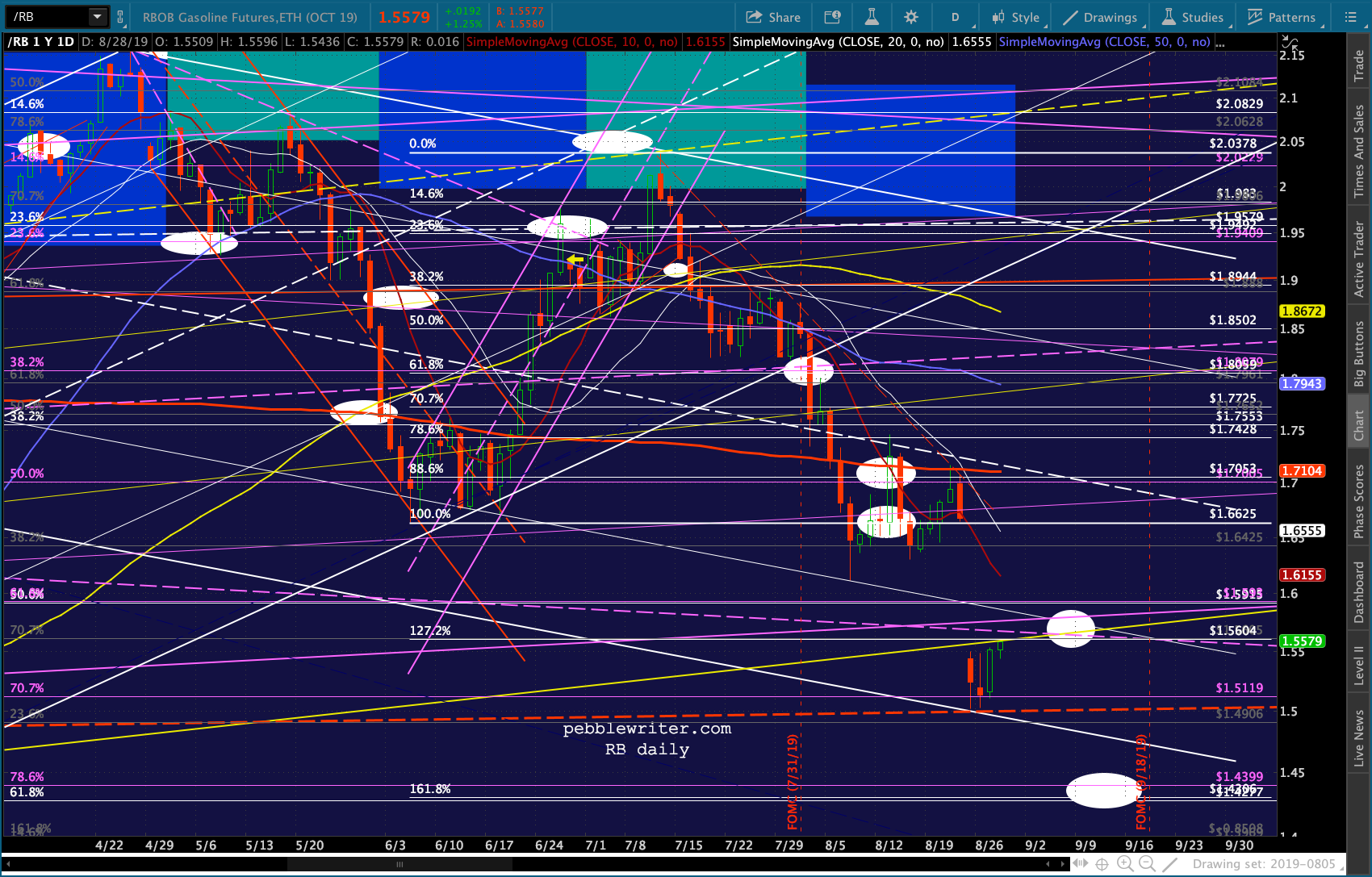

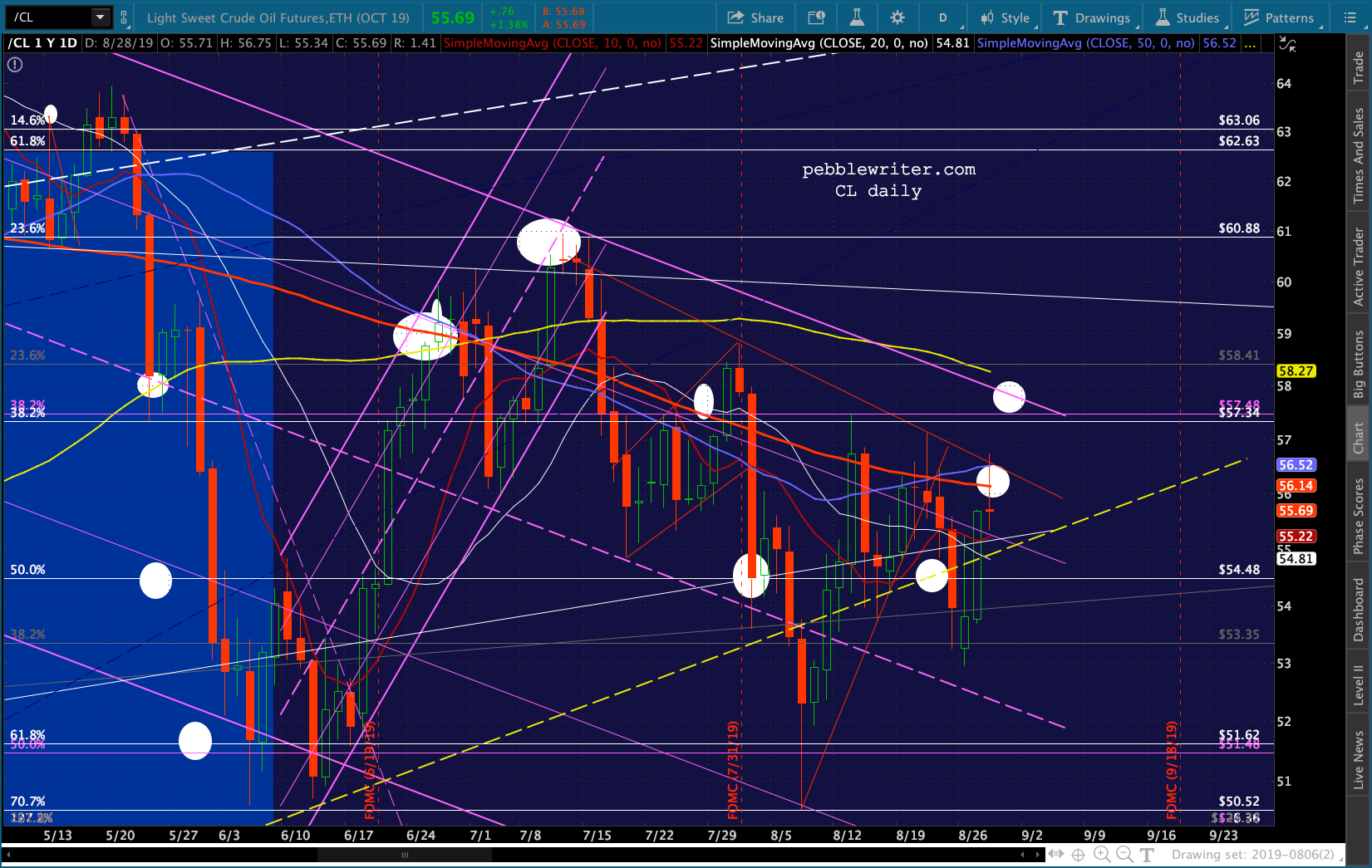

continued for members…Oil is doing all it can, with a bounce last night up through its SMA200 as we expected. This raises some very interesting questions about who controls which data and, thus, which algo factors.

continued for members…Oil is doing all it can, with a bounce last night up through its SMA200 as we expected. This raises some very interesting questions about who controls which data and, thus, which algo factors.

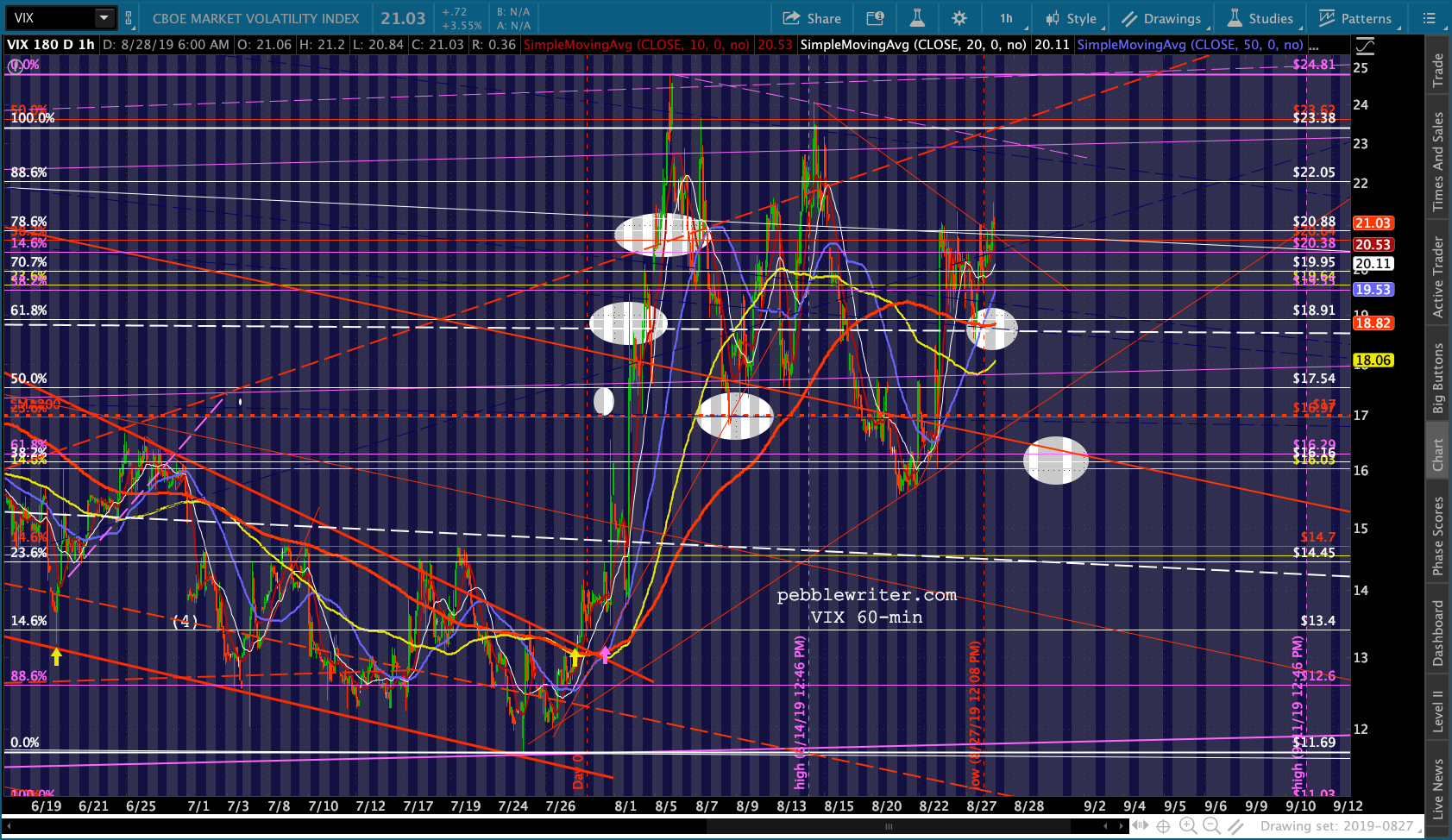

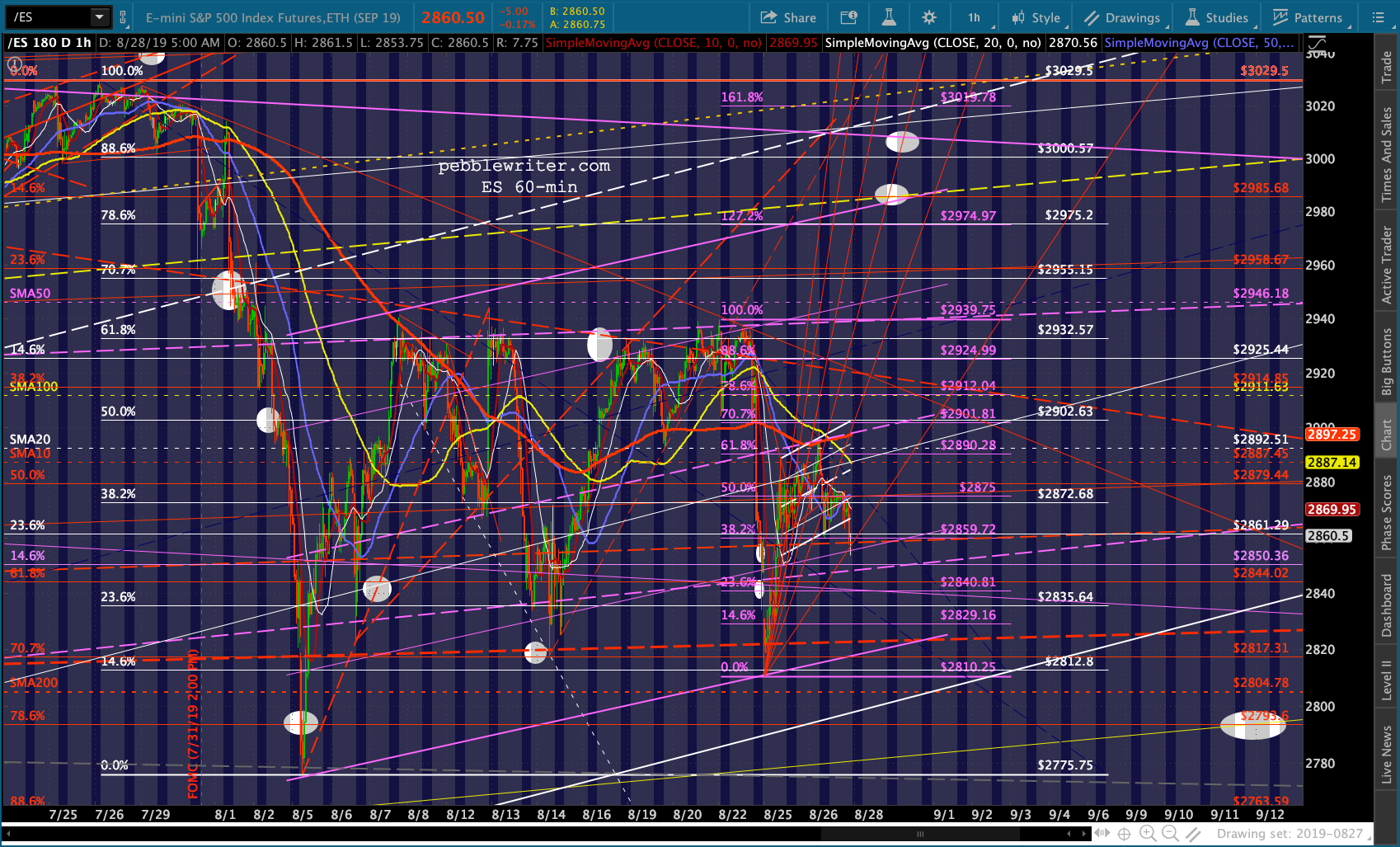

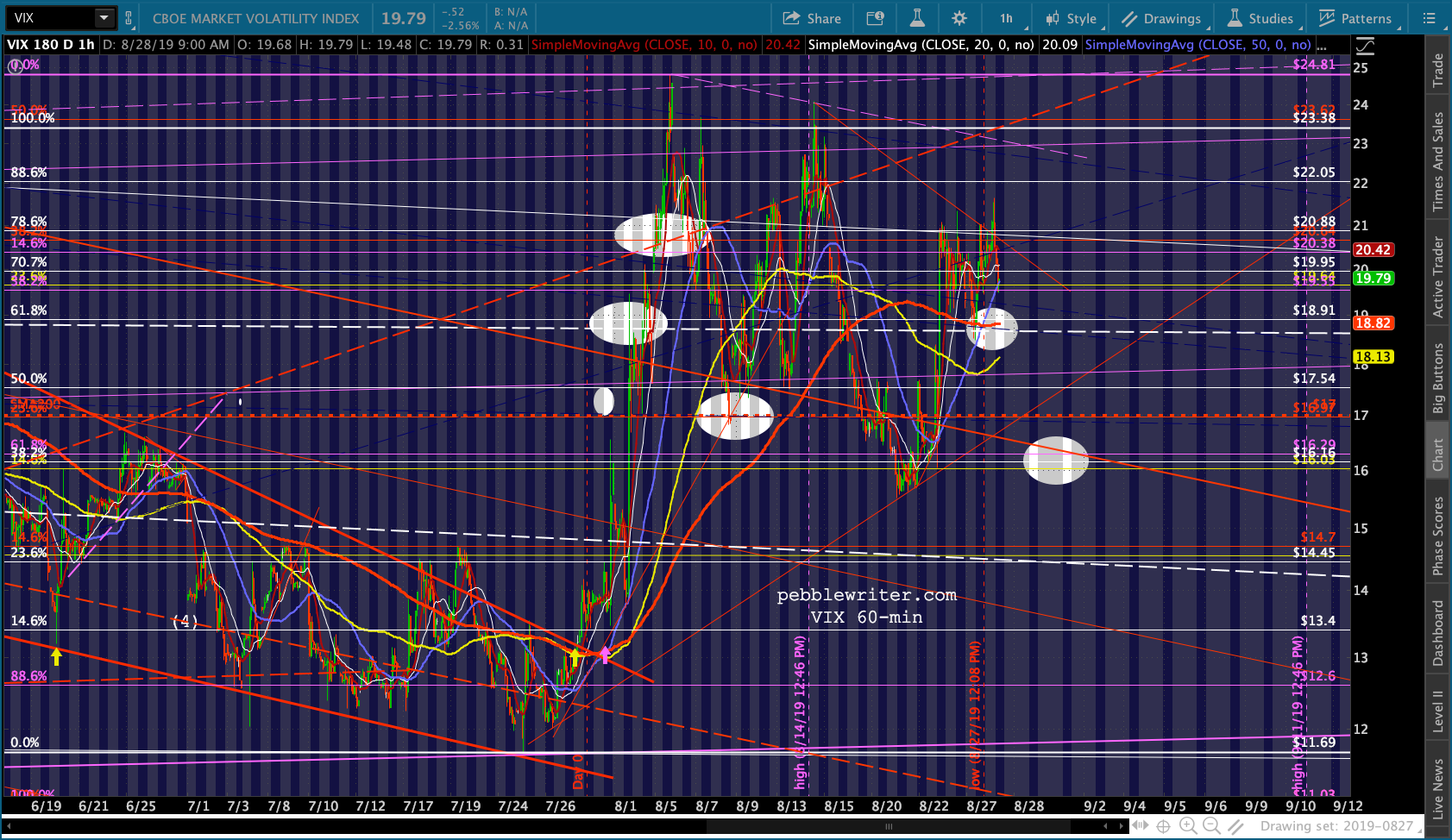

But, VIX will need to reverse its mini-breakout if stocks are to make any headway.

But, VIX will need to reverse its mini-breakout if stocks are to make any headway.

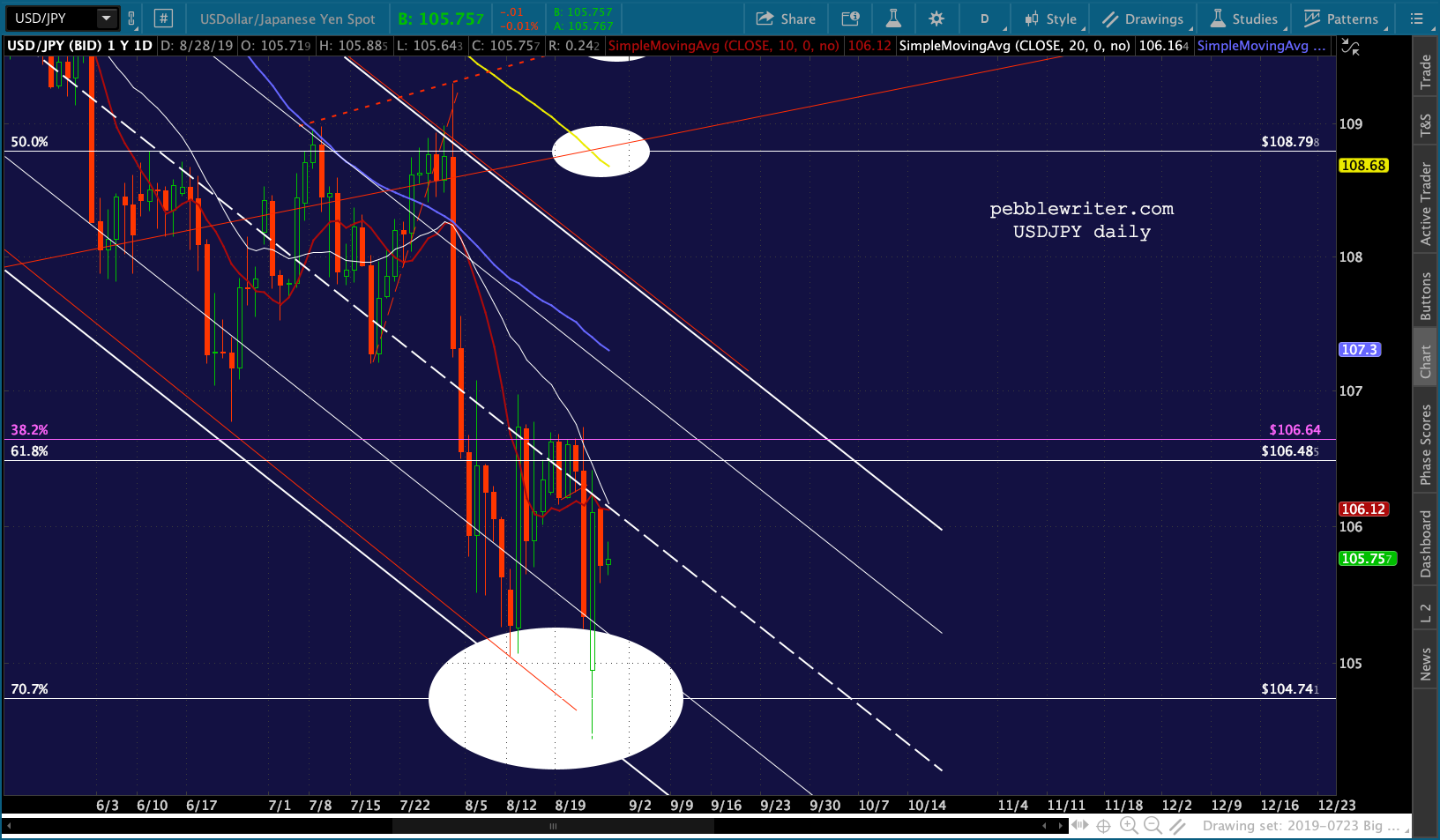

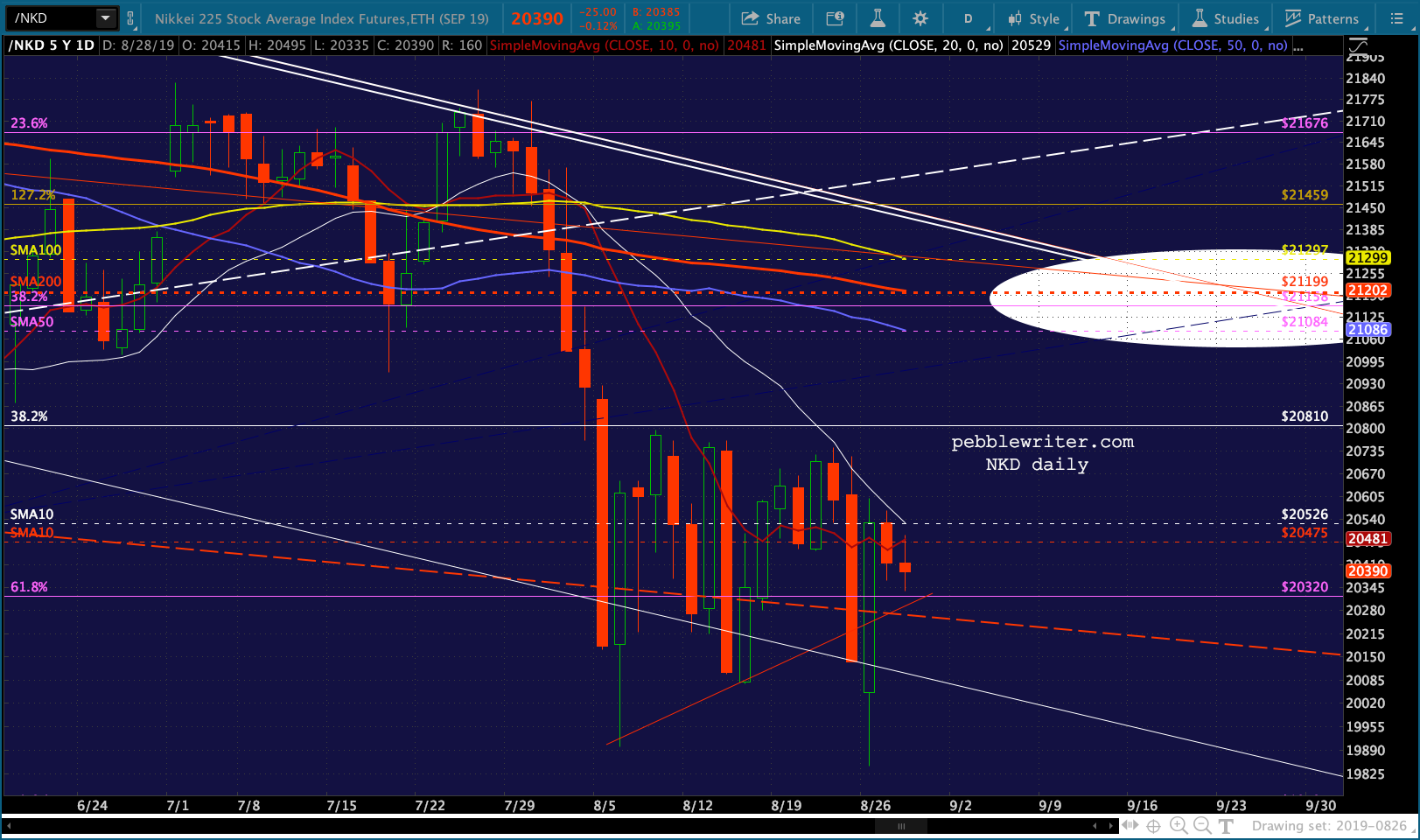

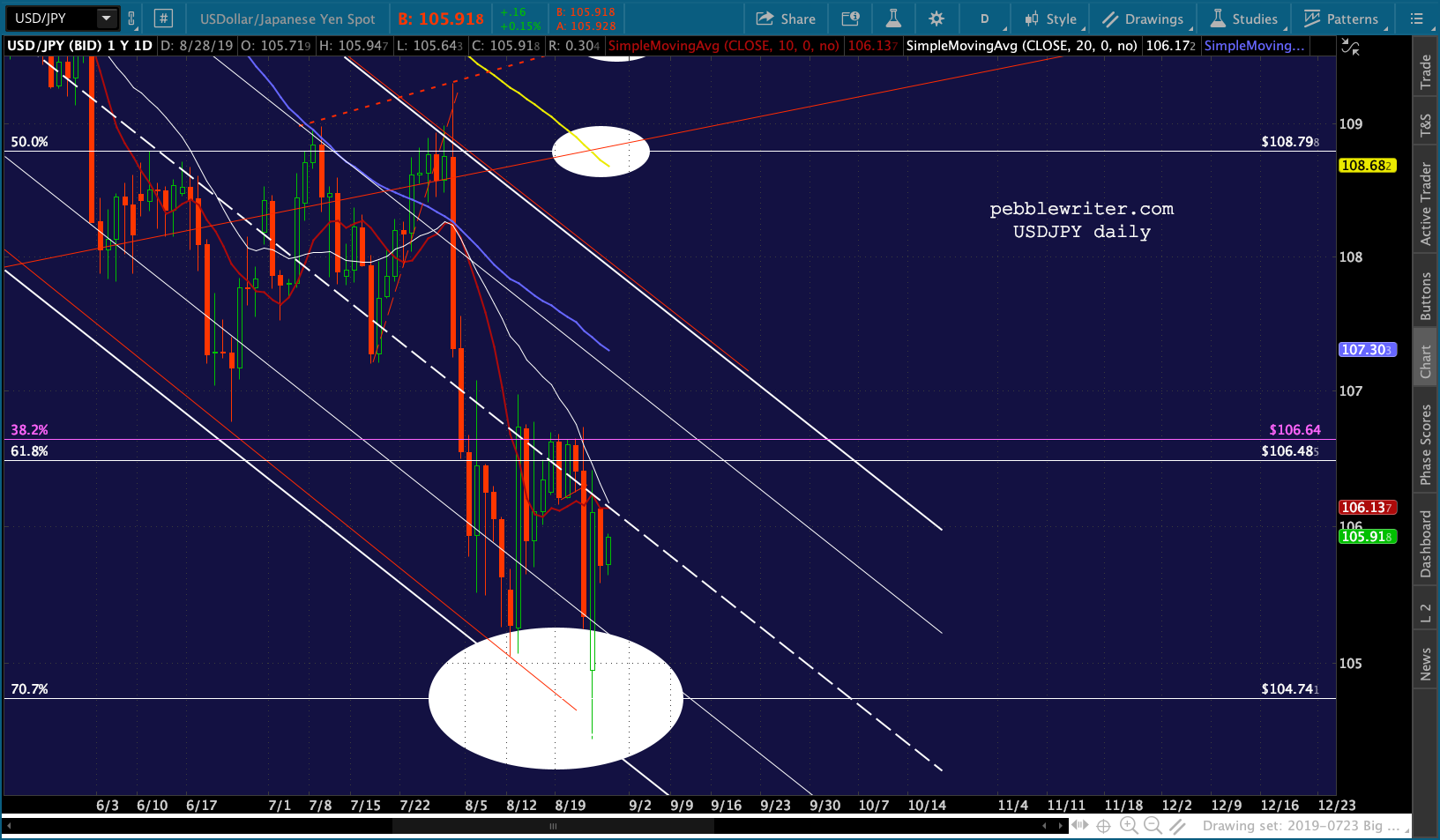

The most troubling development for bulls is that USDJPY has made little headway since bouncing at our latest downside target. It tested and pulled back from its SMA10 — not a good sign for bulls.

The most troubling development for bulls is that USDJPY has made little headway since bouncing at our latest downside target. It tested and pulled back from its SMA10 — not a good sign for bulls. The NKD, which I view as the first derivative of the yen carry trade-oriented USDJPY, has similarly gone nowhere.

The NKD, which I view as the first derivative of the yen carry trade-oriented USDJPY, has similarly gone nowhere. This leaves SPX in a tough spot, with much help needed but, so far, a lukewarm response from the algos. As I wrote yesterday, either we’re not going to get higher highs or this has been a really great headfake.

This leaves SPX in a tough spot, with much help needed but, so far, a lukewarm response from the algos. As I wrote yesterday, either we’re not going to get higher highs or this has been a really great headfake.

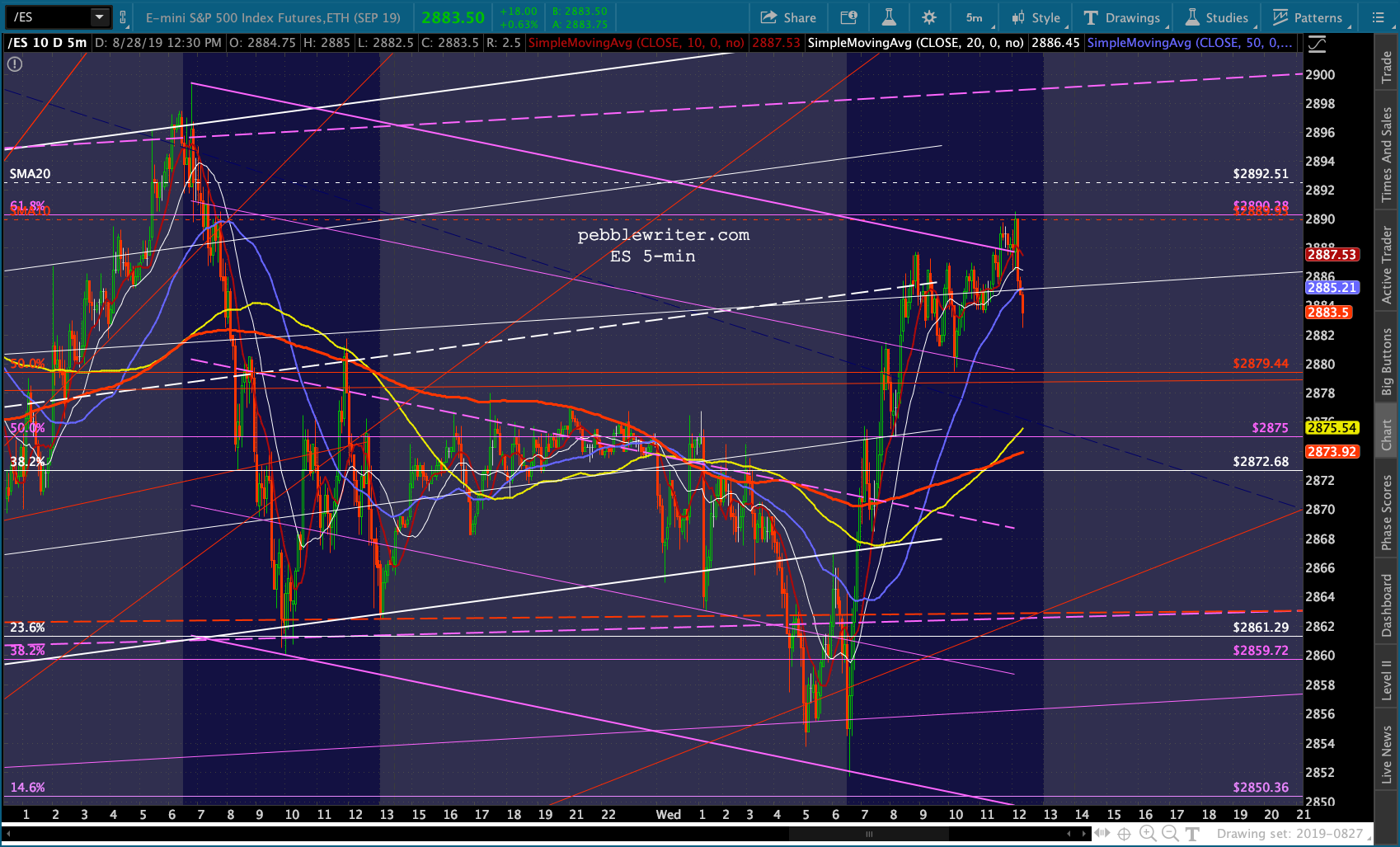

SPX’s and ES’ SMA10s are currently just below its SMA20s (2887 vs 2893.) One good rally would put them back on top, which should help. Otherwise, the picture looks really weak.

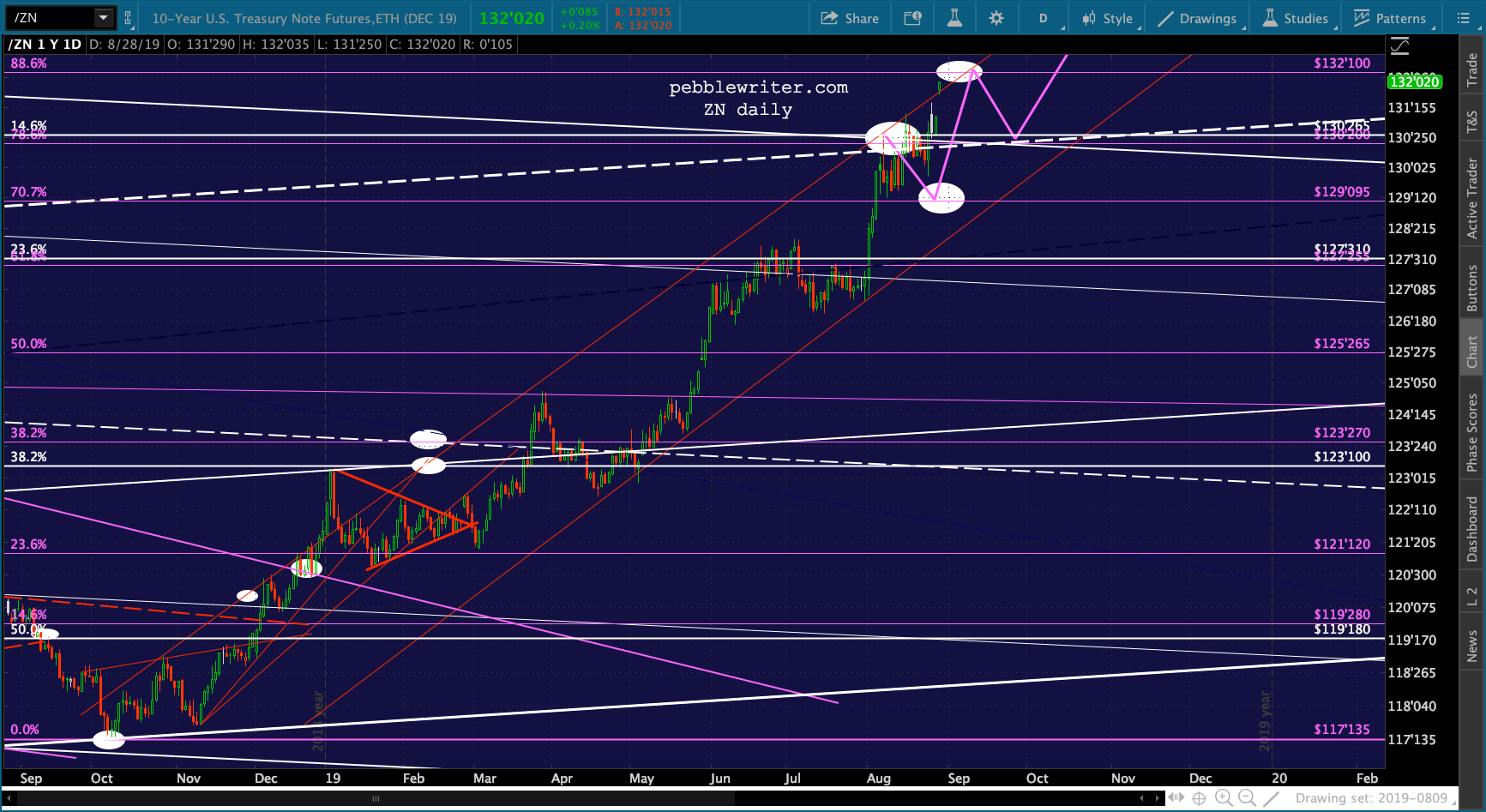

Note that ZN has nearly reached our next upside target – the .886 at 132’100. A pullback here, which would mean a rise in the 10Y yields, would at least temporarily steepen the 2s10s and could reduce some fears about a recession.

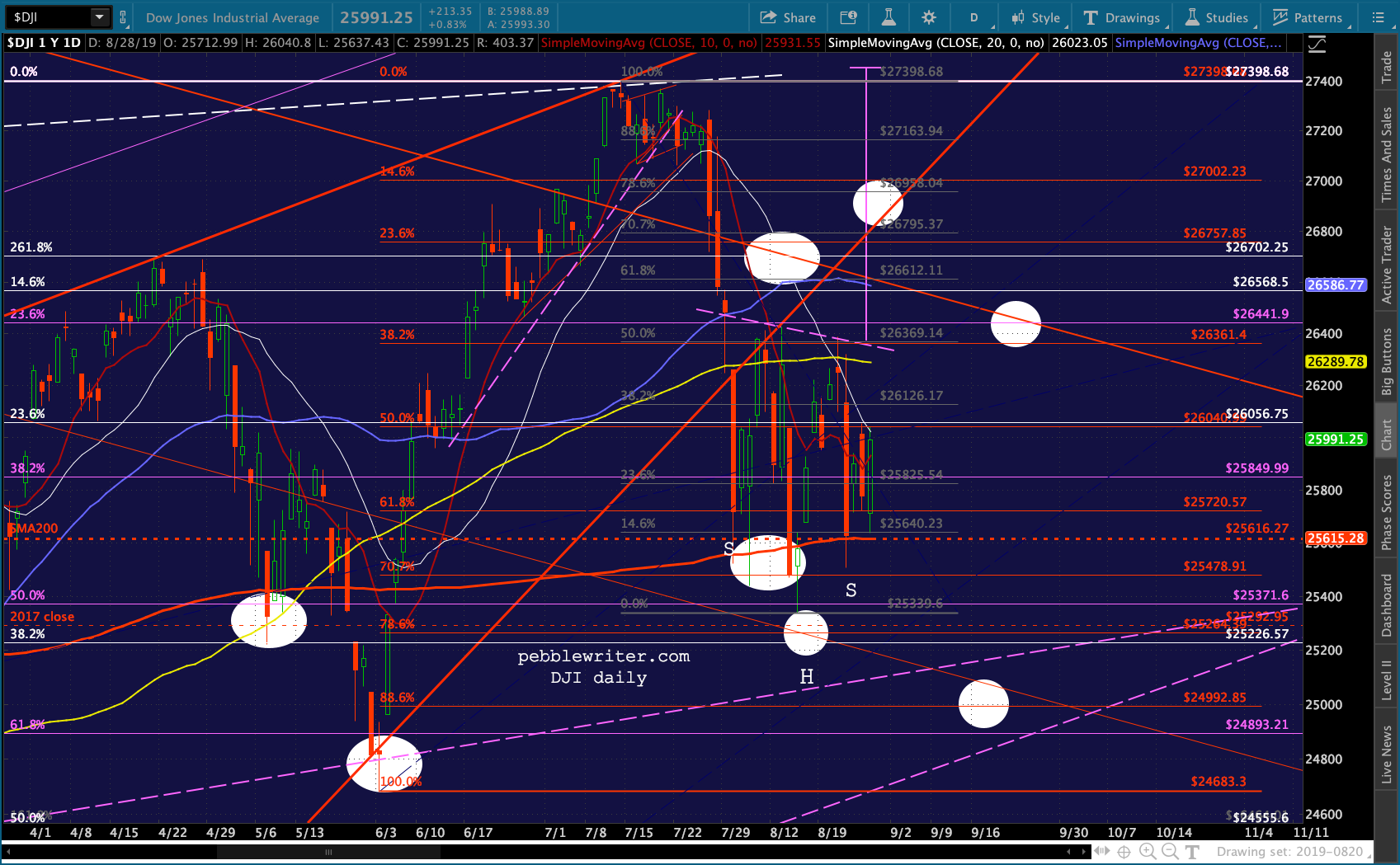

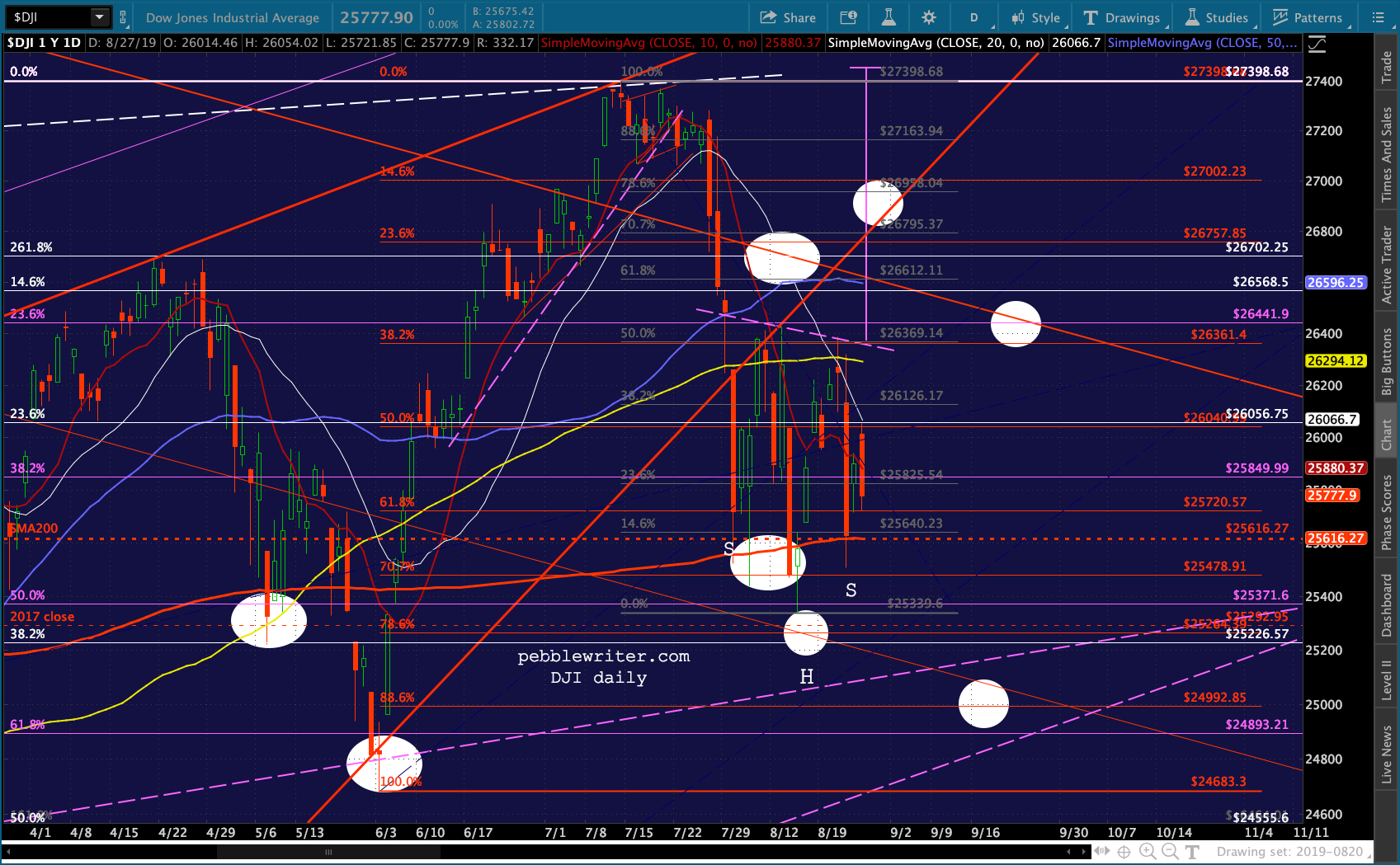

Note that ZN has nearly reached our next upside target – the .886 at 132’100. A pullback here, which would mean a rise in the 10Y yields, would at least temporarily steepen the 2s10s and could reduce some fears about a recession. Last, though I don’t really spend much time on the Dow, it’s an interesting measure of mainstream bullishness and manipulation. It’s currently sitting about 550 points from completing a nice little IH&S which would target new all-time highs. A failure to even reach the neckline (26350ish) would speak volumes.

Last, though I don’t really spend much time on the Dow, it’s an interesting measure of mainstream bullishness and manipulation. It’s currently sitting about 550 points from completing a nice little IH&S which would target new all-time highs. A failure to even reach the neckline (26350ish) would speak volumes. More later.

More later.

UPDATE: 12:40 PM

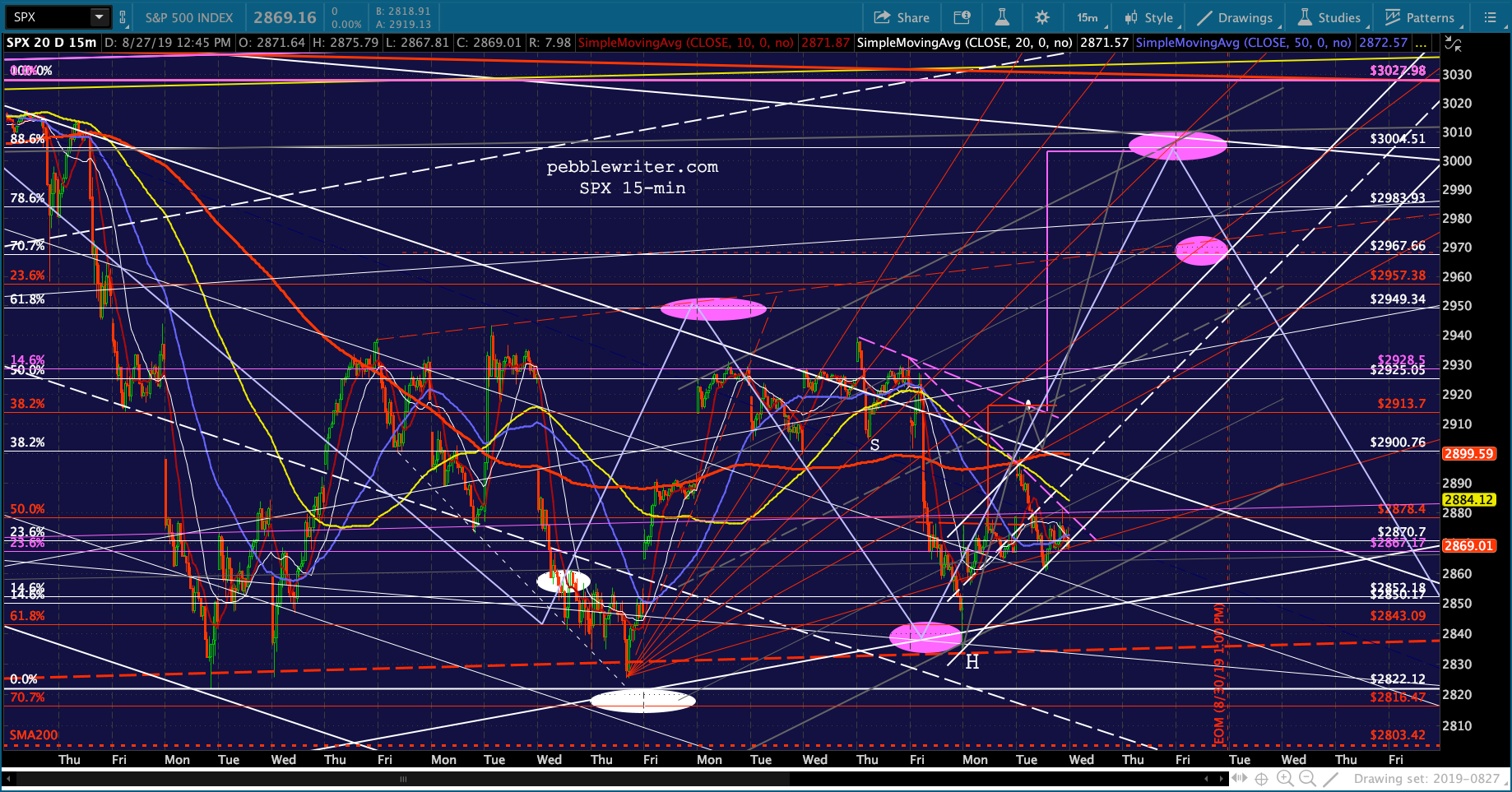

ES and SPX are testing their SMA10s. If the rally is to keep going, this is important resistance to overcome.

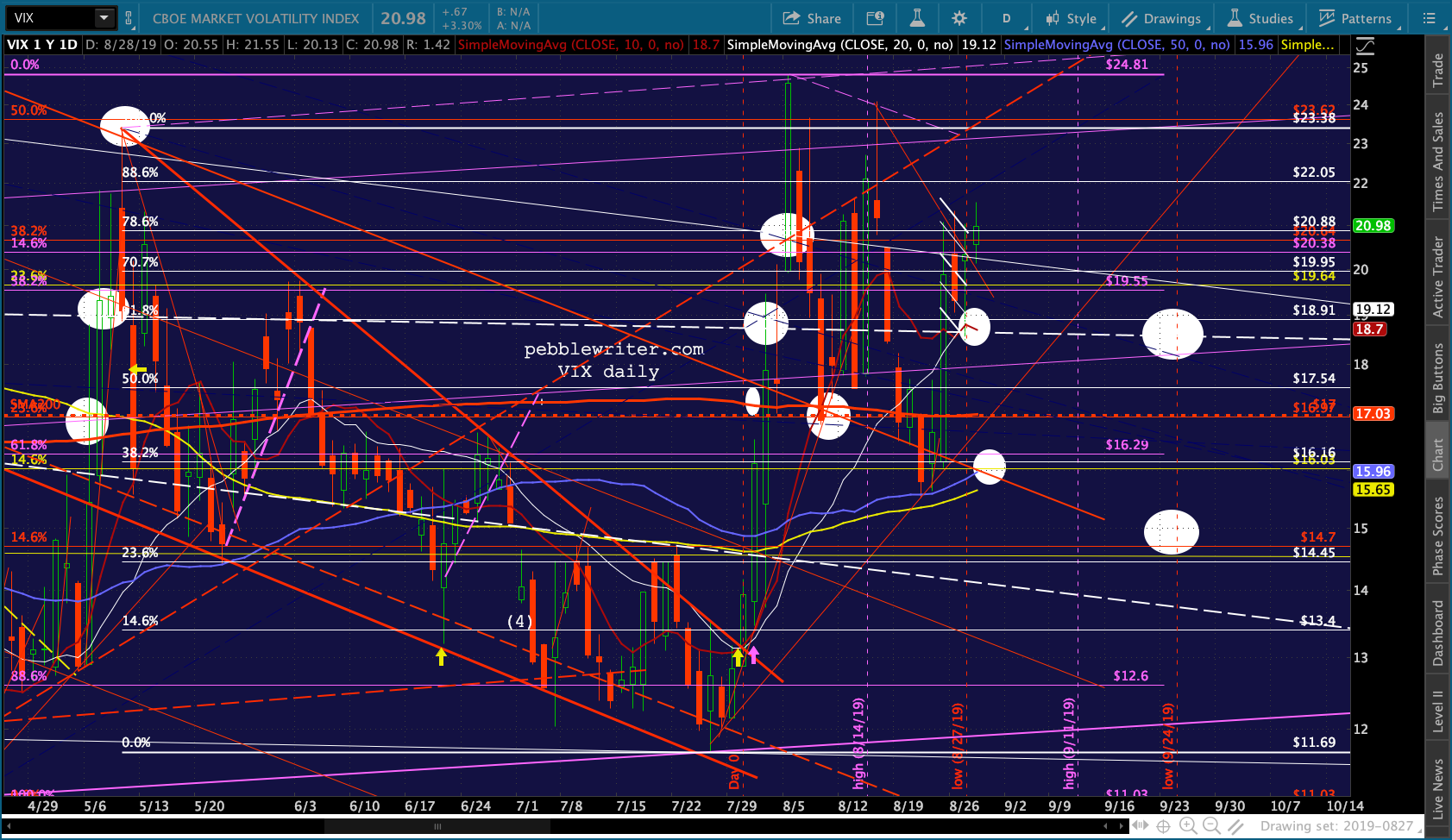

VIX has erased its breakout, but is making a very minimal effort so far.

VIX has erased its breakout, but is making a very minimal effort so far. Note that CL has backed off its SMA200…

Note that CL has backed off its SMA200…  …and, USDJPY has still gone nowhere.

…and, USDJPY has still gone nowhere. Again, if this rally is to continue, we’re going to need participation from all of these factors. I hope I’m wrong, as it would help affirm the analog. But, right now, there’s not much evidence that they will.

Again, if this rally is to continue, we’re going to need participation from all of these factors. I hope I’m wrong, as it would help affirm the analog. But, right now, there’s not much evidence that they will.

UPDATE: 3:30 PM

Going into the close still on the edge of the SMA10…it’s anyone’s guess.