Growing up in Texas, you saw a lot of these guys. They wore clean, polished boots, had the oversized belt buckle. Maybe even a genuine cowboy hat. But, they hauled paddle boards in their duallies and wouldn’t know which end of a bull to milk (not recommended.)

Growing up in Texas, you saw a lot of these guys. They wore clean, polished boots, had the oversized belt buckle. Maybe even a genuine cowboy hat. But, they hauled paddle boards in their duallies and wouldn’t know which end of a bull to milk (not recommended.)

Likewise, Monday’s action had all the appearances of a sharp sell-off, but wound up being a cheap, drugstore imitation. Thank the algos, as usual, for turning a potential rout into a mild-mannered slump — at least for now.

Aside from our analog, an alarming geopolitical outlook, and (don’t laugh) iffy fundamentals, the best argument the bears have going for them is still the technical picture. SPX’s RSI channel makes a great argument for a downturn… …though the BoJ clearly has other plans — making new cycle highs and threatening to break out of the falling channel dating back to February. Really, Shinzo? You want four more years of this 屎?

…though the BoJ clearly has other plans — making new cycle highs and threatening to break out of the falling channel dating back to February. Really, Shinzo? You want four more years of this 屎?

Calling an end to the bounce on Friday made me very uneasy — much more so than calling the top in late July. Days like yesterday, where stocks essentially ignored everything the bears could throw at them, make for sleepless nights.

Calling an end to the bounce on Friday made me very uneasy — much more so than calling the top in late July. Days like yesterday, where stocks essentially ignored everything the bears could throw at them, make for sleepless nights.

continued for members…

I’m writing this Monday night as I expect to be on the road until after the open tomorrow.

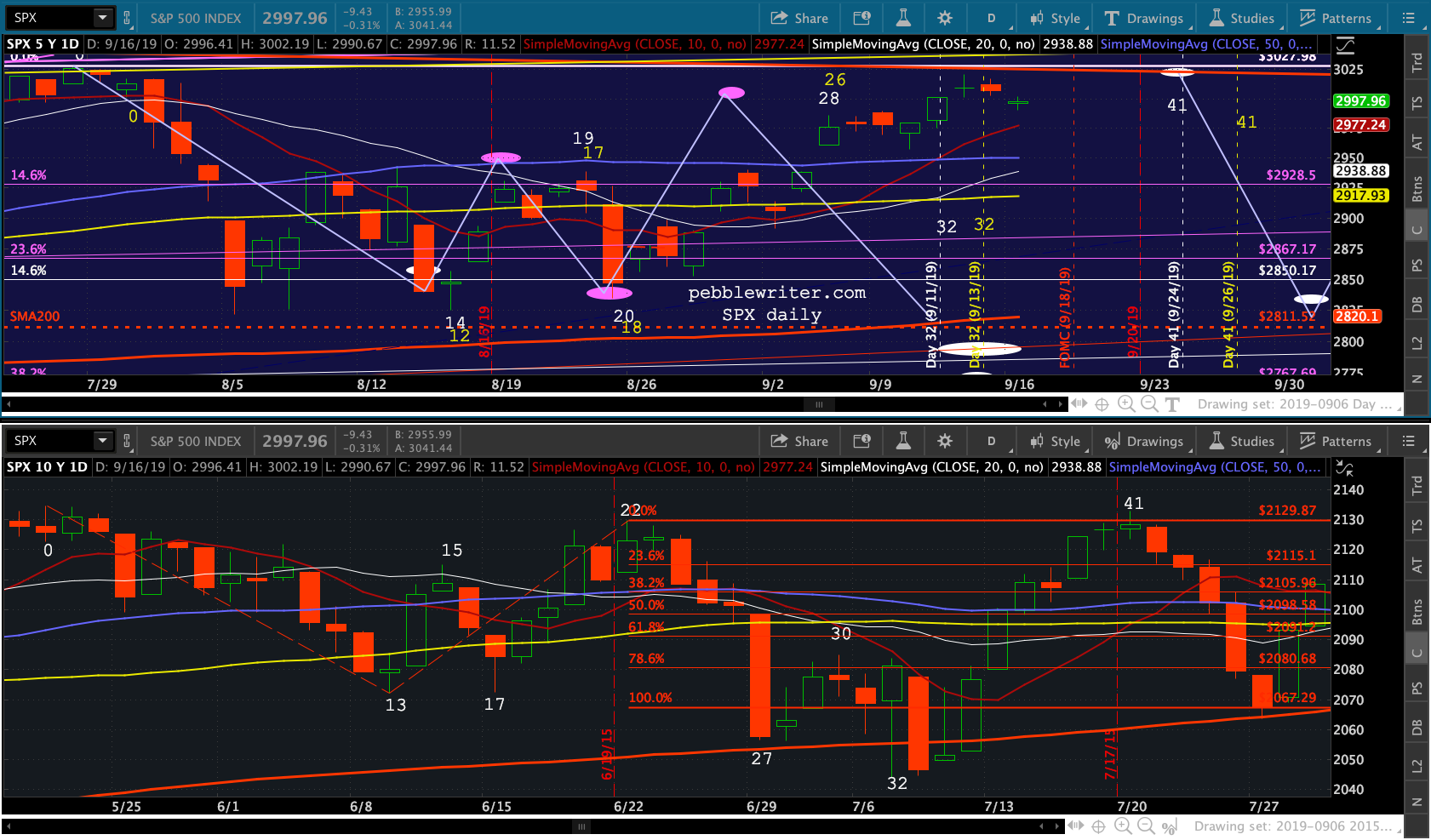

All in all, today was a pretty disappointing day for the bears. Our analog isn’t necessarily dead,but it’s a little green around the gills. The usual factors kept stocks from dropping any more than they did — a measly 0.31%. The big picture hasn’t changed; and, tomorrow’s another day. But, I won’t be shocked if the decline (if it happens) waits until after the FOMC decision.

I still like the idea of a sharp shock designed to impress the FOMC with the need for more easing before their decision on Wednesday. But, that doesn’t leave much time. And, the analog is already at least one day behind schedule is we fudge the dates a little (use Day 33 as the target low and start the count on Jul 30.)

SPX’s SMA200 is now up to 2820.10, still a little shy of the Aug 5 low of 2822.12. Remember, the analog says we’ll get a lower low — so it’s now or never if it’s going to hold in that respect.

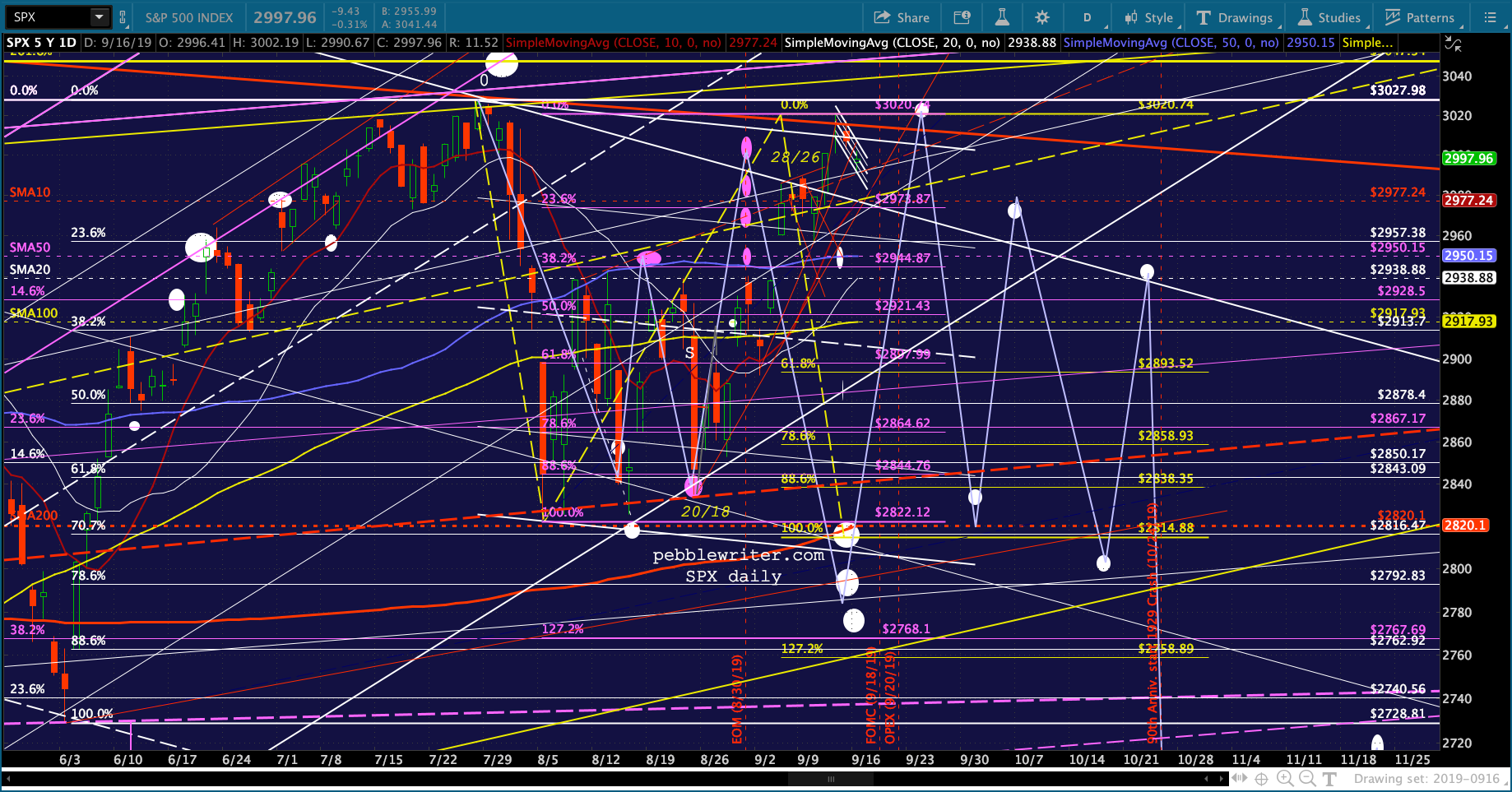

SPX’s SMA200 is now up to 2820.10, still a little shy of the Aug 5 low of 2822.12. Remember, the analog says we’ll get a lower low — so it’s now or never if it’s going to hold in that respect. Obviously, the shallow falling white channel still needs to fall apart.

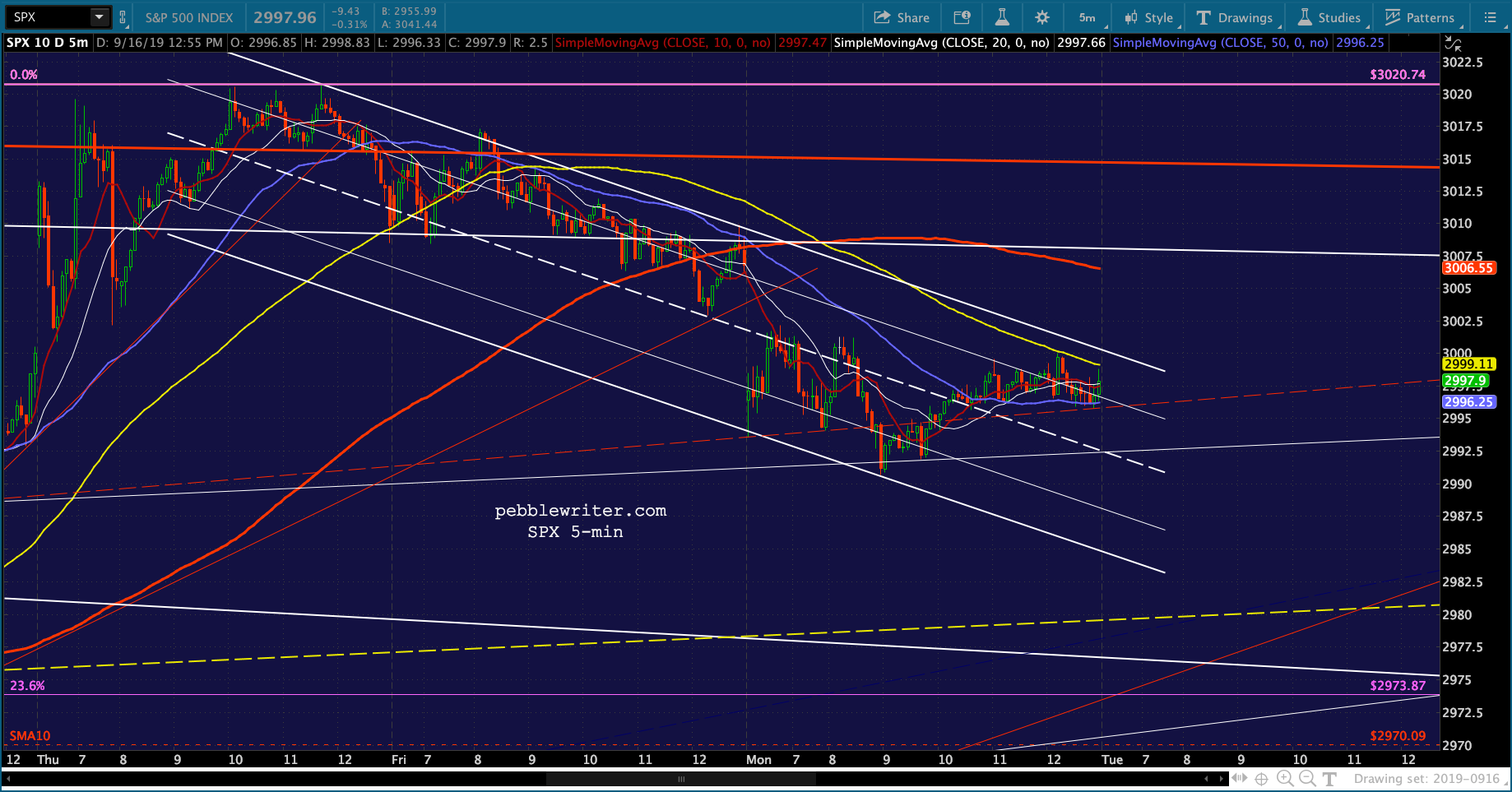

Obviously, the shallow falling white channel still needs to fall apart.  Ditto for ES.

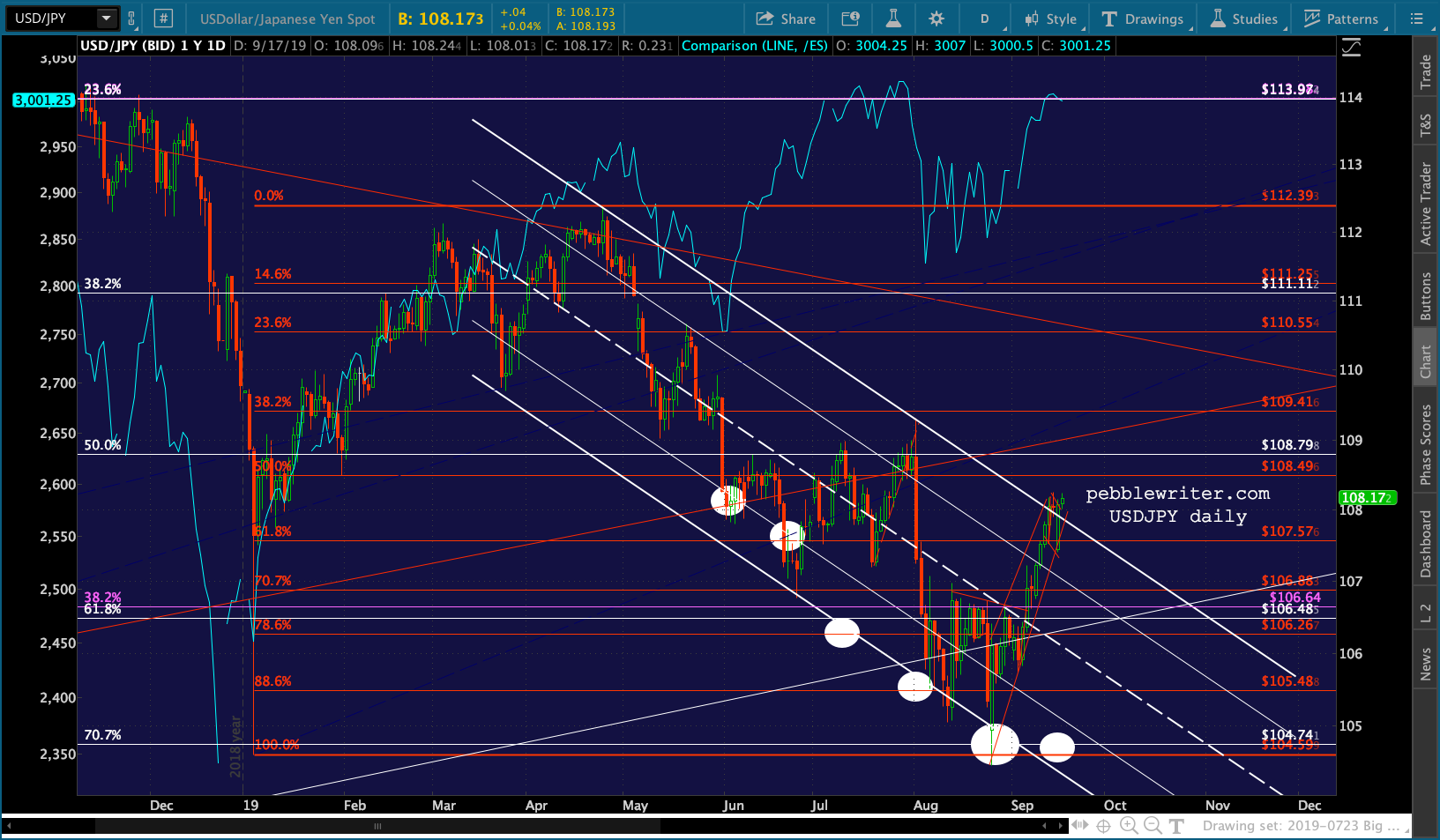

Ditto for ES. There is slight evidence that such an event might be in the works. USDJPY has yet to really break out of its falling white channel.

There is slight evidence that such an event might be in the works. USDJPY has yet to really break out of its falling white channel.  Though it’s certainly threatening to do so. Of course, this is one of those chicken and egg things. If the downside can get going, the yen will strengthen and a falling USDJPY will trigger more selling in stocks, etc.

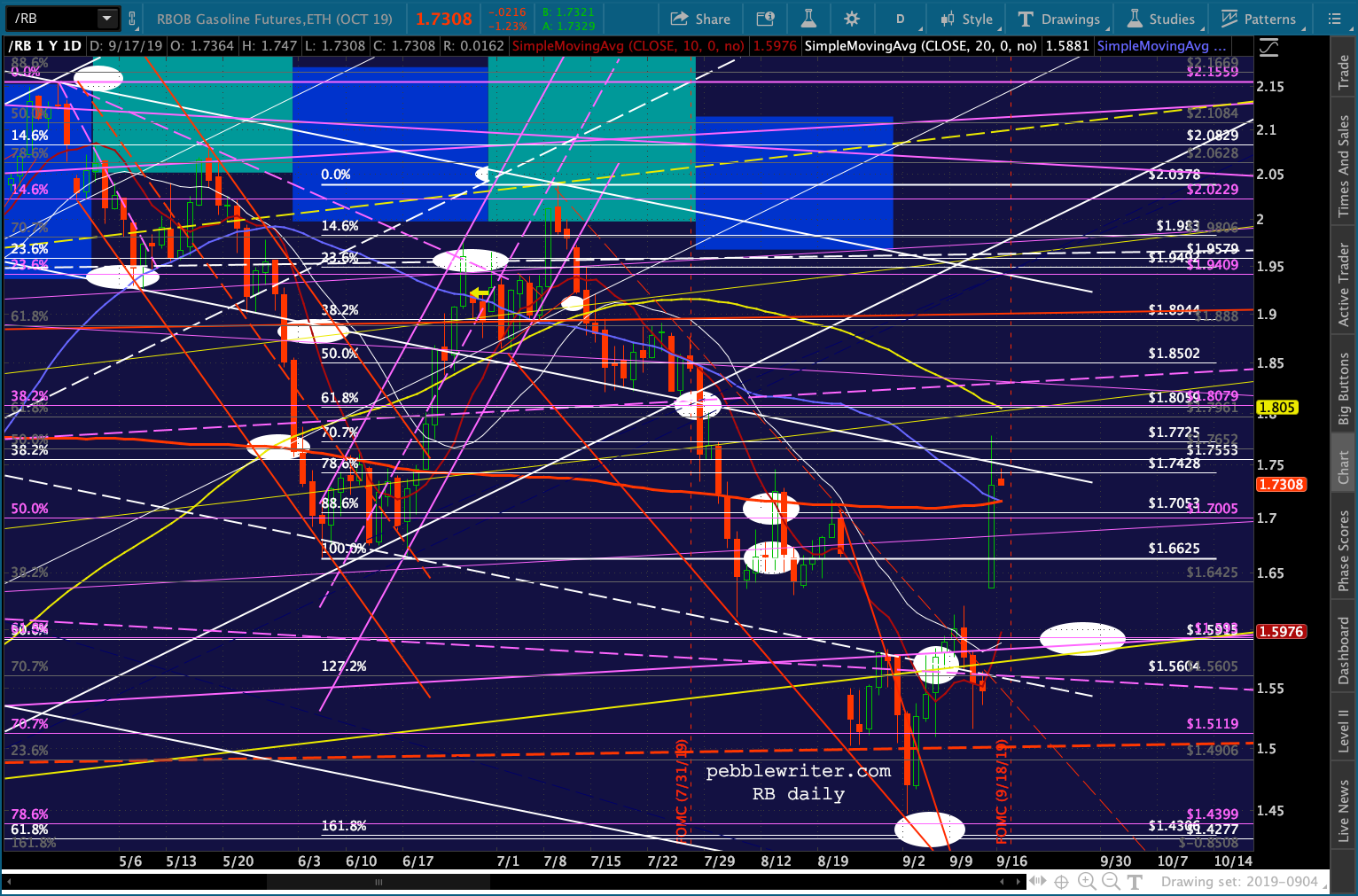

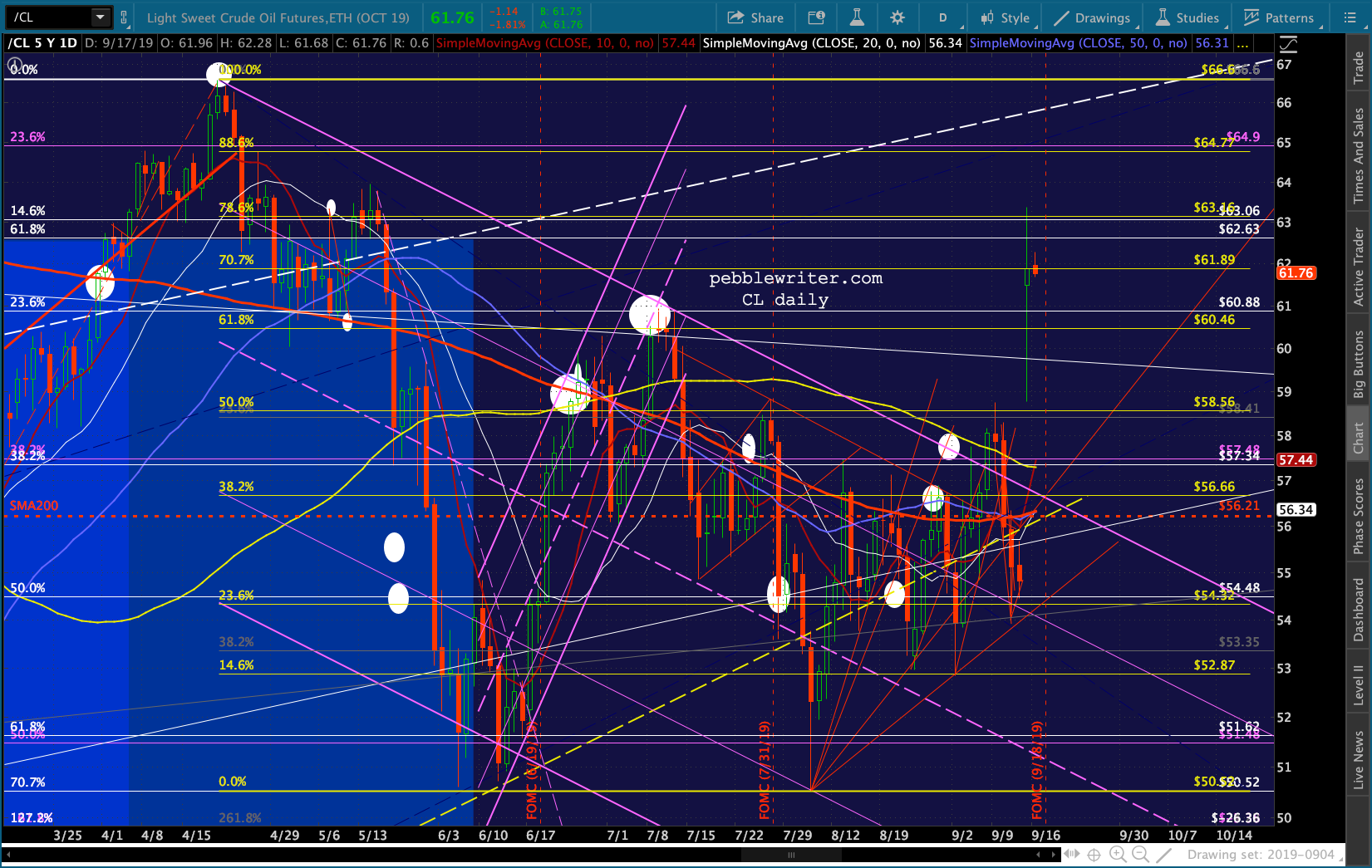

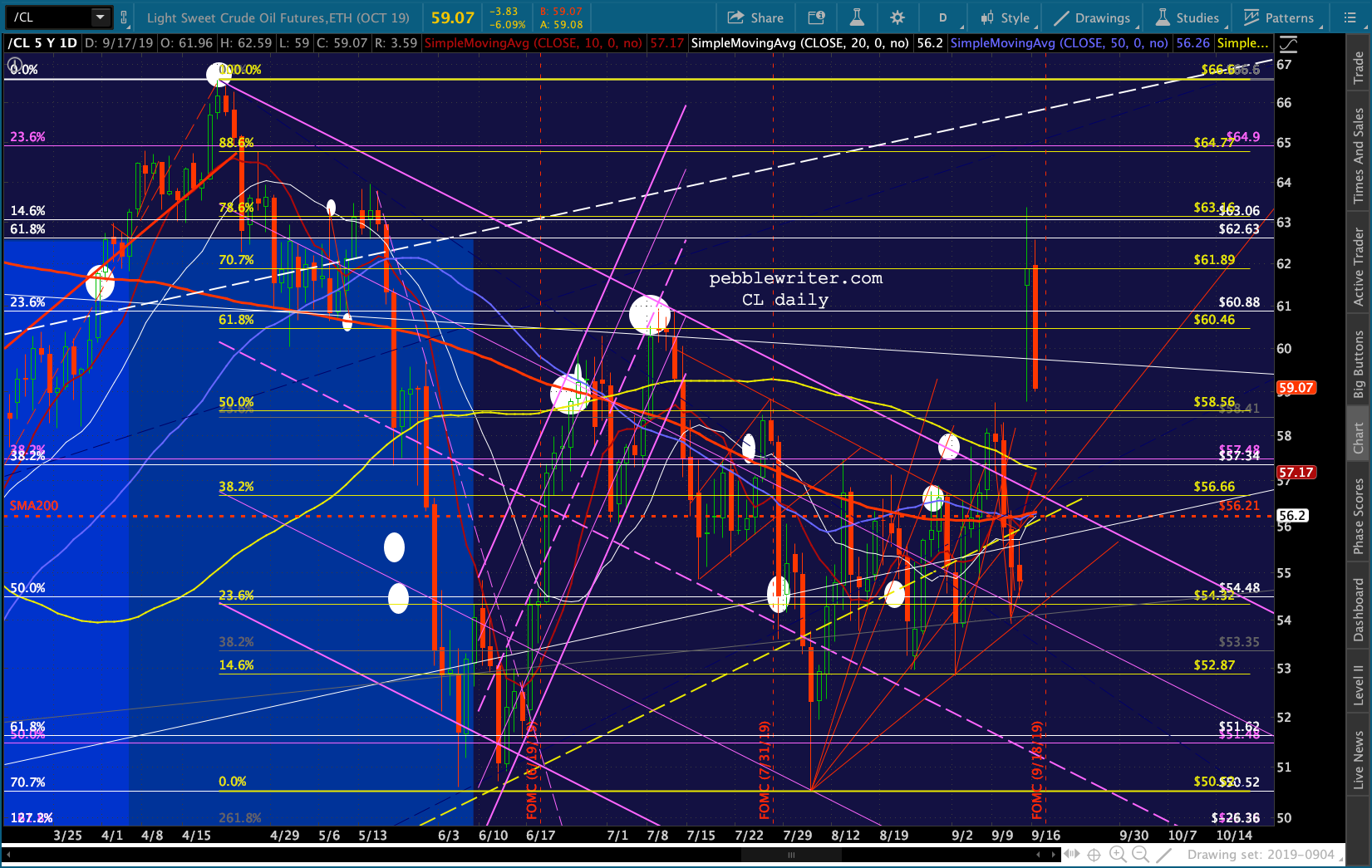

Though it’s certainly threatening to do so. Of course, this is one of those chicken and egg things. If the downside can get going, the yen will strengthen and a falling USDJPY will trigger more selling in stocks, etc. As to CL and RB, they’ve made no further progress than earlier today. That doesn’t mean they won’t, just that they seem to have met at least some resistance — whether real or manufactured. I’d fade both right here with tight stops.

As to CL and RB, they’ve made no further progress than earlier today. That doesn’t mean they won’t, just that they seem to have met at least some resistance — whether real or manufactured. I’d fade both right here with tight stops.

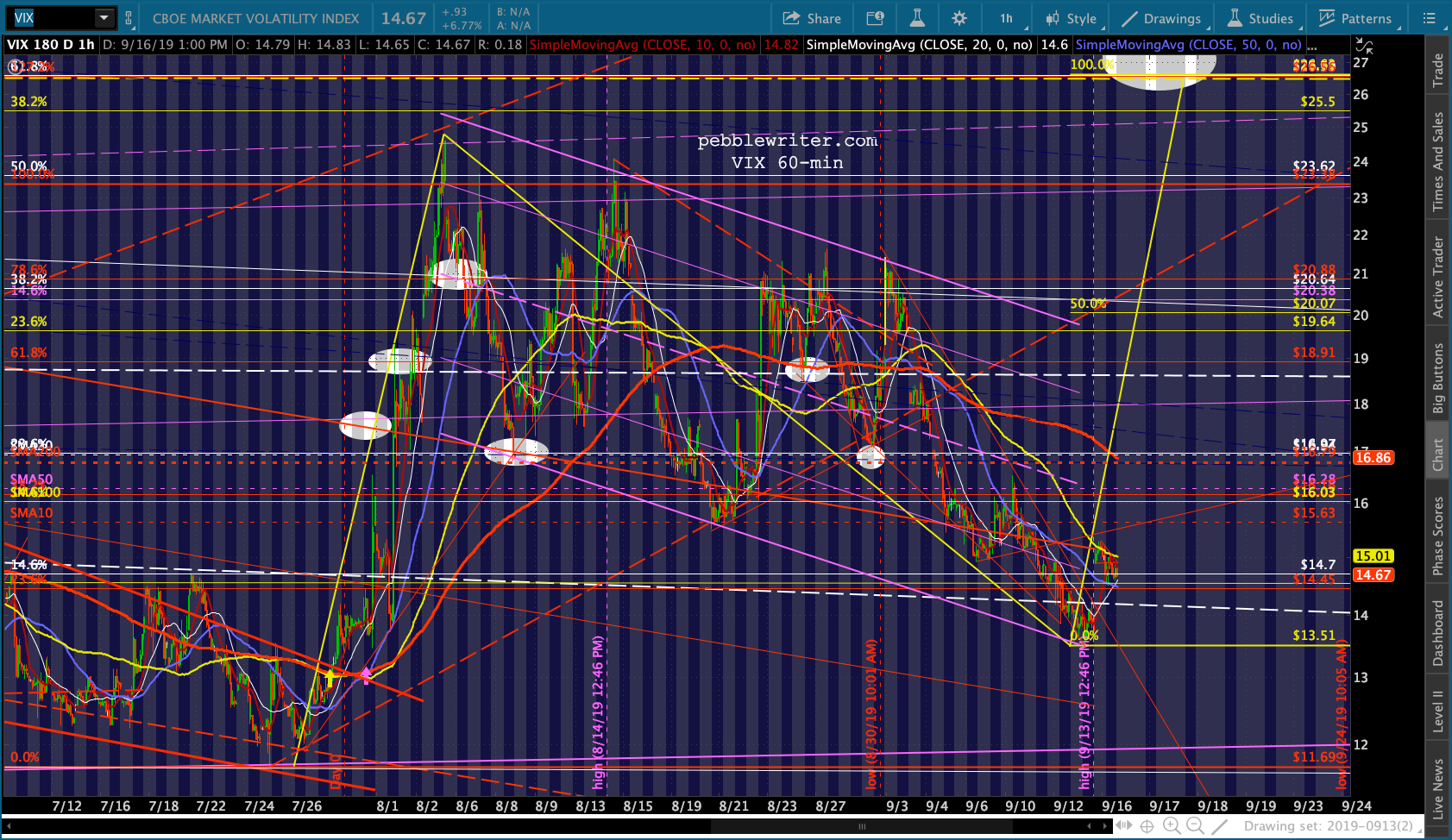

And, for all its machinations, VIX held its own today — closing above its SMA5 200. It’s not much, but it’s something.

And, for all its machinations, VIX held its own today — closing above its SMA5 200. It’s not much, but it’s something.

I hope to be online around 9:45am Tuesday. In the meantime, keep an eye on USDJPY. With VIX offline for the next few hours and CL working against instead of for the bulls as usual, the yen is the factor in charge of the whole shebang.

I hope to be online around 9:45am Tuesday. In the meantime, keep an eye on USDJPY. With VIX offline for the next few hours and CL working against instead of for the bulls as usual, the yen is the factor in charge of the whole shebang.

GLTA.

UPDATE: 10:25 AM

More of the same…algos fully in charge.

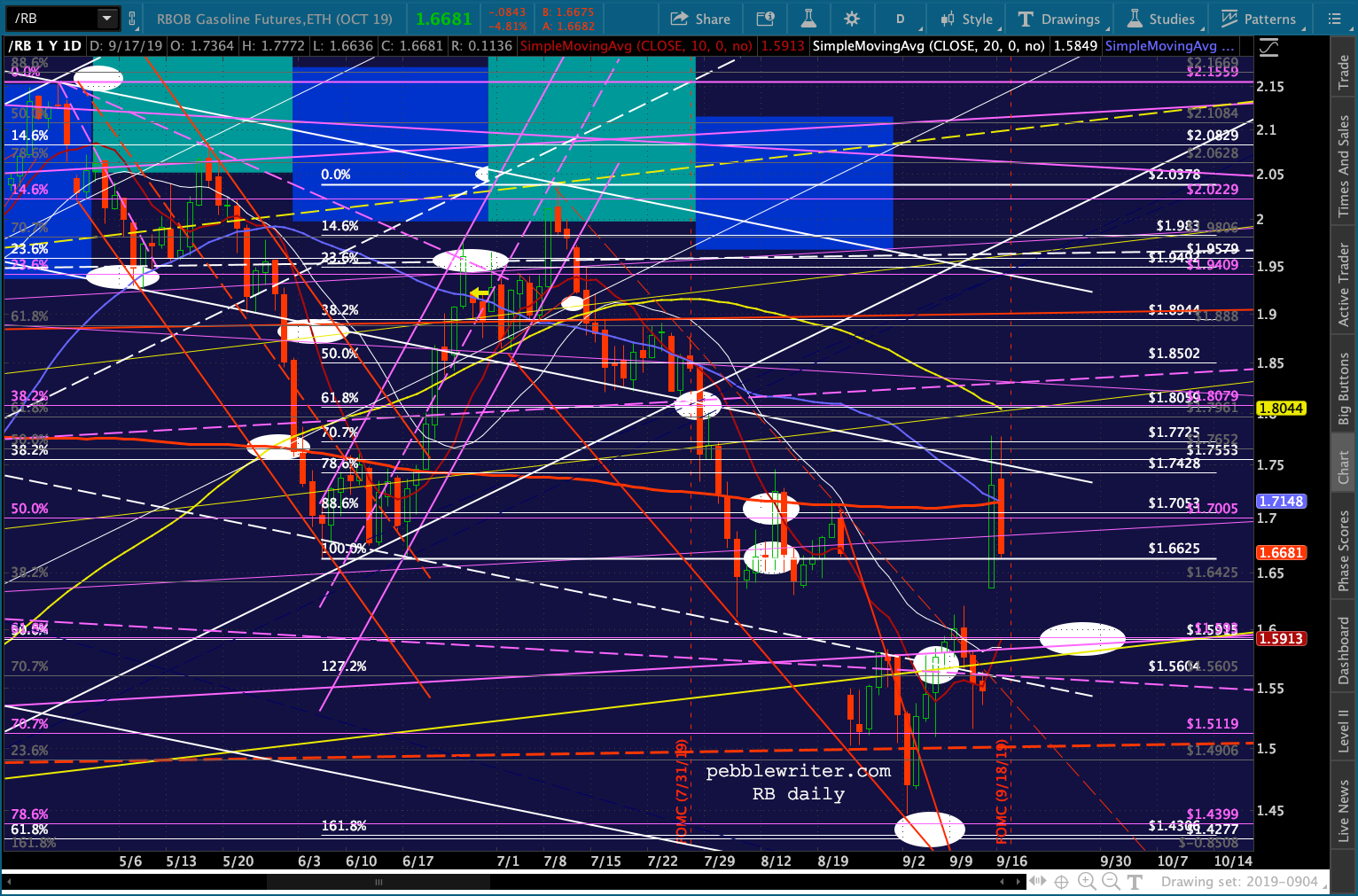

But, check out RB and CL – giving up most of yesterday’s gains.

But, check out RB and CL – giving up most of yesterday’s gains.

UPDATE: 3:35 PM

UPDATE: 3:35 PM

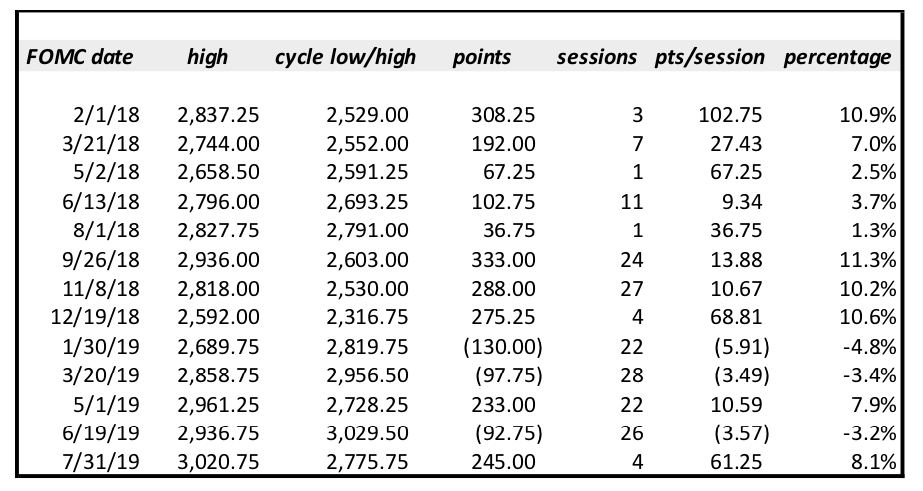

With essentially everybody expecting a 25 bps rate cut tomorrow, let’s turn our attention to the past year. Whether or not the Fed cuts the discount rate, might they disappoint investors? The charts suggest they will. I looked at the 2018-2019 of FOMC meetings to address the question “should I short into the rate decision?”

I looked at the 2018-2019 of FOMC meetings to address the question “should I short into the rate decision?”

The short answer: yes.

All but three meetings produced a cycle decline, with the average being -4.8%. Toss out the three gainers, and the average decline was 7.4%, with 8 of the 11 being over 100 points for an average of 8.7% and 4 of those 8 declining at least 10%.

For these purposes, I’m defining a cycle decline as a subsequent daily low which is lower than the high seen on the day of the meeting. Such decline could take place any day between then and the next FOMC meeting. Cycle highs work the same way: any higher high between the two meetings.

In almost every instance, shorting at the high on the day of the FOMC meeting would have been profitable for at least the first 24 hours. The only exceptions were 1/30/19, 3/20/19 and 6/20/19.

The losses during in the first 24 hours of those shorts would have been very minor — meaning stops would have easily contained the damage. The ultimate cycle highs took an average of 25 sessions. In other words, they were meltups.

The shorts, on the other hand, tended to occur relatively quickly, averaging 10 sessions. Given that almost everybody expects the same decision — a 25bps cut — the potential for a disappointment seems higher than usual. If our analog is still alive, it certainly argues for a rapid, severe drop.

GLTA.