Headline CPI rose 0.2% for the fourth straight month in October. Year-over-year, however, it increased by 2.6% versus 2.4% in September. This was in line our with expectations and increases the odds of the pause we’ve forecast for December’s meeting.

Core CPI’s 3.3% increase (0.3% MoM) further reinforced the market’s concern regarding the inflationary effects of the incoming administration’s plans to enact sweeping tariffs on imported goods.

Core CPI’s 3.3% increase (0.3% MoM) further reinforced the market’s concern regarding the inflationary effects of the incoming administration’s plans to enact sweeping tariffs on imported goods.

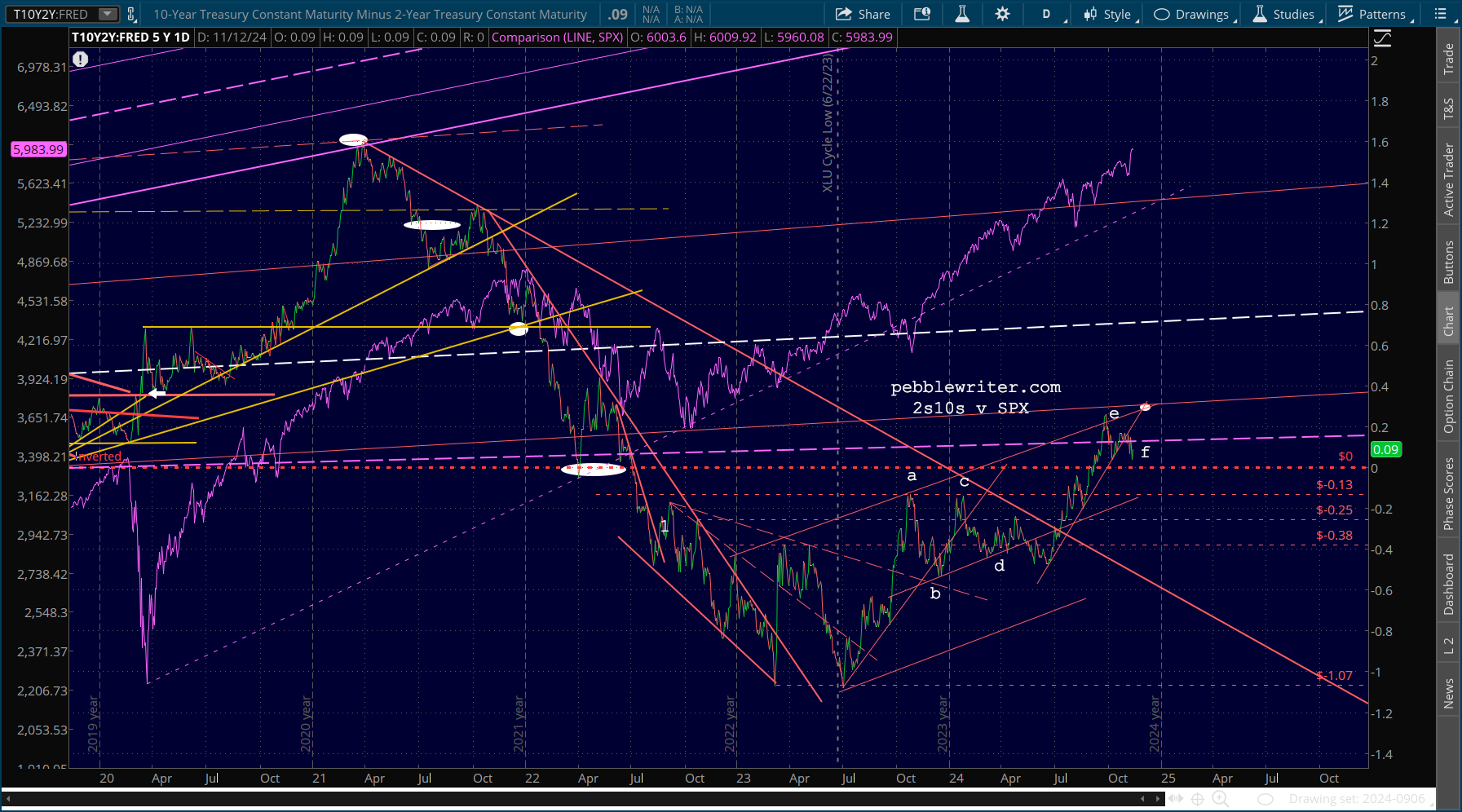

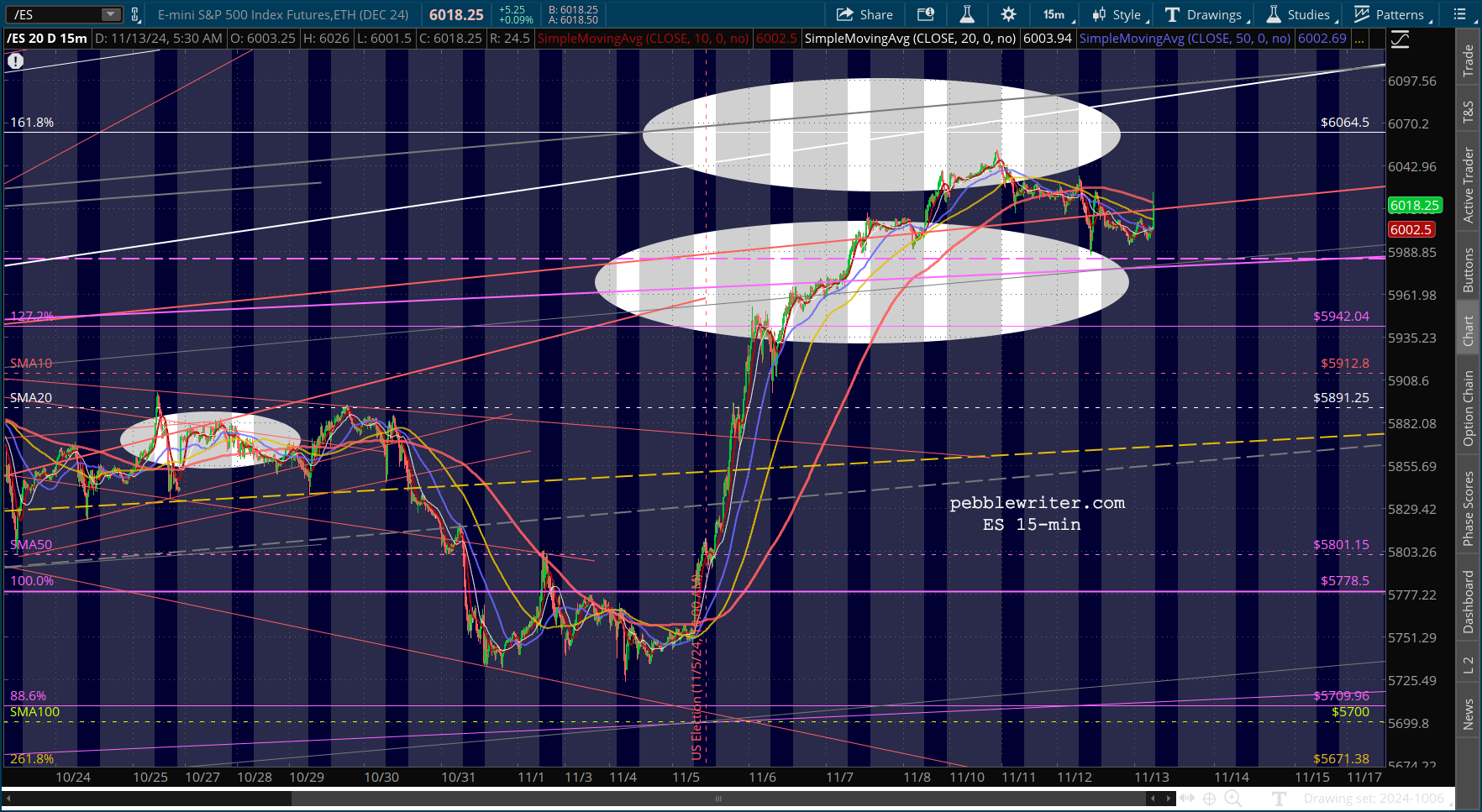

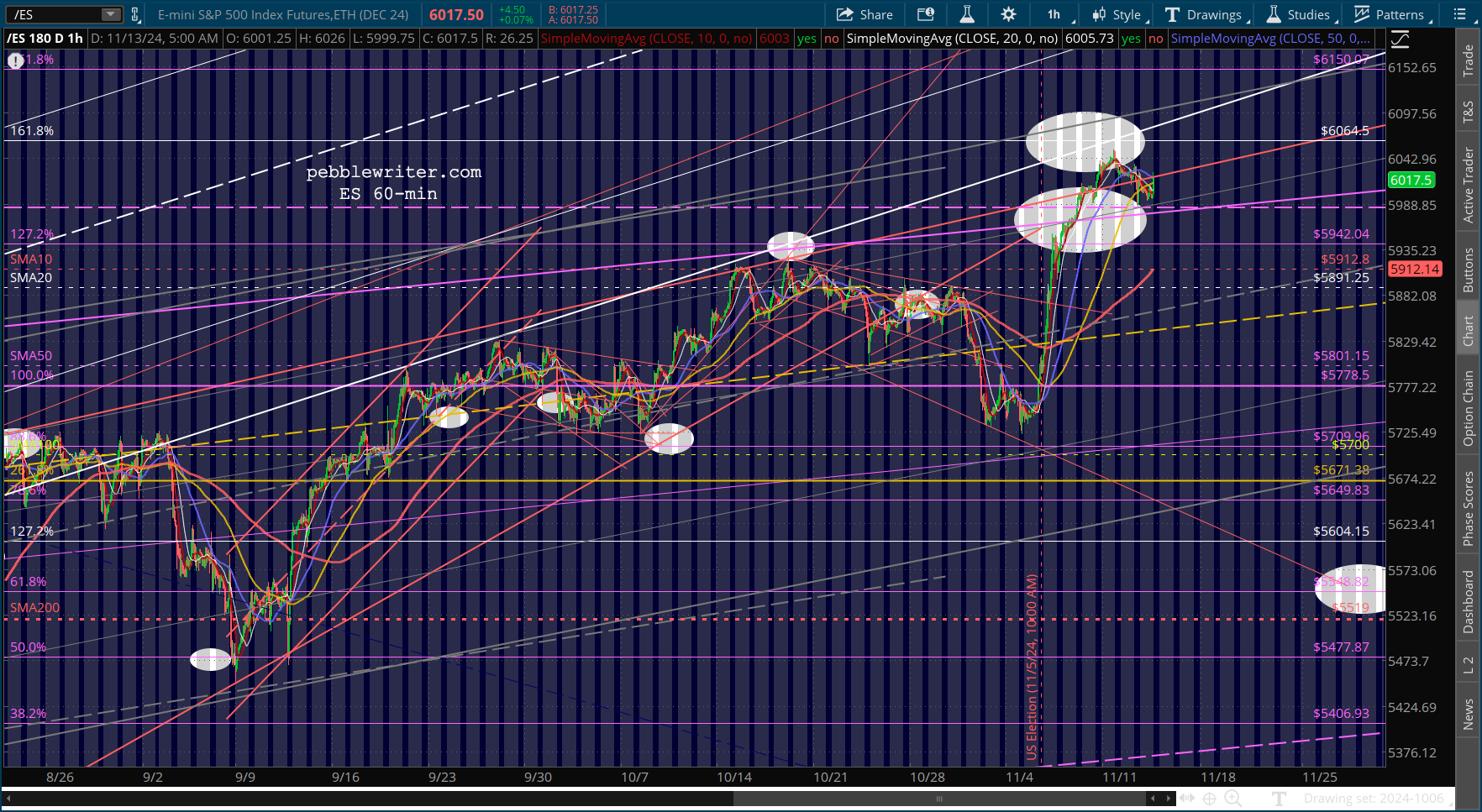

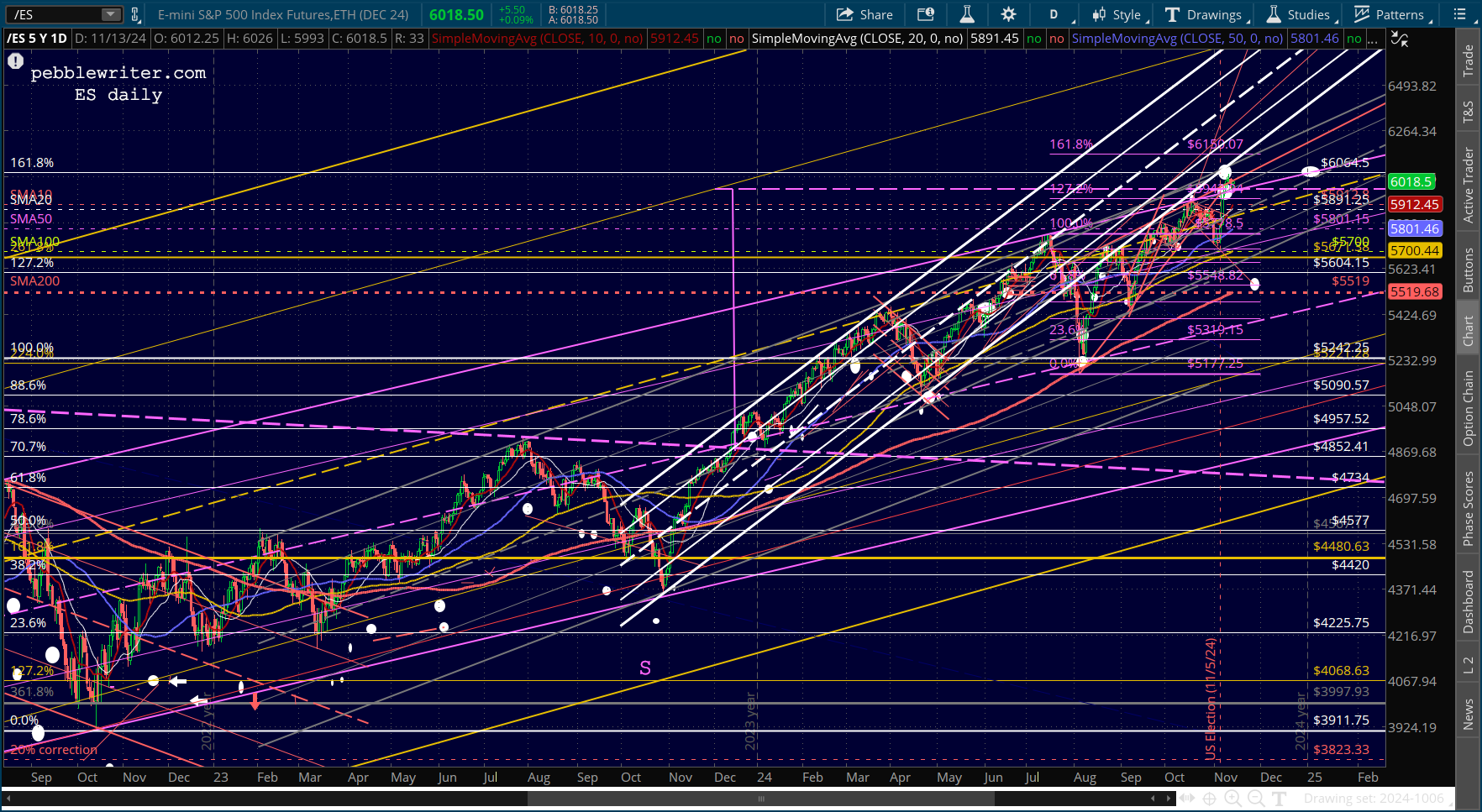

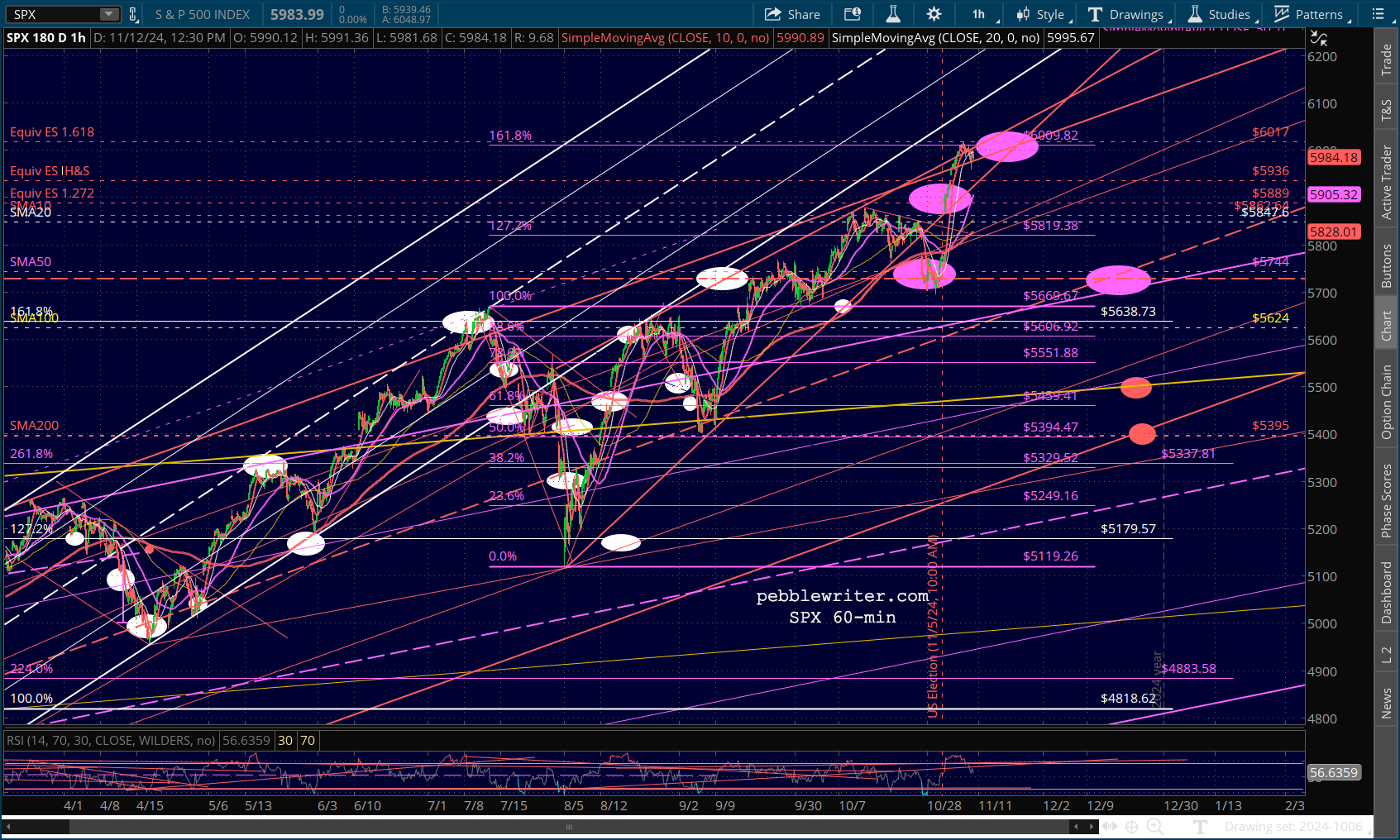

Futures are slightly higher as yields however around important levels of resistance.

continued for members…

continued for members…

SPX’s downside targets represent what would likely happen…

SPX’s downside targets represent what would likely happen… …in the event that VIX doesn’t break down here.

…in the event that VIX doesn’t break down here.  I think it’s asking too much of currencies to carry equities’ water through the end of the year, particularly post the US election.

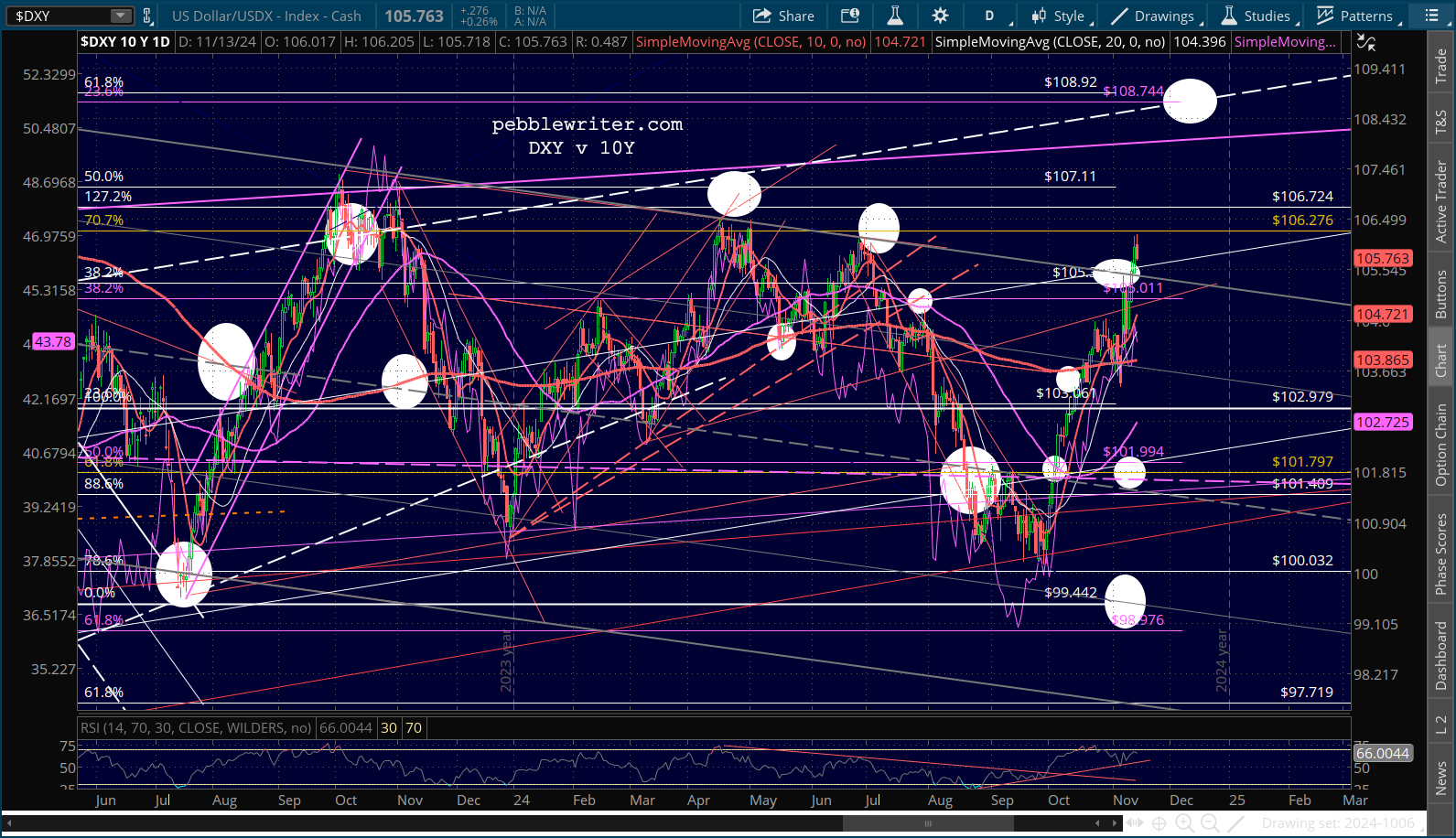

I think it’s asking too much of currencies to carry equities’ water through the end of the year, particularly post the US election.

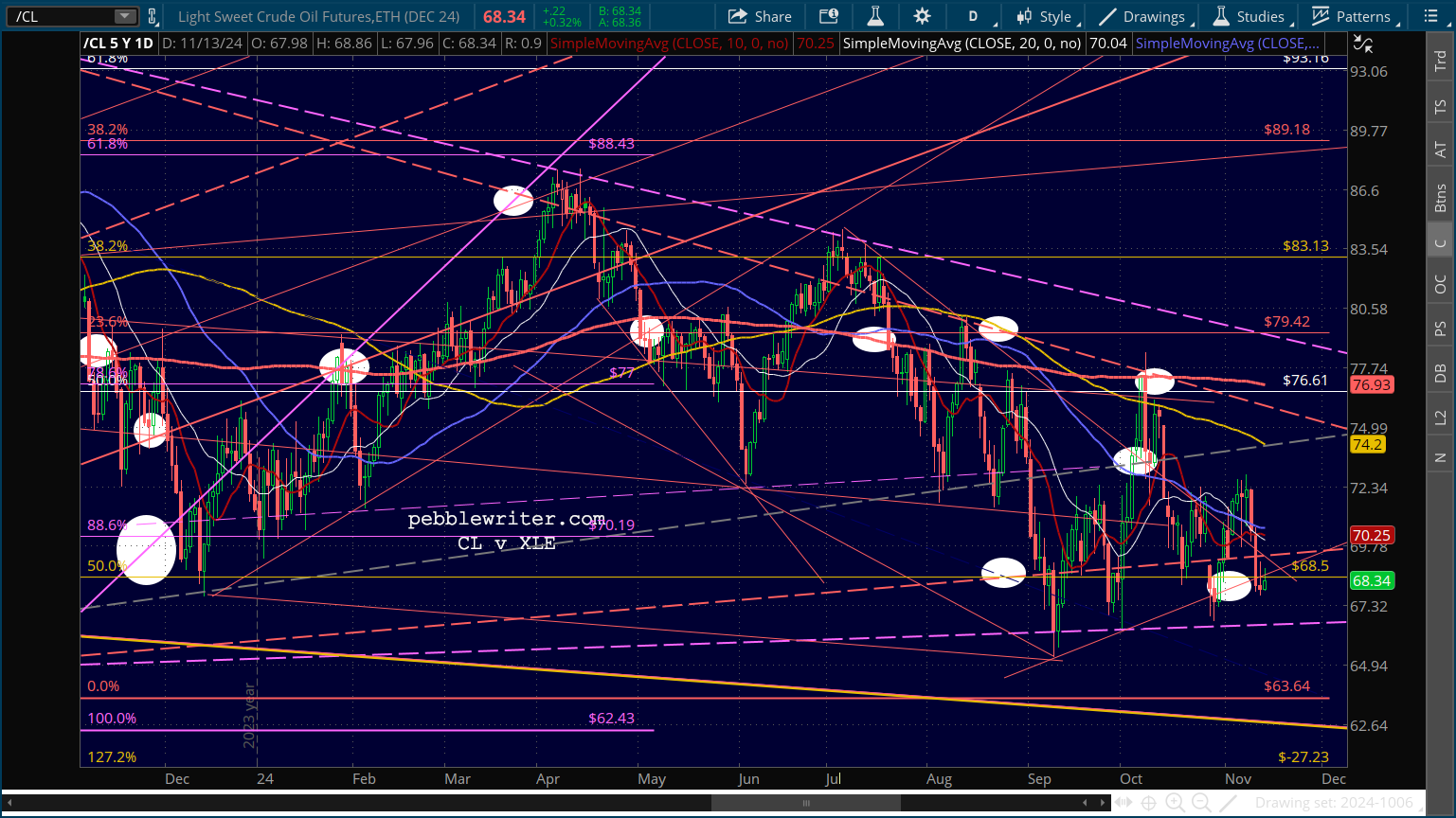

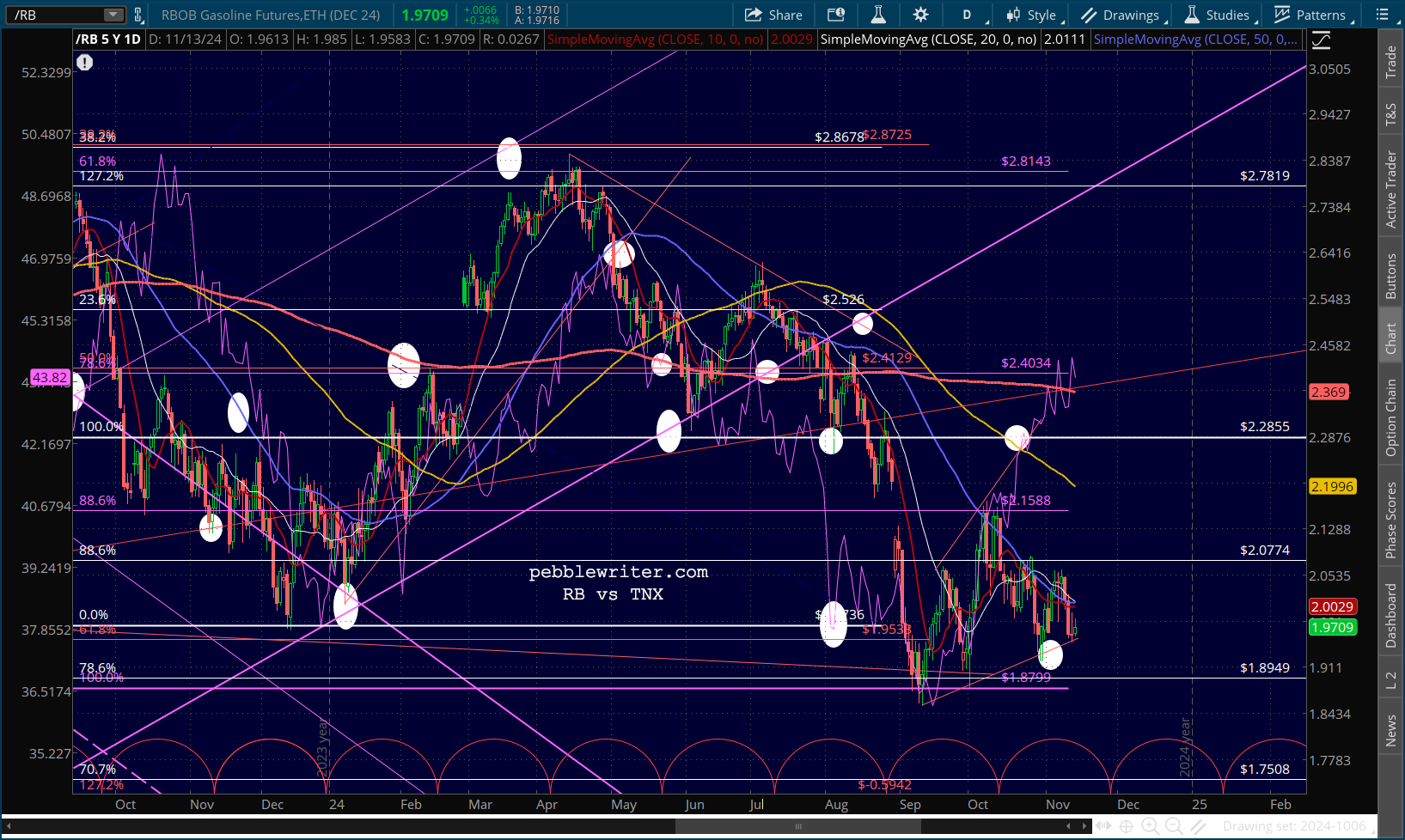

One ray of sunshine is that the rising USD will help offset the increased cost of imports…

One ray of sunshine is that the rising USD will help offset the increased cost of imports… …including oil. Look for CL and RB to break down – as long as the conflict(s) in the Middle East don’t escalate (anyone’s guess.)

…including oil. Look for CL and RB to break down – as long as the conflict(s) in the Middle East don’t escalate (anyone’s guess.)

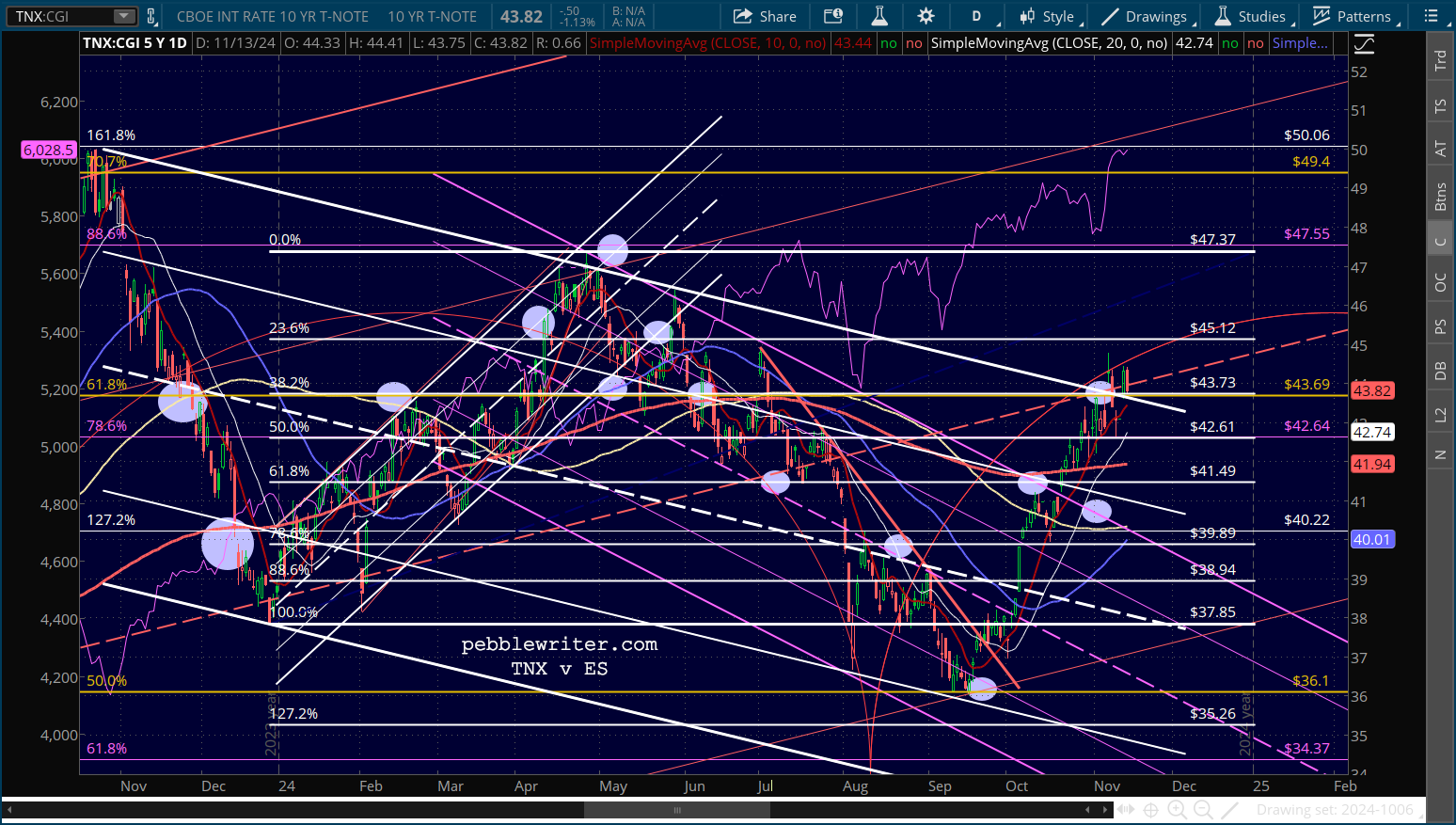

But, the effects are not likely to be enough to prevent the 10Y’s breakout.

But, the effects are not likely to be enough to prevent the 10Y’s breakout.