Futures have rebounded from the worst of their overnight losses, but are still on the wrong side of the tracks following yesterday’s breakdown of the rising wedge.

continued for members… (more…)

continued for members… (more…)

Futures have rebounded from the worst of their overnight losses, but are still on the wrong side of the tracks following yesterday’s breakdown of the rising wedge.

continued for members… (more…)

Futures are again backtesting the 200-day moving average as we approach the open.

continued for members… (more…)

continued for members… (more…)

Powell’s speech will take on added importance following the release of this morning’s hotter than expected Q3 GDP print on the heels of a big ADP miss.

Futures are flat after completing the backtest of the trend line from October we had been expecting.

Futures are flat after completing the backtest of the trend line from October we had been expecting.

continued for members… (more…)

Futures are flat following yesterday’s sharp selloff credited to the economic slowdown in China and hawkish Fedspeak. SPX closed below its 10-day moving average for the first time in 3 weeks, but is clinging to an important Fib level.

continued for members… (more…)

continued for members… (more…)

ES came within 10 points of tagging its 200-day moving average on Friday and is backtesting its 3.618 Fibonacci extension yet again.

continued for members… (more…)

continued for members… (more…)

I want wish all our members a safe and enjoyable holiday. We will take Friday off and be back on Monday, Nov 28.

Markets staged a little celebration of their own yesterday, with ES slipping back up above the 10-day moving average and 3.618 Fib – a gizzard’s throw away from the 200-day.

Otherwise, not much drama around the dinner table other than XLE failing again at its 93.31 double top as a rather inebriated CL stumbled and fell. The divergence is really quite stunning.

Otherwise, not much drama around the dinner table other than XLE failing again at its 93.31 double top as a rather inebriated CL stumbled and fell. The divergence is really quite stunning.

Durable goods came in much stronger than expected. Keep in mind that new home sales and Michigan sentiment will be released at 10am and Oct Fed minutes at 2pm.

continued for members… (more…)

This morning is essentially the mirror image of yesterday, with futures up modestly on the usual algo drivers: VIX, USDJPY and CL.

This is the 8th session in a row of treading water, making it the longest “stall” of the year so far.

This is the 8th session in a row of treading water, making it the longest “stall” of the year so far.

continued for members… (more…)

Futures are off modestly in light trading…

… in the lead up to Wednesday’s important economic data dump. From Briefing.com:

… in the lead up to Wednesday’s important economic data dump. From Briefing.com:

In what is starting out as a quiet week, everything is doing as expected.

In what is starting out as a quiet week, everything is doing as expected.

continued for members… (more…)

Japan’s inflation hit a 40-year high in October, driven by a policy of placing stock market gains above all else.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

Although the BoJ has allowed the 10Y to rise to 0.24%… …they have held short-term rates at -0.1% since 2016.

…they have held short-term rates at -0.1% since 2016. The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market.

The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market. The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

Luckily for Japan, they have no bond market per se. The entirety of Japan’s borrowings are purchased by the BoJ. This monetization of debt has gone on for years without repercussions – until now.

The Nikkei was locked in a falling price channel between Feb 2021 and Mar 2022, when the decline finally reached -20.7%. At that point, it was less than 1% away from its pre-pandemic highs of 24,140. It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old.

It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old. Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Come to think of it, the US faces similar problems.

* * *

In other news, VIX has sent the all-clear to algos to rally at least a little further – this being OPEX and all. continued for members… (more…)

continued for members… (more…)

Economic data came in as expected except for Philly Fed – a huge miss at -19.4 versus -5.0 consensus and -8.7 prior. But, it was the former dove turned chief hawk Jim Bullard who decided enough is enough, suggesting rates could reach as high as 7% before inflation is tamed. Futures were not amused.

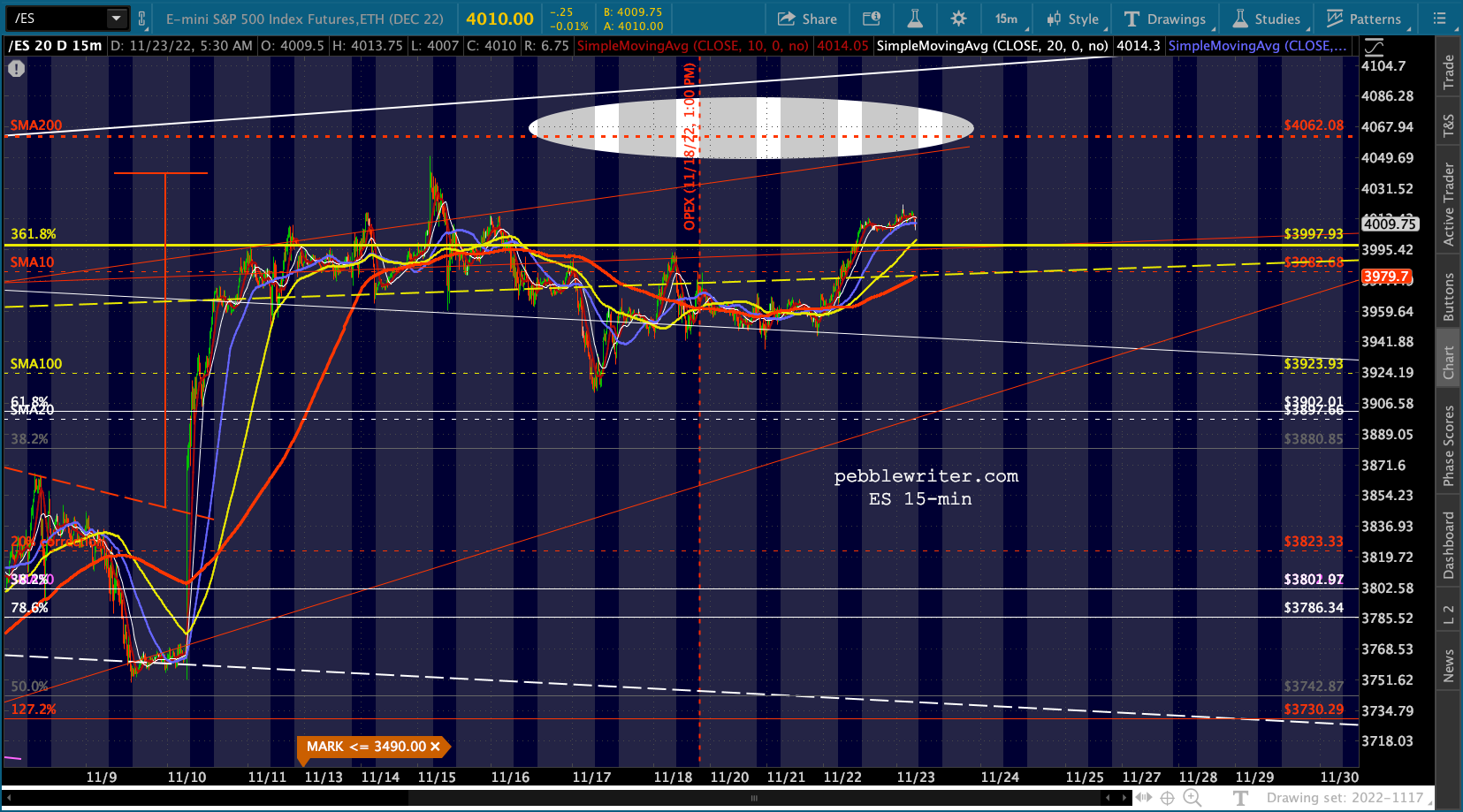

It’s almost inconceivable that ES/SPX won’t tag their SMA200 or channel tops this time. But, even though OPEX is tomorrow, it’s looking that way at the moment.

It’s almost inconceivable that ES/SPX won’t tag their SMA200 or channel tops this time. But, even though OPEX is tomorrow, it’s looking that way at the moment.

continued for members… (more…)