Futures are slightly lower following one of those spasmodic, overdone rallies driven by the latest collapse in VIX which was, in turn, driven by news that the government shutdown might soon be over.

Whether or not it will is still very much up in the air – unlike thousands of flights which were cancelled yesterday. It’s hard to imagine that Trump’s unhinged threats to the air traffic controllers will help.

Whether or not it will is still very much up in the air – unlike thousands of flights which were cancelled yesterday. It’s hard to imagine that Trump’s unhinged threats to the air traffic controllers will help.

This being Veterans Day, we salute all of our current and former service members. My own father served in WWII in the 89th infantry, the division that liberated most of the German concentration camps during a 640 mile march from La Havre, France to Zwickau, Germany – an experience which shook him until his own death. My uncle served in the army in Korea and, similarly, was shocked by what he saw on the battlefield.

I’ve written before about a very close friend, Michael J Novosel, MOH, whose military career began with flying a B-29 in WWII for the army air corp. He was riffed out after the Korean War as a Lieutenant Colonel. Years later, he gave up his air force rank to join the army as a chief warrant officer and fly Huey helicopters in Vietnam, flying 2,543 missions and rescuing 5,589 wounded personnel, including his son Mike Jr. The following week, Mike Jr. returned the favor by saving his father after he was shot down.

Mike was awarded the Medal of Honor for a mission during which he was shot down (one of many) which he described to me as fairly typical. But what impressed me the most was Mike’s evolution as a soldier: from firebombing Japan from the relative safety of a B-29 to hosing blood and body parts out of his Huey after each mission. Like my own father, he learned what most of us can’t fully comprehend – that there’s nothing glorious or glamorous about war. As Steinbeck wrote: “All war is a symptom of man’s failure as a thinking animal.” Perhaps if our political leaders were required to go into battle and witness war’s horrific reality, they’d be less inclined to send so many young people to their deaths and would take better care of those who manage to return.

continued for members… (more…)

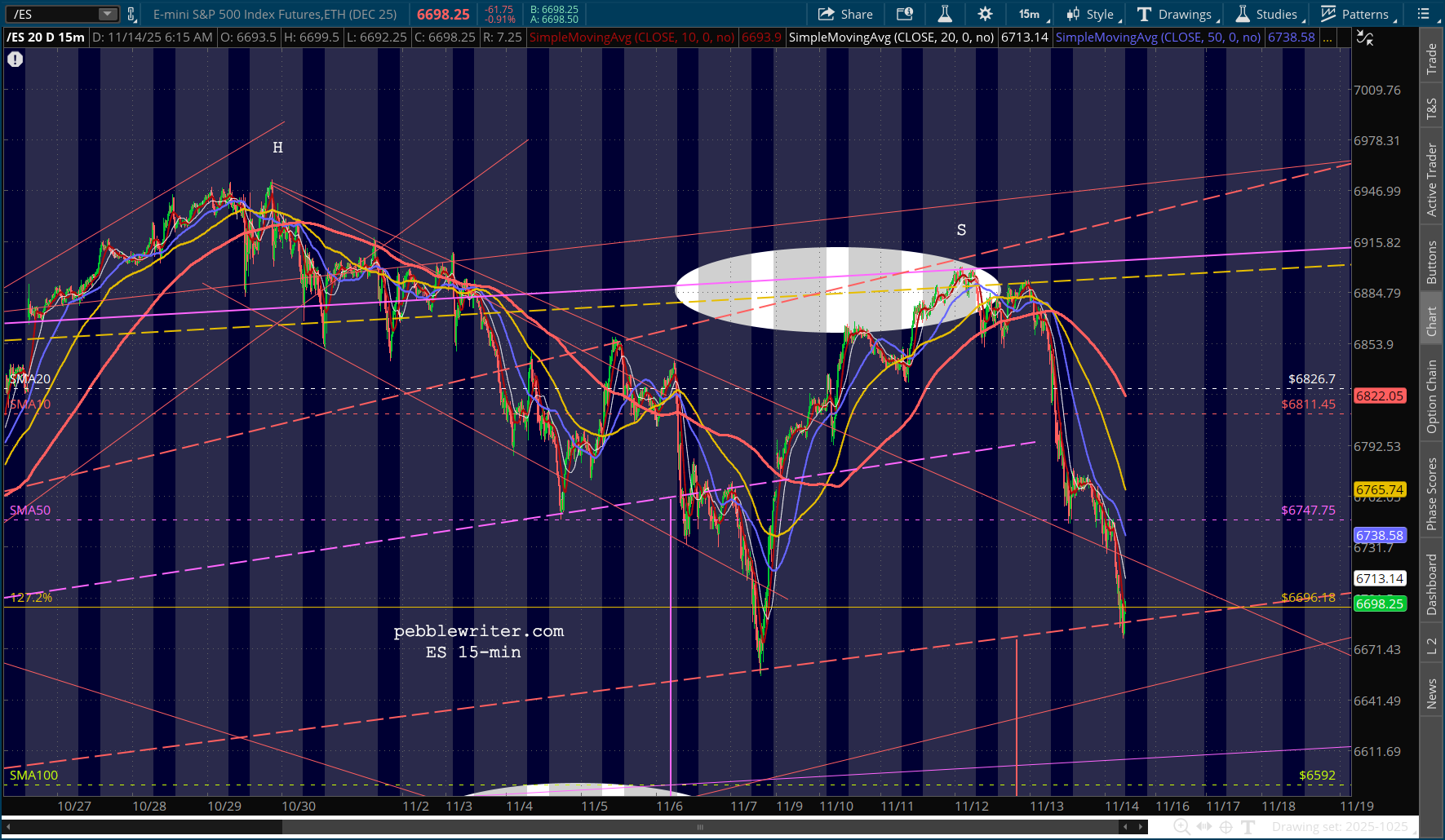

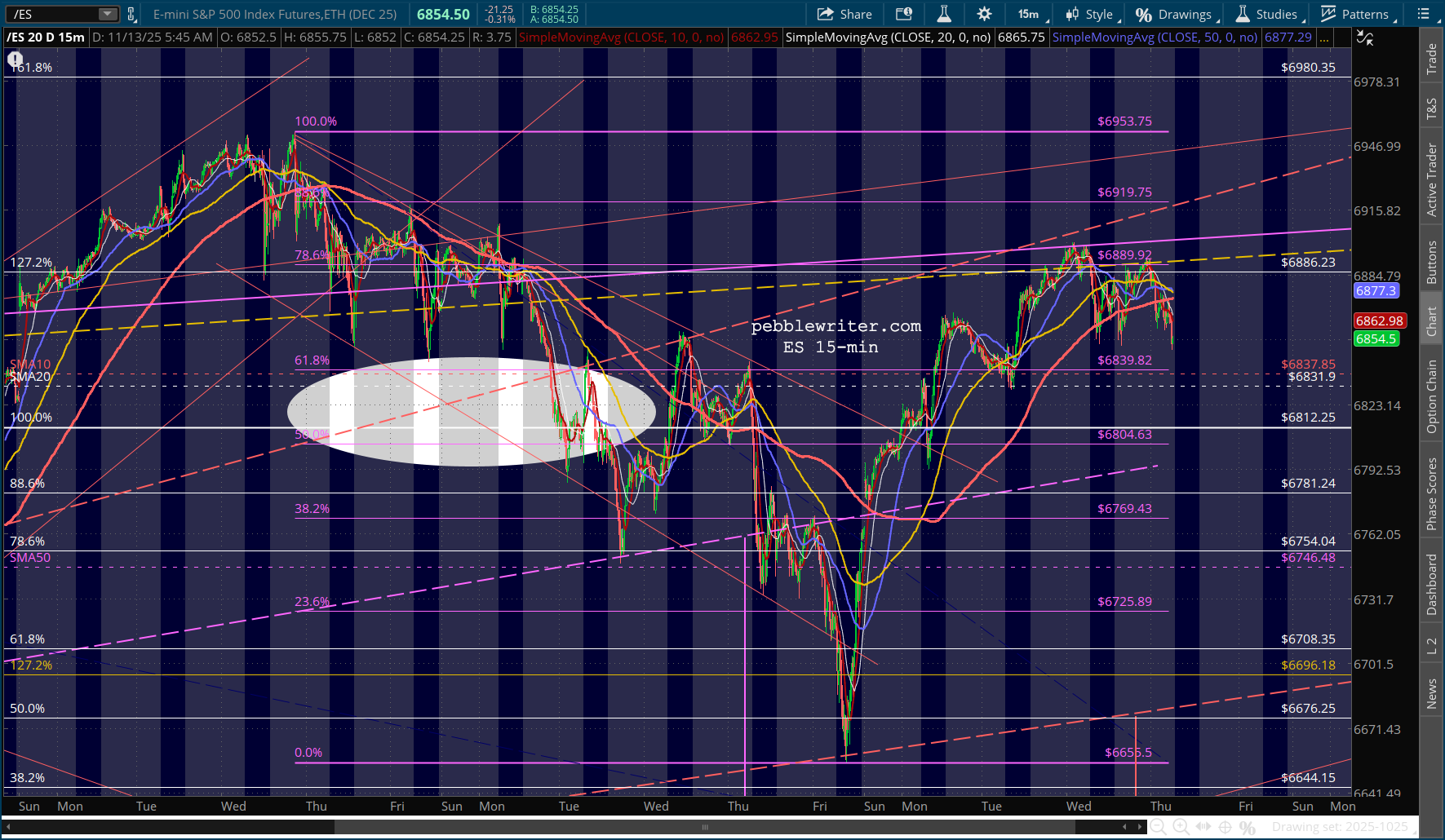

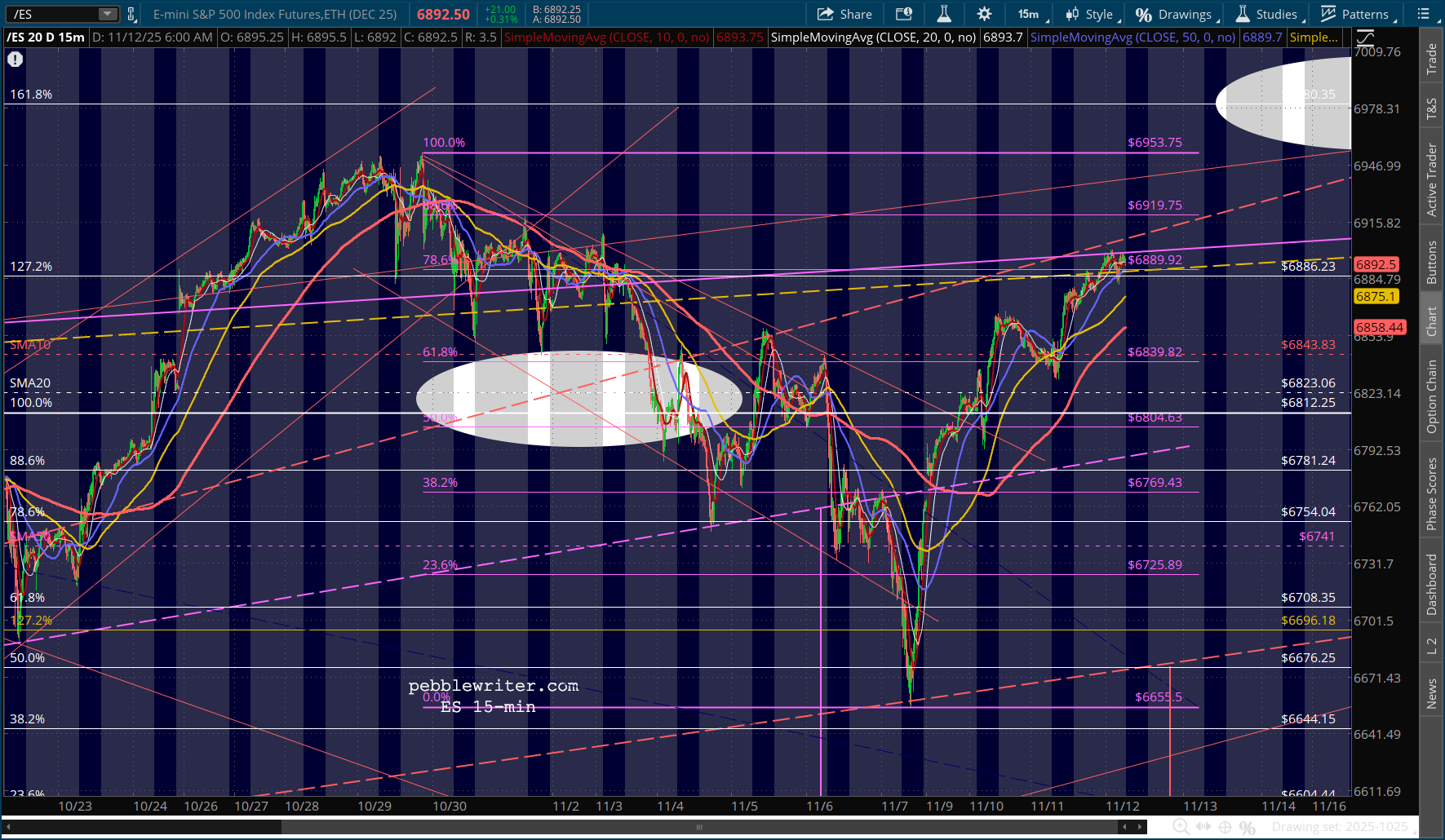

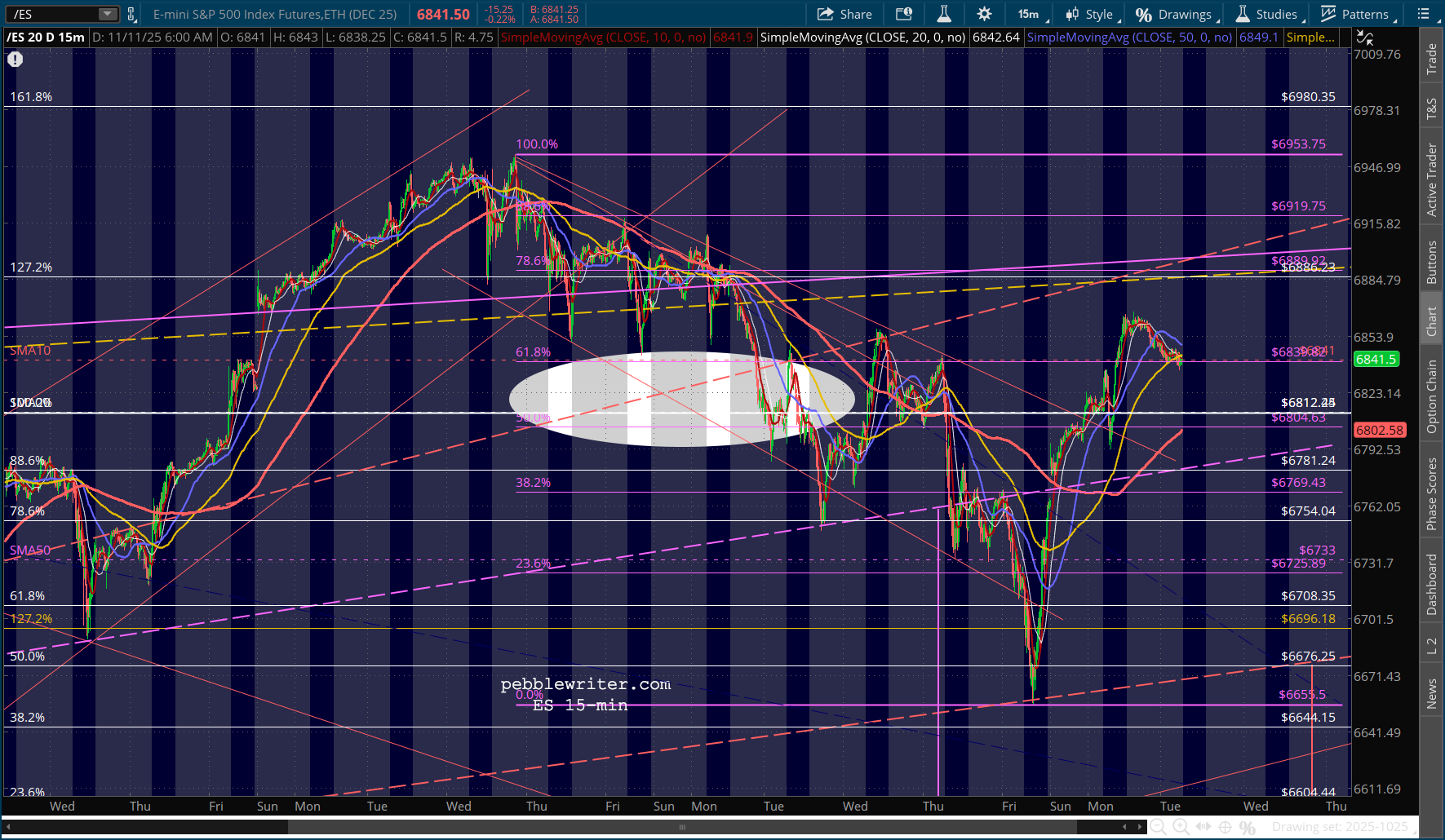

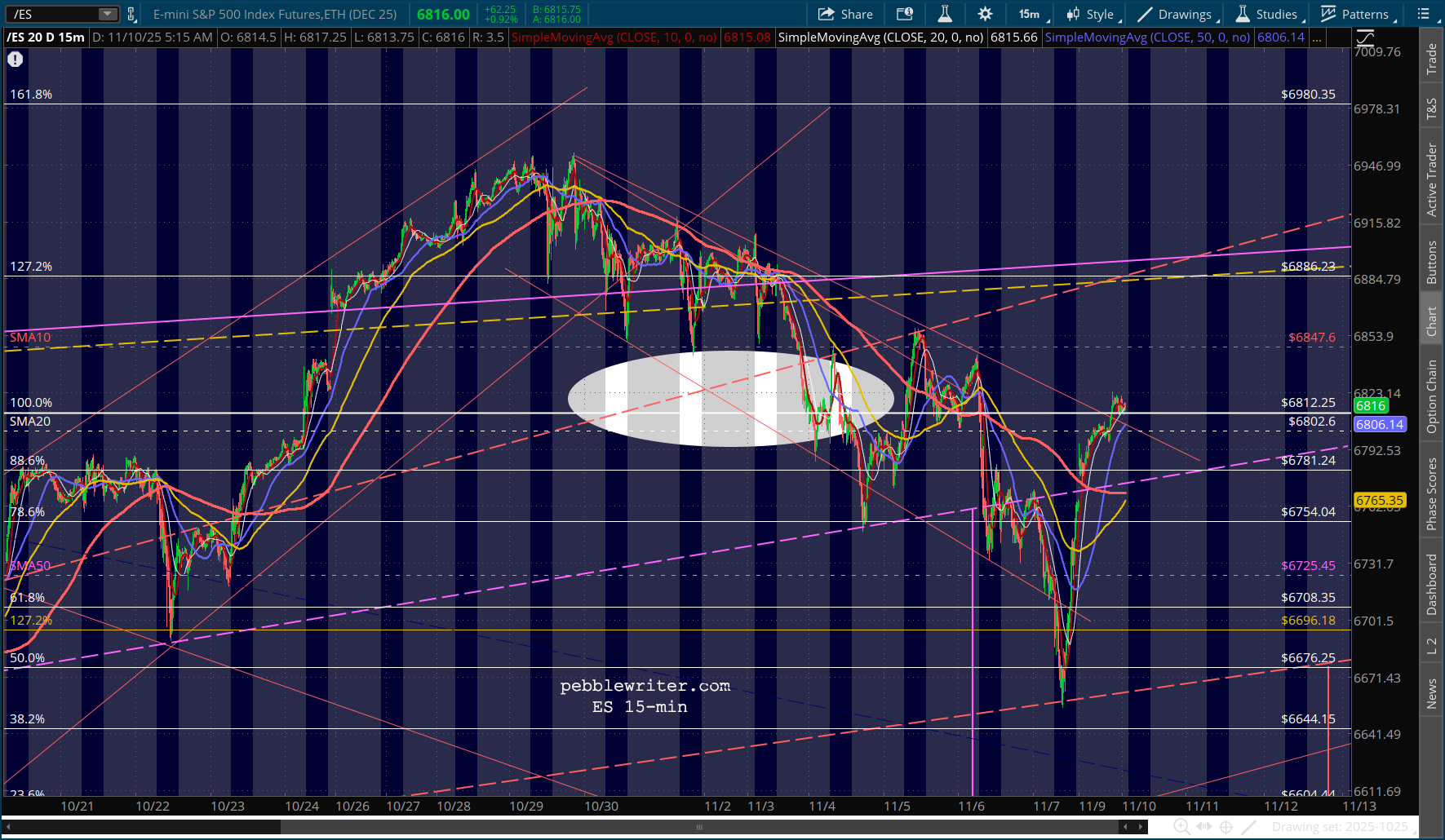

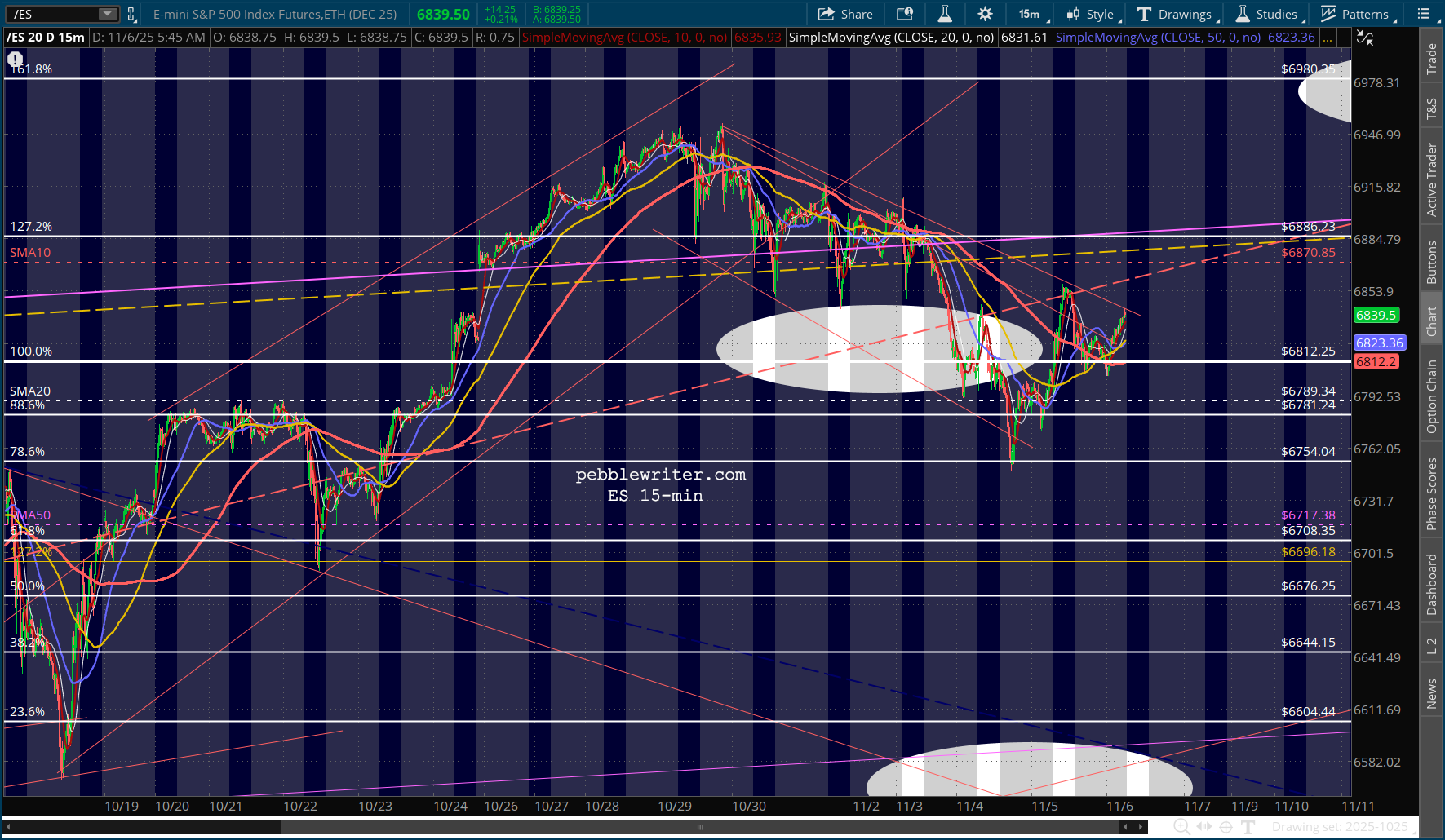

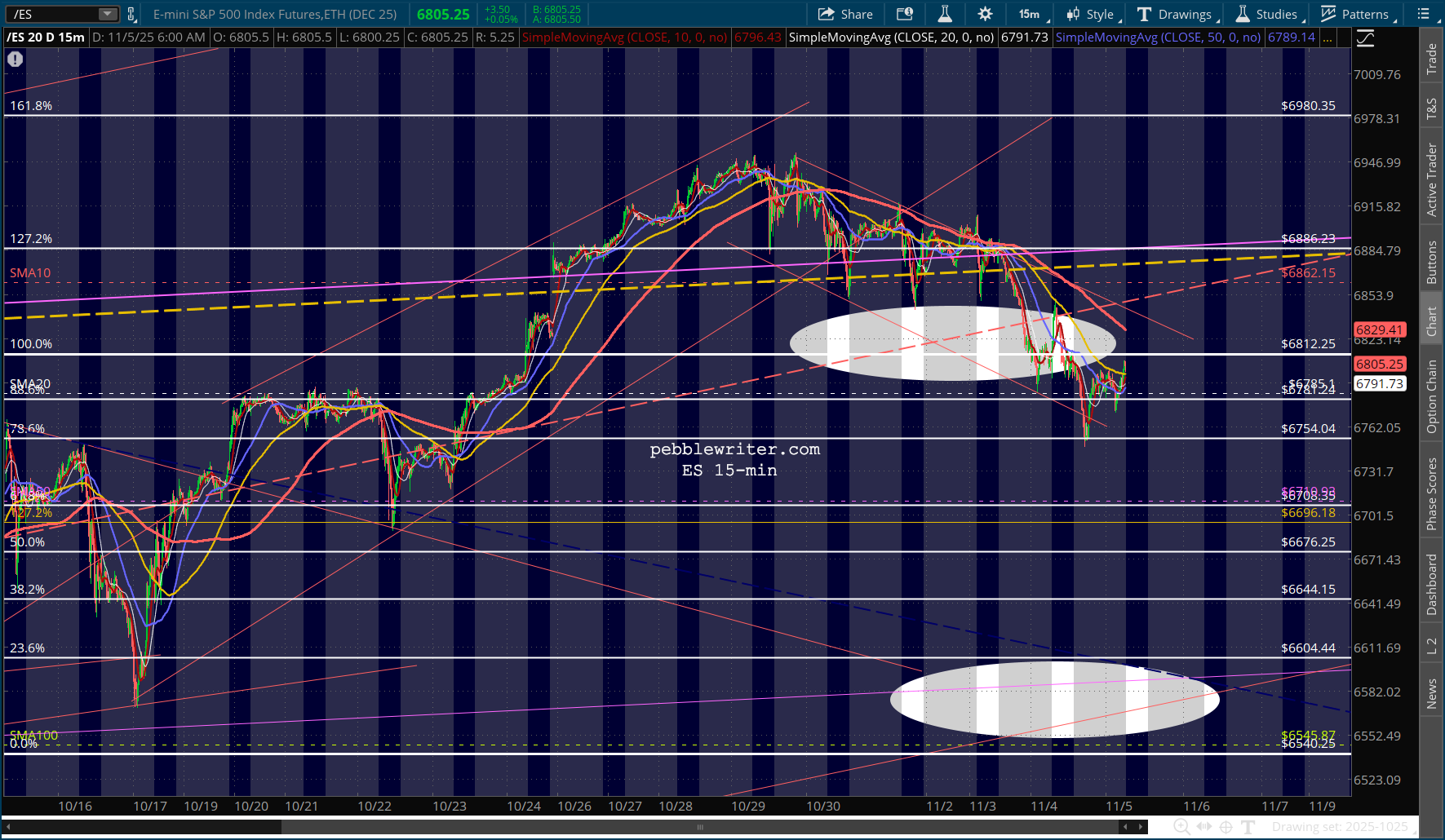

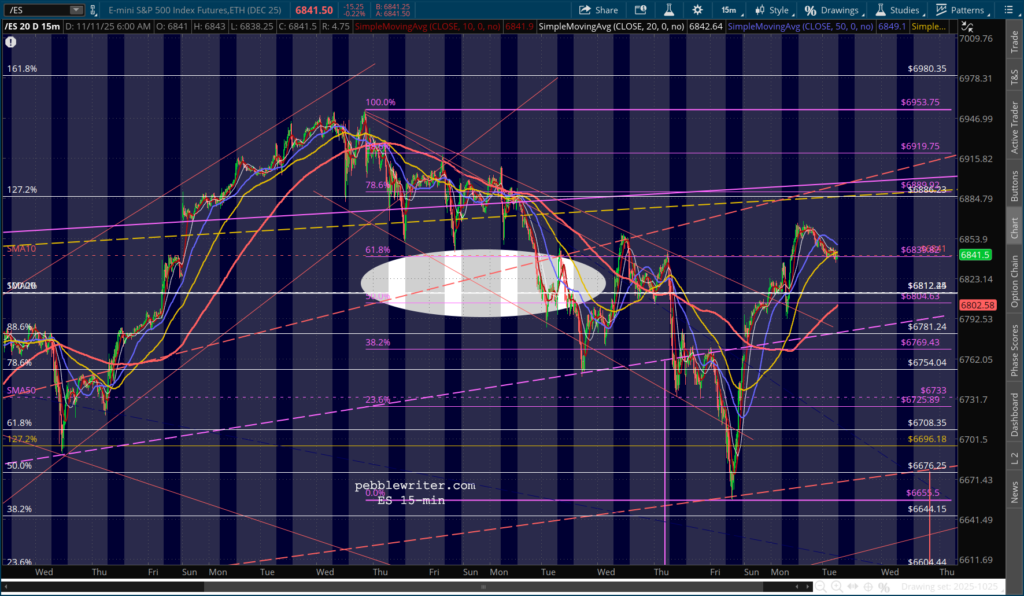

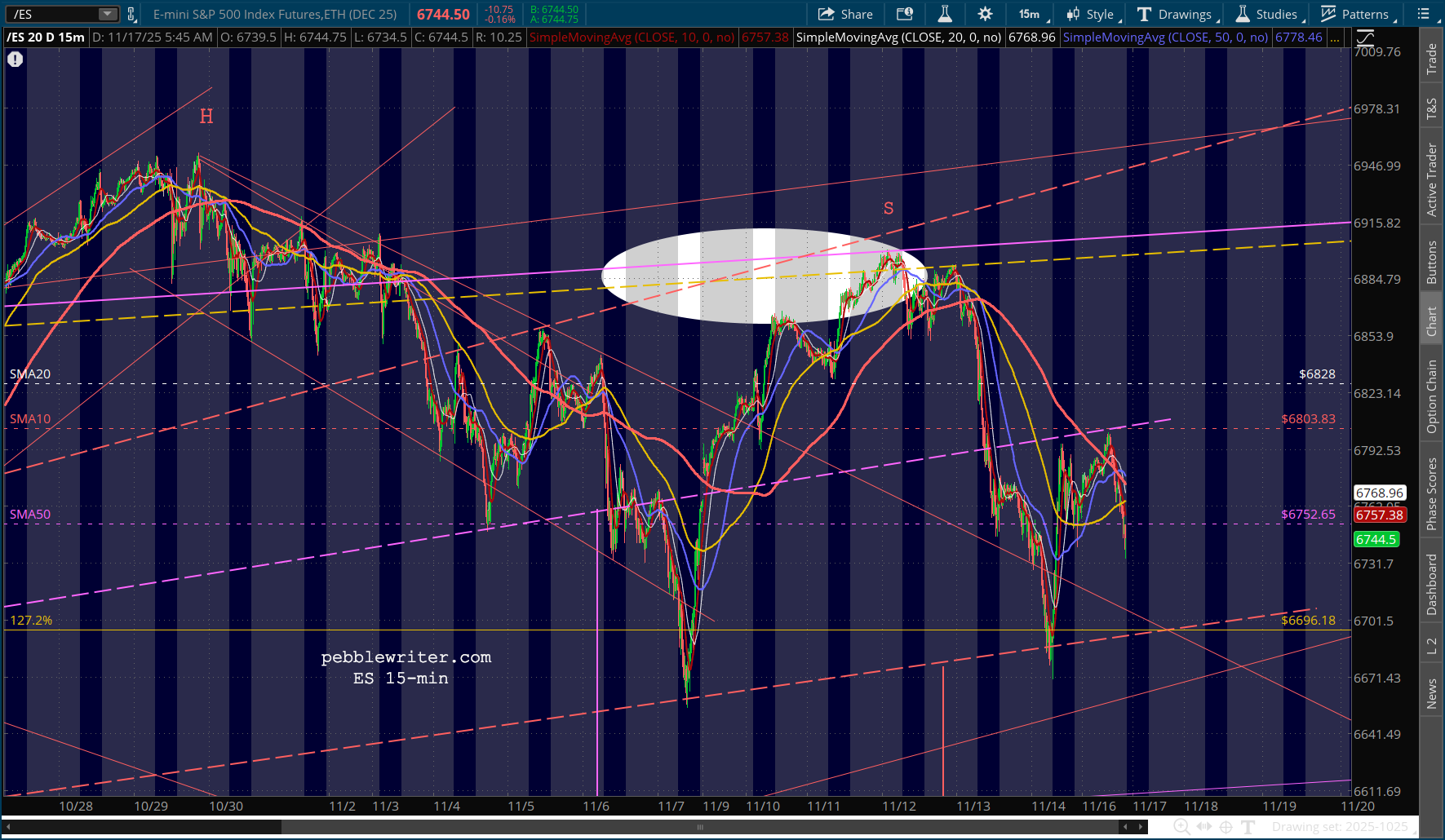

Note that SPX’s SMA200 has finally reached its former highs. As we discussed quite some time ago, this allows a significant backtest with the benefit of the support the SMA200 would offer. It’s a prime opportunity for TPTB to let a little air out of an overinflated market.

Note that SPX’s SMA200 has finally reached its former highs. As we discussed quite some time ago, this allows a significant backtest with the benefit of the support the SMA200 would offer. It’s a prime opportunity for TPTB to let a little air out of an overinflated market.