More data for the hawks, this morning, as starts and permits both handily beat expectations. Which data, exactly, will the Fed depend on in order to cut rates? Futures are off a few points…

Futures are off a few points… …(barely) breaking out of a falling channel at the insistence of a slumping VIX.

…(barely) breaking out of a falling channel at the insistence of a slumping VIX.

continued for members…

continued for members…

Stretched, but not yet broken…

Nothing has really changed from yesterday.

Nothing has really changed from yesterday.  Everything is well-positioned for a decline.

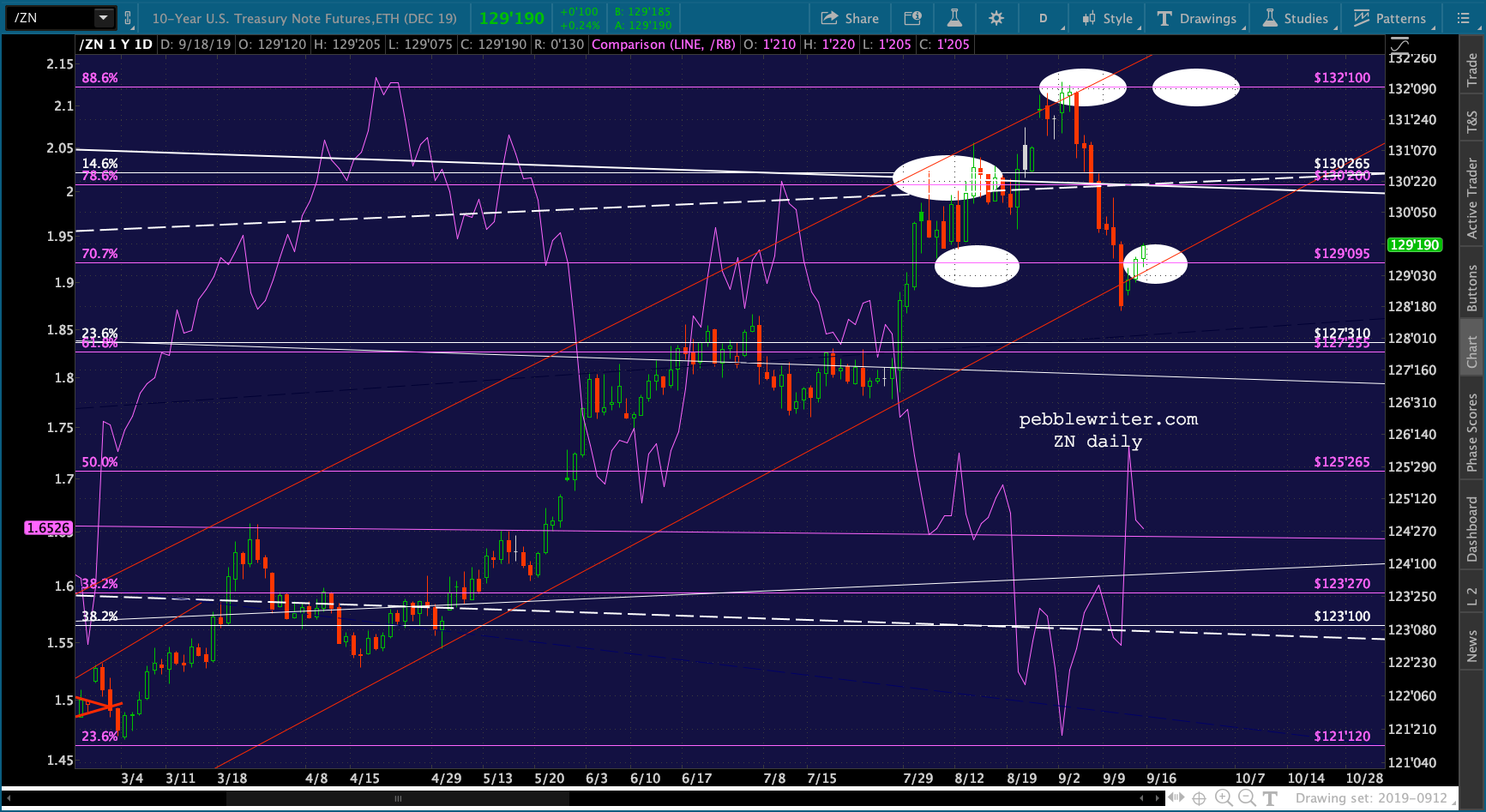

Everything is well-positioned for a decline. The 10Y is bouncing as expected.

The 10Y is bouncing as expected.

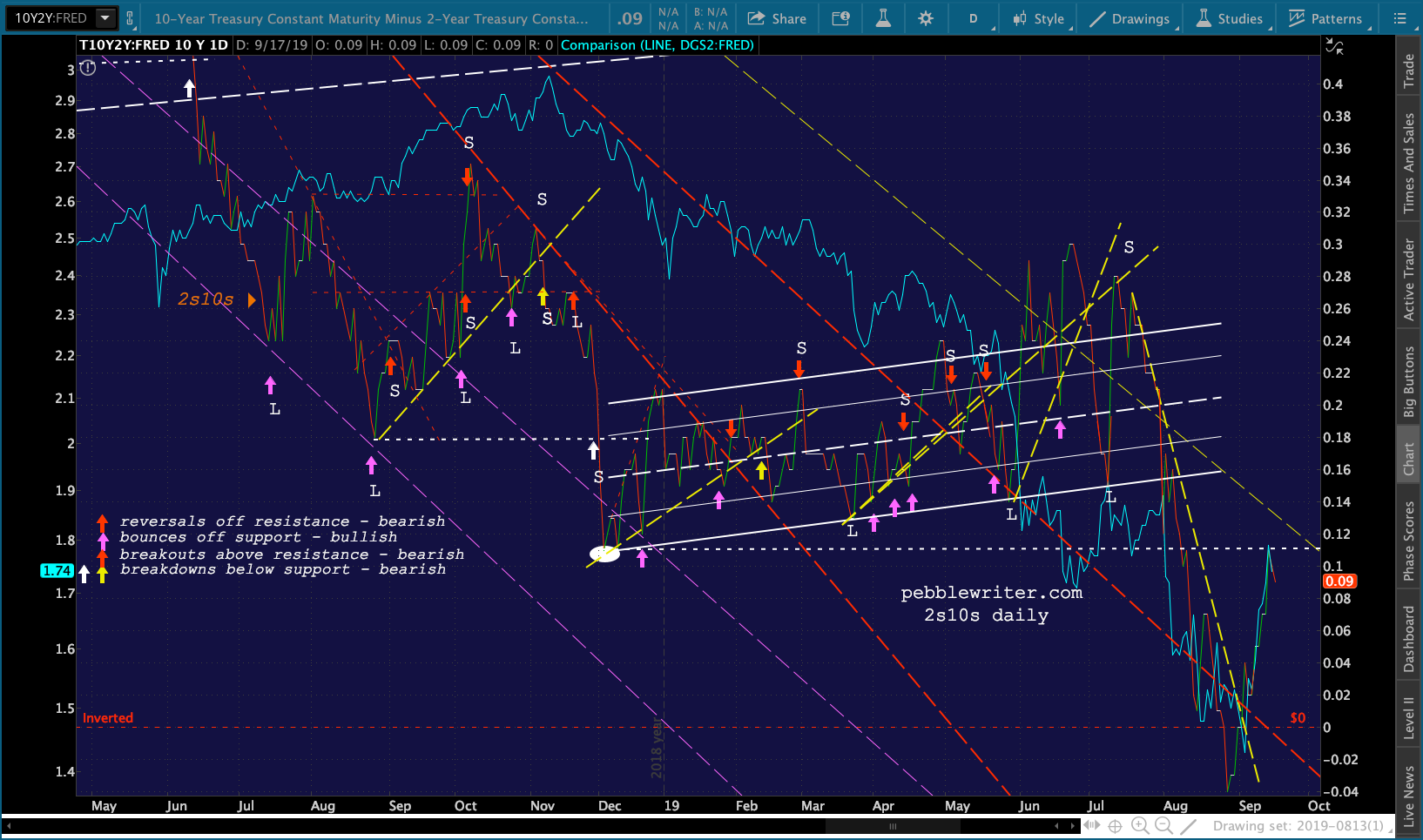

And, the 2s10s has reversed off of overhead resistance, a bearish development — as is the breakout above the steep yellow TL.

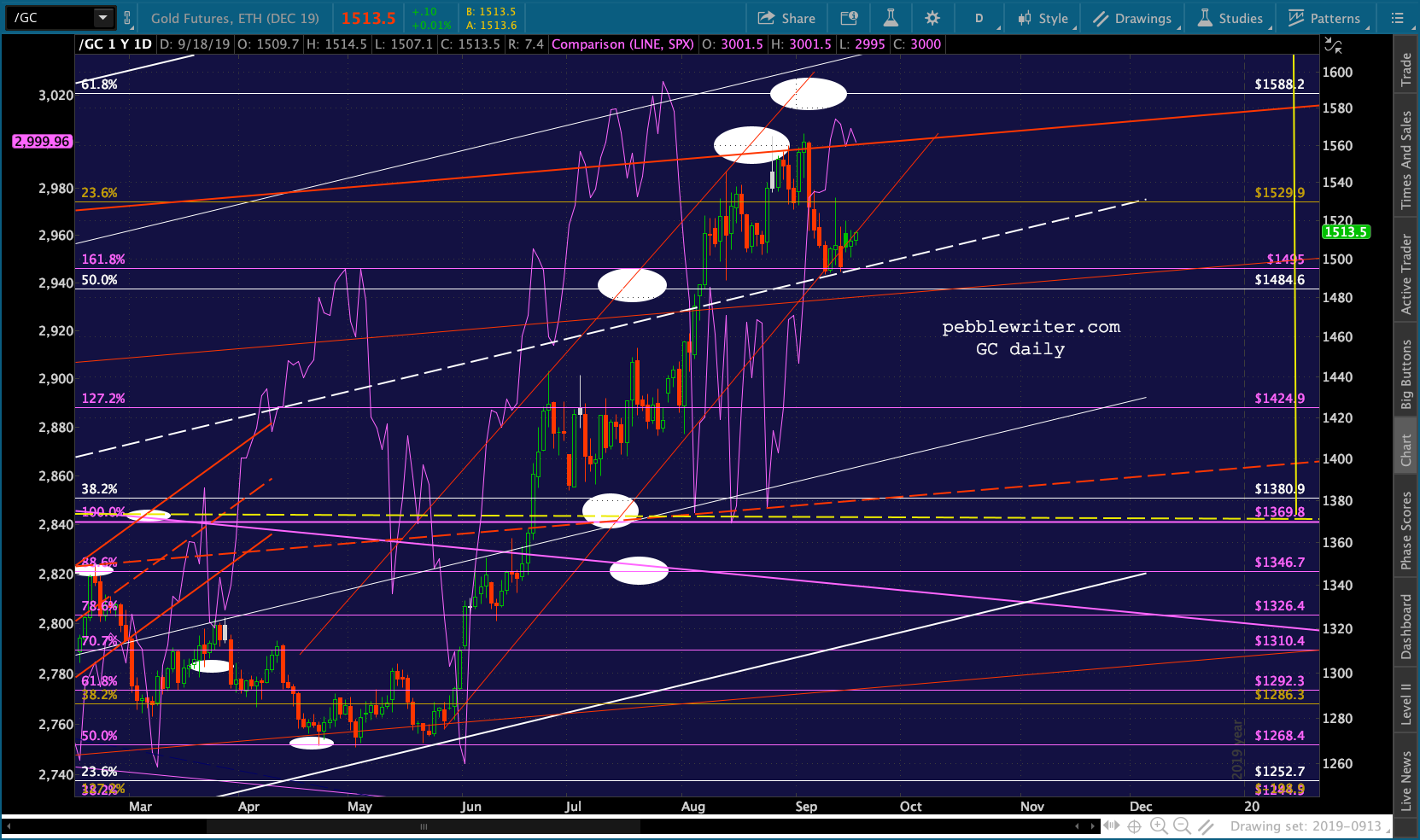

And, the 2s10s has reversed off of overhead resistance, a bearish development — as is the breakout above the steep yellow TL. GC is still bouncing as expected.

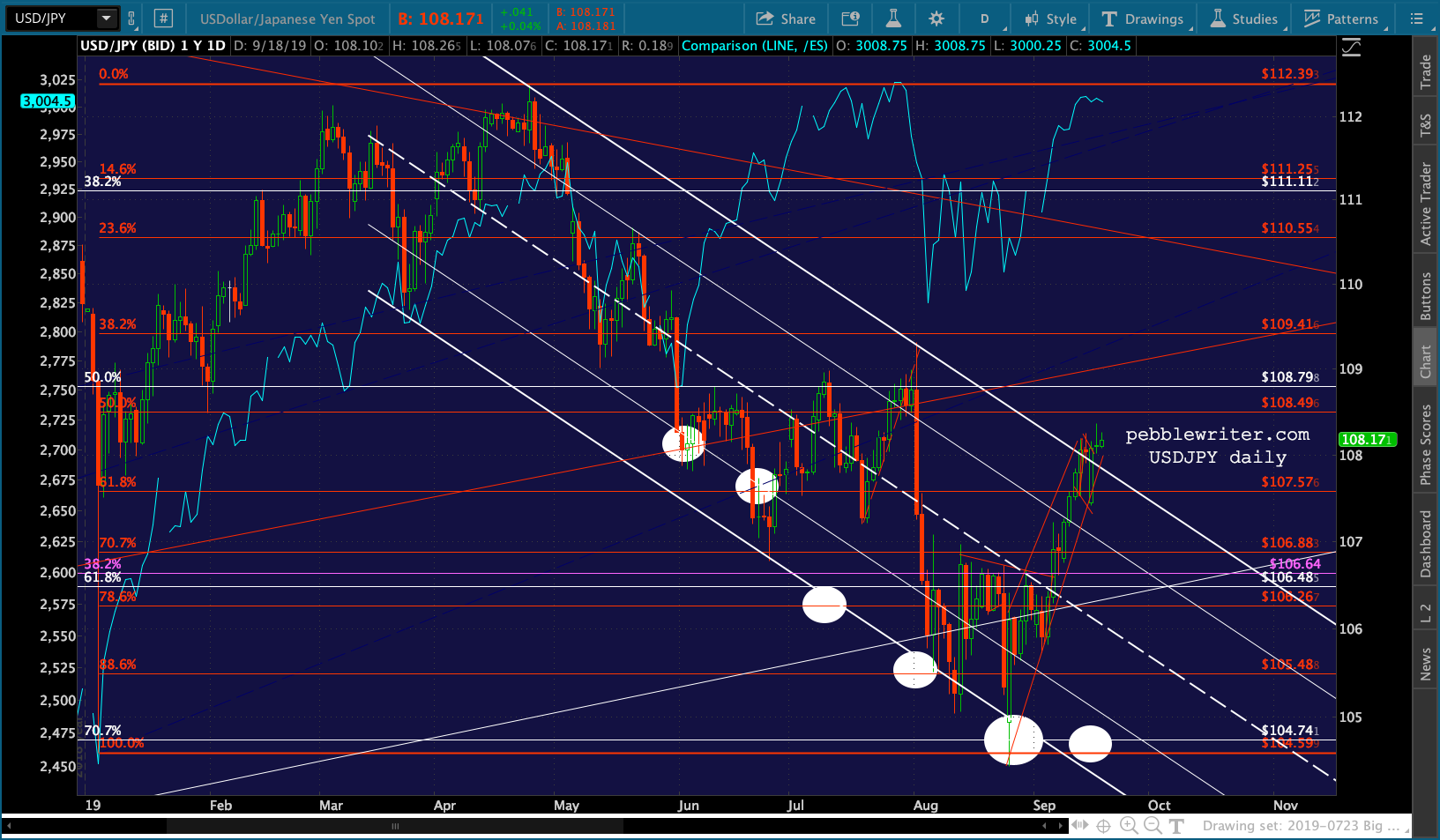

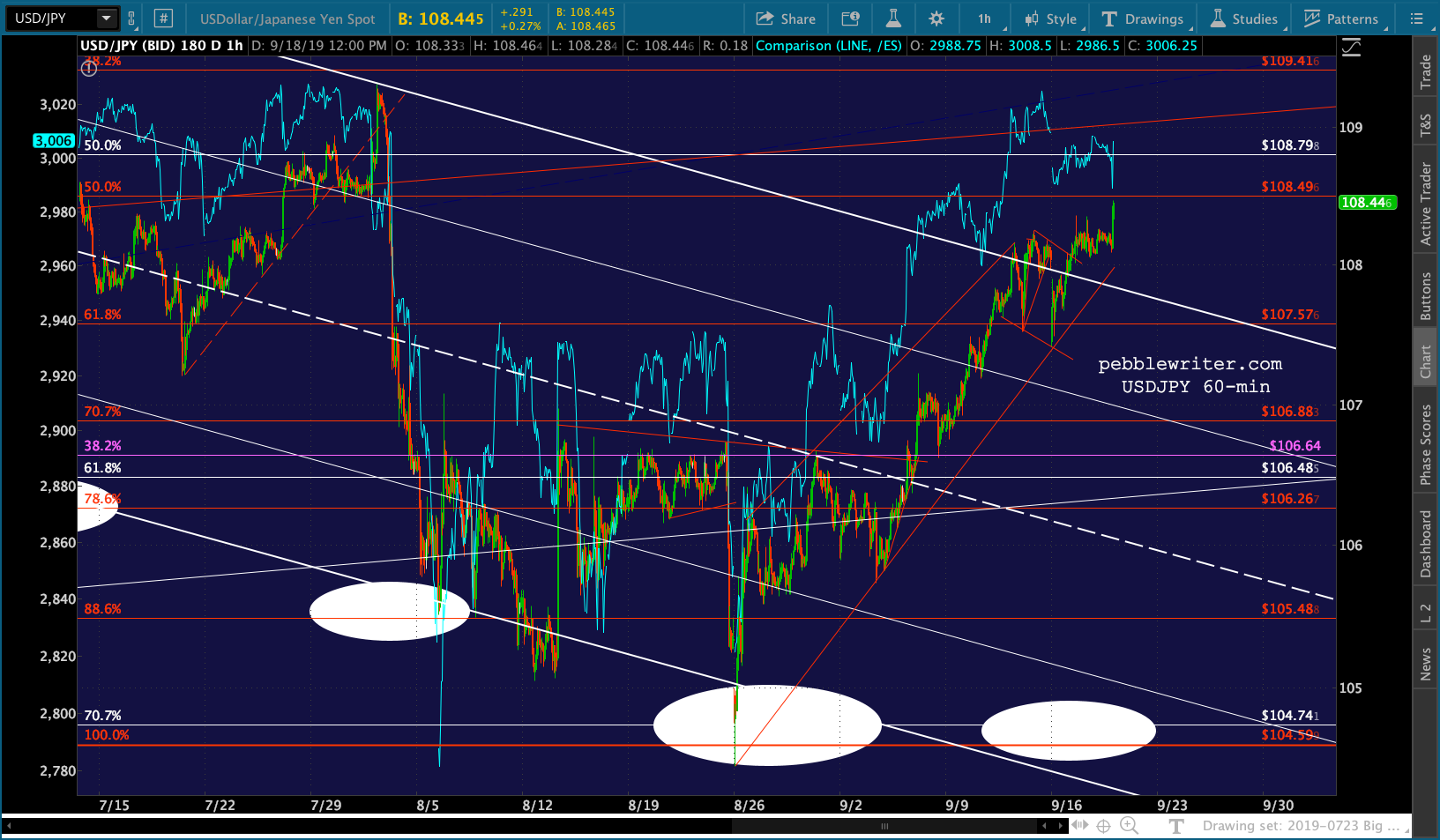

GC is still bouncing as expected. USDJPY is still threatening a breakout, but hasn’t really – at least yet.

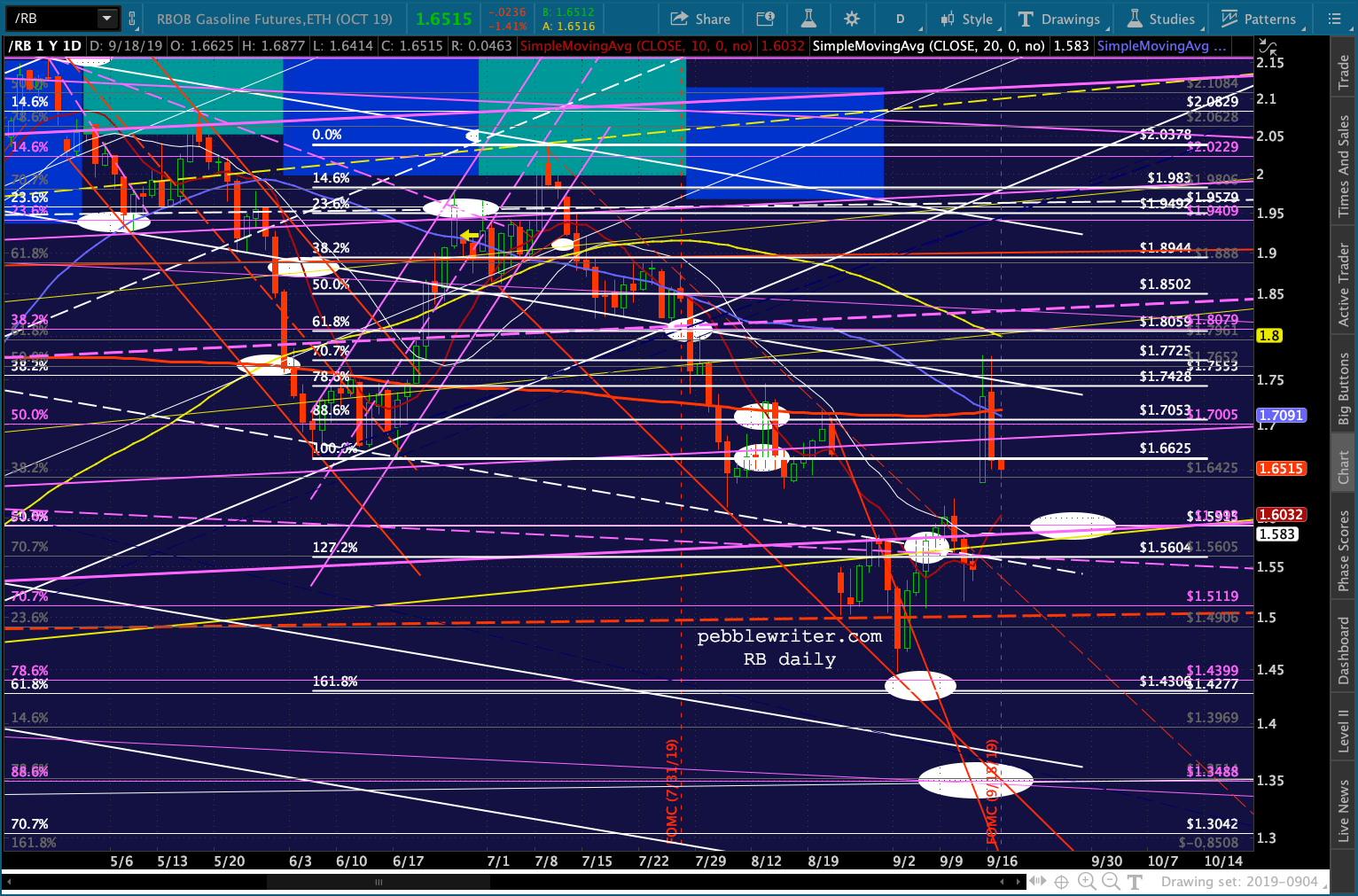

USDJPY is still threatening a breakout, but hasn’t really – at least yet.  RB continues to pull back…

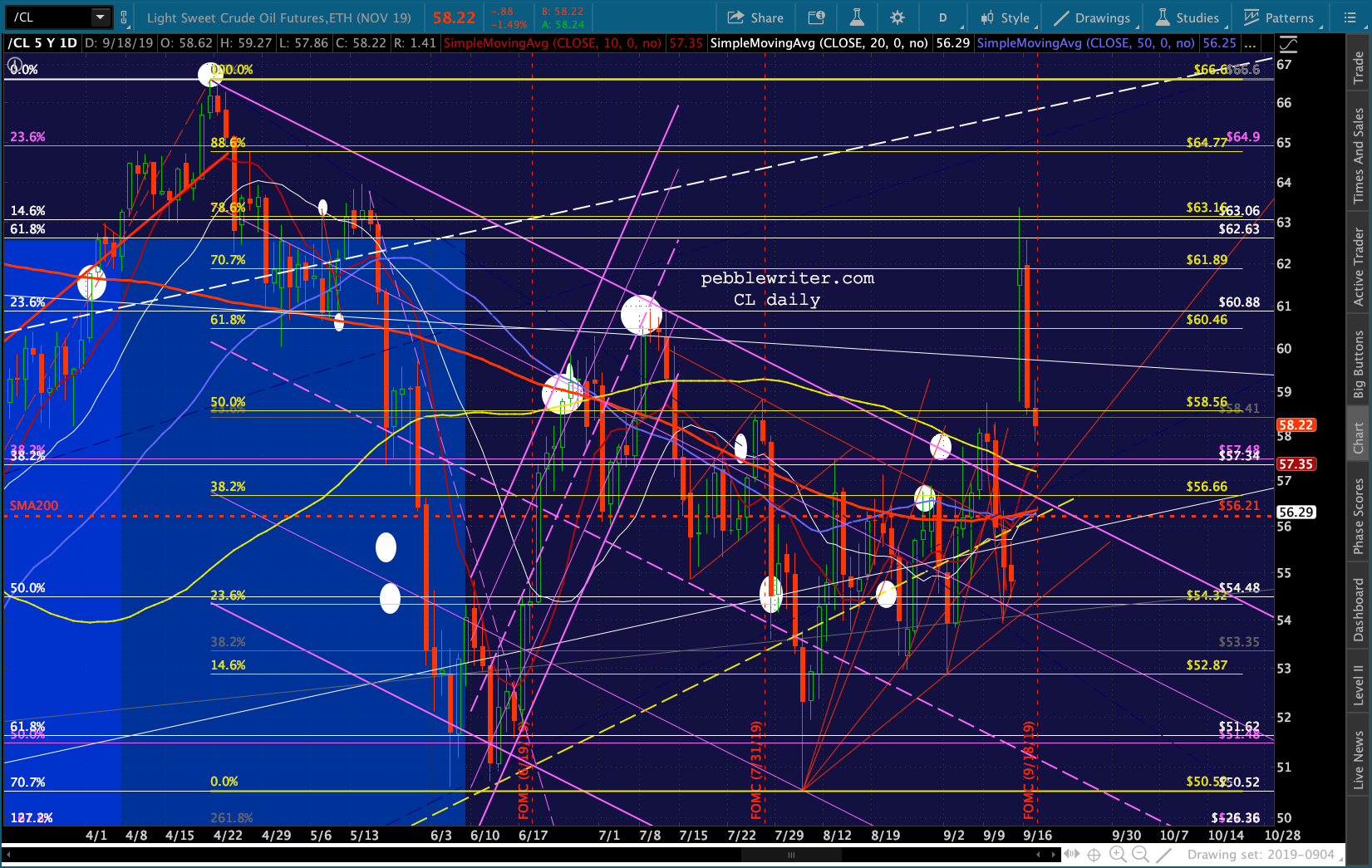

RB continues to pull back…  …while CL has retraced all its breakout — but, closed the gap.

…while CL has retraced all its breakout — but, closed the gap.  It’s safe to say that the market would tank if the FOMC didn’t cut today. It might also tank if they cut 25 bps but the comments reflected a lack of consensus and had a less than dovish tilt. It might even tank if the actions are overly dovish, reflecting more fear about the state of the economy than we thought. About the only action that would likely be bullish for the market would be a 25 bps cut now, new QE – ostensibly to cover the repo fiasco, and somewhat dovish comments along the lines of there being two more cuts likely.

It’s safe to say that the market would tank if the FOMC didn’t cut today. It might also tank if they cut 25 bps but the comments reflected a lack of consensus and had a less than dovish tilt. It might even tank if the actions are overly dovish, reflecting more fear about the state of the economy than we thought. About the only action that would likely be bullish for the market would be a 25 bps cut now, new QE – ostensibly to cover the repo fiasco, and somewhat dovish comments along the lines of there being two more cuts likely.

Having said that, the propping tools and techniques are working just fine. And, there’s always Trump’s Twitter account, which would likely spring into action if stocks began to tank. In other words, while I believe a drop is still likely, this is not the time to bet the farm.

I don’t expect very much to happen until the FOMC announcement at 14:00, so I’m going to work on the analog for a while. More later.

UPDATE: 1:55 PM

A few minutes before the Fed announcement…

UPDATE: 2:02 PM

UPDATE: 2:02 PM

Information received since the Federal Open Market Committee met in July indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports have weakened. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-3/4 to 2 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair, John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were James Bullard, who preferred at this meeting to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent; and Esther L. George and Eric S. Rosengren, who preferred to maintain the target range at 2 percent to 2-1/4 percent.

* * *

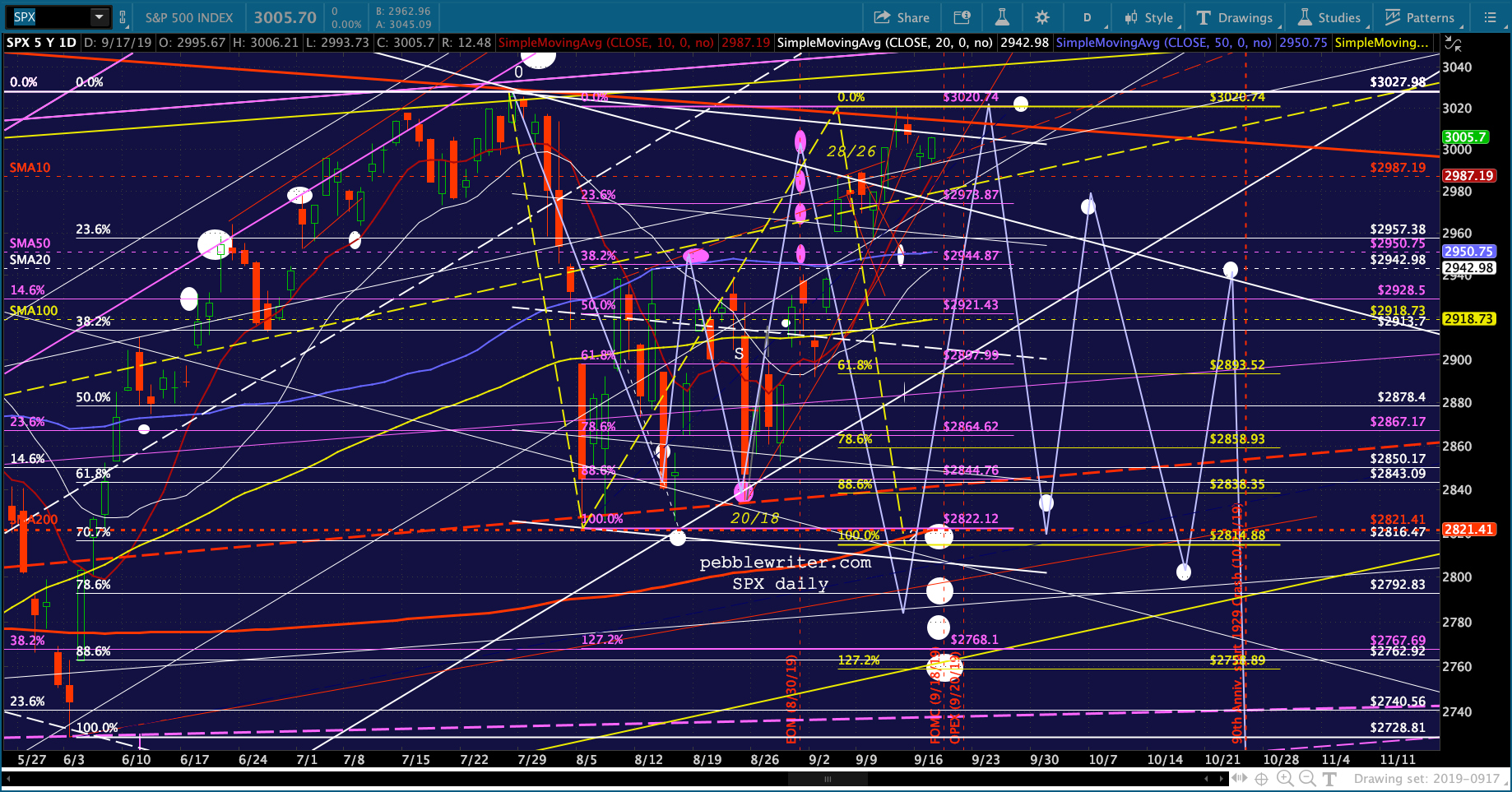

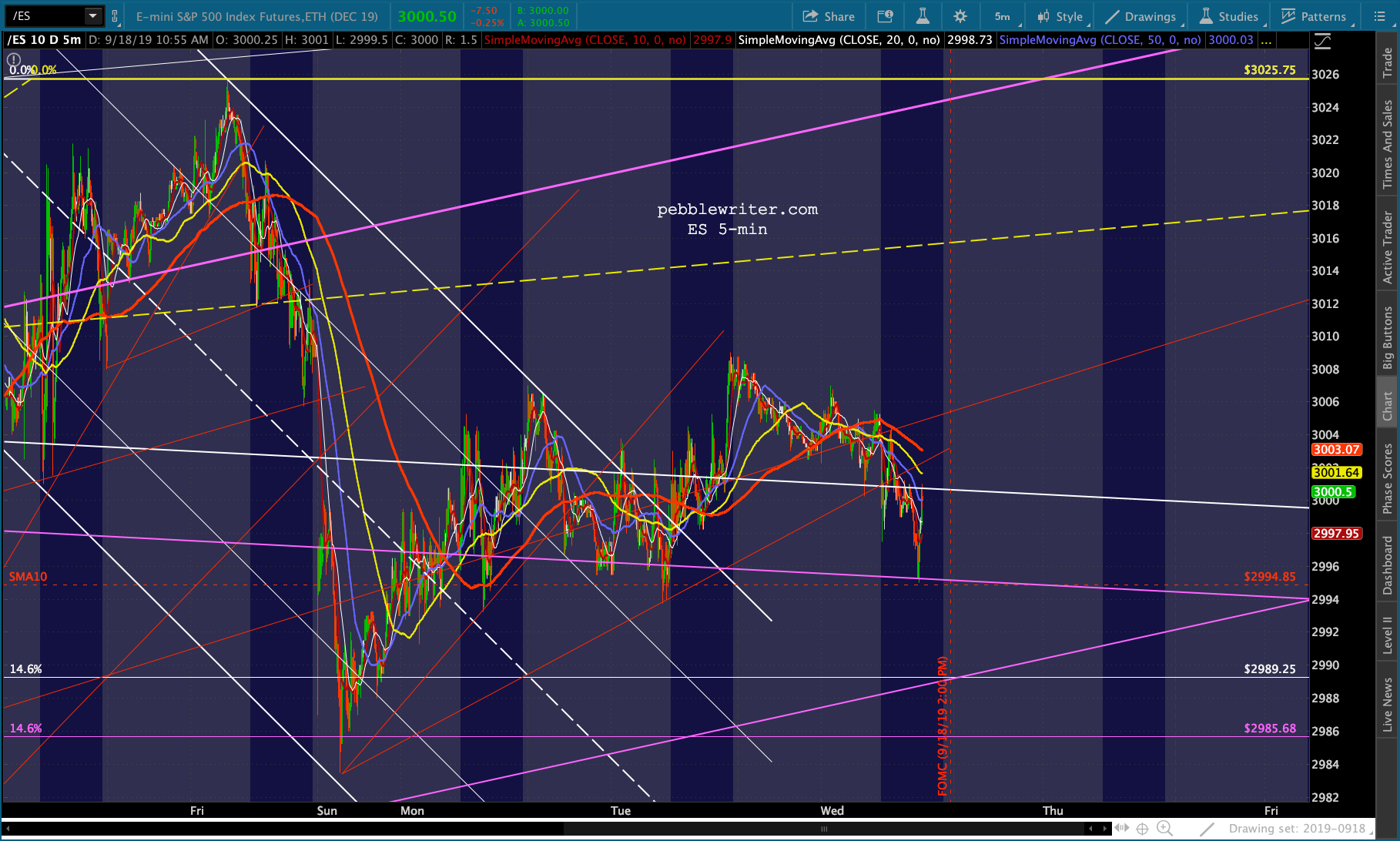

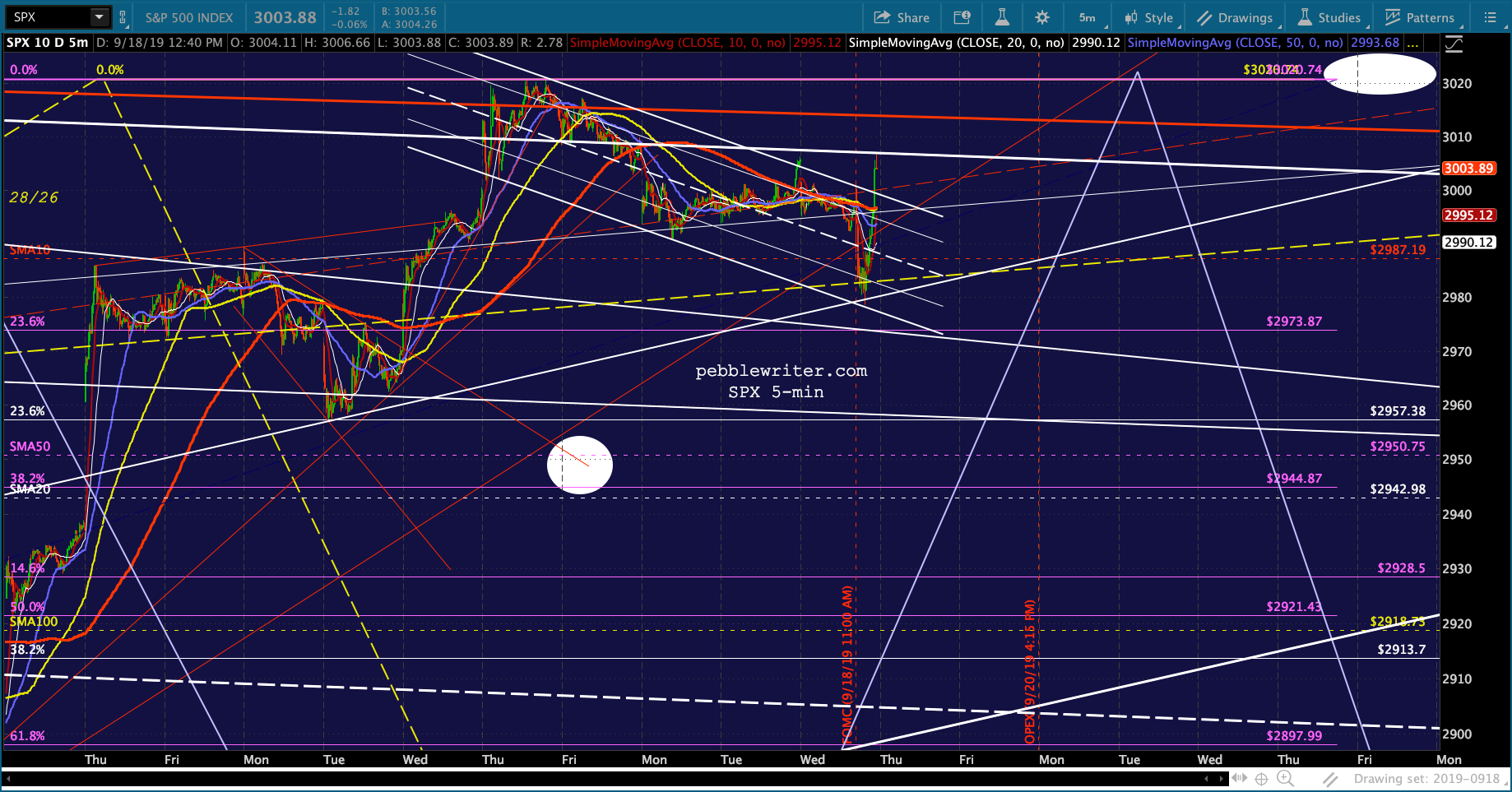

We’ve seen an initial drop which quickly reversed and is bouncing around without clear direction.

Keep an eye on ES’ SMA10 at 2994.85 and VIX’s SMA10 at 14.78.

Keep an eye on ES’ SMA10 at 2994.85 and VIX’s SMA10 at 14.78.

UPDATE: 3:35 PM

Just got a 28-pt bounce back to green thanks to VIX’s collapse and USDJPY’s continuing meltup. It ought to run out of steam right about here if it’s going to — which I still think it will.

SPX and ES are both bouncing like crazy for no particular reason.

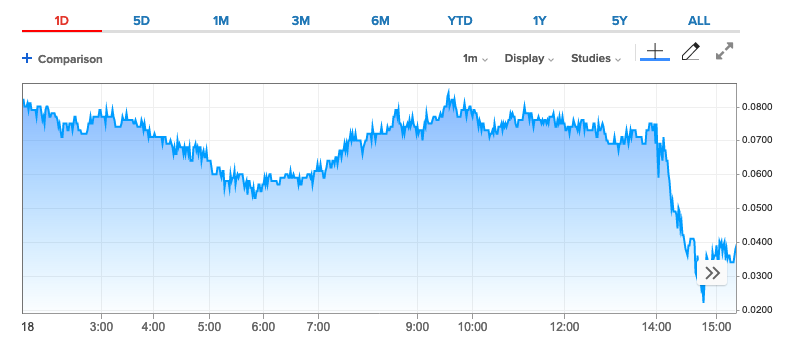

USDJPY is running scared…

USDJPY is running scared…

VIX just closed this morning’s gap.

VIX just closed this morning’s gap. Check out the move in the 2s10s…

Check out the move in the 2s10s…