Futures are flat as algos weigh positive durable goods orders against tariffs to be announced next Wednesday and PCE due out this Friday.

One thing for certain: Trump is hyper focused on the markets, with the second tariff clawback in as many days just 30 minutes ago – this one suggesting that tariffs will be “more lenient than reciprocal” as SPX tries to hang on to its 200-day moving average.

Funny how the softer tone began at about the same time that SPX had dropped 10% from all-time highs.

The financial press seems to be gradually coming around to the point of view we first espoused months ago: tariffs will be a headwind to both the real economy and the markets.

There is no question that consumers will suffer under tariffs as prices on affected goods will increase. Some tariffs will induce consumers to switch to domestic producers. But, we’ve seen in the past that domestic producers use the price increases of foreign producers as an opportunity to raise their own prices. Either way, consumers pay more.

Trump’s argument is that corporations with foreign production as well as foreign producers will bring manufacturing to the US in order to avoid paying tariffs. This is nonsense. It’s incredibly expensive and time consuming to build new production facilities which will have to be staffed by employees who must be paid multiples of their foreign counterparts.

There are exceptions, of course. But, by and large, consumers will pay the price – especially those on the economic margins for whom inflation is the most damaging. Inflation will remain above the Fed’s target 2% and likely increase; interest rates will remain elevated (forget about rate cuts); and, the risk of stagflation will increase.

The Fed will be boxed in, unable to lower interest rates to support a slowing economy while unable to raise them to combat rising inflation. Even wealthy Americans who aren’t very impacted by rising prices will surely notice the impact on their equity portfolios.

Theoretically, an increase in productivity could revive an economy mired in stagflation. But, in reality, the usual cure is a recession – meaning a reset of real and financial asset prices. No joy. This is why Wall Street is crossing its collective fingers that Trump will announce limited, targeted tariffs and use the threat of deeper, broader tariffs to force trade concessions from our trade partners.

The threat of effectively losing access to the US market might be significant enough to force their hands. But, Canada, Mexico, China, Japan and the EU couldn’t be blamed for responding as a parent might to a tantruming child. When deprived of his cookie (a rising stock market) it’s possible that Trump will quit kicking and screaming.

Stay tuned.

continued for members…

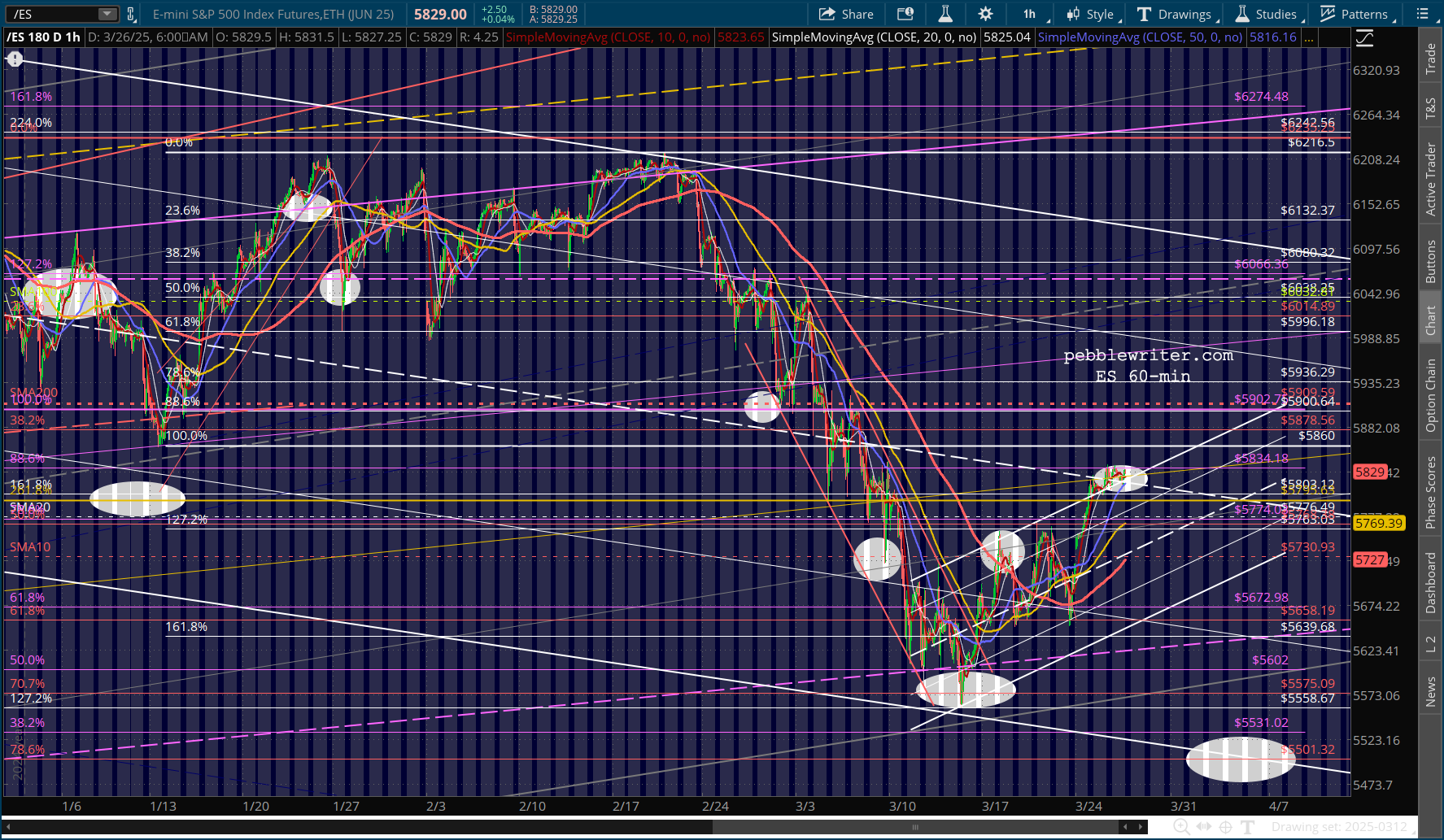

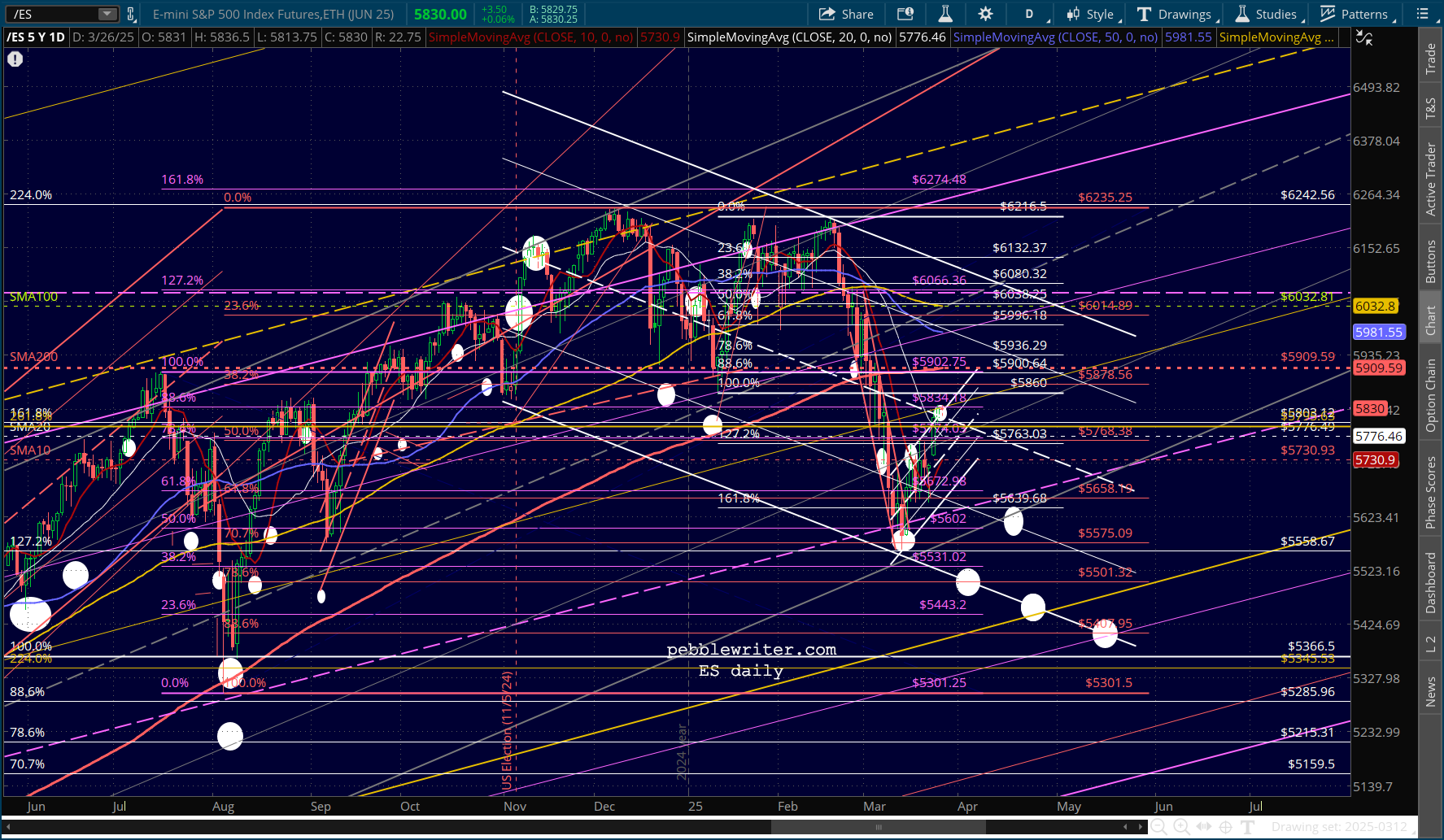

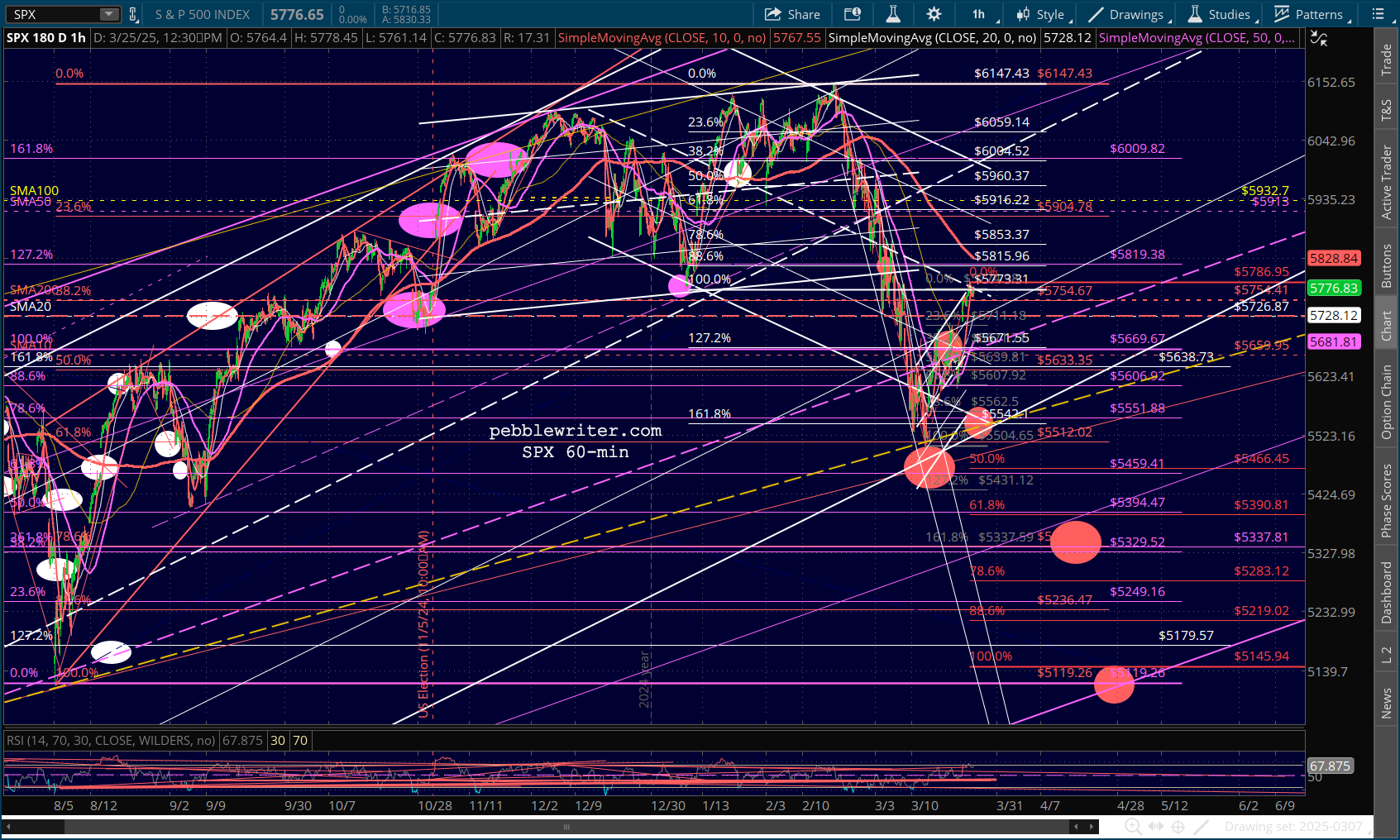

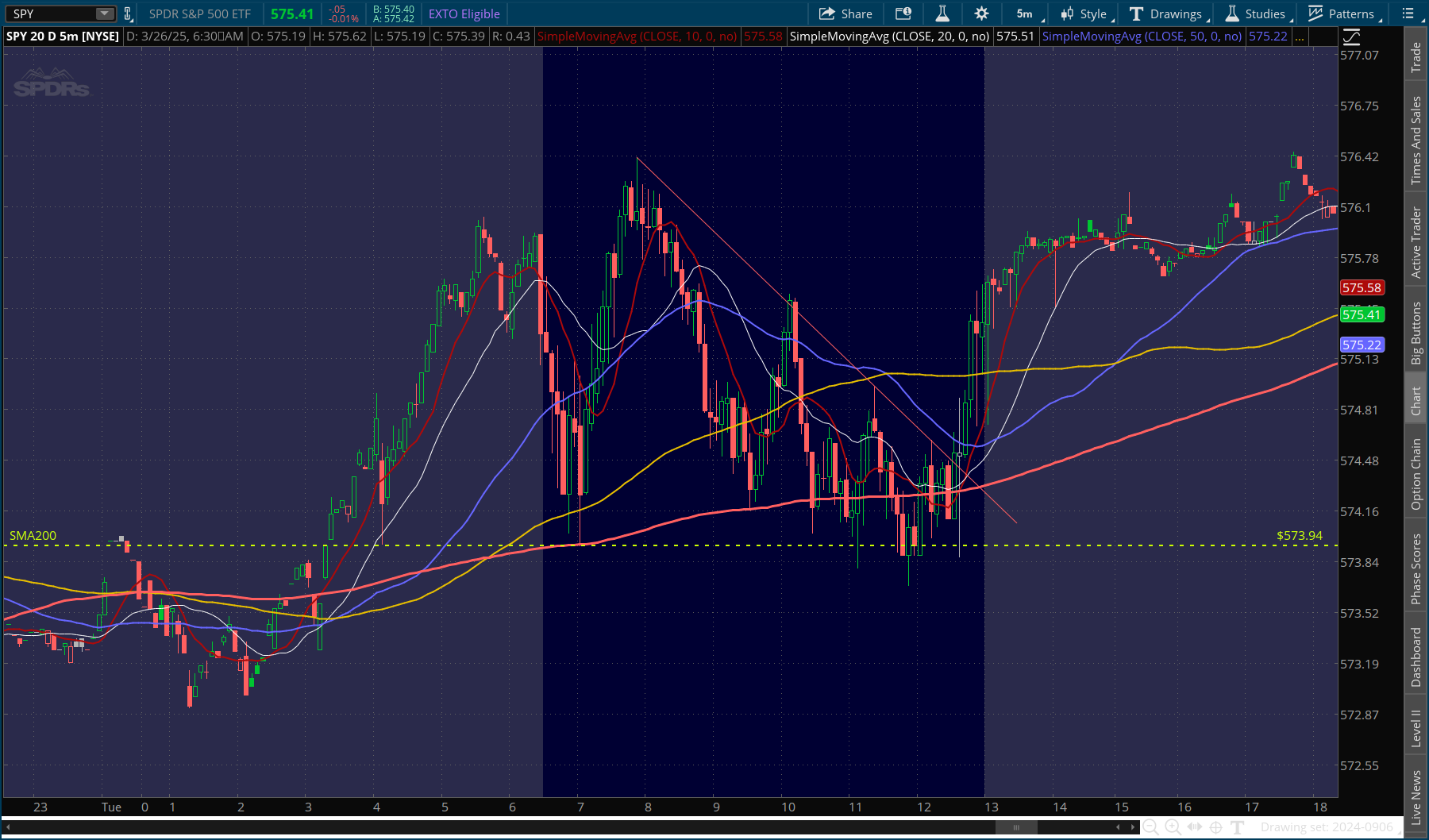

Stocks remain where they were yesterday, with ES well below its SMA200 and SPX propped up just above its. Needless to say, this is important support. So, if it doesn’t hold, our downside targets start looking very good.

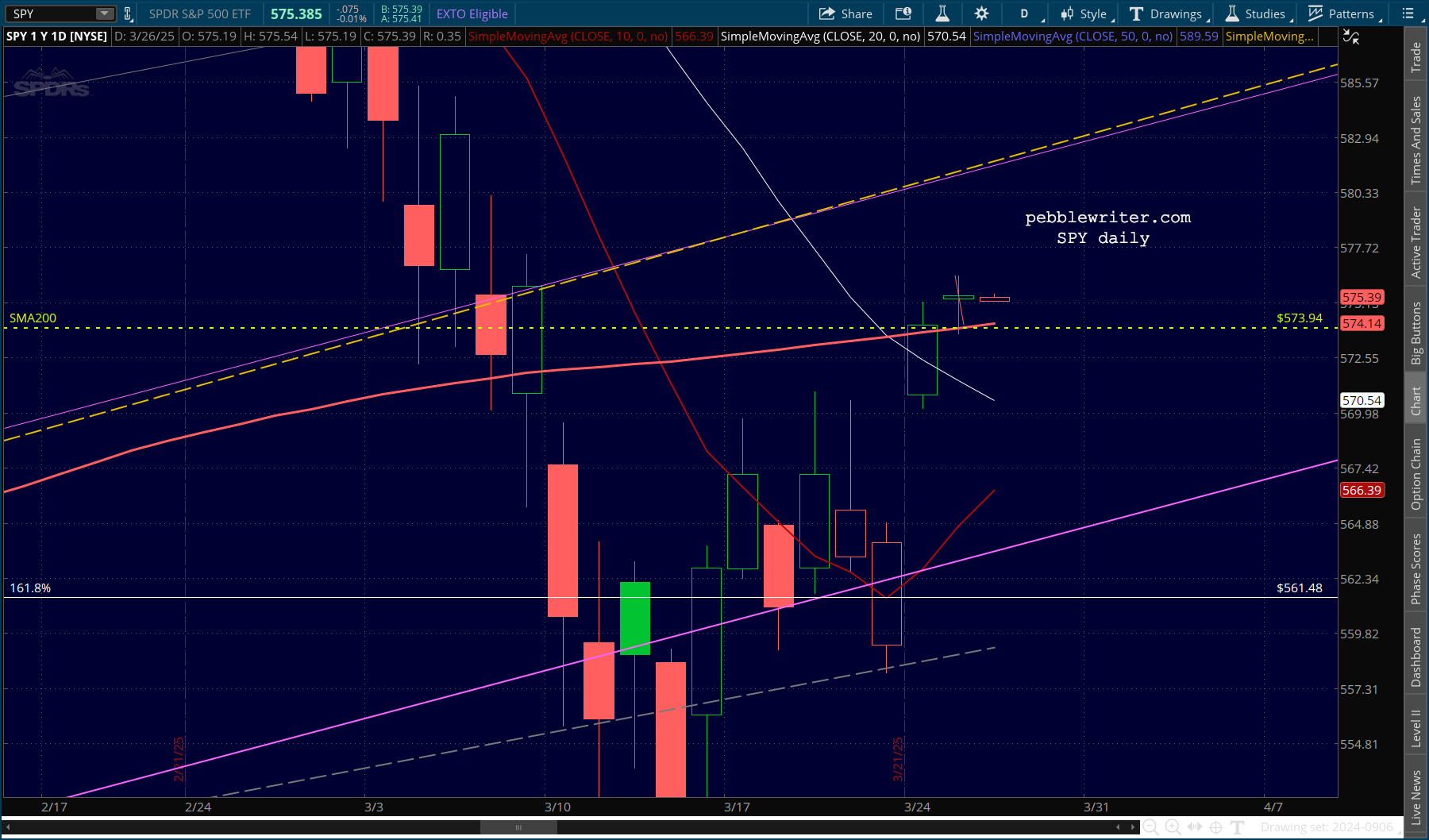

The manipulation was pretty obvious in SPY, which bounced off its SMA200…

The manipulation was pretty obvious in SPY, which bounced off its SMA200…

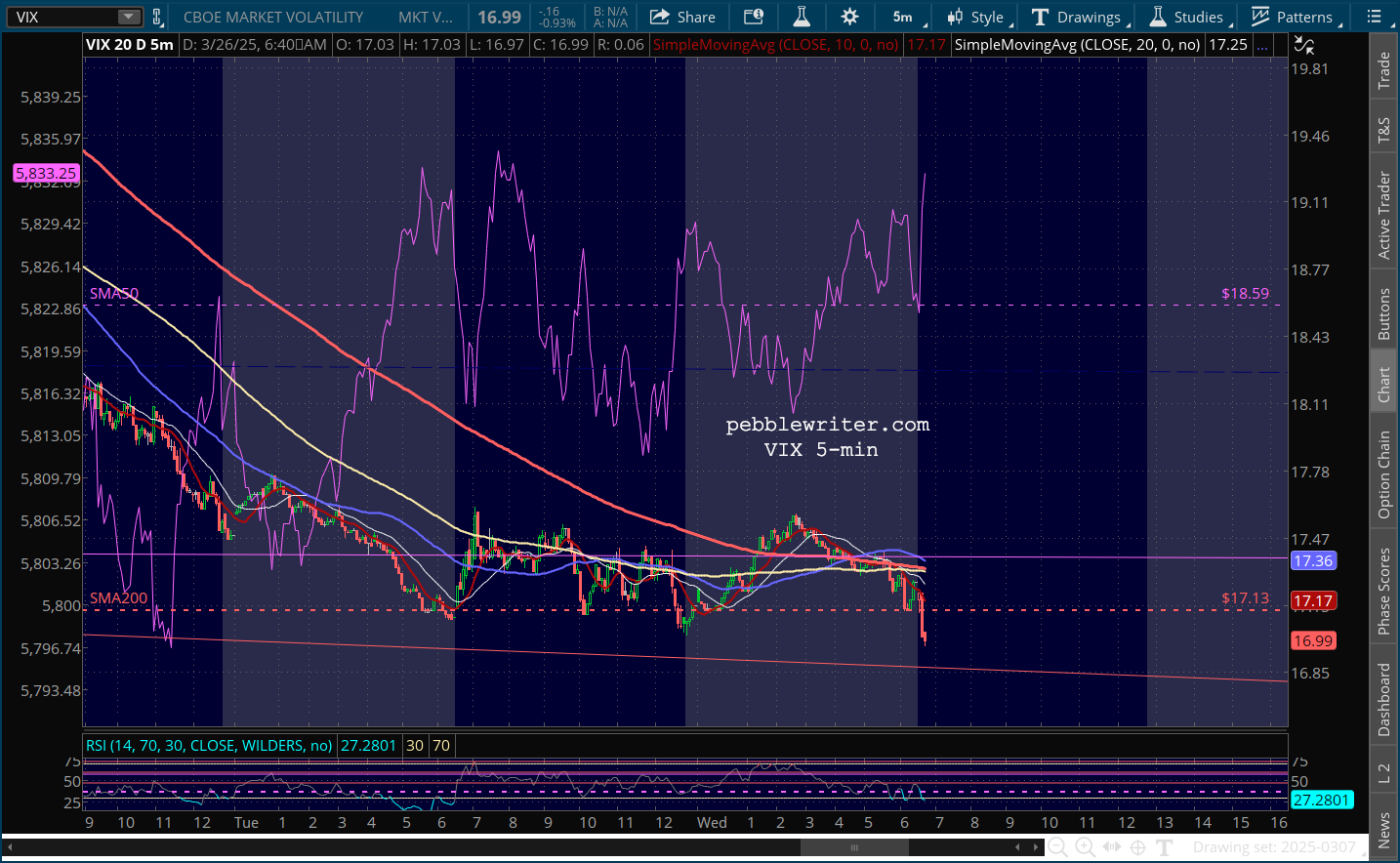

… every time VIX dipped below its SMA200. It continues this morning.

… every time VIX dipped below its SMA200. It continues this morning.

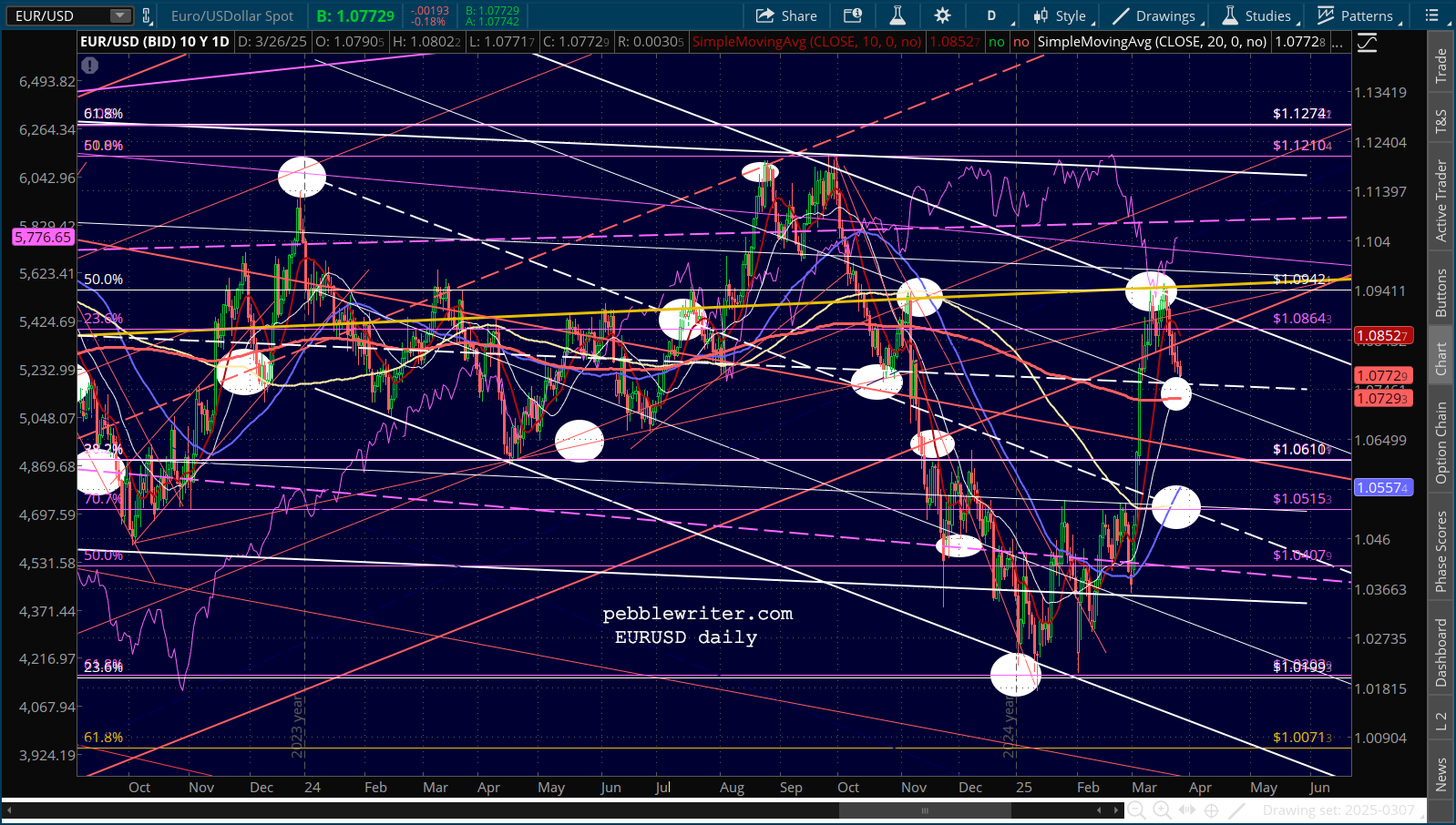

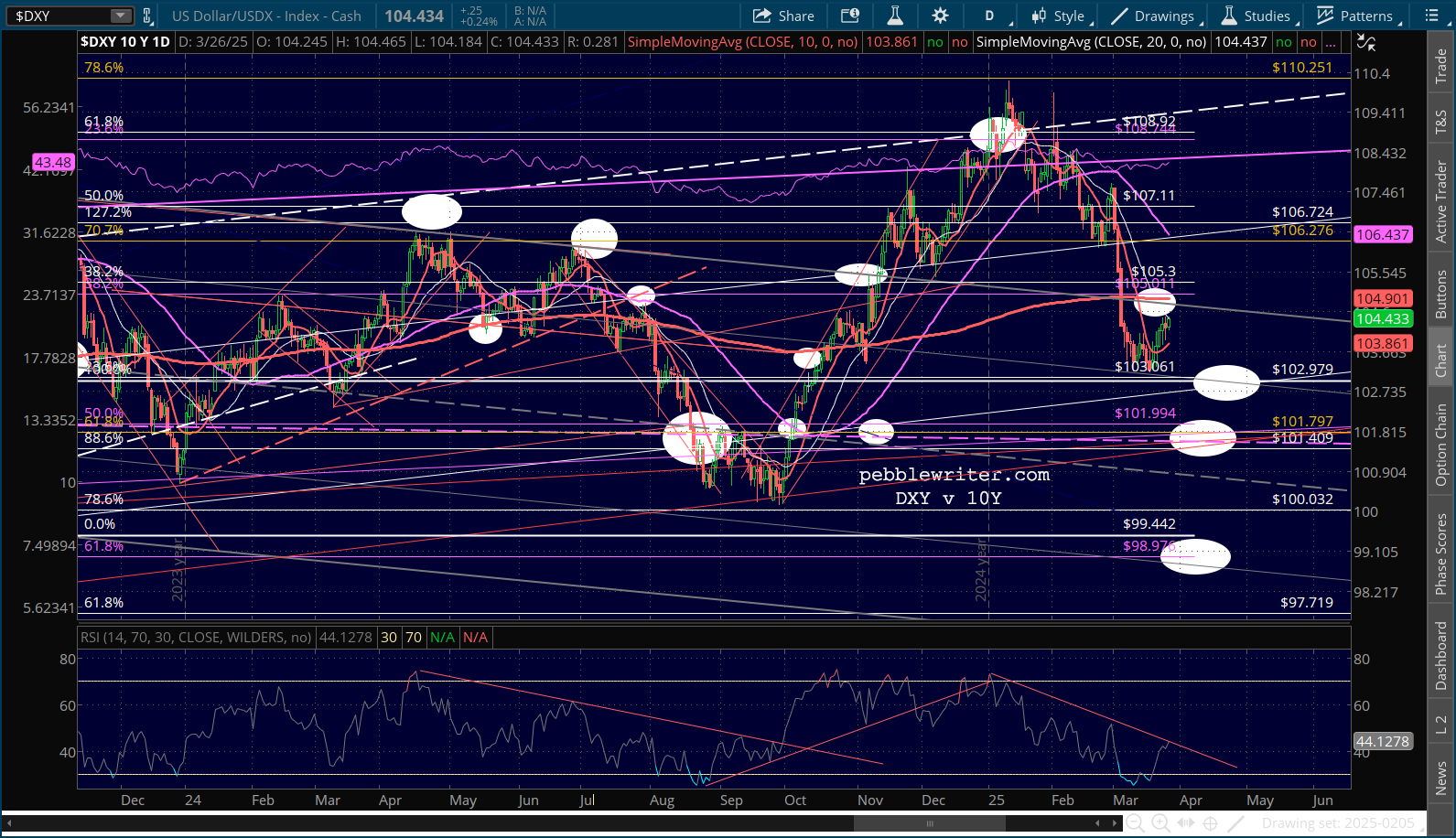

Currencies are little changed, though the USD continues to creep up toward its SMA200.

Currencies are little changed, though the USD continues to creep up toward its SMA200.

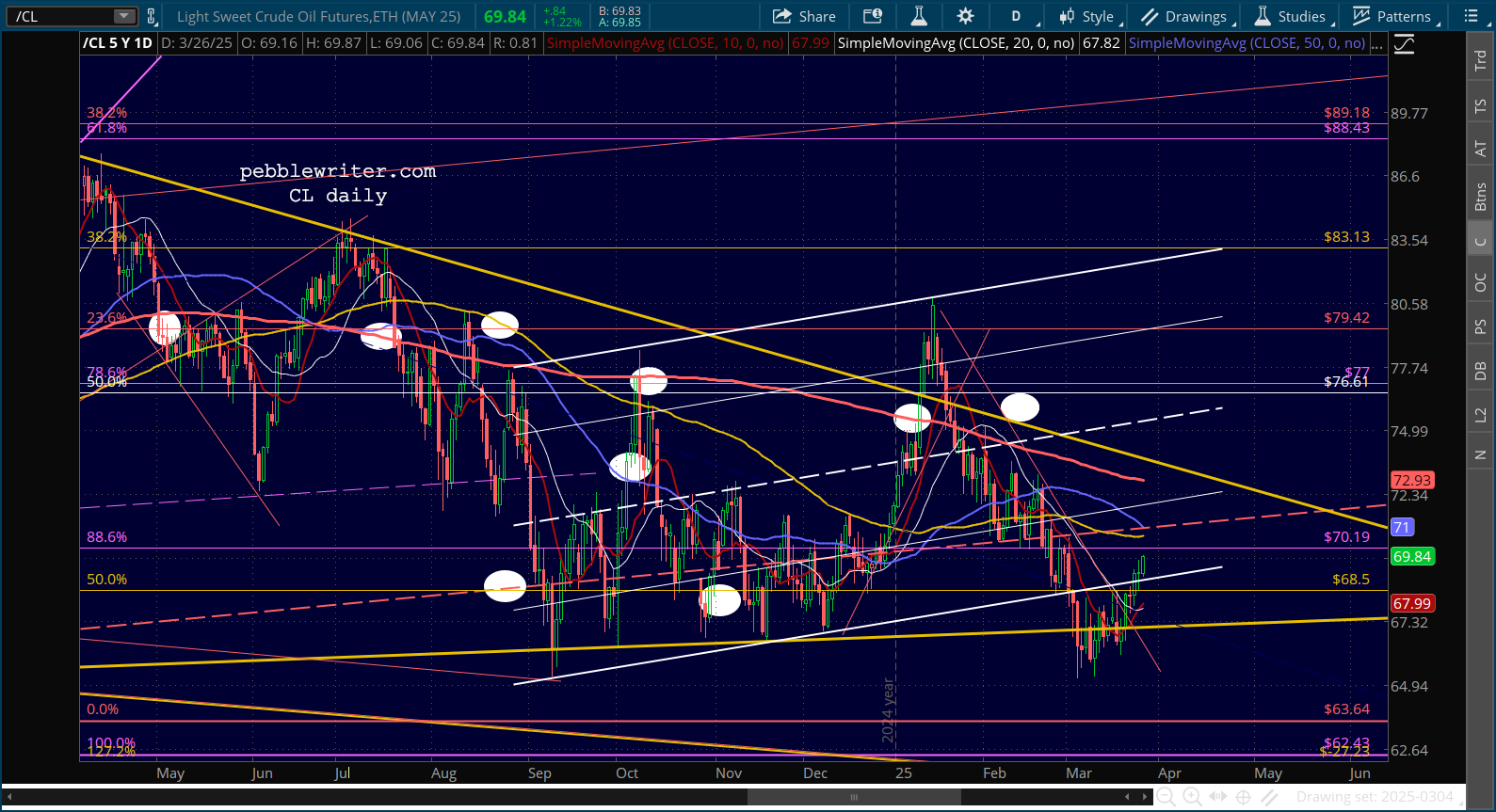

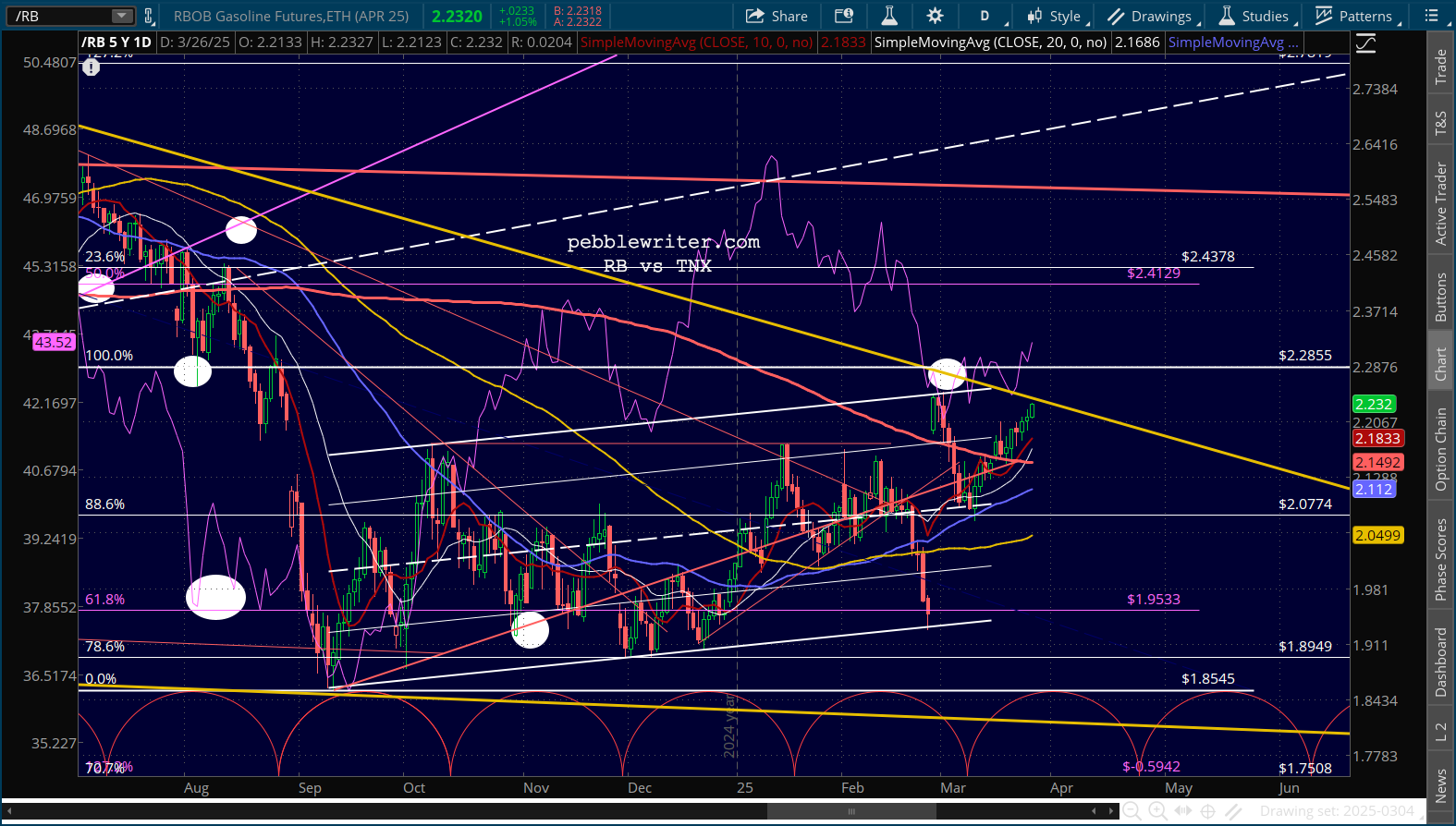

Oil and gas continue to rise…

Oil and gas continue to rise…

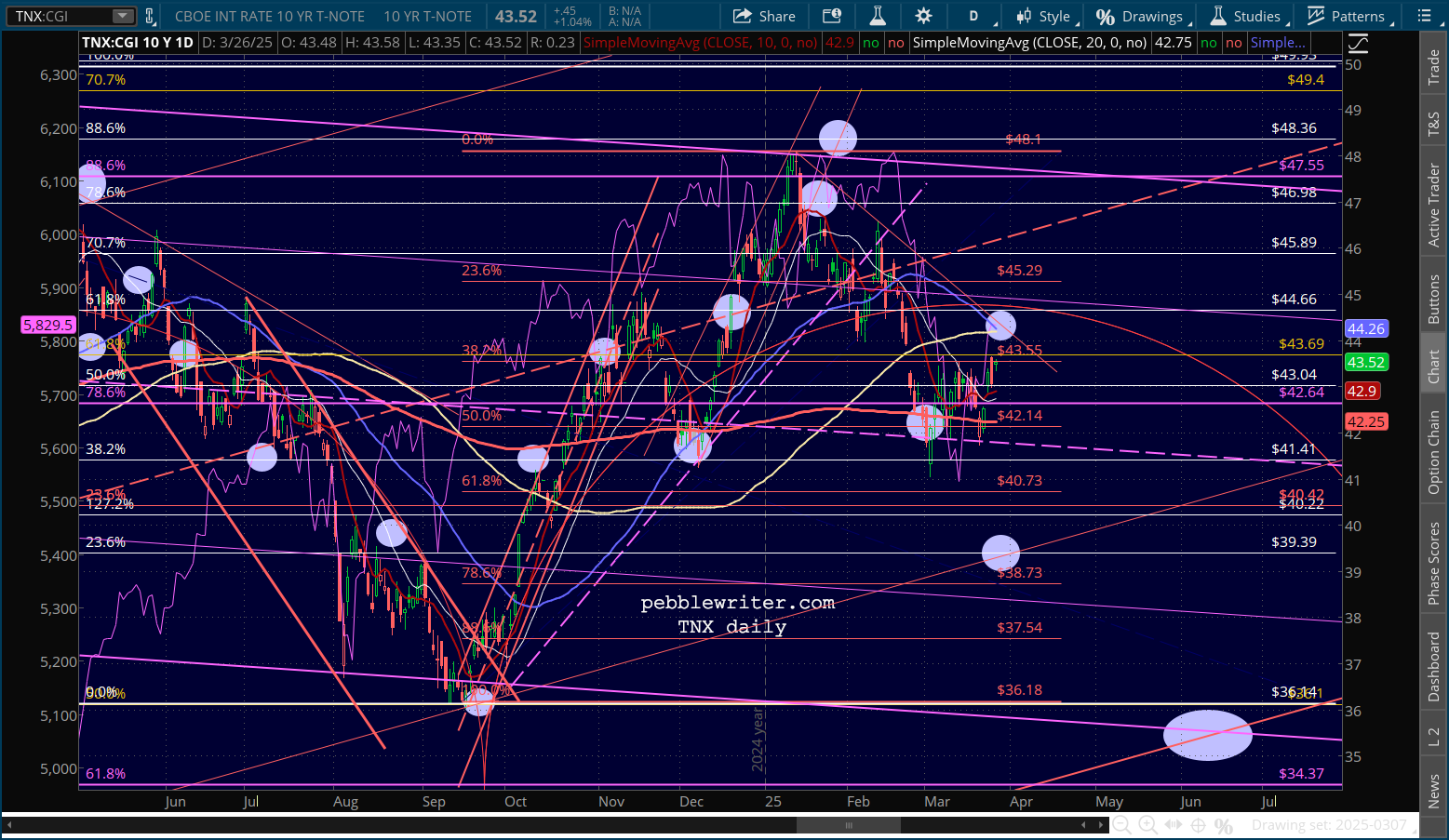

…providing a boost to the 10Y.

…providing a boost to the 10Y.

I don’t know how long the prop job will continue – through Friday’s PCE release or next Wednesday’s tariff announcement? But, it appears that we’re likely in for at least a few more days of the market being buoyed by algos, typically with VIX, every time it shows any weakness.

I don’t know how long the prop job will continue – through Friday’s PCE release or next Wednesday’s tariff announcement? But, it appears that we’re likely in for at least a few more days of the market being buoyed by algos, typically with VIX, every time it shows any weakness.

With government workers being shed by DOGE and inspectors general all being fired, we have to wonder whether the economic data which tells algos whether to buy or sell will be even more dubious than usual.