Futures are up slightly, buoyed by in-line retail sales and much stronger than expected Empire State Manufacturing. Retail sales increased 0.5% MoM and 3.9% YoY, both in line. Ex-auto, sales rose 0.3%. Remember that retail sales are not adjusted for inflation, so the inflation adjusted print was considerably lower.

Speaking of inflation, import prices rose 0.4% versus expectations of flat. Export prices were negligibly higher at 0.1%. U Mich sentiment is due out at 10am ET.

Empire State Manufacturing came in at 11.9, much higher than 1.8 expectations. All in all, this morning’s data doesn’t help support the September rate cut scenario.

continued for members…

continued for members…

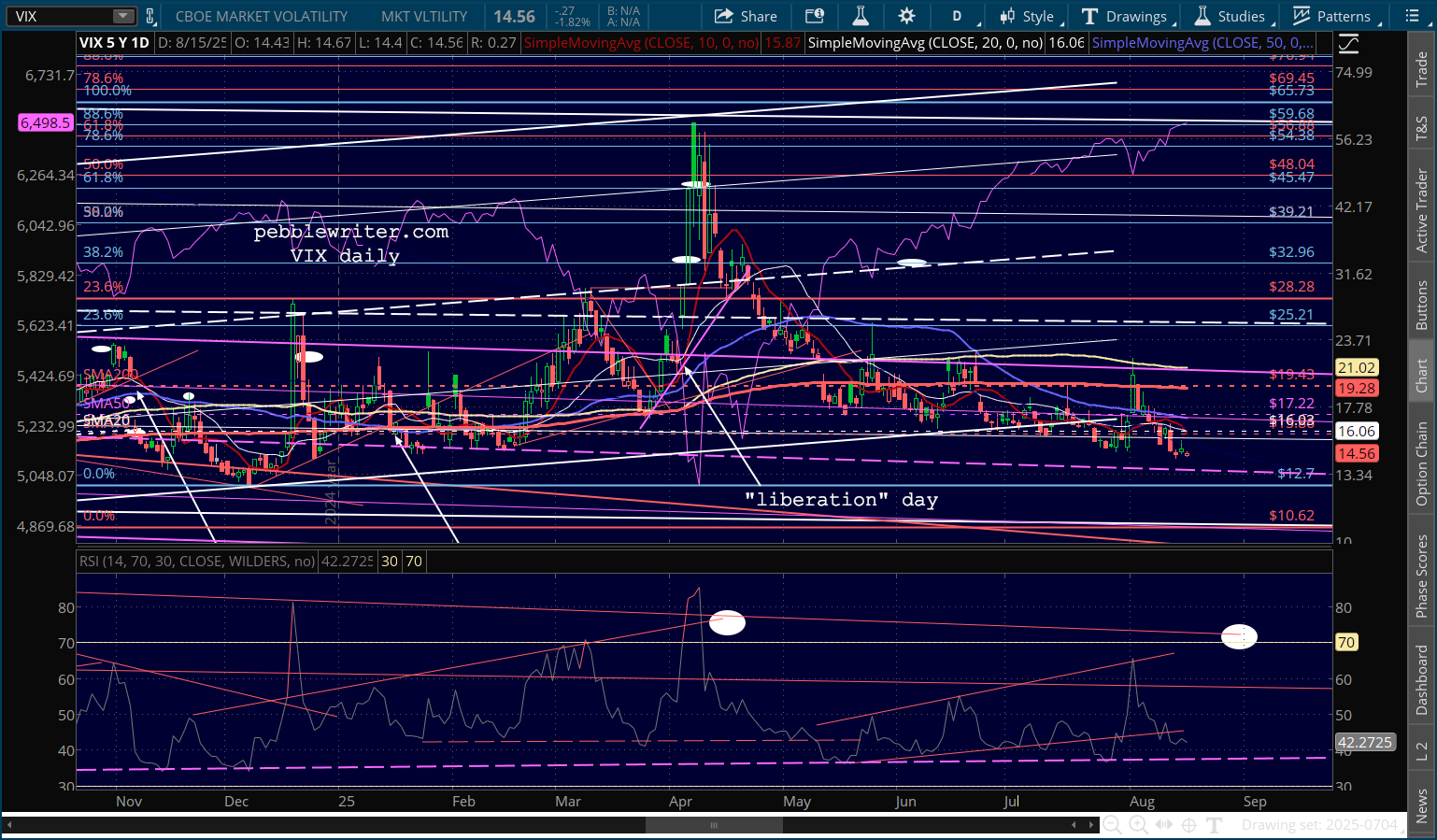

Note that ES and SPX narrowly averted a bearish 10/20 cross yesterday after a late rally prodded by VIX making lower lows and staging its own 10/20 cross.

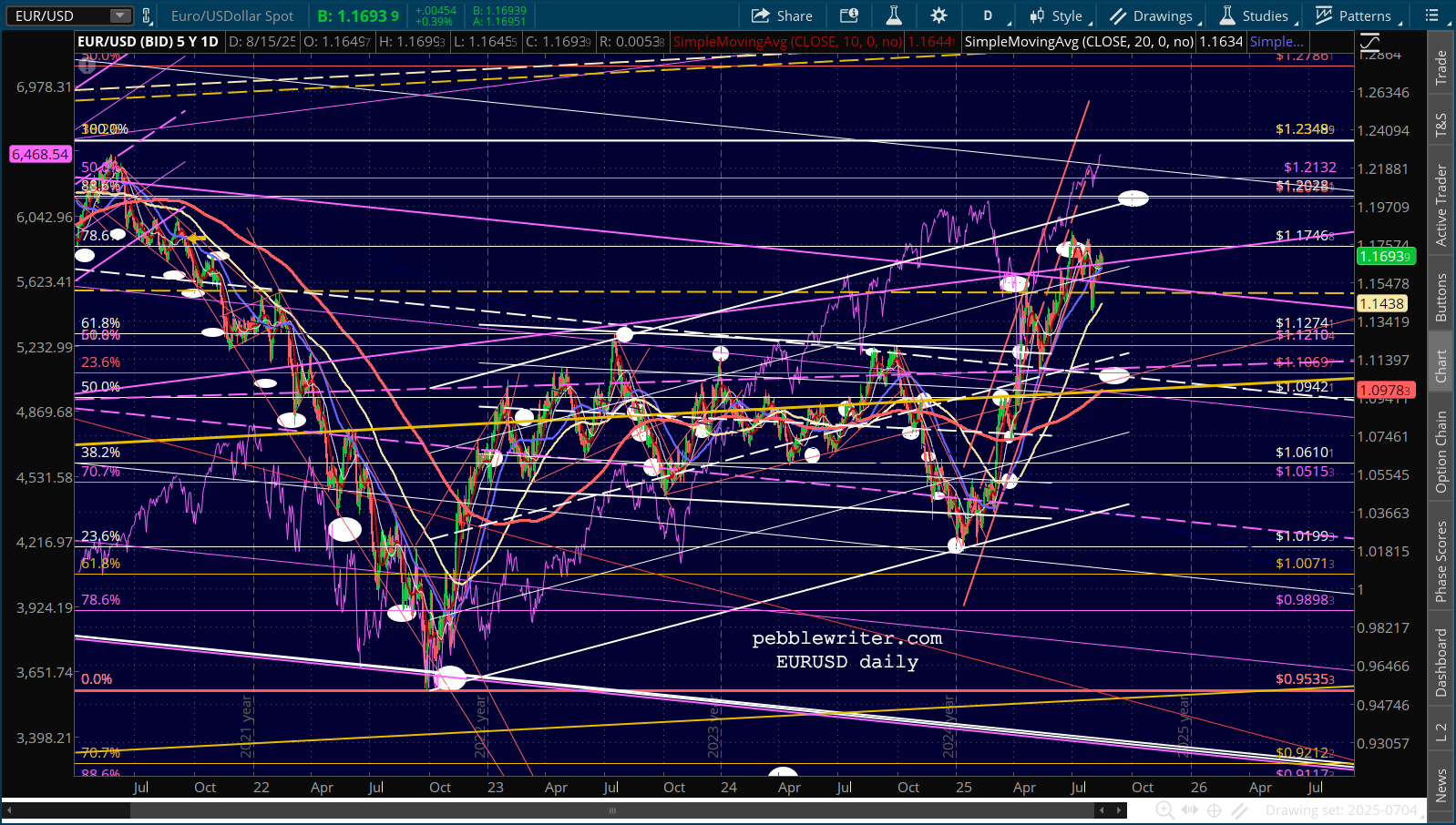

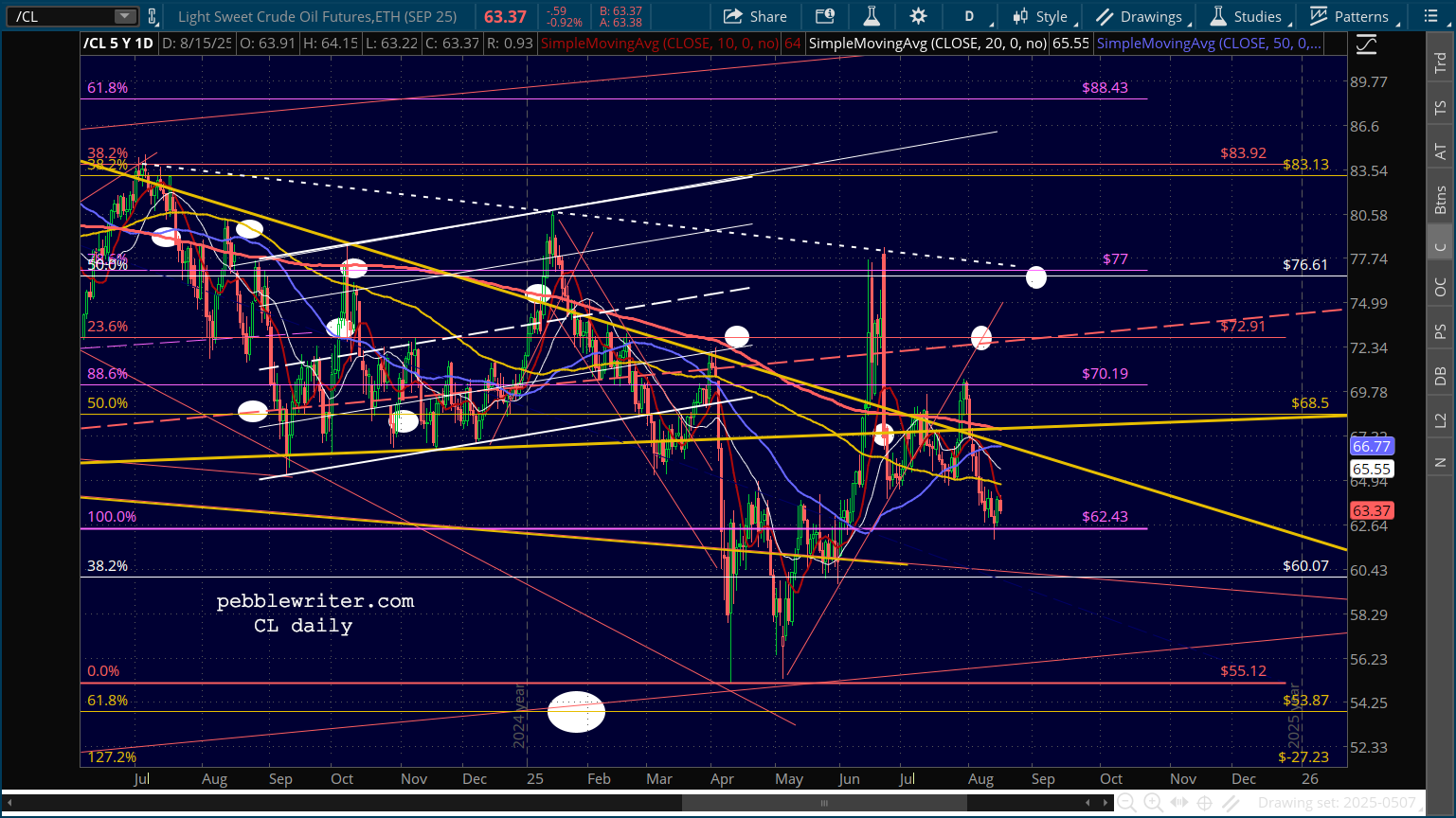

Another day of little change for currencies and oil/gas, though the 10Y is up slightly.

Another day of little change for currencies and oil/gas, though the 10Y is up slightly.