Aside from the wild swings in USDJPY, 2019 has been fairly quiet for the currency pairs we follow. We’ll look at the moves to date, the reasons behind them, and what to expect going forward. Stocks’ performance today will likely depend on whether BA can remain above its 200-day moving average. Fundamentals, dontcha know…

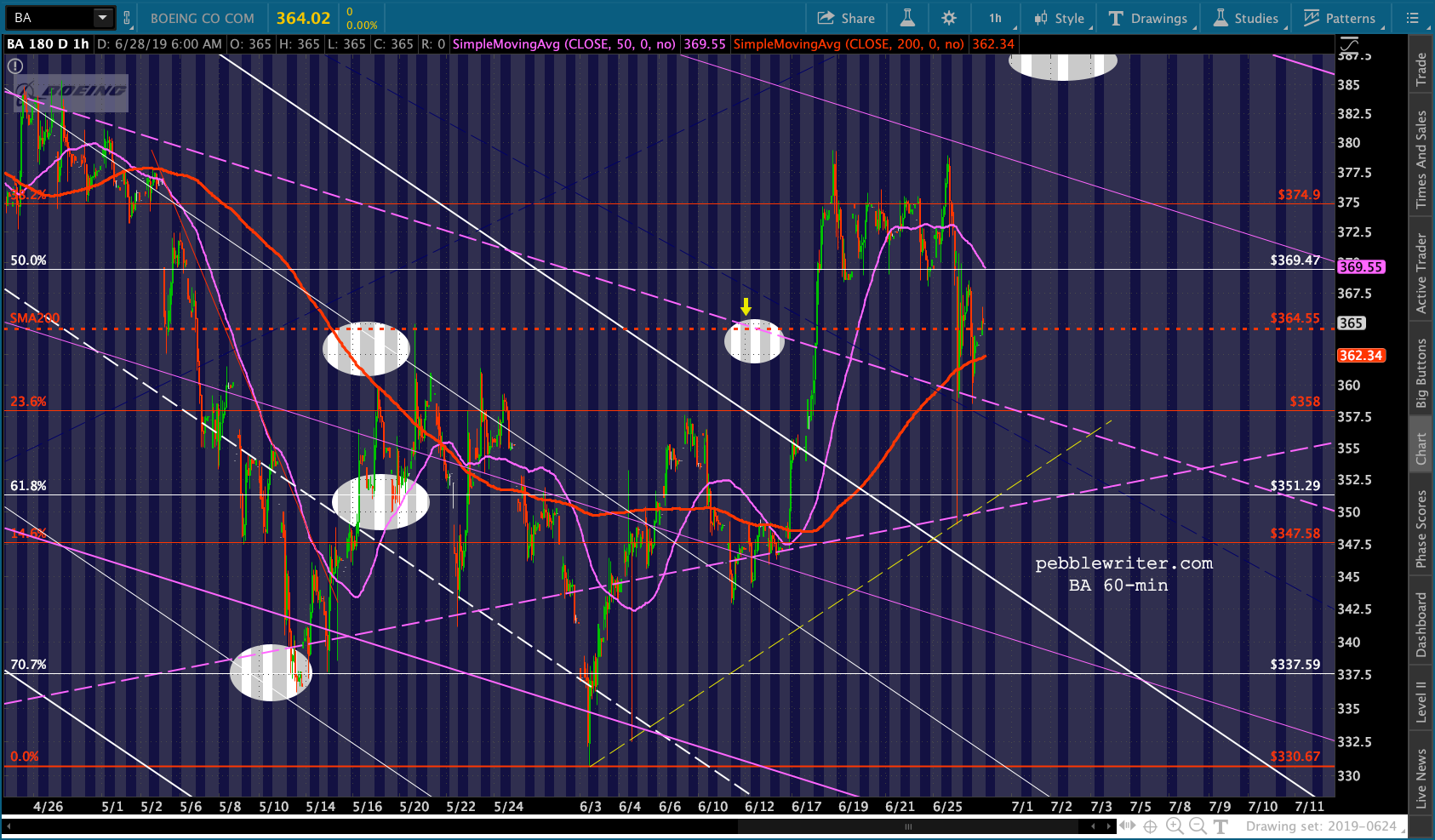

Stocks’ performance today will likely depend on whether BA can remain above its 200-day moving average. Fundamentals, dontcha know…

continued for members…

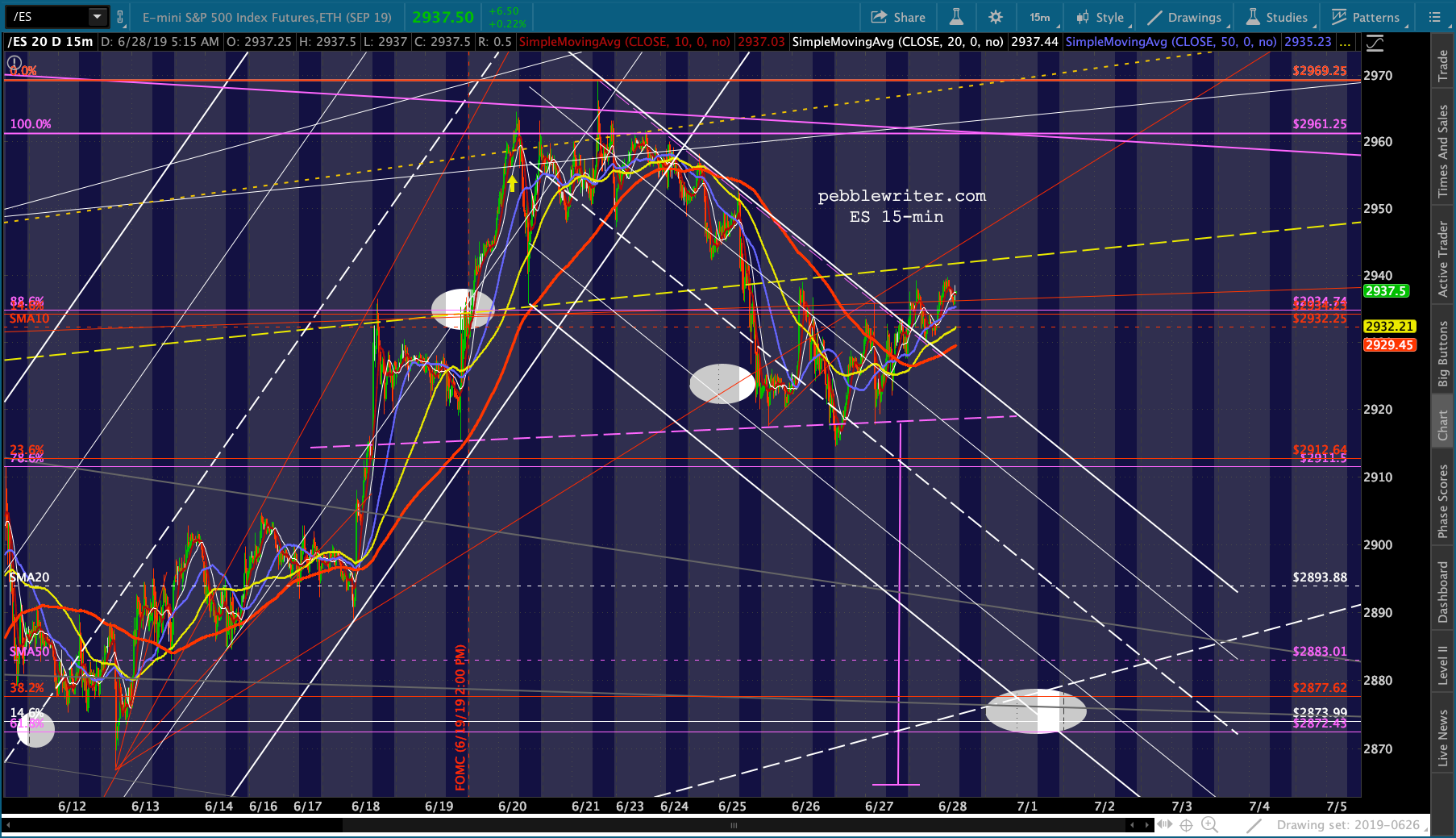

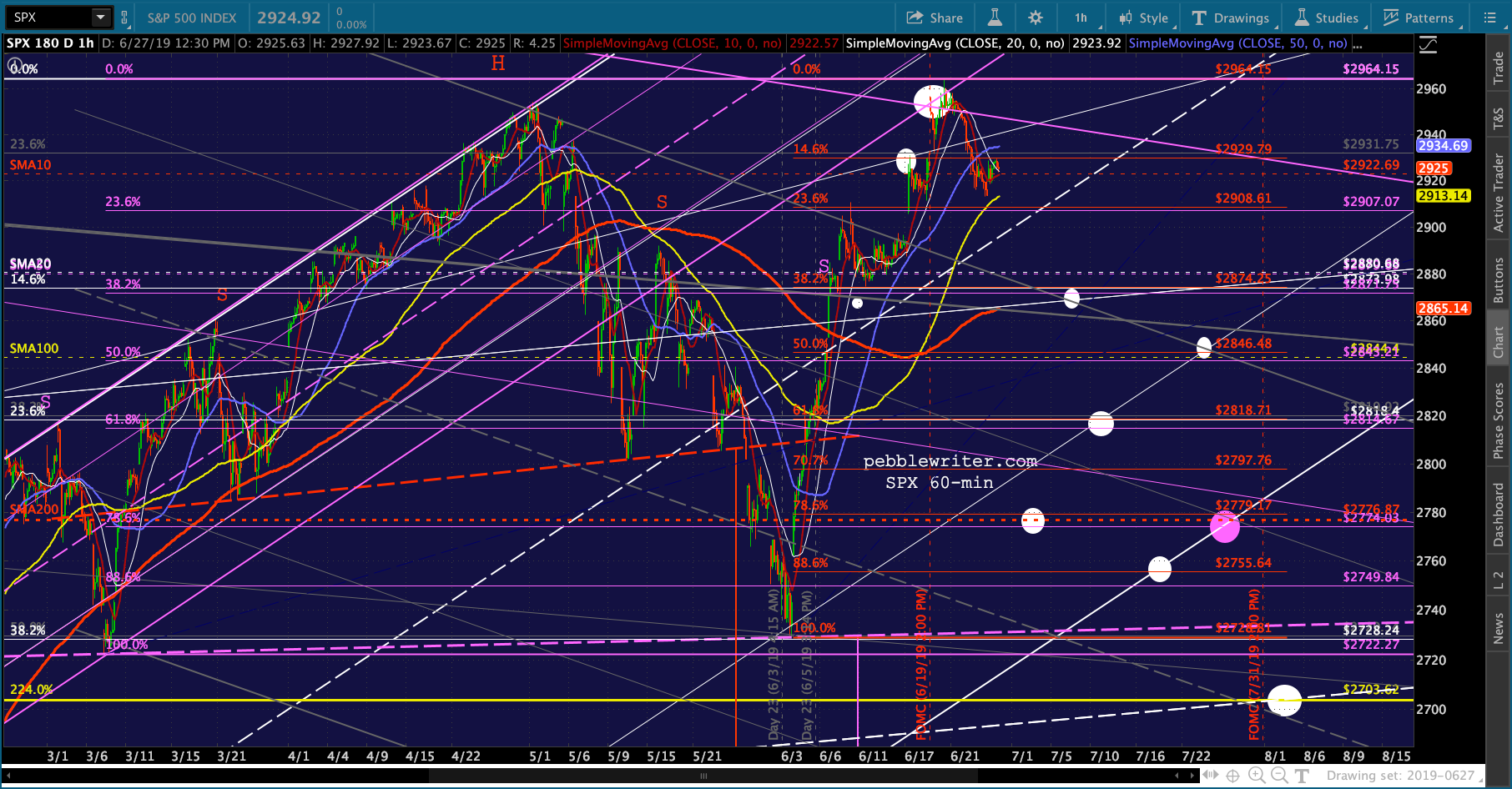

First, a quick look at market conditions this morning. Futures are up 7 points after breaking out of the little falling channel from Jun 20 — this after the small H&S Pattern was (at least) postponed. No surprise that the breakout was driven by VIX’s breakdown…

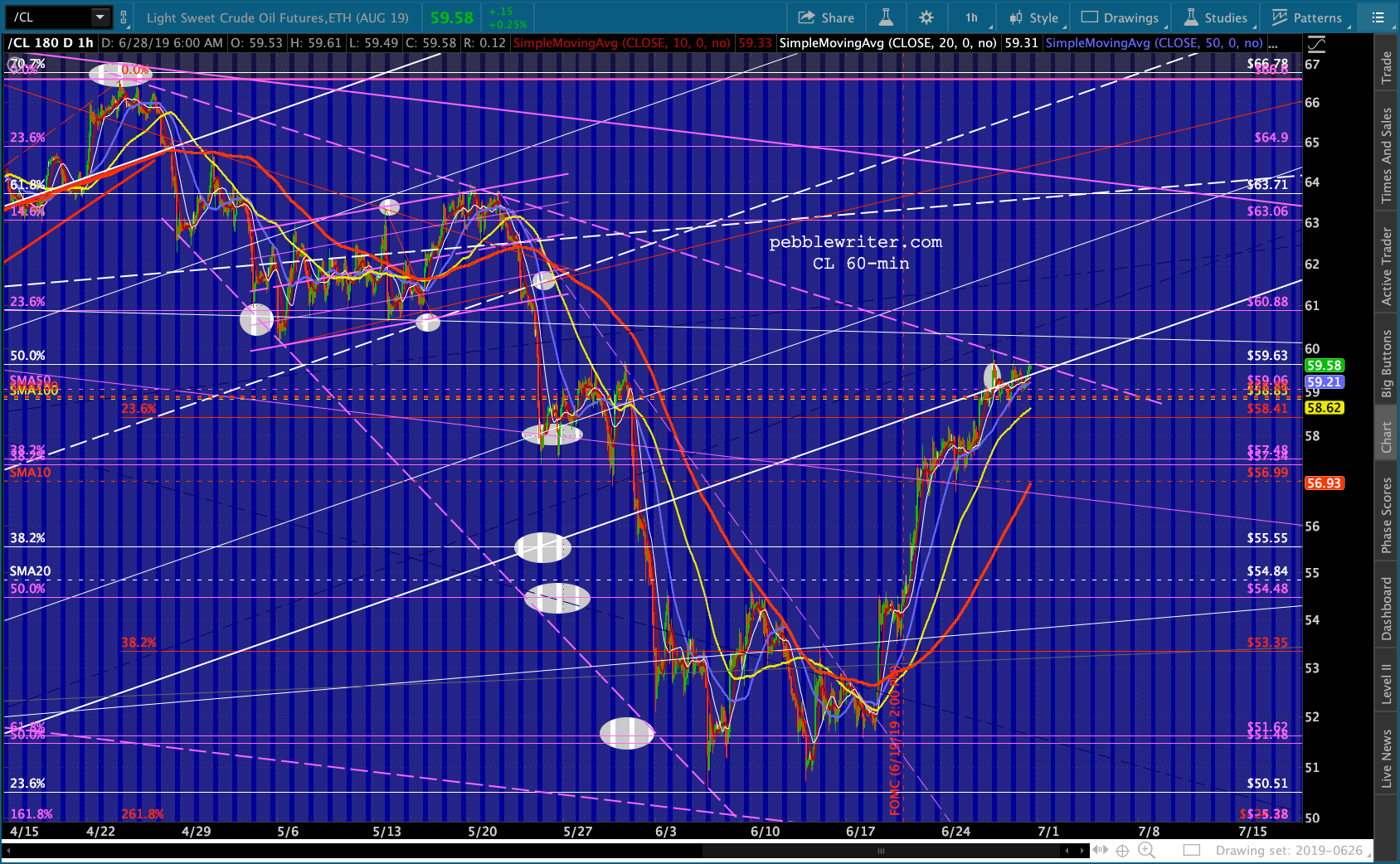

No surprise that the breakout was driven by VIX’s breakdown… …and CL’s continuing threat to break out (it shouldn’t.)

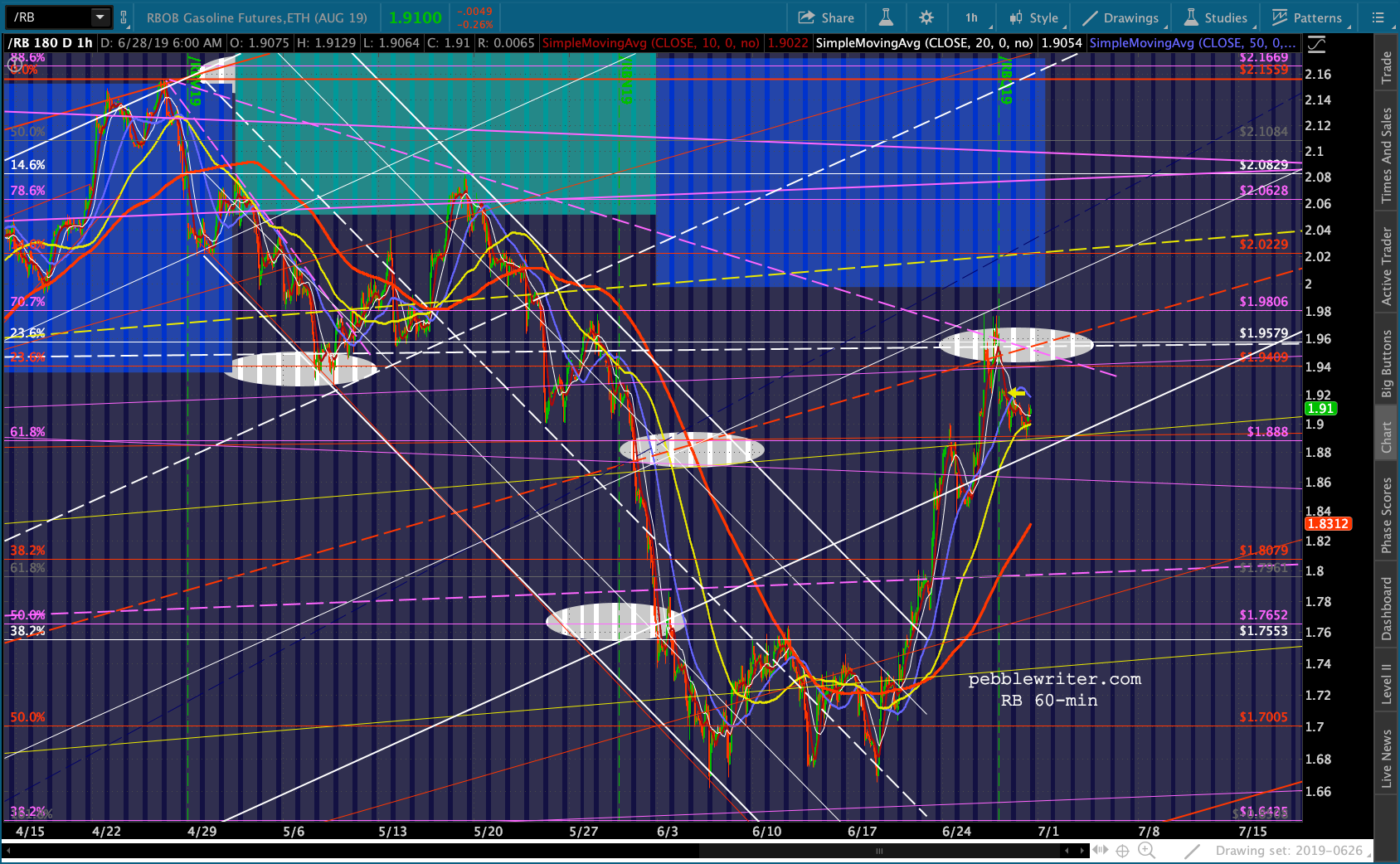

…and CL’s continuing threat to break out (it shouldn’t.) Ditto for RB.

Ditto for RB. This doesn’t change our outlook for SPX — unless of course we get one of those special tweets regarding the trade deal.

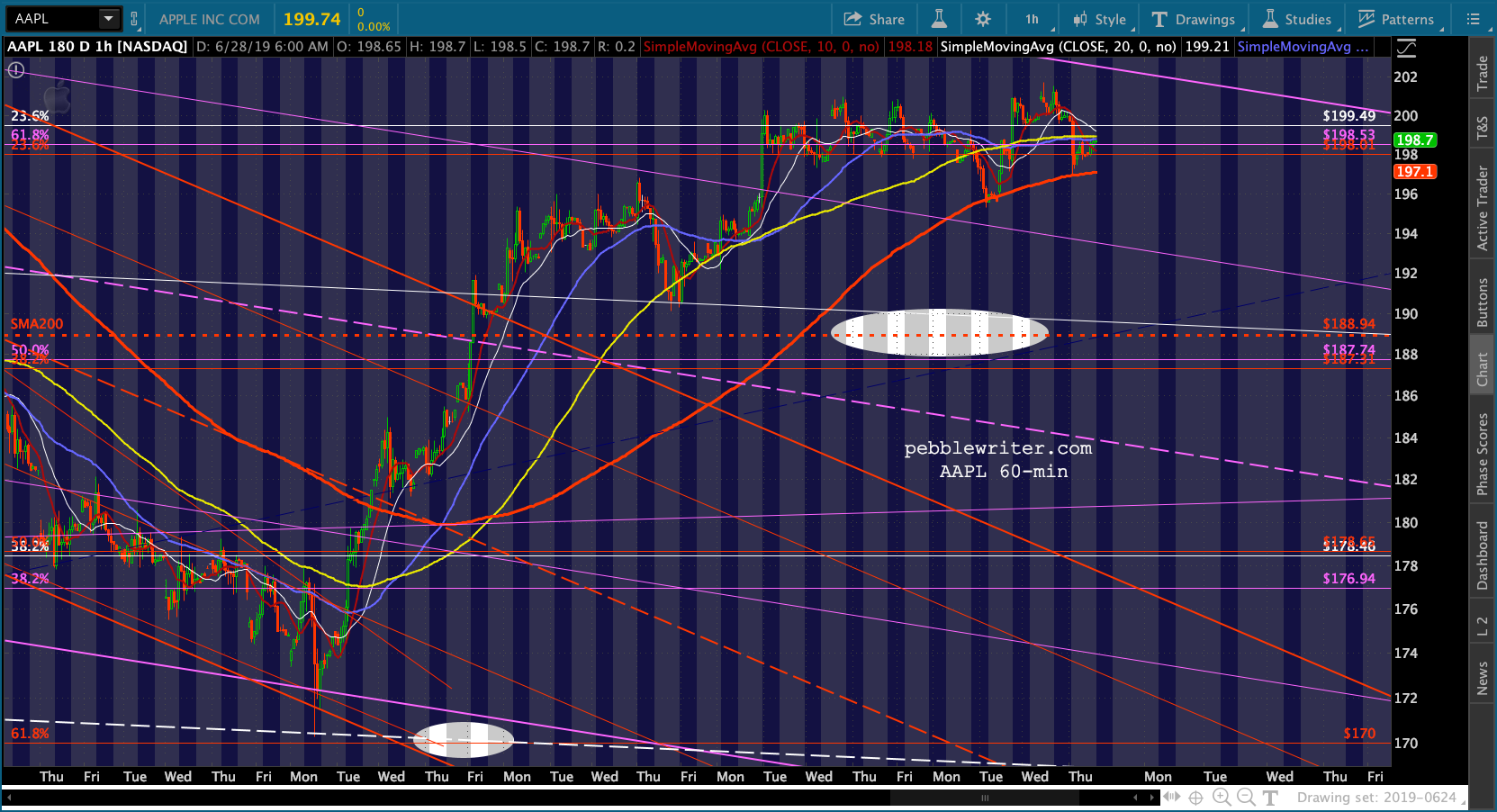

This doesn’t change our outlook for SPX — unless of course we get one of those special tweets regarding the trade deal. AAPL and BA are managing to avoid the worst…for now.

AAPL and BA are managing to avoid the worst…for now.

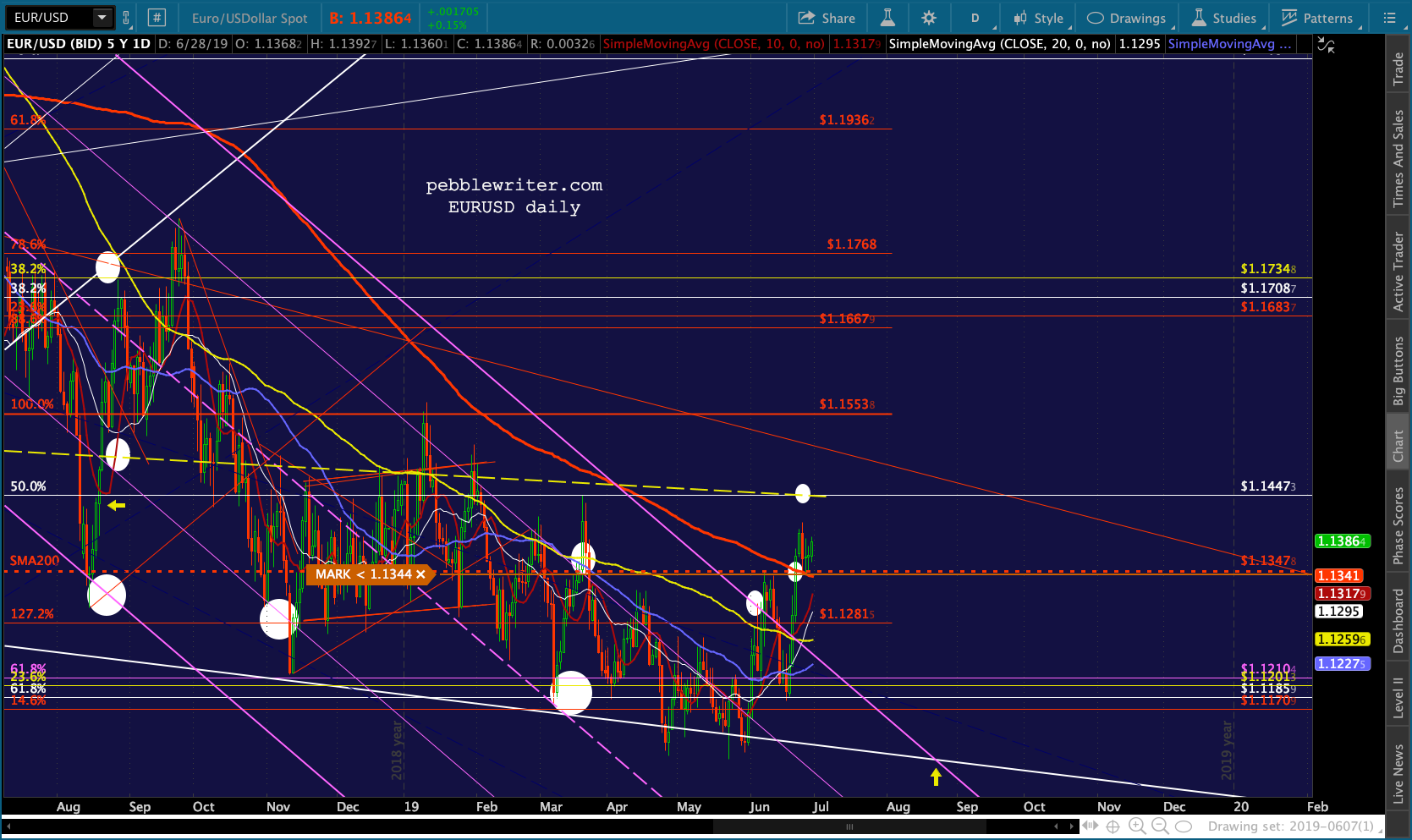

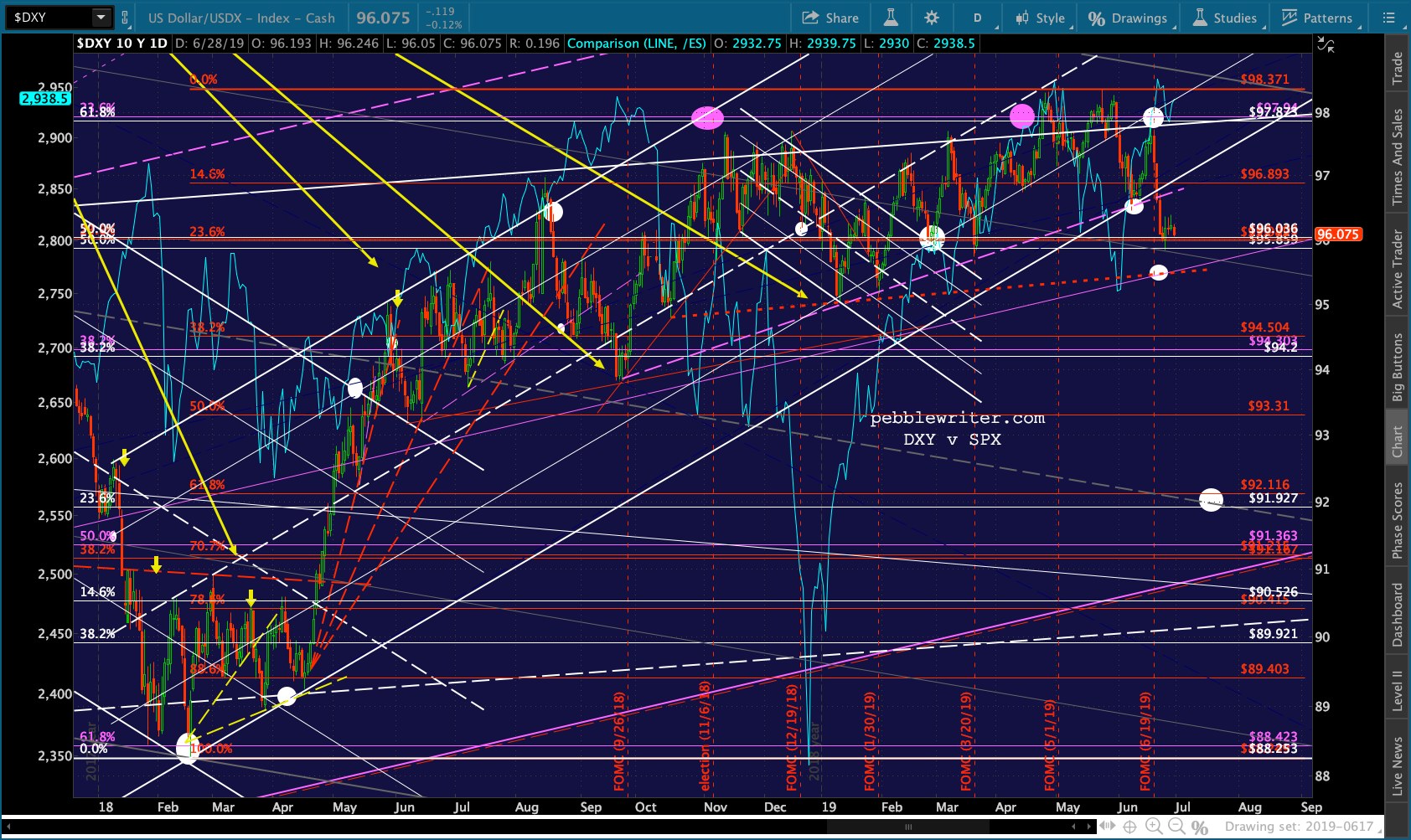

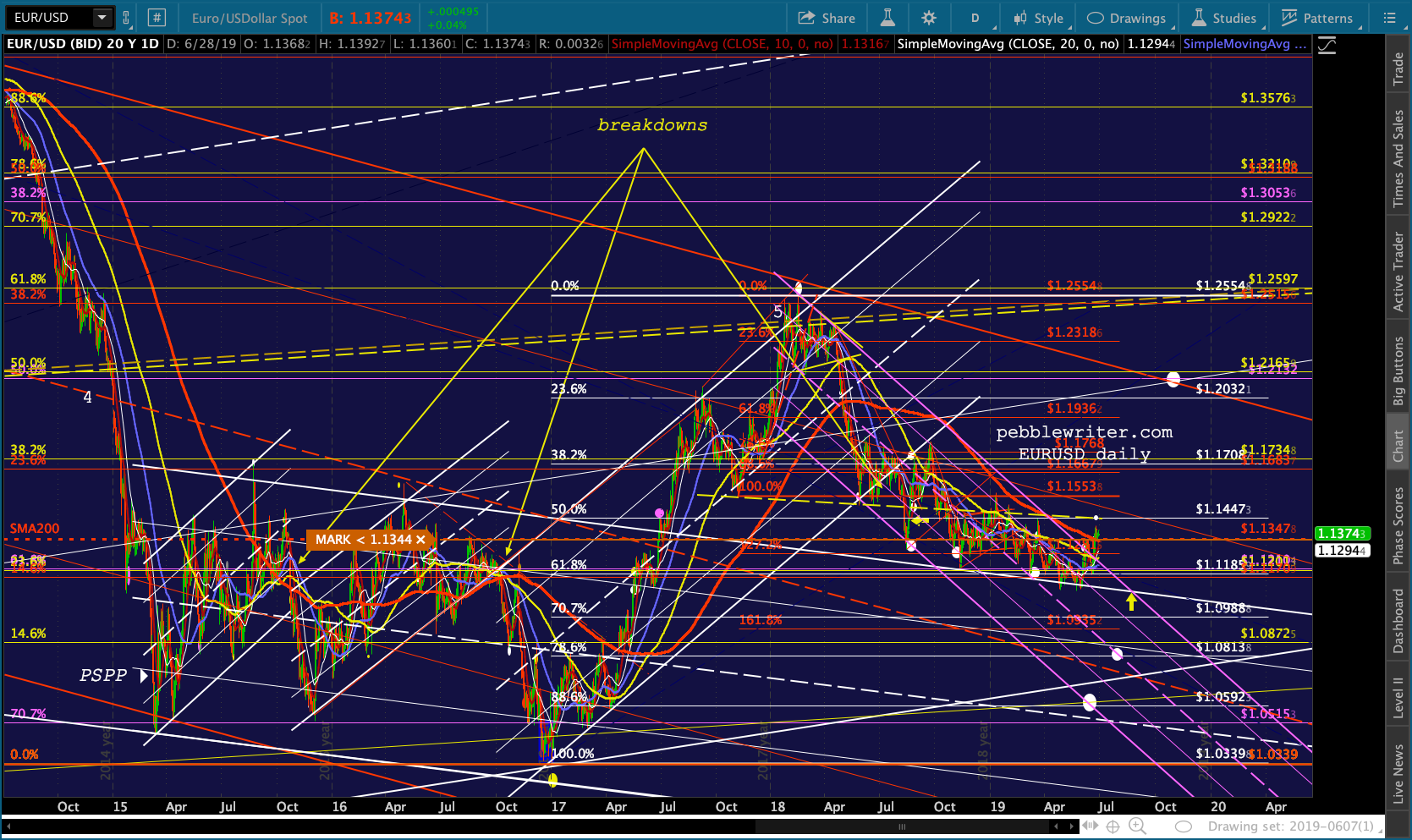

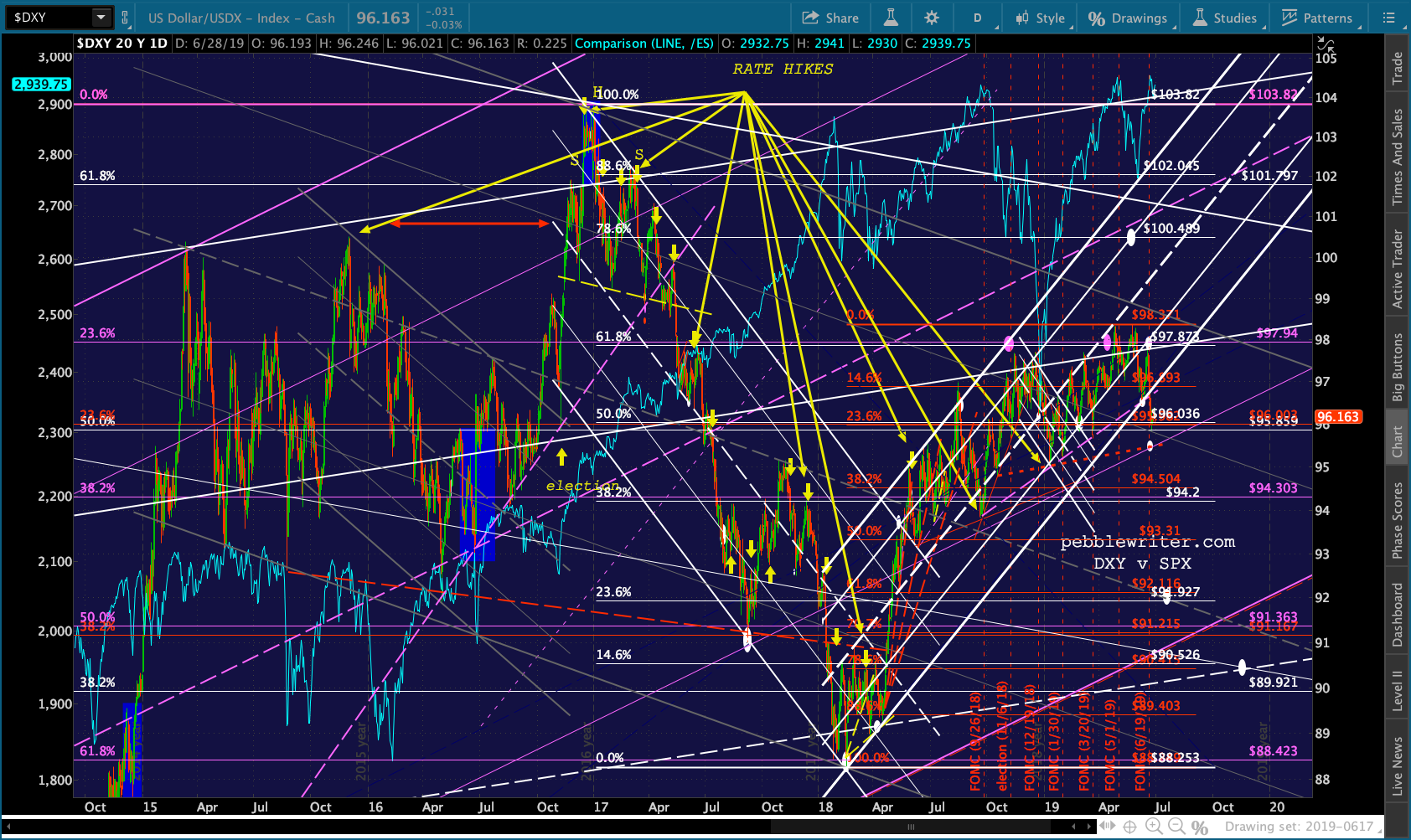

A quick glance at EURUSD and DXY shows the continuing logjam might be drawing to an end.

A quick glance at EURUSD and DXY shows the continuing logjam might be drawing to an end.

My general, big-picture outlook has been that currencies, like everything else, have been managed by central banks to serve the goal of driving equity prices higher. This has mandated low interest rates as our growing pile of debt would not otherwise be serviceable.

My general, big-picture outlook has been that currencies, like everything else, have been managed by central banks to serve the goal of driving equity prices higher. This has mandated low interest rates as our growing pile of debt would not otherwise be serviceable.

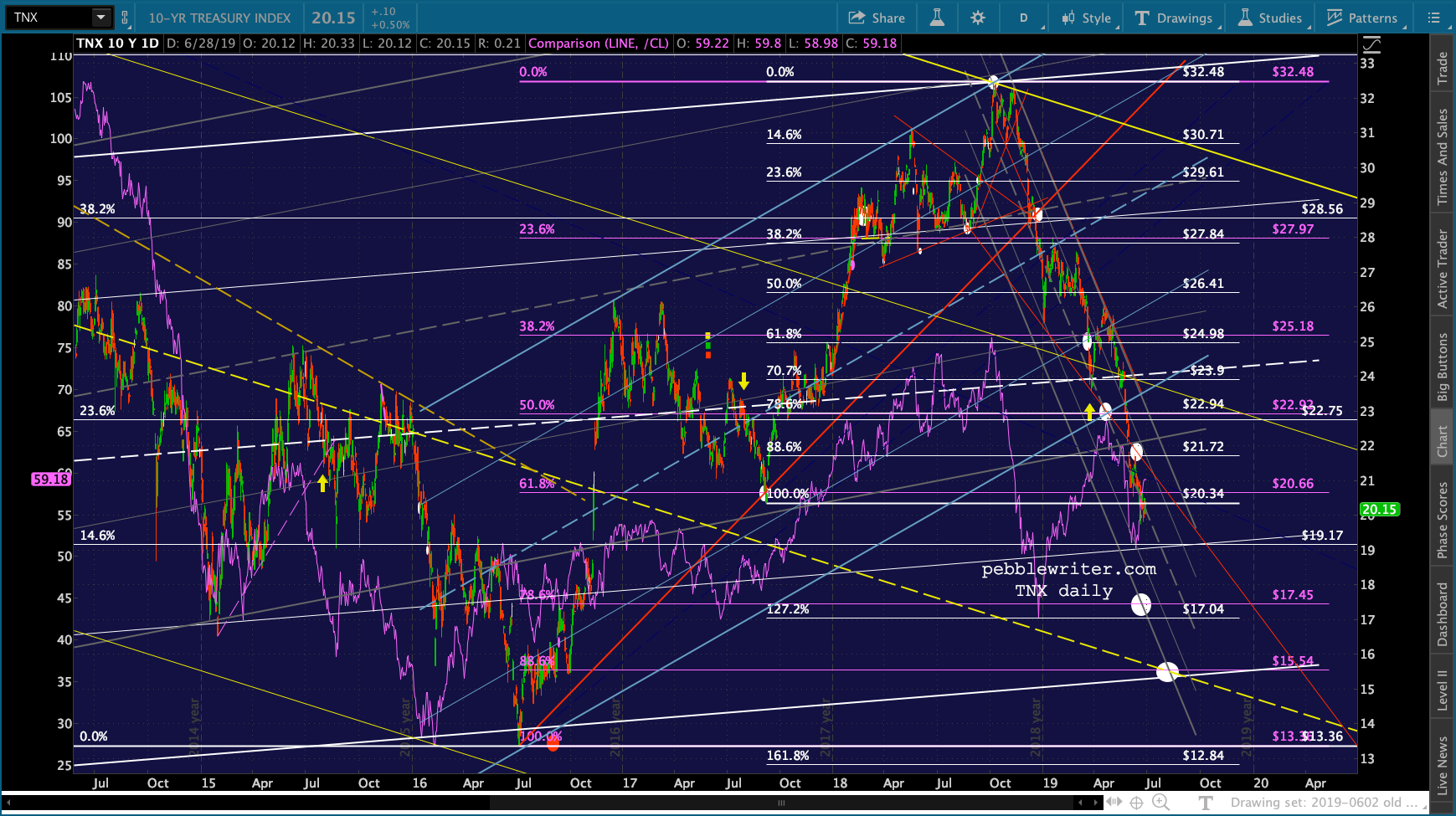

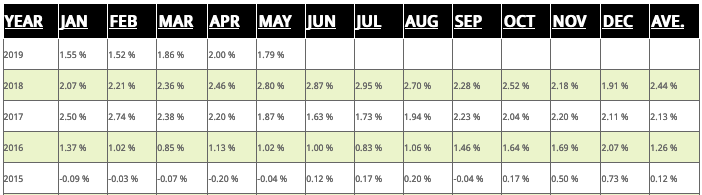

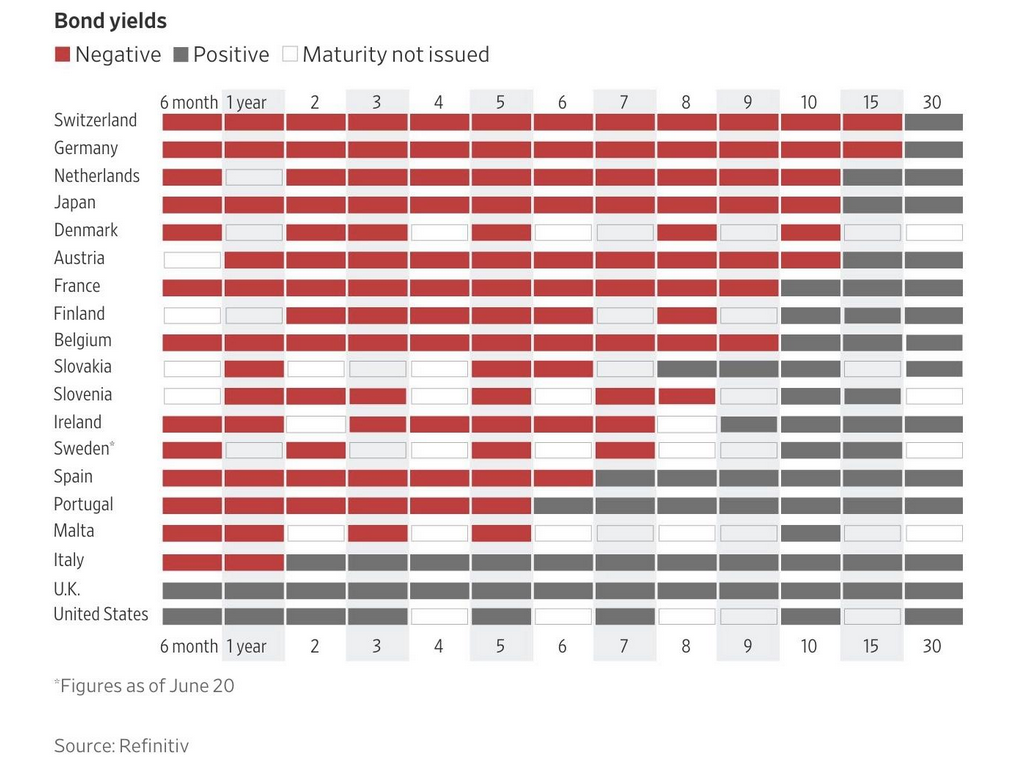

Looking at the 10Y, we saw a departure from the low rate regime between July 2016 and Nov 2018.  This occurred for two reasons. First, rising oil and gas prices drove inflation much higher. CPI averaged 0.12% in 2015 as oil and gas plunged and USDJPY spiked. It started recovering in early 2016 when oil and gas bottomed, topping 2% in Dec 2016 and spending most of the next two years in the 2-3% range. As CPI rose, so did interest rates — the natural relationship between the two.

This occurred for two reasons. First, rising oil and gas prices drove inflation much higher. CPI averaged 0.12% in 2015 as oil and gas plunged and USDJPY spiked. It started recovering in early 2016 when oil and gas bottomed, topping 2% in Dec 2016 and spending most of the next two years in the 2-3% range. As CPI rose, so did interest rates — the natural relationship between the two. In late 2018, after two months of CPI flirting with 3% and the 10Y nearing 3.5%, oil prices plunged. This took the pressure off the 10Y, which has since dropped to below 2%.

In late 2018, after two months of CPI flirting with 3% and the 10Y nearing 3.5%, oil prices plunged. This took the pressure off the 10Y, which has since dropped to below 2%.

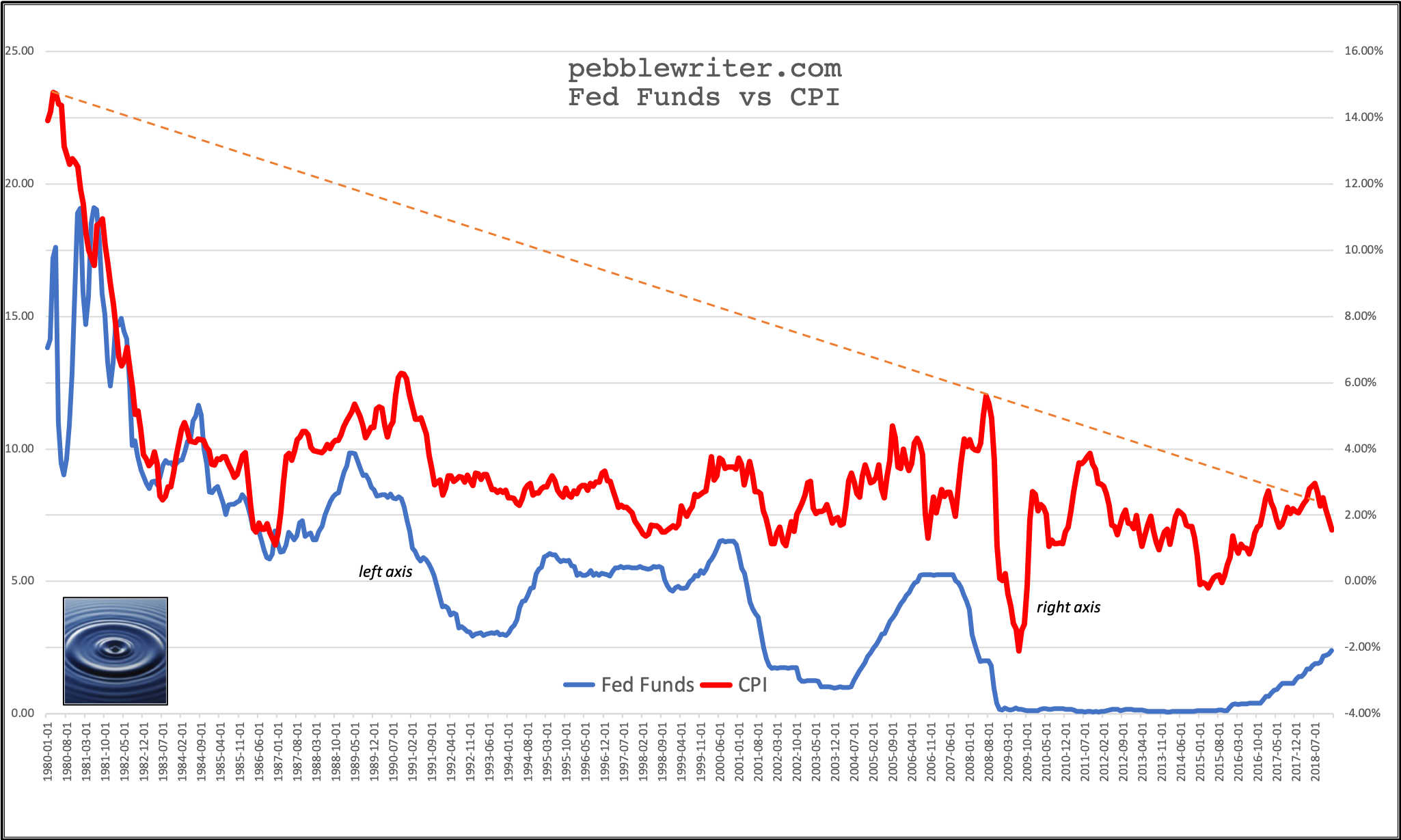

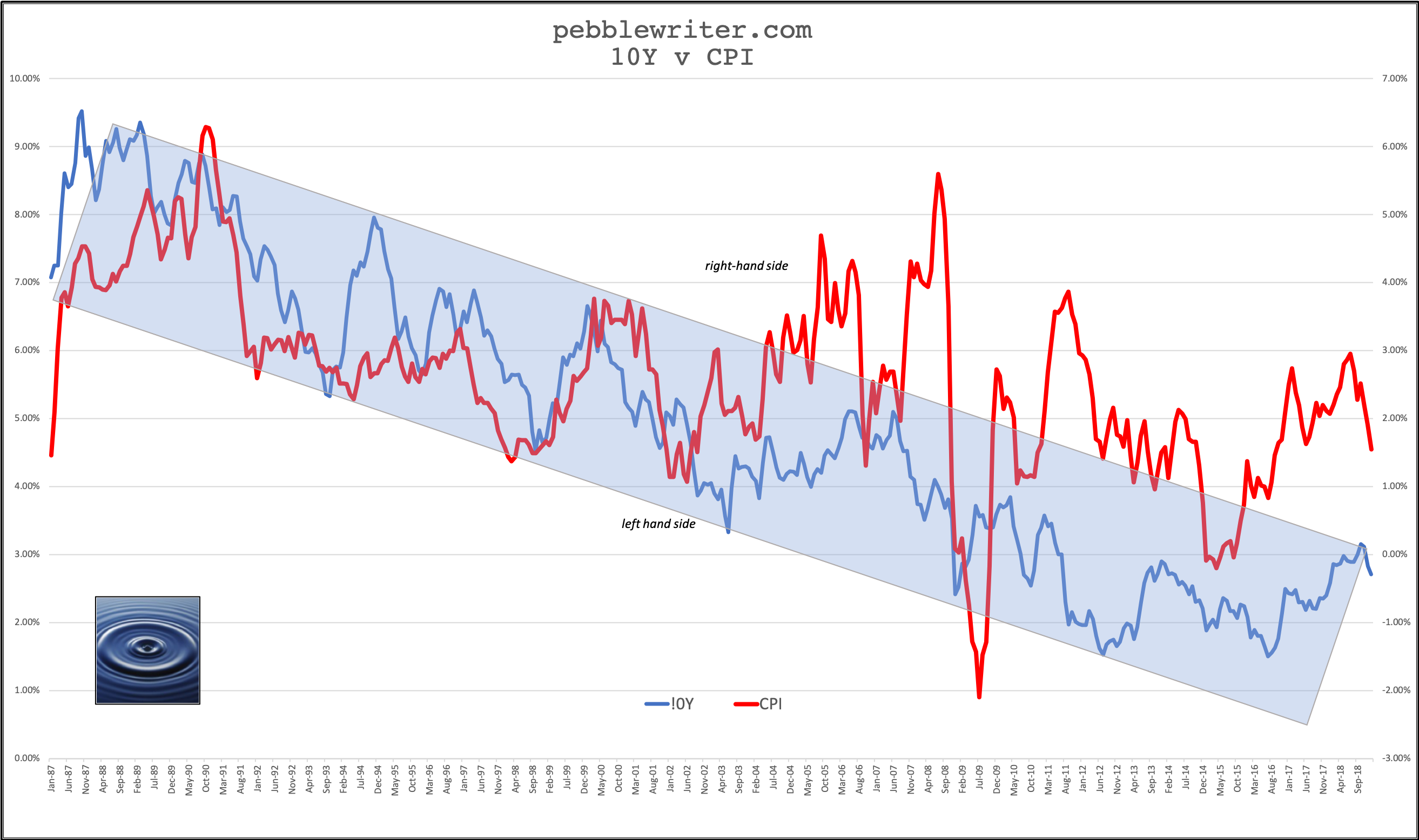

The other reason, of course, is that the Fed wanted to build a little cushion in rates in anticipation of the next time they need to cut. This affects the short end more than the long end.  But, long rates have also been somewhat responsive over the years.

But, long rates have also been somewhat responsive over the years. The problem, of course, is that the 10Y didn’t rise as much as the 2Y…

The problem, of course, is that the 10Y didn’t rise as much as the 2Y… … thus, compressing that portion of the curve and sounding recession alarm bells — which worried equity investors.

… thus, compressing that portion of the curve and sounding recession alarm bells — which worried equity investors. As we’ve discussed many times before, it isn’t the curve going negative that does major damage to stocks. It’s the sharp unwinding as occurred during 2000-2003 and 2007-2009 (the shaded areas above.)

As we’ve discussed many times before, it isn’t the curve going negative that does major damage to stocks. It’s the sharp unwinding as occurred during 2000-2003 and 2007-2009 (the shaded areas above.)

Right now, the Fed has to choose between letting 2s10s break out — which would likely damage stocks quite a bit — or letting the curve invert — which, to investors and economists alike, would signal a recession. Again – not great for stocks.

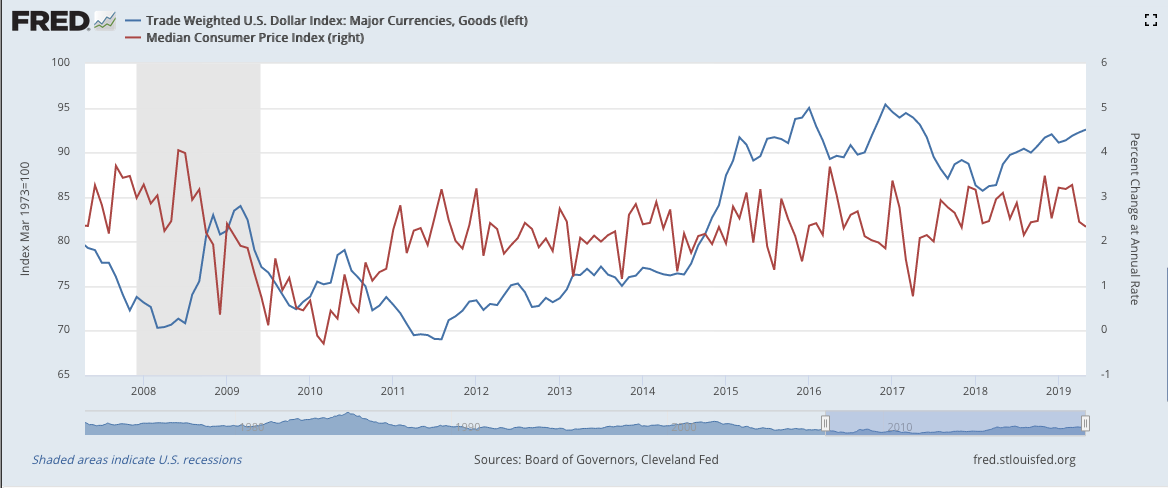

Where do currencies come in? The BoJ and ECB have been very aggressive in depressing interest rates.

As the differential grows between those rates and the US offerings, funds seek out the higher yielding offerings in the US. It boosts the dollar relative to the euro and yen. A rising USDJPY is beneficial to stocks, so no problem there except that (1) Japan’s interest rates are already well below its CPI – a declining yen exacerbates this problem, and (2) a breakout in DXY would depress the US’ already low inflation.

As the differential grows between those rates and the US offerings, funds seek out the higher yielding offerings in the US. It boosts the dollar relative to the euro and yen. A rising USDJPY is beneficial to stocks, so no problem there except that (1) Japan’s interest rates are already well below its CPI – a declining yen exacerbates this problem, and (2) a breakout in DXY would depress the US’ already low inflation.

Low inflation is okay to a point. But, if it gets “too” low, whatever that might be these days, it starts to become obvious that the economy is no longer growing at a healthy clip. Consumer confidence sags, retail sales and spending sag, etc. If inflation is not a threat, rates eventually begin to decline.

Low inflation is okay to a point. But, if it gets “too” low, whatever that might be these days, it starts to become obvious that the economy is no longer growing at a healthy clip. Consumer confidence sags, retail sales and spending sag, etc. If inflation is not a threat, rates eventually begin to decline.

So, the trick is to keep inflation in a sweet spot — which would allow the Fed to keep interest rates in a sweet spot — without the curve further inverting or breaking out. It’s a tall order, and explains why even though USDJPY has been declining (resetting) DXY has been able to avoid breaking out. The solution has been to make sure that EURUSD holds its value.

Remember, if EURUSD breaks out, it means the value of the USD is declining — which offsets its rise courtesy of the JPY. The net effect: flat DXY and EURUSD.

How long can this go on? Having broken above its SMA200, EURUSD is about to backtest the large H&S neckline at 1.1446ish.  DXY’s rising white channel has broken down and it is doing its best to remain below its white .618. without decimating stocks in the last few days of Q2.

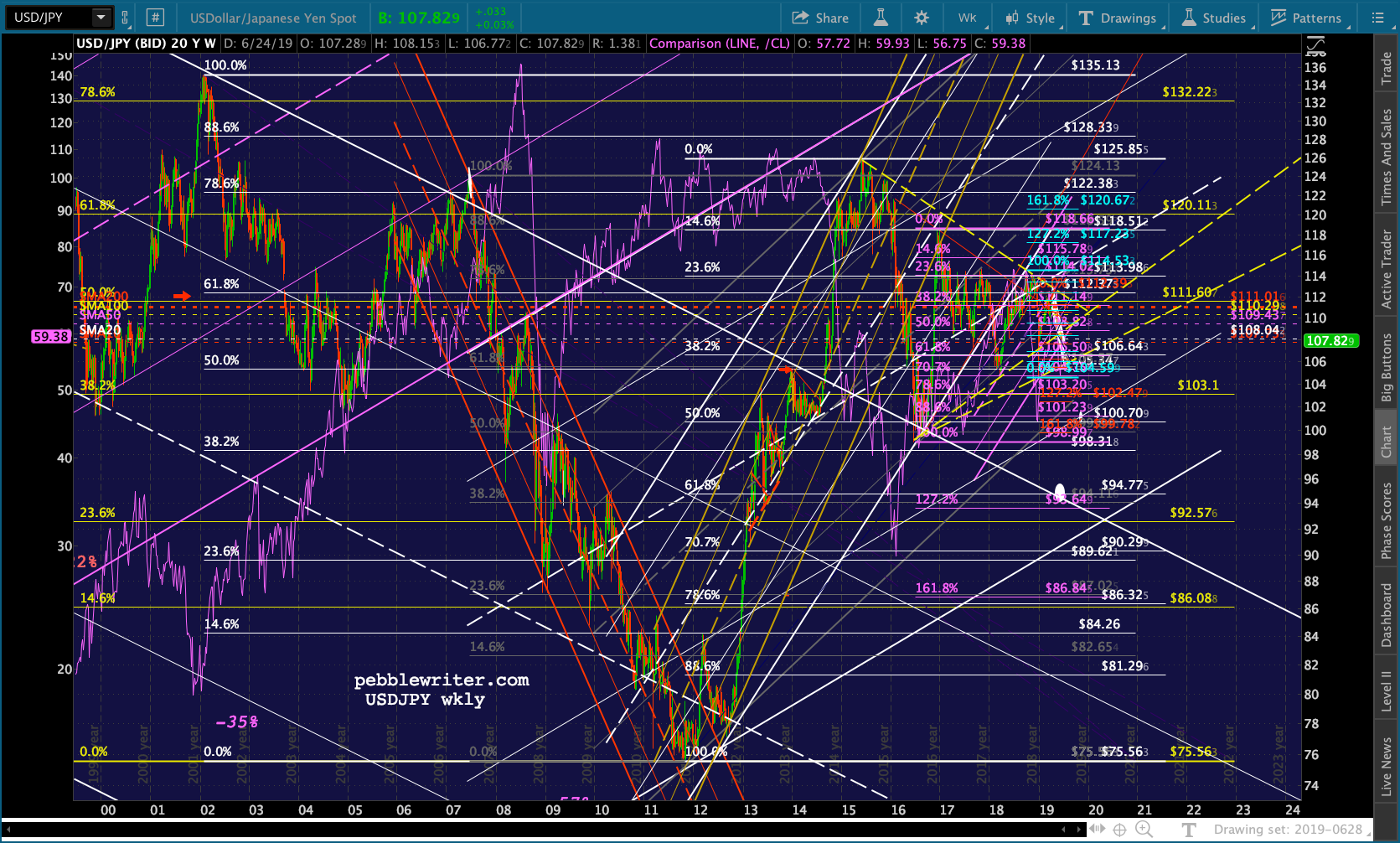

DXY’s rising white channel has broken down and it is doing its best to remain below its white .618. without decimating stocks in the last few days of Q2. If my theory about the Fed and pals angling for Trump’s exit in 2020, keeping stocks elevated will become less important and we could see USDJPY really break down — testing 101 or even 94.77.

If my theory about the Fed and pals angling for Trump’s exit in 2020, keeping stocks elevated will become less important and we could see USDJPY really break down — testing 101 or even 94.77. I’ll continue working on the big picture over the next few days. But, for now, I anticipate DXY finding support at 95.469, EURUSD finding resistance at 1.1447, and USDJPY testing 105.48. If any of those targets break down/out, we’ll revisit the forecast. I expect that we’ll see stocks sell off next week.

I’ll continue working on the big picture over the next few days. But, for now, I anticipate DXY finding support at 95.469, EURUSD finding resistance at 1.1447, and USDJPY testing 105.48. If any of those targets break down/out, we’ll revisit the forecast. I expect that we’ll see stocks sell off next week.

I have a couple of meetings this afternoon, so will sign off for now. Have a great weekend, everyone.