April retail sales came in below expectations this morning, unchanged from March versus +1.0% expected following a 10.7% stimulus-boosted print last month. Core was even more disappointing, shedding 0.8% MoM. Strong increases were seen in cars and food services, with other “opening-up” categories such as clothing, sporting goods, and general merch tumbling sharply.

The annual data was, of course, very positive given where the country was a year ago. Perhaps the better way to evaluate it is by looking at the longer-term picture. Thanks to the stimulus payments, retail sales blew through the long-term trend in January and are just now settling back to trend.

The annual data was, of course, very positive given where the country was a year ago. Perhaps the better way to evaluate it is by looking at the longer-term picture. Thanks to the stimulus payments, retail sales blew through the long-term trend in January and are just now settling back to trend. Of course, the pandemic drove a sharp increase in online sales – while retail employment dropped like a rock during the shutdowns. It has yet to come close to pre-pandemic levels and, given the general decline already underway since 2016, is unlikely to do so anytime soon.

Of course, the pandemic drove a sharp increase in online sales – while retail employment dropped like a rock during the shutdowns. It has yet to come close to pre-pandemic levels and, given the general decline already underway since 2016, is unlikely to do so anytime soon.

The markets could care less about unemployment – focusing instead on the effects of trillions in stimulus and QE, the justification for which is said unemployment. If more people returned to work, the Fed would presumably trim back its support for the markets.

The markets could care less about unemployment – focusing instead on the effects of trillions in stimulus and QE, the justification for which is said unemployment. If more people returned to work, the Fed would presumably trim back its support for the markets.

But don’t count on it. Yield Curve Control is effective, but quite addictive.

But don’t count on it. Yield Curve Control is effective, but quite addictive.

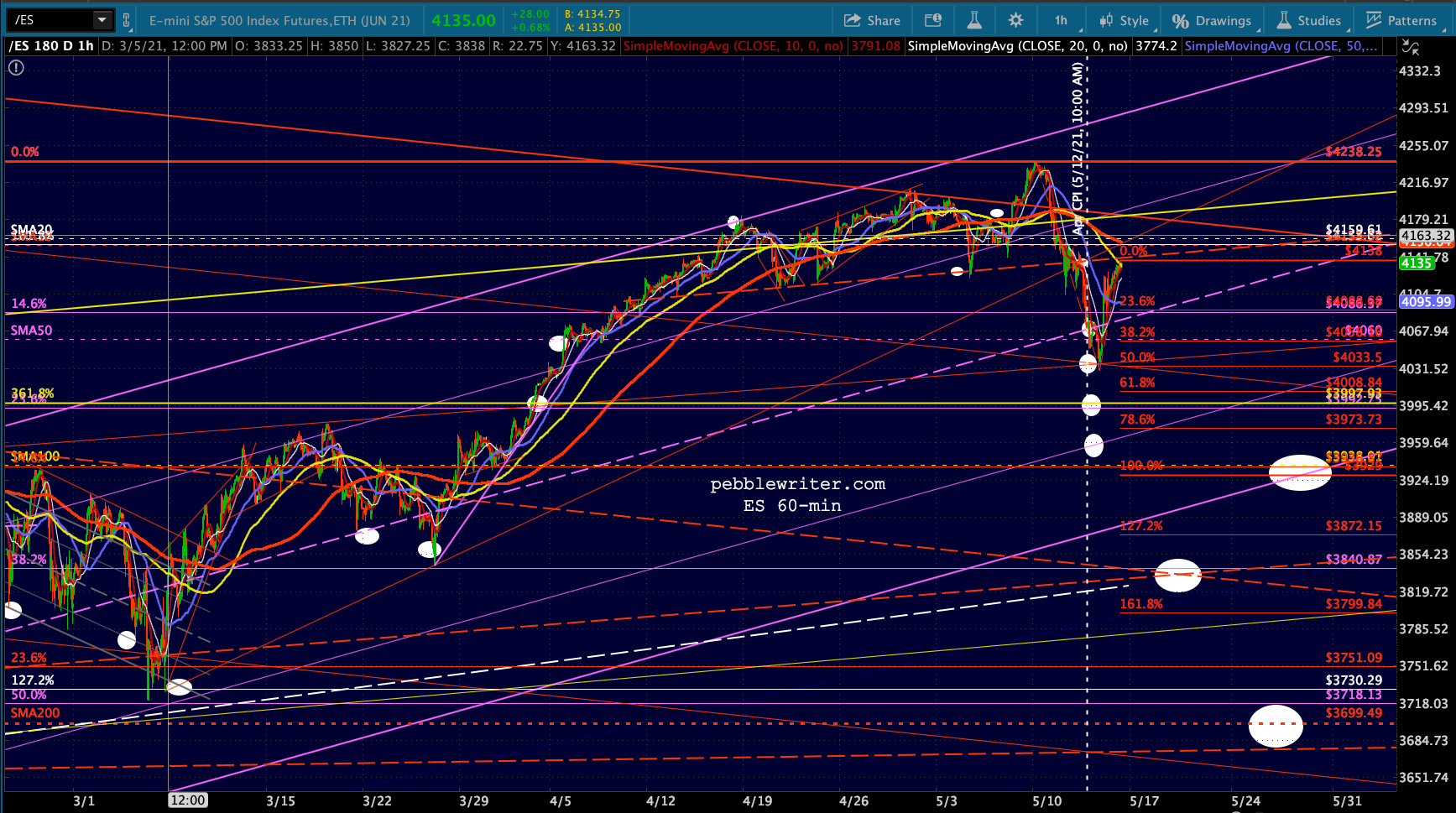

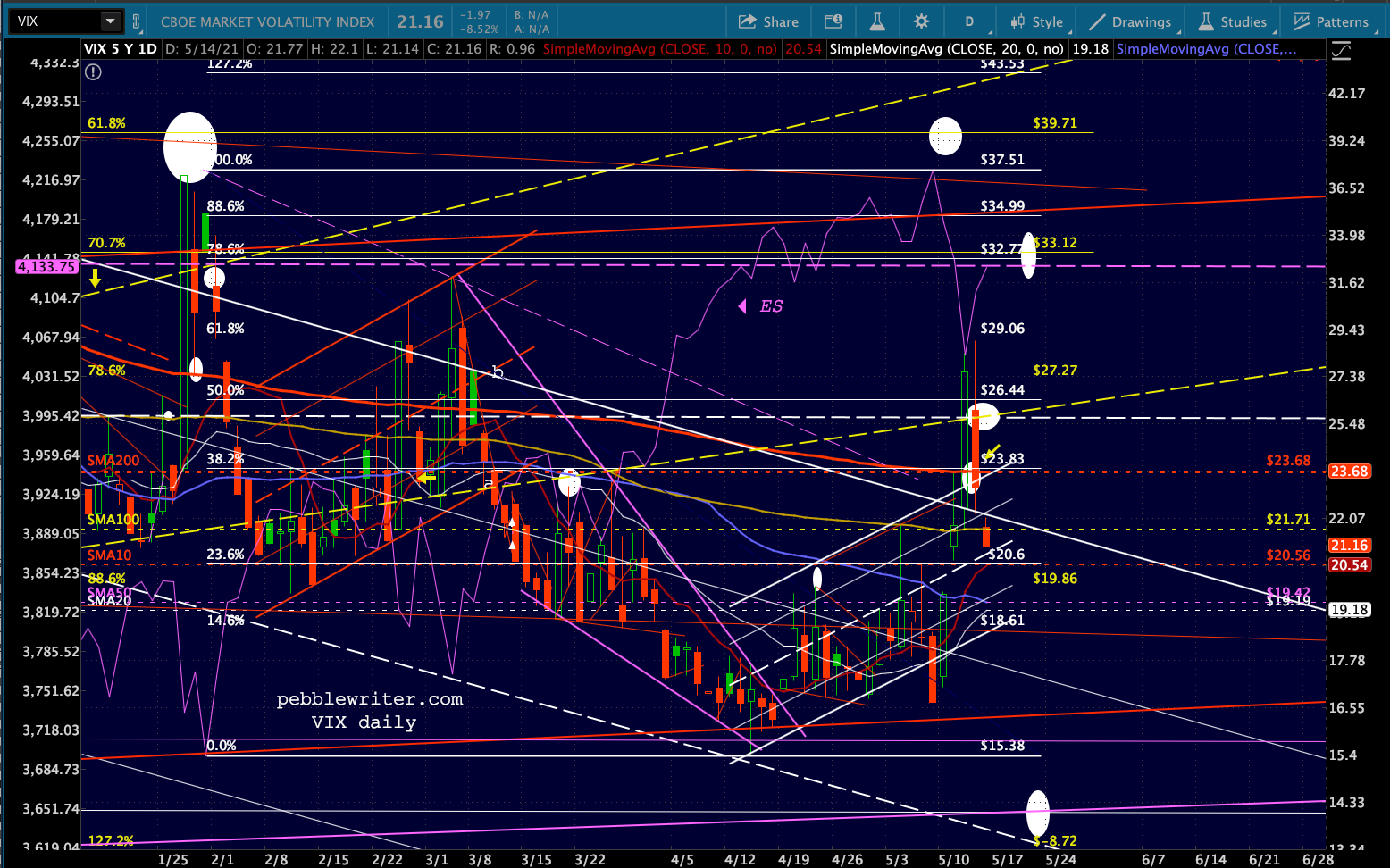

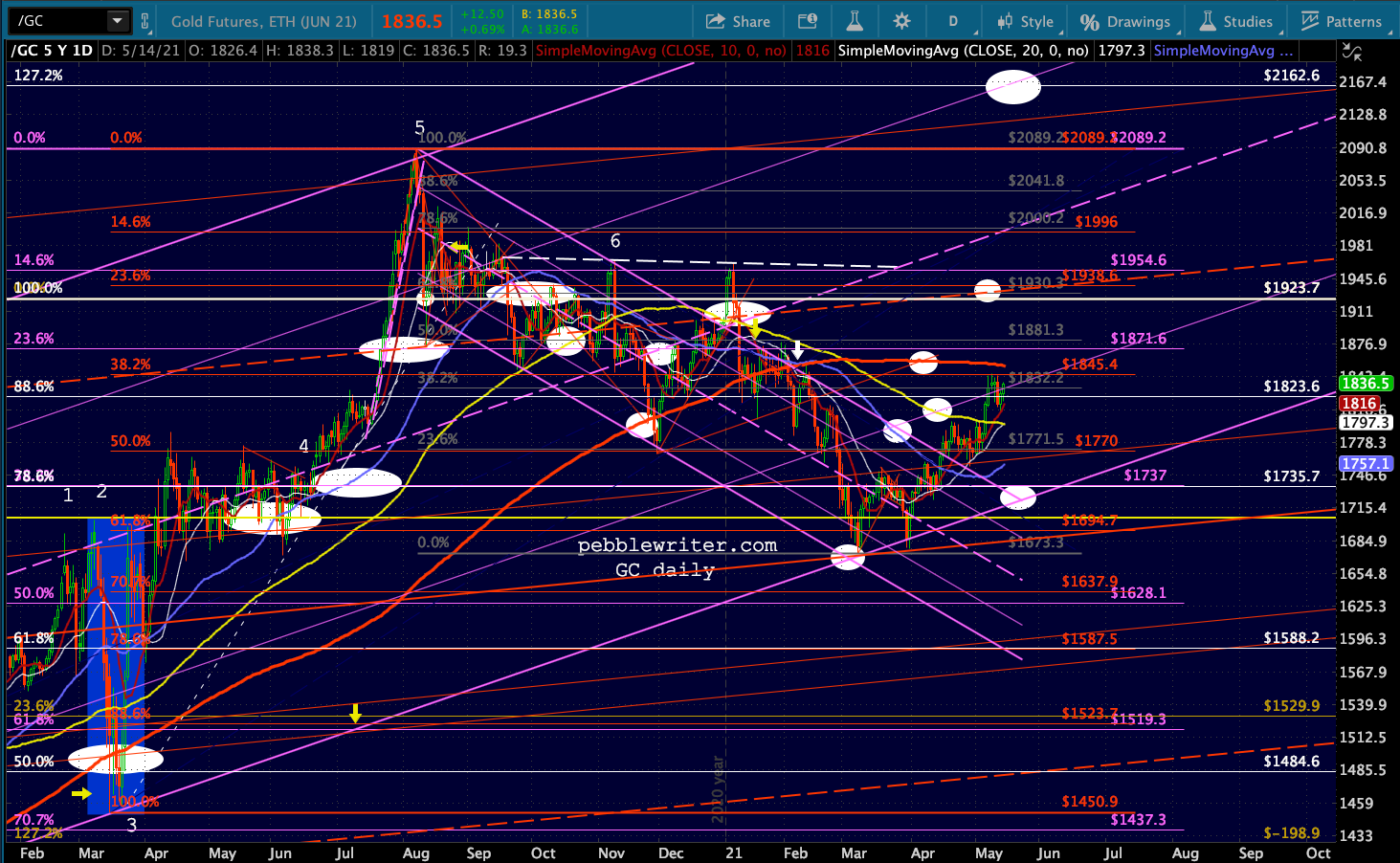

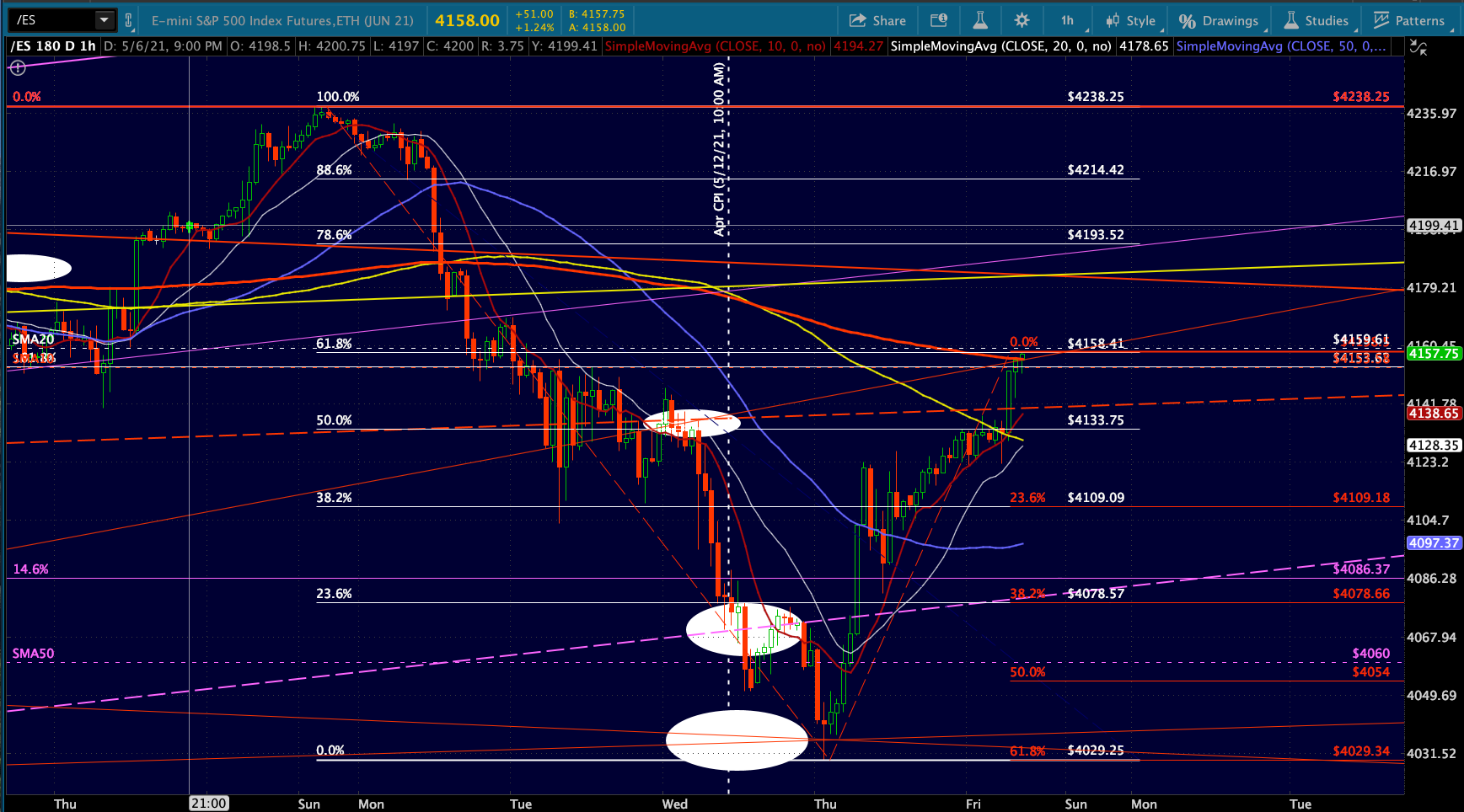

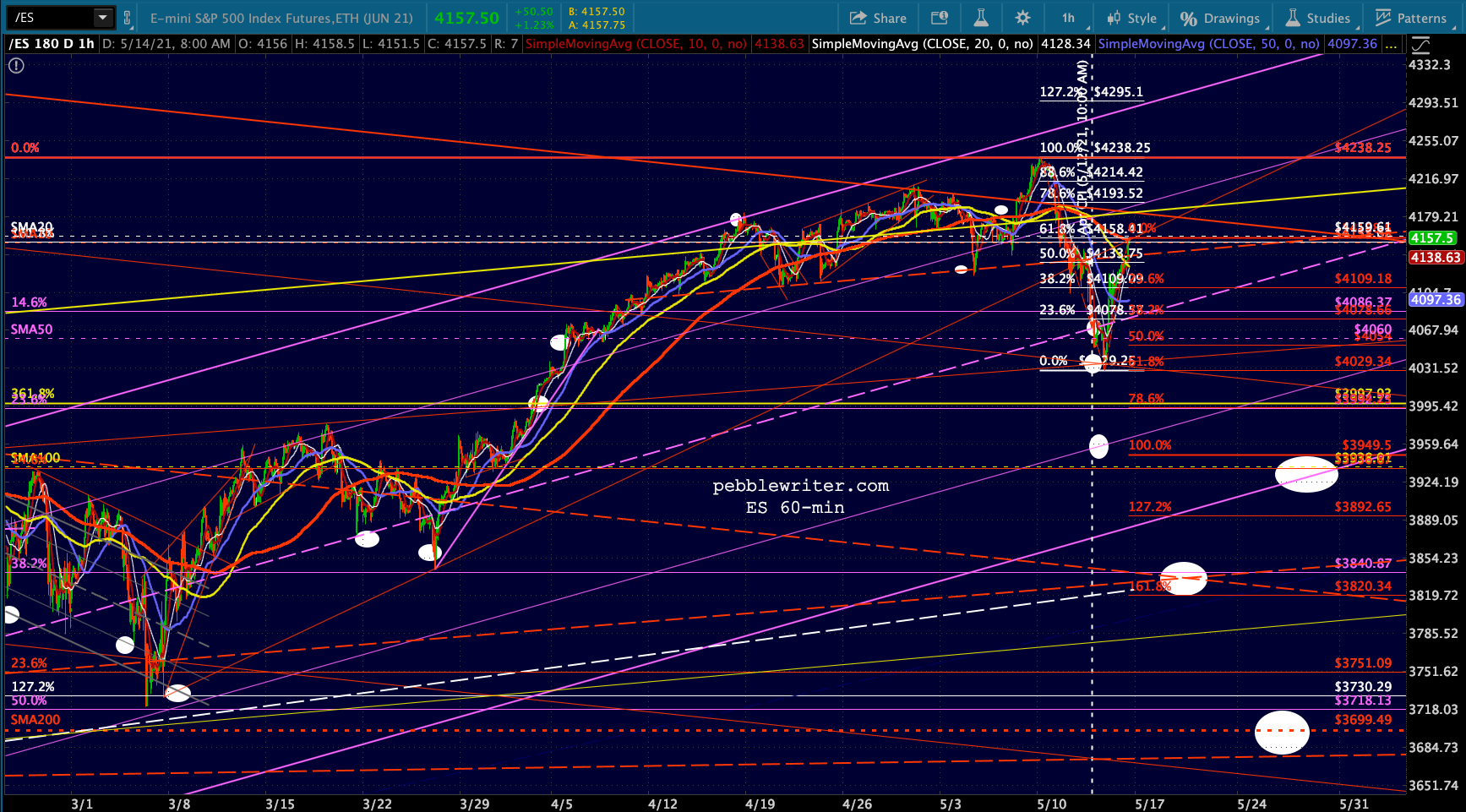

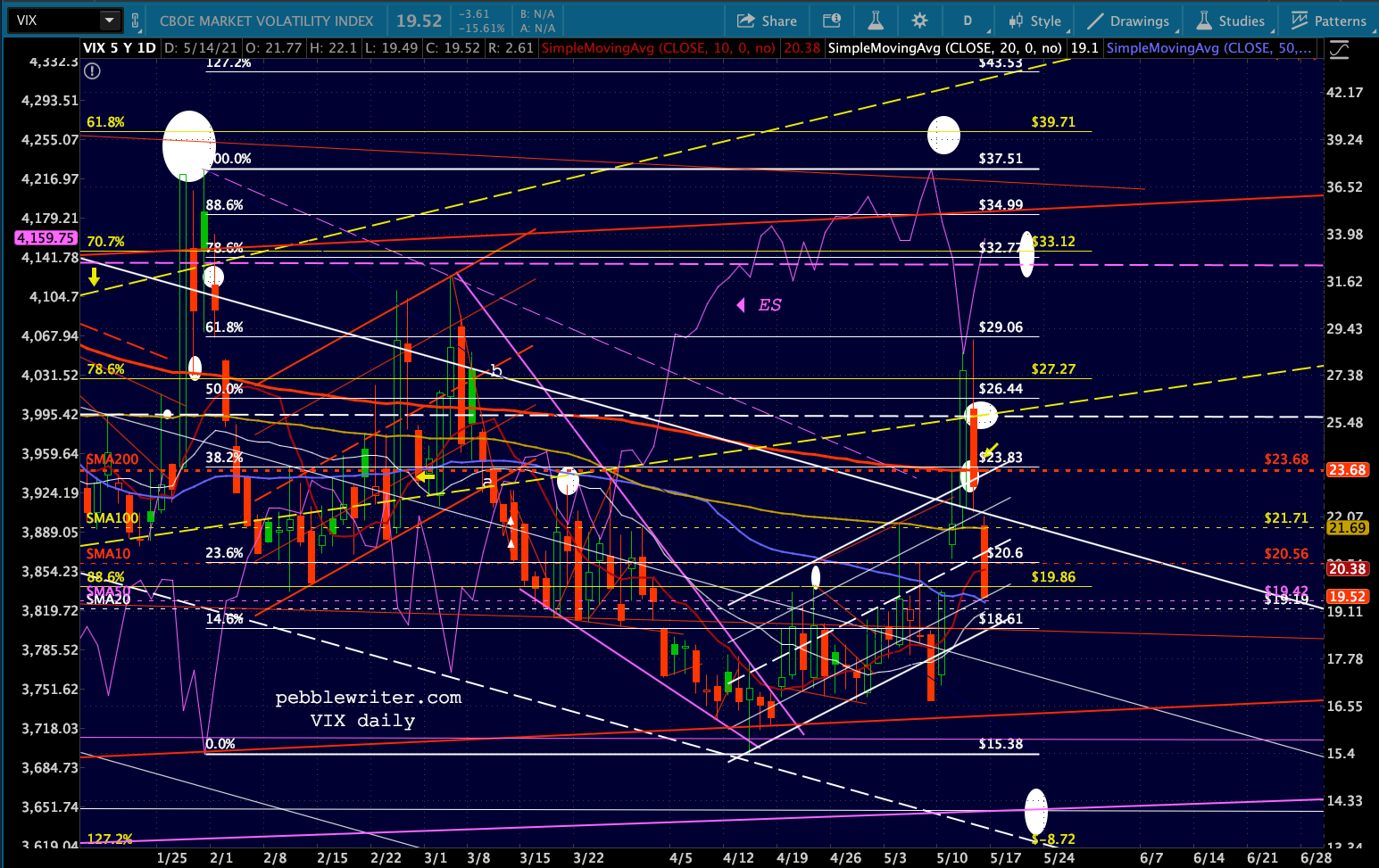

Futures backtested the red TL (erstwhile H&S neckline) overnight, primarily on the usual beatdown in VIX, which closed back below its SMA200 and gapped down below its SMA100 overnight. It’s off about 25% in the last 24 hours – a strong signal to the algos.

continued for members...The bigger picture:

continued for members...The bigger picture:

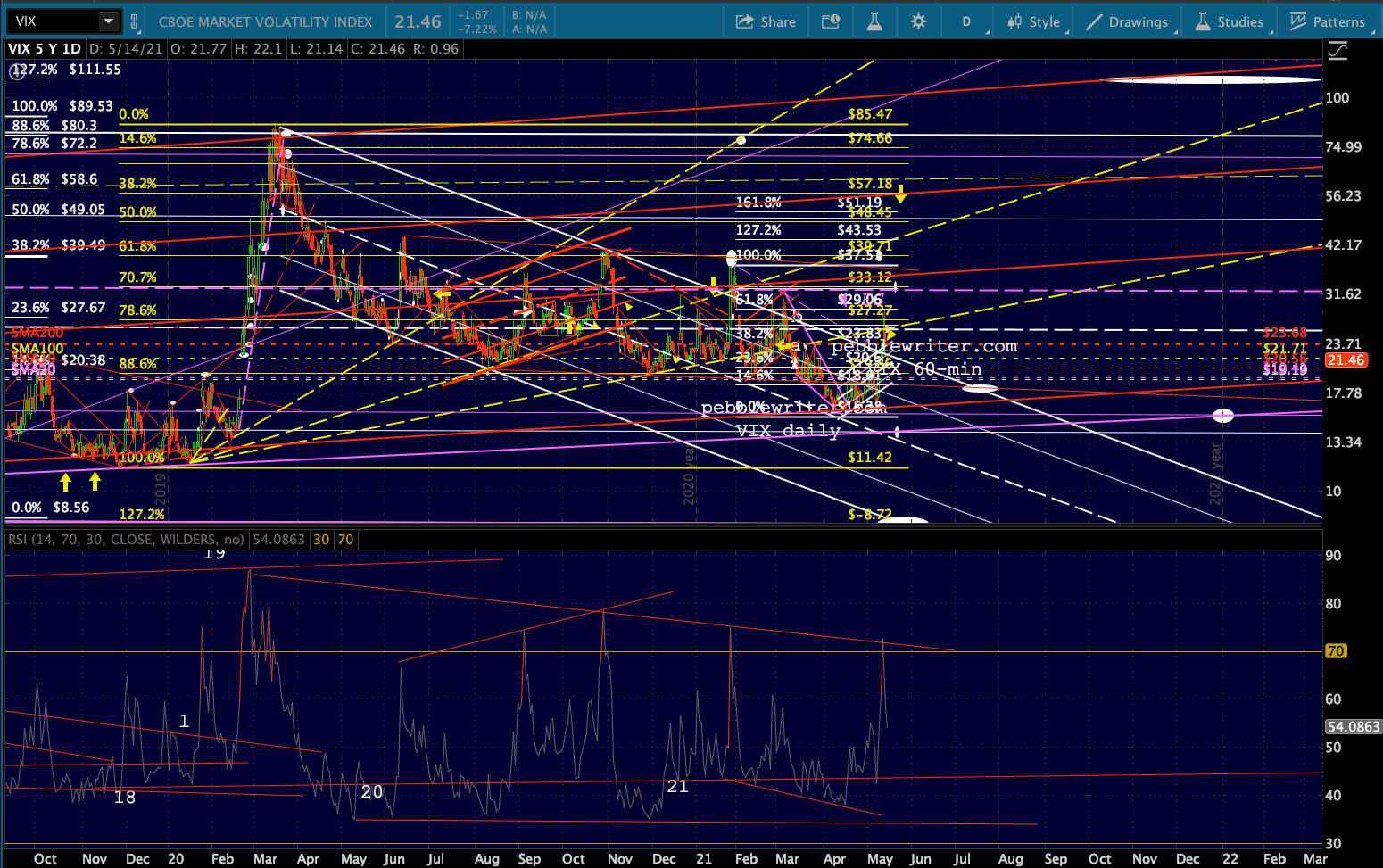

VIX’s beatdown…

VIX’s beatdown…

Note the clear pattern of reversals at VIX’s RSI peaks.

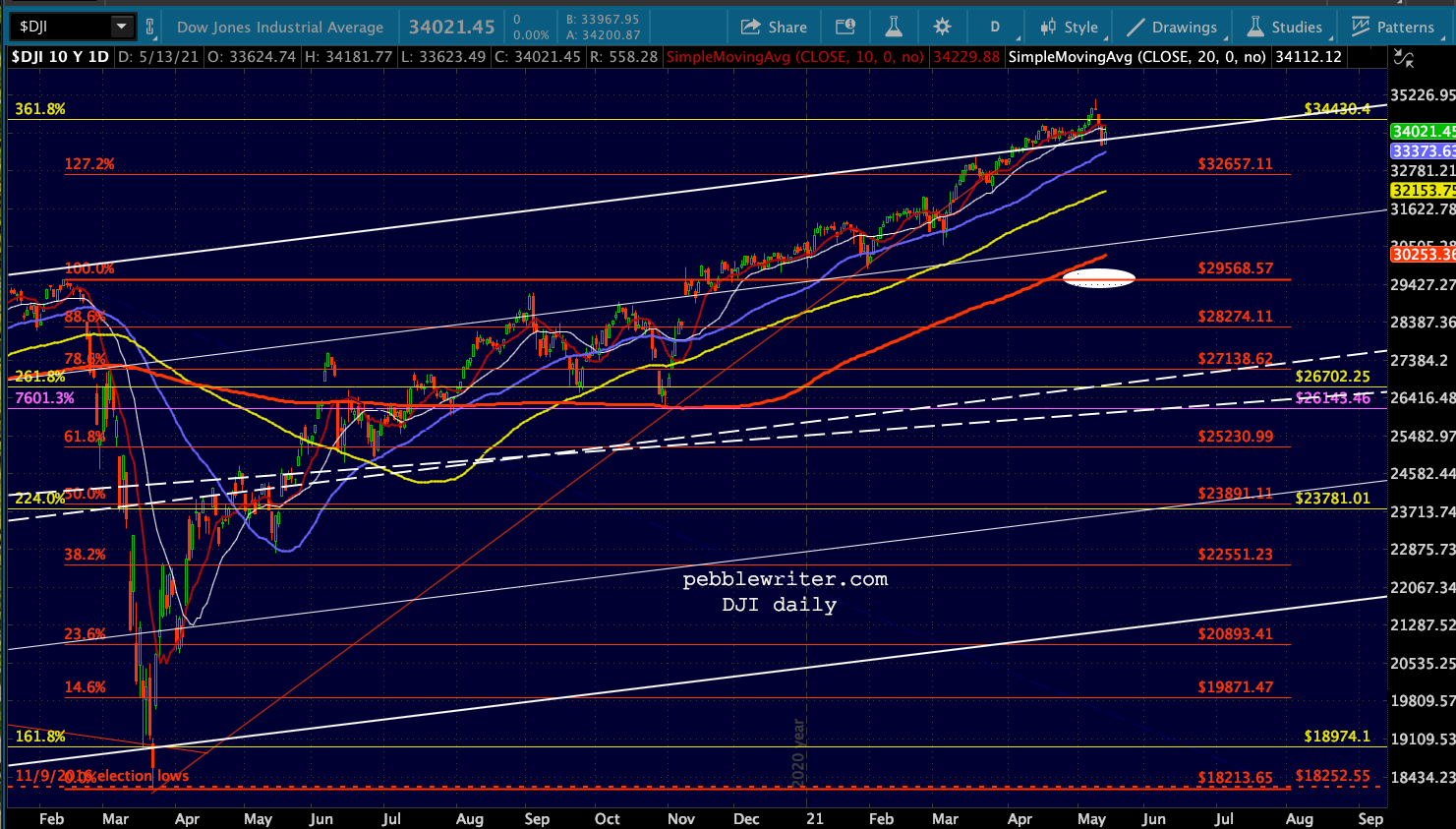

Note the clear pattern of reversals at VIX’s RSI peaks. I’d keep a very close eye on DJI, which closed just below its SMA20 yesterday. Once back on top of the SMA10 (34,268) and SMA20, it might have a hard time breaking down again. If it remains below the SMA10, this is a very good sign for bears looking for another leg down.

I’d keep a very close eye on DJI, which closed just below its SMA20 yesterday. Once back on top of the SMA10 (34,268) and SMA20, it might have a hard time breaking down again. If it remains below the SMA10, this is a very good sign for bears looking for another leg down.

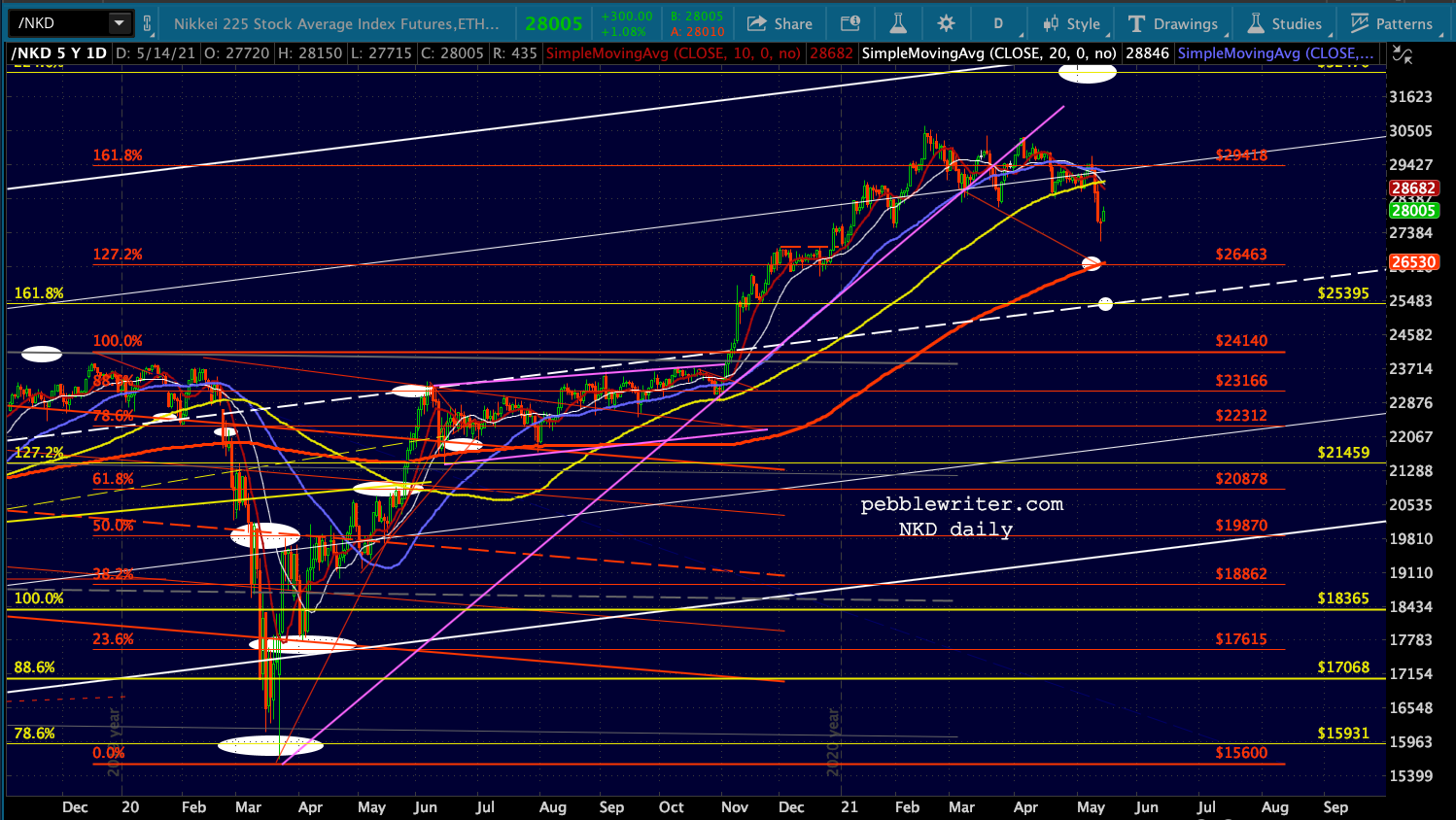

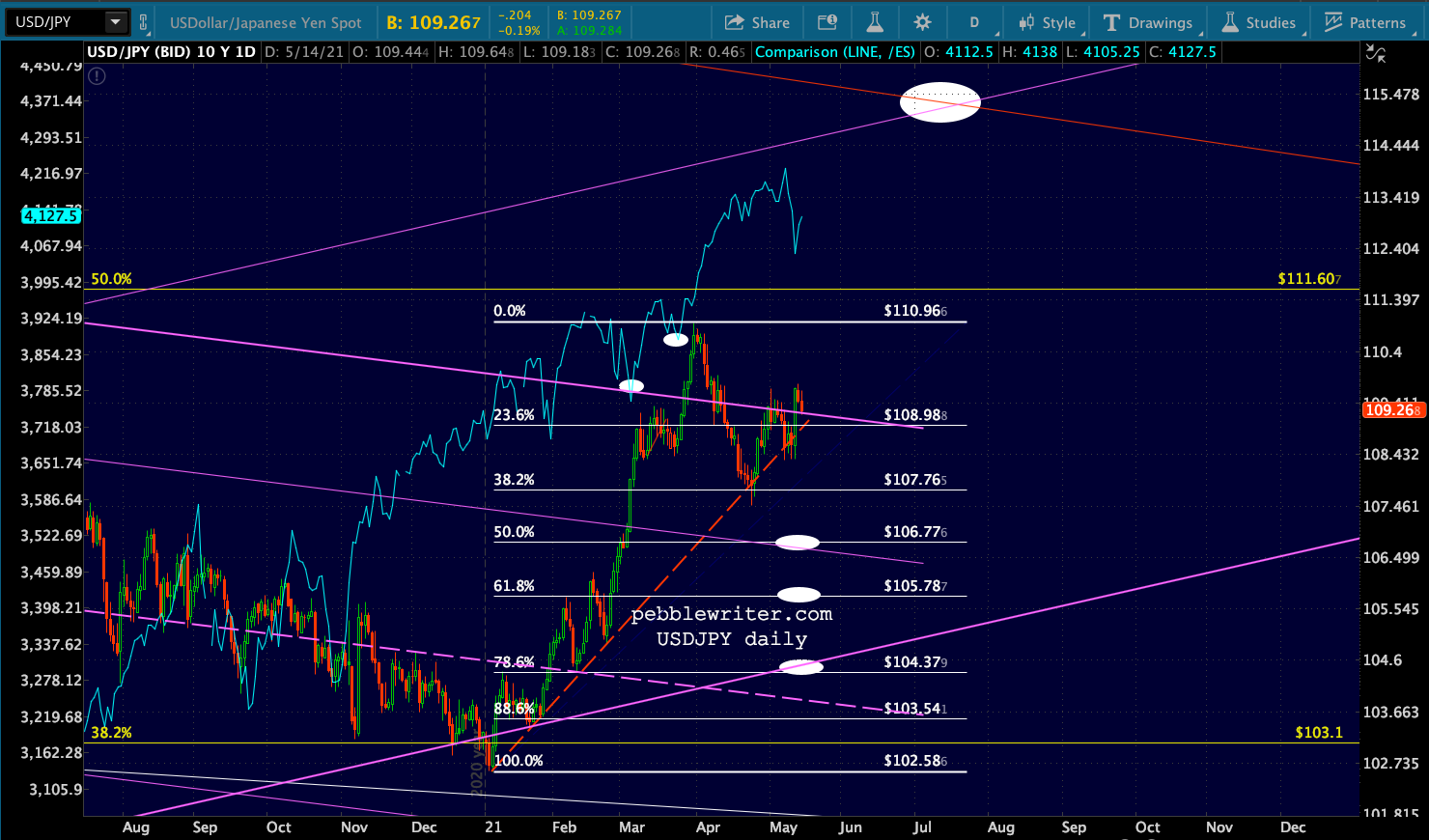

By contrast, NKD is still on track for a SMA200 backtest.

By contrast, NKD is still on track for a SMA200 backtest. The currency picture is still neutral, with USDJPY fading overnight but still in a position to support stocks.

The currency picture is still neutral, with USDJPY fading overnight but still in a position to support stocks.

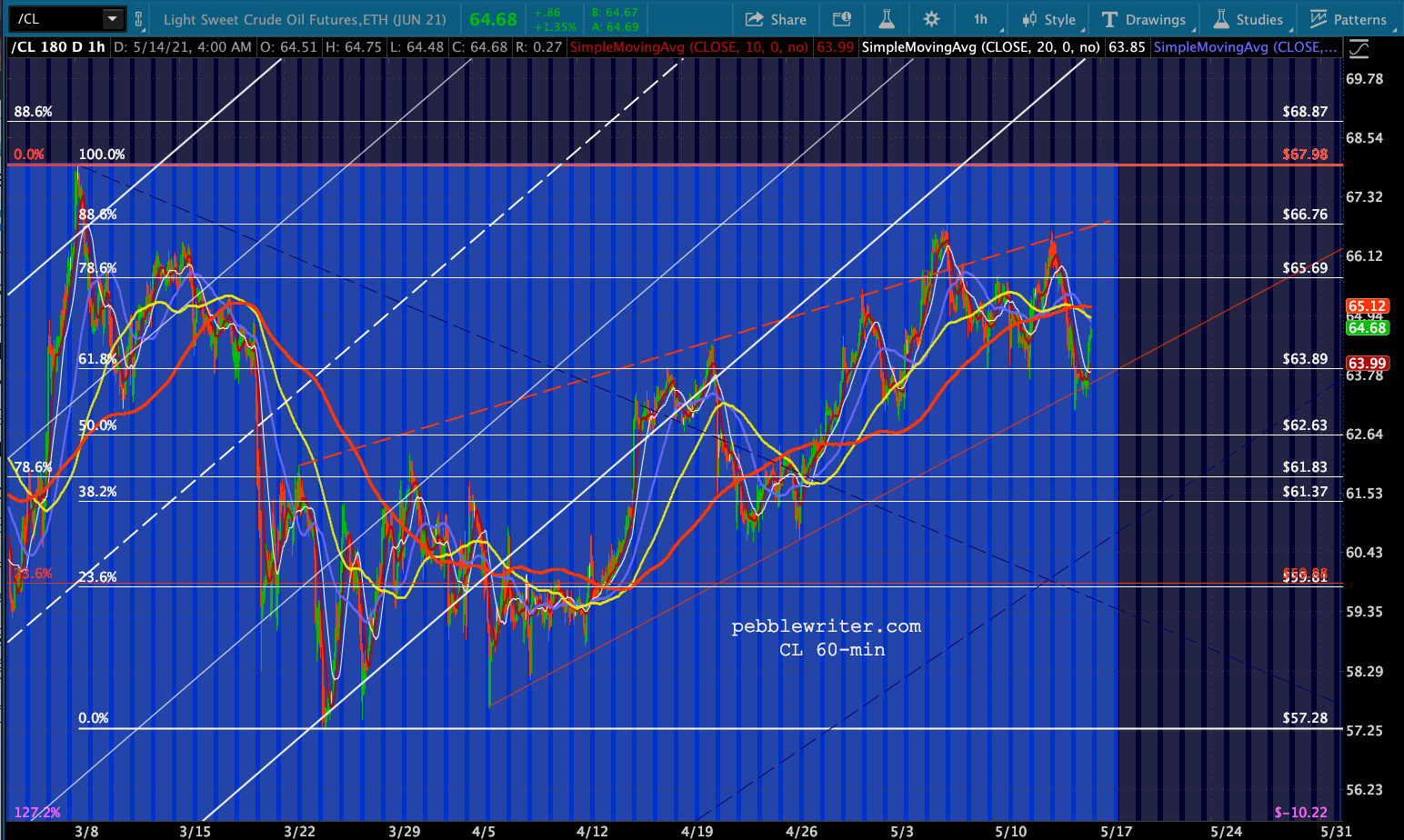

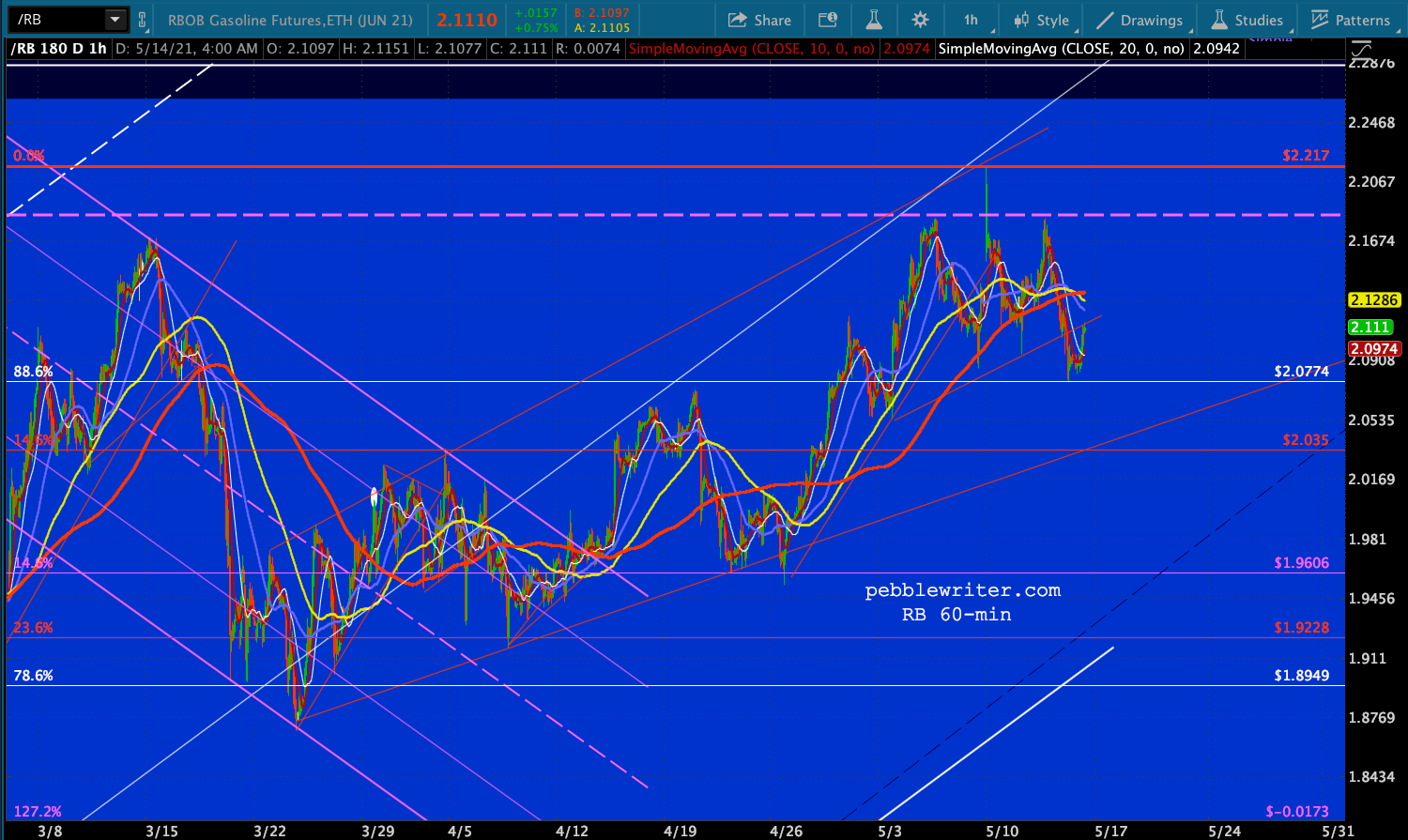

Oil and gas bounced a bit overnight, but note RB’s backtest after the TL breakdown. It’s not much, but it does at least suggest another leg lower.

Oil and gas bounced a bit overnight, but note RB’s backtest after the TL breakdown. It’s not much, but it does at least suggest another leg lower.

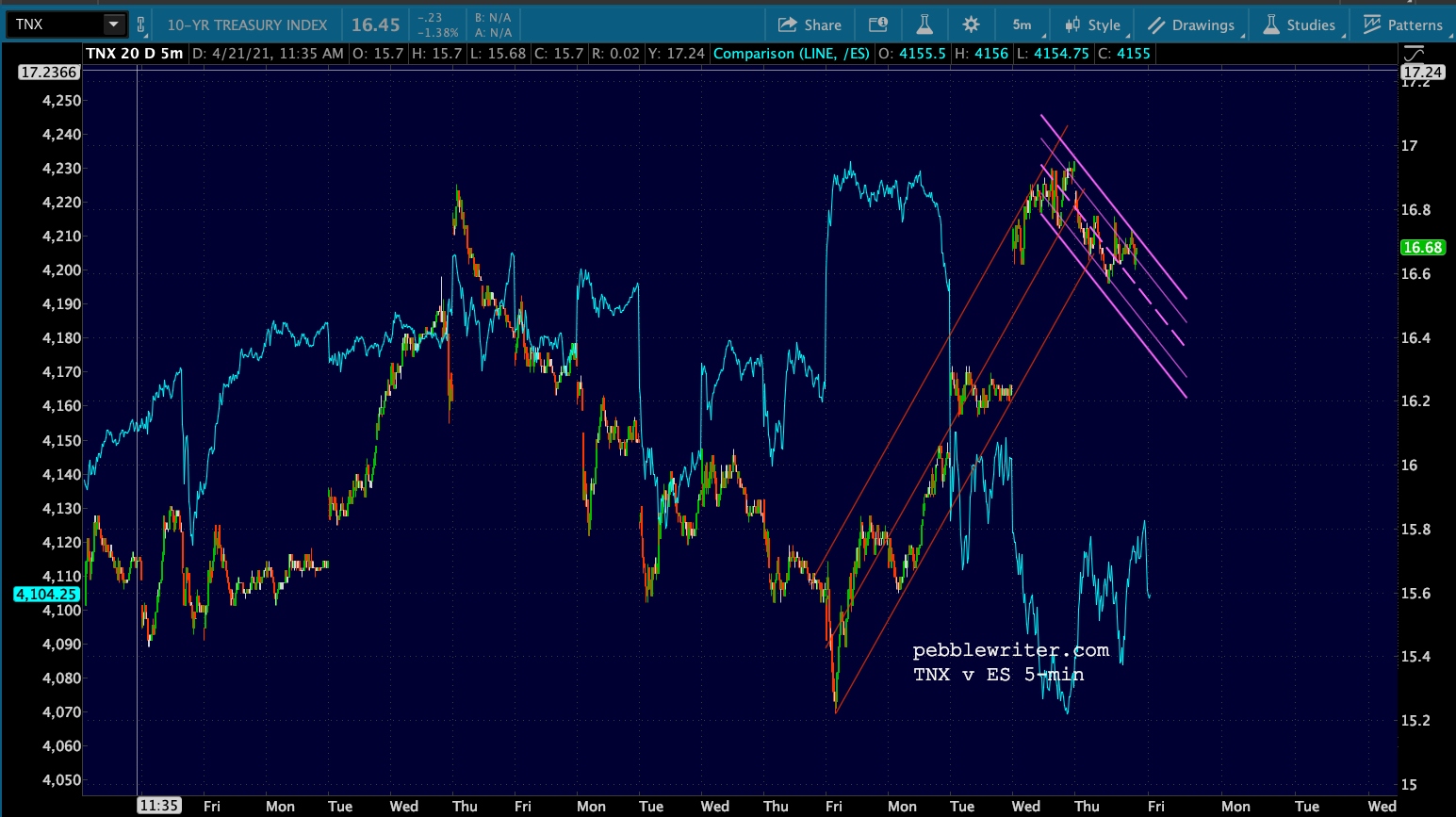

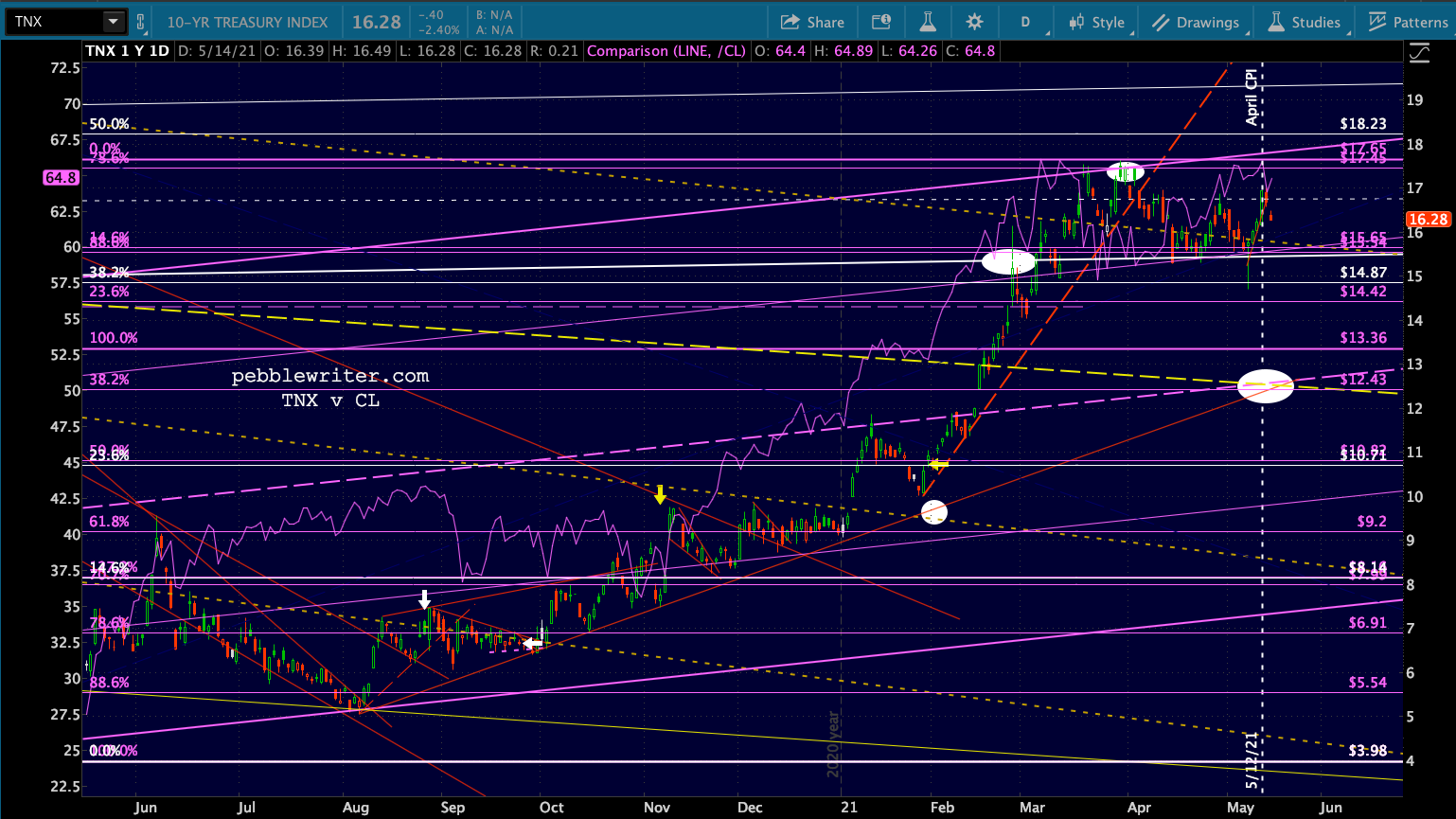

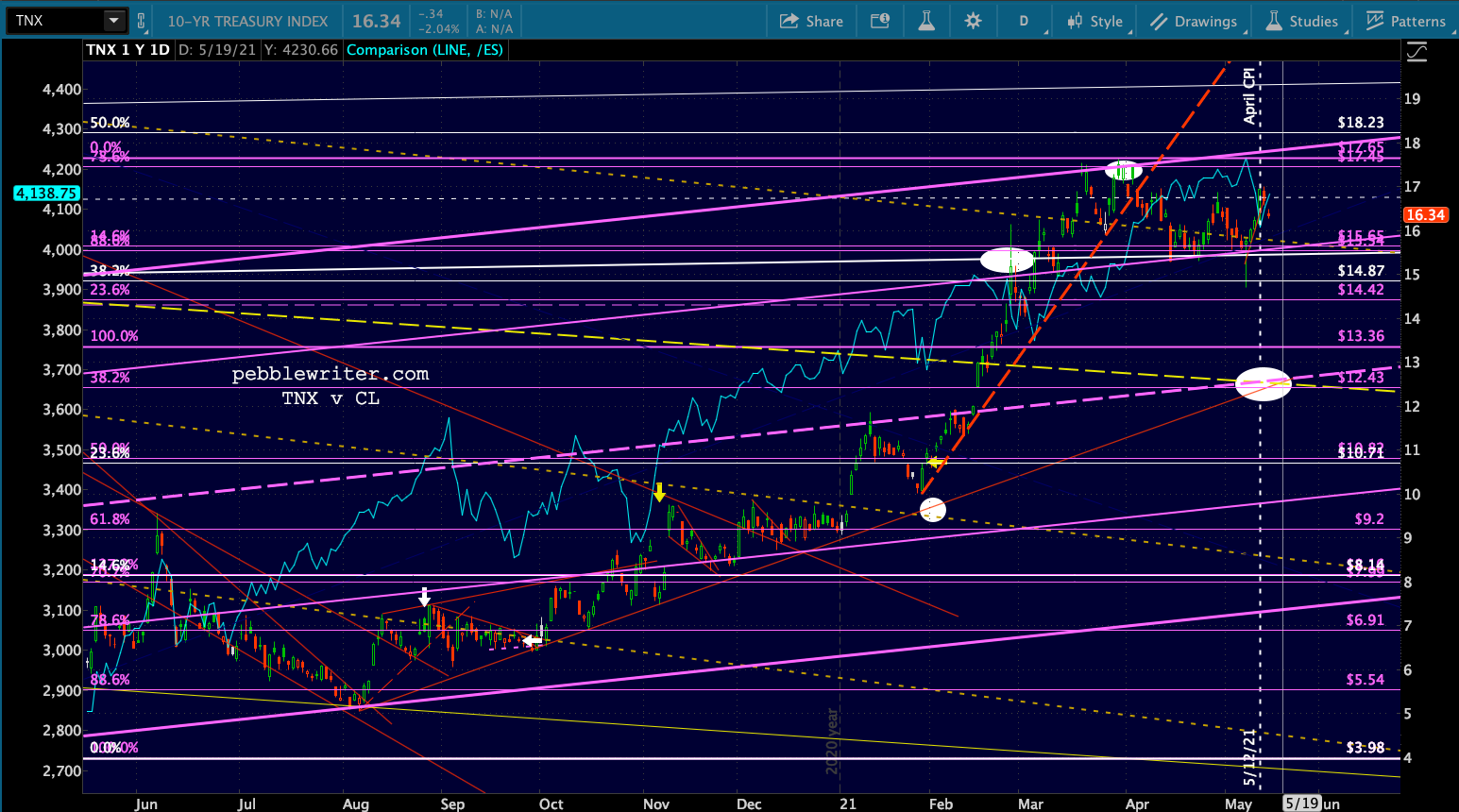

10Y yields are likely to close Wednesday’s gap on the open and are still susceptible, IMO, to a drop to 1.25…

10Y yields are likely to close Wednesday’s gap on the open and are still susceptible, IMO, to a drop to 1.25… …especially if CL sells off.

…especially if CL sells off. Remember, stocks would presumably also be affected.

Remember, stocks would presumably also be affected.

There’s obviously a lot of debate this morning about the CDC’s change in guidance regarding masks and social distancing. To me, this is a very complex situation. I am as ready as anyone to go maskless and return to eating in restaurants and traveling without limitations. But, I am leery of the timing of this decision.

There’s obviously a lot of debate this morning about the CDC’s change in guidance regarding masks and social distancing. To me, this is a very complex situation. I am as ready as anyone to go maskless and return to eating in restaurants and traveling without limitations. But, I am leery of the timing of this decision.

I am obviously a cynic. But, I’m not sure we’re where we need to be in terms of vaccination and the mutant variants are a great concern. Even if we’ve achieved herd immunity in terms of one variant of the virus, what about the others?

Everybody has their own viewpoint, but I would imagine most anti-vaccine and vaccine-resistant folks will take this as a signal to not be vaccinated. A month from now, I hope we’re heralding this decision as a smart, bold step forward rather than a huge mistake.

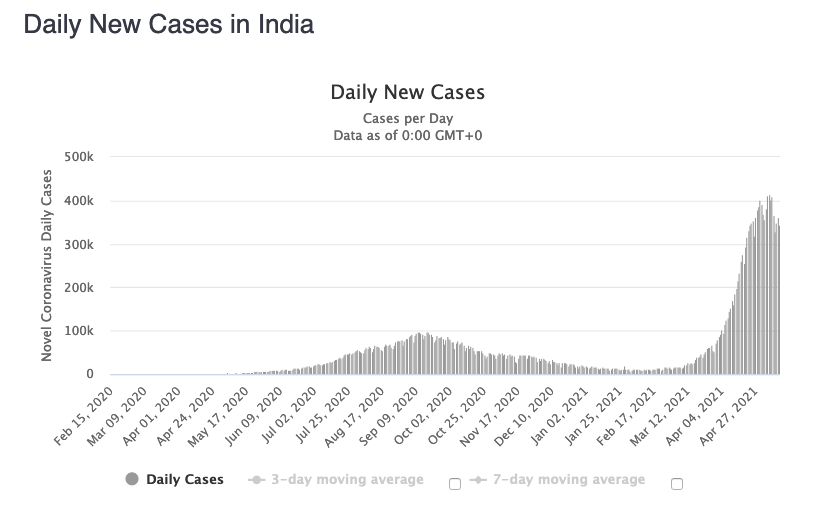

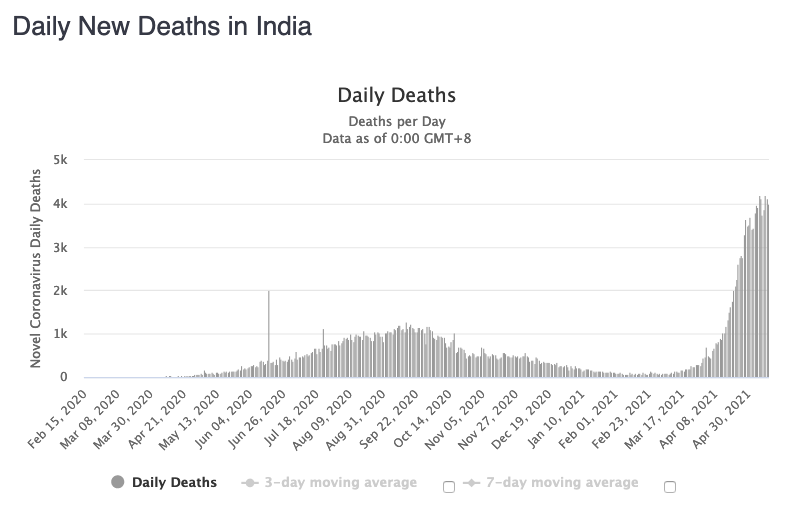

We all know how bad things are in India…

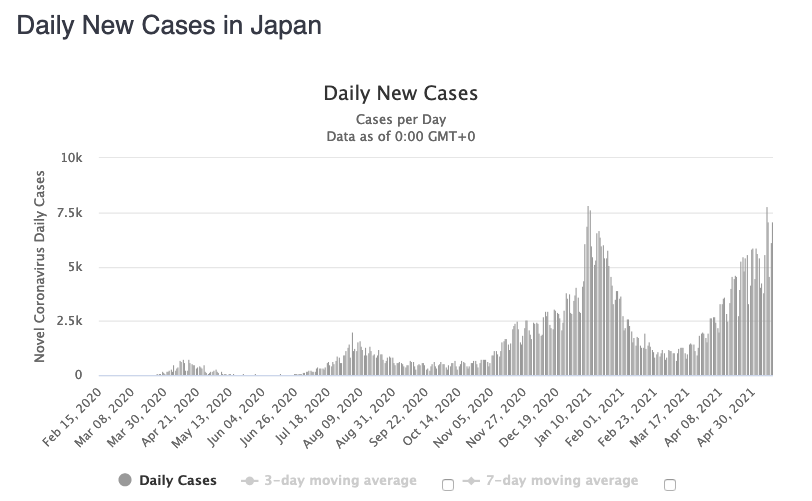

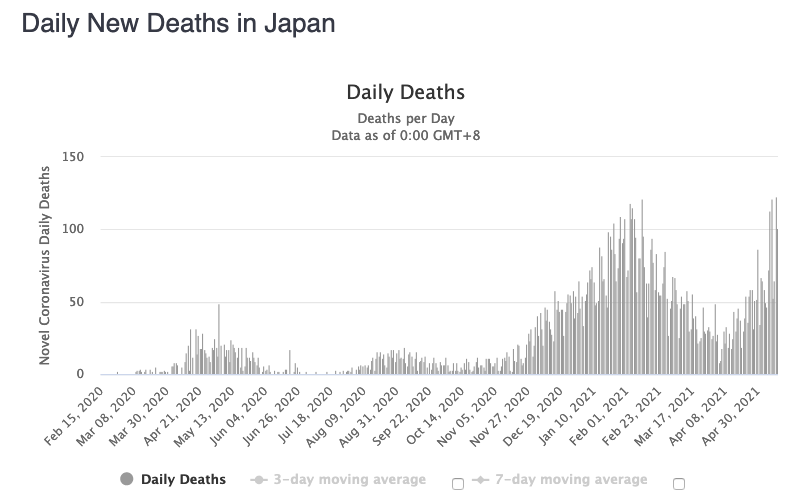

…but they’re not so great in Japan either.

…but they’re not so great in Japan either.

UPDATE: 11:20 AM

UPDATE: 11:20 AM

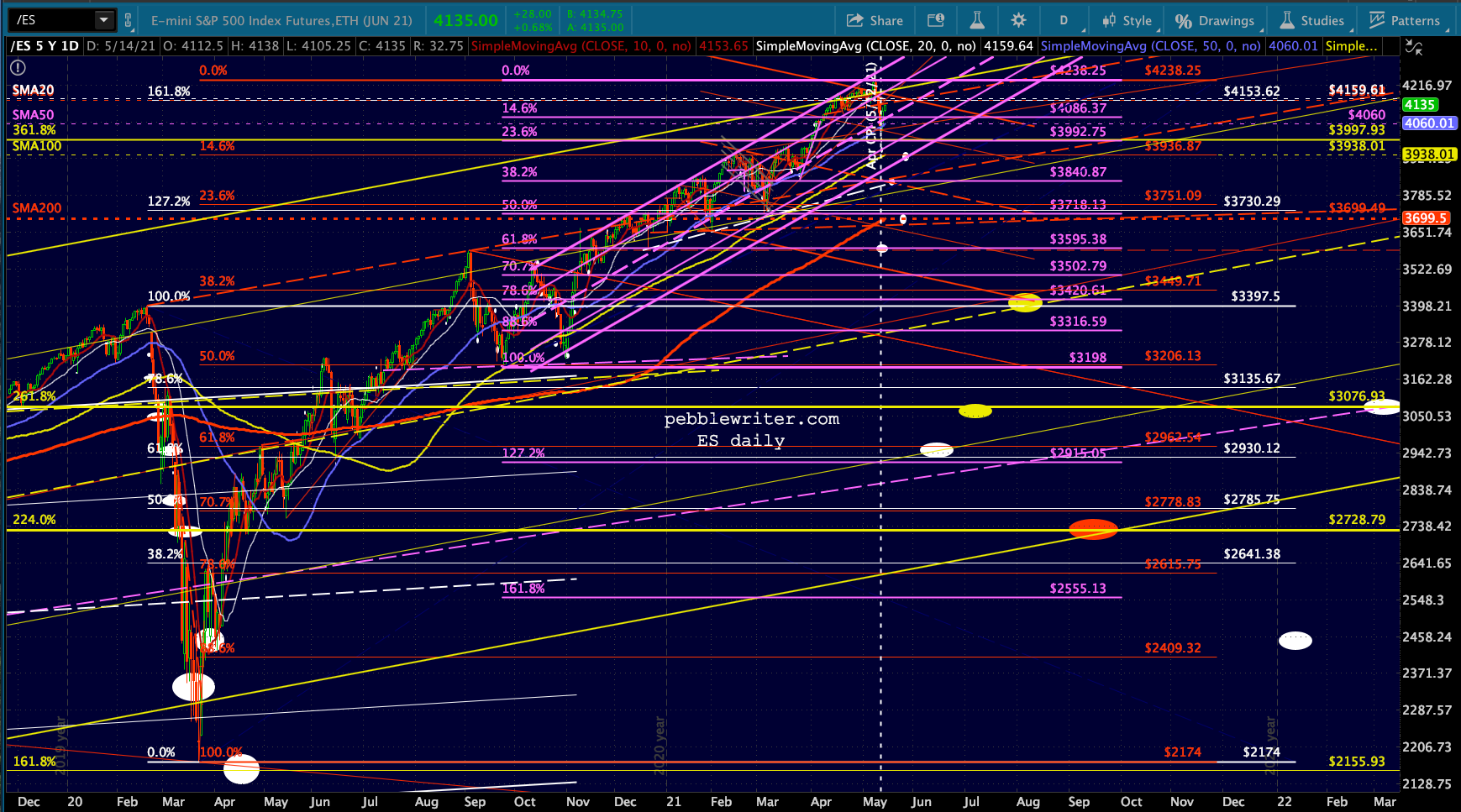

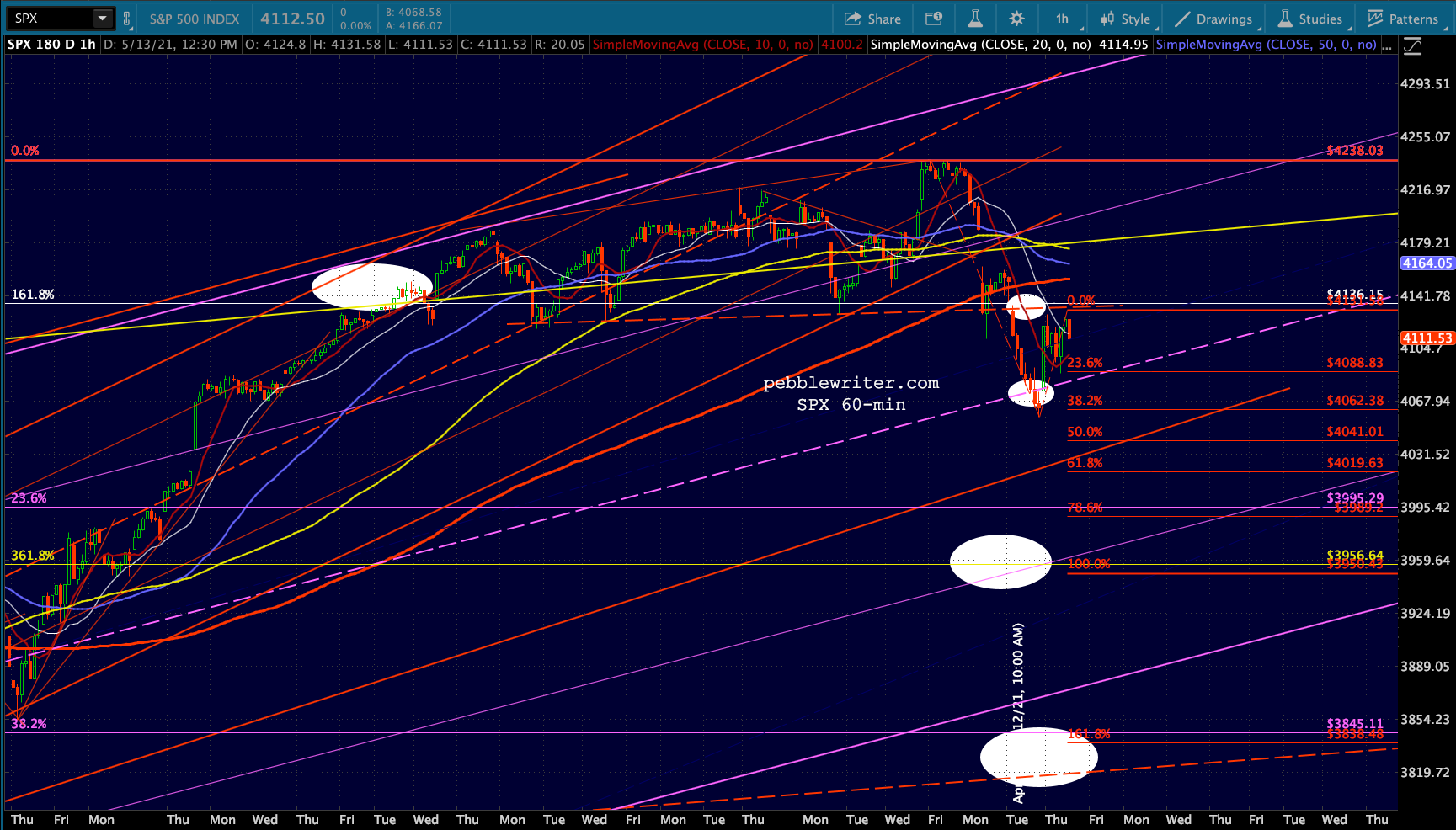

ES just reached a 61.8% retracement of its drop from the 4238 top. This also marks a backtest of the red TL from the March lows.  From here, a C=1.618*A extension would land very close to where the white TL and purple .382 Fib line at 3840 are.

From here, a C=1.618*A extension would land very close to where the white TL and purple .382 Fib line at 3840 are. VIX, having plunged back below its SMA100 and SMA10, is coming up on its SMA50 and has closed the gap from Monday.

VIX, having plunged back below its SMA100 and SMA10, is coming up on its SMA50 and has closed the gap from Monday.

More later…

Comments

2 responses to “Charts I’m Watching: May 14, 2021”

The new cases in India may be much higher than reported, due to the following:

1. The test kits may not detect some new variance.

2. The reported cases number are limited to the number of available test kits

3. There is no incentive to report higher number because local officials get penalized for worsening situation.

I think the real number would be very shocking.

I think you’re right. I’m worried that we’re jumping the gun yet again.