My working theory for oil price forecasting got a big boost yesterday. Regular readers will recall that we’ve had some very accurate calls over the past 15 months — ever since calling the low on Feb 11 [see: USDJPY Finally Relents.]

My premise back then was that algos had become so focused on the price of oil that it needed to rebound in order to prevent the collapse of stock prices below critical support. It also gave USDJPY, previously the most important driver of algos, a chance to fall back to earth lest Japan develop “inconvenient” inflation.

Since then, however, the focus has shifted to micro-managing inflation numbers. The dollar had dropped almost 9% in only 5 months, and desperately needed support. All the jawboning in the world wasn’t helping. But, when CPI topped 2% and kept going — largely on the back of rising oil prices — the FOMC’s rate hike narrative finally sounded plausible.

WTI rose from 26.05 on Feb 11, 2016 to 55.24 on Jan 3, 2017, allowing CPI and PCE to finally break out. But, all good things come to an end. With PCE finally topping 2% and CPI at 2.7%, it was time to put the brakes on — lest investors begin to worry about stagflation.

And, that’s exactly what happened. In March, the EIA reported gas prices increased 18.364% YoY versus February’s 32.48%. This allowed CPI to drop a little: 2.4% versus 2.7% in February. It was a little hard to swallow, given the actual price increases observed in the real world. But, it was hardly surprising, given that many government economic data is made to order.

And, that’s exactly what happened. In March, the EIA reported gas prices increased 18.364% YoY versus February’s 32.48%. This allowed CPI to drop a little: 2.4% versus 2.7% in February. It was a little hard to swallow, given the actual price increases observed in the real world. But, it was hardly surprising, given that many government economic data is made to order.

For any Kool-Aid loving believers in the veracity of government statistics, just know that the April YoY increase in gas prices came in at the same level. The exact same level: 18.364%. In other words, inflation is being very carefully managed via the very careful management of gas prices — or at least the reporting of same. This gives the Fed plenty of room to put the brakes on any further rate increases for the time being — should they so choose. And, it means that WTI’s drop through important support, yesterday, could be quite meaningful.

In other words, inflation is being very carefully managed via the very careful management of gas prices — or at least the reporting of same. This gives the Fed plenty of room to put the brakes on any further rate increases for the time being — should they so choose. And, it means that WTI’s drop through important support, yesterday, could be quite meaningful.

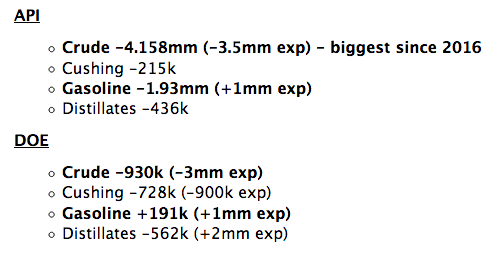

I’ll be watching RBOB like a hawk with today’s EIA inventory report. It finally tagged our 1.5259 target from Mar 3 [see: What is the Fed Trying to Tell Us?] And, like WTI, it is slipping below important support. We remain short from yesterday with our downside targets intact.

We remain short from yesterday with our downside targets intact.

continued for members…

A quick roundup of today’s charts:

CL has dropped through the white channel bottom. As we noted yesterday, 48.20 was important support, meaning we’ll get another leg down here.

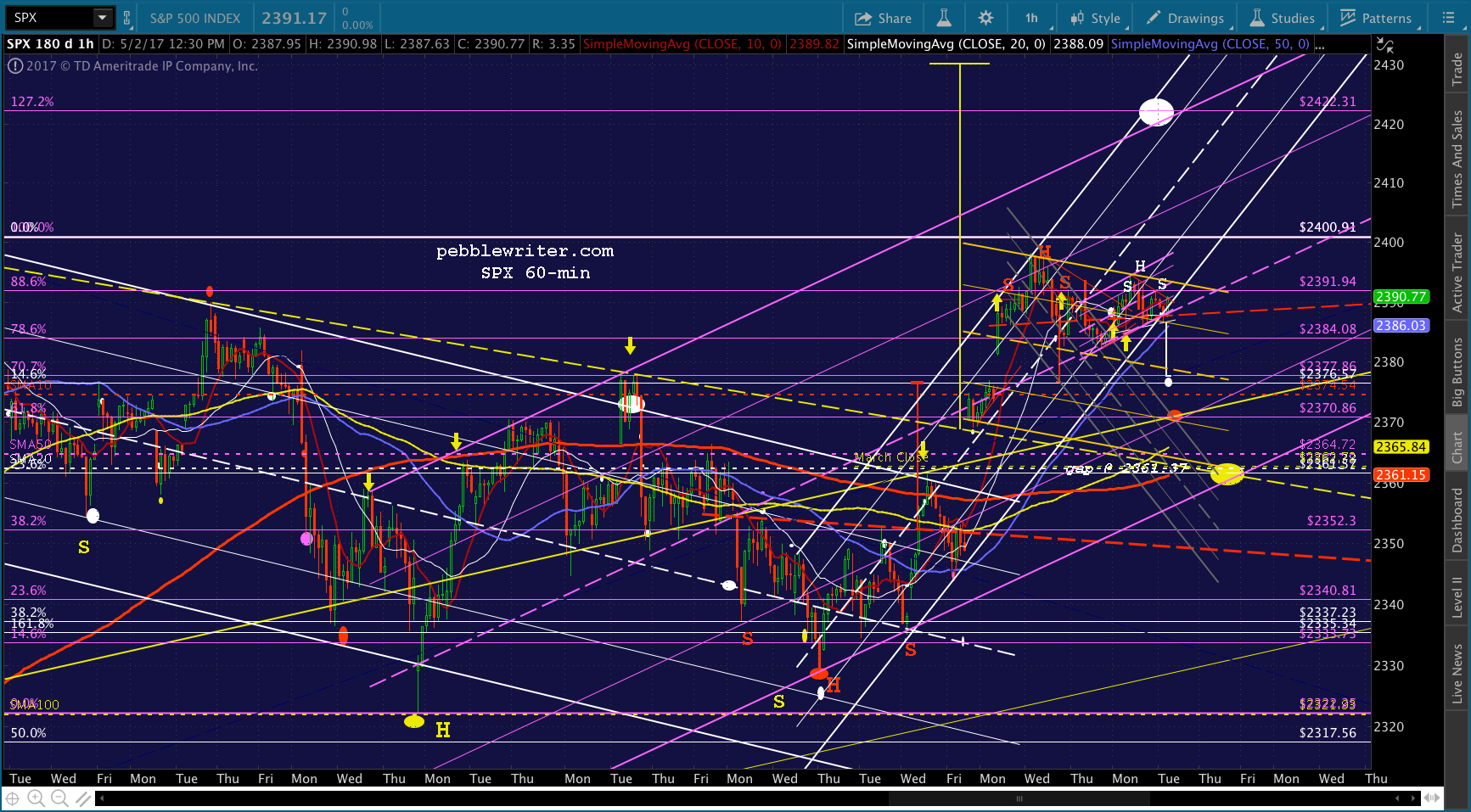

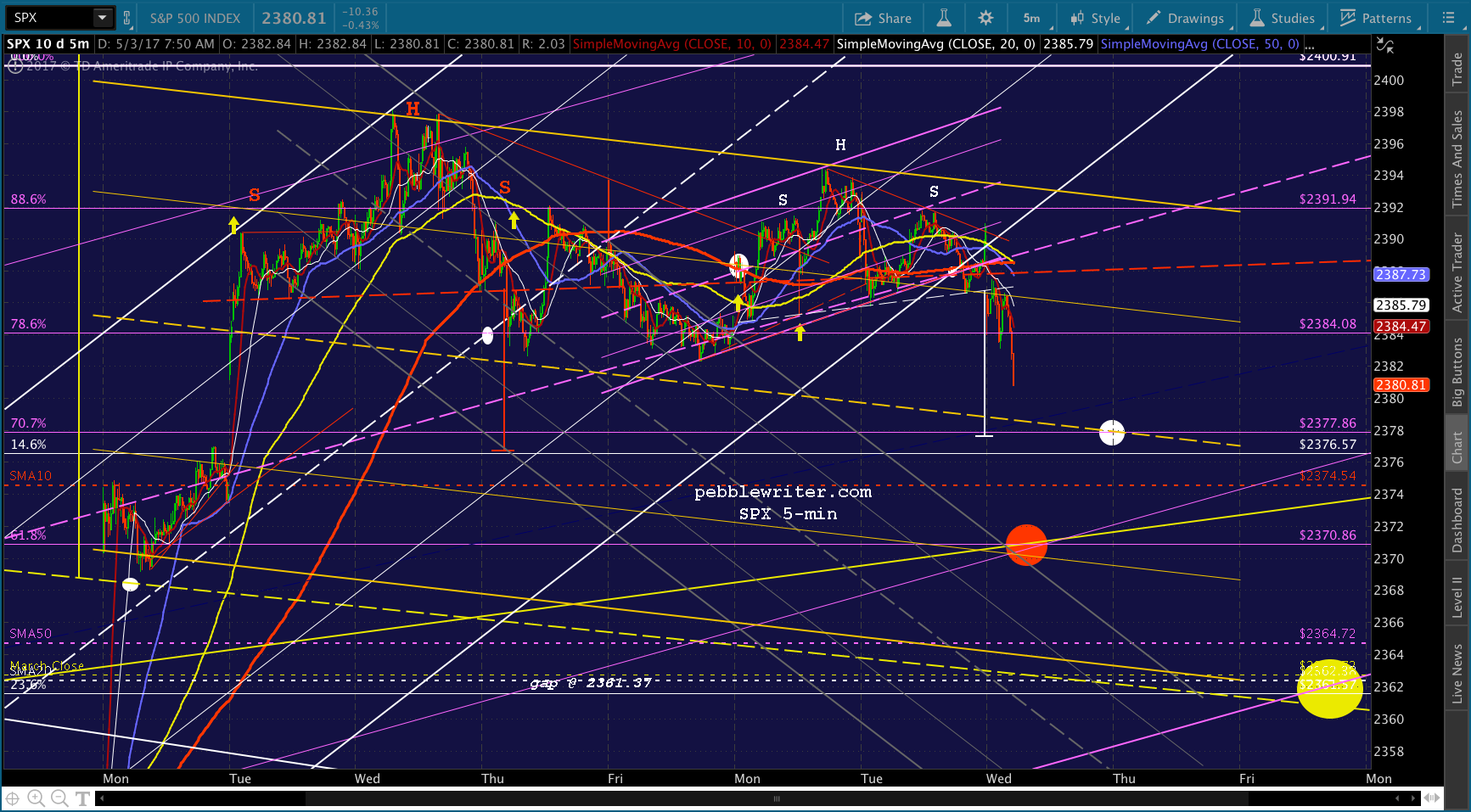

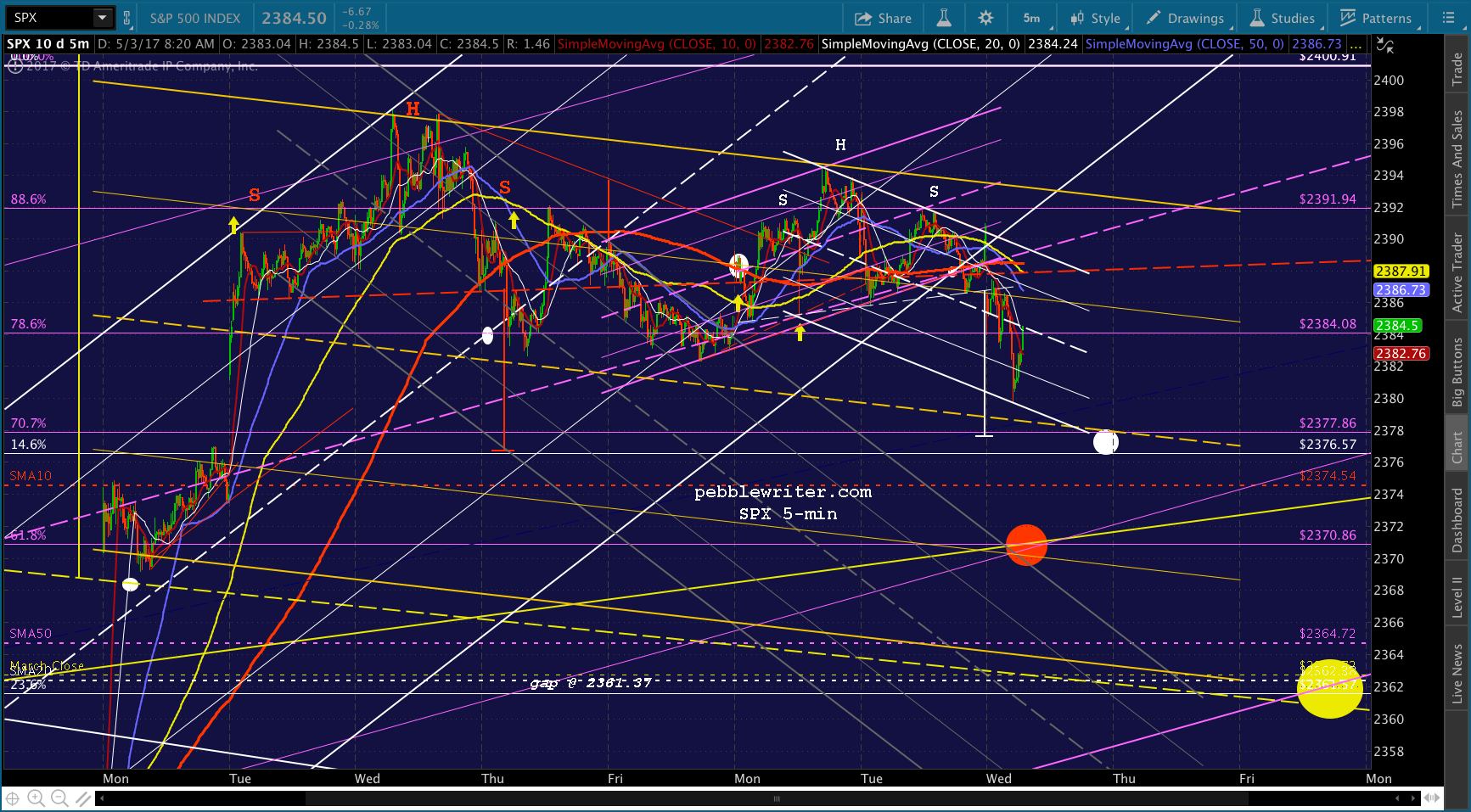

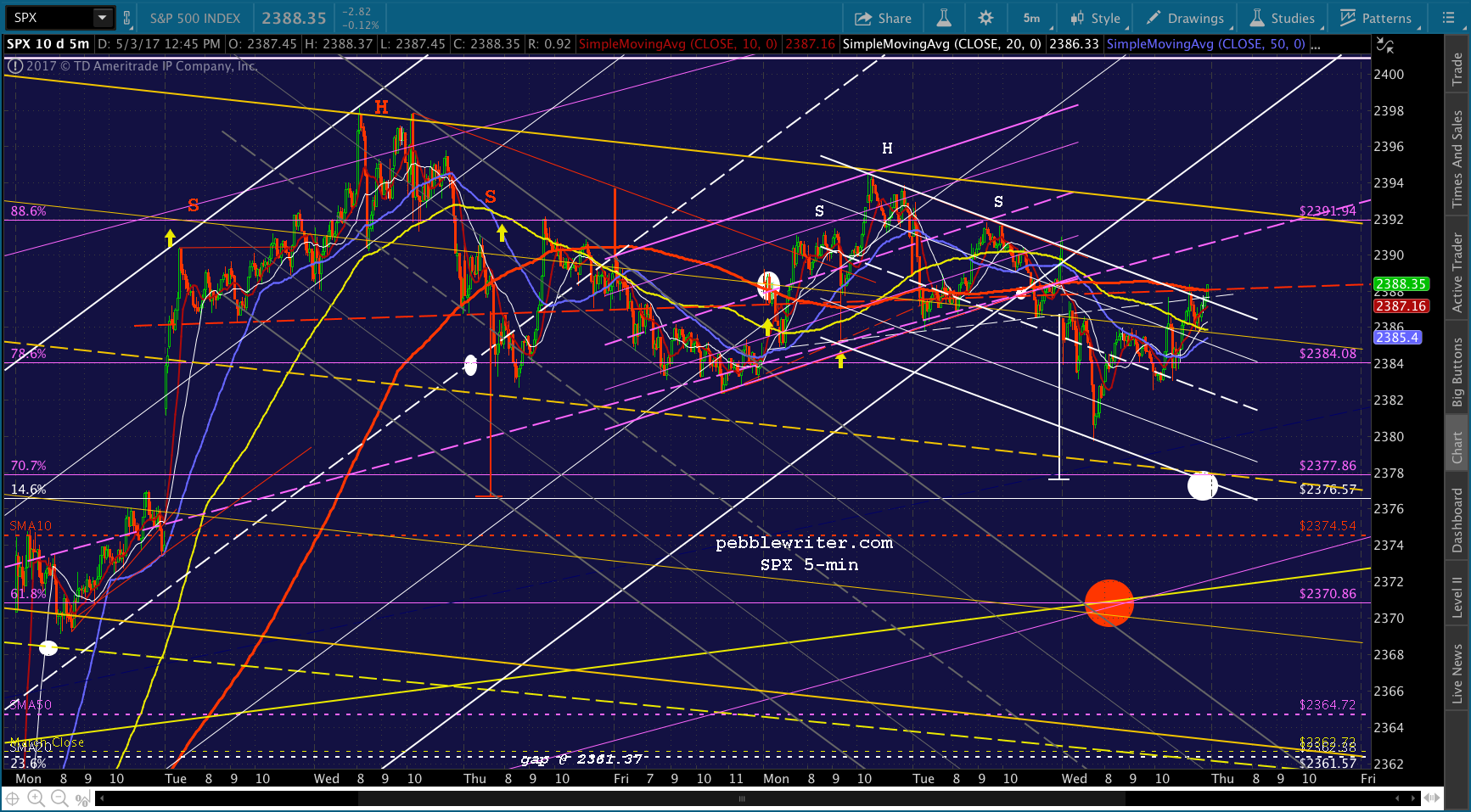

ES completed another little H&S Pattern, this one pointing to 2373.38.

ES completed another little H&S Pattern, this one pointing to 2373.38. A short time ago, USDJPY ran down to tag the SMA5 200 — even though it meant a temporary break down in the red channel that’s been guiding prices higher since the white channel “broke down.”

A short time ago, USDJPY ran down to tag the SMA5 200 — even though it meant a temporary break down in the red channel that’s been guiding prices higher since the white channel “broke down.”

And, SPX still has plenty of choices for downside.

And, SPX still has plenty of choices for downside.

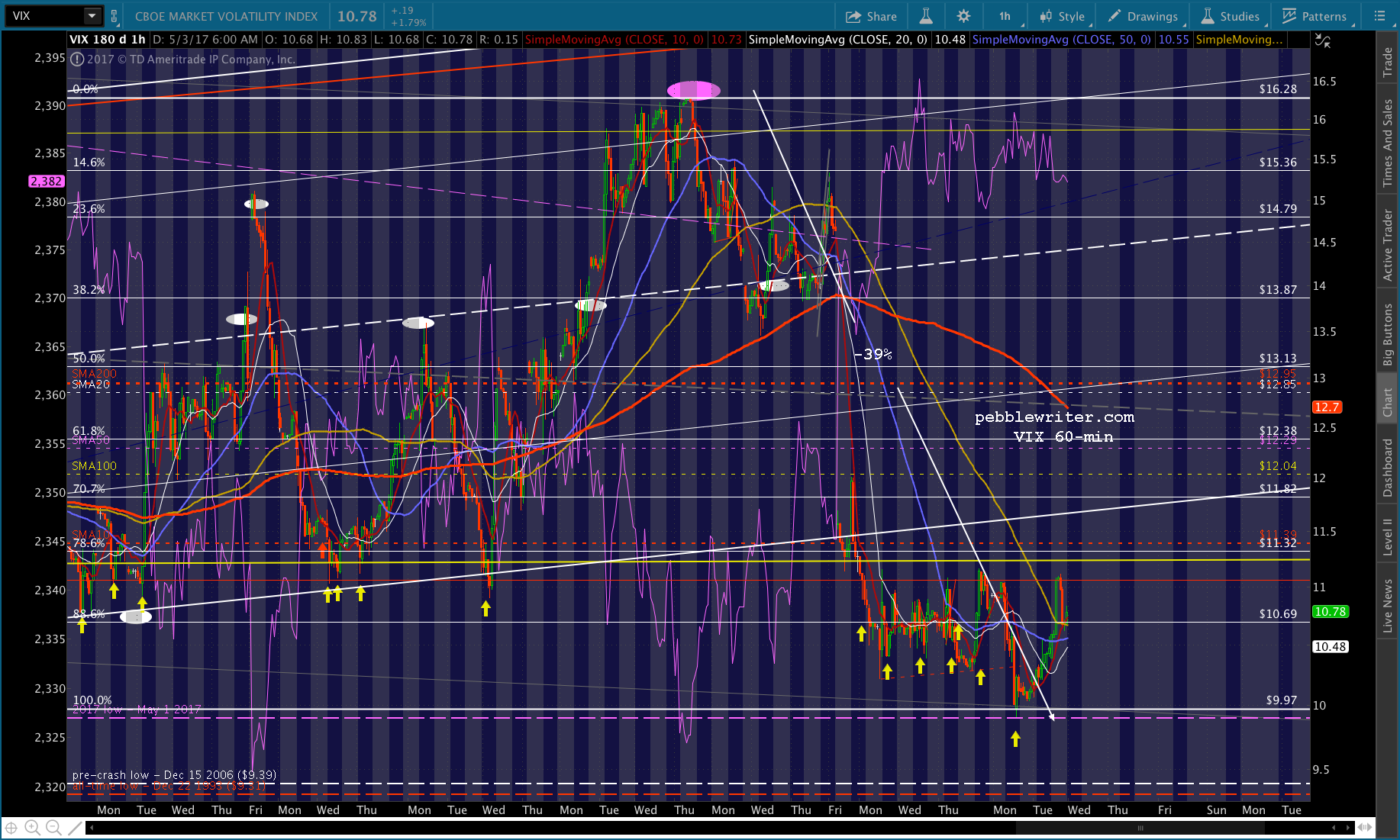

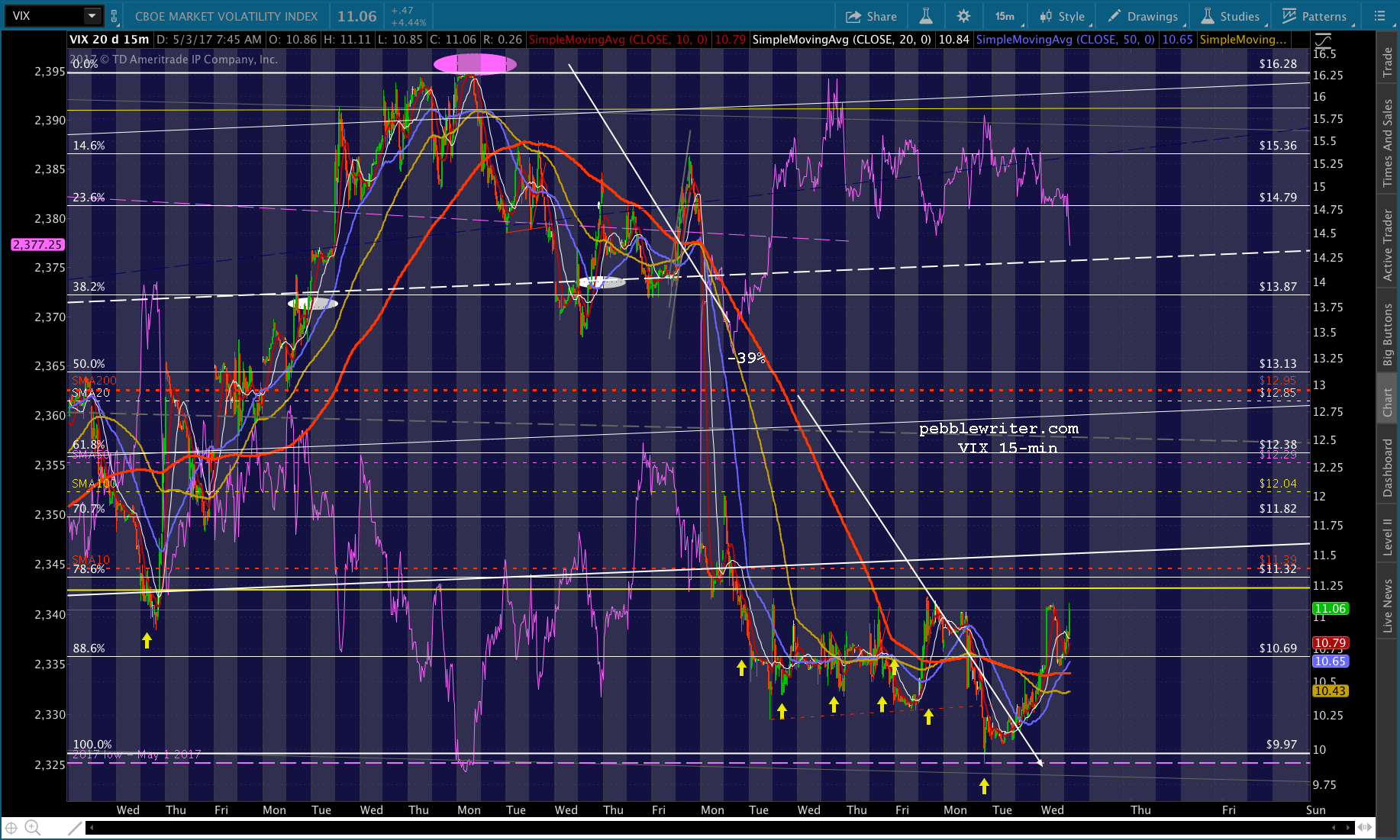

Today’s key will be whether USDJPY and VIX can compensate for CL and RBOB.

Today’s key will be whether USDJPY and VIX can compensate for CL and RBOB.

BTW, I updated the DXY chart to show why I placed the targets where I did. Hopefully, this will answer a few questions.

BTW, I updated the DXY chart to show why I placed the targets where I did. Hopefully, this will answer a few questions.

UPDATE: 10:10 AM

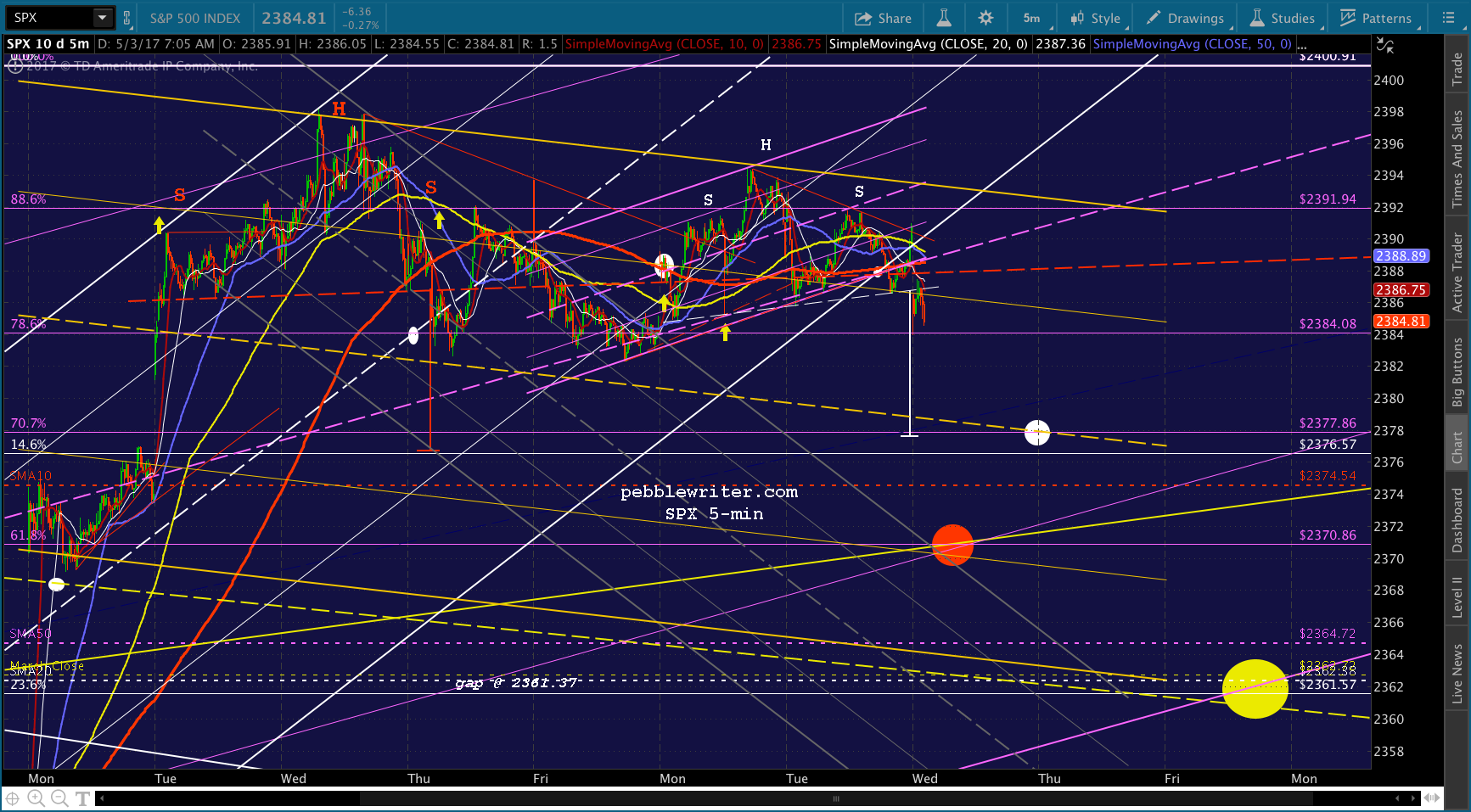

A nice little backtest, and SPX is testing the .786 again. Assuming it drops through, the next support is the .707 at 2377.86 (white dot), followed by the SMA10 at 2374.54 and the red dot at 2370.86 — which has been my preferred target for quite some time. Just a reminder: EIA release inventory data at 10:30. If it confirms yesterday’s API data, CL, RB and SPX could get a nice bump. So, watch your stops. I’d continue to let the SMA5 200, now at 2388.48, be your guide. And, I’d look to cover at 2377.86 if there’s an opportunity, but only after seeing a reversal. Otherwise, 2370.86 is in play.

Just a reminder: EIA release inventory data at 10:30. If it confirms yesterday’s API data, CL, RB and SPX could get a nice bump. So, watch your stops. I’d continue to let the SMA5 200, now at 2388.48, be your guide. And, I’d look to cover at 2377.86 if there’s an opportunity, but only after seeing a reversal. Otherwise, 2370.86 is in play.

Unfortunately, I have to jump on a conference call right at 10:30, so I won’t have a chance to post until after the fact.

UPDATE: 10:53 AM

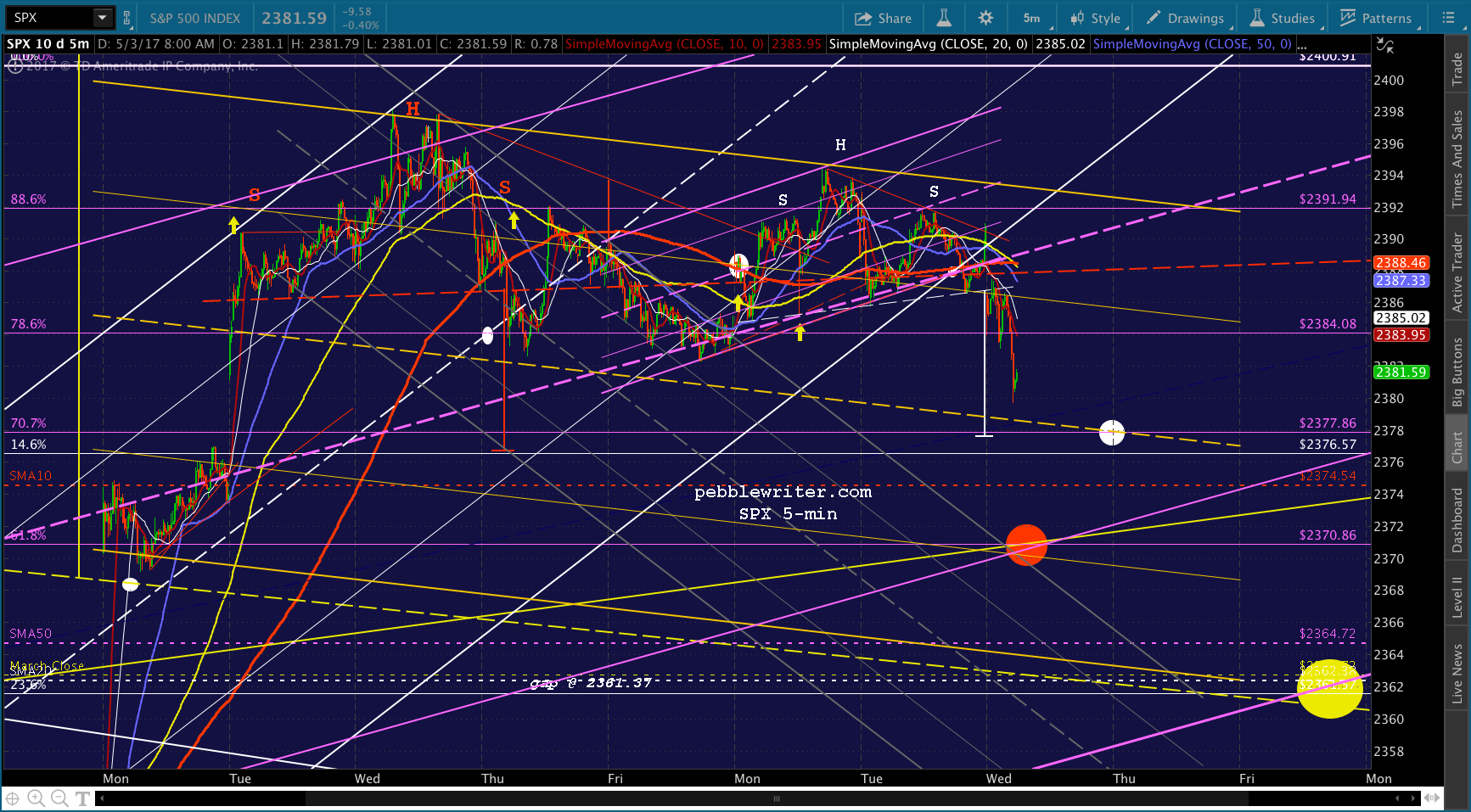

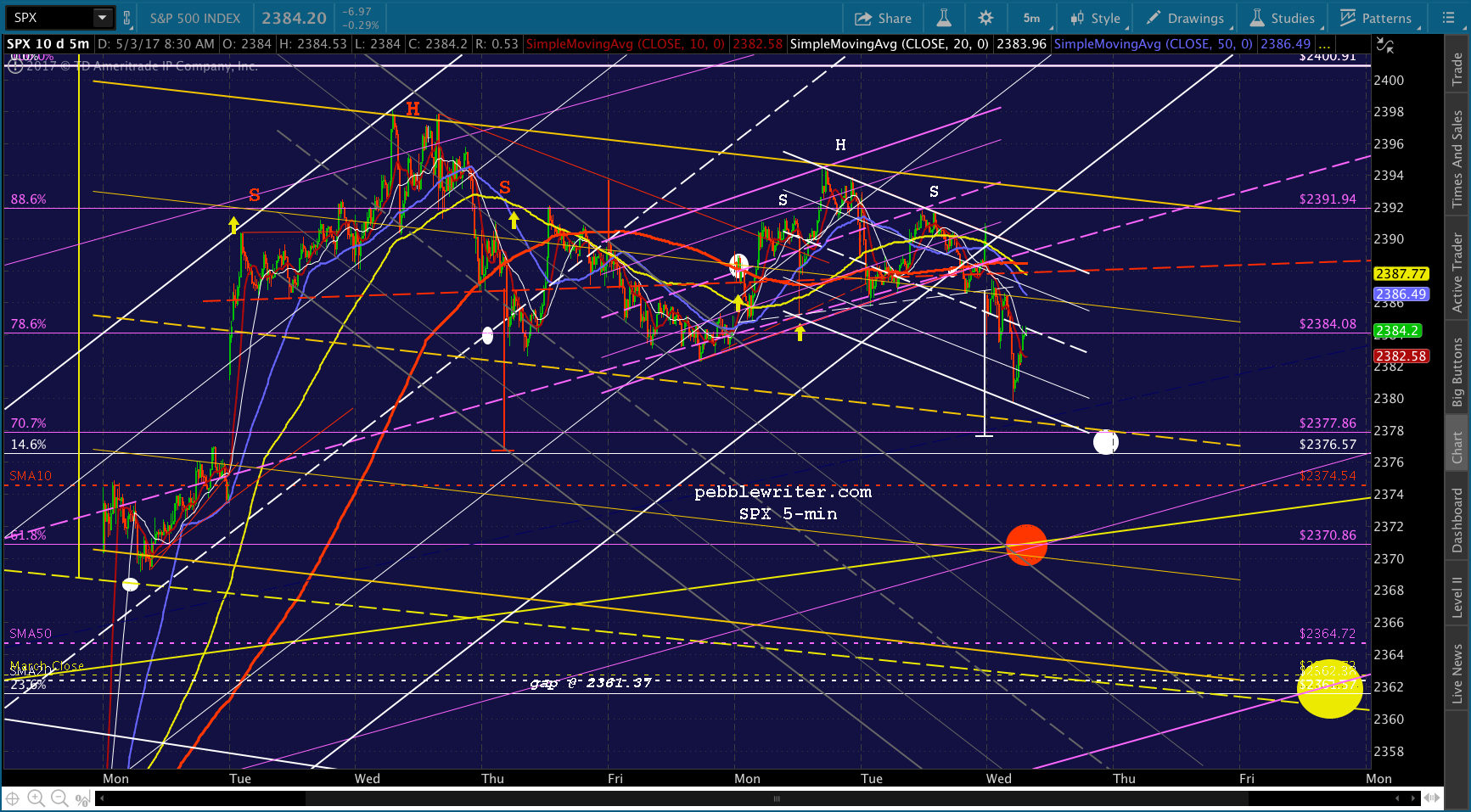

The EIA report was disappointing relative to the API. CL and RB are tumbling, VIX is on the rise, and SPX is nearing our 2377.86 target. Note that although I put the white target on the .707 at 2377.86, there is a gap to be filled at 2376.98. So, don’t be surprised if it overshoots a bit. And, though I hardly need to say it, don’t be surprised if we get a big bounce that delays the eventual tag to the end of the session or even tomorrow morning — when the yellow channel midline passes through the .707.

UPDATE: 11:02 AM

UPDATE: 11:02 AM

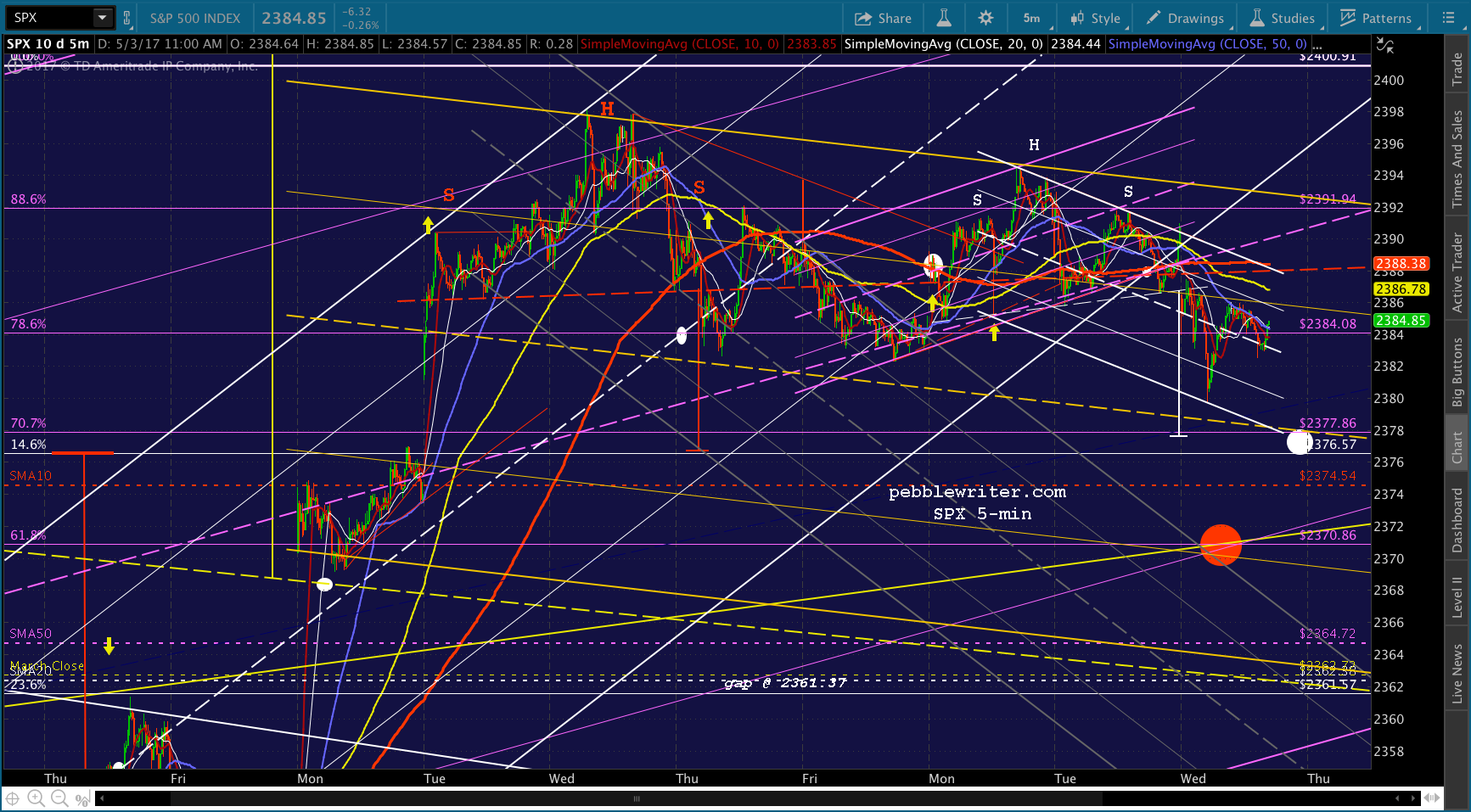

We’re likely to get a nice bounce here at 2380, as ES has tagged its SMA10. A logical target for SPX would be the .786 at 2384 as the SMA5 20 arrives on the scene. So — not necessarily big enough to be worth playing. But, it’s not exactly unusual these days for bounces to get carried away.

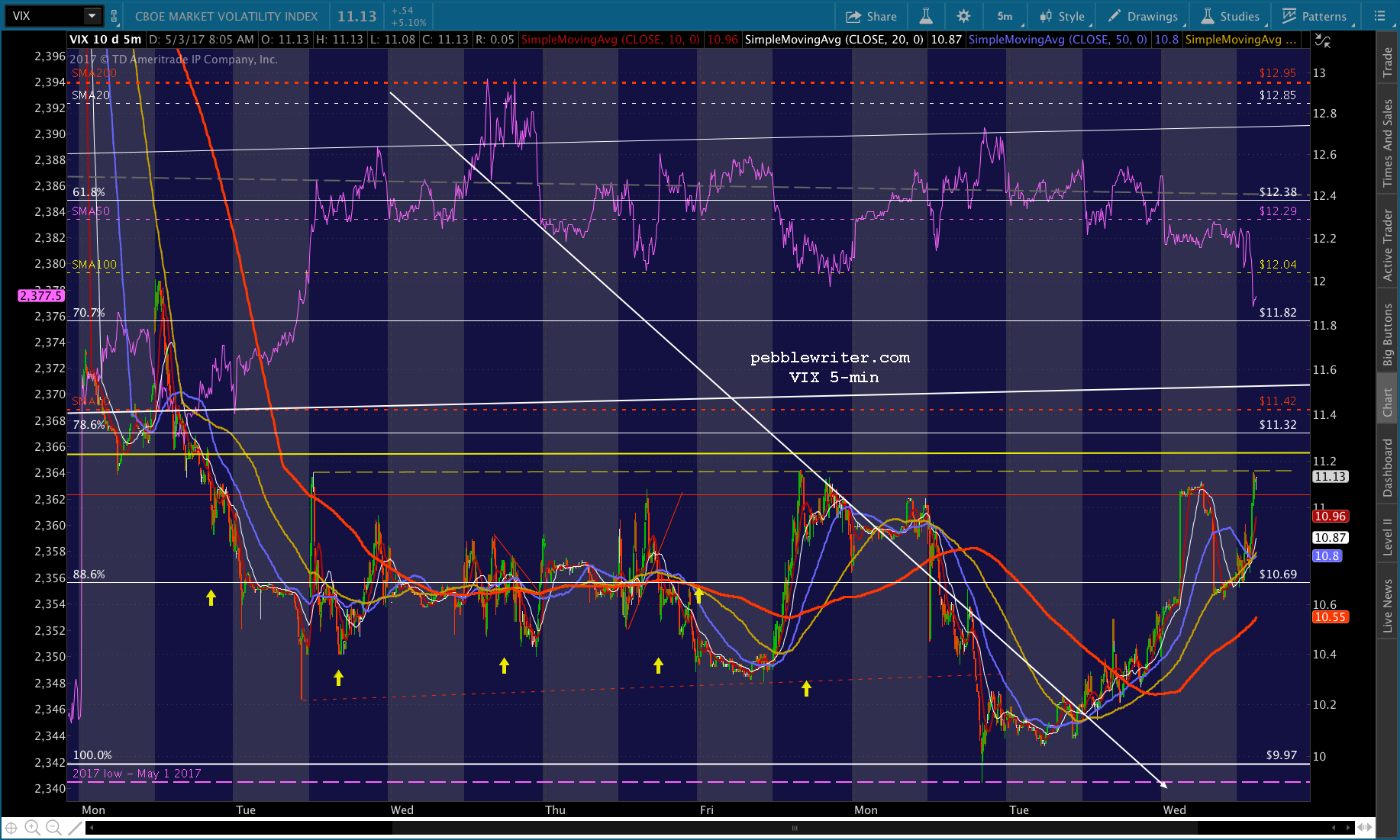

Note that VIX has reached horizontal resistance, with additional resistance just overhead (11.24 – 11.42) at the yellow channel bottom, the .786 and its SMA10.

Note that VIX has reached horizontal resistance, with additional resistance just overhead (11.24 – 11.42) at the yellow channel bottom, the .786 and its SMA10. UPDATE: 11:23 AM

UPDATE: 11:23 AM

Here’s the white midline and SMA5 20. For anyone playing the bounce, this is probably a good spot to revert to short with stops up around the neckline at 2387. UPDATE: 11:32 AM

UPDATE: 11:32 AM

Euro close. USDJPY is falling, but VIX got knocked back by the horizontal resistance — so, that’s a risk to bears unless it punches through.

UPDATE: 2:02 PM

UPDATE: 2:02 PM

USDJPY is fluctuating, and VIX immediately plunged (big surprise.) Looking for SPX to rally at least a little — SMA5 100 and SMA5 200 are the logical targets.

UPDATE: 2:09 PM

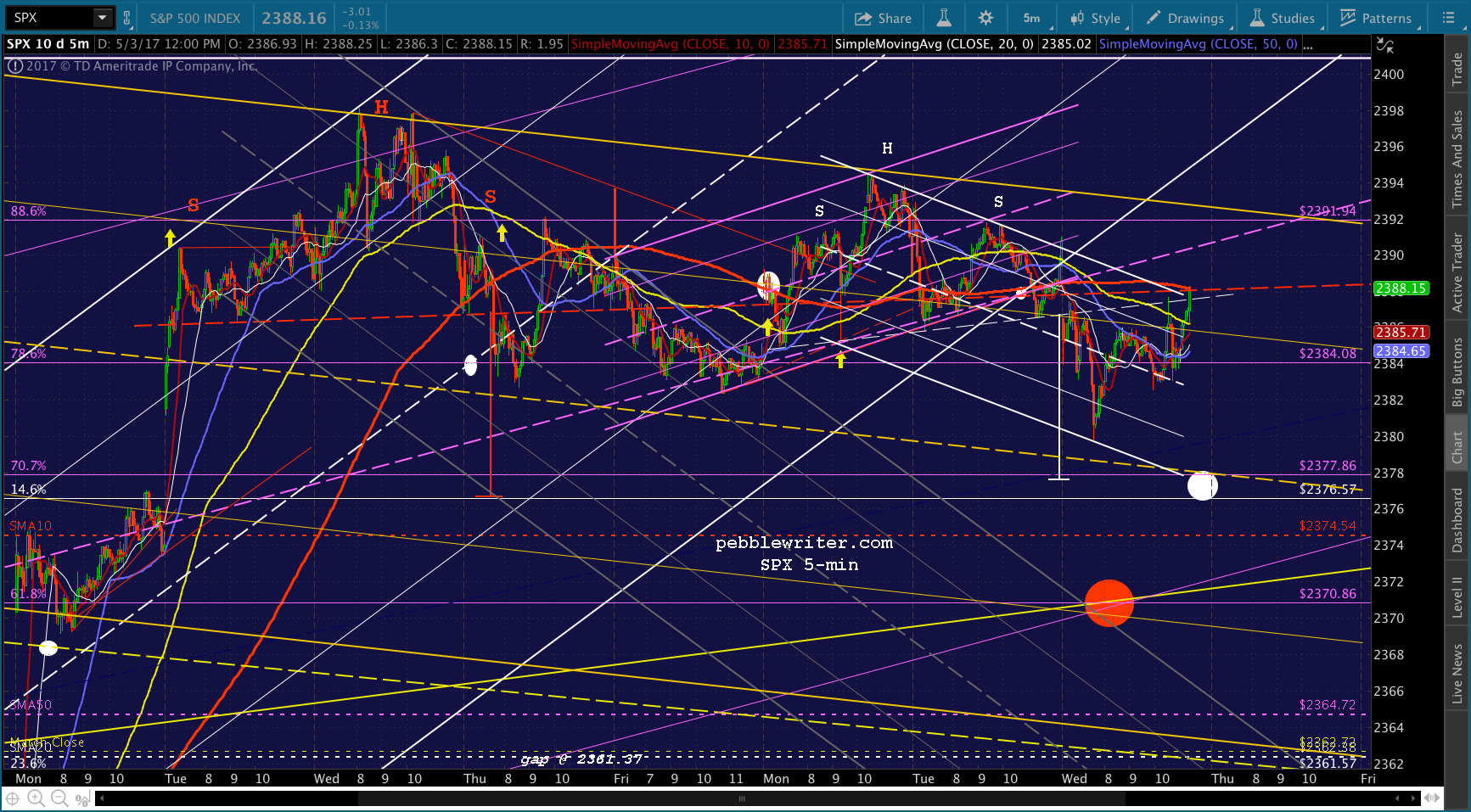

Backtesting the white neckline. Would want to be short anywhere south of here. It appears very likely that the SMA5 200 will reach the neckline by the end of the session. That would make a very attractive bounce target, and leave bears with a tough decision regarding holding short overnight. As always, only do so if you can hedge or handle the gap risk.

UPDATE: 3:05 PM

UPDATE: 3:05 PM

Here’s the SMA5 200 and falling white channel top. Any push through this resistance means it’s time to go to cash. Watch VIX, which just dropped through its SMA5 200, and CL, which is holding on to a slight TL breakout.

UPDATE: 3:50 PM

UPDATE: 3:50 PM

Here we go again — the same crap as yesterday. No telling whether or not they’ll be able to hold the breakout overnight. So, as always, only hold short if you can hedge or deal with the gap risk. Otherwise, cash for the night.

FWIW, CL is breaking down…

FWIW, CL is breaking down… …and, USDJPY looks like it’s run out of room.

…and, USDJPY looks like it’s run out of room.  Bottom line, I believe as long as SPX remains below the purple channel midline, it has good downside potential.

Bottom line, I believe as long as SPX remains below the purple channel midline, it has good downside potential.