The Fed’s Evans, Lacker, Powell, Fischer and Yellen are all appearing in public today, and will no doubt be pressed for confirmation regarding the recent hawkish comments by Dudley, Brainard and Kaplan. I can’t remember a time when there was so much unanimity regarding a rate hike.

SPX was off a whopping 14 points yesterday which, given its recent melt up, felt like much more. Somewhere, some investors are clearly wondering about rising rates. After 8 long years of the most accommodative monetary policy in history, can the Fed and the bulls sell investors on the idea that higher rates are a good thing?

continued for members…

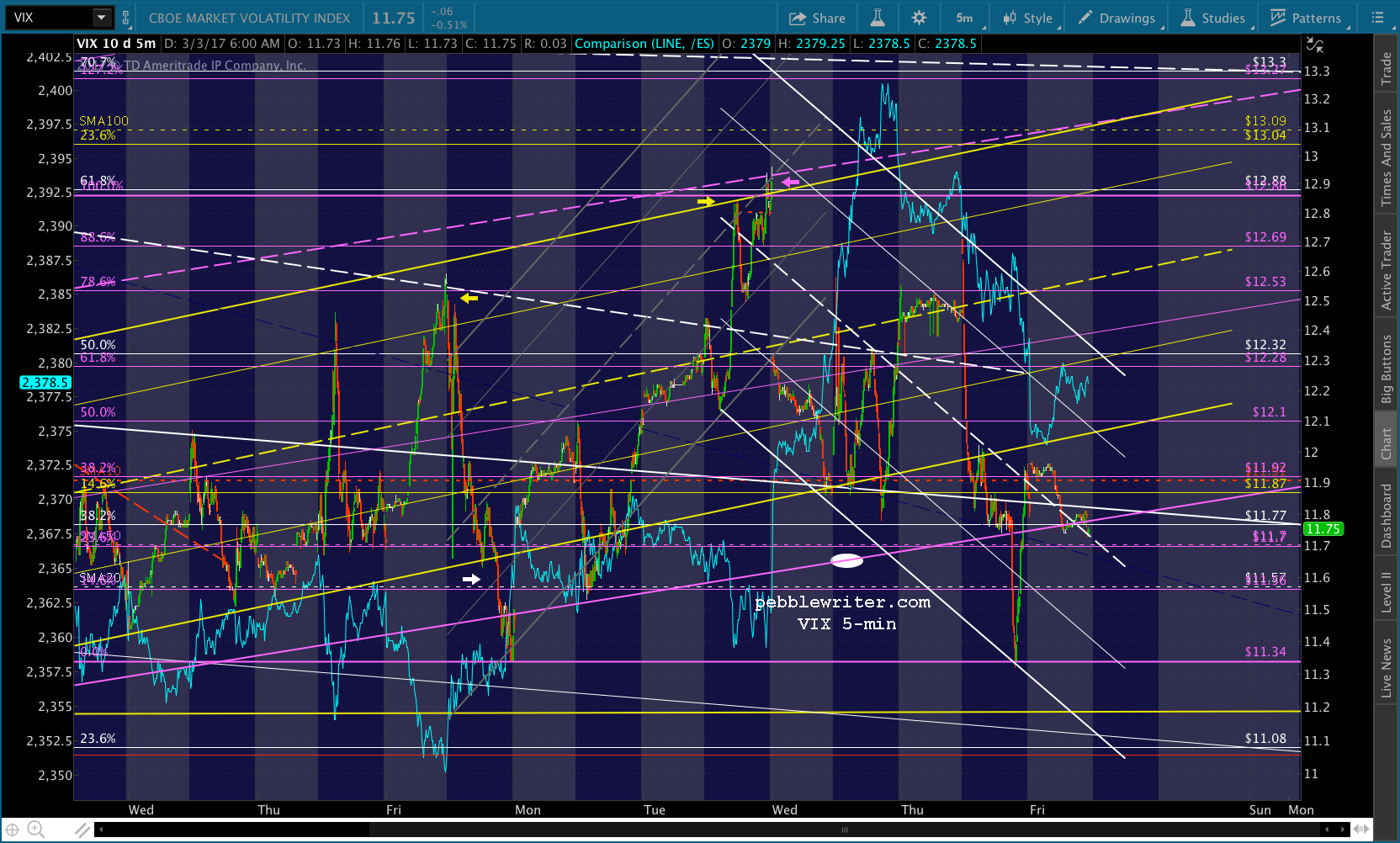

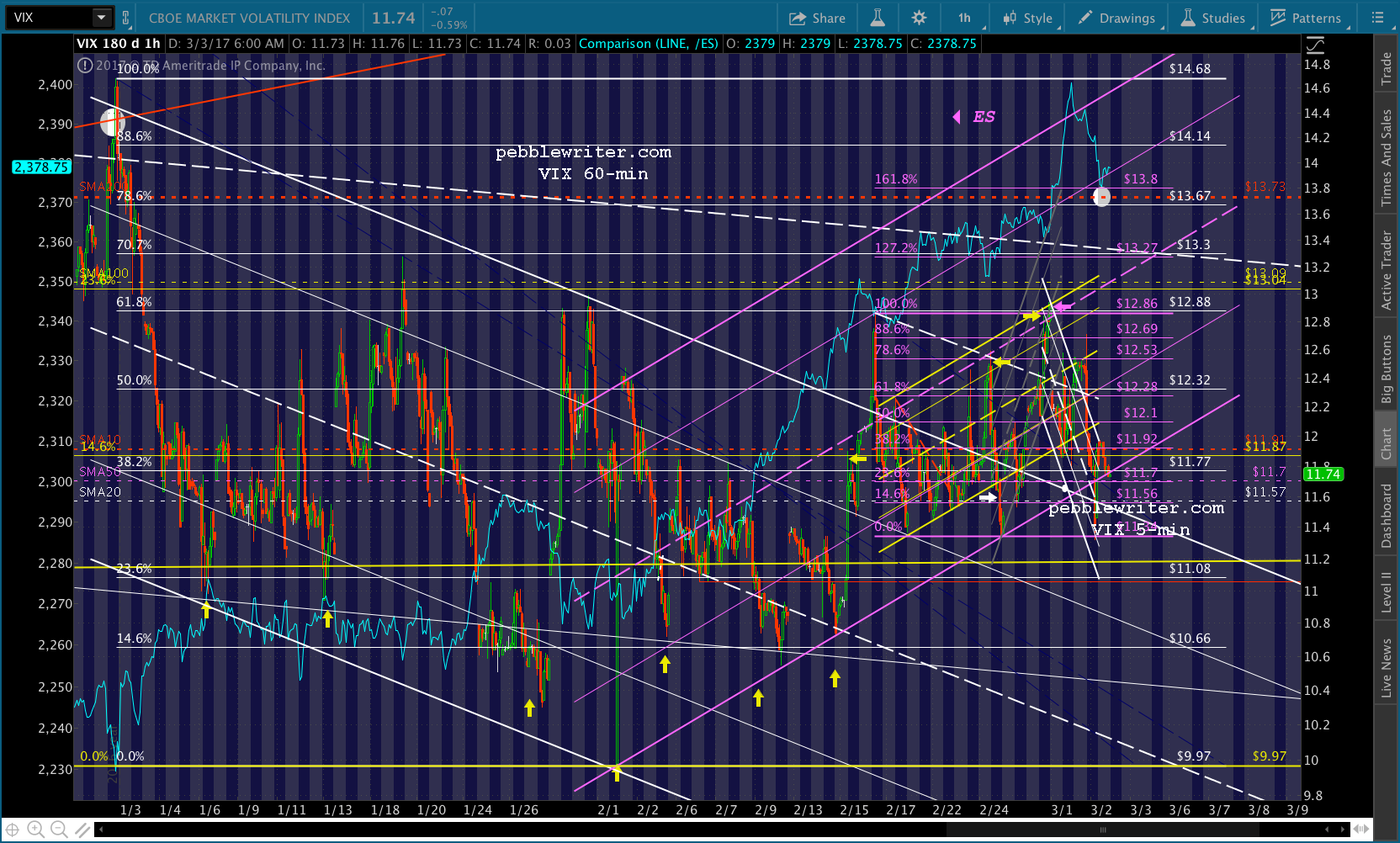

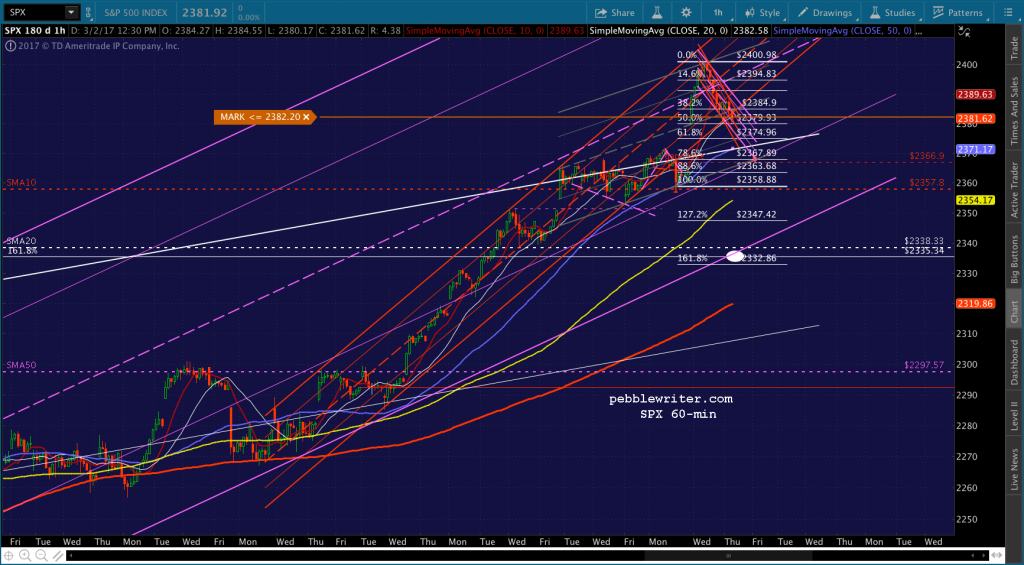

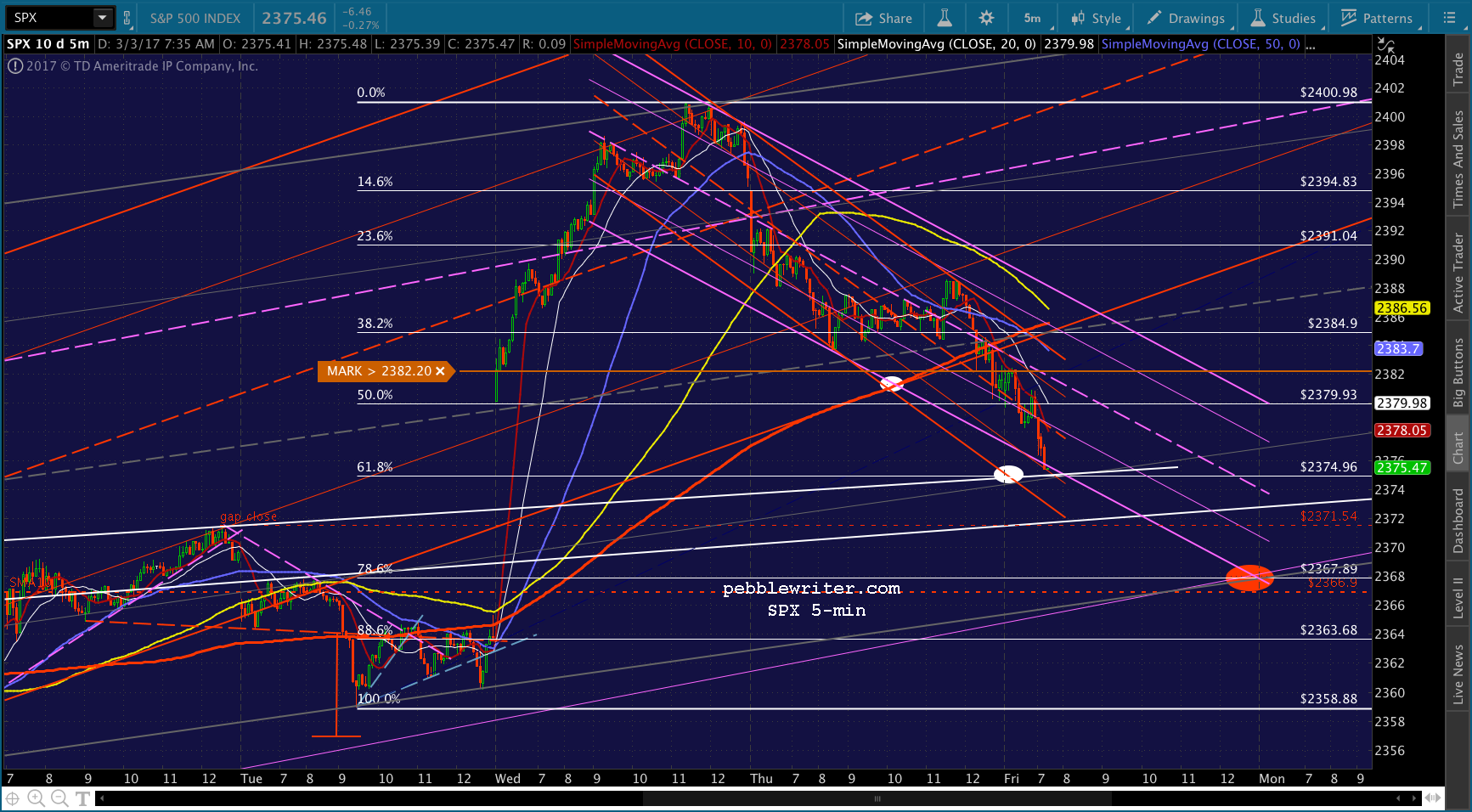

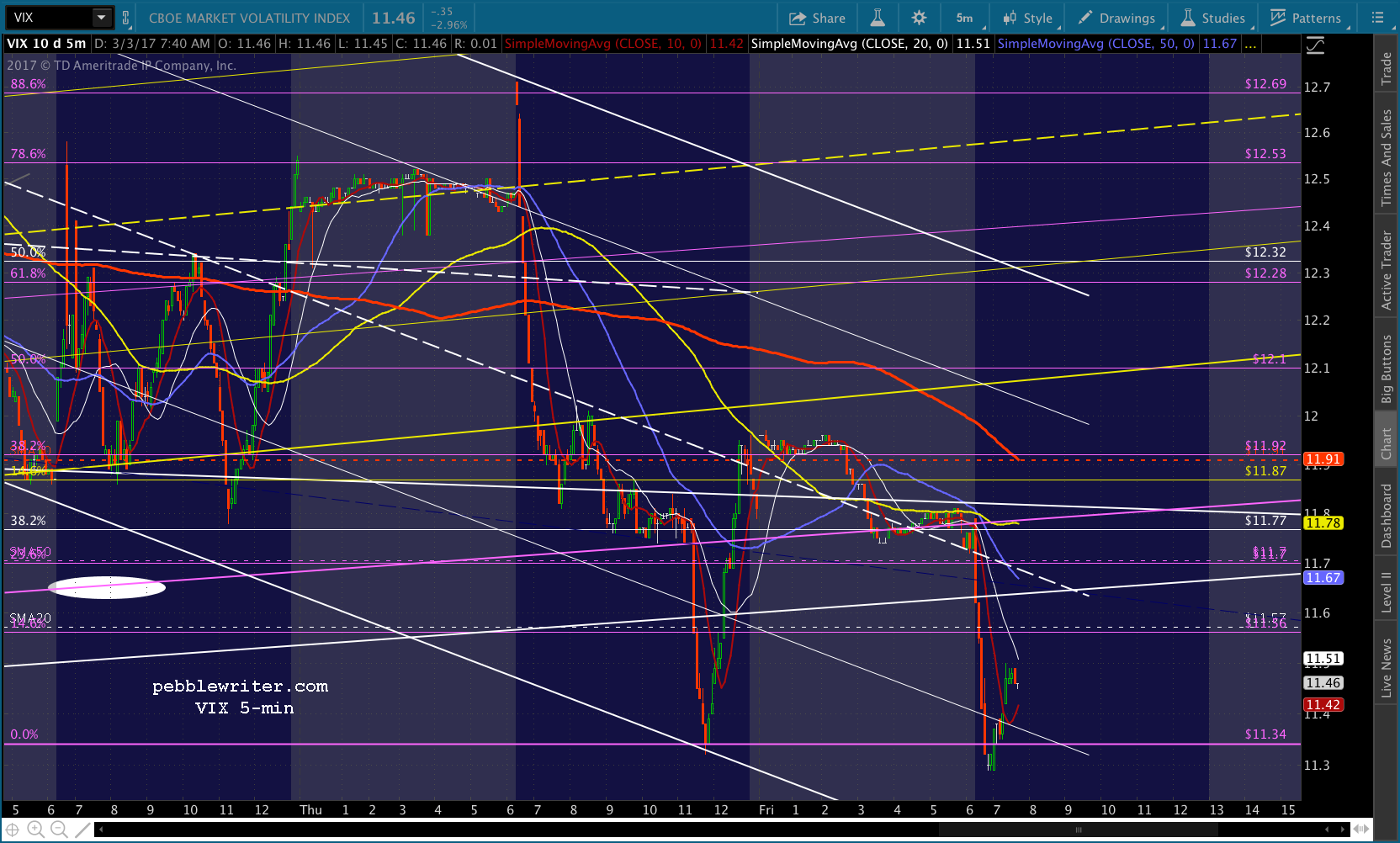

A quick look around the horn shows futures off 3-4 points… …with VIX sitting right at channel support, ready to help — or, not…

…with VIX sitting right at channel support, ready to help — or, not…

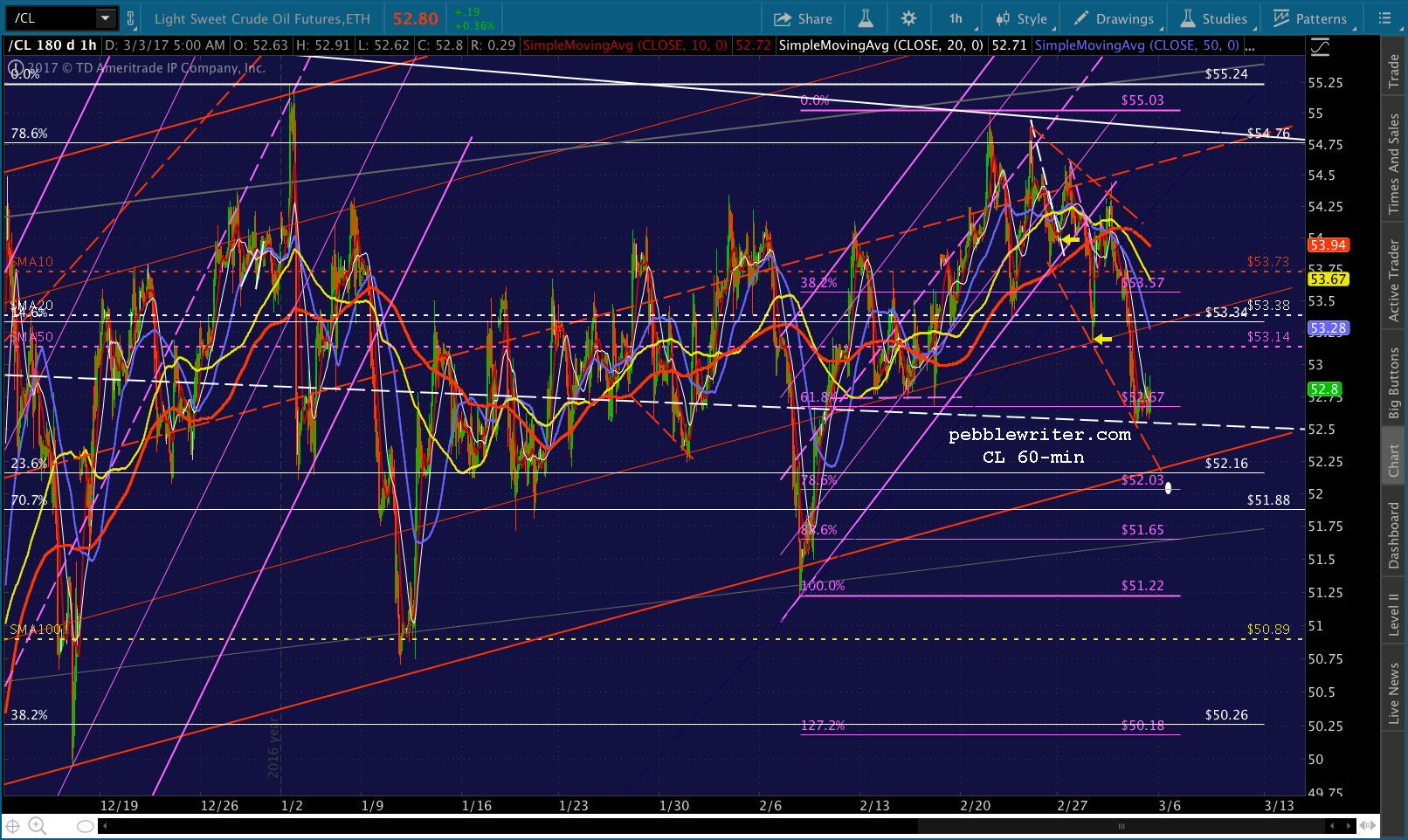

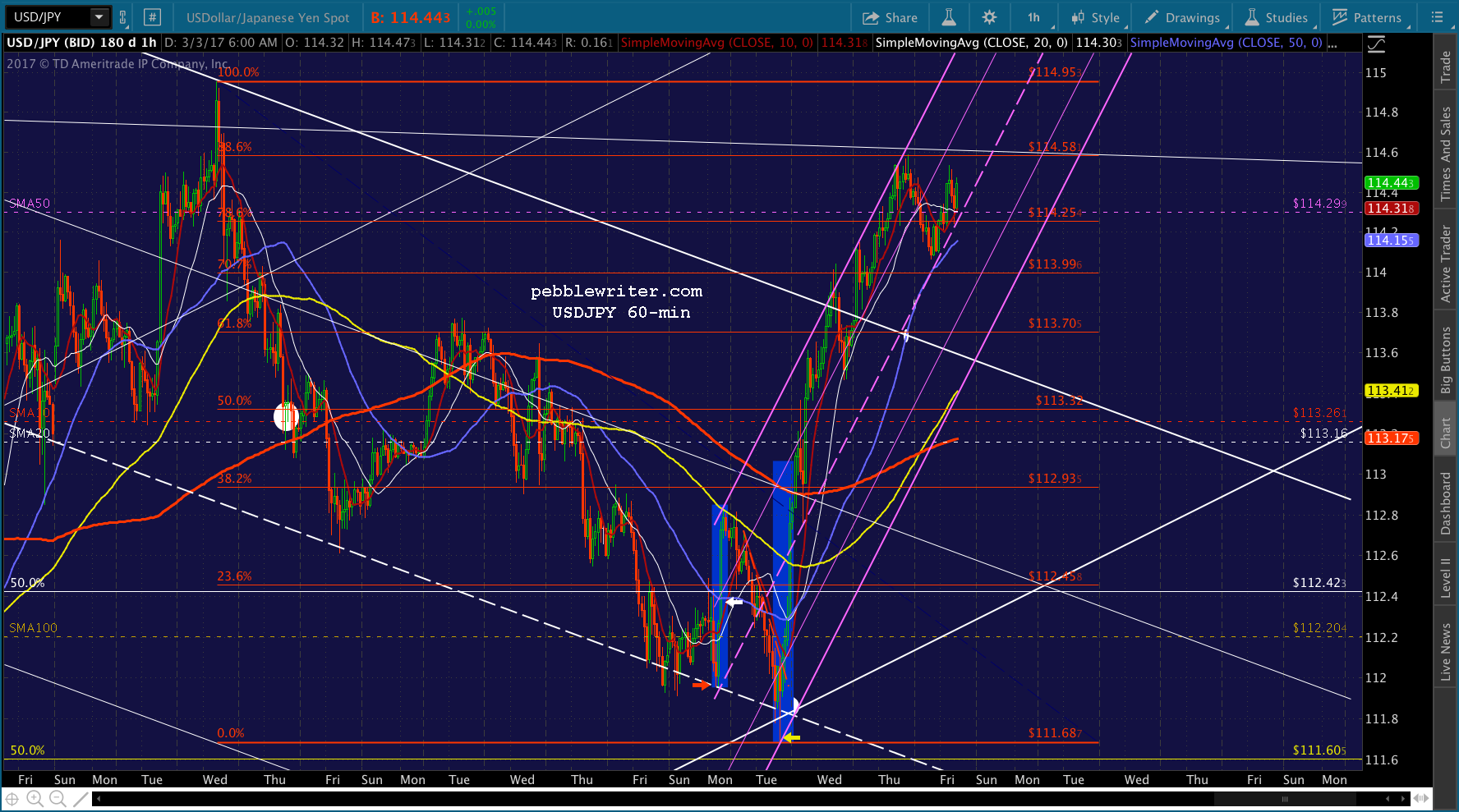

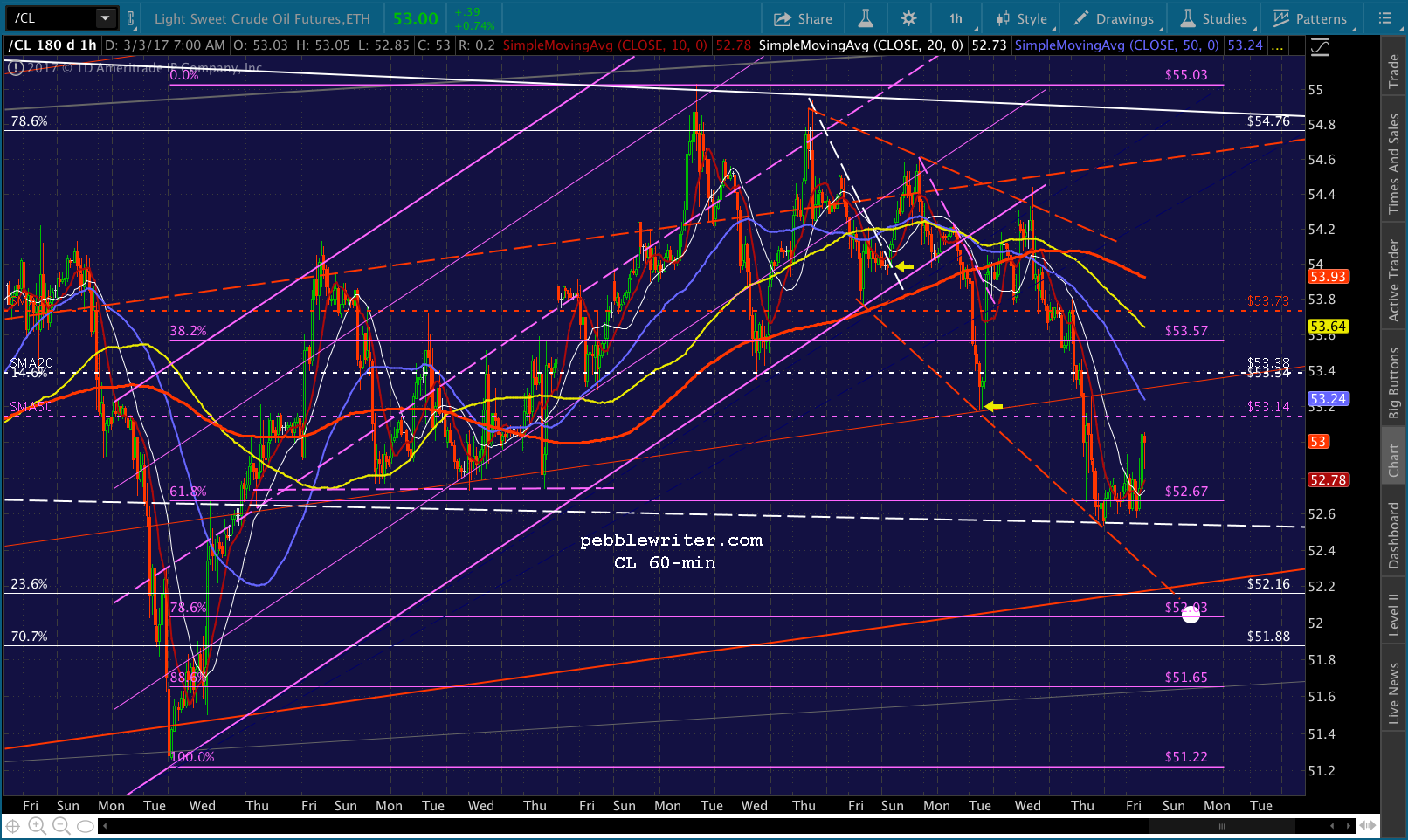

…and USDJPY and CL falling enough overnight to support the decline, but not enough to cause a panic.

…and USDJPY and CL falling enough overnight to support the decline, but not enough to cause a panic.  Note, however, that RBOB is slipping below the white channel bottom and seems intent on fleshing out the red channel, likely at the red .786 at 1.5259.

Note, however, that RBOB is slipping below the white channel bottom and seems intent on fleshing out the red channel, likely at the red .786 at 1.5259.

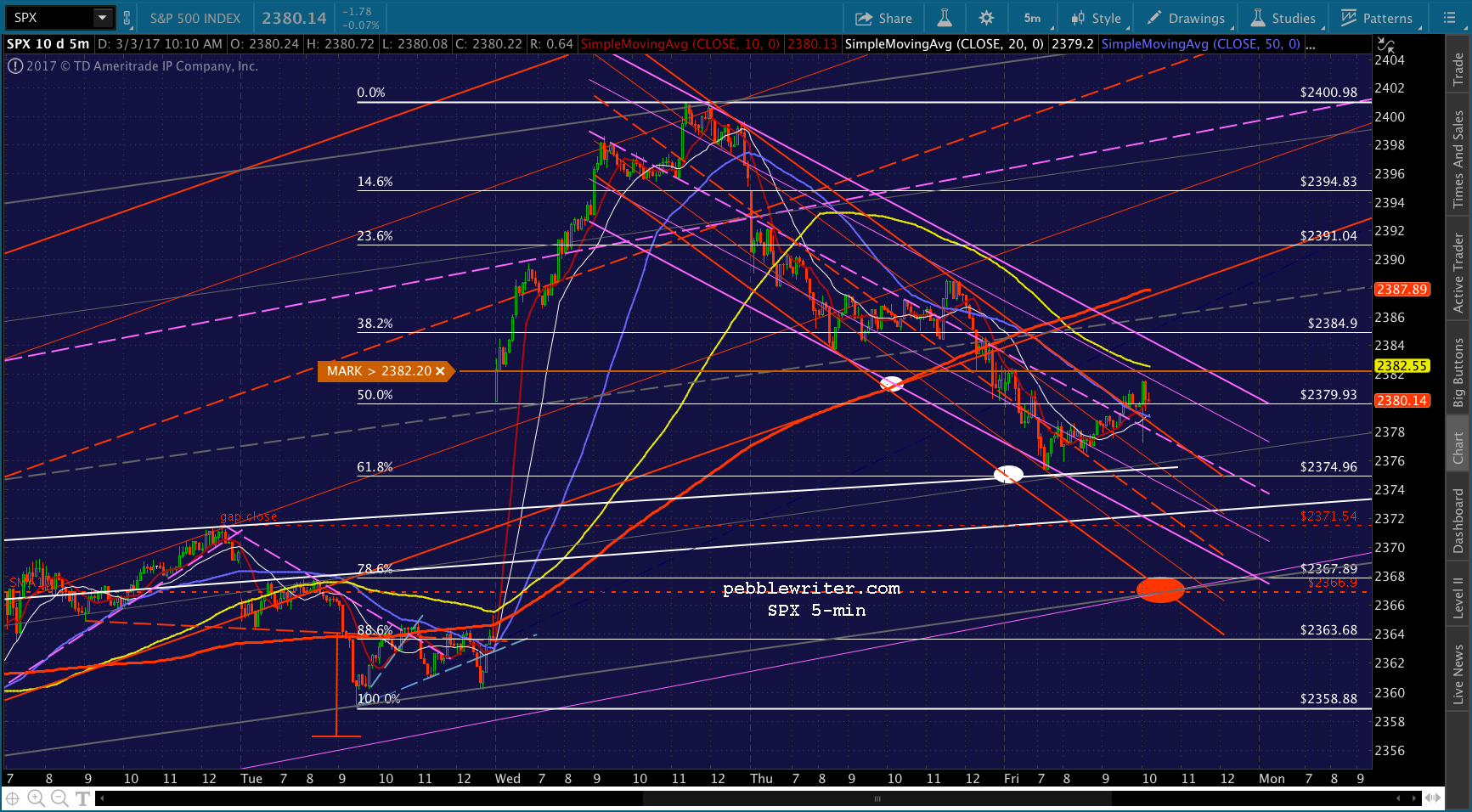

USDJPY at least thought about backtesting the white channel, but chose the rising purple midline instead. It could still happen either today or over the weekend.  It would seem that a decline to 2374.96 is safe, but below that will require some additional help (or, at least, VIX and CL staying out of it.)

It would seem that a decline to 2374.96 is safe, but below that will require some additional help (or, at least, VIX and CL staying out of it.)

* * *

Quick FYI — I have to take off early today. My last post will be around 1pm this afternoon.

* * *

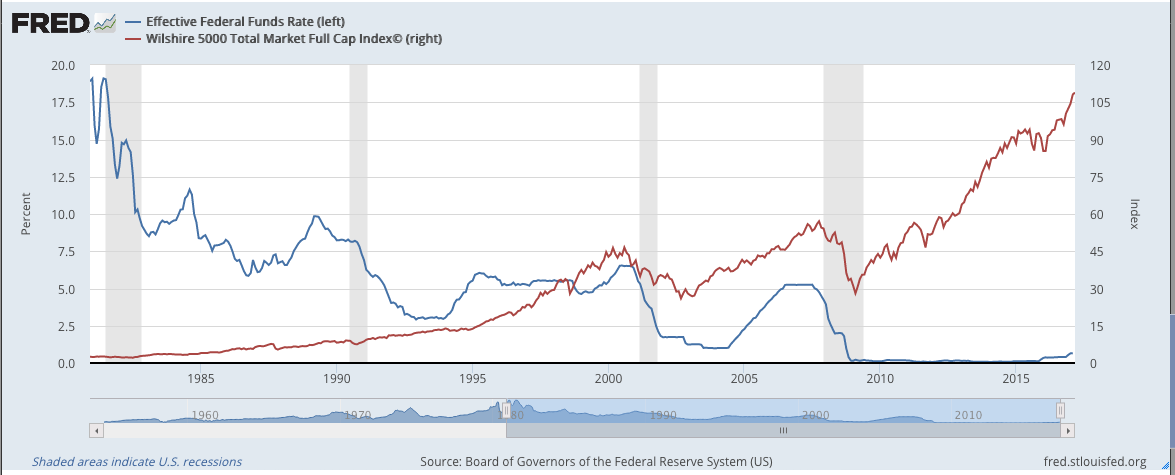

Now, back to the question at hand: can rising rates be good for stocks? An increase in the Fed Funds rate, itself, isn’t necessarily bearish — as the period between 2005-2007 would attest (though, it obviously didn’t end all that well.)

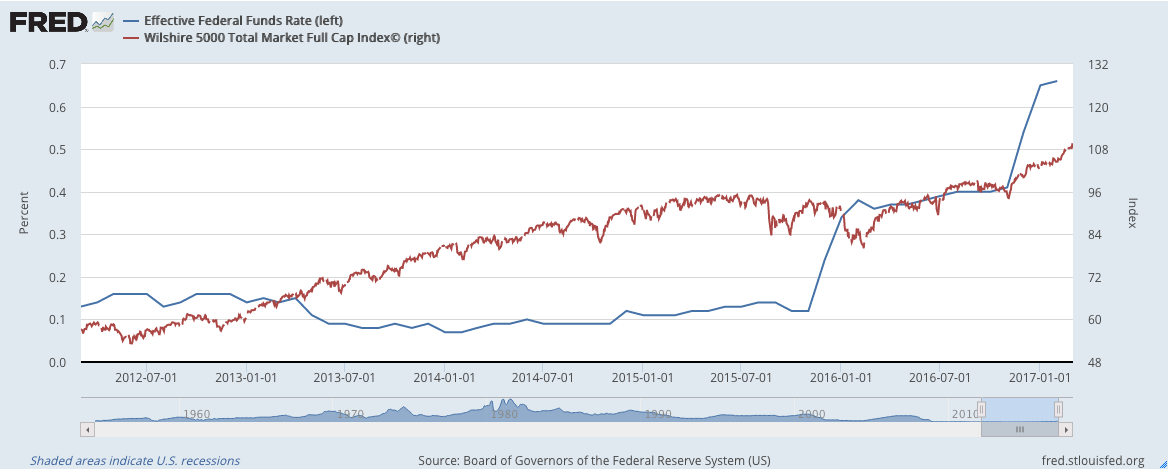

Zooming in on the past five years, we can see that the bulk of the gains came when FF were flat or dropping. The December 2015 increase dinged stocks, while the post-election increase hasn’t. But, again, may would argue that stocks increased in spite of the rate increase (VIX, CL, USDJPY) rather than because of it.

But, if you think of the stock market as big PR campaign, what better way to ensure the rally continues than to “prove” to investors that rising rates not only won’t hurt stocks — but, can actually help them?

I wish I had a nickel for every time I’ve heard how rising rates will help financials make much more money, which will enable the sector to lead all stocks higher. I have no doubt that financials might benefit, provided they’re positioned themselves correctly. But, I doubt the implications would be universally bullish. For every taker of higher interest rates, there’s a payer.

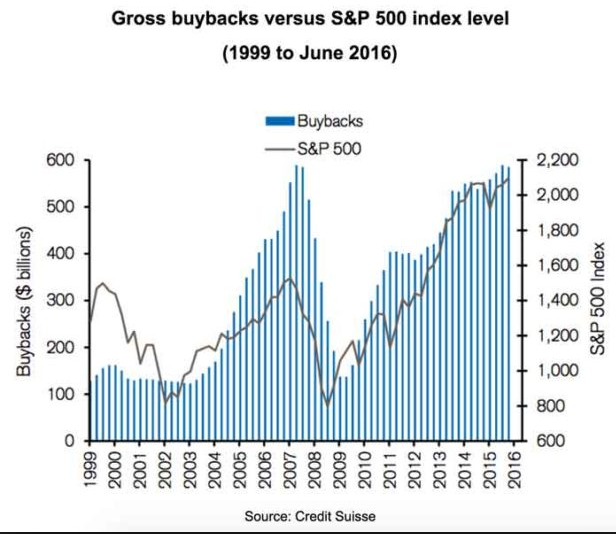

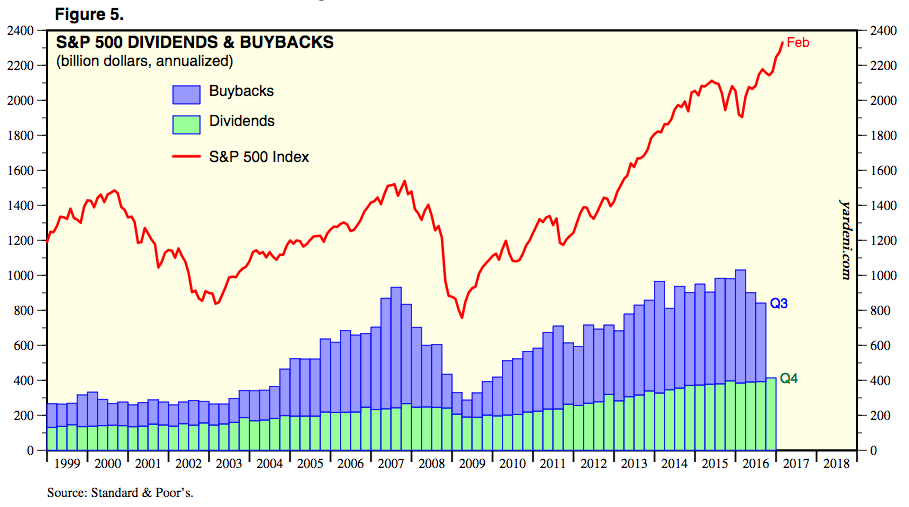

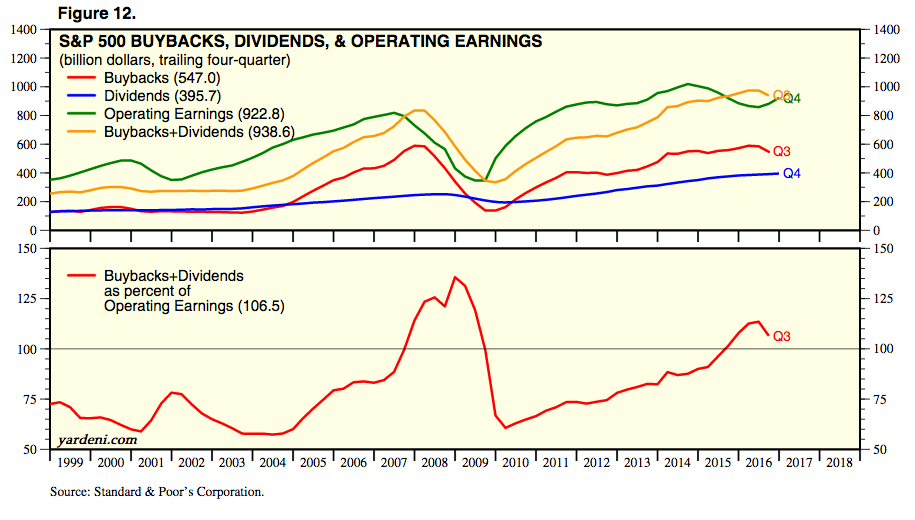

And, corporations are levered to the gills, taking on massive low-interest debt in order to, among other things, buy back stock and make acquisitions at all-time highs. Higher interest rates will hardly benefit these players and those which are simply operating on thin margins (retailers, oil industry, etc.) with too much debt on the books.

Could corporations already be spooked by the prospect of higher rates? This chart from Yardeni Research suggests it’s a very real possibility.

Or, perhaps they’re just spooked at the prospect of spending more than they’re making in order to buy shares at all-time highs. Would that stand up in a careful evaluation of fiduciary duty?

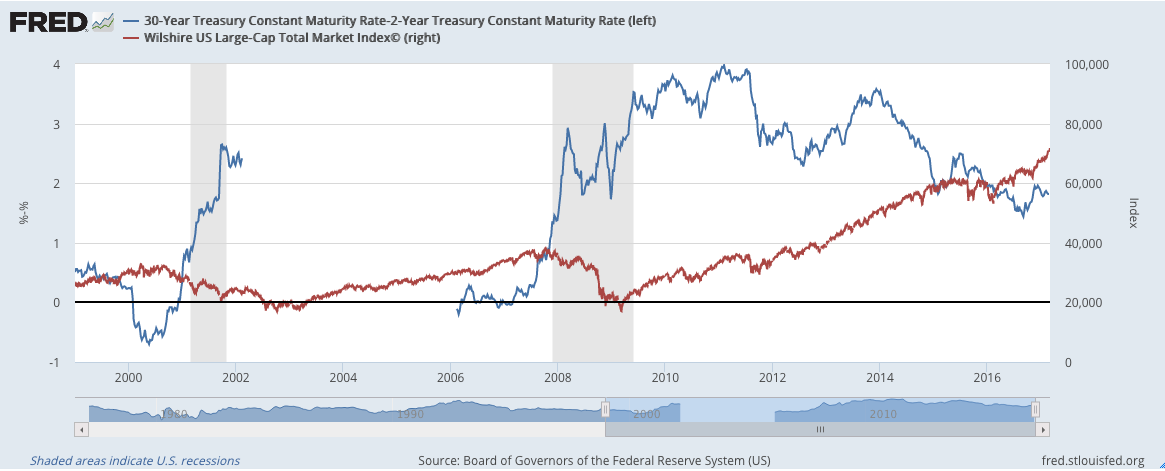

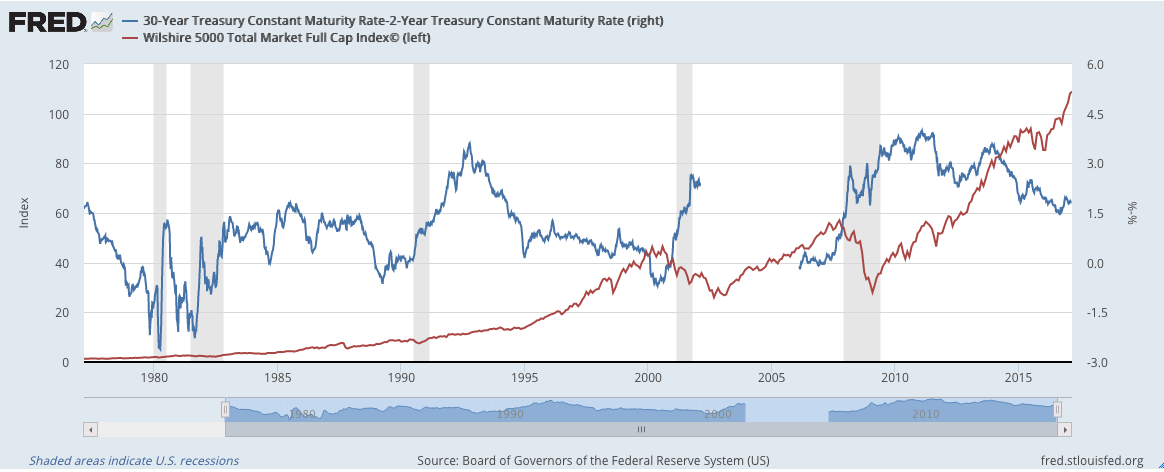

As many have noted, the yield curve has been flattening ever since the US election. Stocks, spurred on by the spike in USDJPY and the crushing of VIX (frequently, only intraday) have largely ignored rates, leading to a strong divergence. This chart appeared in Zerohedge this morning.

Yet, again, it’s hard to draw any clear conclusions regarding spreads and their effect on equity prices. Stocks have risen when spreads were widening, and have risen when they fell.

The most troublesome condition for stocks seem to be when spreads spiked higher, indicating that short-term rates were contracting rapidly. This is to be expected, as: (1) funds flee equities in a correction and are invested in shorter-term treasuries, and (2) more recently, central bankers have lowered rates in times of financial distress.

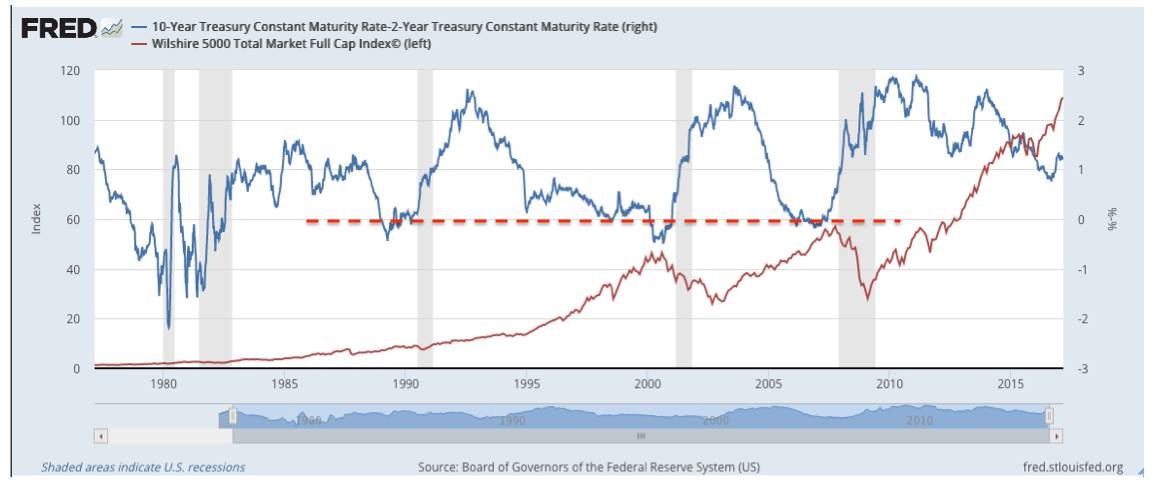

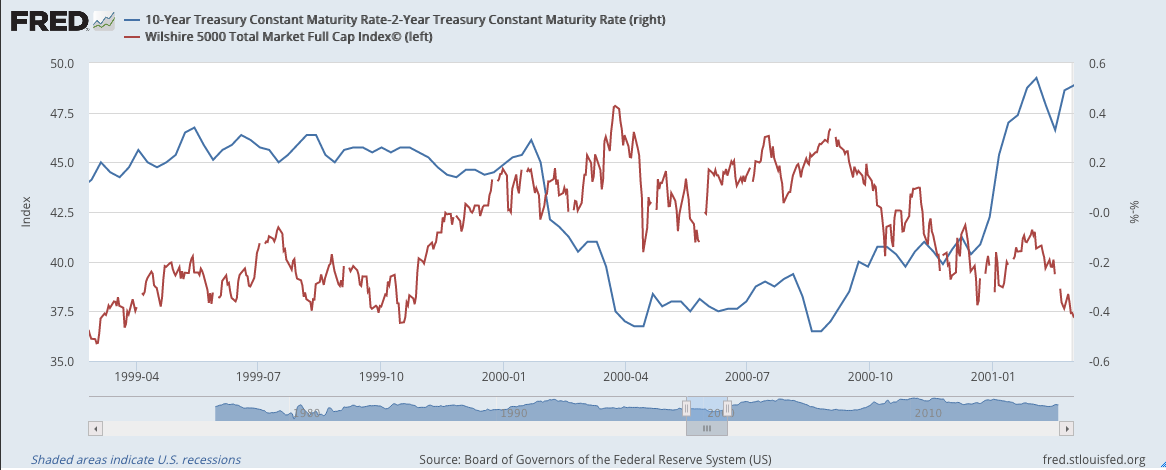

Note that many of the steepest spikes in spreads correlated with equity corrections. BTW, if we look at the 2s10s, the result is very similar. Though, it’s safe to say that inverted curves clearly marked the 2000 and 2007 tops  At best, it has been a sloppy signal. In 2000, the top came almost two months after the curve inverted.

At best, it has been a sloppy signal. In 2000, the top came almost two months after the curve inverted.

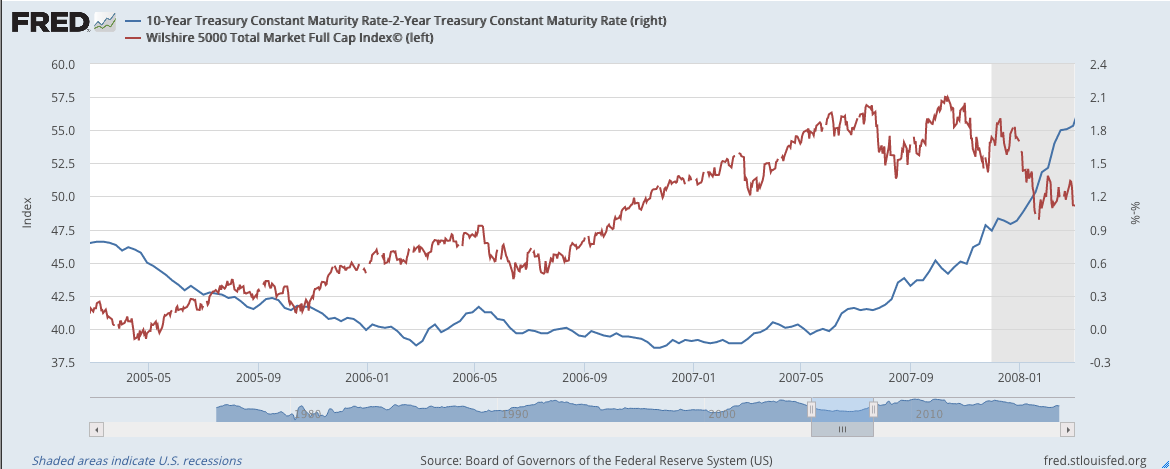

And, in 2007, the top didn’t occur for 18 months post inversion, and about 5 months after it ceased to returned to positive.

And, in 2007, the top didn’t occur for 18 months post inversion, and about 5 months after it ceased to returned to positive.

UPDATE: 10:36 AM

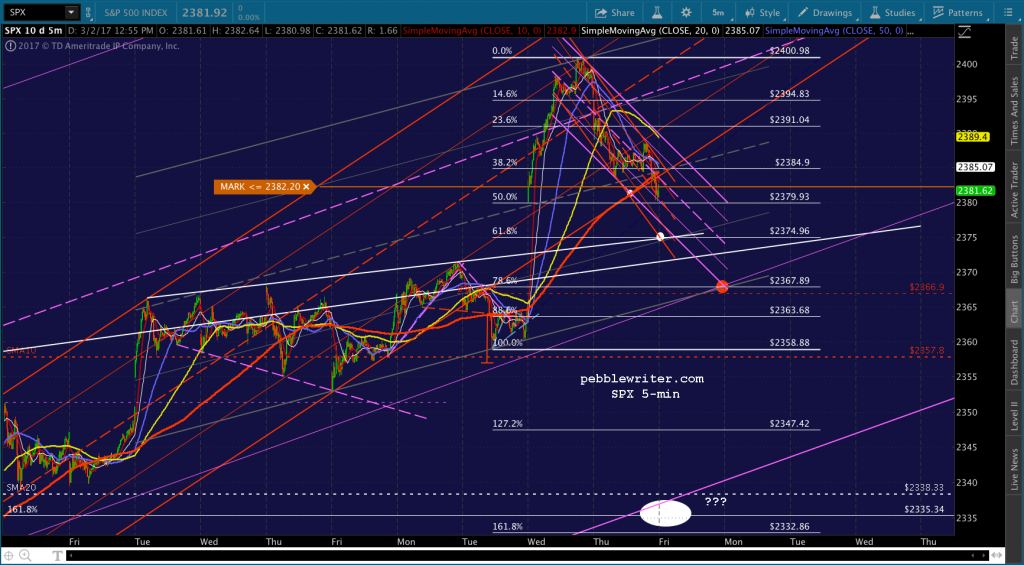

SPX has just about reached our 2374.96 target. I’d say it’s 50:50 whether it bounces here or drops on through to 2371.54 close Tuesday’s gap. The safe bet is to cover yesterday’s short and re-short if it drops through.

My gut tells me it will drop through, as ES could benefit by a drop to at least the SMA10 at 2368.03. But, we’re coming up on the euro close and VIX is still in a position to cause a nice bounce.

And, SPX still hasn’t expressed a preference for the red or purple channel — which could delay a tag of 2371.54 until 1:25 and the SMA10 (which rolled over and is now dropping, by the way) at 2366.90 until the close.

UPDATE: 10:49 AM

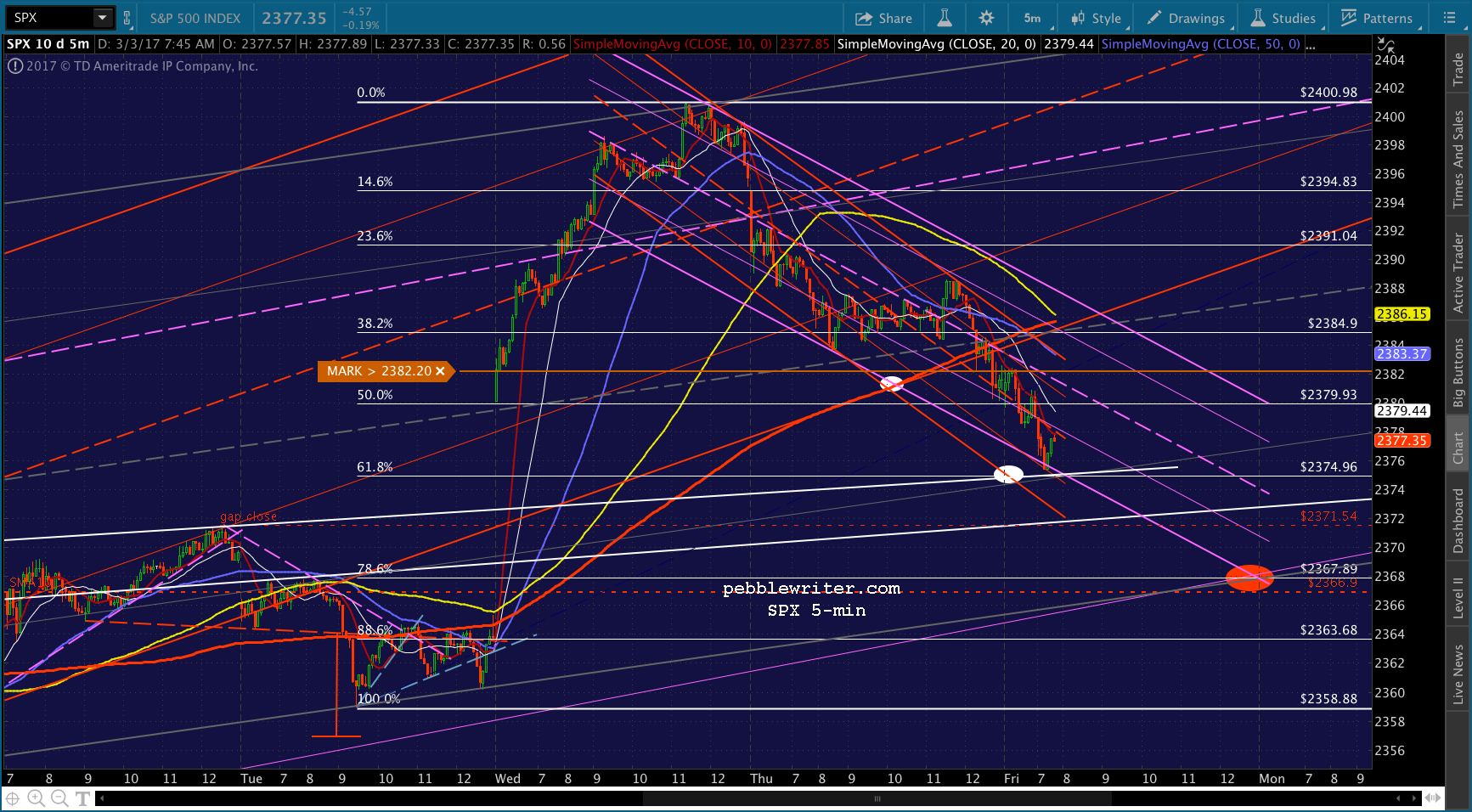

If it’s going to follow the red channel down to 2371 and 2366, this is the place — as, the SMA5 10 has arrived on the scene. If it’s going to delay things, it’ll pop through this resistance and potentially back test the red channel bottom and SMA5 200 at 2386ish by 12:00. Keep an eye on VIX, CL and USDJPY.

UPDATE: 1:13 PM

Janet Yellen has begun speaking, though I’m having a hard time getting alive feed. The content of her speech is available online. So far, the USD and USDJPY are plunging. CL is holding just above the SMA50, and VIX bobbled a little but has essentially gone nowhere. SPX looks like it’s about to drop through its SMA5 10, at which point (2379ish) I’d revert to short for 2371.54 and, if that fails, 2366.90.

I should get a chance to post more later this evening. In the interim, GLTA.