Futures are marginally higher ahead of 2023’s first options expiration.

Note that the 2022 Review and 2023 Forecasts are both completed.

Note that the 2022 Review and 2023 Forecasts are both completed.

continued for members… (more…)

Futures are marginally higher ahead of 2023’s first options expiration.

Note that the 2022 Review and 2023 Forecasts are both completed.

continued for members… (more…)

Futures are up moderately as we approach the open, gaining back much of the losses suffered yesterday in the wake of a dismal pending home sales print (-4.0% versus -0.8% expected, the worst since inception in 2001.) Prices fell MoM for the fourth month in a row.

At this point, it appears the bulls are ready to take a knee and let the clock run out on 2022. Unfortunately, 2023 should prove even more difficult.

At this point, it appears the bulls are ready to take a knee and let the clock run out on 2022. Unfortunately, 2023 should prove even more difficult.

continued for members… (more…)

It seems the algos are content to hold the current line instead of rallying into the end of the year – this Friday.

continued for members… (more…)

continued for members… (more…)

What the algos giveth, David Tepper (bearish) and Q3 GDP (+3.2% vs 2.9% est. and -0.6% last) taketh away. Futures are off sharply as we approach the open.

continued for members… (more…)

continued for members… (more…)

The Bank of Japan has kept interest rates at or below zero for years. Their bet was that the suppression of interest rates (by purchasing Japan’s net issuance, the BoJ now owns over 50%) would offer sufficient protection against both inflation and the 263% debt:GDP – exacerbated by the rapid depreciation of the yen.

Investors, including yours truly, have had their doubts. While effective at propping up equity prices [see: The Yen Carry Trade Explained], the yen’s plunge greatly amplified food and energy price increases. Inflation reached 3.6% in October. It seemed as though something would eventually have to give.

It just did.

The BoJ just announced that they would allow rates to move to as high as 0.5%, sending the 10Y soaring from 25 to 42 bps…

The BoJ just announced that they would allow rates to move to as high as 0.5%, sending the 10Y soaring from 25 to 42 bps…

…and the USDJPY plunging (yen strengthening) by 3.3% – below its 200-day moving average for the first time since Feb 2021.

…and the USDJPY plunging (yen strengthening) by 3.3% – below its 200-day moving average for the first time since Feb 2021.

The BoJ is essentially betting that the small increase in rates will

continued for members… (more…)

As expected, Powell and Co. were not amused by the market’s recent exuberance and decided to take things down a notch.

The algos haven’t yet given up, though, with VIX still under pressure and DXY remaining oversold.

The algos haven’t yet given up, though, with VIX still under pressure and DXY remaining oversold. The reversal is working just fine so far. But, with OPEX tomorrow and two weeks left in the year, we’re left to wonder whether the bulls are ready to throw in the towel.

The reversal is working just fine so far. But, with OPEX tomorrow and two weeks left in the year, we’re left to wonder whether the bulls are ready to throw in the towel.

continued for members… (more…)

Futures are flat following yesterday’s sharp selloff credited to the economic slowdown in China and hawkish Fedspeak. SPX closed below its 10-day moving average for the first time in 3 weeks, but is clinging to an important Fib level.

continued for members… (more…)

continued for members… (more…)

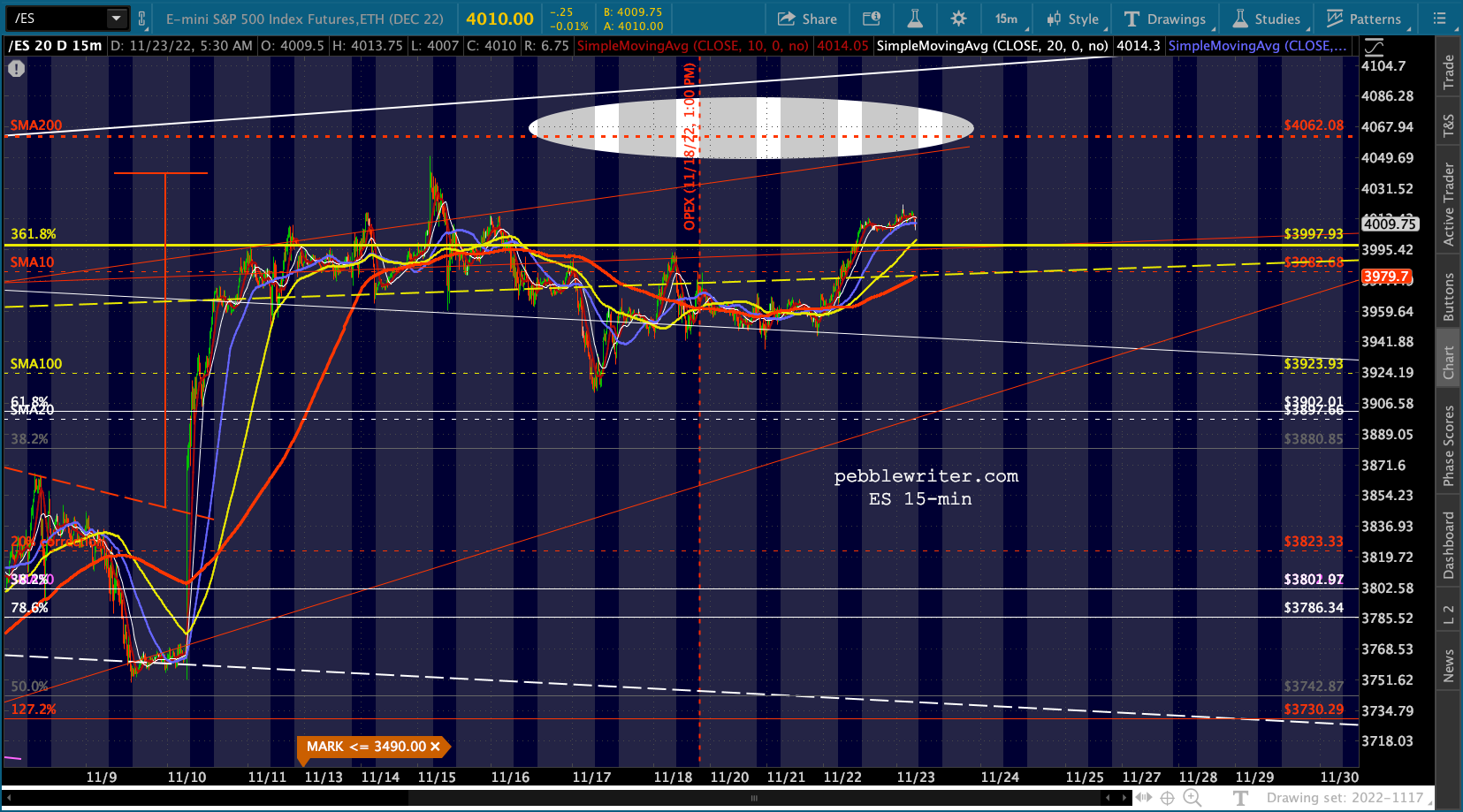

ES came within 10 points of tagging its 200-day moving average on Friday and is backtesting its 3.618 Fibonacci extension yet again.

continued for members… (more…)

continued for members… (more…)

I want wish all our members a safe and enjoyable holiday. We will take Friday off and be back on Monday, Nov 28.

Markets staged a little celebration of their own yesterday, with ES slipping back up above the 10-day moving average and 3.618 Fib – a gizzard’s throw away from the 200-day.

Otherwise, not much drama around the dinner table other than XLE failing again at its 93.31 double top as a rather inebriated CL stumbled and fell. The divergence is really quite stunning.

Otherwise, not much drama around the dinner table other than XLE failing again at its 93.31 double top as a rather inebriated CL stumbled and fell. The divergence is really quite stunning.

Durable goods came in much stronger than expected. Keep in mind that new home sales and Michigan sentiment will be released at 10am and Oct Fed minutes at 2pm.

continued for members… (more…)

Economic data came in as expected except for Philly Fed – a huge miss at -19.4 versus -5.0 consensus and -8.7 prior. But, it was the former dove turned chief hawk Jim Bullard who decided enough is enough, suggesting rates could reach as high as 7% before inflation is tamed. Futures were not amused.

It’s almost inconceivable that ES/SPX won’t tag their SMA200 or channel tops this time. But, even though OPEX is tomorrow, it’s looking that way at the moment.

It’s almost inconceivable that ES/SPX won’t tag their SMA200 or channel tops this time. But, even though OPEX is tomorrow, it’s looking that way at the moment.

continued for members… (more…)