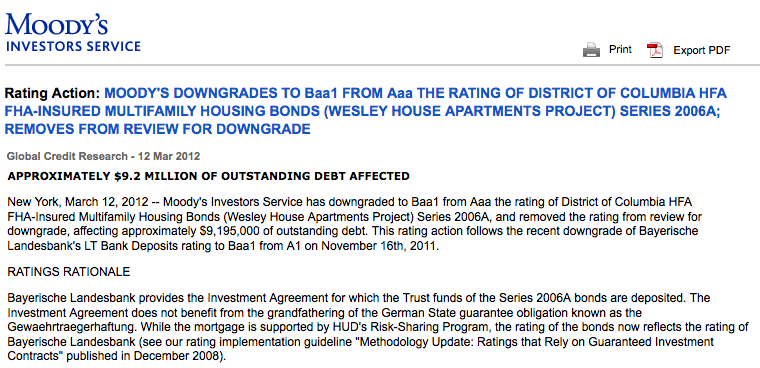

While the talking heads seek to reassure us that the Greek problem is behind us, consider this little-noticed news from Moody’s.

I doubt any of my regular readers own these bonds, and thus would likely feel unaffected by the news. But, I’m seeing more and more of these little blurbs lately. And, the cumulative effect could be devastating to the markets.

Institutional investors (pension funds, corporations, insurance companies, money market/mutual funds, foundations etc.) are all about rules. In almost every case, an investment committee establishes very precise rules governing what the fund may and may not invest in. So, when an instrument formerly rated A1 is downgraded to Baa1, there’s a decent chance some investors will be required to dump it.

Many bond issues lack the inherent credit-worthiness to be considered high grade on their own merits. They purchase credit enhancement from a high grade bank, analogous to renting a co-signer on a loan. When that co-signer’s credit takes a hit, as occurred here when Bayerische Landesbank was downgraded, everything the co-signer vouched for is suddenly affected.

In a healthy, orderly market, it’s not a big deal. The issuer finds a new co-signer and life goes on. But, when there’s a systemic decline in the credit ratings of most of the co-signers out there… well, Houston we have a problem. In the article accompanying the BL downgrade this past November, Moody’s noted:

Moody’s said in July it initiated or continued creditrating reviews for 12 German banks on concern assumptions ofsupport for the lenders may be challenged as the political willto shoulder bailout costs weakens.

Well, with CDS being triggered Friday, banks across Europe are being hit with costs they had assumed would never be realized. And, with Ireland and Portugal scheming to snag their own bailout restructurings, the contingent liability is in store for the Euro Zone financial community is about to soar at a most inopportune time (Basel III.)

Add in the fact that many of the affected countries are facing elections in the coming months — meaning even less support for the sweetheart deals the incumbents made with banks — and it’s pretty likely that more downgradings are in store for the co-signers. Given the degree to which they partook of the latest LTRO, it would seem there are too many snouts in the trough as it is.

So, to bring the idea full-circle, what happens when even more banks suddenly lose support from governments no longer willing to bend over backward to keep them from failing? We’ll be seeing lots more downgrades from the rating agencies — which, of course, means lots more downgrades for all the instruments backed by said banks. Institutional investors will have no choice but to dump the affected instruments — meaning even more underfunded pensions (another story getting no coverage whatsoever) and financial institutions which will lead to…yep… more downgradings.

It’s a feedback loop that could get real ugly, real fast.

Comments

8 responses to “Houston, We Have a Problem…”

I understand there are now people burying gold coins purchased with cash in remote desert locations found only by GPS. Quietly stashing cash outside US borders has become iffy, as one by one the formerly secretive jurisdictions are folding under US govt pressure.

On the tax front… in California they quietly postponed the use of tax loss carry-forwards for AMT purposes. Ouch. No rationale — just wanted more tax revenue.

Retire? Unless you're one of the 1%….retirement is right out the window.

–

That reminds me of Japan. MISH' posted a good article on Japan just earlier. What a demographic utter mess. How can ANYONE expect to retire in Japan?

Unless they can somehow have an army of 50 million robots to look after their elderly, urghh..its not good outlook.

–

Just finishing up our 2011 taxes. There is a new question this year – "At any time during 2011, did you have a financial interest in … a financial account … located in a foreign country" ? It's interesting because we set up a small foreign account the first week 2012 (in case we can ever really retire).

Hmm – if PW's contest was for 1 day (and not 5) I would win !

My sixth sense says that there can't be a sizable downturn until there is more (retail) volume.

Whack-a-mole. ha.

–

re: 'no choice but to sell'.

They could always make it illegal to sell. I don't put anything past them.

–

In the HUGE bigger picture of things…two words come to mind after reading your comment. Not directly related, but via the whole 'currency being printed out of existance'.

Those two words……………. CAPITAL CONTROLS.

—

I gotta say they are scary words to me, since once we reach that stage, what then? Hell, I got a US $ trading account, but its based in the EU. I can only imagine the day when its frozen up by some govt' decree.

Or maybe it'll just all vapourise..ala MF Global. Maybe I'm just being too doomster this evening, lol.

Your point on the exponential rate of the moles….yeah.. it is indeed very important. Clearly, we need to confront this mole problem.

Good wishes.

It's a strategy that will work perfectly — until it doesn't. When it's individual cities, counties, housing finance agencies, etc. — you're right. He can play QE twist whack-a-mole. The problem comes if/ things snowball, and the sellers are disposing of a vast array of FI instruments because they're required to. If you're a bank or insurance company or money market fund, you might have no choice but to sell. How many individual issues can the Fed buy, and at what aggregate cost? It's whack-a-mole where the moles are multiplying at an expoential rate.

The Bernanke can just print to cover the minor regional Muni shortfalls. Why not huh ? If he is going to buy more MBS sometime this year, I'm sure he could get the backing to bail out each of the states who are already insolvent.

–

Benny is pretty good at whacking a square air filter in a round hole.

absolute collapse in Volatility today consider spx is unchaged. What gives??